North America Automotive Operating System Market Size, Share, Trends & Growth Forecast Report By Type (Android, Linux, QNX, Windows, Others), Vehicle Type (Passenger Cars, Commercial Vehicles), Application (Infotainment System, ADAS & Safety System, Connected Services, Body Control & Comfort System, Engine Management & Powertrain Control, Communication & Telematics, Others), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

Market Size, 2025

$5.28 BnMarket Estimate, 2026

$6.01 BnMarket Forecast, 2034

$16.99 BnCAGR, 2026–2034

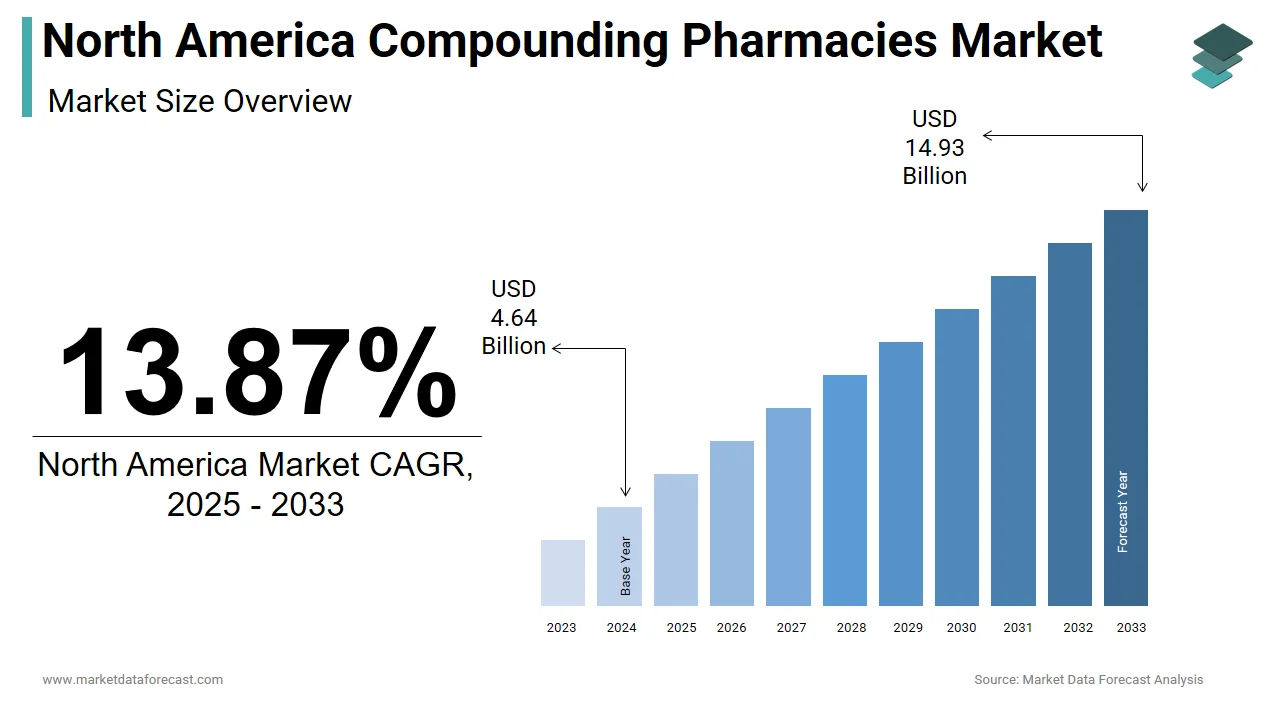

13.87%North America Automotive Operating System Market Size

The size of the North America automotive operating system market was valued at USD 5.28 billion in 2025. This market is expected to grow at a CAGR of 13.87% from 2026 to 2034 and be worth USD 16.99 billion by 2034 from USD 6.01 billion in 2026.

The automotive operating system (AOS) is embedded and real-time software platform that manage vehicle functions, including infotainment, telematics, advanced driver-assistance systems (ADAS), and autonomous driving capabilities. Unlike traditional in-vehicle electronics, modern AOS solutions integrate seamlessly with cloud-based services, smartphone ecosystems, and over-the-air (OTA) updates by enabling continuous performance enhancement and feature expansion. According to the International Data Corporation (IDC), automotive software spending in North America has grown significantly, driven by consumer demand for connected experiences and regulatory mandates for vehicle safety and efficiency. Canada’s automotive sector is also evolving, with increasing investments in smart mobility and AI-driven transportation solutions.

MARKET DRIVERS

Rising Demand for Connected and Autonomous Vehicles

One of the key drivers fueling the North America automotive operating system market is the accelerating adoption of connected and autonomous vehicles, which rely heavily on advanced operating systems for real-time data processing, sensor fusion, and decision-making capabilities. According to the National Highway Traffic Safety Administration (NHTSA), over 40% of new vehicles sold in the U.S. in 2023 included some level of ADAS functionality, necessitating high-performance automotive operating systems capable of managing complex inputs from cameras, LiDAR, radar, and ultrasonic sensors. Automakers such as Tesla, General Motors, and Ford are investing heavily in proprietary operating environments like QNX, Android Automotive, and custom Linux-based platforms to support seamless connectivity, OTA updates, and AI-driven navigation. Moreover, regulatory agencies are pushing for standardized cybersecurity protocols and functional safety compliance, prompting manufacturers to adopt certified automotive operating systems that meet ISO 26262 and AUTOSAR standards.

Integration of Infotainment and In-Vehicle Experience Enhancements

Another significant driver of the North America automotive operating system market is the increasing focus on enhancing the in-vehicle experience through advanced infotainment, voice assistants, and personalized user interfaces, all of which depend on robust automotive operating systems. According to J.D. Power, consumer satisfaction with vehicle technology is now a decisive factor in purchasing decisions, with infotainment and digital cockpit features ranking among the top three considerations for new car buyers. Modern automotive operating systems serve as the backbone for integrating Apple CarPlay, Google Automotive Services, and proprietary digital dashboards, allowing seamless interaction between the driver and vehicle. Additionally, automotive OS providers are collaborating with streaming services, navigation platforms, and voice recognition developers to offer deeply integrated experiences, similar to smartphones and home automation devices.

MARKET RESTRAINTS

Complexity of Software-Hardware Integration Across Vehicle Platforms

A major restraint affecting the North America automotive operating system market is the complexity involved in integrating diverse automotive operating systems with varying hardware architectures and electronic control units (ECUs) across different vehicle makes and models. According to the Society of Automotive Engineers (SAE International), inconsistencies in ECU design and communication protocols across OEMs have made cross-platform software deployment challenging, often leading to increased development time and costs.

Furthermore, automotive supply chains involve numerous Tier 1 and Tier 2 suppliers, each contributing components with proprietary firmware, which is complicating the unification of operating environments. This fragmentation hampers the widespread adoption of standardized operating systems and increases dependency on bespoke development, which is posing a persistent challenge for both software vendors and vehicle manufacturers aiming to deliver consistent digital experiences across their product lines.

Cybersecurity Vulnerabilities and Regulatory Compliance Issues

Another significant constraint influencing the North America automotive operating system market is the growing concern around cybersecurity vulnerabilities and the need to comply with evolving regulatory frameworks governing vehicle software security. According to the U.S. Department of Transportation, cybersecurity risks in automotive systems have become a central focus for federal regulators, prompting discussions around mandatory software audits and intrusion detection mechanisms. Moreover, standards such as ISO/SAE 21434 and UN R155 require automakers to implement comprehensive risk management strategies for vehicle cybersecurity, adding complexity to operating system development and validation. In addition, ensuring compliance with data privacy laws such as the California Consumer Privacy Act (CCPA) and GDPR-aligned policies has further complicated the deployment of automotive operating systems that collect and process user data. These regulatory and security challenges continue to pose barriers to innovation and market expansion for automotive OS providers.

MARKET OPPORTUNITIES

Expansion of Electric and Software-Defined Vehicles

A major opportunity emerging in the North America automotive operating system market is the rapid growth of electric and software-defined vehicles, which are inherently more dependent on sophisticated operating systems for power management, diagnostics, and over-the-air (OTA) updates. As automakers transition away from internal combustion engines toward electrified platforms, the reliance on centralized software control systems has intensified. Unlike traditional vehicles, EVs require extensive software coordination between battery management systems, regenerative braking, and thermal regulation, all of which operate under a unified automotive operating system. Additionally, major automakers are adopting software-first strategies, with brands like GM, Ford, and Rivian developing proprietary operating environments or partnering with tech firms such as Google and Qualcomm to enhance digital capabilities. This trend is encouraging deeper investment in automotive OS platforms that support modularity, interoperability, and long-term software maintenance, which is offering substantial growth potential for OS developers in North America.

Growth of Open-Source and Collaborative Automotive Software Platforms

Another promising avenue for growth in the North America automotive operating system market is the rising adoption of open-source and collaborative software platforms designed to reduce development costs and accelerate innovation. Traditionally, automotive operating systems were proprietary and tightly controlled by individual automakers or Tier 1 suppliers. However, a shift toward modular, shared software stacks is gaining momentum among startups and mid-sized automakers seeking cost-effective solutions. As reported by the Linux Foundation, the Automotive Grade Linux (AGL) project now includes over 150 member organizations, spanning automakers, semiconductor firms, and software developers working together to build a common platform for infotainment, instrument clusters, and telematics. This collaborative approach reduces redundancy and enables faster deployment of new features without reinventing core software infrastructure. Furthermore, companies are leveraging open-source frameworks to develop customized operating environments tailored to specific brand identities and consumer preferences.

MARKET CHALLENGES

Intense Competition from Tech Giants and Proprietary Ecosystems

A major challenge confronting the North America automotive operating system market is the intensifying competition from major technology companies and automakers developing proprietary operating environments, by reduces opportunities for independent OS vendors. Companies like Apple, Google, and Amazon are expanding their influence into automotive software through CarPlay, Android Automotive, and Alexa Auto, respectively, offering fully integrated ecosystems that compete directly with traditional automotive OS providers. Moreover, leading automakers such as Tesla, Ford, and General Motors are building their own in-house operating systems to maintain full control over user interfaces, data flow, and vehicle functionality, further consolidating the market around vertically integrated players.

Rapid Technological Evolution and Platform Obsolescence

Another critical challenge facing the North America automotive operating system market is the fast-paced evolution of automotive software technologies, which can lead to the premature obsolescence of existing platforms and create uncertainty for both automakers and consumers. According to McKinsey & Company, the average lifespan of a vehicle exceeds ten years, yet many automotive operating systems receive active support for less than five, creating a mismatch between hardware longevity and software lifecycle expectations. This issue is further compounded by the increasing use of over-the-air (OTA) updates to introduce new functionalities post-purchase, raising concerns about long-term vendor commitments and upgrade availability. Additionally, platform transitions such as the move from legacy QNX and AUTOSAR-based systems to newer hypervisor-driven and domain-oriented architectures have created integration hurdles for manufacturers, requiring retraining, infrastructure changes, and supplier alignment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Vehicle Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | BlackBerry Limited, Microsoft Corporation, Alphabet Inc., Apple Inc., Wind River Systems, Inc., Hitex GmbH, Bayerische Motoren Werke AG (BMW), Baidu, Inc., NVIDIA Corporation, and Green Hills Software. |

SEGMENTAL ANALYSIS

By Type Insights

The QNX segment dominated the North America automotive operating system market by capturing 42.7% of the share in 2024. A key driver behind this segment’s dominance is the certification of QNX under ISO 26262 ASIL-D standards, making it one of the most trusted real-time operating systems for mission-critical automotive functions. Additionally, leading automakers such as Ford, General Motors, and BMW have embedded QNX into their digital cockpits and domain controllers, ensuring seamless integration with high-performance computing modules.

The Android Automotive OS segment is expected to grow with an expected CAGR of 11.6% in the coming years. One major growth enabler is the familiarity of consumers with Android ecosystems, particularly among users of smartphones running on the Android OS. Moreover, automotive OEMs are leveraging Android Automotive’s extensibility and access to Google Play Services to deliver rich, personalized user experiences, including built-in navigation, music streaming, and voice-controlled smart home integrations.

By Vehicle Type Insights

The passenger cars segment was the largest and held a dominant share of the North America automotive operating system market in 2024. According to J.D. Power, over 75% of new car buyers in the U.S. consider digital cockpit features as a decisive factor in purchasing decisions, which is reinforcing the strategic importance of automotive operating systems in passenger vehicles.

A key growth driver is the integration of Android Automotive OS, QNX-based digital clusters, and OTA-enabled infotainment systems into mainstream passenger car models, enhancing functionality and user experience. As reported by McKinsey & Company, North America accounted for nearly half of all global investments in automotive software in 2023, much of which was directed toward passenger vehicle platforms. Additionally, electric and autonomous vehicle manufacturers are increasingly relying on sophisticated operating systems to manage battery efficiency, driver monitoring, and connectivity features, further boosting demand.

The commercial vehicles segment is expected to grow with an estimated CAGR of 9.8% from 2025 to 2033. This growth is primarily fueled by the digital transformation of fleet management, telematics, and logistics operations, where embedded operating systems play a crucial role in optimizing efficiency, reducing downtime, and improving route planning. Furthermore, government mandates for emissions reduction and vehicle safety compliance are pushing commercial vehicle manufacturers to adopt certified automotive OS platforms that support V2X (vehicle-to-everything) communication and regulatory reporting.

COUNTRY-LEVEL ANALYSIS

United States Automotive Operating System Market Insights

The United States was the top performer in the North America automotive operating system market, with 78.3% of share in 202,4 with a strong automotive technology ecosystem, deep-rooted presence of leading automakers, and extensive R&D activities in connected and autonomous vehicle software. A key growth driver is the accelerated adoption of electric and autonomous vehicles, particularly by Silicon Valley-linked firms such as Tesla, Waymo, and Aurora, which rely heavily on customized automotive operating systems. Moreover, major collaborations between automakers and tech giants such as Google's partnership with General Motors and Qualcomm’s integration with Ford are accelerating the deployment of standardized yet flexible operating environments across North American vehicle lines . The U.S. Department of Transportation also emphasized the need for secure and interoperable automotive software, reinforcing policy support for OS modernization efforts.

Canada Automotive Operating System Market Insights

Canada was positioned second with 12.3% of the North America automotive operating system market share in 2024. The country’s automotive operating system market is characterized by steady growth, driven by government-backed smart mobility initiatives, academic-industry collaborations, and rising interest in electric and autonomous transportation technologies. According to Natural Resources Canada, Canadian investments in zero-emission vehicle infrastructure rose by 14% in 2023, which is supporting broader integration of software-defined vehicle systems.

Additionally, OEMs such as Fiat Chrysler Automobiles (Stellantis) and Magna International are integrating more sophisticated OS platforms into domestic manufacturing plants, particularly for export-bound vehicles requiring international compliance with digital cockpit standards. The Ontario Ministry of Economic Development noted that Magna’s autonomous vehicle division expanded its embedded software team by 25% in 2023 by reflecting growing local expertise in automotive operating systems.

COMPETITIVE LANDSCAPE

The competition in the North America automotive operating system market is intense and rapidly evolving due to the convergence of traditional automakers, technology giants, and emerging software developers. The market is witnessing a shift from fragmented, proprietary systems toward more integrated, scalable, and open-platform solutions that support continuous feature enhancements through over-the-air updates. This transformation has led to increased rivalry not only among established OS providers but also with automakers developing their own in-house systems to maintain control over user experience and data flows.

Innovation remains a central battleground, with companies investing heavily in secure-by-design architectures, functional safety certifications, and compatibility with emerging mobility trends such as electrification, autonomous driving, and smart fleet management. Strategic mergers and acquisitions are becoming more frequent, allowing firms to consolidate their technological strengths and expand into underpenetrated application areas.

Customer-centric approaches such as developer ecosystems, modular software design, and cloud-connected infrastructure are becoming key differentiators. In this dynamic landscape, success depends on a company’s ability to anticipate industry shifts, align with regulatory frameworks, and deliver high-performance, interoperable automotive operating systems that meet both consumer expectations and engineering demands.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America automotive operating system market profiled in the report are

- BlackBerry Limited

- Microsoft Corporation

- Alphabet Inc.

- Apple Inc.

- Wind River Systems, Inc.

- Hitex GmbH

- Bayerische Motoren Werke AG (BMW)

- Baidu, Inc.

- NVIDIA Corporation

- Green Hills Software

TOP LEADING PLAYERS IN THE MARKET

One of the leading players in the North America automotive operating system market is BlackBerry QNX, a real-time operating system widely used in mission-critical automotive applications such as digital instrument clusters, infotainment systems, and advanced driver-assistance systems (ADAS). Its robust security framework and ISO 26262 certification make it a preferred choice among automakers for ensuring functional safety and cybersecurity. BlackBerry QNX plays a pivotal role in shaping global standards for automotive software reliability.

Another key player is Google with its Android Automotive OS, which has emerged as a powerful platform for embedded infotainment and connected car experiences. Google’s influence extends beyond consumer-facing interfaces to deeper integration with voice assistants, cloud services, and app ecosystems.

Microsoft also holds a significant position in the regional market through its Windows-based automotive solutions and growing involvement in vehicle cloud connectivity via Azure. Microsoft supports automakers in integrating over-the-air updates, telematics, and AI-driven analytics into their digital platforms, reinforcing its role in enabling intelligent mobility and enterprise-level data management within the automotive sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the North America automotive operating system market are leveraging deep partnerships with automakers and Tier 1 suppliers to embed their platforms into next-generation vehicle architectures. These collaborations allow OS providers to co-develop customized digital cockpits and ensure seamless integration with hardware components.

Another major strategy involves expanding ecosystem capabilities by integrating third-party apps, cloud services, and AI-powered voice assistants to enhance user engagement and personalization. Companies like Google and Microsoft are positioning their OS offerings as central hubs for connected mobility, offering rich digital experiences that mirror smartphone and home automation environments.

Additionally, firms are focusing on vertical integration and acquisitions to strengthen their software portfolios and gain control over end-to-end automotive computing stacks. OS vendors are accelerating innovation and securing long-term contracts with automotive clients seeking comprehensive software solutions.

RECENT MARKET DEVELOPMENTS

- In January 2024, BlackBerry announced an expanded partnership with a major U.S.-based automaker to deploy QNX-based domain controllers across multiple vehicle lines, which is reinforcing its leadership in real-time operating systems for safety-critical automotive functions.

- In March 2024, Google unveiled a new version of Android Automotive OS featuring enhanced voice recognition, predictive navigation, and deeper integration with EV battery management systems by aiming to capture a larger share of premium passenger and commercial vehicle segments in North America.

- In May 2024, Microsoft launched a dedicated automotive cloud suite powered by Azure and optimized for use with its automotive OS integrations, which is targeting fleet operators and logistics companies seeking advanced telematics and remote diagnostics capabilities.

- In July 2024, a prominent Japanese electronics manufacturer acquired a Canadian startup specializing in Linux-based automotive operating systems by signaling a strategic move to bolster its presence in open-source automotive software development and supplier relationships.

- In September 2024, Qualcomm Technologies partnered with a Detroit-based Tier 1 supplier to develop a unified cockpit platform combining QNX, Android Automotive, and Snapdragon compute modules, which is aiming to offer automakers a turnkey solution for next-generation digital vehicles.

MARKET SEGMENTATION

This North America automotive operating system market research report is segmented and sub-segmented into the following categories.

By Type

- Android

- Linux

- QNX

- Windows

- Others

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Application

- Infotainment System

- ADAS & Safety System

- Connected Services

- Body Control & Comfort System

- Engine Management & Powertrain Control

- Communication & Telematics

- Others

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What drives growth in the North America Automotive Operating System Market?

Growth in the North America Automotive Operating System Market is fueled by rising demand for connected cars, EVs, and advanced driver-assistance

Which operating systems lead the North America Automotive Operating System Market?

QNX, Linux, Android, and proprietary solutions dominate the North America Automotive Operating System Market for in-car and safety systems

Who are major players in the North America Automotive Operating System Market?

Key players in the North America Automotive Operating System Market include BlackBerry, Microsoft, Apple, Alphabet, and Automotive Grade Linux

What applications drive the North America Automotive Operating System Market?

Infotainment, ADAS, navigation, telematics, and vehicle connectivity fuel the North America Automotive Operating System Market’s expansion

How does AI impact the North America Automotive Operating System Market?

AI integration in the North America Automotive Operating System Market enables smart features, predictive safety, and personalized in-car experiences

What’s the CAGR for the North America Automotive Operating System Market by 2033?

The North America Automotive Operating System Market is expected to grow at a CAGR of around 13.87% through 2033, reflecting strong tech adoption

What role do EVs play in the North America Automotive Operating System Market?

EV adoption boosts the North America Automotive Operating System Market, requiring robust OS for battery, charging, and vehicle management

How does cybersecurity affect the North America Automotive Operating System Market?

Cybersecurity is vital in the North America Automotive Operating System Market to protect vehicle data, connectivity, and over-the-air updates

How are cloud-based solutions shaping the North America Automotive Operating System Market?

Cloud-based platforms in the North America Automotive Operating System Market enable real-time updates, diagnostics, and remote management

How does the North America Automotive Operating System Market support autonomous vehicles?

The North America Automotive Operating System Market enables automation, safety, and navigation for self-driving and semi-autonomous vehicles

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com