- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Asia Pacific Integrated Operating Room Market Size

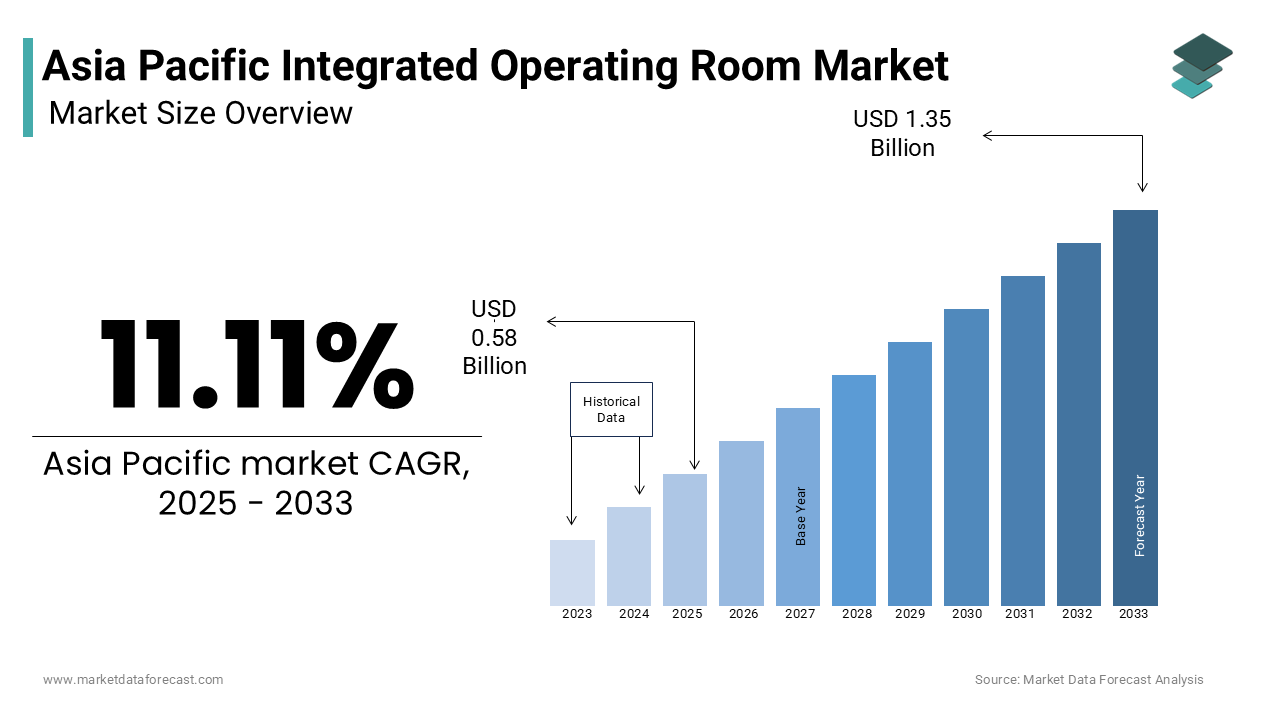

The Asia Pacific Integrated Operating Room Market was worth USD 0.58 billion in 2025. The Asia Pacific market is expected to reach USD 1.49 billion by 2034 from USD 0.64 billion in 2026, rising at a CAGR of 11.11% from 2026 to 2034.

The Asia Pacific integrated operating room market includes a technologically advanced surgical environment where digital systems, medical equipment, and workflow management tools are seamlessly interconnected to enhance surgical precision, reduce procedural errors, and improve patient outcomes. These rooms integrate imaging devices, lighting systems, audio-visual components, and robotic-assisted technologies under a centralized control system, enabling real-time data sharing and streamlined communication among surgical teams. Besides, rising healthcare expenditures and government initiatives aimed at modernizing hospitals are contributing to the integration of digital platforms within surgical suites.

MARKET DRIVERS

Surge in Demand for Minimally Invasive Surgeries

One of the primary drivers of the Asia Pacific integrated operating room market is the rising preference for minimally invasive surgeries (MIS). These procedures offer reduced recovery times, lower infection risks, and enhanced surgical precision—factors that are increasingly influencing both physicians and patients. As per World Health Organization (WHO) data, the number of surgical procedures performed annually in the Asia Pacific region has grown significantly, with MIS accounting for nearly 40% of all surgeries in countries like South Korea and Japan. China, in particular, has witnessed a rapid increase in the adoption of laparoscopic and endoscopic procedures. This trend necessitates the use of integrated operating rooms equipped with high-definition imaging, robotic assistance, and centralized control systems to ensure seamless execution of these complex procedures. Moreover, governments in the region are investing in training programs for surgeons specializing in MIS techniques. For instance, the Indian Ministry of Health launched a national initiative in 2022 to equip 100 government hospitals with advanced surgical suites, many of which incorporate integrated operating systems.

Increasing Healthcare Expenditure and Hospital Modernization Initiatives

A significant driver of the Asia Pacific integrated operating room market is the surge in healthcare expenditure coupled with aggressive hospital modernization efforts. Countries in the region are allocating more resources to upgrade their healthcare infrastructure to meet the rising demand for quality medical services. Japan remains at the forefront of this transformation. Private healthcare providers are also driving this shift; Apollo Hospitals in India and Fortis Healthcare have invested heavily in smart operating theaters equipped with AI-enabled surgical navigation tools. These investments reflect a broader regional trend toward modernized and technology-driven healthcare delivery.

MARKET RESTRAINTS

High Initial Investment and Maintenance Costs

One of the principal restraints hampering the growth of the Asia Pacific integrated operating room market is the substantial initial capital required for installation and ongoing maintenance. Integrated operating rooms consist of sophisticated components such as digital imaging systems, voice-controlled interfaces, robotic arms, and centralized control panels, which collectively contribute to elevated setup costs. According to McKinsey & Company, equipping a single integrated operating suite can cost anywhere between USD 1.5 million and USD 3 million, depending on the level of automation and technological integration. This financial burden is particularly challenging for small and mid-sized hospitals, especially in developing economies like Indonesia, the Philippines, and Vietnam, where healthcare budgets remain constrained. Also, recurring expenses related to software updates, system calibration, and technician training add to the long-term financial strain.

Lack of Skilled Professionals and Standardized Training Programs

Another major restraint affecting the Asia Pacific integrated operating room market is the shortage of trained professionals capable of managing and operating advanced surgical systems. Integrated operating rooms require specialized knowledge not only in surgery but also in digital interface navigation, data integration, and real-time coordination between multiple devices. According to the Asia Pacific Association of Surgical Oncology, only a small percentage of surgical teams in countries like India, Bangladesh, and Cambodia receive formal training in handling integrated surgical environments. The absence of standardized training protocols further exacerbates the issue. In China, despite the rapid deployment of digital operating suites, only 18% of hospitals have structured education programs for staff regarding integrated OR systems, as reported by the Chinese Society of Surgery. This gap in workforce readiness leads to suboptimal utilization of available technology, reducing efficiency gains and delaying ROI.

Moreover, the complexity of integrated systems demands continuous upskilling. The lack of skilled personnel results in prolonged learning curves, increased procedural errors, and underutilization of system capabilities.

MARKET OPPORTUNITIES

Expansion of Telemedicine and Remote Surgical Assistance

The rapid proliferation of telemedicine across the Asia Pacific presents a compelling opportunity for the integrated operating room market. With improved internet connectivity and the rise of 5G networks, remote surgical assistance and real-time consultation during procedures have become increasingly feasible. Telepresence and remote guidance capabilities embedded within integrated operating systems allow senior surgeons to assist colleagues in rural or underserved areas. In India, the Ministry of Electronics and Information Technology reported that telemedicine consultations surged considerably between 2021 and 2023, prompting hospitals to adopt digitally enabled operating rooms to support virtual collaboration. Furthermore, robotic-assisted telesurgery is gaining traction. In 2023, Apollo Hospitals in India successfully conducted a remote robotic cholecystectomy using a 5 G-enabled integrated operating suite—a milestone that underscores the potential for expanding such technologies across the region.

Rise in Medical Tourism and Multi-Specialty Hospitals

The growing prominence of medical tourism in the Asia Pacific is creating a favorable environment for the expansion of integrated operating rooms. Countries such as Thailand, India, Malaysia, and Singapore have emerged as leading destinations for international patients seeking high-quality, cost-effective surgical treatments. Like, Thailand alone welcomed a substantial number of medical tourists in 2023, with orthopedic, cardiovascular, and cosmetic surgeries being the most sought-after procedures. To cater to this influx, healthcare providers are upgrading their surgical infrastructure to meet international standards. Integrated operating rooms play a crucial role in enhancing procedural efficiency, ensuring transparency, and improving post-operative outcomes—key factors influencing medical tourists’ choice of destination. In addition, the rise of multi-specialty hospital chains is accelerating the adoption of advanced surgical environments.

MARKET CHALLENGES

Regulatory Hurdles and Compliance Complexity

A significant challenge facing the Asia Pacific integrated operating room market is the fragmented regulatory landscape and the complexity involved in meeting compliance requirements across different countries. Each nation in the region has distinct medical device approval processes, data privacy laws, and clinical validation protocols, complicating the deployment of integrated surgical systems. In China, the National Medical Products Administration mandates rigorous clinical trials and documentation for foreign manufacturers, extending the time-to-market by several months. Similarly, in India, the Central Drugs Standard Control Organization has introduced stringent guidelines under the Medical Device Rules 2023, requiring manufacturers to demonstrate interoperability and cybersecurity safeguards—an added layer of complexity for integrated OR vendors. Moreover, data protection laws such as Japan’s Act on the Protection of Personal Information and Australia’s Privacy Act impose strict conditions on handling patient data generated within integrated operating environments.

Cybersecurity Vulnerabilities in Digitally Integrated Systems

As integrated operating rooms become increasingly reliant on digital connectivity and real-time data exchange, cybersecurity vulnerabilities pose a serious threat to their widespread adoption. These systems often connect to hospital-wide networks, electronic health records, and cloud-based storage platforms, exposing them to potential cyberattacks. According to Kaspersky Lab, healthcare organizations in the Asia Pacific experienced a major increase in ransomware attacks between 2022 and 2023, with surgical units being among the most targeted departments. Medical devices used in integrated operating rooms, such as robotic surgical assistants and intraoperative imaging systems, frequently run on outdated software with limited security patches. As per the Singapore Cyber Security Agency, a considerable share of medical equipment in hospitals lacks built-in encryption or intrusion detection mechanisms, making them susceptible to breaches. Despite growing awareness, many hospitals in emerging markets like Indonesia and the Philippines lack dedicated cybersecurity teams or incident response plans tailored for integrated systems.

SEGMENTAL ANALYSIS

By Device Insights

The intraoperative diagnostic devices segment constituted the largest in the Asia Pacific integrated operating room market i.e., accounting for a 32.3% of total revenue in 2024. This control over the market is basically associated with the increasing reliance on real-time imaging and monitoring during surgical procedures to enhance precision and reduce complications. These devices include intraoperative MRI, CT scanners, ultrasound systems, and endoscopic visualization tools. Also, government initiatives promoting early diagnosis and advanced treatment modalities are driving adoption. In China, the National Health Commission reported that the installation of intraoperative imaging systems increased significantly year-over-year between 2022 and 2024. The integration of AI-based image analysis software with these devices further enhances their utility, making them indispensable in modern operating suites across the region.

The operating room communication systems segment is projected to witness the fastest growth in the Asia Pacific integrated operating room market, recording a CAGR of 11.4% from 2025 to 2033. This rapid expansion is driven by the increasing need for seamless data exchange among surgical teams, electronic health records (EHRs), and remote surgical collaboration platforms. In India, the Ministry of Health’s push for digital health records has necessitated the integration of real-time communication solutions in surgical environments. Furthermore, the rise in telemedicine-enabled surgeries has amplified the demand for high-speed, secure communication systems.

By Surgical Application Insights

The therapeutics application prevailed in the Asia Pacific integrated operating room market by capturing 61.5% of the total value in 2024. This dominance is fueled by the rising volume of surgical interventions aimed at treating chronic diseases such as cancer, cardiovascular disorders, and orthopedic conditions. According to the World Health Organization (WHO), non-communicable diseases account for a large percentage of all deaths in the Asia Pacific region, necessitating an increase in therapeutic surgical procedures. Moreover, the integration of robotic-assisted surgical platforms in therapeutic applications has enhanced precision and reduced recovery times. For instance, Da Vinci Surgical System installations in Indian hospitals grew notably in 2023, primarily for therapeutic procedures like prostatectomies and hysterectomies, as noted by MedTech Dive. So, the increasing prevalence of lifestyle-related illnesses and the expansion of private healthcare facilities in countries like Thailand and Malaysia further reinforce the demand for integrated operating systems tailored for therapeutic use.

The diagnostics imaging application is emerging as the rapidly expanding segment in the Asia Pacific integrated operating room market, with a predicted CAGR of 10.2% over the forecast period. This growth is largely driven by the increasing integration of real-time imaging technologies into surgical workflows to enable accurate diagnosis and intraoperative decision-making. According to the Asian Society of Radiologists, the deployment of intraoperative imaging systems such as mobile C-arms, fluoroscopes, and portable ultrasounds has expanded significantly, especially in trauma and spinal surgeries. In Australia, a large share of tertiary care hospitals have upgraded to digital imaging-integrated ORs to support minimally invasive diagnostics. Apart from these, the adoption of hybrid operating rooms equipped with advanced imaging capabilities is accelerating in urban centers across South Korea and Japan.

By Type Insights

The segment of audio and video management systems represented the biggest segment in the Asia Pacific integrated operating room market by holding 8.5% of the total market share in 2024. This influence is mainly due to the critical role these systems play in enhancing communication, enabling real-time documentation, and supporting remote surgical training and consultation. Additionally, the integration of voice-controlled interfaces and touch-screen panels allows surgeons to access patient data and imaging without physical contact, reducing contamination risks. In India, the Ministry of Electronics and Information Technology recorded an increase in AV system installations in public hospitals between 2022 and 2024 under its Smart Hospitals initiative.

The instrument tracking systems segment is experiencing the highest growth rate in the Asia Pacific integrated operating room market, with an estimated CAGR of 12.5% in the coming years. This quick development is caused by the increasing emphasis on operational efficiency, infection control, and asset utilization in surgical settings. Like, improper instrument management contributes majorly to surgical delays and post-operative infections in hospitals across the region. To address this, many hospitals in Malaysia and Indonesia have adopted RFID-based tracking solutions to monitor surgical tools in real time. Besides, regulatory mandates in countries like Australia and Japan require comprehensive sterilization and inventory tracking protocols. The Australian Commission on Safety and Quality in Health Care reported that a significant share of major hospitals now use automated tracking systems to ensure compliance and reduce human errors.

REGIONAL ANALYSIS

China remained the largest contributor to the Asia Pacific integrated operating room market and held a 29.3% of the regional share in 2024. The country's growth is driven by rapid urbanization, substantial healthcare investments, and a strong focus on digitizing hospital infrastructure. Moreover, domestic companies such as Mindray and Wisonic are playing a pivotal role in supplying cost-effective integrated OR solutions.

Japan exhibits a pioneering adoption of advanced surgical technologies. The country leads in the adoption of cutting-edge surgical technologies due to its aging population, high healthcare spending, and early embrace of digital hospital ecosystems. Furthermore, Japan’s aging demographic profile—where a large share of the population is aged above 65—has increased the demand for minimally invasive and precision-driven surgeries.

India is a fast-emerging market with high growth potential. The country’s expanding middle class, rising incidence of chronic diseases, and aggressive government-backed healthcare reforms are fueling the demand for technologically advanced surgical infrastructure. Private healthcare providers such as Apollo Hospitals and Fortis Healthcare have also been instrumental in adopting integrated OR systems. With medical tourism and insurance penetration on the rise, India’s integrated operating room market is expected to expand rapidly in the coming decade.

South Korea has a strong emphasis on digital health integration, driven by its advanced healthcare IT infrastructure and strong policy support for digital transformation in hospitals. The country is known for its early adoption of AI, IoT, and cloud-based surgical systems, which are increasingly being incorporated into operating room setups.

Australia is showing high healthcare standards, which are driving technological adoption. It is supported by its well-developed healthcare system, high per capita healthcare spending, and strong emphasis on patient safety and quality care. Also, the adoption of telehealth and remote surgical assistance has gained traction. With a strong regulatory framework and continuous technological advancements, Australia remains a key player in the Asia Pacific integrated operating room market, despite its relatively smaller population size.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific integrated operating room market is intense, marked by the presence of both global leaders and regional players striving to capture a larger share of the growing demand. As healthcare facilities increasingly adopt digitally integrated surgical environments, companies are focusing on differentiation through technological innovation, system interoperability, and enhanced user experience. The market features a mix of established medical device manufacturers and emerging firms, all competing to provide scalable, customizable, and future-ready solutions that align with evolving clinical needs. Strategic positioning is further influenced by varying levels of healthcare infrastructure development across countries, requiring companies to adapt their offerings to local regulatory landscapes and budget constraints. Additionally, the rise of smart hospitals and the push for digitized health records are compelling vendors to integrate AI, IoT, and cloud-based technologies into their systems. Customer relationships play a crucial role, with after-sales service, maintenance, and training becoming decisive factors in securing long-term contracts.

KEY MARKET PLAYERS

Some of the key market players in the Asia Pacific integrated operating room market include

- Stryker Corporation

- KARL STORZ SE & Co. KG

- Olympus Corporation

Top Players in the Asia Pacific Integrated Operating Room Market

KARL STORZ SE & Co. KG is a leading global manufacturer of endoscopic instruments and integrated operating room solutions. The company has a strong presence in the Asia Pacific, offering advanced visualization systems, digital OR integration, and workflow management tools. KARL STORZ is known for its collaboration with hospitals and research institutions to develop customized surgical environments that enhance precision and efficiency.

Getinge AB is a Swedish multinational corporation specializing in medical technologies and hospital solutions, including integrated operating room systems. In the Asia Pacific, Getinge has been instrumental in deploying intelligent OR suites that streamline clinical workflows and improve patient outcomes. The company emphasizes sustainable healthcare infrastructure and offers modular operating room designs tailored to local healthcare needs.

Stryker Corporation is a prominent player in the global medical technology sector with a robust footprint in the Asia Pacific integrated operating room market. Stryker provides comprehensive digital OR solutions, including surgical navigation systems, lighting, tables, and data integration platforms. The company’s strategic collaborations with local distributors and investment in training programs have strengthened its market position.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by leading players is strategic partnerships and collaborations with local healthcare providers, academic institutions, and government bodies. These alliances help companies tailor their integrated operating room solutions to regional requirements while enhancing market penetration through co-development initiatives and joint research projects.

Another key strategy is product innovation and technological advancements, where companies continuously invest in R&D to introduce next-generation integrated systems featuring AI-driven analytics, voice-activated controls, and real-time data synchronization. This not only differentiates them from competitors but also meets the evolving demands of modern surgical environments across the Asia Pacific.

Lastly, expansion through localized distribution networks and direct sales teams allows key players to strengthen their presence in emerging markets.

RECENT MARKET DEVELOPMENTS

- In February 2024, KARL STORZ launched a new line of ultra-high-definition endoscopic visualization systems tailored for hybrid operating rooms across Southeast Asia. This move was aimed at strengthening its foothold in the region by addressing the rising demand for real-time imaging and seamless integration in complex surgical procedures.

- In June 2023, Getinge partnered with a leading Japanese hospital network to deploy fully integrated operating suites equipped with AI-enabled workflow optimization tools. This collaboration was designed to enhance surgical efficiency and support the digital transformation of hospital infrastructure in Japan.

- In September 2024, Stryker announced the establishment of a dedicated training center in Mumbai, India, focused on educating surgeons and hospital staff on the use of integrated operating room technologies. This initiative reflects Stryker’s commitment to improving adoption rates and technical proficiency among healthcare professionals in emerging markets.

- In March 2023, Olympus (now Evident) introduced a modular integrated OR solution for mid-sized hospitals in Indonesia and the Philippines. This scalable system was developed to cater to budget-conscious healthcare providers while maintaining high standards of performance and connectivity.

- In November 2024, B. Braun entered into a strategic alliance with a South Korean digital health firm to integrate its anesthesia and monitoring systems with existing surgical platforms. The partnership aims to offer more cohesive and data-driven operating room environments across the Asia Pacific region.

MARKET SEGMENTATION

This research report on the Asia Pacific integrated operating room market is segmented and sub-segmented into the following categories.

By Device

- Intraoperative Diagnostic Devices

- Operating Room Communication Systems

- Operating Tables Types

- Operating Room Lights

By Surgical Application

- Therapeutics Application

- Diagnostics Imaging Application

By Type

- Operating Room and Procedure Scheduling System

- Recording and Documentation System

- Instrument Tracking System

- Audio and Video Management System

- Operating Room Inventory Management System

- Anesthesia Information Management

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC