Asia Pacific UV LED Market Size, Share, Trends & Growth Forecast Report By Technology (UV-A, UV-B, UV-C), By Application (UV Curing, Lithography, Medical and Scientific, Phototherapy, Sterilization, Disinfection, Counterfeit Detection, Others), By End Use (Industrial, Commercial, Residential), and Country (India, China, Japan, South Korea, Australia, Rest of APAC) – Industry Analysis From 2026 to 2034.

Market Size, 2025

$0.52 BnMarket Estimate, 2026

$0.65 BnMarket Forecast, 2034

$4.13 BnCAGR, 2026–2034

25.9%Asia Pacific UV LED Market Size

The size of the Asia Pacific UV LED market was worth USD 0.52 billion in 2025. The Asia Pacific market is anticipated to grow at a CAGR of 25.9% from 2026 to 2034 and be worth USD 4.13 billion by 2034, from USD 0.65 billion in 2026.

The Asia Pacific UV LED market refers to the section of light-emitting diodes that emit ultraviolet radiation, typically categorized into UVA, UVB, and UVC wavelengths. These LEDs are increasingly being adopted across various industries for applications such as water purification, air disinfection, surface sterilization, medical equipment, and industrial curing. Unlike conventional mercury-based UV lamps, UV LEDs offer advantages like energy efficiency, longer lifespan, compact size, and environmental safety, making them a preferred alternative in sectors requiring sustainable and high-performance solutions. According to recent industry assessments, the Asia Pacific region accounts for one of the fastest-growing shares in the global UV LED landscape, driven by countries such as China, Japan, South Korea, and India. Moreover, government initiatives aimed at improving public health infrastructure and promoting green technologies have further accelerated market penetration.

MARKET DRIVERS

Expansion of Water Treatment Infrastructure in Asia Pacific

One of the primary drivers propelling the Asia Pacific UV LED market is the rapid expansion of water treatment infrastructure, particularly in emerging economies such as India, Indonesia, and Vietnam. With rising concerns over waterborne diseases and deteriorating water quality, governments and private entities are investing heavily in advanced purification systems. UV LEDs offer an efficient, mercury-free, and low-maintenance solution for disinfecting drinking water, wastewater, and industrial effluents.

In China alone, nearly 60% of municipal water treatment plants have upgraded or plan to integrate UV-based disinfection systems by 2025, reflecting a strong shift away from chlorine-based methods due to harmful by-products. Additionally, Japan has been a pioneer in adopting UV LEDs for point-of-use water purifiers in households, contributing significantly to regional market growth.

Growth in Healthcare and Medical Device Applications

The healthcare sector in the Asia Pacific region has emerged as a critical driver for the UV LED market, fueled by increased investments in hospital infrastructure, infection control protocols, and portable medical devices. UV LEDs are increasingly used in hospitals, clinics, and laboratories for surface disinfection, air purification, and sterilization of surgical instruments. Their compact size, low power consumption, and absence of toxic materials make them ideal for incorporation into handheld sanitizers, mobile robots, and embedded sterilization units. This trend is further supported by rising awareness around antimicrobial resistance and the need for chemical-free sterilization alternatives, reinforcing the role of UV LEDs in modern healthcare delivery systems across the region.

MARKET RESTRAINTS

High Initial Costs and Limited Economies of Scale

Despite the promising growth prospects, the Asia Pacific UV LED market faces significant restraints, primarily stemming from high initial costs and limited economies of scale. Compared to traditional mercury-based UV lamps, UV LEDs involve higher production expenses due to the complex materials and fabrication processes required, particularly for deep UV (UVC) variants. Gallium nitride (GaN), aluminum gallium nitride (AlGaN), and sapphire substrates—key components in UV LED manufacturing—are costly and often sourced from a limited number of suppliers, adding to price pressures. Furthermore, the lack of standardized manufacturing practices and relatively lower yield rates in producing high-efficiency UV LEDs contribute to pricing disparities. In countries like Thailand and the Philippines, where municipal budgets for sanitation and healthcare remain constrained, decision-makers are reluctant to invest in these premium-priced systems without clear short-term returns.

Performance Limitations and Technological Immaturity

Another critical restraint affecting the Asia Pacific UV LED market is the current limitations in performance and technological maturity, especially for deep UV-C LEDs. Despite advancements, many UV LED products still struggle with achieving sufficient optical output, wall-plug efficiency (WPE), and operational lifetimes necessary to fully replace conventional UV sources in demanding applications. According to the Solid-State Lighting Program under the U.S. Department of Energy, even as of 2023, most commercial UVC LEDs operate at output powers below 100 mW per chip, necessitating arrays of multiple LEDs to achieve effective disinfection. This increases system complexity and cost, especially in large-scale industrial and municipal applications. In regions like Indonesia and Vietnam, where ambient temperatures are consistently high, thermal management issues further degrade UV LED performance, reducing reliability and lifespan. Also, inconsistent product quality and lack of uniform testing standards across manufacturers create confusion among end-users.

MARKET OPPORTUNITIES

Rising Demand for Sanitization in Consumer Electronics

A major growth opportunity for the Asia Pacific UV LED market lies in its increasing integration into consumer electronics for hygiene and sanitization purposes. As awareness about personal health and cleanliness grows particularly post-pandemic, there is a surge in demand for home appliances and personal gadgets embedded with UV disinfection features. Products such as UV-equipped smartphones, laptop keyboards, toothbrush sanitizers, baby bottle sterilizers, and smart air purifiers are gaining popularity across urban markets in China, South Korea, and Japan. Companies like Xiaomi, LG, and Panasonic have introduced UV-C LED integrated devices into their product portfolios, capitalizing on this trend.

Integration in Semiconductor Manufacturing Equipment

The semiconductor manufacturing industry in the Asia Pacific region presents another promising avenue for UV LED market growth, particularly in lithography, inspection, and cleaning processes. UV LEDs, especially in the deep ultraviolet spectrum, are being explored as alternatives to traditional excimer lasers and mercury lamps for specific precision applications. Their ability to provide localized illumination, reduced heat generation, and compatibility with automated systems makes them suitable for wafer inspection, photoresist curing, and surface cleaning in cleanroom environments. South Korea and Taiwan, two global hubs for semiconductor fabrication, are leading the adoption of UV-C LEDs in front-end manufacturing tools. In particular, UV LEDs are being utilized in photolithography steppers and defect detection scanners, where wavelength precision and stability are crucial. Additionally, Japanese firms such as Canon and Nikon are incorporating UV LEDs into next-generation metrology systems to enhance yield rates and reduce contamination risks.

MARKET CHALLENGES

Fragmented Regulatory Framework Across Countries

One of the key challenges facing the Asia Pacific UV LED market is the fragmented and inconsistent regulatory environment across different countries in the region. Unlike mature markets in North America and Europe, where standardized guidelines govern UV device usage, labeling, safety certifications, and emission limits, Asia Pacific lacks unified regulatory frameworks. This creates uncertainty for manufacturers and delays product approvals, hindering cross-border trade and scalability. Conversely, in countries like Indonesia and the Philippines, regulations are either outdated or non-existent, leading to inconsistent product quality and market fragmentation. According to an analysis by McKinsey & Company, regulatory divergence in the Asia Pacific region can increase compliance costs for multinational companies by up to 20%. In addition, the absence of harmonized electromagnetic compatibility (EMC) and photobiological safety norms, such as those outlined under IEC 62471, creates barriers for original equipment manufacturers (OEMs) integrating UV LEDs into diverse applications.

Supply Chain Constraints and Material Shortages

The Asia Pacific UV LED market is also grappling with supply chain vulnerabilities and raw material shortages that threaten sustained growth. The production of high-performance UV LEDs relies heavily on specialized semiconductor materials such as aluminum gallium nitride (AlGaN) substrates, silicon carbide wafers, and rare-earth dopants. However, disruptions in the global supply chain—exacerbated by geopolitical tensions, export restrictions, and pandemic-related delays—have led to intermittent shortages and price volatility. China, which dominates the global supply of rare earth elements, has imposed export quotas on several critical materials used in optoelectronic components, directly impacting downstream UV LED manufacturing. Moreover, the concentration of wafer fabrication facilities in a few nodes, primarily in Japan and South Korea, leaves the industry exposed to regional shocks such as natural disasters or logistical disruptions. Small and medium-sized enterprises (SMEs) in countries like Malaysia and Vietnam, which rely on imported components, face higher procurement costs and inventory instability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Application, End-Use, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Halma Plc, Koninklijke Philips N.V., Hoenle Group, LG Electronics Inc., Nordson Corporation, SemiLEDs Corporation, Heraeus Holding GmbH, Crystal IS Inc., Seoul Viosys Co., Ltd, and Sensor Electronics Technology Inc. |

SEGMENTAL ANALYSIS

By Technology Insights

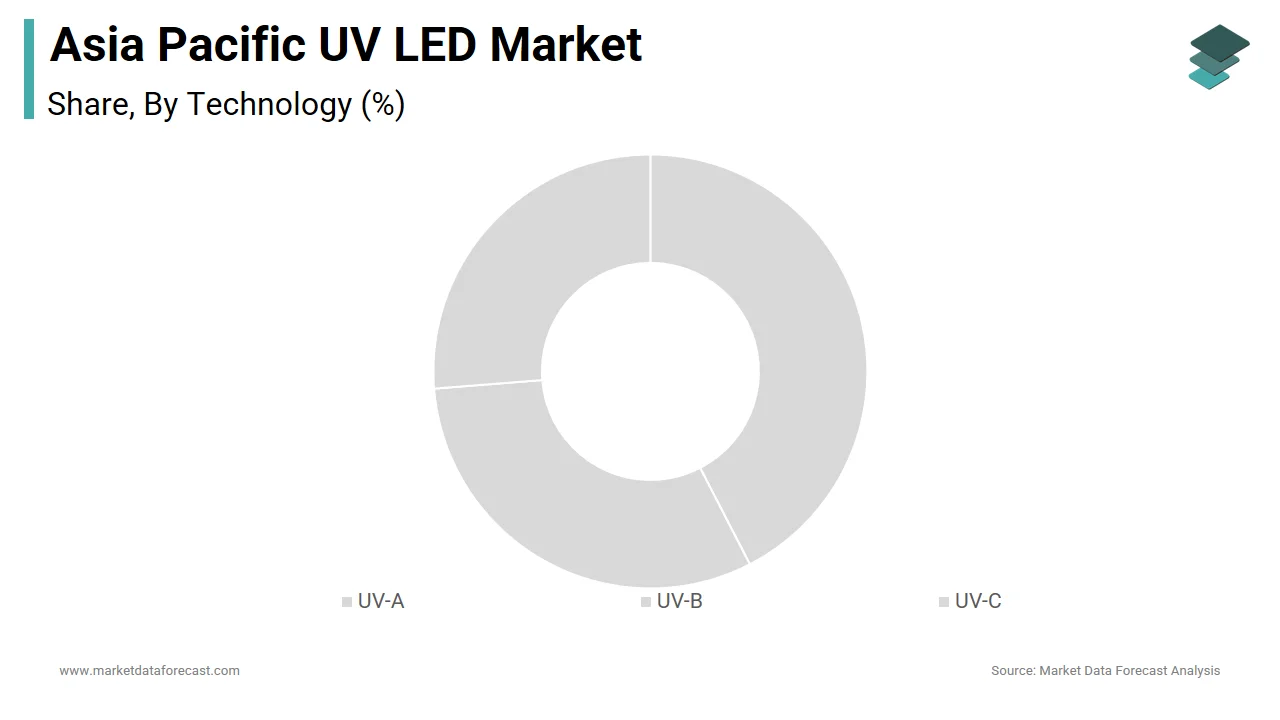

The UV-A LEDs dominated the Asia Pacific UV LED market by accounting for 48.7% of total revenue in 2025. This segment's growth is primarily attributed to its widespread use across industrial curing applications, fluorescence detection, and photopolymerization processes. UV-A LEDs offer optimal wavelengths between 315–400 nm, making them highly effective in curing adhesives, coatings, and inks used in electronics, automotive, and printing industries. Japan, with companies like Nitto Denko and Hamamatsu Photonics, continues to advance UV-A integration into precision manufacturing and sensing technologies. South Korea has also seen a surge in adoption within semiconductor packaging lines.

The UV-C LED segment is projected to register the highest growth in the Asia Pacific UV LED market, expanding at a CAGR of 24.7% from 2026 to 2034. This rapid expansion is driven by increasing demand for chemical-free disinfection solutions in water purification, air treatment, and surface sterilization, particularly in healthcare and food & beverage sectors. Meanwhile, Japan’s Ministry of the Environment has actively promoted UV-C LEDs as part of its Green Growth Strategy, aiming to phase out mercury-containing lighting by 2030.

By Application Insights

Industrial and UV curing applications collectively represented the largest application area in the Asia Pacific UV LED market by capturing 39.9% of total revenue in 2023. This dominance stems from the extensive use of UV-A LEDs in adhesive bonding, ink drying, and conformal coating processes within high-end electronics, automotive, and printed circuit board manufacturing. China remains the epicenter of this demand, with a large number of manufacturing units adopting UV curing systems in electronics assembly and flat panel display production. According to the China Printing Machinery Industry Association, UV curing equipment sales in the country rose by 11% year-on-year in 2023. South Korea’s semiconductor industry is another major driver, leveraging UV LEDs for precise resist curing and wafer-level packaging. In addition, Japanese manufacturers such as Mitsubishi Electric and Tokyo Electron have integrated UV LEDs into factory automation tools to enhance production throughput and reduce energy consumption.

Disinfection stands out as the fastest-growing application segment in the Asia Pacific UV LED market, recording a CAGR of 26.3% during the forecast period. This growth is being fueled by heightened awareness regarding hygiene and infection control across municipal infrastructure, commercial buildings, and healthcare facilities. Moreover, the hospitality sector in Singapore is increasingly deploying UV-LED-equipped cleaning carts and air purifiers in hotel rooms and common areas. These developments emphasize the growing reliance on UV LED disinfection technologies, positioning it as the most rapidly evolving application category in the region.

By End Use Insights

The industrial end-use segment holds the largest share of the Asia Pacific UV LED market by contributing 57.5% of total revenues in 2025. This dominance is largely driven by the integration of UV LEDs into high-tech manufacturing processes such as photolithography, surface curing, and optical inspection across electronics, semiconductors, and automotive industries. China leads this segment, with a significant portion of global printed circuit board (PCB) production occurring within its borders. South Korea’s OLED manufacturing boom has further amplified UV LED adoption, especially in alignment and coating applications. Japanese firms such as Canon and Nikon have embedded UV LEDs into next-generation lithography machines, enhancing precision and reducing thermal damage.

The residential segment is experiencing the highest growth in the Asia Pacific UV LED market, with a CAGR of 23.8% anticipated between 2025 and 2033. This surge is propelled by rising consumer interest in personal health and hygiene, leading to increased adoption of UV LED-equipped home appliances such as air purifiers, water purifiers, and handheld sanitizers. E-commerce platforms like Flipkart and Amazon India reported a year-over-year increase in UV appliance sales during the same period. Similarly, in Indonesia and the Philippines, where waterborne diseases remain a public health concern, consumers are opting for compact and affordable UV purifiers. South Korea has witnessed a rise in UV-embedded smart home devices, including refrigerators and hand dryers.

COUNTRY LEVEL ANALYSIS

China held the top position in the Asia Pacific UV LED market, commanding a market share of 34.5% in 2025. As the world’s largest manufacturing hub, China drives demand across industrial, medical, and consumer electronics segments. The country’s robust investment in semiconductor fabrication, PCB production, and green technology initiatives has accelerated UV LED adoption. Government policies such as the "Made in China 2025" initiative have encouraged the replacement of mercury lamps with UV LEDs in large-scale manufacturing. Chinese firms like Foshan Nationstar Optoelectronics and HC Semitek have significantly scaled their UVC LED production capacities. Furthermore, the Ministry of Ecology and Environment has mandated the phase-out of mercury-based UV lamps in municipal water treatment plants by 2025, reinforcing China’s leadership in shaping the regional UV LED ecosystem.

Japan maintains a strong foothold due to its advanced R&D capabilities, early adoption of UV LED technology, and presence of leading manufacturers such as Nichia Corporation, Panasonic, and Ushio Inc. According to the Japan Electronics and Information Technology Industries Association (JEITA), UV LED exports from Japan exceeded USD 450 million in 2023, with a significant portion directed toward medical device and semiconductor manufacturing clients in other APAC countries. Japan’s Ministry of Economy, Trade and Industry (METI) has actively supported the development of UVC LEDs under its Green Innovation Fund, allocating over JPY 120 billion towards related research and pilot projects since 2021. Hospitals in Tokyo and Osaka have widely adopted UV-C LED disinfection robots, while consumer electronics giant Sharp has launched UV-LED embedded home appliances.

South Korea contributes majorly to the Asia Pacific UV LED market, driven by its prominence in semiconductor manufacturing, OLED production, and advanced healthcare systems. The country leverages UV LEDs for precision applications in electronic material processing, photolithography, and hospital sanitation protocols. Major conglomerates such as Samsung Electro-Mechanics and LG Innotek have integrated UV LEDs into sensor modules and inspection equipment for chip fabrication.

India is distinguished by escalating demand in water purification, healthcare, and consumer electronics. With millions lacking access to potable water, the government’s push for mercury-free disinfection technologies has catalyzed UV LED adoption. Domestic brands like Kent RO Systems and Eureka Forbes are increasingly incorporating imported UV LEDs into their premium filtration models. Moreover, consumer electronics startups such as ViroGuard and CleanSpace are commercializing UV-LED sanitization chambers for phones, masks, and baby products.

Singapore is leveraging its status as a tech-forward city-state and regional innovation center. Despite its small geographical footprint, Singapore plays a disproportionate role in driving high-value UV LED applications in biomedical, pharmaceutical, and smart building sectors. Given its strong emphasis on sustainability and digital infrastructure, Singapore serves as a strategic testbed for next-generation UV LED deployments across the Asia Pacific region.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC UV LED market profiled in this report are Halma Plc, Koninklijke Philips N.V., Hoenle Group, LG Electronics Inc., Nordson Corporation, SemiLEDs Corporation, Heraeus Holding GmbH, Crystal IS Inc., Seoul Viosys Co., Ltd, and Sensor Electronics Technology Inc.

TOP LEADING PLAYERS IN THE MARKET

Nichia Corporation (Japan)

Nichia is a pioneering force in the global and regional UV LED market, recognized for its early advancements in high-efficiency UVC LEDs. As a subsidiary of Nitto Denko Group, Nichia has consistently pushed the boundaries of UV LED performance, particularly in healthcare, water purification, and industrial applications. In the Asia Pacific region, the company plays a dominant role in supplying UV-A and UV-C LEDs to manufacturers across Japan, South Korea, and China.

Seoul Semiconductor Co., Ltd. (South Korea)

Seoul Semiconductor is a major player in the Asia Pacific UV LED landscape, known for its broad portfolio of UV-A and UV-C LEDs tailored for industrial curing, sensing, and sterilization applications. The company has aggressively expanded its UV LED product lines through subsidiaries such as Seoul Viosys, which focuses on deep UV technology. In the Asia Pacific region, Seoul Semiconductor collaborates with electronics and medical device manufacturers to embed UV LEDs into diverse end-use products. Its strong local presence and focus on design-in opportunities have made it a preferred supplier among regional OEMs seeking compact, reliable UV solutions.

Foshan Nationstar Optoelectronics Co., Ltd. (China)

Foshan Nationstar is a leading Chinese manufacturer driving domestic and regional growth in UV LED adoption. It specializes in cost-effective UV-A and UV-C LED solutions for industrial, commercial, and consumer applications. In the Asia Pacific market, the company has capitalized on China’s manufacturing ecosystem to scale production and support downstream integration. Foshan Nationstar actively participates in government-backed clean technology initiatives, enhancing its visibility in municipal water treatment and public health infrastructure projects. Its competitive pricing and localized service model make it a key contributor to expanding UV LED accessibility in emerging markets across Southeast Asia.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading companies in the Asia Pacific UV LED market is product innovation and technology differentiation. Companies are investing heavily in research and development to enhance the efficiency, output, and durability of UV LEDs, particularly in the deep ultraviolet spectrum. By introducing high-performance products tailored for specific applications like disinfection, curing, and sensing, firms aim to capture niche customer segments and maintain a technological edge over competitors.

Another crucial approach is strategic partnerships and collaborations. Many players are forming alliances with system integrators, original equipment manufacturers, and government agencies to accelerate the deployment of UV LED-based solutions. These partnerships enable faster market entry, facilitate regulatory compliance, and encourage broader industry adoption. Collaborations with academic institutions also help companies refine their offerings and drive application-specific improvements.

Lastly, expanding manufacturing capabilities and supply chain localization serves as a core growth tactic. To meet rising demand and reduce dependency on imported components, key participants are setting up dedicated UV LED fabrication units within the region. This not only improves cost efficiencies but also ensures quicker response to market needs and enhances overall competitiveness.

COMPETITION OVERVIEW

The competition in the Asia Pacific UV LED market is intensifying as both established players and emerging firms vie for dominance across multiple application sectors. With increasing awareness about hygiene and sustainability, coupled with supportive regulatory shifts, the market has become highly dynamic. Japanese companies lead in technology development and precision applications, while South Korean firms emphasize integration into electronics and medical devices. China remains the largest production and consumption hub, with domestic manufacturers rapidly scaling up to meet both local and export demand. A growing number of startups are also entering the space, offering innovative designs and alternative business models. The competition is further fueled by ongoing investments in R&D, vertical integration efforts, and cross-border collaborations aimed at strengthening market positioning.

RECENT MARKET DEVELOPMENTS

- In February 2025, Nichia Corporation launched a new line of high-output UVC LEDs specifically designed for air purification and surface disinfection in hospitals and commercial buildings across Japan and South Korea. This move aimed to expand its footprint in the healthcare segment and reinforce its leadership in deep UV technology.

- In June 2025, Seoul Semiconductor announced a strategic partnership with a leading Singapore-based medical device manufacturer to integrate its UV LED modules into sterilization equipment for hospital use. The collaboration was intended to strengthen its presence in the ASEAN region and gain access to fast-growing healthcare infrastructure projects.

- In October 2025, Foshan Nationstar Optoelectronics inaugurated a new UV LED production facility in Guangzhou, focusing on scalable manufacturing of UV-A and UV-C diodes for industrial and residential applications. This expansion was part of its broader effort to serve domestic demand and increase exports to Southeast Asian countries.

- In January 2025, LG Innotek entered into an R&D agreement with a South Korean biotech firm to develop compact UV LED systems for laboratory and pharmaceutical use. The initiative was designed to tap into the growing demand for precision sterilization in life sciences applications across the Asia Pacific region.

- In March 2025, Panasonic introduced a series of UV LED-equipped home appliances, including refrigerators and air purifiers, targeting middle-class consumers in India and Indonesia. This product rollout reflected its strategy to penetrate the residential sector and capitalize on rising health consciousness in emerging markets.

MARKET SEGMENTATION

This Asia Pacific UV LED market research report is segmented and sub-segmented into the following categories.

By Technology

- UV-A

- UV-B

- UV-C

By Application

- Industrial

- UV Curing

- Lithography

- Medical and Scientific

- Phototherapy

- Sensing

- Equipment Sterilization

- Sterilization

- Disinfection

- Deodorization

- Security

- Counterfeit Detection-Money & ID

- Forensic Application

- Others

By End Use

- Industrial

- Commercial

- Residential

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What factors are driving the Asia Pacific UV LED market?

The Asia Pacific UV LED market is driven by rising demand for energy-efficient lighting, growth in sterilization and disinfection applications, and expanding electronics and healthcare industries.

2. What challenges does the Asia Pacific UV LED market face?

The Asia Pacific UV LED market faces challenges such as high initial costs, limited awareness in some sectors, and technical barriers in achieving higher efficiency and longer lifespan for UV LEDs.

3. What opportunities exist in the Asia Pacific UV LED market?

Opportunities in the Asia Pacific UV LED market include advancements in water and air purification, increasing adoption in medical devices, and expansion of UV curing in printing and manufacturing.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com