- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

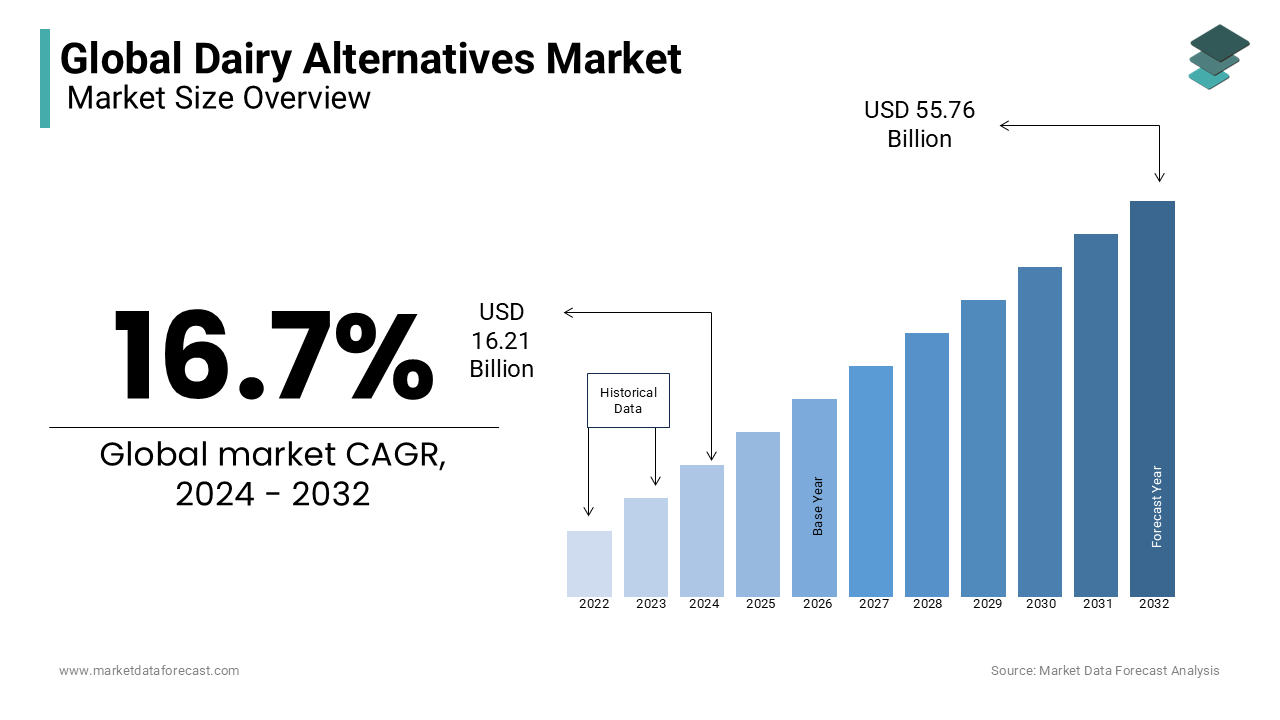

Market Size, 2025

$18.92 BnMarket Estimate, 2026

$22.08 BnMarket Forecast, 2034

$75.96 BnCAGR, 2026–2034

16.7%Global Dairy Alternatives Market Size

The global dairy alternatives market size was valued at USD 18.92 billion in 2025 and is estimated to reach USD 75.96 billion by 2034 from USD 22.08 billion in 2026, registering a CAGR of 16.7% from 2026 to 2034

The Dairy Alternatives is a plant-based and fermentation-derived products designed to replicate the sensory, nutritional, and functional attributes of traditional dairy, including milk, yogurt, cheese, and ice cream. According to the Food and Agriculture Organization of the United Nations, global milk production has plateaued in efficiency gains, with methane emissions from dairy cattle accounting for approximately 2.9% of total anthropogenic greenhouse gas emissions. As per the Intergovernmental Panel on Climate Change, livestock systems contribute significantly to land-use change, with dairy farming occupying nearly 26% of the world’s ice-free terrestrial surface.

MARKET DRIVERS

Escalating Consumer Awareness of Environmental Impact of Animal Agriculture

The growing consumer recognition of the environmental toll associated with conventional dairy farming is significantly boosting the growth of the global dairy alternatives market. Livestock production is a major contributor to deforestation, water depletion, and greenhouse gas emissions, prompting environmentally conscious consumers to shift toward plant-based options. According to the Food and Agriculture Organization of the United Nations, the global dairy sector is responsible for approximately 2.9 billion metric tons of CO₂-equivalent emissions annually, representing nearly 4% of all human-induced climate emissions. Land use disparities are equally stark; the University of Oxford’s 2023 analysis of global food systems revealed that dairy farming uses 11 times more land per gram of protein than plant-based alternatives. Retailers like Tesco and Woolworths have responded by introducing carbon labeling on dairy and alternative products.

Rising Prevalence of Lactose Intolerance and Dairy-Related Health Concerns

The widespread incidence of lactose intolerance and increasing scrutiny of dairy’s role in chronic health conditions are significantly amplifying the growth of the global dairy alternatives market. The National Institutes of Health states that approximately 68% of the global population exhibits some degree of lactase deficiency, with prevalence exceeding 90% in East Asian, West African, and Indigenous American populations. This biological constraint has created a natural market for lactose-free, plant-based substitutes that offer comparable calcium and vitamin D fortification without gastrointestinal discomfort. Beyond intolerance, concerns about saturated fat, hormones, and antibiotic residues in conventional dairy are influencing dietary shifts. Similarly, the Shanghai Municipal Center for Disease Control encourages plant milk consumption among schoolchildren to reduce obesity risks.

MARKET RESTRAINTS

Sensory and Functional Limitations in Product Performance

Many dairy alternatives continue to face consumer resistance due to deficiencies in taste, texture, and culinary functionality compared to traditional dairy is restricting the growth of the global dairy alternatives market. These sensory gaps are particularly pronounced in high-heat applications; oat milk, for instance, tends to scorch during steaming, limiting its utility in café environments. As per the American Dairy Science Association, only 22% of commercial plant-based yogurts achieve the same viscosity and syneresis resistance as Greek yogurt, leading to consumer dissatisfaction. Additionally, fermentation-based alternatives, while promising, remain cost-prohibitive for mass adoption. Consumer Reports’ 2023 taste panel ranked seven of the top ten best-selling plant milks below conventional whole milk in overall satisfaction.

High Production Costs and Limited Economies of Scale

The elevated cost structure of dairy alternative production is a significant barrier to broad market penetration in price-sensitive regions, which is to hinder the growth of the global dairy alternatives market. Fermentation-based dairy proteins, such as those produced by precision fermentation, can cost upwards of USD 10 per liter at current scale, as reported by the Good Food Institute in 2023. These cost disparities are reflected in retail pricing, where plant-based cheeses often retail at two to three times the price of their dairy counterparts, discouraging adoption among lower-income consumers.

MARKET OPPORTUNITIES

Advancements in Precision Fermentation and Cellular Agriculture

The precision fermentation by enabling the production of real milk proteins such as casein and whey without animals, thereby bridging the sensory and nutritional gap between traditional and plant-based dairy is substantially to promote new opportunities for the growth of the global dairy alternatives market. Companies like Perfect Day and Remilk utilize genetically engineered microflora to produce identical dairy proteins through fermentation, which are then incorporated into lactose-free, animal-free milk, cheese, and ice cream. Additionally, fermentation facilities can be modular and geographically decentralized, reducing supply chain vulnerabilities. In Singapore, Eat Just’s cultured dairy proteins are being integrated into school nutrition programs as part of the nation’s Future Food initiative.

Expansion into Emerging Markets with Tailored Product Formulations

The adaptation of dairy alternatives to local tastes, ingredients, and nutritional needs is likely to influence the growth of the global dairy alternatives market. According to the International Institute of Tropical Agriculture, coconut milk is already consumed by over 300 million people across Indonesia, the Philippines, and Nigeria, providing a ready-made platform for commercialization. Similarly, in India, companies like Epigamia and Milky Mist have successfully localized by using malai and chhachh as inspiration for traditional-style plant yogurts.

MARKET CHALLENGES

Regulatory Ambiguity and Labeling Restrictions

The regulatory scrutiny over naming conventions, compositional standards, and health claims, is to impede the growth of the global dairy alternatives market. Several countries have enacted legislation restricting the use of terms like “milk,” “cheese,” and “butter” for non-dairy products. In 2023, the European Union’s Court of Justice upheld a ban on plant-based products using dairy terminology, a decision supported by France’s National Assembly, which argued that such labeling misleads consumers. These measures increase packaging complexity and reduce shelf appeal. In the United States, the FDA has initiated a rulemaking process to define “milk” and “cheese” for labeling purposes, potentially forcing rebranding across major product lines. According to the Plant Based Foods Association, 38% of new product launches in 2023 were delayed due to labeling compliance issues.

Ingredient Sourcing Sustainability and Environmental Trade-offs

The rising environmental burdens, particularly concerning water use, monoculture farming, and biodiversity loss is quietly to degrade the growth of the global dairy alternatives market. Almond milk, one of the most popular substitutes, has come under scrutiny for its high water footprint and impact on pollinator health. According to the Pacific Institute, almond cultivation in California consumes approximately 4.3 billion gallons of water annually, with a single nut requiring 1.1 gallons to grow. This has exacerbated water stress in drought-prone regions, prompting the state’s Department of Water Resources to impose irrigation limits in 2023. Oat farming, while more sustainable, is increasingly associated with glyphosate use; a 2023 Consumer Reports analysis detected residues in 29 of 31 oat-based dairy products tested.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 16.7% |

| Segments Covered | By Application, Distribution Channel and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Vitsoy International Holding Limited, CP Kelko, Daiya Foods Inc, WhiteWave Foods Company, Nutriops S.L, OT AB, Eden Foods, Freedom Food Group Co Ltd, Blue Diamond Grower Inc, Hain Celestial Group and Others. |

SEGMENTAL ANALYSIS

By Application Insights

The plant-based milk segment was accounted in holding a prominent share of the global dairy alternatives market in 2025 with its role as the foundational category that introduced consumers to dairy-free living. According to the United States Department of Agriculture, over 68% of American households now purchase plant-based milk, with oat and soy variants leading in retail volume. The category benefits from early regulatory clarity and standardization; Codex Alimentarius has established guidelines for labeling and fortification, ensuring product consistency.

The Non-dairy creamers segment is likely to grow with an expected CAGR of 16.4% during the forecast period with the rising consumption of specialty coffee and the integration of plant-based options in foodservice environments. As per the National Coffee Association, 65% of coffee drinkers in the U.S. use some form of creamer, and among them, 38% now prefer non-dairy versions, citing dietary restrictions, vegan lifestyles, and cleaner labels. Innovation has accelerated, with brands like Califia Farms and Nestlé launching barista-grade liquid and powdered creamers that resist curdling and enhance mouthfeel. These products are increasingly fortified with MCT oils and prebiotics to appeal to the health-conscious consumer. Additionally, private-label creamers are expanding in supermarkets, offering cost-effective alternatives.

By Distribution Channel Insights

The supermarkets segment was the largest and held 52.8% of global dairy alternatives market share in 2025 with its ability to offer wide product variety, competitive pricing, and prominent shelf placement in dedicated “plant-based” or “free-from” sections. Major retailers such as Walmart, Kroger, and AEON have expanded refrigerated plant-based dairy aisles, often co-locating alternatives with traditional dairy to facilitate direct comparison. Supermarkets benefit from established cold chain logistics, enabling the distribution of perishable items like yogurt and cream cheese. Additionally, in-store promotions, sampling events, and loyalty program integrations have proven effective in driving trial and repeat purchases.

The online stores segment is expected to register a CAGR of 18.7% during the forecast period with the increasing preference for e-grocery shopping, subscription models, and direct-to-consumer (DTC) brand engagement. According to the U.S. Census Bureau, online grocery sales reached USD 148 billion in 2023, with plant-based products overrepresented in digital baskets. Subscription services like Misfits Market and Thrive Market offer curated plant-based boxes, improving accessibility and reducing trial barriers. In India and Southeast Asia, platforms such as BigBasket and RedMart have introduced dedicated “vegan” filters and bundled offers, enhancing discoverability. A 2023 study by McKinsey & Company found that 54% of plant-based food buyers prefer online channels for their wider selection and ability to read ingredient labels in detail. Additionally, DTC brands like Oatly and Miyoko’s Creamery use digital platforms to educate consumers, share recipes, and launch limited-edition products. The integration of AI-driven recommendations and same-day delivery in urban centers further enhances convenience.

REGIONAL ANALYSIS

North America Dairy Alternatives Market Insights

North America was the top performer of the global dairy alternatives market with 38.2% of share in 2025 with the high consumer awareness, robust regulatory frameworks, and early adoption of plant-based lifestyles. The United States Department of Agriculture notes that plant-based milk now accounts for 15% of total milk sales by volume, surpassing lactose-free dairy milk. According to the Plant Based Foods Association, U.S. retail sales of plant-based foods reached USD 8.1 billion in 2023, with dairy alternatives contributing nearly 40%. California, New York, and Ontario serve as epicenters of product development, hosting major brands like Danone North America (Silk), Oatly, and Ripple. The region benefits from strong venture capital investment in food tech, with USD 1.3 billion allocated to alternative protein startups in 2023, according to the Good Food Institute. Additionally, federal dietary guidelines increasingly recognize plant-based diets as nutritionally adequate, lending credibility to the category. Retail penetration is near-universal, with Walmart, Kroger, and Whole Foods dedicating extensive shelf space. Foodservice integration is also advanced, with chains like Panera Bread and Dunkin’ offering plant-based creamers and cheeses.

Europe Dairy Alternatives Market Insights

Europe dairy alternatives market was positioned second by holding 11.2% of the share in 2025 with the stringent environmental policies, high animal welfare standards, and government-backed dietary shifts. The European Union’s Farm to Fork Strategy aims to reduce dairy consumption by 2030 as part of its climate neutrality goals, incentivizing plant-based innovation. Retail consolidation enhances market access; Carrefour, Tesco, and Aldi now offer over 200 plant-based dairy SKUs across their networks. In Sweden, plant milk accounts for over 40% of total milk sales, as reported by IRI, reflecting deep cultural integration. Fortification with vitamin B12, calcium, and iodine is standard, addressing nutritional concerns. However, regulatory challenges persist, with the EU restricting dairy terminology for non-animal products.

Asia Pacific Dairy Alternatives Market Insights

Asia Pacific dairy alternatives market growth is esteemed to grow with prominent CAGR in the next coming years with the region’s foundation lies in traditional foods soy milk, coconut milk, and tofu by providing a natural entry point for modernized alternatives. India’s dairy alternatives market grew by 22% in 2023, fueled by lactose intolerance prevalence exceeding 60% and the rise of veganism in urban centers like Mumbai and Bangalore. Government initiatives are emerging; Singapore’s “30 by 30” food security goal includes support for alternative proteins. However, price sensitivity and limited cold chain infrastructure constrain rural penetration.

Latin America Dairy Alternatives Market Insights

Latin America dairy alternatives market growth is gearing up with steady growth owing to the agricultural abundance, rising middle-class health awareness, and regional innovation. The continent is a natural producer of key raw materials soybeans in Brazil, coconuts in Colombia, and almonds in Chile by enabling cost-effective local manufacturing. Chile has emerged as a regulatory leader, becoming the first Latin American country to implement front-of-package warning labels on high-sugar and high-fat dairy products, indirectly promoting plant-based alternatives. Retail chains like Cencosud and Walmart Mexico have expanded plant-based sections, while e-commerce platforms such as Mercado Libre report 29% year-on-year growth in alternative dairy sales.

Middle East and Africa Dairy Alternatives Market Insights

The Middle East and Africa dairy alternatives market is to grow steadily in the next coming years. Urban centers like Dubai, Johannesburg, and Nairobi are witnessing a surge in health-conscious consumers and vegan lifestyles, supported by expanding expatriate communities and wellness trends. The UAE’s Ministry of Climate Change and Environment has launched the “National Food Security Strategy 2051,” which includes investment in alternative proteins and sustainable agriculture. In 2023, plant-based milk sales in the Gulf Cooperation Council (GCC) grew by 24%, according to NielsenIQ, with almond and oat variants leading. Retailers like Spinneys and Pick n Pay have introduced dedicated plant-based aisles, while e-commerce platforms such as Jumia are boosting accessibility. South Africa’s Woolworths reported a 31% increase in plant-based yogurt sales in 2023, reflecting rising demand. However, challenges remain, including high import dependency, limited local production, and price premiums. Initiatives like Kenya’s coconut milk cooperatives and Egypt’s soybean cultivation programs are beginning to address supply gaps.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Vitsoy International Holding Limited, CP Kelko, Daiya Foods Inc., WhiteWave Foods Company, Nutriops S.L, OT AB, Eden Foods, Freedom Food Group Co Ltd, Blue Diamond Grower Inc., and Hain Celestial Group are a few of the notable companies in the global dairy alternatives market.

The competitive environment in the dairy alternatives market is marked by a dynamic interplay between pioneering plant-based brands, legacy food corporations, and biotech innovators. Established players like Oatly and Danone dominate through brand recognition, retail penetration, and consumer trust, while legacy dairy companies such as Fonterra and Lactalis are repositioning themselves with plant-based portfolios to retain relevance. The emergence of precision fermentation firms like Perfect Day and Remilk is disrupting the category by offering animal-free dairy proteins that bridge the sensory gap, introducing a new tier of technological competition. Regional players in Asia, Africa, and Latin America are gaining ground by leveraging local ingredients and cultural familiarity with plant-based staples, challenging global brands on authenticity and affordability. Price competition is intensifying, particularly in supermarkets where private-label alternatives are undercutting branded products. Differentiation is achieved through sustainability claims, nutritional enhancement, and foodservice integration. Regulatory divergence across markets adds complexity, with naming restrictions in Europe and labeling debates in the U.S. shaping brand strategies.

TOP PLAYERS IN THE MARKET

Oatly Group AB

Oatly has emerged as a transformative force in the global dairy alternatives landscape by leveraging its proprietary enzyme technology to produce creamy, scalable oat-based milk with a low environmental footprint. In 2023, Oatly partnered with Starbucks Japan to become the exclusive oat milk supplier across all company-operated stores, significantly boosting brand visibility and accessibility. The company has also invested in urban pop-up cafes in Shanghai and Sydney to engage directly with consumers and promote plant-based lifestyles. Oatly actively collaborates with foodservice operators, convenience stores, and e-commerce platforms to enhance distribution.

Danone SA

Danone has prominence its influence in the dairy alternatives market through its Silk, Alpro, and So Delicious brands, which span plant-based milks, yogurts, and desserts. In Asia Pacific, the company has intensified its focus on innovation and localization, launching rice-based and coconut-milk yogurts adapted to regional flavor preferences in Southeast Asia. Danone strengthened its presence in India by expanding distribution of plant-based products through modern retail and e-commerce channels in 2023. The company also invested in cold chain infrastructure to support the availability of perishable alternatives in urban centers. Through its partnership with Singapore’s Health Promotion Board, Danone promoted plant-based dairy as part of balanced diets under the national “Healthy 365” campaign. Alpro products are now available in over 15,000 outlets across Australia and New Zealand, supported by carbon-neutral certification and recyclable packaging initiatives. Danone’s integration of sustainability, nutrition science, and regulatory engagement has positioned it as a trusted, science-backed player.

Perfect Day, Inc.

Perfect Day is redefining the dairy alternatives market through precision fermentation, producing animal-free milk proteins without livestock. The company’s whey and casein proteins are identical to those in cow’s milk but require 97% less water and 60% less energy to produce, as per a 2023 lifecycle assessment by the University of California, Davis. In Asia Pacific, Perfect Day has forged strategic alliances with regional food manufacturers to launch next-generation dairy-free products. In 2023, it partnered with Thai Union Group to develop sustainable, animal-free dairy ingredients for functional foods and beverages in Southeast Asia. The company also collaborated with Japan’s Kewpie Corporation to explore fermentation-derived proteins for infant nutrition and clinical applications. Perfect Day’s proteins are now used in ice creams, yogurts, and protein powders sold in Singapore, Australia, and South Korea. Regulatory approvals from Singapore’s Food Agency and Australia’s FSANZ have accelerated commercialization.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the dairy alternatives market are deploying a spectrum of strategies to consolidate their influence and adapt to evolving consumer and regulatory landscapes. A dominant approach is product innovation, with companies investing in next-generation formulations that improve taste, texture, and nutritional profiles through protein fortification and allergen reduction. Precision fermentation and cellular agriculture are being leveraged to create animal-free dairy proteins that mimic the functional properties of casein and whey. Strategic partnerships with foodservice chains, such as Oatly’s collaboration with Starbucks, enhance visibility and normalize plant-based consumption. Vertical integration is gaining traction, with firms securing upstream supply chains for raw materials like oats, soy, and coconuts to ensure sustainability and cost control. Digital engagement and direct-to-consumer models are being scaled to build brand loyalty and gather consumer insights. Sustainability is embedded as a core differentiator, with brands adopting carbon labeling, recyclable packaging, and regenerative agriculture commitments. Additionally, companies are navigating regulatory challenges by engaging with policymakers and investing in clinical studies to support health claims. Mergers and acquisitions are accelerating by enabling rapid technology acquisition and market access.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Oatly launched its oat milk production facility in Singapore by enabling localized manufacturing for the Asia Pacific region and reducing carbon emissions from transportation by 40%.

- In March 2023, Danone partnered with Starbucks Japan to become the exclusive supplier of plant-based milk, which is expanding its presence in over 1,500 café locations and increasing consumer accessibility.

- In August 2023, Perfect Day collaborated with Thai Union Group to develop animal-free dairy proteins for functional foods by targeting health-conscious consumers in Southeast Asia.

- In November 2023, Alpro introduced a new line of coconut-based yogurts fortified with probiotics and calcium that is tailored to consumer preferences in Australia and New Zealand.

- In February 2025, Silk expanded its distribution network in India by partnering with BigBasket and Nature’s Basket, which is enhancing availability of plant-based milk and creamers in major urban centers.

MARKET SEGMENTATION

This research report on the global dairy alternatives market has been segmented and sub-segmented based on application, distribution channel and region.

By Application

- Milk

- Cheese

- Yogurt

- Ice Creams

- Creamers

By Distribution Channel

- Supermarkets

- Health Stores

- Pharmacies

- Online Stores

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa