- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

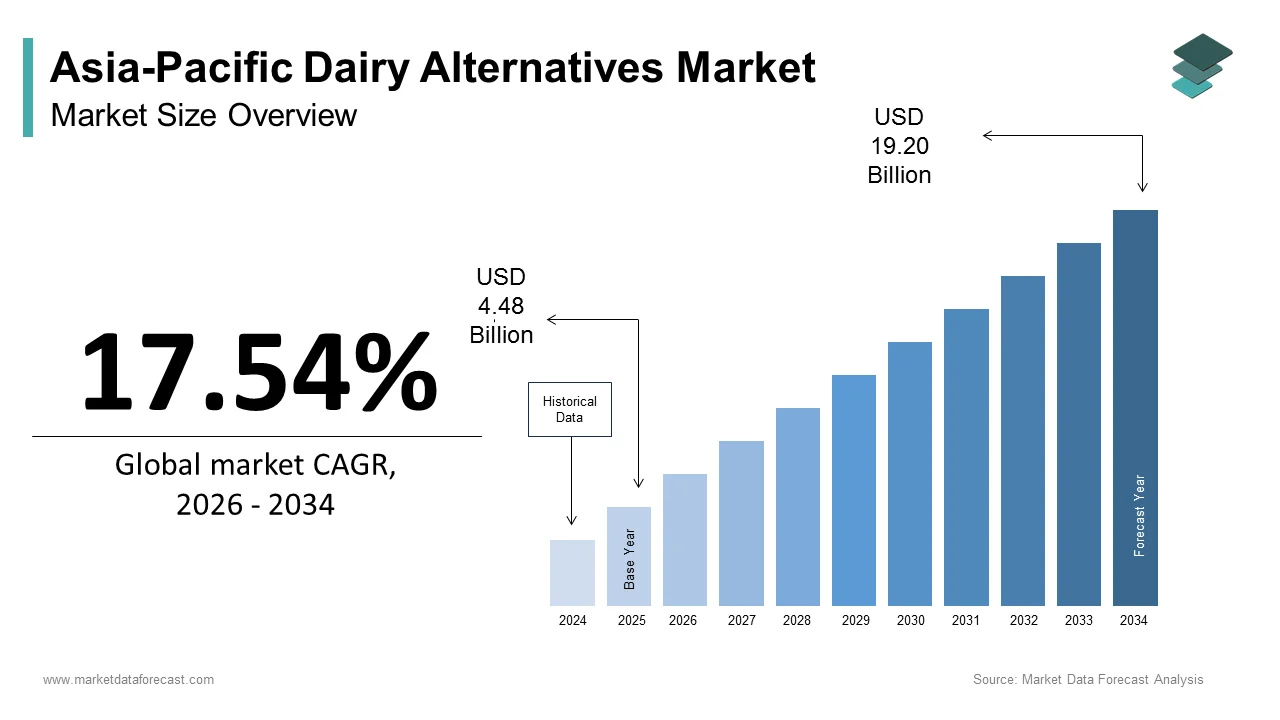

Market Size, 2025

$4.48 BnMarket Estimate, 2026

$5.27 BnMarket Forecast, 2034

$19.20 BnCAGR, 2026–2034

17.54%Asia-Pacific Dairy Alternatives Market Size

The dairy alternatives market size in Asia-Pacific was calculated to be USD 4.48 billion in 2025 and is anticipated to be worth USD 19.20 billion by 2034, from USD 5.27 billion in 2026, growing at a CAGR of 17.54% during the forecast period.

Dairy alternatives are plant-based food and beverage products designed to replace traditional dairy items like milk, cheese, yogurt, and butter. This market includes alternatives derived from soy almond oat coconut rice and emerging sources such as pea and hemp. The market is defined by its rapid evolution from niche health food status to mainstream consumption driven by changing dietary habits and environmental consciousness. In the Asia Pacific region the cultural context is unique as many populations have historically consumed soy milk making the transition to other plant based options more seamless. Medical and genetic research shows that lactose intolerance affects approximately 80% to 90% of adults across East Asia, serving as a key biological driver for choosing non-dairy alternatives. As per the World Health Organization the prevalence of noncommunicable diseases linked to high saturated fat intake is rising in the region prompting consumers to seek lower cholesterol options. The market is further shaped by urbanization and increased disposable incomes which allow consumers to experiment with premium imported and local brands. Regulatory frameworks in countries like China and Australia are evolving to standardize labeling and ensure safety which builds consumer trust. The definition of this market extends beyond mere substitution to include functional benefits such as added vitamins and probiotics. Innovation in texture and flavor is critical as Asian consumers often prefer specific mouthfeels and sweetness levels. The sector represents a significant shift in agricultural value chains as demand for crops like oats and almonds increases. This transformation is supported by advancements in food technology that improve the stability and taste of plant based emulsions.

MARKET DRIVERS

High Prevalence of Lactose Intolerance and Dairy Allergies

The high prevalence of lactose intolerance and dairy allergies is a key biological driver for the Asia Pacific Dairy Alternatives Market. A significant portion of this population cannot digest lactose effectively. Unlike Western markets where dairy avoidance is often a lifestyle choice in Asia it is frequently a physiological necessity. According to the National Institutes of Health lactose malabsorption affects up to 95 percent of adults in some Asian populations including those in China Japan and Southeast Asia. This widespread condition creates a consistent and inherent demand for lactose free alternatives that do not cause digestive discomfort. Medical research shows that consumers easily recognize the symptoms of lactose intolerance, like bloating and diarrhea, leading them to actively search for dairy-free alternatives to stay comfortable. The awareness of these health issues has grown due to better medical education and public health campaigns. Manufacturers are responding by formulating products that are not only lactose free but also fortified with calcium and vitamin D to address potential nutritional gaps. The demographic shift towards an aging population further amplifies this driver as digestive efficiency declines with age. Consumers are increasingly reading labels and avoiding dairy ingredients in processed foods which boosts the sales of dedicated dairy alternative products. The cultural acceptance of soy milk as a traditional beverage provides a strong foundation for the adoption of newer alternatives like oat and almond milk. This biological imperative ensures a stable and growing customer base that is less susceptible to fleeting trends. The market benefits from this permanent dietary requirement which drives continuous innovation in digestible and nutritious formulations.

Rising Health Consciousness and Chronic Disease Prevention

The rising health consciousness and focus on chronic disease prevention are also propelling the expansion of the Asia Pacific Dairy Alternatives Market. Consumers are increasingly associating plant-based diets with better long-term health outcomes. The region is experiencing a surge in lifestyle related diseases such as obesity type 2 diabetes and cardiovascular conditions which are linked to high saturated fat consumption. According to the World Health Organization, cardiovascular diseases are the leading cause of death in the region, claiming an estimated 4.3 million lives each year in South-East Asia alone. Consumers are increasingly aware of the link between animal fat intake and heart health leading them to choose plant based alternatives that are naturally cholesterol free. According to medical guidelines published in The Lancet, reducing salt intake and eating a balanced diet are the primary strategies for managing blood pressure and boosting heart health in Asian countries. Plant based milks such as almond and oat are perceived as lighter and healthier options that support weight management and metabolic health. The trend towards preventive healthcare is particularly strong among the middle class in urban centers who have access to health information and premium products. Social media and digital health platforms amplify messages about the benefits of plant based nutrition influencing purchasing decisions. Manufacturers are leveraging this trend by highlighting the low calorie and low sugar attributes of their products. The integration of functional ingredients such as fiber and protein further enhances the health appeal. This driver is reinforced by government initiatives promoting healthy eating habits and reduced sugar consumption. The shift towards holistic wellness ensures that dairy alternatives are viewed as essential components of a balanced diet.

MARKET RESTRAINTS

Price Sensitivity and Affordability Constraints

Price sensitivity and affordability constraints are major barriers to the Asia Pacific Dairy Alternatives Market. This is because plant-based options are often significantly more expensive than conventional dairy milk. In many developing countries within the region such as India Indonesia and Vietnam the majority of consumers are highly price sensitive and prioritize cost over premium features. According to the World Bank the average income per capita in lower middle income Asian countries remains below USD 4000 limiting the disposable income available for premium food products. High shelf prices mean plant-based alternatives often cost up to twice as much as dairy milk, preventing daily purchases by mass-market shoppers. Raw material costs for nuts and oats are volatile and often subject to import duties which further elevates retail prices. Local production capabilities for certain alternatives are still developing leading to reliance on expensive supply chains. Consumers in rural areas and lower income urban segments view dairy alternatives as luxury items rather than daily staples. This economic barrier limits market penetration to affluent urban demographics restricting overall volume growth. Manufacturers struggle to achieve economies of scale due to fragmented demand across diverse countries. The lack of local sourcing for key ingredients like almonds exacerbates the cost issue. Until production costs decrease or subsidies are introduced plant based milks will remain inaccessible to a large portion of the population. This financial constraint slows the transition from niche to mainstream adoption in price sensitive markets.

Limited Availability and Supply Chain Infrastructure

Limited availability and underdeveloped supply chain infrastructure further hamper the growth of the Asia Pacific Dairy Alternatives Market. This is particularly true in rural and semi urban areas. While major cities have well stocked supermarkets offering a variety of plant based milks remote regions often lack access to these products due to logistical challenges. According to the Asian Development Bank inadequate cold chain infrastructure in many Southeast Asian countries leads to high spoilage rates for perishable goods including fresh plant based beverages. As per McKinsey Company the last mile delivery costs in fragmented Asian markets are high making it difficult for brands to distribute products profitably outside metropolitan hubs. Many plant based alternatives require refrigeration to maintain freshness and quality which is not consistently available in smaller retail outlets. The reliance on imported raw materials such as almonds from California or oats from Europe introduces supply chain vulnerabilities and delays. Geopolitical tensions and trade barriers can disrupt the flow of ingredients affecting production schedules and inventory levels. Local farmers in Asia are primarily focused on traditional crops like rice and soy leaving gaps in the supply of specialized ingredients like hemp or flax. The lack of localized processing facilities means that many products are manufactured abroad and shipped in increasing costs and carbon footprints. This logistical complexity hinders the ability of brands to maintain consistent stock levels and competitive pricing. Expanding distribution networks requires significant capital investment which many smaller players cannot afford. The infrastructure gap remains a critical bottleneck for market expansion in less developed parts of the region.

MARKET OPPORTUNITIES

Expansion into Traditional Culinary Applications

The expansion into traditional culinary applications offers a major opportunity for the Asia Pacific Dairy Alternatives Market. Manufacturers are adapting products to suit local tastes and cooking methods. Unlike Western markets where plant based milk is primarily consumed in coffee or cereal Asian consumers use dairy alternatives in a wide range of savory and sweet dishes. For instance creamy oat milk is being marketed as a substitute for coconut milk in Thai curries while almond milk is used in Indian sweets. This localization strategy allows brands to integrate their products into daily meals rather than positioning them as occasional treats. The versatility of plant based ingredients enables innovation in ready to cook mixes and meal kits that cater to busy urban lifestyles. Manufacturers are collaborating with local chefs and food influencers to demonstrate creative uses of dairy alternatives in traditional recipes. This approach helps overcome cultural resistance by framing plant based options as enhancements to familiar dishes. The opportunity extends to the food service sector where restaurants are increasingly offering plant based menu items to attract health conscious diners. By aligning with culinary traditions companies can drive higher frequency of use and deeper market penetration. This cultural integration transforms dairy alternatives from niche imports to essential kitchen staples.

Growth of E Commerce and Direct to Consumer Channels

The growth of e-commerce and direct-to-consumer channels paves the way for the expansion of the Asia-Pacific Dairy Alternatives Market. These bypass traditional retail barriers and reach wider audiences. Digital platforms enable brands to educate consumers offer subscriptions and deliver fresh products directly to homes which is crucial for maintaining quality. As per Alibaba Group the rise of online grocery shopping has accelerated during recent years with consumers preferring the convenience of home delivery for bulky items like milk cartons. Direct to consumer models allow brands to collect valuable data on consumer preferences and tailor marketing strategies accordingly. Subscription services ensure recurring revenue and customer loyalty by automating regular deliveries of favorite products. Social commerce platforms such as TikTok and Instagram are increasingly used to launch new flavors and engage with younger demographics through interactive content. The ability to reach consumers in tier two and tier three cities without establishing physical distribution networks reduces operational costs. Online channels also facilitate the introduction of niche products such as hemp or macadamia milk which may not have shelf space in traditional stores. Brands can leverage digital marketing to tell their sustainability stories and build emotional connections with buyers. This digital transformation democratizes access to dairy alternatives and accelerates market growth across diverse geographic locations.

MARKET CHALLENGES

Regulatory Ambiguity and Labeling Standards

Regulatory ambiguity and inconsistent labeling standards are major challenges for the Asia Pacific dairy alternatives market, as companies navigate complex and varying legal frameworks across countries. The use of terms such as milk yogurt and cheese for plant based products is contested in several jurisdictions creating uncertainty for manufacturers. According to the Food and Agriculture Organization differing definitions of dairy terms in countries like China India and Australia complicate cross border trade and marketing strategies. As per the European Union although not in Asia their strict regulations influence global standards causing confusion for exporters who must adapt labels for different markets. In some Asian countries regulators are considering bans on using dairy terminology for plant based products to prevent consumer confusion which could limit branding options. The lack of harmonized standards for nutritional claims such as high protein or calcium enriched requires companies to conduct separate testing for each market. This regulatory fragmentation increases compliance costs and delays product launches. Manufacturers must invest in legal expertise to ensure that their packaging meets local requirements which can be contradictory. The uncertainty discourages investment in long term brand building as rules may change unexpectedly. Consumer trust can be eroded if labeling is perceived as misleading or inconsistent. The industry advocates for clear and fair labeling guidelines that allow for accurate communication of product benefits. Navigating this regulatory maze requires agility and constant monitoring of policy developments in each target country.

Sensory Acceptance and Taste Preferences

Sensory acceptance and taste preferences are a significant hurdle for the Asia Pacific Dairy Alternatives Market. Many consumers find the flavor and texture of plant-based milks inferior to dairy. Traditional dairy milk has a distinct creamy mouthfeel and neutral taste that is deeply ingrained in Asian culinary culture. Achieving a neutral flavor profile often requires extensive processing which can strip away natural nutrients and increase costs. The variability in taste between batches due to natural ingredient fluctuations further complicates consumer satisfaction. In regions where soy milk is traditional consumers have high expectations for quality and consistency which new entrants struggle to meet. The challenge is compounded by the diverse palates across Asia with some populations preferring sweeter beverages while others favor savory profiles. Manufacturers must invest heavily in research and development to mask off flavors and improve texture without relying on excessive additives. Failure to deliver a pleasing sensory experience leads to low trial conversion and negative word of mouth. Overcoming these sensory hurdles is critical for mainstream adoption as taste is the primary determinant of food choice. Continuous innovation in formulation and processing is required to meet the high sensory standards of Asian consumers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.54% |

| Segments Covered | By Application, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the rest of APAC. |

| Market Leaders Profiled | The Hain Celestial Group Inc., The WhiteWave Foods Company, Nutriops S.L., Freedom Foods Group Limited, Blue Diamond Growers, Archer Daniels Midland Company, Sanitarium Health & Wellbeing Company, Daiya Foods Inc., SunOpta Inc., Earth’s Own Food Company and Eden Foods, Inc. |

SEGMENTAL ANALYSIS

By Application Insights

In 2025, the milk segment held the majority share of the Asia Pacific Dairy Alternatives Market because of its status as a staple beverage and direct substitute for conventional dairy milk. In many Asian cultures particularly in East and Southeast Asia soy milk has been consumed for centuries making the transition to other plant based milks culturally seamless. The versatility of plant based milk allows it to be used in beverages cooking and baking which expands its utility beyond simple drinking. Consumers in countries like China and Japan prefer ready to drink formats which are widely available in vending machines and convenience stores. The high prevalence of lactose intolerance further cements milk as the primary choice for those seeking digestive comfort. Manufacturers focus heavily on this segment because it requires less complex processing than cheese or yogurt allowing for lower production costs and wider distribution. The familiarity of liquid formats reduces the barrier to trial for new consumers who may be hesitant about textured alternatives. This segment benefits from continuous innovation in flavors such as barley rice and black sesame which appeal to local palates. The widespread availability of shelf stable options also supports its leadership as it does not always require cold chain logistics.

The domination of the Milk segment is further reinforced by the strong consumer demand for fortified liquid nutrition that supports overall health and wellness. Plant based milks are often enriched with calcium vitamin D and vitamin B12 to match the nutritional profile of cow milk addressing concerns about nutrient deficiencies. The liquid format allows for easy integration of these nutrients without affecting taste or texture significantly. Health conscious consumers in urban areas prefer milk alternatives that offer low calorie and low cholesterol options for weight management and heart health. The perception of plant based milk as a lighter and cleaner option compared to full fat dairy drives its adoption among younger demographics. Marketing campaigns often highlight the natural origins and absence of artificial additives which resonates with the clean label trend. The ease of incorporating fortified milk into daily routines such as morning coffee or smoothies ensures consistent repeat purchases. This health oriented positioning differentiates milk from other applications like ice cream which are viewed as indulgent treats. The focus on preventive healthcare in the region amplifies the demand for nutritious liquid alternatives.

The cheese segment is expected to exhibit a noteworthy CAGR of 12.5% from 2026 to 2034 due to the rising influence of Western cuisine and the expansion of the food service sector. As pizza burgers and pasta become increasingly popular in Asian countries the demand for dairy free cheese alternatives is surging. Consumers are seeking melts and stretches similar to dairy cheese which drives innovation in coconut oil and starch based formulations. The youth demographic in countries like South Korea and China is particularly influenced by global food trends leading to higher trial rates of vegan cheese. Food manufacturers are collaborating with restaurant chains to develop customized cheese solutions that perform well in high heat applications. This B2B demand accelerates market growth as large volumes are purchased for commercial use. The introduction of retail packs in supermarkets also supports home usage for cooking and snacking. The novelty factor of vegan cheese attracts early adopters who are willing to experiment with new textures and flavors. This segment benefits from the broader trend of plant based dining becoming mainstream in urban centers.

The rapid growth of the Cheese segment is fueled by significant advancements in technology that improve the texture and melting properties of plant based cheeses. Early versions of vegan cheese were criticized for their poor melt and rubbery texture but recent innovations have addressed these issues effectively. Ingredients such as tapioca starch and coconut oil are blended with cashew or almond bases to achieve the desired consistency. These improvements make vegan cheese suitable for a wider range of culinary applications including grilled sandwiches and baked dishes. Consumer satisfaction with these enhanced products drives repeat purchases and positive word of mouth. Manufacturers are investing in research to create artisanal varieties such as cheddar and mozzarella that appeal to discerning tastes. The ability to produce cheese that browns and bubbles like dairy cheese removes a major barrier to adoption. This technological breakthrough allows vegan cheese to compete directly with dairy in terms of sensory experience. The growing availability of high quality vegan cheese in retail stores further supports its rapid expansion. As consumers become more familiar with these improved products the segment is poised for sustained high growth.

By Distribution Channel Insights

The hypermarkets and supermarkets segment was the largest in the Asia Pacific Dairy Alternatives Market and occupied a 41.8% share in 2025. Its extensive reach and the trust consumers place in physical retail environments are the factors supporting the prominence of this segment. These outlets offer a wide variety of brands and products allowing consumers to compare prices and read labels before purchasing. The presence of refrigerated sections in these stores is crucial for perishable dairy alternatives such as fresh soy milk and yogurt. Major chains like AEON Lotte Mart and Walmart have dedicated shelves for plant based products increasing visibility and accessibility. The ability to physically inspect packaging and check expiration dates builds consumer confidence especially for first time buyers. Promotional activities and in store sampling events conducted in supermarkets drive trial and awareness. The consolidation of retail power in Asia means that listing in major supermarkets is essential for brand success. These channels also benefit from established supply chains that ensure consistent stock availability. The convenience of one stop shopping encourages households to include dairy alternatives in their regular grocery baskets. This broad accessibility and consumer preference for tactile shopping experiences solidify the leadership of hypermarkets and supermarkets.

The spearheading of Hypermarkets and Supermarkets is also strengthened by strategic shelf placement and the introduction of private label dairy alternatives. Retailers are increasingly placing plant based milks and yogurts alongside conventional dairy products to facilitate easy comparison and substitution. These store brands often mimic the packaging and branding of national leaders making them attractive to price sensitive shoppers. The control retailers have over shelf space allows them to promote high margin private label items effectively. Consumers trust supermarket brands for consistency and safety which lowers the risk of trying new products. The integration of digital price tags and loyalty programs in supermarkets enhances the shopping experience and encourages repeat purchases. Retailers also use data analytics to optimize inventory and reduce waste ensuring that fresh products are always available. The ability to bundle dairy alternatives with other healthy foods creates cross selling opportunities. This strategic approach by retailers maximizes visibility and conversion rates. The combination of convenient location competitive pricing and trusted branding ensures that hypermarkets and supermarkets remain the primary channel for dairy alternative sales.

The online Stores segment is predicted to witness the highest CAGR of 14.2% over the forecast period owing to the unparalleled convenience and expanded product variety they offer. E commerce platforms allow consumers to access a wide range of niche and imported brands that may not be available in local supermarkets. Consumers appreciate the ability to read detailed product descriptions and reviews which helps them make informed decisions. The home delivery model is particularly appealing for bulky items like milk cartons which are heavy and inconvenient to carry. Online platforms also offer competitive pricing and discounts which attract price sensitive buyers. The rise of quick commerce services that deliver groceries within hours further boosts the attractiveness of online channels. Digital marketing and targeted ads on social media drive traffic to online stores increasing visibility for new brands. The ability to reach consumers in remote areas where physical retail infrastructure is limited expands the market reach. Online stores also facilitate the launch of new products through exclusive digital releases. This combination of convenience variety and accessibility drives the rapid growth of the online channel.

The quick surge of Online Stores is fueled by effective digital engagement and personalized recommendations that enhance the shopping experience. E commerce platforms use artificial intelligence and data analytics to suggest products based on past purchases and browsing behavior. Brands use social media influencers and live streaming sessions to demonstrate product uses and engage with potential buyers. Interactive features such as quizzes help consumers identify the right dairy alternative for their dietary needs. The integration of user generated content such as recipes and testimonials builds community and trust. Online platforms also offer easy return policies and customer support which reduces purchase anxiety. The ability to track orders in real time provides transparency and reassurance. Digital loyalty programs reward frequent buyers with points and discounts encouraging repeat purchases. The seamless integration of payment options including digital wallets simplifies the checkout process. This high level of engagement and personalization creates a compelling value proposition for digital shoppers. The continuous improvement in user interface and experience ensures that online stores remain the preferred channel for tech savvy consumers.

REGIONAL ANALYSIS

China Dairy Alternatives Market Analysis

China led the Asia Pacific Dairy Alternatives Market and captured a 62.4% share in 2025. The demand for dairy alternatives in China was supported by its massive population and growing health consciousness. The country is characterized by a high prevalence of lactose intolerance which makes plant based milks a necessity for many consumers. According to sources, China's plant-based milk market is expanding steadily due to a large lactose-intolerant population, with traditional soy milk holding a major share while oat and coconut milks grow rapidly. The government support for food security and sustainable agriculture encourages the development of local plant based industries. E commerce platforms like JD.com and Tmall play a crucial role in distribution offering wide accessibility to various brands. Chinese consumers are increasingly aware of the environmental impact of food choices driving interest in sustainable alternatives. The presence of international brands alongside local players creates a competitive landscape that fosters innovation. Regulatory standards for labeling and safety are becoming stricter ensuring product quality. The trend towards westernized diets increases the consumption of dairy alternatives in coffee and baking. The vast market size and evolving consumer preferences ensure sustained growth. China serves as a key driver of regional trends with its rapid adoption of new technologies and flavors. The focus on health and wellness continues to shape the market dynamics.

India Dairy Alternatives Market Analysis

India continues to be a significant player in the Asia Pacific Dairy Alternatives market because of a strong cultural tradition of plant based eating. The country has a large vegetarian population which naturally aligns with the consumption of dairy alternatives. According to the Ministry of Food Processing Industries the production of soy milk and other plant based beverages is increasing to meet domestic demand. The rising incidence of lifestyle diseases is prompting consumers to seek healthier options with lower saturated fat. Traditional beverages such as badam milk and thandai are being modernized and packaged for retail sale. The expansion of organized retail and e commerce improves access to branded products in urban areas. Government initiatives promoting millet and pulse based foods further boost the sector. The young demographic is open to experimenting with global trends such as oat and almond milk. Local manufacturers are leveraging traditional recipes to create unique products that appeal to local tastes. The cost sensitivity of the market drives innovation in affordable packaging and formulations. India potential for growth is substantial due to its large population and shifting dietary habits. The integration of modern processing technologies enhances product quality and shelf life.

Japan Dairy Alternatives Market Analysis

Japan was positioned second in the Asia Pacific Dairy Alternatives market and held a 12.5% share in 2025. This position was supported by high health awareness and an aging population. The country has a long history of consuming soy milk which serves as a foundation for other plant based options. According to the Ministry of Agriculture Forestry and Fisheries the demand for functional foods including plant based milks is steady among older consumers. The convenience store culture ensures wide availability of ready to drink plant based beverages. Innovations in flavor such as black sesame and red bean appeal to traditional palates. The government promotion of healthy eating habits supports the adoption of low calorie and cholesterol free options. The presence of established food companies drives continuous product development and marketing. Japanese consumers are willing to pay for high quality products with proven health benefits. The trend towards minimalism and clean labeling resonates with local preferences. The aging population seeks nutritious options that support bone and heart health. Japan serves as a trendsetter for premiumization and quality standards in the region. The focus on sustainability and ethical sourcing is gaining traction among younger buyers.

South Korea Dairy Alternatives Market Analysis

South Korea holds a noteworthy position in the Asia Pacific Dairy Alternatives Market due to a strong influence from global food trends and a youthful demographic. The country is characterized by rapid adoption of vegan and plant based lifestyles particularly among millennials and Gen Z. According to the Korea Agro Fishery and Food Trade Corporation the import and local production of oat and almond milk are increasing significantly. Social media plays a crucial role in spreading awareness and influencing purchasing decisions. Korean consumers are highly interested in aesthetic and packaging which brands leverage to attract attention. The government support for green growth and sustainable food systems encourages industry innovation. Local startups are emerging with unique formulations that cater to specific dietary needs. The popularity of K beauty and wellness extends to dietary choices promoting internal health. The convenience of online shopping and quick delivery supports market growth. South Korea serves as a hub for innovation and trend setting in the region. The focus on premium and specialized products drives market value.

Australia Dairy Alternatives Market Analysis

Australia is anticipated to expand significantly in the Asia Pacific Dairy Alternatives market during the forecast period owing to high per capita consumption and strong environmental consciousness. The country has one of the highest rates of veganism and flexitarianism in the world driving demand for plant based options. According to the Australian Bureau of Statistics, while sales of plant-based milks have grown fast over recent years, conventional dairy milk still makes up the vast majority of total milk sales across the country. The presence of major global and local brands creates a competitive and innovative market. Supermarkets play a dominant role in distribution with extensive shelf space for dairy alternatives. The government support for agricultural innovation supports the production of local ingredients like oats and almonds. Consumers are well educated about the health and environmental benefits of plant based diets. The trend towards clean label and organic products is particularly strong. Australia serves as a testing ground for new products and flavors before regional expansion. The high disposable income allows consumers to afford premium alternatives. The focus on transparency and traceability builds consumer trust.

COMPETITION OVERVIEW

The competition in the Asia Pacific Dairy Alternatives Market is intense and characterized by a mix of established local giants and emerging international brands. Local players leverage their deep understanding of regional tastes and strong distribution networks to maintain dominance in traditional categories like soy milk. International brands compete by introducing premium products such as oat and almond milk targeting urban and affluent consumers. Innovation in flavor texture and nutritional fortification is a key differentiator as companies strive to meet evolving consumer expectations. Price competition is significant in price sensitive markets while premiumization drives growth in developed economies. Regulatory standards and labeling requirements vary across countries adding complexity to market entry and expansion. Supply chain efficiency and sustainability credentials are increasingly important competitive factors. Digital marketing and e commerce capabilities enable brands to reach wider audiences and engage directly with consumers. The market sees frequent new product launches and collaborations with food service providers to boost visibility. Consolidation through acquisitions is common as larger players seek to expand their portfolios. This dynamic environment requires continuous adaptation and innovation to sustain competitive advantage.

KEY MARKET PLAYERS

A few major players of the Asia-Pacific dairy alternatives market include

- The Hain Celestial Group Inc

- The WhiteWave Foods Company

- Nutriops S.L

- Freedom Foods Group Limited

- Blue Diamond Growers

- Archer Daniels Midland Company

- Sanitarium Health & Wellbeing Company

- Daiya Foods Inc

- SunOpta Inc

- Earth’s Own Food Company

- Eden Foods, Inc

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific Dairy Alternatives Market primarily focus on product innovation and localization to meet diverse consumer preferences. Companies invest heavily in research and development to create new flavors and textures using local ingredients such as soy coconut and oats. Strategic partnerships with food service providers and coffee chains help increase brand visibility and drive trial among consumers. Expansion of distribution networks through e commerce platforms and modern retail outlets ensures wider accessibility. Sustainability initiatives including eco friendly packaging and ethical sourcing are central to corporate strategies to appeal to environmentally conscious buyers. Marketing campaigns emphasize health benefits and lifestyle alignment to attract younger demographics. Companies also pursue mergers and acquisitions to consolidate market position and access new technologies. These strategies collectively drive growth and enhance competitiveness in the dynamic regional landscape.

Leading Players in the Asia-Pacific Dairy Alternatives Market

- Vitasoy International Holdings Limited is a dominant force in the Asia Pacific dairy alternatives sector with deep roots in soy based beverages. The company leverages its extensive distribution network across China and Southeast Asia to maintain strong brand visibility and consumer loyalty. Recent actions to strengthen its market position include the launch of innovative plant based products such as oat milk and almond milk to diversify its portfolio beyond traditional soy. Vitasoy has also invested in sustainable sourcing practices and upgraded manufacturing facilities to improve efficiency and reduce environmental impact. The company actively engages in marketing campaigns that highlight the health benefits of plant based nutrition appealing to health conscious consumers. By expanding its product range and enhancing operational capabilities Vitasoy continues to solidify its leadership in the regional market. Their focus on quality and innovation ensures they remain competitive against both local and international rivals.

- Oatly Group AB has rapidly expanded its presence in the Asia Pacific market by capitalizing on the growing popularity of oat milk among urban consumers. The company focuses on premium positioning and sustainability which resonates with environmentally aware buyers in countries like China Japan and Singapore. Recent actions include establishing local production facilities in China to reduce supply chain costs and improve product freshness. Oatly has also partnered with major coffee chains and restaurants to integrate its products into food service offerings increasing brand exposure. The company utilizes digital marketing and social media influencers to engage with younger demographics and build brand community. By emphasizing its carbon footprint labeling and ethical sourcing Oatly differentiates itself from competitors. These strategic moves enable Oatly to capture significant market share in the premium segment and drive growth in the region.

- Yangyuan Food & Beverage Co Ltd is a key player in the Chinese market known for its walnut milk and other plant based beverages. The company focuses on leveraging traditional Chinese ingredients to create unique dairy alternatives that appeal to local tastes. Recent actions to strengthen its market position include the expansion of its production capacity and the introduction of new flavors and formulations. Yangyuan has also enhanced its distribution channels by strengthening partnerships with e commerce platforms and modern retail outlets. The company invests in research and development to improve the nutritional profile and taste of its products. By focusing on health benefits such as brain health and immunity Yangyuan attracts health conscious consumers. Their commitment to quality and innovation helps them maintain a strong competitive edge in the domestic market. This localized approach allows Yangyuan to effectively compete with global brands.

MARKET SEGMENTATION

This research report on the Asia-Pacific dairy alternatives market has been segmented and sub-segmented based on application, distribution channel & region.

By Application

- Milk

- Cheese

- Yogurt

- Ice Creams

- Creamers

By Distribution Channel

- Hypermarkets/Supermarkets

- Online Stores

- Convenience Stores

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC