Asia Pacific Electric Water Heater Research Report By Product (Storage, Non-storage), Application, Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2026 to 2034

Asia Pacific Electric Water Heater Market Size

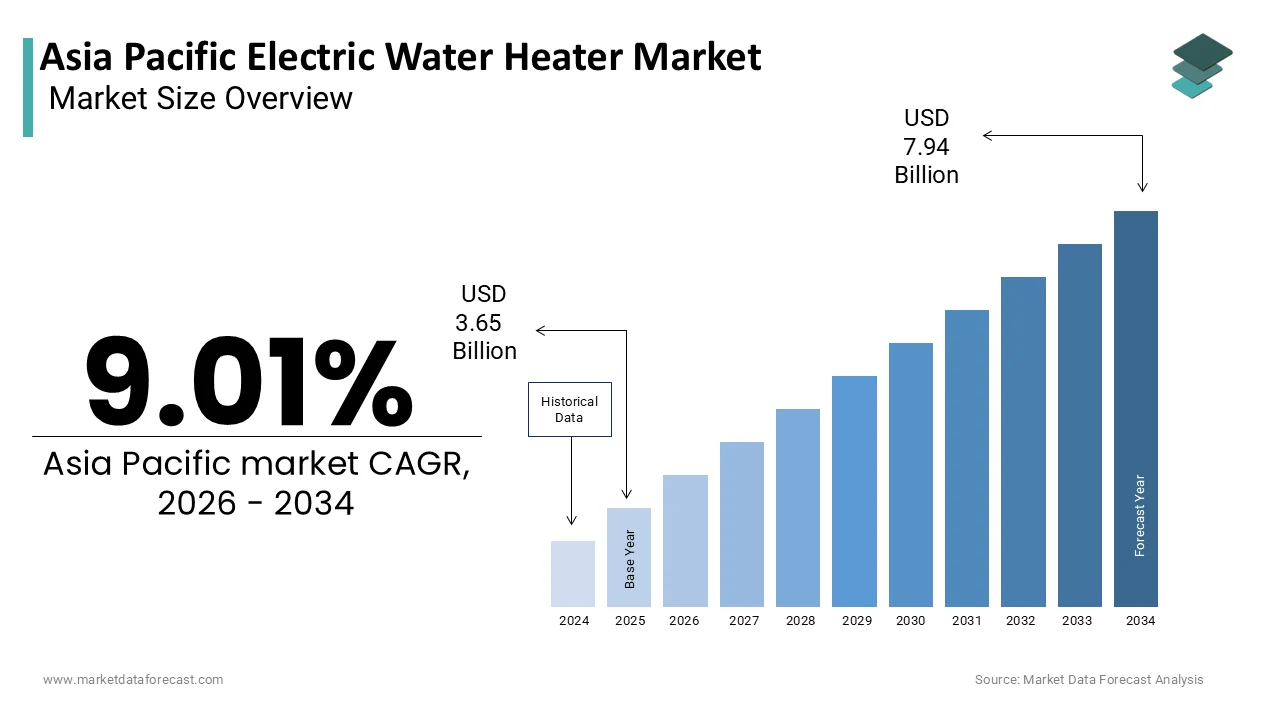

The Asia Pacific electric water heater market was valued at USD 3.65 billion in 2025, is estimated to reach USD 3.98 billion in 2026, and is projected to reach USD 7.94 billion by 2034, growing at a CAGR of 9.01% from 2026 to 2034.

An electric water heater is an electric-powered water heating system across residential, commercial, and institutional sectors. These systems are widely adopted in regions where access to natural gas is limited, and electricity is the primary energy source for domestic and commercial heating applications. The market includes a range of products such as storage tank models, instant (tankless) units, and heat pump-based electric water heaters, each catering to varying consumer needs and climatic conditions.

According to the International Energy Agency, electricity consumption in the Asia Pacific region reached record levels in 2023, with residential and commercial water heating contributing significantly to overall demand. In addition, in developed economies such as Australia and Japan, advanced electric models with smart controls and energy-saving features are gaining popularity.

Additionally, government policies promoting electrification and cleaner energy sources are shaping market dynamics. In India, the Ministry of Power has been expanding grid connectivity to rural areas, enhancing access to electric appliances. These developments highlight the growing importance of electric water heaters in the Asia Pacific region, positioning the market as a key component of the broader home appliance and energy sectors.

MARKET DRIVERS

Expansion of Electricity Access in Rural and Remote Areas

The expansion of electricity access in rural and remote areas, where gas infrastructure is either underdeveloped or entirely absent, is one of the primary drivers of the Asia Pacific electric water heater market. This expansion has been particularly notable in countries like India, Indonesia, and the Philippines, where government-led electrification programs have significantly increased grid connectivity.

The increased access has led to a surge in demand for electric household appliances, including water heaters. Similarly, in Indonesia, the state electricity company PLN has been expanding its rural electrification program, with over 90% of villages now having access to electricity, as per the Indonesian Ministry of Energy and Mineral Resources.

Moreover, in the Philippines, where natural gas pipelines are limited to major urban centers, electric water heaters remain the dominant choice in newly electrified regions. As rural electrification continues to progress, the electric water heater market is expected to grow steadily across the Asia Pacific region.

Rising Consumer Preference for Low-Maintenance and Easy-to-Install Water Heating Solutions

The growing consumer preference for low-maintenance and easy-to-install water heating solutions, particularly in urban and semi-urban settings, is another significant driver of the Asia Pacific electric water heater market. Also, installation complexity and maintenance requirements play a crucial role in consumer decision-making, especially in densely populated cities where space and technical expertise are limited.

In countries like Australia and Japan, where apartment-based living is prevalent, compact electric water heaters are increasingly favored for their ease of installation and minimal space requirements.

Besides, in developing economies such as Vietnam and Thailand, where technical expertise for gas system installation is limited, electric water heaters offer a more straightforward alternative. As consumer preferences shift toward convenience and simplicity, the electric water heater market is poised for sustained growth across the Asia Pacific region.

MARKET RESTRAINTS

High Energy Costs and Operational Expenses

The high energy costs and operational expenses associated with electric water heating systems are one of the primary restraints affecting the Asia Pacific electric water heater market. Compared to gas-based alternatives, electric water heaters typically consume more electricity, leading to higher utility bills for consumers.

In countries like the Philippines and Indonesia, where electricity tariffs are among the highest in the region, consumers often find electric water heaters financially burdensome. This high cost discourages widespread adoption, particularly in middle-income households.

Moreover, in India, where electricity tariffs vary by state, many consumers opt for alternative heating solutions such as solar or LPG-based systems to reduce energy expenses. These financial considerations limit the market potential of electric water heaters in several Asia Pacific countries.

Limited Energy Efficiency of Conventional Electric Water Heaters

The relatively low energy efficiency of conventional electric water heaters compared to gas and heat pump-based alternatives is another significant restraint on the Asia Pacific electric water heater market. In countries like Australia and Japan, where energy efficiency regulations are stringent, consumers are increasingly shifting toward more efficient alternatives. The efficiency limitations are prompting consumers and businesses to explore alternative water heating solutions, thereby restraining the growth of conventional electric water heaters in the Asia Pacific market.

MARKET OPPORTUNITIES

Growing Adoption of Heat Pump Water Heaters in Residential and Commercial Applications

The growing adoption of heat pump water heaters in both residential and commercial applications is a major opportunity in the Asia Pacific electric water heater market. Unlike conventional electric water heaters, which generate heat directly through resistance, heat pump models extract ambient heat from the surrounding environment, significantly improving energy efficiency. As governments across the region continue to incentivize clean energy technologies, the heat pump segment is poised for sustained growth in the Asia Pacific electric water heater market.

Expansion of Smart and Connected Electric Water Heater Technologies

The increasing integration of smart and connected technologies into electric water heating systems is another significant opportunity in the Asia Pacific electric water heater market. With the rise of smart homes and IoT-enabled appliances, manufacturers are embedding features such as mobile connectivity, real-time energy monitoring, and automated temperature control into electric water heaters.

In Japan, leading manufacturers have introduced smart electric water heaters that allow users to monitor and control water temperature via smartphone applications.

Moreover, governments across the region are encouraging the adoption of smart energy systems to reduce overall consumption. In Singapore, the Smart Nation initiative has been promoting the use of smart water heating solutions in both residential and commercial buildings. These developments indicate that the integration of smart functionalities into electric water heaters presents a substantial growth opportunity for market players in the Asia Pacific region.

MARKET CHALLENGES

Intense Competition from Alternative Water Heating Technologies

The increasing competition from alternative water heating technologies, particularly gas, solar, and heat pump-based systems, is a major challenge facing the Asia Pacific electric water heater market. Governments across the region are promoting cleaner and more energy-efficient alternatives to reduce carbon emissions and lower energy costs. Like, in India, the Ministry of New and Renewable Energy has been offering subsidies for solar water heater installations, making them more cost-competitive than electric models for many consumers. This growing shift toward alternative technologies poses a formidable challenge to the electric water heater market across the Asia Pacific region.

Rapid Technological Obsolescence and Innovation Pressure

The Asia Pacific electric water heater market faces increasing pressure from rapid technological obsolescence, compelling manufacturers to continuously innovate to stay competitive. As consumer expectations and regulatory standards evolve, companies must invest heavily in research and development to introduce more efficient, smarter, and environmentally friendly products.

In Japan, where technological innovation is a key market driver, manufacturers such as Panasonic and Mitsubishi are constantly upgrading their product lines to incorporate AI-based optimization features and mobile connectivity.

This rapid technological evolution not only increases R&D costs but also shortens product lifespans, making it difficult for smaller players to keep up with market demands. As a result, the electric water heater industry in the Asia Pacific faces significant innovation-driven challenges.

SEGMENTAL ANALYSIS

By Product Insights

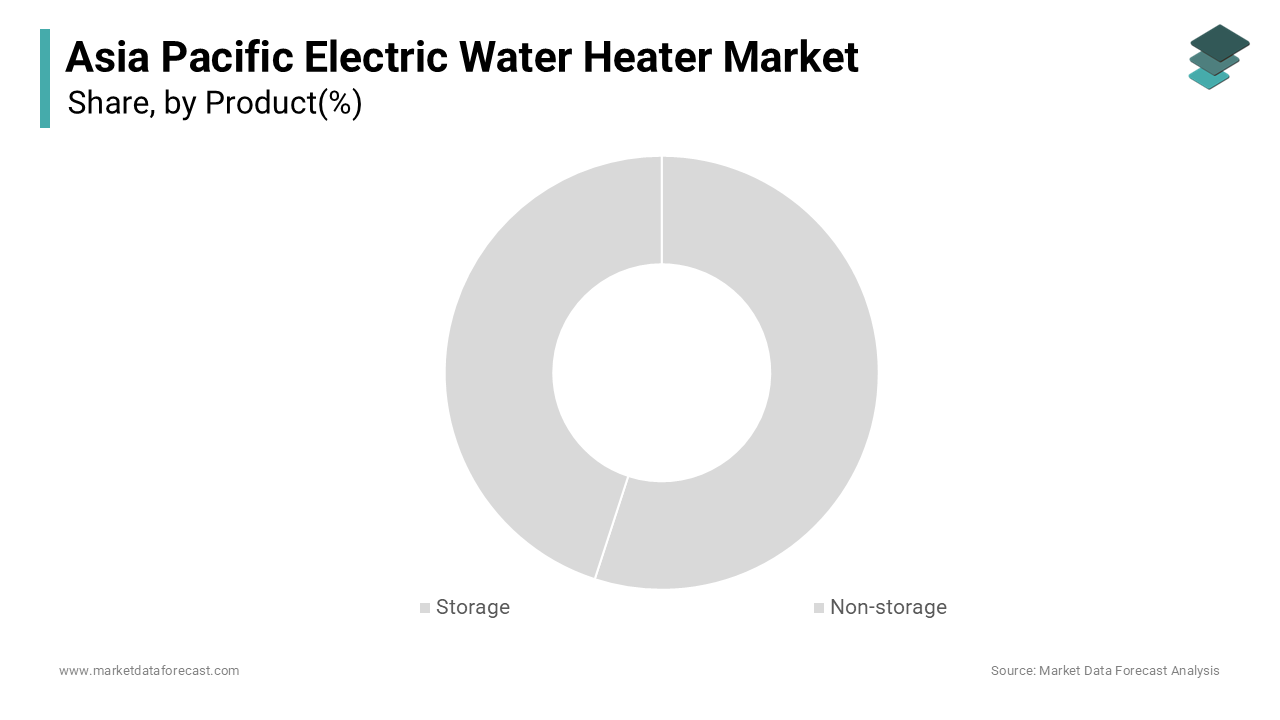

The storage electric water heater segment dominated the Asia Pacific electric water heater market by accounting for a 65.6% of total volume in 2025. The prominence of this segment is primarily attributed to the widespread use of storage models in both residential and commercial applications, particularly in countries where electricity is the primary energy source and an uninterrupted hot water supply is essential.

These models are preferred for their ability to store hot water, ensuring availability even during power outages or fluctuating electricity supply. The combination of infrastructure limitations, consumer familiarity, and reliability continues to solidify the storage segment’s leading position in the Asia Pacific electric water heater market.

The non-storage or tankless electric water heater segment is the fastest-growing within the Asia Pacific electric water heater market and is projected to expand at a CAGR of 9.8% from 2025 to 2033. The quick expansion of this segment is primarily driven by increasing consumer preference for energy-efficient and space-saving appliances, particularly in urban areas where compact living spaces and rising energy costs are key purchasing considerations. These models are especially popular in cities like Tokyo and Osaka, where high-density housing and limited installation space favor on-demand systems.

Moreover, technological advancements such as smart controls, digital ignition, and modulating heating elements have enhanced the appeal of tankless electric water heaters. As consumer awareness of energy efficiency and convenience continues to rise, the non-storage electric water heater segment is poised for sustained growth across the Asia Pacific region.

By Application Insights

The residential application segment commanded the Asia Pacific electric water heater market by accounting for a substantial portion of total volume in 2025. The dominance of this segment is primarily driven by the rising number of household formations, increasing disposable incomes, and expanding access to electricity in both urban and rural areas across the region. Additionally, rising consumer awareness regarding convenience and comfort has further boosted residential adoption. With continued urban expansion and growing middle-class populations, the residential segment remains the largest and most stable application area for electric water heaters in the Asia Pacific region.

The commercial application segment is the fastest-growing within the Asia Pacific electric water heater market and is projected to expand at a CAGR of 9.3% from 2025 to 2033. This growth is primarily driven by the rapid expansion of the hospitality, healthcare, and retail sectors across the region, where a continuous and high-volume hot water supply is essential.

Moreover, the rise of large-scale commercial complexes and integrated townships in Southeast Asia has further accelerated market growth. These factors collectively contribute to the rapid growth of the commercial application segment in the Asia Pacific electric water heater market.

REGIONAL ANALYSIS

India Electric Water Heater Market Insights

India spearheaded the Asia Pacific electric water heater market by accounting for a 26.4% of total regional demand in 2025. As the region’s second-largest population and a rapidly urbanizing economy, India has seen a surge in demand for electric water heaters, particularly in residential and small commercial applications. A key driver of market growth is the lack of widespread gas infrastructure outside major cities, making electric water heaters the preferred choice for most households. Additionally, rising disposable incomes and increased home construction under the Pradhan Mantri Awas Yojana (PMAY) have further fueled demand. Moreover, in the commercial sector, the expansion of hospitality and healthcare infrastructure has contributed to market growth. With continued electrification and rising consumer demand, India remains the largest market for electric water heaters in the Asia Pacific region.

China Electric Water Heater Market Insights

China is rapidly growing in the Asia Pacific electric water heater market. The country’s market is experiencing steady expansion due to increasing urbanization, rising disposable incomes, and government initiatives promoting electrification in residential and commercial sectors. A key driver of market growth is the rapid expansion of residential construction, particularly in southern and western provinces where gas infrastructure is less developed. Additionally, in urban centers like Shanghai and Guangzhou, apartment-based living has led to increased adoption of compact electric models. With continued investment in residential and commercial infrastructure, China remains a key growth market for electric water heaters in the Asia Pacific region.

Japan Electric Water Heater Market Insights

Japan secured a significant share of the Asia Pacific electric water heater market. The country has a well-developed residential and commercial infrastructure, with a significant portion of households and businesses relying on electric water heaters, particularly in high-rise buildings where gas venting is complex. One of the primary drivers of market growth is the widespread adoption of advanced electric water heating technologies, including heat pump and smart water heaters. Additionally, Japan’s aging population and rising healthcare demand have led to increased construction of elderly care facilities, all of which require reliable hot water systems. With continued emphasis on technological advancement and sustainability, Japan remains a key player in the Asia Pacific electric water heater market.

Australia Electric Water Heater Market Insights

Australia is another key player in the Asia Pacific electric water heater market. The country benefits from a strong regulatory framework that encourages the adoption of energy-efficient heating solutions, particularly in residential and commercial buildings. A key driver of market growth is the country’s preference for high-efficiency and low-emission water heating systems. Moreover, the hospitality sector remains a major consumer of electric water heaters. With continued policy support and a growing focus on reducing carbon emissions, Australia remains a significant contributor to the Asia Pacific electric water heater marke

South Korea Electric Water Heater Market Insights

South Korea is known for its advanced home appliance industry and high adoption of smart and energy-efficient technologies. A key growth driver is the integration of smart features into electric water heaters, including mobile connectivity, automated temperature control, and real-time energy monitoring. Additionally, government-led energy efficiency programs have encouraged the replacement of older models with high-efficiency units. Moreover, South Korea’s dense urban population and high-rise commercial infrastructure favor the installation of compact, high-performance water heating systems. As the country continues to emphasize technological innovation and sustainability, the electric water heater market is expected to maintain steady growth.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Asia Pacific Electric Water Heater Market include

- AO Smith Corporation

- Rheem Manufacturing Company

- Bradford White Corporation

- A.O. Smith (Asia)

- Haier Group

- Midea Group

- Rinnai Corporation

- Bosch Thermotechnology

- Panasonic Corporation

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Ariston Thermo Group

- Stiebel Eltron GmbH & Co. KG

- Royal Sunnan (Eurotec Group)

- Electrolux AB

- Hong Kong Company — GREE Electric Appliances Inc.

- Stand by Electric Water Heater Co.

- Arcelik A.S. (Beko brand)

- AO Smith India

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific electric water heater market is marked by a mix of global industry leaders and emerging regional players, all striving to capture market share through innovation, service excellence, and strategic positioning. The market is moderately concentrated, with a few dominant companies maintaining strong footholds due to their brand recognition, extensive product portfolios, and well-established distribution networks. However, the increasing demand for energy-efficient and smart-enabled electric water heaters is pushing both large and mid-sized players to invest heavily in research and development. Companies are also focusing on sustainability, after-sales service, and digital integration to differentiate themselves in a competitive landscape. As electrification and infrastructure development accelerate across the region, the competition is expected to intensify further, with new entrants and local manufacturers challenging the dominance of global players by offering cost-effective and region-specific solutions. This evolving dynamic is shaping a more diverse and competitive market environment.

Top Players in the Asia Pacific Electric Water Heater Market

A. O. Smith Corporation

A. O. Smith is a global leader in water heating technology and holds a dominant position in the Asia Pacific electric water heater market. The company is known for its innovation in high-efficiency electric and heat pump water heaters. With a strong presence in China and India, A. O. Smith has played a key role in introducing advanced electric water heating systems tailored to regional energy needs and infrastructure conditions.

Panasonic Corporation

Panasonic is a major player in the Asia Pacific region, particularly in Japan and Southeast Asia, where it has built a strong reputation for producing reliable, energy-efficient, and smart-enabled electric water heaters. The company’s integration of IoT and energy-saving technologies has positioned it as a preferred choice among consumers seeking convenience and sustainability.

Haier Smart Home Co., Ltd.

Haier is a leading Chinese manufacturer with a significant influence in the domestic and regional electric water heater market. The company combines local market insights with global technological expertise to offer a wide range of electric water heaters. Haier’s focus on product diversification and after-sales service has strengthened its market leadership in the Asia Pacific.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by leading players in the Asia Pacific electric water heater market is product innovation and technological advancement. Companies are continuously developing energy-efficient, smart-enabled, and compact models to meet evolving consumer preferences and regulatory requirements. These innovations help manufacturers differentiate their offerings and capture a larger market share.

Another critical strategy is strategic partnerships and collaborations. By aligning with local distributors, utility providers, and government agencies, companies can enhance their market penetration and streamline supply chain operations. These collaborations also support after-sales service networks, which are crucial for customer satisfaction and brand loyalty.

Lastly, expansion into emerging markets and localization of production play a vital role in strengthening market presence. Manufacturers are setting up regional manufacturing units and adapting product designs to suit local climatic conditions and consumer preferences, ensuring cost efficiency and faster delivery across the Asia Pacific region.

RECENT MARKET DEVELOPMENTS

- In February 2023, A. O. Smith launched a new line of high-efficiency electric heat pump water heaters tailored for residential use in China, targeting urban consumers seeking energy-saving and sustainable home solutions.

- In July 2023, Panasonic introduced a smart-enabled electric water heater with mobile connectivity and real-time energy monitoring features, specifically designed for the Japanese and South Korean markets to enhance user convenience and energy efficiency.

- In November 2023, Haier expanded its manufacturing facility in India to increase production capacity and better serve the growing demand for affordable and reliable electric water heaters in the region.

- In March 2025, Rinnai entered into a strategic distribution agreement with a leading local supplier in Indonesia to strengthen its presence in the rapidly growing residential electric water heater market.

- In August 2025, Bradford White Corporation launched a new series of compact electric water heaters designed for small living spaces, catering to the rising trend of urban apartment living across Southeast Asia.

MARKET SEGMENTATION

This research report on the Asia Pacific Electric Water Heater Market is segmented and sub-segmented into the following categories.

By Product

- Storage

- Non-storage

By Application

- Residential

- Commercial

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What are the major factors driving market growth?

Key drivers include urbanization, rising disposable incomes, energy efficiency awareness, increasing residential construction, and government support for sustainable appliances.

What challenges does the market face?

Challenges include high electricity consumption, price volatility of raw materials like copper and steel, rural electrification issues, and competition from gas and solar heaters.

What is the outlook for the Asia Pacific Electric Water Heater Market?

The market has a positive outlook, with growing opportunities in smart appliances, urban housing, and eco-friendly heating solutions.

Is the demand for electric water heaters rising in rural areas?

Yes, but growth is slower due to limited electricity access and preference for gas-based or solar water heaters in off-grid areas.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com