Asia Pacific PET Packaging Market Research Report – Segmented By Packaging Type (Rigid Packaging, Flexible Packaging),Form, Pack Type, Filling Technology, End User, and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2026 to 2034

Market Size, 2025

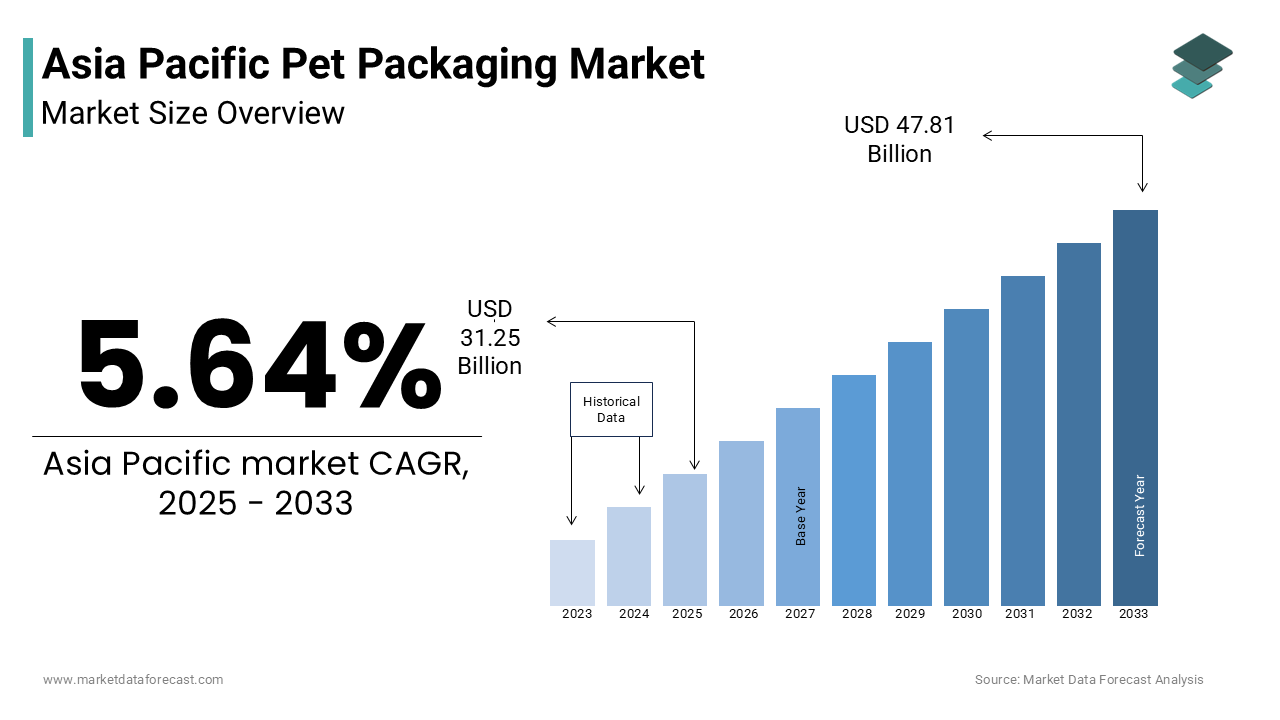

$31.25 BnMarket Estimate, 2026

$32.96 BnMarket Forecast, 2034

$50.43 BnCAGR, 2026–2034

5.46%Asia Pacific PET Packaging Market Report Summary

The Asia Pacific PET packaging market was valued at USD 31.25 billion in 2025, is estimated to reach USD 32.96 billion in 2026, and is projected to reach USD 50.43 billion by 2034, growing at a CAGR of 5.46% during the forecast period from 2026 to 2034. The growth of the Asia Pacific PET packaging market is driven by rapid urbanization, rising demand for packaged food and beverages, and the expansion of the textile and apparel industry. Increasing consumption of bottled water, soft drinks, and ready-to-eat products, along with the region’s dominance in polyester fiber production, is further fueling market growth. Moreover, the growing focus on sustainability, advancements in recycling technologies, and the adoption of circular economy practices are strengthening the demand for PET and recycled PET materials across the region.

Key Market Trends

-

Rising demand for PET packaging is driven by the growth of bottled beverages and packaged food consumption.

-

Increasing use of PET in the textile industry for polyester fiber production across major Asian economies.

-

Growing adoption of recycled PET (rPET) and circular economy practices to meet sustainability goals.

-

Expansion of chemical recycling technologies to process complex plastic waste streams.

-

Increasing development of bio-based PET and sustainable polymer alternatives.

Segmental Insights

- Based on packaging type, the rigid packaging segment was the largest and held a significant share of the Asia Pacific PET packaging market in 2025. The segment’s dominance is attributed to the extensive use of PET bottles and containers in beverages, food, and household products.

- Based on form, the amorphous PET segment accounted for a major share of the Asia Pacific PET packaging market in 2025. The dominance of this segment is driven by its clarity, lightweight nature, and suitability for beverage bottles and food packaging applications.

- Based on end user, the beverages industry segment was the largest, occupying a prominent share of the Asia Pacific PET packaging market in 2025. The dominance of this segment stems from the high consumption of bottled water, carbonated soft drinks, and juices across the region.

Regional Insights

The Asia Pacific PET packaging market is witnessing strong growth across major economies, supported by large population bases, industrial expansion, and increasing consumer demand for packaged goods.

- China was the largest contributor, accounting for 45.4% of the Asia Pacific PET packaging market share in 2025, driven by its massive manufacturing base, dominant textile industry, and high consumption of bottled beverages.

- India is emerging as a high-growth market due to rapid urbanization, expanding retail infrastructure, and increasing demand for packaged food and beverages.

- Japan continues to perform strongly, supported by advanced recycling infrastructure, high-quality manufacturing standards, and strong adoption of recycled PET materials.

- South Korea is witnessing notable growth, driven by technological advancements, regulatory support for recycled plastics, and strong demand from the automotive and electronics industries.

- Indonesia is also emerging as a key growth market due to its large population, rising middle class, and increasing consumption of packaged products.

Competitive Landscape

The Asia Pacific PET packaging market is characterized by the presence of global petrochemical companies and regional manufacturers competing through scale, innovation, and sustainability initiatives. Leading players are focusing on vertical integration, expansion of recycling capacities, and development of advanced PET materials to strengthen their market position. Investments in chemical recycling, bio-based PET, and strategic partnerships with brand owners are shaping the competitive landscape. Prominent players in the Asia Pacific PET packaging market include Indorama Ventures Public Company Limited, Reliance Industries Limited, Far Eastern New Century Corporation, Toray Industries Inc., Zhuhai Zhongfu Enterprise Co., Ltd., SCG Packaging Public Company Limited, Uflex Ltd., Ester Industries Ltd., and Dynapack Asia.

Asia Pacific PET Packaging Market Size

The Asia Pacific PET packaging market size was valued at USD 31.25 billion in 2025 and is anticipated to reach USD 32.96 billion in 2026, from USD 50.43 billion by 2034, growing at a CAGR of 5.46% during the forecast period from 2026 to 2034.

PET packaging encompasses the production, distribution, and consumption of polyethylene terephthalate resin, which is a versatile thermoplastic polymer essential for packaging textiles and engineering applications. This region serves as the global epicentre for both manufacturing capacity and end-user demand, driven by rapid industrialization and a burgeoning middle class. The material is critical for producing beverage bottles, food containers, synthetic fibers, and films due to its clarity, strength, and recyclability. According to the United Nations Economic and Social Commission for Asia and the Pacific, the region has a very large population that creates immense baseline demand for packaged goods and consumer products that rely on PET. As per the World Bank, urbanization in developing Asian nations is expected to increase significantly by 2030, which is fostering a shift toward modern retail formats where plastic packaging is predominant. The textile sector also remains a massive consumer, with the International Textile Manufacturers Federation indicating that Asia is the leading region in global polyester fiber production, which is derived from PET. Environmental regulations are increasingly shaping the landscape, pushing manufacturers toward circular economy models. As per the Asian Development Bank, waste management infrastructure is improving across major economies, facilitating higher recycling rates. This dynamic interplay between massive consumption, industrial output, and sustainability mandates defines the current trajectory of the PET industry in the Asia Pacific region.

MARKET DRIVERS

Explosive Growth in the Bottled Beverage and Packaged Food Sector

The rising demand for bottled water, soft drinks, and ready-to-eat food items stands is primarily propelling the growth of the Asia Pacific PET packaging market forward. Rapid urbanization and changing lifestyle patterns have led consumers to prioritize convenience and hygiene, driving a massive shift away from loose goods toward pre-packaged solutions. According to the International Council of Beverages Associations, the Asia Pacific region has become a leading consumer of bottled water, necessitating vast quantities of PET resin for bottle production. Furthermore, the expansion of modern retail chains and e-commerce platforms has accelerated the need for durable, lightweight, and transparent packaging that ensures product visibility and shelf life. As per the Food and Agriculture Organization, the processed food market in Southeast Asia has shown consistent growth in recent years, with PET trays and containers being the preferred choice for manufacturers due to their barrier properties against moisture and oxygen. The rising disposable income in emerging economies like India and Vietnam has further amplified this trend, as consumers increasingly purchase branded beverages and snacks. According to Nielsen IQ, sales of single-serve beverages in rural Asian markets have expanded, highlighting the penetration of PET packaging into previously untapped demographic segments. This relentless consumption pattern ensures a steady and growing offtake of virgin and recycled PET materials across the continent.

Robust Expansion of the Textile and Apparel Industry

The thriving textile and apparel sector in Asia Pacific acts as a formidable driver for the Asia Pacific PET packaging market, specifically through the consumption of polyester fiber which is synthesized from PET resin. The region dominates global textile manufacturing, supplying fast fashion brands and domestic markets with synthetic fabrics that offer durability, wrinkle resistance, and cost efficiency. According to the International Textile Manufacturers Federation, China, India, and Vietnam collectively account for a significant share of global polyester fiber production, creating a massive internal demand loop for PET feedstock. The rise of athleisure and performance wear has further boosted demand, as polyester blends are essential for moisture-wicking and stretchable fabrics used in sportswear. As per the World Trade Organization, textile exports from Asia Pacific nations have reached substantial levels, with synthetic fibers comprising the largest share of this volume. Additionally, the growing domestic middle class in countries like Indonesia and Thailand is purchasing more clothing, driving local consumption of polyester garments. According to the Asian Development Bank, household expenditure on clothing and footwear in developing Asia is expected to continue growing, directly correlating with increased PET resin requirements for fiber spinning. The versatility of PET allows it to be blended with cotton or other natural fibers, expanding its application scope beyond pure synthetics and securing its position as a foundational material for the regional textile economy.

MARKET RESTRAINTS

Stringent Environmental Regulations and Single-Use Plastic Bans

The implementation of rigorous environmental policies and outright bans on single-use plastics across various Asia Pacific nations poses a significant restraint on the growth of the virgin Asia Pacific PET packaging market. Governments are increasingly recognizing the ecological damage caused by plastic waste, leading to legislative actions that restrict the production and use of certain PET items like bags, cutlery, and straws. According to the United Nations Environment Programme, multiple countries in the Asia Pacific region have enacted full or partial bans on specific single-use plastic products since 2020, forcing manufacturers to seek alternative materials such as paper, glass, or biodegradable polymers. In India, the government enforced a comprehensive ban on identified single-use plastic items in 2022, which disrupted supply chains and reduced demand for specific grades of PET resin. As per the Centre for Science and Environment, compliance with these varying national regulations increases operational costs for producers who must adapt their product lines and invest in compliant alternatives. Furthermore, extended producer responsibility schemes are mandating that companies bear the cost of collecting and recycling their packaging, which is adding financial pressure. According to the World Resources Institute, compliance costs for plastic manufacturers in Southeast Asia have risen due to new waste management levies. These regulatory headwinds create uncertainty for long-term investment in virgin PET capacity and compel the industry to pivot rapidly toward sustainable practices or face penalties and market exclusion.

Volatility in Crude Oil and Feedstock Prices

The inherent dependence of PET production on crude oil and its derivatives, specifically purified terephthalic acid and monoethylene glycol, which is exposes the market to severe price volatility that constrains profitability and demand stability and further hindering the regional market expansion. Since PET is a petrochemical product, fluctuations in global energy markets directly impact manufacturing costs, which is making it difficult for producers to maintain consistent pricing for downstream customers. According to the International Energy Agency, crude oil prices have experienced significant swings due to geopolitical tensions and supply chain disruptions, causing erratic cost structures for Asian petrochemical plants. As per Platts energy information service, the price of paraxylene, a key precursor for PTA, has surged in certain quarters, which is squeezing margins for PET converters who struggle to pass these costs onto price-sensitive consumers in developing markets. This volatility discourages long-term contracts and leads to inventory hoarding or demand destruction when prices peak. According to the Asian Petrochemical Industry Conference, small and medium-sized converters in the region have faced declines in operating rates during periods of extreme feedstock price instability. Furthermore, the lack of hedging instruments in some emerging Asian markets exacerbates the risk and this is leaving local manufacturers vulnerable to global market shocks. This economic unpredictability hampers steady market expansion and forces many buyers to switch to cheaper, albeit less functional and alternative packaging materials

MARKET OPPORTUNITIES

Advancement in Chemical Recycling and Circular Economy Initiatives

The transition toward a circular economy offers a promising opportunity for the Asia Pacific PET packaging market through the adoption of advanced chemical recycling technologies that can process contaminated and mixed plastic waste into high-quality rPET. Unlike mechanical recycling, which often degrades polymer quality, chemical recycling breaks PET down to its molecular building blocks, allowing for the production of food-grade recycled resin suitable for bottling. According to the Ellen MacArthur Foundation, plastic recycling in Asia remains limited, indicating a vast untapped resource that can be converted into valuable feedstock. As per the Japan Chemical Industry Association, investments in depolymerization facilities in Japan and South Korea are expected to increase significantly, which is enabling the region to meet growing corporate commitments for recycled content. Major brands are increasingly demanding rPET for their packaging, creating a premium market segment. According to the Global PET Bottle Recycling Initiative, demand for food-grade rPET in Asia Pacific is projected to grow steadily, which is outpacing the supply of mechanically recycled material. Governments are also supporting this shift, with the Chinese government including high-value plastic recycling in its 14th Five-Year Plan and this is offering subsidies for technology upgrades. By leveraging these technologies, the industry can reduce reliance on virgin fossil feedstocks, comply with strict sustainability mandates, and unlock new revenue streams from waste valorisation.

Innovation in Bio-Based PET and Sustainable Polymer Blends

The development and commercialization of bio-based PET, derived from renewable resources such as sugarcane and corn offer a significant opportunity in the Asia Pacific PET packaging market. This innovation allows manufacturers to reduce the carbon footprint of their packaging while maintaining the performance characteristics of conventional PET. According to the Bioplastics Council, global capacity for bio-based plastics is set to expand, with Asia Pacific poised to become a major production hub due to its abundant agricultural feedstock availability. As per the Thai Bioplastics Industry Association, Thailand and Indonesia are investing heavily in biorefineries to produce bio-monoethylene glycol, a key component for partially bio-based PET bottles. This shift aligns with the sustainability goals of multinational corporations operating in the region who are striving for carbon neutrality. According to the European Bioplastics association, bio-based PET is expected to capture a portion of the total PET market in Asia, driven by premium brand adoption in the beverage and cosmetics sectors. Furthermore, blending bio-based PET with traditional resin allows for a gradual transition without compromising supply stability. As per the Asian Productivity Organization, government incentives for green chemistry in countries like Malaysia and the Philippines are accelerating pilot projects. Embracing bio-based solutions enables the industry to future-proof its operations against fossil fuel depletion and tightening carbon regulations.

MARKET CHALLENGES

Inadequate Waste Collection Infrastructure and Low Recycling Rates

A critical challenge facing the Asia Pacific PET packaging market is the fragmented and often inadequate waste collection infrastructure, which results in low recycling rates and significant environmental leakage despite high consumption volumes. While consumption of PET is soaring, the systems required to collect, sort, and process post-consumer waste lag behind, particularly in developing nations and rural areas. According to the World Bank, solid waste collection in low-income Asian countries remains insufficient, with much of it ending up in open dumps or waterways. As per the Ocean Conservancy, several rivers in Asia are among the top contributors to global ocean plastic pollution, highlighting the severity of the leakage issue. This lack of efficient collection limits the availability of clean post-consumer PET flakes needed for recycling, forcing manufacturers to rely on virgin material or import waste, which is becoming increasingly restricted. According to the Global Alliance for Incinerator Alternatives, informal waste pickers handle a large share of recycling in some Asian cities, yet they lack the technology to process complex multi-layer PET packaging effectively. The disparity between high production capacity and poor end-of-life management creates a reputational risk for the industry and invites stricter regulatory crackdowns. Building robust formal collection networks requires massive capital investment and coordinated policy efforts that are currently slow to materialize across the diverse political landscapes of the region.

Complex Regulatory Fragmentation Across Diverse Jurisdictions

The Asia Pacific region comprises a vast array of countries with divergent regulatory frameworks regarding plastic production, usage, and disposal, which is creating a complex compliance landscape that challenges multinational PET producers and further challenging the regional market expansion. Each nation imposes different standards for food contact safety, recycled content mandates, and labeling requirements, which is making it difficult to standardize operations and supply chains across borders. According to the Asia-Pacific Economic Cooperation forum, the lack of harmonization in plastic regulations increases compliance costs for regional operators who must navigate distinct legal regimes. As per the Singapore National Environment Agency, while some nations like Singapore and Japan have advanced waste management laws, others in the Mekong region are still formulating basic plastic policies, leading to inconsistent enforcement and market uncertainty. This fragmentation hinders the establishment of a seamless regional circular economy for PET. According to the International Chamber of Commerce, conflicting definitions of what constitutes recyclable or compostable across Asian markets confuse consumers and complicate logistics for exporters. Furthermore, sudden policy shifts, such as unexpected import bans on plastic scrap, can disrupt supply chains overnight. As per the Asian Institute of Management, navigating this regulatory maze requires significant legal resources and local expertise, acting as a barrier to entry for smaller players and slowing down the adoption of uniform sustainability practices across the continent.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.46% |

| Segments Covered | By Packaging Type, Form, Pack Type, Filling Technology, End User and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC. |

| Market Leaders Profiled | Indorama Ventures Public Company Limited, Reliance Industries Limited, Far Eastern New Century Corporation, Toray Industries Inc., Zhuhai Zhongfu Enterprise Co., Ltd., SCG Packaging Public Company Limited, Uflex Ltd., Ester Industries Ltd., and Dynapack Asia. |

REGIONAL ANALYSIS

China PET Packaging Market Analysis

China emerged as the undisputed leader in the Asia Pacific PET packaging market by commanding 45.4% of the regional market share in 2025. The Chinese market is characterized by a fully integrated supply chain, from raw material production to downstream conversion, which is making it the global price setter for PET resin. The colossal scale of the Chinese textile industry that consumes more than half of the world's polyester fiber is creating an insatiable demand for PET feedstock, which is primarily driving the dominance of China in this regional market. According to the China National Textile and Apparel Council, the country produces massive volumes of chemical fibers, with polyester accounting for the majority. The second critical driver is the thriving beverage sector, where the rising middle class drives unprecedented consumption of bottled water and soft drinks. As per the China Beverage Industry Association, bottled water production in China has reached very high levels, requiring millions of tons of PET resin annually. Furthermore, the government's push for a circular economy has spurred investments in large-scale recycling infrastructure. According to the National Development and Reform Commission, China plans to increase its plastic waste recycling rate significantly by 2025, which will reshape the source type dynamics while maintaining overall market dominance. The sheer magnitude of both production and consumption ensures China remains the central pillar of the regional PET landscape.

India PET Packaging Market Analysis

India is a promising regional segment in the European market. The rapid economic growth and a young demographic that is driving a consumption boom in packaged goods and apparel are driving the Indian market growth. The Indian PET packaging market is defined by a transition from informal to organized retail, which is accelerating the adoption of branded PET packaging across urban and rural areas. A key driving factor is the explosive growth of the bottled water and beverage industry, fueled by health consciousness and inadequate tap water infrastructure in many regions. According to the Bureau of Indian Standards, the packaged drinking water market in India has grown rapidly, making it one of the fastest-growing segments globally and a major consumer of PET preforms. The second major driver is the robust textile and garment sector, which serves both domestic needs and export markets, relying heavily on polyester fibers. As per the Ministry of Textiles, India's polyester fiber production has increased, supported by government incentives like the Production Linked Incentive scheme that encourage local manufacturing. Additionally, the government's ban on certain single-use plastics has boosted demand for PET bottles as a preferred alternative for liquid packaging. According to the Plastic Waste Management Authority, the shift toward recyclable PET packaging has gained momentum, with major brands committing to higher recycled content. The combination of demographic dividends and policy support positions India as a high-growth engine for the regional PET market.

Japan PET Packaging Market Analysis

Japan accounted for a substantial share of the Asia Pacific PET packaging market in 2025. The Japanese market is unique due to its world-leading collection and recycling infrastructure, which creates a distinct dynamic where recycled PET commands a significant premium and market presence. The highly efficient separate collection system mandated by the Container and Packaging Recycling Law that ensures a steady supply of high-quality post-consumer PET flakes is propelling the growth of the Japan in the Asia-Pacific market. According to the Japan Container and Packaging Recycling Association, recycling rates for PET bottles in Japan consistently remain among the highest globally, fostering a closed-loop system that reduces reliance on virgin resin for certain applications. The second critical factor is the demand for high-performance engineering PET in the automotive and electronics sectors, where Japanese manufacturers lead in developing advanced composite materials. As per the Japan Petrochemical Industry Association, demand for engineering-grade PET in automotive components has grown, driven by the electrification of vehicles and the need for lightweight, heat-resistant parts. Furthermore, consumer awareness regarding sustainability is exceptionally high, pushing brands to adopt recycled PET bottles for premium products. According to the Ministry of the Environment, Japan aims to reduce single-use plastic waste significantly by 2030, further incentivizing the shift toward circular PET solutions. This focus on quality and sustainability defines Japan's specialized role in the regional market.

South Korea PET Packaging Market Analysis

South Korea is estimated to witness a prominent CAGR in the Asia Pacific PET packaging market during the forecast period. South Korea is notable for its advanced chemical industry and aggressive government policies promoting a circular economy. The South Korean market reflects a balance between strong domestic consumption and a sophisticated export-oriented manufacturing sector that demands high-specification PET materials. A major driving factor is the stringent regulatory framework that mandates increasing ratios of recycled content in plastic products, forcing producers to invest in advanced recycling technologies. According to the South Korea Ministry of Environment, the government has enforced rules requiring plastic manufacturers to include recycled material in their products, with targets set to rise further by 2030. The second pivotal factor is the robust demand from the electronics and automotive industries, which utilize engineering PET for high-durability components. As per the Korea Petrochemical Industry Association, exports of engineered PET compounds have grown, driven by global demand for lightweight automotive parts and durable electronic housings. Additionally, the popularity of convenience stores and ready-to-eat meals in Korean urban culture sustains high demand for clear PET food containers. According to the Korea Consumer Agency, sales of packaged fresh foods in PET trays have increased, reflecting changing dietary habits. The synergy between regulatory push and industrial pull ensures South Korea remains a key innovator and consumer in the PET value chain.

Indonesia Asia Pacific PET Packaging Market Analysis

Indonesia is predicted to showcase a notable CAGR in the Asia Pacific PET packaging market during the forecast period owing to its large population, rapid urbanization, and growing status as a manufacturing hub for textiles and beverages. The market status is characterized by high growth potential but faces challenges related to waste management infrastructure, creating a dichotomy between rising consumption and environmental concerns. The key driving factor is the burgeoning middle class which is increasingly adopting branded beverages and packaged foods, leading to a surge in PET bottle consumption. According to the Indonesian Bottled Water Manufacturers Association, bottled water sales in Indonesia have risen sharply, making it one of the largest markets in Southeast Asia. The second major driver is the expanding textile industry, which leverages Indonesia's competitive labor costs to become a major global supplier of polyester garments. As per the Indonesian Textile Association, polyester fiber imports and local production have increased to meet export orders from global fashion brands. Furthermore, the government has launched roadmaps to reduce marine plastic debris, which includes initiatives to improve PET collection rates and encourage the use of recycled materials. According to the Ministry of Marine Affairs and Fisheries, pilot projects for waste banks and recycling centers have been expanded to many cities, aiming to capture more post-consumer PET. Despite infrastructure gaps, the fundamental demand drivers position Indonesia as a critical growth market in the region.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific PET Packaging Market is shaped by a mix of global packaging giants and agile regional manufacturers striving to capture market share through innovation, localization, and sustainability initiatives. As pet ownership rises and consumers become more discerning about product quality and packaging aesthetics, companies are under pressure to offer differentiated, functional, and environmentally responsible packaging solutions. The market sees intense rivalry not only in pricing but also in design, material sourcing, and performance features, particularly among flexible packaging providers. Regulatory changes related to food safety and recyclability are further influencing competitive strategies, pushing firms to invest heavily in R&D and compliance measures. Additionally, the growth of e-commerce and private label pet brands is altering traditional supplier-buyer dynamics, encouraging packaging companies to engage directly with retailers and online platforms. This dynamic environment fosters both opportunity and challenge, where agility, innovation, and responsiveness to shifting consumer trends determine long-term success.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Asia Pacific PET Packaging Market include

- Indorama Ventures Public Company Limited

- Reliance Industries Limited

- Far Eastern New Century Corporation

- Toray Industries Inc.

- Zhuhai Zhongfu Enterprise Co., Ltd.

- SCG Packaging Public Company Limited

- Uflex Ltd.

- Ester Industries Ltd.

- Dynapack Asia

Top Players in the Asia Pacific PET Packaging Market

Indorama Ventures Public Company Limited

Indorama Ventures stands as a global leader in the PET industry with a massive integrated production footprint across the Asia Pacific region. The company operates numerous facilities that produce purified terephthalic acid and PET resin, serving diverse sectors from packaging to textiles. Recently Indorama Ventures has aggressively expanded its recycled PET capacity by acquiring recycling plants and partnering with major brands to secure feedstock supply chains. The firm actively invests in advanced chemical recycling technologies to produce food-grade recycled resin that meets stringent international safety standards. Its contribution to the global market includes setting benchmarks for sustainability through circular economy initiatives and reducing carbon emissions across its value chain. By focusing on innovation and operational excellence, Indorama Ventures strengthens its position as a preferred supplier for multinational corporations seeking reliable and eco-friendly polymer solutions throughout the dynamic Asian marketplace.

Reliance Industries Limited

Reliance Industries Limited dominates the Indian and broader Asian PET landscape as one of the largest producers of polyester and petrochemicals globally. The company leverages its vast refining capabilities to ensure a cost-effective and stable supply of raw materials for its world-scale PET manufacturing units. Recent strategic actions include significant investments in expanding production capacity and integrating recycled PET lines to cater to growing demand for sustainable packaging solutions. Reliance Industries actively collaborates with global brand owners to develop custom polymer grades that enhance performance and recyclability. Its contribution to the global market involves driving down costs through economies of scale while pioneering green chemistry initiatives such as bio-based PET development. The firm continues to strengthen its market presence by optimizing logistics networks and adopting digital technologies to improve efficiency and customer responsiveness across the rapidly evolving Asia Pacific region.

Toray Industries Inc

Toray Industries Inc is a premier Japanese manufacturer renowned for its high-performance PET films and engineering plastics that serve critical applications in electronics and automotive sectors. The company distinguishes itself through advanced material science research that delivers specialized PET products with superior thermal and mechanical properties. Recent efforts focus on developing sustainable film solutions using recycled content and bio-based feedstocks to align with global environmental goals. Toray Industries actively expands its production facilities in Southeast Asia to be closer to key customers in the electric vehicle and consumer electronics industries. Its contribution to the global market includes providing innovative materials that enable lightweighting and energy efficiency in modern transportation and devices. By fostering strong partnerships with downstream manufacturers and investing in next-generation recycling technologies, Toray Industries reinforces its leadership in the high-value segment of the Asia Pacific PET Packaging Market.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific PET Packaging Market primarily focus on vertical integration to secure steady supplies of raw materials like purified terephthalic acid and monoethylene glycol while controlling production costs. Companies invest heavily in expanding their recycled PET capacities to meet rising demand for sustainable packaging and comply with stricter environmental regulations across the region. Strategic partnerships with global brand owners and waste management firms enable manufacturers to establish closed-loop systems that ensure a consistent flow of high-quality post-consumer feedstock. Firms are increasingly adopting advanced chemical recycling technologies to produce food-grade recycled resin that complements traditional mechanical recycling methods. Expanding production facilities in emerging Southeast Asian nations allows participants to capitalize on growing domestic consumption and reduce logistics expenses. Manufacturers also prioritize research and development to create specialized PET grades for high-growth sectors such as electric vehicles and flexible electronics. Additionally, companies utilize digital supply chain tools to optimize inventory management and enhance responsiveness to fluctuating market demands throughout the diverse Asia Pacific landscape.

RECENT MARKET DEVELOPMENTS

- In March 2024, Amcor launched a new line of fully recyclable stand-up pouches specifically designed for premium pet food brands in Japan and South Korea, aiming to support regional sustainability commitments while enhancing shelf appeal and consumer convenience.

- In July 2023, Sonoco expanded its production facility in Shanghai to include a dedicated line for multi-layer flexible pet food packaging, reinforcing its ability to serve China’s growing demand for high-barrier, durable packaging solutions tailored for wet and dry pet foods.

- In November 2024, Huhtamaki, a major global packaging provider, entered into a joint venture with an Indian pet food manufacturer to co-develop compostable sachets for single-serve pet treats, aligning with the country’s increasing focus on plastic waste reduction and eco-conscious branding.

- In February 2023, UFlex established a new research and development center in Singapore focused on flexible pet packaging innovations, including oxygen barriers, resealable closures, and digital printing technologies aimed at improving product longevity and visual appeal.

- In September 2024, Constantia Flexibles introduced a range of lightweight, tamper-evident aluminum-laminated pouches for pet supplements in Australia, targeting the growing demand.

MARKET SEGMENTATION

This research report on the Asia Pacific PET Packaging Market is segmented and sub-segmented into the following categories.

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Form

- Amorphous PET

- Crystalline PET

By Pack Type

- Bottles and Jars

- Bags and Pouches

- Trays

- Lids/Caps and Closures

- Others

By Filling Technology

- Hot Fill

- Cold Fill

- Aseptic Fill

- Others

By End User

- Beverages Industry

- Bottled Water

- Carbonated Soft Drinks

- Milk and Dairy Products

- Juices

- Beer

- Others

- Household Goods Sector

- Food Industry

- Pharmaceutical Industry

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is driving the growth of the PET packaging market in Asia Pacific?

The key growth drivers include rising demand for packaged food and beverages, increasing urbanization, growing e-commerce, sustainability initiatives, and cost-effective lightweight packaging solutions.

What are the key trends in the Asia Pacific PET packaging market?

Key trends include a shift toward recyclable and sustainable packaging, lightweight and durable materials, adoption of rPET (recycled PET), and smart packaging innovations.

What is the future outlook for the PET packaging market in Asia Pacific?

The market is expected to grow steadily, driven by sustainability trends, increased consumption of ready-to-eat and on-the-go products, and rising awareness of eco-friendly packaging solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com