Asia Pacific Embedded Software Market Research Report – Segmented By Operating Systems (General Purpose Operating System (GPOS), Real-time Operating System (RTOS), Others), Functionality, Vertical, Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2025 to 2033

Asia Pacific Embedded Software Market Size

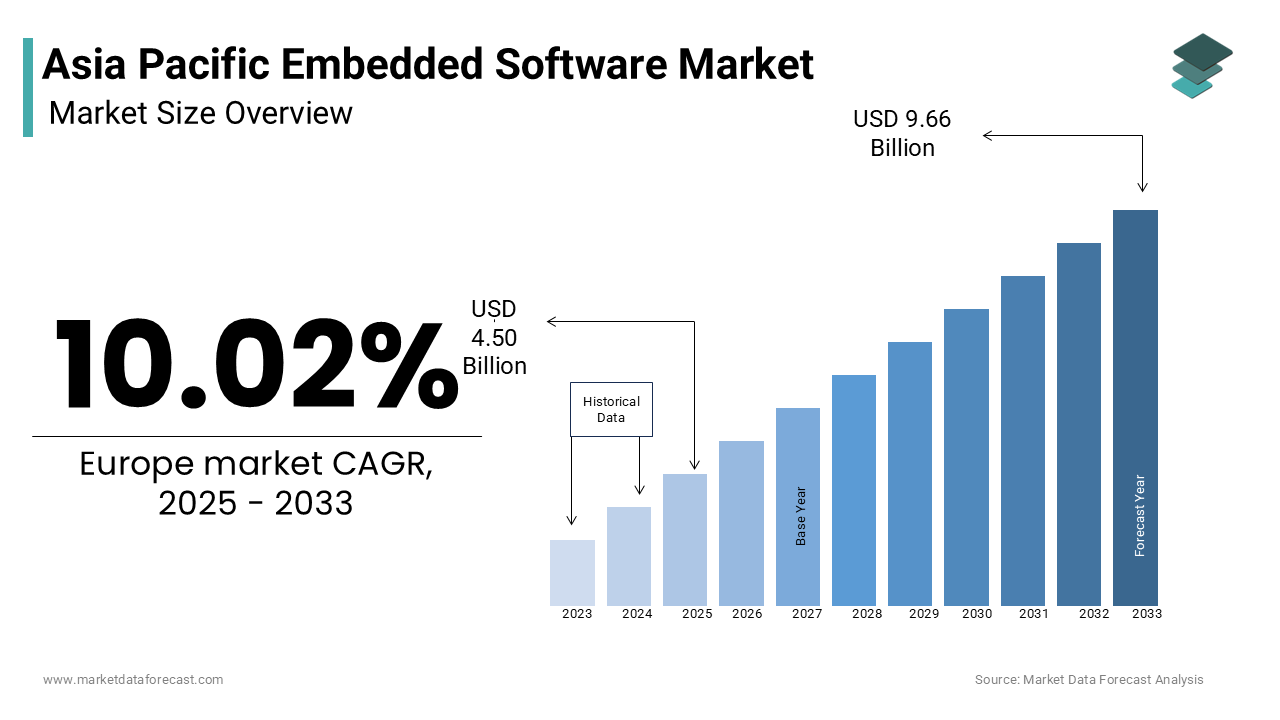

The Asia Pacific Embedded Software Market was worth USD 4.09 billion in 2024. The Asia Pacific market is expected to reach USD 9.66 billion by 2033 from USD 4.50 billion in 2025, rising at a CAGR of 10.02% from 2025 to 2033.

Embedded software refers to specialized programming integrated into hardware systems to perform dedicated functions, ensuring efficiency, reliability, and real-time operation. According to Deloitte, over 70% of electronic devices manufactured in the Asia Pacific rely on embedded systems, escalating their role in modern technology ecosystems. For instance, the proliferation of smart home devices in countries like South Korea and Japan has been driven by sophisticated embedded software that enables seamless connectivity and automation. Additionally, the rise of Industry 4.0 initiatives has accelerated the adoption of embedded solutions in manufacturing, with factories leveraging these systems for predictive maintenance and process optimization. As per PwC, the integration of artificial intelligence (AI) into embedded software has further expanded its capabilities, enabling smarter decision-making and enhanced user experiences.

MARKET DRIVERS

Rising Demand for Smart Devices

The exponential growth in demand for smart devices is a primary driver of the Asia Pacific embedded software market. The proliferation of Internet of Things (IoT) devices, such as wearable fitness trackers, smart home appliances, and connected vehicles, has created a robust need for advanced embedded software to manage complex functionalities. For example, companies like Samsung and Xiaomi are integrating embedded software into their products to enhance features such as voice recognition, energy efficiency, and real-time data processing. This trend is prominent in urban centers like Singapore and Seoul, where consumers prioritize convenience and automation. Additionally, the rise of smart city initiatives has further amplified demand for embedded solutions, as governments invest in intelligent infrastructure to improve traffic management, energy consumption, and public safety.

Adoption of Industry 4.0 Technologies

Another significant driver is the rapid adoption of Industry 4.0 technologies across manufacturing sectors in the Asia Pacific region. Embedded software plays a crucial role in enabling automation, data exchange, and real-time monitoring in smart factories. According to McKinsey & Company, over 60% of manufacturers in the region have implemented Industry 4.0 solutions, relying heavily on embedded systems to optimize production processes. For instance, automotive manufacturers in Japan and South Korea use embedded software to power advanced driver-assistance systems (ADAS) and autonomous driving technologies, ensuring precision and safety. Additionally, the integration of machine learning algorithms into embedded platforms has enabled predictive maintenance, reducing downtime and operational costs. A study by Accenture revealed that businesses adopting embedded software for industrial automation achieve a 25% increase in productivity.

MARKET RESTRAINTS

High Development Costs and Complexity

One of the most significant restraints facing the Asia Pacific embedded software market is the high cost and complexity associated with developing and maintaining these systems. Designing embedded software requires specialized expertise in hardware-software integration, real-time operating systems, and low-level programming languages, which can be prohibitively expensive for small and medium-sized enterprises (SMEs). According to Frost & Sullivan, the average cost of developing an embedded system exceeds $500,000, which is making it inaccessible for many startups and smaller organizations. Additionally, the shortage of skilled professionals exacerbates the issue, as companies often struggle to find engineers proficient in embedded technologies. For instance, a survey by KPMG revealed that over 70% of tech firms in Southeast Asia face challenges in recruiting qualified embedded software developers. These financial and resource constraints hinder widespread adoption, particularly in developing economies where regulatory enforcement is weak, and businesses prioritize immediate operational needs over long-term investments.

Fragmented Regulatory Frameworks

Another major restraint is the fragmented nature of regulatory frameworks governing embedded software across the Asia Pacific region. While countries like Japan and Australia have established robust standards for cybersecurity and data privacy, others lag in enacting comprehensive legislation. According to the Asia-Pacific Economic Cooperation (APEC), only 40% of member economies have implemented national cybersecurity strategies, which is leading to inconsistencies in compliance requirements. For example, India’s Information Technology Act does not adequately address vulnerabilities in embedded systems, while Indonesia’s data privacy framework remains underdeveloped. This lack of harmonization complicates cross-border operations for multinational corporations, forcing them to navigate multiple regulatory landscapes. Furthermore, differing standards for encryption protocols and data localization policies create additional barriers. As per Deloitte, multinational companies operating in the Asia Pacific spend an average of 15% more on compliance-related activities compared to other regions due to these disparities.

MARKET OPPORTUNITIES

Integration with Artificial Intelligence and Machine Learning

The integration of artificial intelligence (AI) and machine learning (ML) into embedded software presents a transformative opportunity for the Asia Pacific market. AI-driven embedded systems can analyze vast amounts of data in real time, enabling smarter decision-making and enhanced functionality. According to IBM, AI-powered embedded solutions can reduce operational inefficiencies by up to 30% by making them highly attractive to industries such as healthcare and automotive. For example, medical device manufacturers in Japan are leveraging AI-enabled embedded software to develop predictive diagnostics tools, improving patient outcomes and reducing healthcare costs. Similarly, automotive companies in South Korea are incorporating ML algorithms into embedded platforms to enhance autonomous driving capabilities by ensuring precision and safety.

Expansion into Emerging Markets

Another promising opportunity lies in expanding embedded software solutions into emerging markets within the Asia Pacific region. Countries like Vietnam, Thailand, and Indonesia are witnessing rapid industrialization and digital transformation, creating a fertile ground for embedded technologies. According to the World Bank, the middle-class population in Southeast Asia is projected to double by 2030, which is driving demand for affordable and scalable embedded solutions. For instance, local enterprises in these markets are increasingly adopting embedded software to enhance product functionalities, from smart agricultural equipment to energy-efficient home appliances. Additionally, partnerships with local governments and industry associations can facilitate awareness campaigns and capacity-building programs, fostering trust among stakeholders.

MARKET CHALLENGES

Shortage of Skilled Workforce

The scarcity of skilled professionals proficient in embedded software development poses a significant challenge to the Asia Pacific market. According to Cybersecurity Ventures, the global shortage of skilled IT professionals is expected to reach 3.5 million unfilled positions by 2025, with the Asia Pacific accounting for nearly 40% of this deficit. In countries like Malaysia and Thailand, universities produce fewer than 500 embedded software specialists annually, far below industry requirements. This shortage forces organizations to either outsource critical functions or operate with understaffed teams, which is increasing the risk of project delays and technical errors. Additionally, the rapid evolution of embedded technologies necessitates continuous upskilling, which many professionals struggle to achieve due to limited access to advanced training programs. For instance, a survey by EY revealed that only 25% of embedded software practitioners in the region receive regular training updates.

Lack of Awareness Among SMEs

Another pressing challenge is the lack of awareness about the benefits and applications of embedded software among small and medium-sized enterprises (SMEs) in the Asia Pacific. Many SMEs underestimate their potential to leverage embedded technologies, viewing them as complex and cost-prohibitive rather than as tools for enhancing competitiveness. According to Grant Thornton, over 60% of SMEs in the region do not integrate embedded solutions into their product development processes. This complacency stems from a limited understanding of potential risks and the perceived complexity of implementation. Furthermore, the absence of dedicated R&D departments in smaller organizations exacerbates the problem, as employees often lack the technical knowledge to identify and mitigate gaps. This lack of awareness not only hampers innovation but also undermines broader efforts to create a technologically advanced ecosystem, as excluded SMEs cannot contribute to or benefit from the digital economy.

REGIONAL ANALYSIS

China led the Asia Pacific embedded software market by accounting for 30.4% of the share in 2024 with a massive manufacturing base and technological advancements have creating a fertile ground for embedded software adoption. Enterprises in sectors like automotive, consumer electronics, and industrial automation rely heavily on embedded systems to enhance product functionality and operational efficiency. According to the National Bureau of Statistics of China, over 50% of electronic devices produced in the region incorporate embedded software, reflecting its widespread use.

Japan's embedded software market was positioned second by holding 18.4% of share in 2024 with its advanced technological infrastructure and emphasis on precision positioning it is a leader in adopting AI-driven embedded software solutions. Japanese corporations prioritize efficiency and innovation, particularly in industries like automotive and robotics. According to the Japan External Trade Organization, over 70% of large enterprises use embedded systems to power autonomous driving technologies and smart manufacturing processes. Additionally, the integration of machine learning algorithms into embedded platforms has gained traction, enabling predictive maintenance and real-time decision-making.

India’s booming IT sector and rapidly evolving startup ecosystem are major drivers of embedded software adoption. Indian enterprises are increasingly leveraging embedded solutions to enhance product functionalities, from smart agricultural equipment to energy-efficient home appliances. According to the Ministry of Electronics and Information Technology, over 60% of tech startups in India have integrated embedded software into their offerings, reflecting its growing importance. Additionally, government-led initiatives promoting IoT and smart city projects have further bolstered the market by ensuring steady growth.

South Korea's focus on innovation and digital transformation has driven the adoption of advanced embedded software solutions is likely to fuel the growth of the market. South Korean enterprises, particularly in the electronics and automotive sectors, rely on embedded systems to manage complex functionalities and ensure precision. Additionally, government initiatives promoting smart factories and Industry 4.0 technologies have accelerated the adoption of integrated digital tools by positioning South Korea as a key player in the regional market.

Australia’s strong emphasis on regulatory compliance and corporate governance has fueled demand for embedded software in industries like healthcare, mining, and telecommunications. Australian enterprises spend significant resources on developing embedded solutions to meet stringent safety and environmental standards. According to the Australian Securities and Investments Commission, over 30% of legal disputes arise from poorly managed embedded systems, incentivizing businesses to adopt automated solutions. Additionally, the rise of remote work has accelerated the adoption of cloud-based embedded platforms by ensuring accessibility and scalability.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

The key players in the Asia Pacific embedded software market include Intel Corporation, Microsoft Corporation, IBM Corporation, Texas Instruments Incorporated, Qualcomm Technologies Inc., NXP Semiconductors N.V., STMicroelectronics, Renesas Electronics Corporation, Samsung Electronics Co., Ltd., and Wind River Systems, Inc.

The Asia Pacific embedded software market is characterized by intense competition, driven by a mix of global giants and regional innovators striving to capture market share. Established players like Mitsubishi Electric, LG Electronics, and Samsung bring extensive resources and technological expertise, enabling them to dominate key segments such as IoT-enabled devices and smart manufacturing. At the same time, regional companies leverage their deep understanding of local cultures and regulatory frameworks to carve out niche positions. The market’s dynamic nature is further amplified by rapid technological advancements, which compel vendors to continuously innovate and adapt. Strategic collaborations with governments and industry bodies play a crucial role in shaping competitive strategies, particularly in emerging markets. Additionally, the rise of cloud computing and digital transformation initiatives has created new opportunities for differentiation, as companies strive to offer seamless and scalable solutions. This interplay of innovation, localization, and strategic positioning ensures that the market remains vibrant and highly contested.

Top Players in the Asia Pacific Embedded Software Market

Mitsubishi Electric Corporation

Mitsubishi Electric is a global leader in the embedded software market, renowned for its advanced solutions tailored to industries like automotive, manufacturing, and robotics. The company’s embedded systems integrate seamlessly with hardware to enable real-time processing, predictive maintenance, and energy-efficient operations. Mitsubishi Electric has strengthened its presence in the Asia Pacific by focusing on Industry 4.0 technologies, offering scalable solutions that cater to diverse industrial needs.

LG Electronics

LG Electronics is a prominent player in the embedded software market, leveraging its expertise in smart home devices, automotive systems, and consumer electronics. The company’s embedded solutions emphasize connectivity, automation, and user-centric design, enabling seamless integration across IoT ecosystems. LG has expanded its footprint in the Asia Pacific by collaborating with local tech firms to address unique regional challenges, such as energy efficiency and urbanization. Its focus on sustainability and cutting-edge research positions it as a key enabler of digital transformation globally.

Samsung Electronics

Samsung Electronics specializes in high-performance embedded software for applications ranging from smartphones to industrial automation. Its solutions are designed to deliver reliability, scalability, and real-time performance, making them ideal for mission-critical environments. Samsung has deepened its engagement in the Asia Pacific by investing in AI-driven embedded platforms and fostering collaborations with startups and academic institutions.

Top Strategies Used by Key Players in the Asia Pacific Embedded Software Market

Integration of AI and Machine Learning

Leading players are increasingly incorporating artificial intelligence (AI) and machine learning (ML) into their embedded software platforms to enhance functionality and adaptability. These technologies enable predictive analytics, real-time decision-making, and automation, addressing complex challenges in industries like healthcare and automotive. For instance, AI-driven embedded systems can optimize energy consumption in smart factories or improve diagnostics in medical devices. This strategy not only improves operational efficiency but also differentiates vendors in a competitive market.

Expansion Through Strategic Partnerships

Strategic partnerships with local enterprises, governments, and research institutions have become a cornerstone of success in the Asia Pacific embedded software market. Collaborations with public sector organizations help promote awareness campaigns and regulatory compliance initiatives, fostering trust among stakeholders. Additionally, partnerships with technology firms facilitate the integration of advanced tools by ensuring scalability and reliability. These alliances enable companies to expand their reach and influence across diverse markets.

Focus on Localization and Customization

Key players are prioritizing localization and customization to address the unique needs of businesses in the Asia Pacific region. By offering multilingual interfaces and region-specific features, vendors can cater to diverse consumer preferences. This approach not only enhances user experience but also fosters brand loyalty. Additionally, customization allows companies to adapt their solutions to specific industries, such as manufacturing and healthcare by ensuring relevance and applicability in diverse operational contexts.

RECENT MARKET DEVELOPMENTS

- In April 2024, Mitsubishi Electric launched a new AI-powered embedded platform tailored to address the growing demand for smart factory solutions in Southeast Asia. This initiative aims to enhance its market presence by offering region-specific solutions that align with local industrial needs.

- In June 2023, LG Electronics partnered with a leading telecommunications provider in South Korea to integrate its embedded software into IoT-enabled home appliances. This collaboration seeks to streamline connectivity and automation, improving user experiences for end consumers.

- In September 2023, Samsung introduced a blockchain-enabled feature to ensure tamper-proof records for embedded systems used in financial applications across India. This move strengthens its dominance in ethical cybersecurity practices and addresses growing concerns about transparency.

- In February 2024, Mitsubishi Electric acquired a regional startup specializing in AI-driven predictive maintenance solutions. This acquisition allows Mitsubishi to expand its capabilities in industrial automation, catering to the evolving needs of manufacturers in the Asia Pacific region.

- In November 2023, LG collaborated with a government agency in Singapore to promote the adoption of embedded software tools among small and medium-sized enterprises (SMEs). This initiative aims to foster digital resilience and increase market penetration among underserved segments.

MARKET SEGMENTATION

This research report on the Asia Pacific Embedded Software Market is segmented and sub-segmented into the following categories.

By Operating System

- General Purpose Operating System (GPOS)

- Real-time Operating System (RTOS)

- Others

By Functionality

- Standalone Systems

- Real-Time Embedded Systems

- Mobile Embedded Systems

- Networked Embedded Systems

By Vertical

- Computing Devices

- Consumer Electronics

- Industrial Automation

- Automotive

- Manufacturing

- Telecommunications

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is driving the growth of the Asia Pacific embedded software market?

Growth in the Asia Pacific embedded software market is driven by increasing demand for smart consumer electronics, the expansion of the automotive sector, adoption of IoT devices, advancements in industrial automation, and the growth of 5G and telecommunications infrastructure.

What challenges does the Asia Pacific embedded software market face?

Major challenges include software complexity, increasing cybersecurity threats, integration with legacy systems, and a shortage of skilled embedded software developers.

What is the future outlook for the Asia Pacific embedded software market?

The future outlook is positive, with expectations of strong growth fueled by rising IoT adoption, smart city development, electric vehicle (EV) integration, and AI-enabled embedded applications across various industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com