Global Plant-based Protein Market Size, Share, Trends & Growth Forecast Report By Type (Isolates, Concentrates, Protein Flour), Application (Protein Beverages, Dairy Alternatives, Meat Alternatives, Protein Bars, Processed Meat, Poultry & Seafood and Bakery Products), Source (Soy, Pea, Wheat and Others), And Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis (2026 to 2034)

Global Plant-Based Protein Market Summary

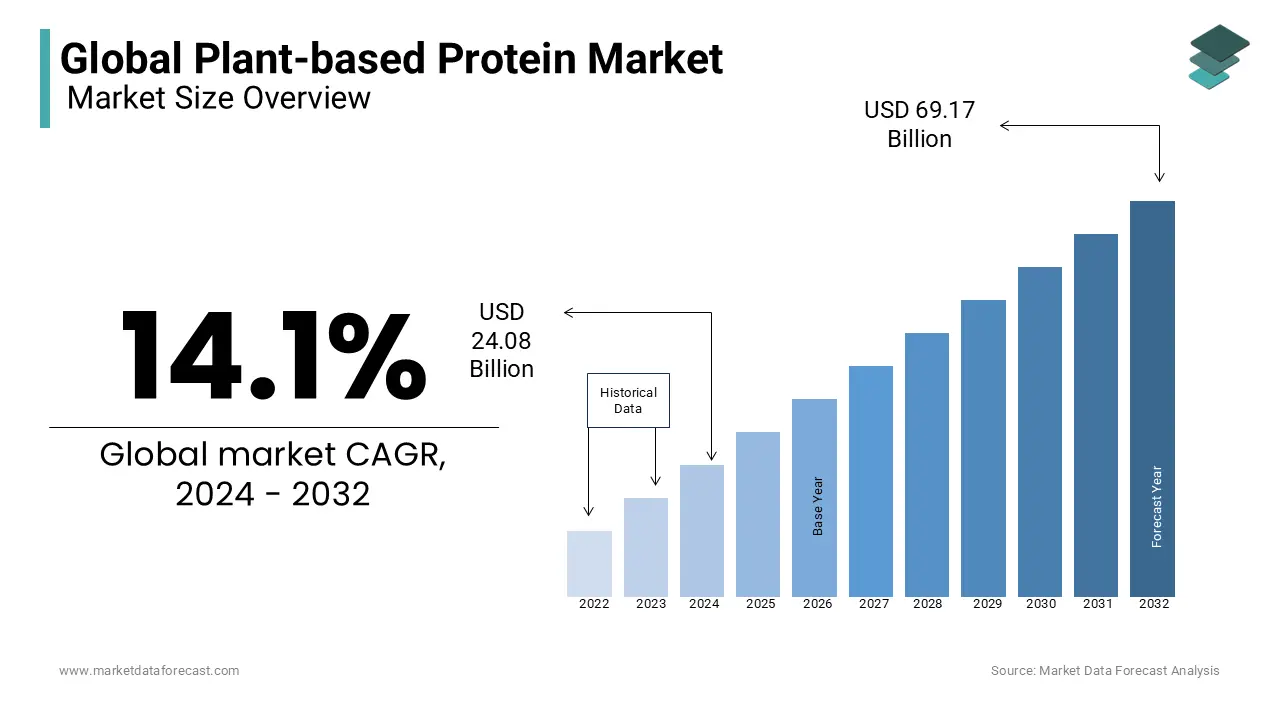

The global plant-based protein market size was valued at USD 27.48 billion in 2025. The global market size is estimated to grow at a CAGR of about 14.1% from 2026 to 2034 and be worth USD 90.06 billion by 2034 from USD 31.35 billion in 2026. The growth of the global plant-based protein market is driven by rising consumer adoption of vegan and flexitarian diets, increasing demand for sustainable and clean-label protein alternatives, and growing innovation in plant-based meat and dairy substitutes. Expanding applications across food, beverages, sports nutrition, and functional products are further accelerating market growth.

Key Market Trends

- Rising adoption of plant-based meat alternatives among flexitarian consumers.

- Increasing demand for protein isolates with high nutritional value and purity.

- Growing use of soy protein as a widely available and cost-effective source.

- Expansion of functional foods, beverages, and sports nutrition categories.

- Strong focus on sustainability and environmentally friendly food production.

Segmental Insights

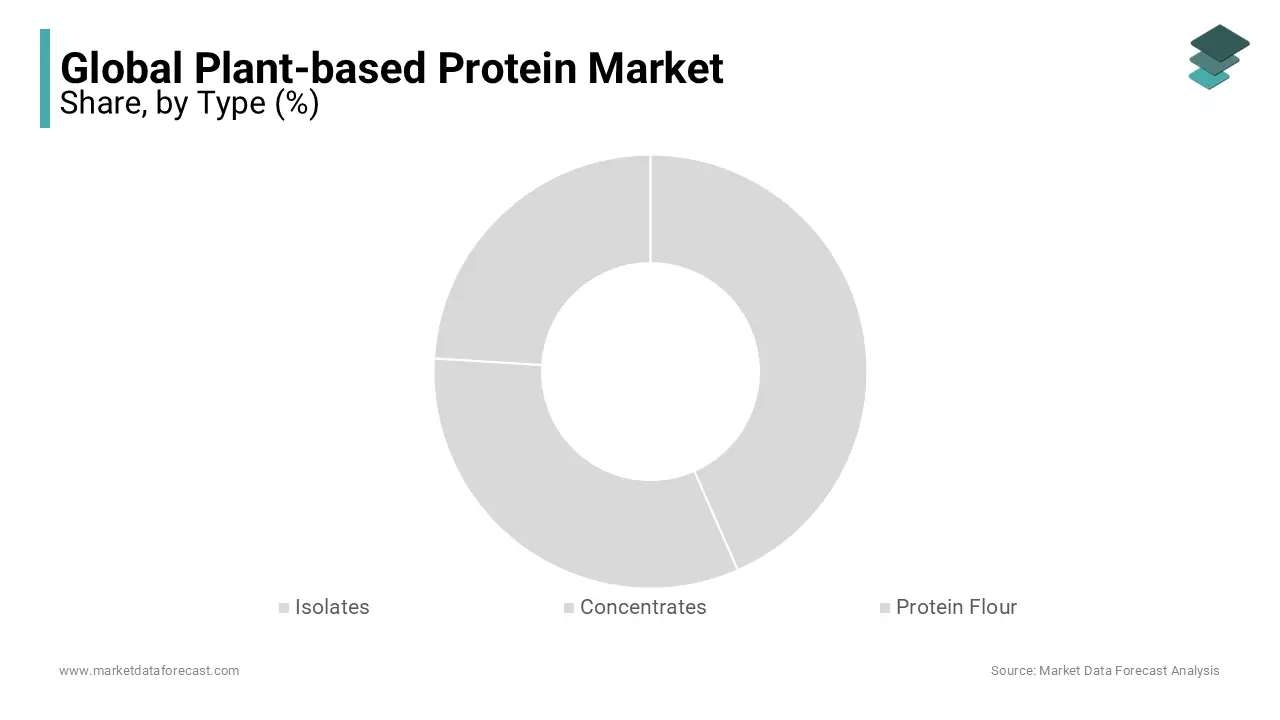

- Based on type, the plant-based protein isolates segment held the largest share of the global market at 46.3% in 2025, reflecting strong demand for high-protein, functional ingredients.

- Based on application, the meat alternatives segment represented the leading category in 2025, capturing 34.5% of the market, supported by rising global demand for plant-based meat substitutes.

- Based on the source, the soy protein segment dominated in 2025 with 48.8% share, owing to its affordability, availability, and versatility in food applications.

Regional Insights

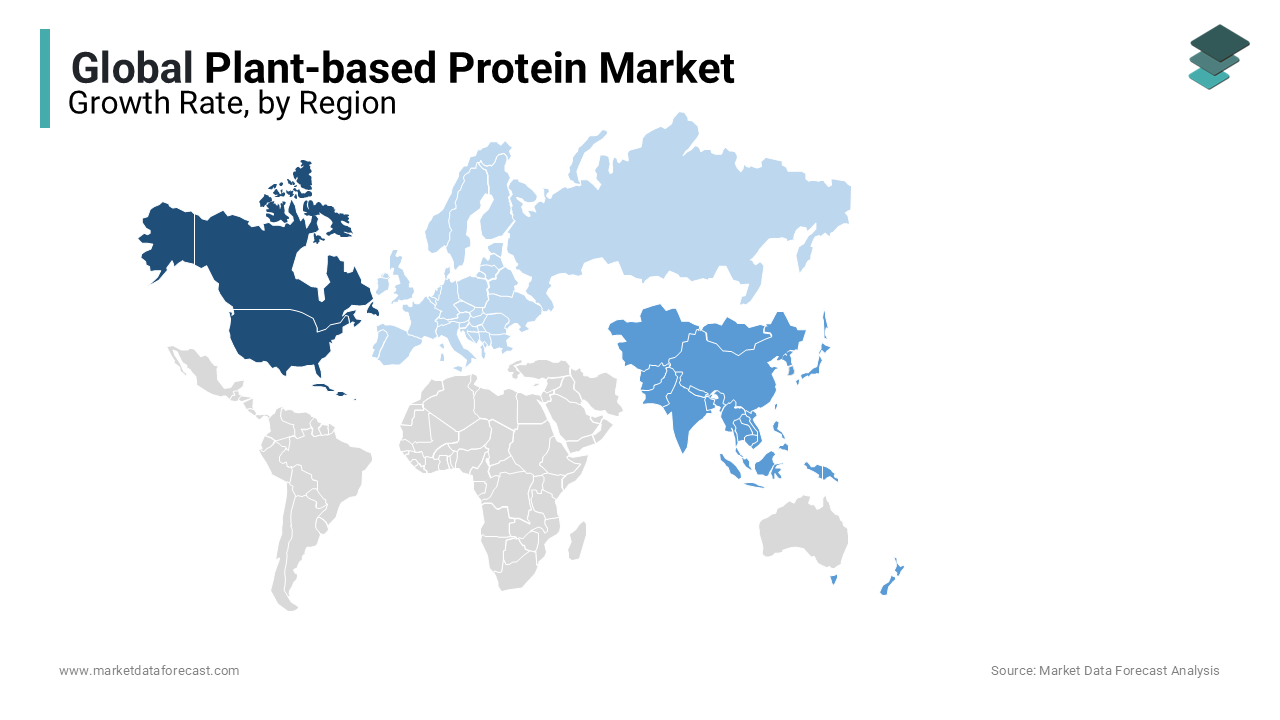

- North America led the global plant-based protein market in 2025, accounting for 38.3% share, driven by a strong consumer shift toward vegan and flexitarian diets, robust product innovation, and widespread retail availability.

- Europe is witnessing steady growth, supported by regulatory backing for sustainable diets and increasing adoption of plant-based foods.

- Asia-Pacific is projected to grow at the fastest CAGR, fueled by rising middle-class incomes, changing dietary habits, and growing health awareness.

- Latin America and the Middle East & Africa are emerging markets, supported by increasing investments in plant-based food startups and growing consumer demand for alternative proteins.

Competitive Landscape

Key players in the global plant-based protein market include Cargill Inc., Archer Daniels Midland, DuPont, Kerry Group, Glanbia PLC, Tate & Lyle PLC, Ingredion Inc., Burcon NutraScience Corp., Axiom Foods, Royal DSM N.V., and Sotexpro S.A. These companies are focusing on new protein ingredient development, partnerships with food manufacturers, and sustainability initiatives to strengthen their global presence.

Global Plant-based Protein Market Size

The global plant-based protein market size was valued at USD 27.48 billion in 2025. The global market size is estimated to grow at a CAGR of about 14.1% from 2026 to 2034 and be worth USD 90.06 billion by 2034 from USD 31.35 billion in 2026.

Plant-based Protein is derived from non-animal sources—such as legumes, grains, seeds, and algae—engineered to deliver high-quality protein for human consumption. These proteins are increasingly formulated into meat analogs, dairy alternatives, protein powders, and fortified foods to meet evolving dietary preferences and sustainability imperatives. Unlike conventional animal-derived proteins, plant-based variants offer lower environmental footprints and align with ethical and health-conscious consumer choices. Water usage is another critical concern. The integration of plant proteins into mainstream diets is further supported by advances in food technology, including extrusion and fermentation processes that improve texture and flavor. With increasing awareness of the environmental and health implications of animal agriculture, plant-based proteins are transitioning from niche offerings to essential components of future food systems.

MARKET DRIVERS

Growing Consumer Awareness of Health Benefits Associated with Plant-Based Diets

The rising consumer recognition of the health advantages linked to reduced animal protein intake and increased consumption of plant-derived nutrients is a pivotal driver of the plant-based protein market. Epidemiological studies consistently associate plant-forward diets with lower risks of cardiovascular disease, type 2 diabetes, and certain cancers. Furthermore, plant proteins such as lentils, chickpeas, and quinoa offer additional benefits, including high fiber content, phytonutrients, and lower saturated fat levels—factors increasingly prioritized by health-conscious consumers. The influence of digital wellness platforms and registered dietitians promoting plant-centric eating has amplified public trust. As clinical evidence continues to validate the long-term health benefits of plant-based nutrition, consumer behavior is shifting from trend-driven experimentation to sustained dietary transformation, fueling sustained demand for innovative and nutritionally complete plant protein products.

Urgent Need for Sustainable Food Systems Amid Climate Change Pressures

The escalating environmental cost of conventional animal agriculture is a compelling force accelerating the adoption of plant-based proteins as a sustainable alternative. Livestock farming occupies a notable share of global agricultural land while providing a smaller portion of the world’s calories. This inefficiency places immense strain on ecosystems, contributing to deforestation, biodiversity loss, and excessive water consumption. In contrast, producing one kilogram of pea protein generates fewer emissions than an equivalent amount of beef protein. Land use efficiency is equally striking—soy and pea cultivation require less land than cattle farming for the same protein yield. Water scarcity further underscores the urgency. Governments and multilateral institutions are responding. So, the scalability and ecological efficiency of plant-based proteins make them indispensable to building resilient, low-impact food systems.

MARKET RESTRAINTS

Sensory and Textural Limitations of Current Plant-Based Protein Products

Despite advancements, a significant restraint on the plant-based protein market remains the inability of many products to fully replicate the sensory experience of animal-derived meats and dairy. Consumers frequently cite issues such as rubbery textures, beany aftertastes, and inconsistent mouthfeel as reasons for discontinuing use. The structural complexity of animal muscle tissue—particularly its fibrous, juicy consistency—remains challenging to mimic using plant proteins alone. Soy, wheat, and pea isolates often require extensive processing, which can degrade nutritional quality and introduce off-flavors. Moreover, cooking behavior varies widely; many plant-based products fail to sear, sizzle, or bleed like real meat, diminishing their appeal in home and restaurant kitchens. Until food science achieves greater precision in structuring plant proteins at the molecular level, sensory deficiencies will continue to constrain mainstream adoption, especially among flexitarian and meat-centric consumers.

High Production Costs and Complex Supply Chain Dependencies

The economic viability of plant-based protein manufacturing is hindered by elevated production costs and fragile supply chains for key raw materials. While demand grows, the infrastructure for large-scale, cost-efficient processing of plant proteins remains underdeveloped compared to conventional animal agriculture. Isolating protein from crops like peas and fava beans requires energy-intensive wet fractionation and drying processes, increasing operational expenses. The cost of producing one kilogram of pea protein isolate is higher than that of whey protein on a per-gram amino acid basis. Additionally, reliance on a narrow range of crops creates supply vulnerabilities is making the market susceptible to climatic disruptions and export restrictions. Contract farming networks are limited, and processing facilities are concentrated, leading to bottlenecks. Smaller manufacturers struggle to secure consistent feedstock, while scaling production requires substantial capital investment in biorefineries. The lack of standardized agricultural support, such as subsidies or crop insurance for protein-rich legumes, further discourages farmer participation. Until supply chains become more diversified, resilient, and economically balanced, the affordability and scalability of plant-based proteins will remain constrained, limiting their competitiveness against conventional animal products.

MARKET OPPORTUNITIES

Expansion into Emerging Markets with Rising Middle-Class Consumption

A transformative opportunity for the plant-based protein market lies in penetrating emerging economies where urbanization, income growth, and health awareness are reshaping dietary habits. Countries across Southeast Asia, Latin America, and Africa are witnessing a burgeoning middle class with increasing disposable income and exposure to global wellness trends. Traditional diets in many of these regions are already plant-centric, providing a cultural foundation for product acceptance. In Indonesia, where tofu and tempeh have been dietary staples for centuries, modern plant-based brands are leveraging local flavors and formats to gain traction. Multinational companies are partnering with regional food manufacturers to develop affordable, shelf-stable products tailored to local palates. Hence, the strategic localization of plant-based protein offerings presents a profound opportunity to drive both commercial growth and public health improvement.

Innovation in Fermentation and Precision Biology for Next-Generation Proteins

Advancements in fermentation and precision biology are unlocking a new frontier in plant-based protein development, enabling the creation of high-performance ingredients with superior functionality and flavor. Precision fermentation—where microorganisms are engineered to produce specific proteins—allows for the synthesis of dairy-like casein or egg albumin without animal involvement. Companies like Perfect Day and Remilk are commercializing animal-free whey and casein for use in ice cream, cheese, and protein shakes, overcoming the texture limitations of traditional plant substitutes. Mycoprotein, derived from fungal fermentation, has gained renewed interest due to its fibrous structure and high digestibility—Quorn, a mycoprotein-based brand. Additionally, biomass fermentation using single-cell proteins from algae and bacteria offers scalable, climate-resilient protein sources. With CRISPR and synthetic biology accelerating strain optimization, fermentation is poised to revolutionize the sector by delivering proteins that are not only sustainable but indistinguishable from animal-derived counterparts in taste and performance.

MARKET CHALLENGES

Achieving Cost Parity with Animal-Based Proteins

Achieving price competitiveness with conventional meat and dairy products is one of the most persistent challenges in the plant-based protein market. Despite growing demand, plant-based alternatives often retail at a premium, deterring cost-sensitive consumers. This disparity stems from underdeveloped supply chains, low economies of scale, and high R&D expenditures. Animal agriculture benefits from decades of government subsidies, established infrastructure, and vertical integration—factors that plant-based producers are still building. Scaling production requires massive investment in processing facilities, yet private funding remains volatile. Retailers also contribute to the gap by placing plant-based products in specialty sections with lower turnover, increasing per-unit costs. Until production efficiencies and policy support close the cost gap, widespread adoption will remain limited to higher-income demographics.

Navigating Regulatory and Labeling Disputes Across Jurisdictions

The plant-based protein sector faces mounting regulatory scrutiny over product naming, labeling claims, and safety assessments, creating operational uncertainty and market access barriers. Several countries have enacted restrictions on terms like “milk,” “cheese,” and “burger” for plant-based products, arguing they mislead consumers. These inconsistencies complicate global branding strategies and increase compliance costs. Additionally, health claims are tightly regulated—only proteins meeting specific digestibility and amino acid profile thresholds can carry “complete protein” labels in regions like the EU. In emerging markets, unclear or absent regulations create both risks and opportunities. Without coherent international frameworks, companies must navigate a fragmented legal landscape, slowing innovation and market expansion.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 14.1% |

| Segments Covered | By Type, Application, Source, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Cargill Inc., Archer Daniels Midland, DuPont, Kerry Group, Glanbia PLC, Tate & Lyle PLC, Ingredion Inc., Burcon NutraScience Corp, Axiom Foods, Royal DSM N.V., And Sotexpro S.A. |

SEGMENTAL ANALYSIS

By Type Insights

The plant-based protein isolates segment held the largest share of the market with 46.3% in 2025. This dominance is primarily driven by their superior protein content and functional properties, making them ideal for use in high-performance food and beverage applications. Isolates typically contain more protein by weight, with minimal carbohydrates and fats, which aligns with the formulation needs of sports nutrition, clinical supplements, and clean-label products. Its solubility, emulsification, and gelling capabilities make it indispensable in ready-to-drink protein shakes and meat analogs, where texture and mouthfeel are paramount. Additionally, regulatory bodies such as the European Food Safety Authority have approved health claims linking soy protein isolate to reduced LDL cholesterol, further enhancing its appeal. The pharmaceutical and medical nutrition sectors also favor isolates for enteral feeding formulas, where consistent nutrient delivery is essential. With manufacturers investing in advanced extraction technologies like membrane filtration and isoelectric precipitation to improve purity and reduce off-flavors, isolates continue to set the benchmark for quality and efficacy in the plant-based protein landscape.

The protein flour segment is emerging as the fastest-growing type and is projected to expand at a CAGR of 15.8% from 2026 to 2034. This rapid growth is fueled by its cost-effectiveness, minimal processing, and compatibility with traditional food systems, particularly in developing economies. Unlike isolates and concentrates, protein flours retain fiber, vitamins, and phytonutrients, offering a whole-food profile that resonates with clean-label and organic consumers. Chickpea flour, for instance, contains protein along with iron and folate, making it a nutritionally dense ingredient. In India, besan (chickpea flour) is used in over 50 traditional dishes, providing a cultural entry point for fortified versions. The rise of gluten-free and allergen-conscious diets has further boosted demand—lentil and fava bean flours are naturally gluten-free and increasingly used in pasta and baked goods. Small-scale producers are leveraging this familiarity to launch fortified flours targeting malnutrition. As consumers shift toward minimally processed, sustainable ingredients, protein flours are gaining traction not only as functional additives but as foundational elements of future food systems.

By Application Insights

The meat alternatives segment represented the prominent application in the plant-based protein market by capturing 34.5% of the total share in 2025. This lead position is anchored in the global effort to reduce reliance on conventional livestock farming while satisfying consumer demand for familiar taste and texture. The environmental toll of animal agriculture is a key motivator. This stark contrast has prompted governments and institutions to promote meat substitutes; for example, public schools in cities like Los Angeles and Paris have integrated plant-based meals into their menus. Technological advancements have also improved product fidelity—Beyond Meat’s burger uses heme derived from genetically engineered yeast to replicate the sizzle and aroma of beef. Additionally, major fast-food chains have accelerated adoption;

Protein beverages are the fastest-growing application segment and are anticipated to grow at a CAGR of 16.3% between 2026 and 2034. This surge is driven by rising health consciousness, active lifestyles, and the demand for convenient, on-the-go nutrition. Ready-to-drink (RTD) protein beverages now dominate the functional drinks category, particularly among millennials and Gen Z consumers. Plant-based RTDs, including oat, pea, and almond protein shakes, are gaining ground due to their lower environmental impact and allergen-friendly profiles. Brands like Ripple and OWYN have reported triple-digit growth in retail distribution, driven by partnerships with major retailers and fitness centers. In Asia, protein-fortified soy milk is a staple in countries like Japan and China, where traditional consumption patterns provide a strong foundation for innovation. With e-commerce platforms enabling direct-to-consumer sales and personalized nutrition, protein beverages are evolving into a dynamic, high-margin segment with global scalability.

By Source Insights

The soy segment remained the dominant source in the plant-based protein market by holding a 48.8% share in 2025. Its growth is rooted in decades of agricultural infrastructure, high protein yield, and well-established processing techniques. Soybeans contain protein by dry weight, one of the highest among plant sources, and offer a complete amino acid profile, including leucine, which is critical for muscle synthesis. The crop is cultivated at scale. This abundance ensures a stable supply and relatively low input costs. Soy protein is also highly functional, exhibiting excellent water and fat binding, which is essential for meat analogs and dairy alternatives. Traditional diets in East Asia have long incorporated soy in forms like tofu, tempeh, and miso, creating deep consumer familiarity and acceptance. Additionally, regulatory bodies such as the U.S. Food and Drug Administration have authorized heart health claims for soy protein, citing its ability to reduce LDL cholesterol when consumed as part of a balanced diet. Despite concerns about allergenicity and genetic modification, non-GMO and fermented soy variants are gaining traction.

Pea protein is the fastest-growing source segment and is projected to expand at a CAGR of 17.2% from 2026 to 2034. This acceleration is driven by its hypoallergenic nature, sustainability profile, and favorable sensory characteristics compared to other legumes. Unlike soy and dairy, pea protein is not a major allergen, making it suitable for a broader consumer base, including infants and individuals with sensitivities. The European Commission recognizes pea as a low-risk allergen, facilitating its use in infant formula and clinical nutrition. Water usage is also significantly lower—producing one kilogram of pea protein requires less water than dairy protein. The functional properties of pea protein have improved dramatically due to advancements in wet fractionation and enzymatic treatment, enabling better solubility and reduced bitterness. Companies like Roquette and Burcon have developed proprietary processes to enhance flavor and texture, making peas ideal for meat and dairy analogs.

REGIONAL ANALYSIS

North America Plant-Based Protein Market Insights

North America led the global plant-based protein market by commanding 38.3% of the share in 2025. The region’s growth is underpinned by high consumer awareness, robust venture capital funding, and a mature ecosystem of food tech innovation. The United States, in particular, has become a hub for alternative protein startups. Regulatory support is growing, with the FDA modernizing labeling guidelines and the USDA investing in alternative protein research. Canada complements this momentum with strong agricultural capacity for pea and lentil production. The presence of major players like Maple Leaf Foods and Beyond Meat ensures continuous product innovation. With widespread distribution, cultural openness to dietary change, and institutional backing, North America remains the most advanced and influential market for plant-based proteins.

Europe Plant-Based Protein Market Insights

Europe holds a key share, which is driven by stringent environmental policies, strong consumer ethics, and government-led dietary transitions. Countries like Germany, the UK, and the Netherlands are at the forefront. Public institutions are accelerating adoption. The Netherlands funds research into precision fermentation through its National Institute for Public Health and the Environment. However, regulatory fragmentation persists—labeling laws vary across member states, complicating pan-European branding. Despite this, the convergence of climate urgency, health awareness, and technological innovation positions Europe as a critical driver of global market evolution.

Asia-Pacific Plant-Based Protein Market Insights

Asia-Pacific is witnessing rapid transformation due to urbanization, rising disposable incomes, and traditional plant-based diets. China has launched its policy in agriculture, aiming to cut meat consumption. The country is also investing heavily in alternative protein R&D. India’s Ayushman Bharat initiative includes nutrition security programs that incorporate fortified legume proteins to combat malnutrition. While Western-style meat analogs are still niche, traditional formats like tofu, tempeh, and seitan provide a strong foundation for innovation. With government support and deep-rooted vegetarian traditions, the Asia-Pacific is poised for exponential growth.

Latin America Plant-Based Protein Market Insights

Latin America holds a notable share of the global market, with Brazil and Mexico emerging as key growth engines. The region benefits from abundant agricultural resources and a growing health-conscious middle class. Brazil is the world’s largest exporter of soybeans, producing millions of metric tons annually. This domestic supply chain advantage enables cost-effective protein processing. Mexican consumers are increasingly adopting plant-based diets. Chile has implemented front-of-package warning labels on high-sugar and high-fat foods, indirectly promoting healthier protein choices. However, meat remains culturally central, and affordability is a barrier. Despite challenges, startups like Fazenda Futuro in Brazil are gaining traction with affordable meat analogs. With strong raw material access and evolving consumer habits, Latin America is gradually building a competitive plant-based ecosystem.

Middle East and Africa Plant-Based Protein Market Insights

The Middle East and Africa collectively represent a small share of the market, with significant disparities between subregions. Gulf countries like the UAE and Saudi Arabia are leading adoption, driven by food security concerns and economic diversification strategies. However, indigenous crops like cowpea, bambara groundnut, and moringa offer high-protein, climate-resilient alternatives. With strategic investments in the Gulf and untapped potential in traditional crops, the region is slowly emerging as a fragmented but promising frontier for plant-based innovation.

COMPETITION OVERVIEW

The competitive dynamics of the plant-based protein market are defined by a convergence of traditional agribusinesses, ingredient specialists, and disruptive food technology firms, all vying for influence across a rapidly evolving value chain. Incumbents leverage their scale, supply chain infrastructure, and R&D capabilities to dominate ingredient supply, while agile startups focus on niche innovations in texture, flavor, and bioengineering. Differentiation increasingly hinges on technological sophistication—particularly in protein structuring, fermentation, and sensory optimization—rather than mere product replication. Companies are investing in proprietary processing techniques to overcome longstanding challenges such as beany aftertastes, poor mouthfeel, and limited functionality in cooking applications. Brand positioning also plays a crucial role, with players emphasizing sustainability, clean labels, allergen-free formulations, and cultural relevance to capture diverse consumer segments. Geopolitical factors, including food security policies and agricultural subsidies, further shape regional competitiveness. Mergers, joint ventures, and pilot-scale biorefinery investments are common as firms seek to consolidate capabilities and accelerate time-to-market. As consumer expectations mature from novelty to performance, the battleground has shifted from availability to authenticity, scalability, and environmental integrity, making innovation and adaptability the defining traits of market leaders.

Key Market Participants

Companies playing a prominent role in the global plant-based protein market include

- Cargill Inc.

- Archer Daniels Midland

- DuPont

- Kerry Group

- Glanbia PLC

- Tate & Lyle PLC

- Ingredion Inc.

- Burcon NutraScience Corp

- Axiom Foods

- Royal DSM N.V.

- Sotexpro S.A.

Cargill, ADM, Kerry Group, DuPont Danisco, and Glanbia are the leading players in the global plant-based protein market. These companies implement strategies like expansions, mergers and acquisitions, and product launches. To gain a competitive edge in terms of revenue, organizations are investing more in innovative products with the aid of new plant proteins like hemp and chia. As of late, ADM (US) extended its geographic presence in Brazil with the development of another soy protein production complex in Campo Grande, MatoGrossodoSul, Brazil, at an estimated USD 250 million. The intricate details will make a scope of functional protein focus and will be included in ADM's present product offering.

Leading Players in the Global Market

ADM (Archer-Daniels-Midland Company) is a global leader in plant-based protein innovation, leveraging its vast agricultural network and deep expertise in ingredient science to deliver scalable, high-quality protein solutions. The company has invested heavily in advancing plant protein functionality, focusing on texture, flavor, and nutritional completeness for use in meat and dairy alternatives. ADM operates integrated biorefineries that extract and refine proteins from peas, soy, and other legumes, ensuring traceability and sustainability across the supply chain. Its collaboration with food manufacturers and startups enables customized formulations tailored to regional tastes and application needs. By integrating sustainability into its core operations and pioneering fermentation-based ingredients, ADM has positioned itself as a foundational enabler of the next-generation food ecosystem, bridging traditional agriculture with future-forward nutrition.

CHS Inc. plays a pivotal role in the plant-based protein market through its ownership of Supro®, one of the most recognized soy protein brands worldwide. With decades of experience in oilseed processing and ingredient development, CHS has established a reputation for producing functional, non-GMO, and allergen-friendly plant proteins. The company emphasizes clean-label solutions, supporting manufacturers in creating transparent, minimally processed products that meet evolving consumer expectations. CHS’s vertical integration—from crop sourcing to refined protein—ensures consistency and quality across applications ranging from beverages to meat analogs. Its research initiatives focus on improving solubility, reducing off-notes, and enhancing sustainability in protein extraction. Through strategic partnerships and a strong North American processing footprint, CHS continues to influence the formulation standards of plant-based foods on a global scale.

Roquette is a frontrunner in pea protein innovation, having pioneered large-scale production of NUTRALYS® pea protein, a benchmark ingredient in the alternative protein industry. The company’s commitment to sustainable agriculture and bioprocessing excellence has enabled it to supply major food brands with functional, hypoallergenic, and nutritionally balanced proteins. Roquette operates state-of-the-art facilities in Europe, North America, and Asia, allowing for global distribution and localized support. Beyond pea, the company is expanding into mycoprotein and fermentation-derived proteins, reinforcing its role as a technology-driven ingredient supplier. Its collaborations with biotech firms and food developers focus on improving sensory profiles and expanding application versatility. By combining agricultural stewardship with cutting-edge food science, Roquette has become a key architect in the evolution of plant-based and precision-fermented protein solutions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

- A primary strategy among leading players is vertical integration, encompassing control over the supply chain from crop cultivation to final ingredient production. Companies are securing long-term contracts with farmers, investing in processing infrastructure, and developing proprietary seed varieties to ensure consistent quality, traceability, and cost efficiency. This approach reduces dependency on third-party suppliers and enhances sustainability credentials.

- Another critical strategy is strategic collaboration with food tech startups, research institutions, and consumer brands to co-develop next-generation products. These partnerships enable rapid innovation in texture, flavor, and nutritional enhancement, particularly in mimicking animal-based foods more accurately and affordably.

- A third dominant approach is diversification into novel protein sources such as fermentation-derived proteins, mycoprotein, and cellular agriculture. By expanding beyond traditional soy and pea, companies are future-proofing their portfolios, addressing allergen concerns, and tapping into high-growth segments like precision biology, thereby establishing leadership in the emerging alternative protein landscape.

Global Plant-Based Protein Market News

- In March 2025, ADM launched an innovation center in Chicago dedicated to plant-based and fermentation-derived proteins, enabling faster co-development with food manufacturers and startups on texture and flavor optimization.

- In January 2025, Roquette inaugurated its expanded pea protein production facility in Canada, significantly increasing capacity and reinforcing its supply chain resilience for global food brands.

- In May 2023, CHS Inc. introduced a new line of non-GMO, solvent-free soy protein isolates under its Supro® brand, designed specifically for clean-label dairy alternatives and infant nutrition.

- In February 2025, Unilever partnered with a European biotech firm to develop animal-free dairy proteins using precision fermentation, aiming to launch in its plant-based ice cream and yogurt lines by 2026.

- In July 2023, Ingredion expanded its plant-based protein portfolio by acquiring a specialty starch technology firm, enhancing the binding and moisture retention properties of meat analogs.

MARKET SEGMENTATION

This research report on the global plant-based protein market has been segmented and sub-segmented based on type, application, source, and region.

By Type

- Isolates

- Concentrates

- Protein Flour

By Application

- Protein Beverages

- Dairy Alternatives

- Meat Alternatives

- Protein Bars

- Processed Meat

- Poultry & Seafood

- Bakery Product

By Source

- Soy

- Pea

- Wheat

- Others

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What factors are driving growth in the plant-based protein market?

Rising vegan and flexitarian populations, health awareness, sustainability concerns, and demand for alternative proteins are major growth drivers.

2. Which sources dominate the plant-based protein market?

Soy protein leads the market, followed by pea protein, wheat protein, rice protein, and other legume-based proteins.

3. How is health consciousness influencing demand?

Consumers prefer plant-based proteins due to benefits such as lower cholesterol, improved digestion, and reduced environmental impact.

4. What are the key applications of plant-based proteins?

Major applications include meat alternatives, dairy alternatives, sports nutrition, bakery products, snacks, and beverages.

5. What role does sustainability play in the market?

Plant-based proteins have a lower carbon footprint and require fewer natural resources compared to animal-based proteins, driving adoption.

6. Which distribution channels are important for plant-based protein products?

Supermarkets, health food stores, online retail platforms, and direct-to-consumer channels are key distribution routes.

7. What challenges does the plant-based protein market face?

Taste and texture issues, higher production costs, allergen concerns, and limited consumer awareness in some regions are key challenges.

8. How is innovation shaping the plant-based protein market?

Advancements in processing technologies, flavor masking, texturization, and blended protein formulations are driving innovation.

9. What role does clean-label demand play in this market?

Consumers increasingly prefer non-GMO, organic, allergen-free, and minimally processed plant-based protein products.

10. What is the future outlook for the plant-based protein market?

The market is expected to grow strongly, supported by expanding food applications, sustainability trends, and increasing investment in alternative proteins.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com