- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

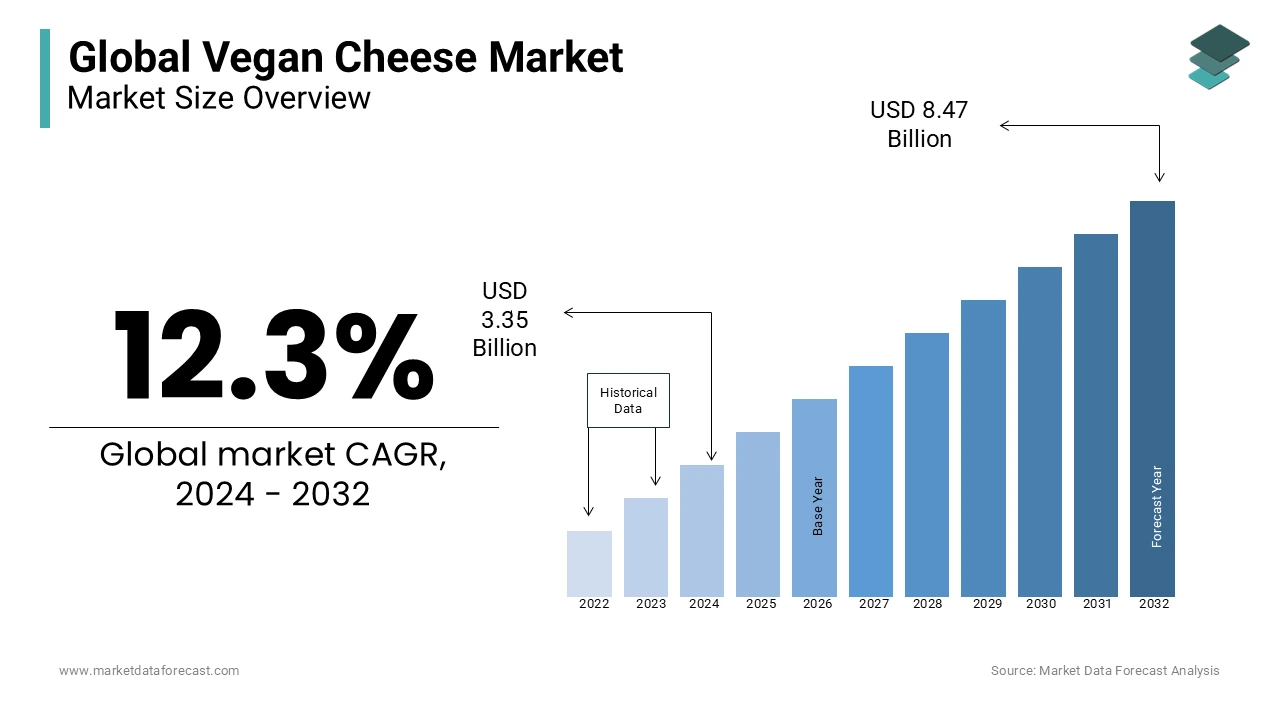

Market Size, 2025

$3.76 BnMarket Estimate, 2026

$4.22 BnMarket Forecast, 2034

$10.67 BnCAGR, 2026–2034

12.3%Global Vegan Cheese Market Summary

The global vegan cheese market was valued at USD 3.76 billion in 2025, is projected to reach USD 4.22 billion in 2026, and is expected to grow substantially to USD 10.67 billion by 2034, registering a CAGR of 12.3% from 2026 to 2034. Growth is driven by rising adoption of plant-based diets, increased lactose intolerance cases, and expanding consumer demand for sustainable and cruelty-free dairy alternatives. Improvements in vegan cheese texture, flavor, and meltability—combined with strong retail availability and growing vegan product innovation—continue to support rapid global market expansion.

Key Market Trends

- Rising demand for plant-based dairy alternatives, especially among flexitarians and vegans.

- Strong growth in mozzarella-style vegan cheese, supported by rising use in pizzas and fast-food applications.

- Increasing focus on nut-based cheeses, particularly cashew, almond, and coconut variants.

- Expansion of B2C retail channels, including supermarkets and specialty vegan stores.

- Growing investment in clean-label, allergen-free, and fortified vegan cheese formulations.

Segmental Insights

- Based on product, the mozzarella segment dominated with over 30% share in 2023, driven by its extensive use in fast food, baked dishes, and global cuisine.

- Based on source, the cashew segment accounted for 36.4% share in 2023 and is expected to remain the leading base ingredient due to its creamy texture and versatility.

- Based on end use, the B2C segment led with 56.7% share in 2023, supported by rising household adoption and the wide availability of vegan cheese in retail stores.

Regional Insights

- Europe generated more than 35% of global revenue in 2023 and will continue leading the market due to strong vegan food adoption, advanced retail infrastructure, and rising preference for plant-based dairy alternatives.

- North America remains a major growth region driven by innovation, premium product launches, and expanding vegan consumer base.

- Asia Pacific is emerging rapidly as awareness of plant-based diets and sustainable food choices increases.

Competitive Landscape

The vegan cheese market is moderately competitive, with brands focusing on improving product taste, texture, and nutritional quality. Companies are investing in R&D, expanding global retail distribution, and introducing new clean-label and allergen-friendly varieties to enhance their market presence.

Key players in the global vegan cheese market include:

Violife Foods, Daiya Foods, Tyne Chease Limited, Vtopian Artisan Cheese Company, Kite Hill, Miyoko’s Kitchen Company, Vermont Farmstead Company, Good Planet Foods, Follow Your Heart, and Galaxy Nutritional Foods, Inc.

Global Vegan Cheese Market Size

The global vegan cheese market size was valued at USD 3.76 billion in 2025, and the global market size is expected to reach USD 10.67 billion by 2034 from USD 4.22 billion in 2026. The market's promising CAGR for the predicted period is 12.3%.

Vegan cheese encompasses a diverse array of dairy free alternatives formulated to replicate the taste, texture, and melting properties of traditional cheese using plant based ingredients. Primary bases include nuts such as cashews and almonds, soy, coconut oil, and increasingly innovative sources like fermented precision fermentation proteins. This sector has evolved from a niche dietary substitute to a mainstream culinary staple driven by ethical, environmental, and health considerations. According to the Food and Agriculture Organization of the United Nations, the livestock sector accounts for approximately 11.1% of all human induced greenhouse gas emissions, which motivates consumers to seek lower impact food options. Furthermore, the World Health Organization states that high consumption of saturated fats found in many dairy products is linked to cardiovascular diseases, prompting a shift toward plant based fats. The definition of vegan cheese now extends beyond simple analogs to include artisanal aged varieties and functional shreds that perform identically to dairy in cooking applications. As per the Good Food Institute, investment in alternative protein technologies reached $1.6 billion in 2023, indicating strong industrial confidence in this category. Regulatory bodies are also refining labeling standards to ensure transparency regarding ingredient sourcing and nutritional content. The market is characterized by rapid innovation in fermentation technology, which enhances flavor complexity and mouthfeel. Consumers are no longer willing to compromise on sensory experience, driving manufacturers to invest heavily in research and development. This dynamic landscape positions vegan cheese as a critical component of the broader sustainable food system transformation.

MARKET DRIVERS

Rising Prevalence of Lactose Intolerance and Dairy Allergies

The increasing global prevalence of lactose intolerance and milk allergies is primarily driving the growth of the global vegan cheese market. Lactose intolerance affects a significant portion of the adult population worldwide, leading to digestive discomfort upon consuming dairy products. According to the National Institutes of Health, approximately 68% of the world's population has lactose malabsorption, with higher rates observed in Asian, African, and Native American communities. In the United States, the Food and Drug Administration mandates clear labeling of allergens including milk, which has heightened awareness and driven demand for clearly labeled dairy free options. As per the American College of Gastroenterology, as many as 90% of people from some areas of Eastern Asia and 80% of American Indians have some degree of lactose intolerance. Many individuals who previously avoided cheese due to health concerns are now embracing vegan alternatives that offer similar culinary versatility without adverse reactions. The American College of Gastroenterology notes that symptoms of lactose intolerance can significantly impact quality of life, prompting patients to strictly eliminate dairy from their diets. This medical necessity creates a loyal customer base that relies on vegan cheese for daily nutrition and meal preparation. Additionally, the rise in diagnosed casein allergies among children has prompted parents to seek plant based substitutes early in life, fostering long term brand loyalty. Manufacturers respond by fortifying these products with calcium and vitamin B12 to address nutritional gaps left by excluding dairy. This health driven demand ensures consistent growth regardless of fluctuating ethical trends.

Growing Ethical Consciousness and Animal Welfare Advocacy

Ethical considerations regarding animal welfare and the environmental impact of industrial dairy farming are further fuelling the expansion of the global vegan cheese market. Consumers are increasingly aware of the conditions in which dairy cows are raised and the ethical implications of conventional milk production. According to the Humane Society of the United States, around 5.7 million cats and dogs enter shelters annually, and millions of people choose plant based lifestyles because they do not want to use animals. Documentaries and social media campaigns have exposed the realities of the dairy industry, influencing public perception and purchasing behavior. As per the United Nations Environment Programme, deforestation is responsible for about 11% of global greenhouse gas emissions, further motivating environmentally conscious shoppers to switch to plant based options. Younger demographics, particularly Millennials and Generation Z, are at the forefront of this shift, prioritizing brands that align with their values of sustainability and compassion. According to NielsenIQ, sales of chilled plant based food in UK supermarkets grew by 1.7% in the last 12 weeks of 2025, indicating a strong market preference for responsible sourcing. Vegan cheese brands often emphasize their cruelty free status and lower carbon footprint in marketing efforts, resonating with this value driven segment. Retailers are expanding their plant based sections to accommodate this demand, making vegan cheese more accessible. This ethical momentum is not transient but represents a structural change in consumer values that supports long term market expansion.

MARKET RESTRAINTS

Sensory Disparities in Texture and Melting Performance

Despite technological advancements, sensory disparities in texture, flavor, and melting capabilities remain a significant restraint for the vegan cheese market. Many consumers find that plant based alternatives fail to fully replicate the complex mouthfeel, stretch, and melt of traditional dairy cheese. According to the International Food Information Council, taste still shapes choices, but interest in textured sensory rich foods is up 44% year over year. Coconut oil based cheeses often lack the protein structure necessary for proper stretching, while nut based varieties may have a grainy texture that differs from the smoothness of dairy. The Maillard reaction, which creates the desirable browning and flavor in melted dairy cheese, is difficult to mimic with plant proteins and fats. This sensory gap limits the usage of vegan cheese in certain culinary applications, such as pizza and grilled sandwiches, where performance is critical. As per the Good Food Institute, while innovation is rapid, achieving parity with dairy remains a technical challenge that requires substantial research and development investment. Negative initial experiences can deter repeat purchases, creating a hurdle for market penetration among flexitarians who are accustomed to dairy standards. Manufacturers struggle to balance clean label ingredients with the functional additives needed to improve texture. Until the sensory experience matches or exceeds that of dairy cheese, a segment of potential customers will remain hesitant to switch permanently.

Higher Price Points Compared to Conventional Dairy Products

The premium pricing of vegan cheese compared to conventional dairy counterparts is further impeding the expansion of the global vegan cheese market. Plant based cheeses typically cost significantly more due to higher raw material costs, complex processing requirements, and smaller economies of scale. According to the Bureau of Labor Statistics, the consumer price index for cheese and related products decreased by 1.5% in early 2026. Cashews, almonds, and other premium nuts used in artisanal vegan cheeses are subject to volatile global commodity prices, which further inflate production costs. In contrast, the conventional dairy industry benefits from established supply chains, government subsidies in many regions, and massive scale efficiency. As per the United States Department of Agriculture, dairy farmers received 36% of what consumers paid for Cheddar cheese in grocery stores in 2022. This price disparity makes vegan cheese a luxury item for many households rather than a staple grocery purchase. Economic downturns and inflationary pressures exacerbate this issue, causing consumers to prioritize essential items over premium alternatives. Retailers may hesitate to allocate extensive shelf space to high priced items with slower turnover rates. While prices are expected to decrease as production scales up, the current cost barrier restricts mass market adoption and confines the product largely to affluent urban demographics.

MARKET OPPORTUNITIES

Advancements in Precision Fermentation Technology

Advancements in precision fermentation technology is a promising opportunity for the vegan cheese market. This biotechnology allows microorganisms to produce casein and whey proteins identical to those found in cow's milk, which can then be used to create vegan cheese with authentic melting and stretching properties. According to the Good Food Institute, precision fermentation has attracted billions of dollars in investment, which is signalling strong industry confidence in its commercial viability. Companies utilizing this technology can bypass the sensory limitations of plant based fats and starches, offering a product that is indistinguishable from traditional cheese in taste and texture. The United States Food and Drug Administration have begun establishing regulatory pathways for these novel ingredients, facilitating their entry into the market. As per McKinsey and Company, biological innovations could generate up to $4 trillion in annual economic impact by 2030 to 2040, with food and agriculture being key sectors. This technology also appeals to ethically motivated consumers who avoid animal exploitation but miss the sensory experience of dairy. By leveraging fermentation, brands can position their products as both cruelties free and gastronomically superior. This innovation opens doors to partnerships with major food service providers and restaurants that require high performance ingredients. The ability to scale production efficiently will eventually lower costs, making these advanced cheeses accessible to a broader audience.

Expansion into Emerging Markets with Rising Health Awareness

Expansion into emerging markets in Asia Pacific, Latin America, and the Middle East offers significant growth opportunities for the global vegan cheese market as health awareness and disposable incomes rise. These regions are experiencing a surge in lifestyle diseases such as diabetes and heart disease, prompting consumers to seek healthier dietary options. According to the World Health Organization, noncommunicable diseases are the leading cause of death globally, with rapid urbanization in developing countries contributing to this trend. Plant based diets are increasingly viewed as a preventive health measure, driving demand for dairy free alternatives. According to the Asian Development Bank, the middle class in Asia is expanding rapidly, which is creating a larger consumer base capable of affording premium health foods. Local tastes and preferences can be addressed by developing vegan cheeses using regional ingredients such as tofu, coconut, and cashews which are already staples in many Asian cuisines. As per Euromonitor International, the health and wellness sector in emerging markets is growing at a faster rate than in developed nations. International brands can partner with local distributors to navigate regulatory landscapes and cultural nuances. E commerce platforms facilitate access to niche products in areas with limited physical retail infrastructure. By tailoring products to local flavors and price points, companies can capture early mover advantage in these high growth regions.

MARKET CHALLENGES

Complex Regulatory Landscape and Labeling Restrictions

The complex and evolving regulatory landscape regarding labeling and terminology is a significant challenge to the growth of the global vegan cheese market. In several jurisdictions, dairy industry lobbies have successfully pushed for restrictions on using terms like cheese, milk, or butter for plant based products. According to the European Court of Justice, plant based products cannot use designations such as milk, butter, or cheese, which are legally reserved for animal products. In the United States, the Food and Drug Administration continues to evaluate labeling standards, leading to uncertainty for brands navigating state level legislation. These regulatory ambiguities increase compliance costs and limit the ability of companies to clearly communicate product identity to consumers. As per the Plant Based Foods Association, legal battles over labeling divert resources from innovation and marketing efforts. Confusion among consumers regarding what constitutes vegan cheese versus dairy blends can lead to mistrust or accidental purchases by those with allergies. Standardization of definitions across different markets is lacking, requiring companies to adapt packaging and messaging for each region. This fragmentation complicates global expansion strategies and supply chain management. Furthermore, strict regulations on novel ingredients, such as those derived from precision fermentation, require lengthy approval processes delaying market entry. Navigating this legal maze requires substantial legal expertise and lobbying efforts, which can be prohibitive for smaller startups.

Supply Chain Volatility for Key Raw Materials

Supply chain volatility for key raw materials such as nuts, seeds, and coconut oil is further challenging the expansion of the global vegan cheese market. Many premium vegan cheeses rely on cashews, almonds, and coconuts which are susceptible to climate change, pests, and geopolitical instability. According to the Food and Agriculture Organization of the United Nations, climate variability significantly impacts crop yields leading to price fluctuations and supply shortages. For instance, droughts in major cashew producing regions like Vietnam and India can drastically reduce availability and drive up costs. Coconut oil prices are also highly volatile due to weather patterns and changing export policies in Southeast Asia. As per the World Bank, commodity price shocks can disrupt production schedules and erode profit margins for manufacturers who cannot easily pass costs to consumers. Dependence on specific geographic regions for these ingredients creates vulnerability to local disruptions such as labor strikes or trade disputes. Securing long term supply contracts is difficult in such an unpredictable environment, forcing companies to maintain higher inventory levels which ties up capital. Sustainability concerns regarding water usage in almond farming and deforestation in coconut production add another layer of complexity, requiring rigorous sourcing audits. Brands committed to ethical sourcing face higher costs and limited supplier options. Ensuring consistent quality and availability of raw materials is critical for maintaining consumer trust and operational stability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.3% |

| Segments Covered | By Source, Product, End Use, and Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Violife Foods, Daiya Foods, Tyne Chease Limited, Vtopian Artisan Cheese Company, Kite Hill, Miyoko’s Kitchen Company, Vermont Farmstead Company, Good Planet Foods, Follow Your Heart, Galaxy Nutritional Foods, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The mozzarella segment dominated the market by accounting for 33.2% of the global market share in 2025. The growth of mozzarella segment in the global market is primarily driven by the universal popularity of pizza and Italian cuisine which rely heavily on the melting and stretching properties of mozzarella. As per the National Association of Pizza Operators, pizza consumption remains one of the most frequent dining choices in North America and Europe, creating a consistent demand for high performance vegan alternatives. Consumers seek plant based mozzarella that mimics the melt and stretch of dairy cheese without compromising texture. The rise of home cooking during recent years has further amplified this demand as individuals attempt to recreate restaurant quality meals at home. According to the International Dairy Foods Association, mozzarella is the top cheese variety consumed in the United States and accounts for approximately 33% of total cheese production. Vegan brands have invested significantly in improving the functional attributes of their mozzarella shreds and blocks to meet these expectations. Retailers prioritize stocking vegan mozzarella due to its high turnover rate and broad consumer appeal. The availability of various formats including slices, shreds, and balls enhances convenience for different culinary uses. This segment benefits from strong brand recognition and extensive distribution networks. The ability of vegan mozzarella to perform well in baked dishes makes it a staple in both household pantries and food service operations, ensuring its continued market leadership.

However, the cream cheese segment is estimated to record a promising CAGR of 12.2% over the forecast period in the global market owing to the increasing popularity of plant based spreads for bagels, toast, and crackers, as well as its use in vegan desserts such as cheesecakes and frostings. According to the Specialty Food Association, plant based food sales grew to $8.1 billion in 2023 with plant based cream cheese being a significant contributor. The versatility of cream cheese in both savory and sweet applications makes it a valuable ingredient for home bakers and professional chefs. Social media trends showcasing vegan baking recipes have significantly boosted consumer interest and trial. As per the Good Food Institute, plant based cheese sales grew by 15.1% in late 2024, showing that innovation in fermentation technology has improved the texture and tanginess of vegan cream cheese. Major coffee chains and bakeries are incorporating vegan cream cheese into their menus driving visibility and acceptance. The convenience of ready to use tubs appeals to busy consumers looking for quick meal solutions. Additionally, the perception of cream cheese as a indulgent treat allows for premium pricing strategies. Brands are introducing flavored variants such as herb and garlic or strawberry to diversify offerings. This combination of culinary versatility and lifestyle alignment ensures sustained high growth for the cream cheese segment.

By Source Insights

The cashew segment dominated the market by capturing 36.7% of the global market share in 2025. The growth of cashew segment in the global market is majorly attributed to the unique ability of cashews to create a smooth creamy texture that closely resembles traditional dairy cheese when blended. Cashews have a neutral flavor profile that allows for easy seasoning and customization making them ideal for a wide range of cheese styles, from cheddar to brie. According to the International Nut and Dried Fruit Council, global cashew production is estimated at 5.4 million metric tonnes for the 2023 to 2024 season. High income consumers in North America and Europe prefer cashew based cheeses for their premium quality and clean label attributes. The absence of strong beany or nutty aftertastes makes cashew cheese more palatable to mainstream audiences compared to soy or almond based alternatives. As per the United States Department of Agriculture, global cashew nut imports were valued at billions of dollars reflecting growing demand from the plant based food industry. Artisanal producers often highlight the use of whole cashews to emphasize quality and minimal processing. Retailers cater to this preference by dedicating shelf space to premium cashew cheese brands. The versatility of cashew base allows for innovation in aged and fermented varieties which command higher price points. This combination of sensory appeal and perceived value ensures that cashew remains the preferred source for high end vegan cheese products.

On the other end, the soy segment is experiencing the fastest growth within the vegan cheese market and is estimated to exhibit a CAGR of 10.5% over the forecast period owing to the cost effectiveness of soy protein and the well-established infrastructure for soy processing globally. Soy based cheeses offer a viable affordable alternative to nut based options, which is making them accessible to price sensitive consumers. According to the American Soybean Association, soybeans account for about 90% of US oilseed production ensuring consistent supply and stable pricing. Advances in texturization technology have significantly improved the mouthfeel and meltability of soy cheese, addressing previous sensory concerns. In Asia Pacific, where soy is a dietary staple, consumer acceptance of soy based products is naturally high. As per the Food and Agriculture Organization of the United Nations, global soybean production reached 372 million tonnes in 2023 to 2024, providing a robust raw material base for manufacturers. Large food corporations are leveraging their existing soy processing facilities to produce vegan cheese at scale, reducing entry barriers. The neutral taste of soy protein allows for effective flavor masking and enhancement. Regulatory approvals for soy ingredients are widespread, facilitating easier market entry in various regions. This economic advantage combined with technological improvements positions soy as a key driver of mass market adoption for vegan cheese.

By End Use Insights

The B2C segment dominated the market by holding the highest share of 63.1% of the global market in 2025 due to the widespread availability of vegan cheese in supermarkets, hypermarkets, and online retail platforms, which is making it easily accessible to individual consumers. The rise in home cooking and health consciousness has prompted households to stock plant based alternatives for daily consumption. According to NielsenIQ, retail sales of plant based meat alternatives grew by 15% in late 2024, indicating strong consumer demand. Direct to consumer channels allow brands to engage directly with shoppers through educational content and subscription models, fostering loyalty. The proliferation of e commerce has expanded reach beyond urban centers, enabling rural consumers to access specialized products. As per the United States Census Bureau, retail e commerce sales reached $289.2 billion in the fourth quarter of 2023, providing a convenient avenue for purchasing perishable goods with improved cold chain logistics. Retailers promote vegan cheese through prominent shelf placement and promotional campaigns increasing visibility. Consumer willingness to experiment with new flavors and brands in a retail setting drives volume sales. The personal nature of dietary choices means that individual purchasing decisions dominate the market landscape. This direct engagement allows for immediate feedback and product iteration strengthening brand consumer relationships.

However, the B2B segment is predicted to expand at a CAGR of 13.3% over the forecast period in the global market owing to the increasing incorporation of vegan cheese into restaurant menus, fast food chains, and institutional catering services. Food service providers are responding to consumer demand for plant based options by partnering with suppliers to source high quality vegan cheese. According to the National Restaurant Association, 40% of operators say adding plant based items is a top trend to attract diverse customer bases. Quick service restaurants are launching vegan burgers and pizzas featuring specialized melting cheeses that drives bulk procurement. As per the World Tourism Organization, international tourist arrivals reached 88% of pre pandemic levels in 2023, which has accelerated the adoption of inclusive menu options. Institutional buyers, such as schools and hospitals, are also integrating vegan cheese to accommodate dietary restrictions and promote health. Bulk purchasing agreements provide stability for manufacturers and encourage investment in large scale production capabilities. The standardization of vegan cheese in commercial kitchens ensures consistent quality and performance. This sector benefits from long term contracts and predictable demand patterns. The visibility of vegan cheese in popular dining establishments further normalizes its consumption among the general public.

REGIONAL ANALYSIS

North America Vegan Cheese Market Analysis

North America led the vegan cheese market globally in 2025 with 36.9% of the global market share. The high consumer awareness and a well-developed retail infrastructure for plant based products are majorly driving the dominance of North America in the global vegan cheese market. The United States is the primary driver with a strong culture of dietary experimentation and health consciousness. According to the Plant Based Foods Association, retail sales of plant based foods in the US reached $8.1 billion in 2023 reflecting sustained consumer interest. Canada also contributes significantly with supportive government policies promoting sustainable agriculture. The presence of major vegan cheese brands and innovative startups fosters a competitive landscape. Retailers, such as Whole Foods and Trader Joe’s, dedicate extensive shelf space to vegan options enhancing accessibility. The trend towards flexitarianism is widespread with many consumers reducing dairy intake for health reasons. Regulatory clarity regarding labeling supports market transparency. Investment in food technology hubs in Silicon Valley and other regions drives innovation in fermentation and protein alternatives. The mature market focuses on product improvement and premiumization. Consumer education campaigns by non-profits and industry groups further boost adoption. This robust ecosystem ensures North America remains the central engine of global market growth.

Europe Vegan Cheese Market Analysis

Europe accounted for a promising share of the global vegan cheese market in 2025. The European region is driven by stringent environmental regulations and strong animal welfare sentiments among consumers. Countries such as Germany, the United Kingdom, and France are leading adopters of plant based diets. As per the European Commission, the Farm to Fork Strategy aims to reduce the environmental impact of food systems encouraging shifts towards plant based consumption. Traditional dairy industries are adapting by launching their own vegan lines. Retailers across Europe have expanded their free from sections catering to lactose intolerant and vegan shoppers. The prevalence of vegan festivals and cultural events promotes awareness and trial. Regulatory frameworks regarding novel foods are strict but provide a clear pathway for innovation. Consumer preference for organic and non GMO ingredients influences product formulation. The diversity of culinary traditions in Europe leads to varied cheese preferences requiring localized product strategies. Sustainability certifications play a crucial role in purchasing decisions. This combination of regulatory support and cultural acceptance ensures steady market expansion.

Asia Pacific Vegan Cheese Market Analysis

Asia Pacific is anticipated to record the fastest CAGR in the global vegan cheese market during the forecast period owing to the urbanization, and increasing health awareness. China, India, and Japan are key markets with large populations adopting modern lifestyles. As per the Food and Agriculture Organization of the United Nations, global agricultural production must increase by 60% by 2050, prompting governments to explore alternative protein sources. Traditional plant based diets in countries like India provide a foundational acceptance of non dairy foods. However, the concept of vegan cheese is newer and gaining traction among urban millennials. International brands are entering the market through partnerships with local distributors. E commerce platforms facilitate access to niche products in vast geographic areas. Cultural preferences for tofu and soy based products offer a natural entry point for soy based vegan cheeses. Government initiatives to improve food security and sustainability support market development. Challenges include price sensitivity and limited cold chain infrastructure in rural areas. Despite these hurdles the sheer size of the population offers immense potential. The market is expected to grow rapidly as awareness spreads and affordability improves.

Latin America Vegan Cheese Market Analysis

Latin America is predicted to account for a notable share of the global vegan cheese market during the forecast period due to the rich agricultural base and growing interest in health and wellness. Brazil and Mexico are the largest markets driven by expanding middle classes and urbanization. As per the Inter American Institute for Cooperation on Agriculture, the region accounts for 13% of global food production providing abundant raw materials. Local entrepreneurs are launching artisanal vegan cheese brands using indigenous ingredients. Economic volatility affects purchasing power but demand for healthy options persists among affluent segments. Retail expansion in major cities improves availability of specialized products. Cultural appreciation for cheese in cuisines such as Mexican and Argentinean creates opportunities for localized vegan alternatives. Social media influences dietary trends among younger demographics. Regulatory frameworks are evolving to support food safety and labeling. Challenges include infrastructure limitations and competition from low cost dairy products. However the trend towards sustainability and ethical consumption is gaining momentum. The market offers long term growth potential as economic conditions stabilize and awareness increases.

Middle East and Africa Vegan Cheese Market Analysis

The Middle East and Africa is expected to showcase steady growth in the global vegan cheese market throughout the forecast period owing to the religious dietary laws such as Halal, which align with plant based principles, and rising health consciousness in Gulf countries. The United Arab Emirates and South Africa are key markets with sophisticated retail sectors. As per the World Bank, urbanization in Sub Saharan Africa is occurring at a rate of 4% annually leading to changes in dietary habits and greater exposure to global food trends. Tourism and hospitality sectors in Dubai and Cape Town drive demand for diverse menu options including vegan cheese. Local production is limited but imports are growing. Religious observances such as Ramadan see increased demand for plant based meals. Economic disparities limit mass market adoption but niche segments are expanding. Government initiatives to enhance food security encourage exploration of alternative proteins. Challenges include high import costs and limited local manufacturing. However the young demographic profile and increasing internet penetration support market education. The region offers strategic opportunities for brands targeting premium and ethical consumer segments.

COMPETITIVE LANDSCAPE

The competition in the Vegan Cheese Market is intense and characterized by a mix of established dairy corporations entering the space and agile specialized startups. Large food conglomerates leverage their extensive distribution networks and financial resources to launch private label and branded vegan options. They compete on price and availability aiming to capture mass market share through mainstream retail channels. Independent brands differentiate themselves through artisanal quality unique flavor profiles and strong ethical branding. These niche players often command premium prices by appealing to discerning consumers seeking authenticity and clean labels. Innovation in ingredient technology such as precision fermentation serves as a key battleground for achieving superior melt and stretch. Regulatory challenges regarding labeling terms create a complex environment where brands must navigate varying legal frameworks. Consumer education remains critical as companies strive to overcome perceptions of inferior taste or texture. Collaborations with chefs and influencers help validate product quality and drive trial. The market sees frequent product launches and reformulations as brands seek to match dairy performance. This dynamic landscape requires continuous adaptation and strategic investment to maintain competitiveness and drive growth in the evolving plant based sector.

KEY MARKET PLAYERS

Some of the notable companies in the global vegan cheese market are

- Violife Foods

- Daiya Foods

- Tyne Chease Limited

- Vtopian Artisan Cheese Company

- Kite Hill

- Miyoko’s Kitchen Company

- Vermont Farmstead Company

- Good Planet Foods

- Follow Your Heart

- Galaxy Nutritional Foods, Inc.

Top Players in the Market

- Miyoko’s Creamery is a pioneering brand in the vegan cheese sector renowned for its artisanal approach and commitment to traditional cheesemaking techniques. The company utilizes cashew milk and microbial cultures to create complex aged cheeses that appeal to gourmet consumers. Recent actions include expanding distribution into major retail chains across North America and Europe to increase accessibility. Miyoko’s has also invested in sustainable packaging initiatives using recyclable materials to align with environmental values. The brand actively engages in educational campaigns to promote plant based lifestyles and ethical consumption. By focusing on high quality ingredients and authentic flavors Miyoko’s strengthens its position as a premium leader. Its innovation in fermented nut based cheeses sets industry standards for texture and taste. This strategic focus on craftsmanship and sustainability ensures long term loyalty among discerning customers who prioritize both flavor and ethics in their dietary choices.

- Violife Foods is a global leader in the vegan cheese market known for its wide range of dairy free alternatives that melt and stretch effectively. The company leverages coconut oil and starch blends to create products that mimic the functionality of traditional cheese. Recent actions involve launching new varieties such as smoked provolone and feta blocks to diversify its portfolio. Violife has expanded its presence in international markets through strategic partnerships with distributors in Asia and Latin America. The brand emphasizes affordability and accessibility making vegan cheese available to a broader audience. Violife invests heavily in marketing campaigns featuring chefs and influencers to demonstrate culinary versatility. Its commitment to being free from lactose soy gluten and nuts appeals to consumers with multiple dietary restrictions. This inclusive approach strengthens its market position by catering to diverse health needs. Continuous product innovation and global expansion efforts ensure Violife remains a dominant force in the competitive plant based cheese landscape.

- Follow Your Heart is a prominent player in the vegan cheese market recognized for its pioneering Vegenaise and extensive line of plant based cheeses. The company focuses on creating clean label products using simple and recognizable ingredients. Recent actions include upgrading manufacturing facilities to increase production capacity and meet growing demand. Follow Your Heart has introduced new shredded and sliced options targeting the convenient meal preparation segment. The brand actively participates in trade shows and community events to build direct connections with consumers. Its commitment to sustainability is evident in solar powered operations and waste reduction programs. Follow Your Heart strengthens its market position by maintaining strong relationships with natural food retailers and mainstream grocery chains. The company’s emphasis on transparency and quality resonates with health conscious shoppers. By continuously refining recipes and expanding product lines Follow Your Heart ensures relevance in a dynamic market. Its legacy and innovation drive sustained growth and consumer trust in the evolving vegan cheese industry.

Top Strategies Used by the Key Market Participants

Key players in the Vegan Cheese Market primarily focus on product innovation by utilizing fermentation technology to enhance texture and flavor profiles. Companies invest heavily in expanding distribution networks to secure shelf space in mainstream retail outlets globally. Strategic partnerships with food service providers enable integration into restaurant menus and institutional catering services. Brands leverage digital marketing and social media engagement to educate consumers and build community loyalty. Sustainability initiatives including eco friendly packaging and carbon neutral commitments differentiate brands in a crowded marketplace. Acquisitions of smaller artisanal brands allow larger corporations to diversify portfolios and access niche segments. Pricing strategies aim to balance premium positioning with affordability to attract wider demographics. These strategies collectively enable participants to overcome sensory barriers and drive mass adoption of plant based cheese alternatives.

MARKET SEGMENTATION

This research report on the global vegan cheese market has been segmented and sub-segmented based on Product, Source, End-Use & region.

By Product

- Mozzarella

- Cheddar

- Parmesan

- Ricotta

- Cream Cheese

By Source

- Cashew

- Soy

By End Use

- B2C

- B2B

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa