Asia Pacific Frozen Pizza Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Type, Pizza Toopings, Pizza Size, And By Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From 2025 to 2033

Asia Pacific Frozen Pizza Market Size

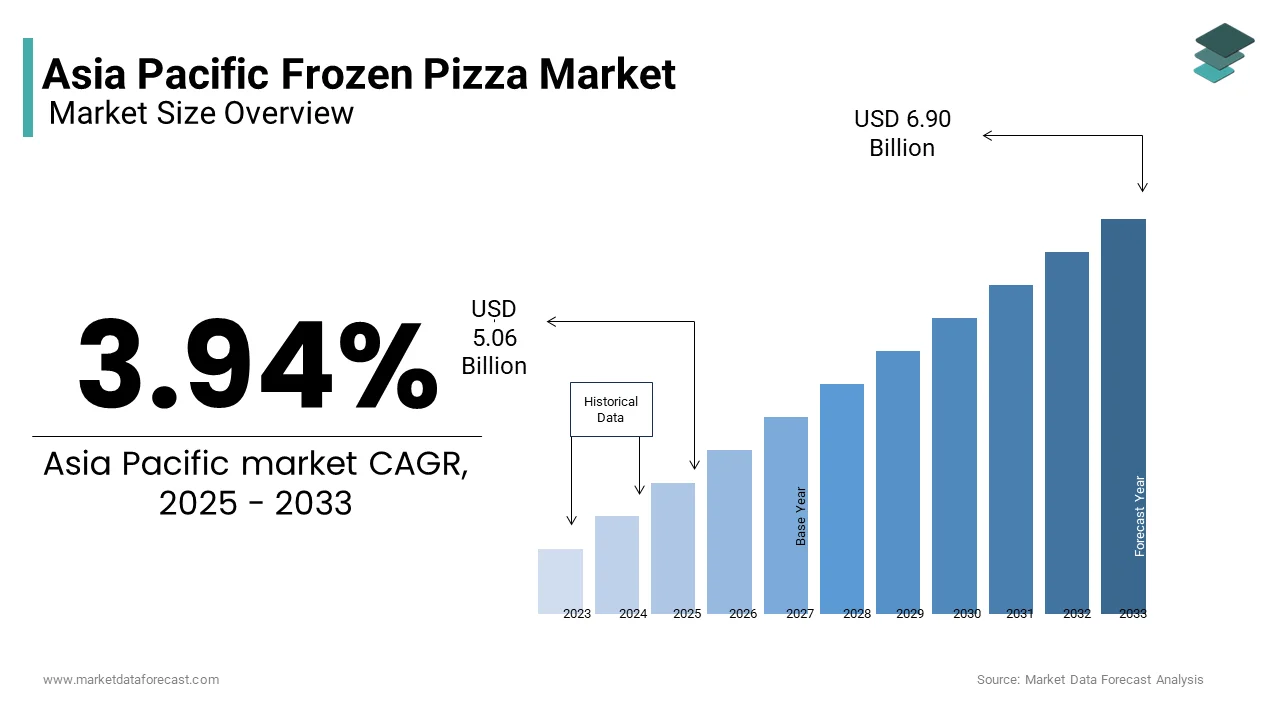

The Asia Pacific frozen pizza market size was valued at USD 4.87 billion in 2024 and is anticipated to reach USD 5.06 billion by 2025 from USD 6.90 billion by 2033, growing at a CAGR of 3.94% during the forecast period from 2025 to 2033.

MARKET DRIVERS

Rising Urbanization and Changing Lifestyles

Rising urbanization and evolving lifestyles are pivotal drivers propelling the Asia Pacific frozen pizza market forward, particularly among younger demographics. This shift is especially pronounced in countries like China and India, where rapid urbanization has led to busier lifestyles and a growing preference for quick, hassle-free meal options. Moreover, innovations such as localized flavors and healthier ingredient options have further boosted demand. These dynamics underscore how urbanization and lifestyle changes continue to fuel the dominance of frozen pizza in the region.

Growing Popularity of Western Cuisine

The growing popularity of Western cuisine serves as another major driver for the Asia Pacific frozen pizza market, which is driven by globalization and the influence of the media. This trend is particularly evident in countries like South Korea and Singapore, where exposure to global food trends through social media and streaming platforms has reshaped dining preferences. Besides, collaborations between food brands and celebrity chefs have further amplified this trend. Another significant factor is the rise of themed restaurants and food festivals, which have normalized pizza as a mainstream dish. These elements collectively position Western cuisine as a cornerstone of the frozen pizza market’s rapid expansion in the region.

MARKET RESTRAINT

Cultural Preference for Fresh Ingredients

Cultural preferences for fresh ingredients pose a significant restraint to the Asia Pacific frozen pizza market, particularly in rural and traditional communities. This resistance stems from deeply rooted culinary traditions that emphasize the use of fresh, locally sourced ingredients. Also, limited awareness about the nutritional value and convenience of frozen pizzas further stifles adoption in underdeveloped areas. For instance, traditional beliefs associating frozen foods with lower quality deter regular consumption, particularly among older generations. Additionally, the lack of refrigeration infrastructure in remote regions restricts product availability, further limiting market penetration. Without targeted educational campaigns and affordable pricing strategies tailored to rural demographics, the market risks alienating a significant segment of the population.

Fluctuating Raw Material Costs

Fluctuating raw material costs present another critical restraint hampering the Asia Pacific frozen pizza market, impacting production timelines and profitability. The reliance on key ingredients like cheese, wheat, and tomato paste makes the industry vulnerable to price volatility, especially in regions prone to supply chain disruptions. According to the Food and Agriculture Organization (FAO), global cheese prices surged significantly in 2022 due to geopolitical tensions and export restrictions, directly affecting frozen pizza manufacturers. These inconsistencies translate into higher retail prices, deterring price-sensitive consumers in emerging markets. Additionally, import tariffs and trade barriers further complicate the cross-border movement of raw materials, resulting in financial losses for exporters. For instance, stringent quality certifications required by countries like Japan and South Korea delay shipments, exacerbating operational inefficiencies.

MARKET OPPORTUNITY

The expansion into emerging markets offers a lucrative opportunity for the Asia Pacific frozen pizza market, driven by untapped consumer bases and evolving purchasing power. Countries like Vietnam, Indonesia, and the Philippines present fertile ground for growth, with their expanding middle-class populations increasingly gravitating toward convenient and Western-inspired food options. Also, the average annual income in these nations has risen over the past five years, enabling greater discretionary spending on processed food products, including frozen pizza. Companies investing in localized distribution networks stand to capture significant market share, particularly through partnerships with small retailers and cooperatives. Moreover, government initiatives promoting agribusiness in Southeast Asia have facilitated the establishment of new cold storage facilities, ensuring a steady supply of high-quality raw materials. For instance, Vietnam’s recent focus on modernizing its food processing sector has led to an increase in frozen pizza production over the past three years.

Innovation in product offerings represents a transformative opportunity for the Asia Pacific frozen pizza market, enabling brands to differentiate themselves and attract diverse consumer segments. As consumer preferences evolve, there is a growing appetite for value-added variants such as organic, plant-based, and specialty frozen pizzas tailored to specific dietary needs. This trend has spurred companies to experiment with formulations like gluten-free and vegan pizzas, catering to niche markets seeking specialized nutrition. Moreover, the introduction of eco-friendly packaging, such as biodegradable cartons and reusable containers, has resonated strongly with environmentally conscious buyers, boosting brand loyalty in urban areas. Innovations in processing techniques, such as flash freezing, have also enhanced product quality, preserving natural flavors while extending shelf life. For instance, a report by the Australian Institute of Food Science and Technology notes that flash-frozen pizzas retain more nutrients compared to conventionally processed variants, appealing to health enthusiasts. This focus on innovation not only diversifies product portfolios but also positions the Asia Pacific region as a hub for next-generation frozen food solutions.

MARKET CHALLENGES

Intense market competition poses a significant challenge to the Asia Pacific frozen pizza market, as numerous players vie for dominance in an increasingly saturated landscape. The entry of multinational corporations alongside local brands has fragmented the market, leading to aggressive pricing wars and eroding profit margins. This proliferation forces smaller players to either consolidate or exit the market, as they struggle to match the marketing budgets and distribution networks of larger conglomerates. Brand differentiation has become increasingly difficult, with consumers often prioritizing cost over loyalty.

Supply chain disruptions pose a significant challenge to the Asia Pacific frozen pizza market, impacting production timelines and distribution efficiency. The reliance on imported raw materials like cheese and tomato paste makes the industry vulnerable to logistical bottlenecks, especially in regions prone to extreme weather events and geopolitical tensions. According to the Asian Development Bank, typhoons and monsoon floods caused a notable reduction in cold chain logistics capacity in Southeast Asia during 2021, leading to shortages and increased operational costs. These disruptions are exacerbated by inadequate infrastructure in rural farming areas, where transportation networks often struggle to meet the demands of large-scale production. For instance, stringent quality certifications required by countries like Japan and South Korea delay shipments, resulting in financial losses for exporters. A report by the Food and Agriculture Organization notes that nearly 20% of frozen pizzas produced in the region fail to reach international markets due to compliance issues. Such inefficiencies not only inflate operational expenses but also limit market penetration in high-demand areas. While investments in cold chain logistics and warehousing are underway, progress remains uneven, particularly in less-developed economies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.94% |

| Segments Covered | By Size, Distribution, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the rest of APAC. |

| Market Leaders Profiled | Hansen Foods, Inc., Freiberger Lebensmittel GmbH Co., Atkins Nutritionals, Inc., Daiya Food Inc., NC, Nestlé SA, Oetker GmbH, McCain Foods Ltd, California Pizza Kitchen, One Planet Pizza, and Bellisio Foods Inc |

SEGMENT ANALYSIS

By Size Insights

The regular size segment was at the forefront of the Asia Pacific frozen pizza market, with a 50.6% of the total share in 2024. This growth is driven by its affordability and versatility, making it a popular choice for single-person households and small families. A key factor fueling this dominance is the growing trend of solo dining and smaller household sizes in urban areas. Another factor is the rise of convenience stores, which stock regular-sized pizzas due to their compact packaging and ease of storage.

The large size segment is predicted to advance at a CAGR of 8.55, emerging as the fastest-growing category in the Asia Pacific frozen pizza market. This quick progress is fueled by the increasing prevalence of family gatherings and social dining occasions. Among the crucial drivers of this growth is the growing preference for shared meals among larger households. As per the Asian Development Bank, multi-generational households are common in countries like China and Vietnam, driving demand for larger portion sizes that cater to group consumption. An additional important factor is the influence of promotional offers, such as bundled deals and discounts, which make large-sized pizzas more attractive to budget-conscious buyers. A notable share of consumers in urban areas prefer purchasing large pizzas during festive seasons, further boosting seasonal demand.

By Distribution Channel Insights

The offline sales segment dominated the Asia Pacific frozen pizza market by holding a 60% share in 2024. This leading position is underpinned by the widespread presence of brick-and-mortar retailers, including supermarkets, hypermarkets, and convenience stores, which remain the primary touchpoints for most consumers. A critical aspect driving this dominance is the trust and reliability associated with offline purchases. In addition, the strong distribution networks of established brands ensure extensive shelf space in urban centers like Jakarta and Manila. For instance, offline sales of frozen pizzas grew in 2022, driven by strategic partnerships with modern retail chains. A different contributing point is the influence of promotional activities, such as discounts and loyalty programs, which enhance customer retention.

The segment of online sales is the fastest-growing distribution channel in the Asia Pacific frozen pizza market, with a projected CAGR of 12.8%. This rapid rise is fueled by the increasing penetration of e-commerce platforms and the growing preference for convenience among urban consumers. A primary driver of this surge is the rise of digital literacy and internet access. Moreover, the integration of AI-driven recommendations and personalized marketing campaigns has amplified consumer engagement, driving an increase in online sales since 2020. Another significant factor is the influence of social media influencers and wellness experts, who promote frozen pizzas through targeted advertisements and reviews.

COUNTRY ANALYSIS

Top Leading Countries In The Market

China Frozen Pizza Market Analysis

China holds the largest revenue share in the Asia Pacific frozen pizza market, i.e., 28.8% in 2024. The country's vast population and rising disposable incomes make it a natural hub for consumption. A key driving factor is the government's push for modernizing food processing industries, with initiatives encouraging the adoption of Western dietary habits. Urbanization has also spurred demand, particularly in cities like Shanghai and Beijing, where frozen pizzas are increasingly viewed as a convenient meal option.

India Frozen Pizza Market Analysis

India is a significant and rapidly growing region in this market. The country's youthful population and growing exposure to global cuisines drive demand for frozen pizzas, particularly in metropolitan cities. According to the Confederation of Indian Industry, frozen pizza sales in urban areas like Mumbai and Delhi have surged significantly annually since 2020, fueled by dual-income households and the influence of Western culture. Additionally, the rise of e-commerce platforms has amplified accessibility, with online sales growing notably in 2022.

Japan Frozen Pizza Market Analysis

Japan plays a major role in this market and is benefiting from its aging population's reliance on convenience foods. Frozen pizzas have become a staple due to their ease of preparation and variety, with urban areas seeing annual growth in demand. Government initiatives promoting sustainable agriculture have further expanded availability, enhancing market penetration.

Australia Frozen Pizza Market Analysis

Australia is experiencing a positive CAGR and holds a significant position in the market, with its emphasis on fitness and wellness positioning frozen pizzas as essential for quick meals. According to the Australian Institute of Health and Welfare, 50% of adults regularly consume frozen pizzas, with healthier variants like whole wheat and vegetable-loaded options gaining popularity.

South Korea Frozen Pizza Market Analysis

South Korea is expected to continue expanding. It is driven by its tech-savvy population and booming e-commerce sector. Urban centers like Seoul witness an annual growth in online frozen pizza sales, fueled by influencer-driven campaigns and subscription models.

COMPETITIVE LANDSCAPE

The Asia Pacific frozen pizza market is characterized by intense competition, with numerous players vying for dominance in an increasingly saturated landscape. Established global brands like Nestlé and Dr. Oetker compete alongside regional leaders such as Schwan's Company, each striving to differentiate itself through unique value propositions. While multinational corporations leverage their extensive distribution networks and marketing budgets to capture urban markets, local players focus on affordability and cultural relevance to appeal to broader demographics. The entry of private-label products from major retailers further intensifies the rivalry, pressuring branded manufacturers to innovate continuously. Sustainability and health consciousness have emerged as key battlegrounds, with companies investing in eco-friendly packaging and clean-label formulations to gain a competitive edge. Additionally, the rise of e-commerce has leveled the playing field, enabling smaller brands to challenge incumbents by reaching consumers directly.

KEY MARKET PLAYERS

Major key Players in the Asia Pacific frozen pizza market are

- Hansen Foods, Inc

- Freiberger Lebensmittel Gmbh Co

- Atkins Nutritionals, Inc

- Nestlé (Through its brand DiGiorno)

- Daiya Foods Inc

- Schwan's Company (Through its brand Freschetta)

- Nestlé SA

- Oetker GmbH

- McCain Foods Ltd

- California Pizza Kitchen

- One Planet Pizza

- Bellisio Foods Inc

Top Players In the Market

- Nestlé, through its DiGiorno brand, is a dominant player in the Asia Pacific frozen pizza market, known for its high-quality ingredients and innovative product offerings. The company has significantly contributed to the global market by introducing premium frozen pizzas tailored to local tastes, such as those featuring Asian-inspired toppings. Its commitment to sustainability and ethical sourcing practices has strengthened its reputation, making it a trusted choice among environmentally conscious consumers. Nestlé’s strategic partnerships with major retailers and e-commerce platforms have further strengthened its presence in urban markets across the region.

- Dr. Oetker, through its Ristorante brand, has carved a niche in the Asia Pacific market by focusing on gourmet frozen pizzas that appeal to health-conscious and premium buyers. The company’s emphasis on clean-label ingredients and authentic Italian flavors resonates with consumers seeking high-quality meal options. By aligning with local distributors and promoting sustainable packaging, Dr. Oetker has fostered trust and loyalty among its customer base. Its contributions to the global market include pioneering innovative freezing techniques, which have set new standards for freshness and taste in the industry.

- Schwan's Company, through its Freschetta brand, is a regional leader that leverages its deep understanding of consumer preferences to tailor its frozen pizza offerings. The company’s strong distribution network and collaborations with supermarkets and convenience stores have enabled it to penetrate both urban and rural markets effectively. Freschetta’s efforts to promote healthier variants, such as whole wheat and vegetable-loaded pizzas, have expanded its appeal beyond traditional consumers to health enthusiasts.

Top Strategies Used by Key Players In The Market

Localized Product Offerings

Key players in the Asia Pacific frozen pizza market are increasingly focusing on localized product offerings to cater to diverse consumer preferences. By incorporating region-specific flavors and ingredients, companies are able to resonate with local tastes and cultural preferences. This strategy not only enhances brand acceptance but also strengthens their competitive edge in a crowded marketplace. Collaborations with local chefs and culinary experts further amplify the authenticity of these offerings, driving consumer engagement and loyalty.

Sustainability Initiatives

Sustainability has become a cornerstone of market strategies, with companies emphasizing eco-friendly practices to appeal to environmentally conscious buyers. From adopting recyclable packaging to promoting sustainable sourcing of raw materials, key players are investing in initiatives that reduce their environmental footprint. These efforts not only align with global trends toward green consumption but also position brands as responsible corporate citizens. Partnerships with environmental organizations further reinforce their commitment to sustainability, enhancing brand equity and fostering long-term relationships with consumers.

Digital Marketing and E-commerce Expansion

To strengthen their position, leading companies are leveraging digital marketing and expanding their e-commerce presence. Social media campaigns, influencer collaborations, and targeted advertisements are being used to reach tech-savvy consumers, particularly in urban areas. Simultaneously, investments in online platforms and subscription models ensure seamless accessibility and convenience.

RECENT MARKET NEWS

- In April 2023, Nestlé launched a series of frozen pizzas featuring Asian-inspired toppings, such as teriyaki chicken and spicy kimchi. This move was aimed at appealing to local taste preferences and expanding its product portfolio in urban markets.

- In June 2023, Dr. Oetker partnered with local organic farms in Thailand to source fresh ingredients sustainably. This initiative reinforced the company’s commitment to ethical sourcing and enhanced its reputation among eco-conscious buyers.

- In August 2023, Schwan's Company introduced recyclable packaging for its entire Freschetta product range. This shift toward sustainable packaging aligned with global environmental trends and strengthened its market positioning.

- In October 2023, Nestlé collaborated with fitness influencers across Australia and New Zealand to promote its healthier frozen pizza variants as convenient meal options for health enthusiasts. This campaign boosted brand visibility and engagement among health-conscious consumers.

- In February 2024, Dr. Oetker expanded its e-commerce operations by partnering with major online retailers in India and Indonesia. This strategic move increased accessibility and tapped into the growing demand for online purchases of frozen food products in these regions.

MARKET SEGMENTATION

This research report on the Asia Pacific frozen pizza market is segmented and sub-segmented into the following categories.

By Type

- Bread Pizza

- Filled Crust Pizza

- Thin Crust Pizza, Etc

By Pizza Toppings

- Cheese

- Meat

- Fruits And Vegetables

By Pizza Size

- Medium

- Regular

- Large.

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What’s fueling the growth of the Asia Pacific Frozen Pizza Market?

Rapid urbanization, dual-income households, and demand for convenient, Western-inspired meals—especially among younger consumers—are driving adoption, supported by improved cold-chain logistics and supermarket freezer expansion.

Which countries show the highest growth potential in the Asia Pacific Frozen Pizza Market?

China and India lead in volume growth due to rising middle-class spending and foodservice modernization, while Japan, South Korea, and Australia represent mature, premium segments with demand for gourmet and health-focused variants.

How are local tastes shaping product innovation in the Asia Pacific Frozen Pizza Market?

Manufacturers are adapting toppings and sauces to regional palates—e.g., teriyaki chicken and seafood in Japan, tandoori paneer and spicy Sichuan in India, kimchi and bulgogi in Korea—making localization key to mainstream acceptance.

Are health and wellness trends influencing formulations in the Asia Pacific Frozen Pizza Market?

Yes—demand is rising for reduced-sodium, whole-grain crust, plant-based cheese, and vegetable-loaded options, especially in Australia and urban China, as consumers seek “better-for-you” convenience without sacrificing taste.

Who are the major players in the Asia Pacific Frozen Pizza Market?

Global brands like Dr. Oetker, Nestlé (DiGiorno, California Pizza Kitchen), and Ajitto (Japan) compete with strong local players such as AFC Holdings (Japan), Kraft Heinz (via partnerships), Mother Dairy (India), and private labels from retailers like AEON and Walmart China.

How is e-commerce changing frozen pizza distribution in the Asia Pacific Frozen Pizza Market?

Online grocery (e.g., JD Fresh, Meituan, Blinkit) and quick-commerce platforms now offer reliable last-mile cold delivery—enabling direct-to-consumer trials, limited-edition launches, and subscription models for repeat purchases.

What role does the foodservice channel play in the Asia Pacific Frozen Pizza Market?

Pizzerias, cafés, and hotels use frozen bases for consistency and cost control, while cloud kitchens leverage par-baked pizzas for rapid delivery—making B2B a strategic, high-volume segment beyond retail.

Are sustainability concerns affecting packaging in the Asia Pacific Frozen Pizza Market?

Increasingly—brands are shifting to recyclable mono-material trays, eliminating plastic overwraps, and exploring compostable films to meet APAC’s tightening plastic regulations (e.g., India’s EPR rules, Japan’s 2025 packaging targets).

What challenges hinder wider adoption in the Asia Pacific Frozen Pizza Market?

Persistent perception of frozen pizza as “low quality” in some markets, high energy costs for home freezing, and flavor authenticity gaps compared to fresh pizzerias—though premiumization and chef collaborations are countering this.

What’s the market outlook for 2025–2030 in the Asia Pacific Frozen Pizza Market?

The Asia Pacific Frozen Pizza Market is projected to grow at a robust CAGR, driven by convenience culture, culinary globalization, and cold-chain expansion—evolving from a niche import to a mainstream category with localized, premium, and functional innovations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com