Asia Pacific In-Building Wireless Market Research Report – Segmented By Offerings (Infrastructure, Services), End-user , Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2025 to 2033

Asia Pacific In-Building Wireless Market Size

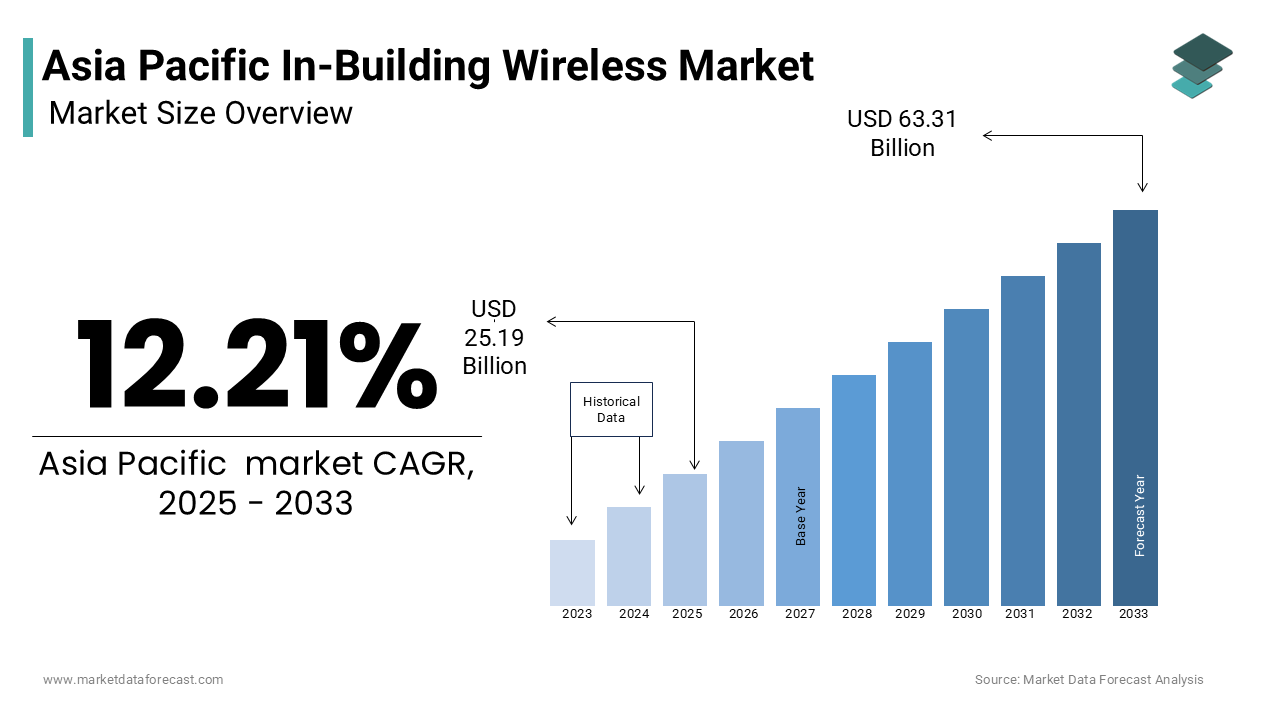

The Asia Pacific In-Building Wireless Market was worth USD 22.45 billion in 2024. The Asia Pacific market is expected to reach USD 63.31 billion by 2033 from USD 25.19 billion in 2025, rising at a CAGR of 12.21% from 2025 to 2033.

The Asia Pacific in-building wireless market refers to the deployment of wireless communication systems within commercial, residential, and industrial structures to ensure seamless connectivity and network reliability. These systems include Distributed Antenna Systems (DAS), small cells, Wi-Fi networks, and Internet of Things (IoT)-enabled infrastructure that collectively address signal loss, interference, and capacity issues within enclosed environments. As urbanization accelerates across the region, with increasing reliance on mobile connectivity for both personal and enterprise applications, demand for robust indoor wireless solutions has surged. Countries such as China, India, Japan, and South Korea are witnessing a rise in smart building initiatives, which integrate advanced communication technologies to support automation, security, and energy efficiency.

MARKET DRIVERS

Expansion of Smart Cities and Urban Infrastructure Projects

One of the key drivers fueling the growth of the in-building wireless market in the Asia Pacific is the aggressive expansion of smart city initiatives and large-scale urban infrastructure projects. Governments across the region are investing heavily in transforming traditional urban centers into technologically integrated ecosystems that rely on seamless wireless connectivity for public services, transportation, surveillance, and utilities management. In China alone, the Ministry of Housing and Urban-Rural Development reported that over 500 cities have launched smart city programs since 2020, many of which involve retrofitting existing buildings or constructing new facilities equipped with intelligent communication infrastructures. The integration of 5 G-ready infrastructure within these developments further amplifies the need for scalable DAS and small cell deployments.

Rising Demand for Seamless Indoor Connectivity in Commercial Real Estate

A significant driver propelling the Asia Pacific in-building wireless market is the escalating demand for uninterrupted indoor connectivity within commercial real estate properties. Businesses across sectors such as banking, hospitality, retail, and healthcare increasingly depend on high-speed wireless access to facilitate day-to-day operations, enhance customer experience, and deploy digital tools effectively.

In Australia, the Property Council of Australia reported that 85% of commercial property developers incorporated dedicated in-building wireless systems in new constructions launched between 2021 and 2023. Similarly, in Singapore, where the Infocomm Media Development Authority mandates minimum connectivity standards for all new commercial buildings, the adoption of enterprise-grade wireless solutions has become standard practice. This trend is mirrored in Japan, where Tokyo’s metropolitan government estimates that over 90% of newly built office complexes now feature multi-carrier DAS installations to accommodate diverse employee and visitor connectivity needs.

Furthermore, as per ABI Research, the number of Wi-Fi 6 access points deployed in commercial buildings across South Korea increased by 38% in 2023 compared to the previous year, reflecting heightened investment in next-generation wireless technologies. The convergence of remote work trends, mobile-first strategies, and cloud-based business models has made in-building wireless infrastructure indispensable for maintaining productivity and service quality in modern workplaces across the region.

MARKET RESTRAINTS

High Deployment Costs and Technical Complexity

Despite growing demand, the Asia Pacific in-building wireless market faces a notable restraint in the form of high deployment costs and technical complexity associated with integrating wireless infrastructure within existing and new buildings. The installation of distributed antenna systems (DAS), small cells, and other indoor connectivity solutions requires substantial capital expenditure, including hardware procurement, engineering design, site surveys, and ongoing maintenance.

Moreover, technical challenges related to frequency planning, signal interference, and multi-carrier coordination add layers of complexity to deployment processes. Additionally, retrofitting older buildings with modern wireless systems often involves structural modifications, which can lead to project delays and increased labor expenses. The lack of standardized regulations across different Asia Pacific markets further complicates deployment. For example, as per the Australian Communications and Media Authority, compliance with local spectrum policies and carrier-specific requirements frequently results in additional costs and prolonged implementation timelines. These financial and technical barriers hinder widespread adoption among small and medium enterprises, limiting the market's growth potential in certain segments.

Spectrum Congestion and Regulatory Hurdles

Another significant restraint affecting the Asia Pacific in-building wireless market is the growing issue of spectrum congestion, coupled with stringent regulatory frameworks. As mobile data consumption continues to surge, especially indoors, the available radio spectrum becomes increasingly saturated, leading to performance degradation in wireless networks. Regulatory authorities in several countries impose strict licensing conditions and spectrum allocation rules that complicate the deployment of private wireless networks and in-building solutions. In India, for instance, the Telecom Regulatory Authority of India mandates that enterprises seeking to operate private LTE networks must obtain spectrum licenses, which are both costly and time-consuming to secure. Furthermore, as per PwC’s 2023 global telecom regulatory survey, inconsistent spectrum policies across ASEAN nations create operational inefficiencies for multinational companies attempting to deploy uniform in-building wireless architectures. These regulatory complexities not only slow down market expansion but also increase the total cost of ownership for end-users, acting as a deterrent to the broader adoption of advanced indoor wireless solutions.

MARKET OPPORTUNITIES

Adoption of Private 5G Networks in Industrial and Enterprise Environments

A major opportunity emerging in the Asia Pacific in-building wireless market is the increasing adoption of private 5G networks within industrial and enterprise settings. Unlike traditional public cellular networks, private 5G offers businesses enhanced control over network performance, security, and latency, making it ideal for mission-critical applications in manufacturing, logistics, healthcare, and education. In South Korea, for example, the Ministry of Science and ICT reports that over 200 manufacturing plants have implemented private 5G networks since 2021 to enable real-time automation, robotics control, and AI-driven analytics. Similarly, in Japan, Toyota and Hitachi have partnered with NTT DOCOMO to deploy 5 G-enabled smart factories where in-building wireless connectivity supports autonomous guided vehicles and predictive maintenance systems.

Additionally, as per Frost & Sullivan, enterprise spending on private wireless infrastructure in Australia is expected to grow at a compound annual rate of 22% through 2028. This shift reflects a broader trend where organizations seek greater autonomy over their communication infrastructure. The ability of private 5G to seamlessly integrate with edge computing and IoT platforms positions it as a transformative force in reshaping the Asia Pacific in-building wireless landscape.

Integration of Wireless Technologies in Green Building Initiatives

An emerging opportunity in the Asia Pacific in-building wireless market is the integration of wireless communication systems within green building initiatives aimed at improving energy efficiency and sustainability. Governments and private sector stakeholders across the region are increasingly adopting green certification standards such as LEED (Leadership in Energy and Environmental Design) and BCA Green Mark in Singapore, which emphasize the use of smart technologies to reduce carbon footprints. According to the World Green Building Council, over 40% of new commercial constructions in the Asia Pacific were certified green in 2023, up from 25% in 2020.

Wireless technologies play a crucial role in enabling smart lighting, HVAC control, occupancy sensing, and real-time energy monitoring—all essential components of sustainable building management systems. For instance, as per the Building and Construction Authority of Singapore, buildings equipped with IoT-enabled wireless sensors demonstrated an average energy savings of 18–25% compared to conventional structures. In India, the Bureau of Energy Efficiency notes that smart wireless controls contributed to a 20% reduction in electricity consumption across certified green buildings in 2022.

Moreover, the adoption of low-power wide-area networks (LPWAN) such as LoRaWAN and NB-IoT is gaining traction in smart cities like Seoul and Melbourne, where wireless sensors are used to optimize water usage, waste management, and indoor air quality.

MARKET CHALLENGES

Interoperability Issues Across Multi-Vendor and Multi-Technology Deployments

One of the foremost challenges confronting the Asia Pacific in-building wireless market is the lack of interoperability across multi-vendor and multi-technology deployments. This challenge is particularly pronounced in large commercial complexes and mixed-use buildings where multiple service providers, equipment manufacturers, and communication standards coexist. In Japan, the Ministry of Internal Affairs and Communications found that over 40% of recent in-building wireless deployments experienced performance bottlenecks due to incompatible hardware configurations between cellular and Wi-Fi infrastructures.

Standardization gaps further exacerbate the problem. While industry bodies such as IEEE and 3GPP have made strides in defining common frameworks, regional disparities in implementation persist. For instance, as per GSMA Intelligence, inconsistencies in frequency band allocations across ASEAN countries complicate the cross-border deployment of unified wireless solutions. These interoperability concerns not only delay time-to-market but also limit scalability, posing a significant barrier to the cohesive expansion of the Asia Pacific in-building wireless ecosystem.

Cybersecurity Vulnerabilities in Expanding Indoor Wireless Networks

Cybersecurity vulnerabilities present a growing challenge with the proliferation of interconnected devices and the adoption of open wireless architectures. The increasing reliance on Wi-Fi 6, 5G, and IoT-enabled systems within commercial and residential buildings has introduced new attack surfaces, exposing sensitive data and operational systems to potential breaches. According to Kaspersky’s 2023 Threat Landscape Report, cyberattacks targeting enterprise wireless networks in the Asia Pacific increased by 34% compared to the previous year, with in-building infrastructures being a primary point of entry.

Weak authentication mechanisms, insufficient encryption, and misconfigured access points contribute significantly to this risk. In Singapore, the Cyber Security Agency revealed that over 20% of security incidents in smart buildings during 2022 stemmed from compromised wireless endpoints, leading to unauthorized access and data exfiltration. Similarly, in India, the Data Security Council of India noted a spike in ransomware attacks exploiting poorly secured Wi-Fi networks in corporate offices, resulting in operational disruptions and financial losses.

Moreover, as per PwC’s Asia Pacific State of Information Security Survey, less than 40% of organizations in the region have implemented comprehensive security protocols for their indoor wireless ecosystems. The absence of standardized security benchmarks for in-building wireless deployments further compounds the issue. Addressing these vulnerabilities requires a coordinated effort between regulators, infrastructure providers, and end-users to implement robust security measures without compromising network performance, a balance that remains elusive in many parts of the market.

SEGMENTAL ANALYSIS

By Offering Insights

The infrastructure was the largest segment in the Asia Pacific in-building wireless market with a dominant share in 2024 due to the increasing deployment of Distributed Antenna Systems (DAS) and Small Cells across commercial and industrial buildings to address growing indoor coverage gaps and support high-speed data transmission. The demand for robust infrastructure is being driven by the rapid expansion of smart cities and digitized real estate developments. As per McKinsey Global Institute, nearly 45% of all new commercial constructions in the region now incorporate multi-operator DAS networks to ensure seamless connectivity. Additionally, the proliferation of 5G services has accelerated the adoption of Small Cells, which are essential for densifying urban networks and supporting high-capacity indoor applications. GSMA Intelligence notes that Small Cell installations in South Korea grew by 37% year-over-year in 2023 due to aggressive carrier investments and enterprise-led digital transformation initiatives.

The services segment is lucratively growing with a CAGR of 13.8% from 2025 to 2033 owing to the rising need for managed and professional services such as network planning, integration, maintenance, and optimization. A key driver behind this surge is the increasing complexity of wireless infrastructures, particularly with the integration of private 5G, Wi-Fi 6, and IoT technologies. As reported by Deloitte, more than 60% of medium and large enterprises in Australia and Singapore now prefer outsourced services for in-building wireless deployments to reduce operational overheads and ensure compliance with evolving regulatory standards. Additionally, the growing trend of cloud-based wireless management solutions is boosting service demand. According to IDC Asia Pacific, the adoption of cloud-managed wireless services among enterprises rose by 18% in 2023, reflecting a shift toward scalable, flexible, and cost-efficient service models that support long-term connectivity strategies.

By End User Insights

The commercial campuses dominated the Asia Pacific in-building wireless market by capturing 42.3% in 2024. This segment includes corporate offices, business parks, retail complexes, and co-working spaces where uninterrupted wireless connectivity is crucial for daily operations, employee productivity, and customer engagement. One of the primary drivers behind this dominance is the widespread adoption of smart building technologies. The Singapore Building and Construction Authority reports that certified green buildings equipped with intelligent wireless systems have grown by 22% annually since 2020, enhancing energy efficiency and occupant experience. Moreover, the proliferation of mobile-first workflows and cloud-based collaboration tools has heightened reliance on seamless indoor connectivity.

The entertainment & sports venues segment is emerging with a CAGR of 15.3% from 2025 to 2033. This rapid expansion is driven by the increasing number of large-scale events, stadiums, amusement parks, and entertainment centers requiring high-density wireless connectivity to support thousands of simultaneous users. A key factor fueling this growth is the rising consumer demand for immersive experiences through augmented reality (AR), live streaming, and real-time social media interaction during sporting and entertainment events. Additionally, governments and event organizers are investing heavily in digital infrastructure to enhance fan engagement and security. For instance, the Japan National Stadium integrated AI-powered crowd analytics and ultra-low latency connectivity for real-time broadcasting, which is setting a benchmark for future venue deployments across the region.

REGIONAL ANALYSIS

China was accounted in holding 28.6% of the Asia Pacific in-building wireless market share in 2024 with its aggressive push toward digital infrastructure modernization, supported by strong government policies and extensive 5G rollout programs. The Smart Cities initiative, covering more than 500 urban centers, is a key driver for in-building wireless adoption. As reported by McKinsey Global Institute, over 60% of new commercial developments in Tier-1 cities like Shanghai and Shenzhen now include distributed antenna systems (DAS) and small cells to meet enterprise-grade connectivity needs. Furthermore, the rapid digitization of industries such as manufacturing, finance, and healthcare is creating sustained demand for reliable indoor wireless networks. China continues to set the pace for the broader Asia Pacific region in terms of both deployment scale and technological innovation in the in-building wireless domain.

India was positioned second in the Asia Pacific in-building wireless market by holding 14.3% of the share in 2024. The country’s growth is primarily fueled by its ambitious digital infrastructure development plans and the government’s push for smart city and smart building initiatives. As per the Ministry of Housing and Urban Affairs, the Smart Cities Mission has allocated over USD 30 billion for the development of digitally enabled urban infrastructure across 100 cities, which is significantly boosting demand for in-building wireless solutions.

Japan in-building wireless market growth is likely to grow with a CAGR of 11.2% of share in 2024. The country’s mature telecommunications landscape and early adoption of advanced wireless technologies place it at the forefront of indoor connectivity innovation. A key driver behind Japan’s strong market presence is its emphasis on automation and digital transformation in industries such as manufacturing, healthcare, and logistics. Furthermore, Japan’s aging population has spurred investment in smart healthcare infrastructure, where wireless connectivity plays a vital role in remote patient monitoring and hospital automation. The Building Standards Act mandates minimum connectivity standards for public and commercial buildings, reinforcing the necessity of robust indoor wireless systems.

South Korea in-building wireless market growth is gearing up with new opportunities in the next coming years. A major driver of growth is the government-backed K-Urban regeneration program, which focuses on upgrading existing urban infrastructure with smart technologies. As reported by the Korea Real Estate Board, over 40% of new commercial developments in Seoul now feature Wi-Fi 6E and Small Cell integrations to support high-density connectivity. Moreover, South Korea’s manufacturing and technology sectors are rapidly adopting private 5G networks. Samsung and Hyundai have implemented dedicated indoor wireless setups in production plants to support autonomous machinery and real-time quality monitoring. The country’s regulatory environment also supports rapid deployment, with streamlined spectrum allocation processes for enterprise use cases. These developments reinforce South Korea’s position as a leader in high-performance in-building wireless ecosystems.

Australia in-building wireless market growth is ascribed to be driven by the strong investment in commercial real estate, government-led smart infrastructure projects, and increasing demand for high-speed indoor connectivity. According to the Property Council of Australia, over 85% of new commercial buildings launched between 2021 and 2023 included dedicated in-building wireless systems, which reflects a shift toward digitally enabled workplaces. Additionally, the transport and hospitality sectors are increasingly adopting in-building wireless solutions. Sydney Airport, for example, completed a major DAS upgrade in 2023 to support seamless passenger connectivity. With continued investment in 5G and fiber backhaul, Australia is strengthening its position as a key player in the Asia Pacific in-building wireless market.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

CommScope, Corning Incorporated, Huawei Technologies Co., Ltd., Nokia, Samsung Electronics Co., Ltd., Telefonaktiebolaget LM Ericsson, JMA Wireless, Airspan Networks, ZTE Corporation, and TE Connectivity are some of the key market players in the Asia Pacific in-building wireless market.

The competition in the Asia Pacific in-building wireless market is intense, driven by rapid technological advancements and increasing demand for seamless indoor connectivity across diverse sectors. A mix of global giants and regional players coexist, each striving to capture market share through innovation, strategic alliances, and tailored solutions. Companies are focusing on delivering scalable, interoperable, and future-ready wireless infrastructures that support evolving use cases in commercial, industrial, and public spaces. With governments pushing for digital infrastructure modernization, vendors are under pressure to offer cost-effective and efficient deployment models. The rise of private 5G networks, integration with IoT, and the need for secure, high-capacity indoor coverage are reshaping competitive dynamics. This evolving landscape ensures that competition remains fierce, with continuous product enhancements and market positioning strategies playing a decisive role in long-term success.

Top Players in the Asia Pacific In-Building Wireless Market

Huawei Technologies Co., Ltd.

Huawei plays a leading role in shaping the Asia Pacific in-building wireless market through its comprehensive portfolio of indoor connectivity solutions, including Distributed Antenna Systems (DAS), Small Cells, and enterprise-grade Wi-Fi infrastructure. The company has been instrumental in supporting large-scale smart city initiatives across China and Southeast Asia by integrating next-generation wireless technologies into commercial and industrial buildings. Huawei’s focus on innovation and strategic partnerships with local telecom operators enables it to deliver tailored solutions that meet evolving connectivity demands. Its influence extends beyond the regional market, as it remains a dominant force in global telecommunications infrastructure.

Nokia Corporation

Nokia is a key player in the Asia Pacific in-building wireless market, offering advanced private wireless networks, indoor DAS, and cloud-based management systems. The company has been actively engaged in deploying mission-critical communication solutions for enterprises, government institutions, and transportation hubs across the region. Nokia's commitment to open standards and interoperability makes its offerings highly adaptable for multi-vendor environments. Through extensive R&D investments and collaborations with regional telecom regulators, Nokia continues to drive the adoption of secure and scalable indoor wireless networks, reinforcing its strong foothold in both enterprise and public sector applications.

CommScope Holding Company, Inc.

CommScope is a major contributor to the Asia Pacific in-building wireless ecosystem, providing end-to-end infrastructure solutions such as fiber-based DAS, Wi-Fi access points, and network optimization tools. The company supports a wide range of verticals including healthcare, education, retail, and transportation with customized indoor connectivity platforms. CommScope’s expertise in hybrid wired-wireless architectures allows seamless integration with existing building infrastructures.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by key players in the Asia Pacific in-building wireless market is strategic partnerships and joint ventures with local telecom operators, system integrators, and government bodies. These collaborations help companies tailor their offerings to regional requirements while accelerating project execution and regulatory compliance. Another critical approach is product innovation and R&D investment, where firms continuously develop next-generation solutions such as AI-driven network analytics, cloud-managed wireless systems, and energy-efficient hardware to meet evolving customer needs. Additionally, market expansion through acquisitions and localized presence is widely adopted, allowing companies to strengthen distribution networks, enhance service delivery capabilities, and gain a competitive advantage in emerging markets within the region.

RECENT MARKET DEVELOPMENTS

- In March 2024, Huawei partnered with SoftBank Corp in Japan to deploy an indoor 5G network solution at Tokyo Haneda Airport. This collaboration aimed to enhance passenger experience by ensuring seamless connectivity and ultra-low latency for real-time applications.

- In July 2023, Nokia launched a new private wireless platform specifically designed for manufacturing facilities in South Korea. The initiative was intended to support Industry 4.0 transformation by enabling reliable and secure in-building connectivity for automation and data analytics.

- In November 2023, CommScope announced a strategic alliance with Optus in Australia to upgrade enterprise in-building wireless infrastructure. The partnership focused on expanding Wi-Fi 6 and DAS deployments across commercial campuses and public venues to meet rising connectivity demands.

- In February 2024, Ericsson expanded its indoor solutions portfolio in India by introducing a compact 5G radio unit for enterprise buildings. The move was aimed at strengthening its position in the growing Indian market by catering to digital transformation needs across multiple sectors.

- In May 2023, Samsung Electronics collaborated with SK Telecom to roll out AI-powered indoor wireless systems in Seoul’s major business districts. The initiative sought to improve network efficiency and user experience by leveraging intelligent traffic management and predictive maintenance technologies.

MARKET SEGMENTATION

This research report on the Asia Pacific in-building wireless market is segmented and sub-segmented into the following categories.

By Offering

- Infrastructure

- Distributed Antenna System (DAS)

- Small Cells

- Services

By End User

- Commercial Campuses

- Government

- Transportation & Logistics

- Entertainment & Sports Venues

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What factors are driving the growth of this market in Asia Pacific?

Key growth drivers include the deployment of 5G networks, increased demand for mobile data and seamless indoor coverage, adoption of smart building technologies, and rising IoT integration.

What are the future trends expected in the Asia Pacific in-building wireless market?

Key trends include the integration of AI and machine learning for network optimization, the adoption of cloud-based network management, growing use of hybrid DAS and small cell systems, and the expansion of private 5G networks within enterprises and industrial facilities.

What is the long-term growth outlook for the Asia Pacific in-building wireless market?

The long-term outlook is strong, with the market expected to grow steadily through 2032, supported by 5G expansion, urban development, government digitalization initiatives, and rising consumer expectations for uninterrupted connectivity indoors.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com