Global Bagels Market Size, Share, Trends & Growth Forecast Report By Type (Fresh and Frozen Bagels and Pre-Packaged Bagels), Application (Supermarkets, Food Service, Convenience Store and Others), And Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis (2026 to 2034)

Market Size, 2025

$5.88 BnMarket Estimate, 2026

$6.27 BnMarket Forecast, 2034

$10.52 BnCAGR, 2026–2034

6.68%Global Bagels Market Size

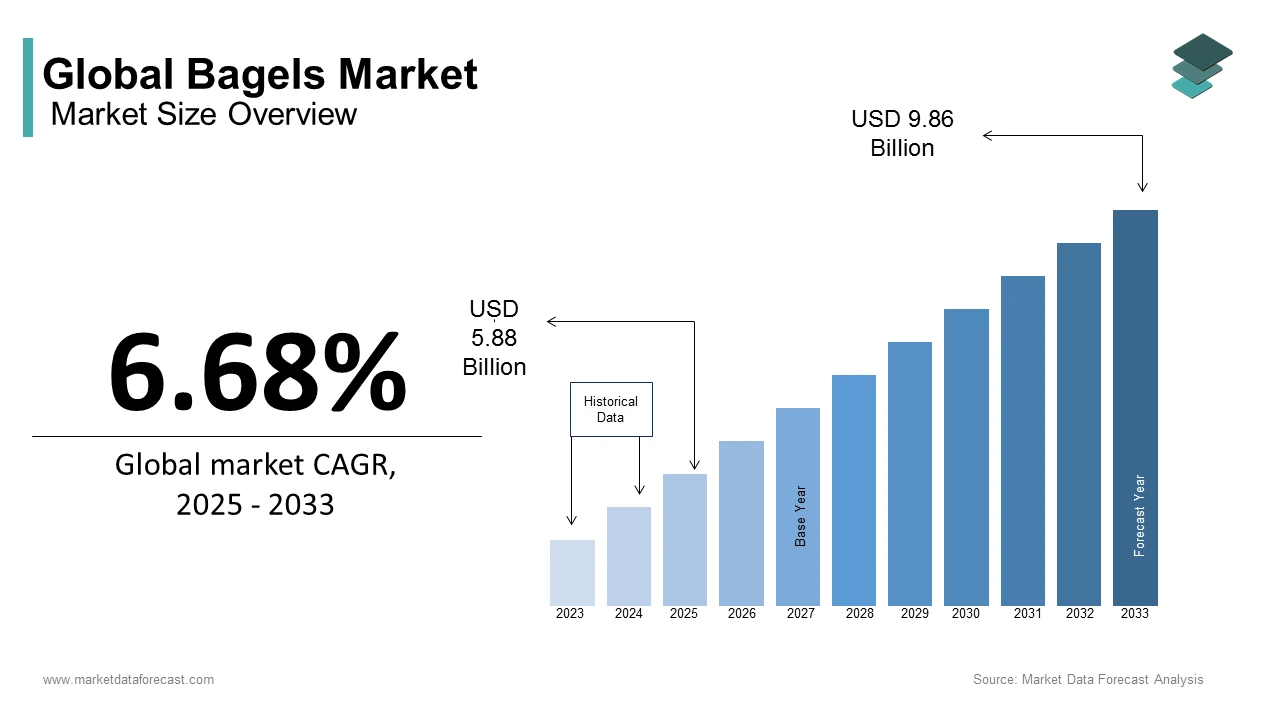

The global bagels market Size was calculated to be USD 5.88 billion in 2025 and is anticipated to be worth USD 10.52 billion by 2034 from USD 6.27 billion in 2026, growing at a CAGR of 6.68% during the forecast period.

Bagels are ring-shaped bread products characterized by their dense, chewy interior and crisp exterior. This culinary staple has evolved from a niche ethnic food to a mainstream breakfast and snack option globally. The definition includes various formulations such as traditional yeast-leavened bagels, gluten-free alternatives, and whole-grain variants. Consumers increasingly view bagels as a versatile canvas for both sweet and savory toppings, driving diverse consumption occasions. According to the United States Department of Agriculture, wheat flour consumption per capita in the United States remained stable at approximately 130 pounds annually in 2024, indicating sustained demand for wheat-based products. The cultural integration of bagels into daily dining routines is evident in the proliferation of specialized bakeries and café chains. In Canada, the popularity of artisanal baking has surged with local bakeries emphasizing traditional boiling and baking methods. As per Statistics Canada, the number of retail bakeries increased by 6% in 2024, reflecting consumer preference for fresh and locally produced goods. The market is defined by a shift towards premiumization, where the quality of ingredients and the authenticity of the preparation method command higher prices. Health-conscious consumers are also influencing the market by demanding options with reduced sodium or enhanced nutritional profiles. This dynamic landscape requires producers to balance tradition with innovation to meet evolving dietary preferences. The bagel serves not only as a food item but as a cultural symbol of convenience and comfort in urban lifestyles across North America and expanding into other regions.

MARKET DRIVERS

Versatility and Convenience in Modern Diets

The inherent versatility and convenience of bagels are fuelling their widespread adoption in modern diets, which is one of the key factors driving the growth of the European bagels market. Bagels can be consumed at any time of day and paired with a vast array of toppings ranging from cream cheese and smoked salmon to avocado and egg. This adaptability makes them an ideal choice for busy consumers seeking quick, yet satisfying meal options. According to the National Restaurant Association, 45% of consumers cited convenience as the most important factor in their food choices in 2024. The portability of bagels allows for easy consumption during commutes or at workspaces, aligning with the fast-paced nature of contemporary life. Furthermore, the rise of remote work has led to an increase in home-based breakfast preparations, where bagels offer a simple and customizable solution. According to the Bureau of Labor Statistics, the average American spends approximately 8 minutes on food preparation and clean-up for breakfast, as per 2024 data. This trend favors ready-to-eat or easily prepared items like bagels. Retailers have responded by offering pre-sliced and toasted varieties, further enhancing convenience. The ability of bagels to maintain freshness for several days also reduces food waste and appeals to household shoppers. This combination of culinary flexibility and ease of use ensures that bagels remain a staple in pantries and menus alike. The product’s neutral flavor profile allows it to complement both sweet and savory ingredients, making it appealing to a broad demographic spectrum.

Growing Preference for Artisanal and Premium Products

The growing consumer preference for artisanal and premium food products is significantly driving the bagels market expansion. Modern consumers are increasingly discerning about the quality and origin of their food, seeking authentic experiences and superior taste. Artisanal bagels made with high-quality flour, natural starters, and traditional boiling methods are perceived as healthier and more flavorful than mass-produced alternatives. According to Nielsen IQ, sales of premium bakery products in North America grew by 8% in 2024, outpacing the growth of standard bakery items. This shift is driven by millennials and Generation Z consumers who value transparency and craftsmanship in food production. Social media platforms play a crucial role in this trend by showcasing visually appealing artisanal bagels and unique flavor combinations. In major urban centers, the number of specialized bagel shops has increased by 12% since 2022. These establishments often source ingredients locally, supporting sustainable agriculture and community economies. The willingness of consumers to pay a premium for perceived quality and authenticity supports higher profit margins for producers. Additionally, the trend towards clean label products encourages manufacturers to eliminate artificial preservatives and additives. This demand for purity and quality drives innovation in ingredient sourcing and baking techniques. As consumers become more educated about food production, they seek out brands that align with their values of quality and sustainability. This cultural shift towards premiumization ensures sustained growth for artisanal bagel producers.

MARKET RESTRAINTS

Health Concerns Related to Refined Carbohydrates

Health concerns related to the consumption of refined carbohydrates and high glycemic index foods are hindering the growth of the global bagels market. Traditional bagels are primarily made from refined white flour, which can cause rapid spikes in blood sugar levels. This characteristic is increasingly scrutinized by health-conscious consumers and medical professionals alike. According to the Centers for Disease Control and Prevention, approximately 38 million people in the United States have diabetes as of 2024. This prevalent health condition drives many individuals to reduce their intake of high-carbohydrate foods. Furthermore, the rising incidence of obesity and metabolic syndrome has led to widespread adoption of low-carb and ketogenic diets. As per the International Food Information Council, 20% of consumers reported following a low-carb diet in 2024. These dietary trends directly conflict with the traditional composition of bagels. Although whole-grain and multigrain options exist, they often still contain significant amounts of carbohydrates. The perception of bagels as calorie-dense and nutritionally sparse discourages regular consumption among fitness enthusiasts and weight watchers. Nutritional labeling regulations also highlight the high sodium content in many commercial bagels, which can deter health-conscious buyers. The challenge for the industry lies in reformulating products to meet these health standards without compromising texture and taste. Until viable low-carb alternatives gain widespread acceptance and palatability, health concerns will continue to limit market expansion among specific demographic segments.

Volatility in Raw Material Prices

Volatility in raw material prices, particularly wheat and energy costs, is another substantial restraint on the bagels market. Wheat is the primary ingredient in bagel production, and its price is subject to fluctuations due to weather conditions, geopolitical tensions, and supply chain disruptions. According to the Food and Agriculture Organization of the United Nations, global wheat prices increased by 15% in 2024 due to adverse weather events in key producing regions. These cost increases directly impact the production expenses of bagel manufacturers who operate on thin margins. Energy costs are another critical factor, as baking is an energy-intensive process requiring significant electricity and gas for ovens and proofing equipment. In North America, industrial energy prices rose by 10% in 2024, as per the Bureau of Labor Statistics. These rising operational costs force manufacturers to either absorb the losses or pass them on to consumers through higher prices. Price increases can dampen consumer demand, particularly in price-sensitive segments. Small and independent bakeries are particularly vulnerable to these fluctuations as they lack the purchasing power of large corporations to negotiate better rates. Supply chain inconsistencies can also lead to production delays and inventory shortages, affecting product availability. The unpredictability of input costs makes long-term financial planning difficult for businesses. This economic pressure stifles innovation and expansion efforts as companies prioritize cost containment over growth initiatives.

MARKET OPPORTUNITIES

Expansion into Gluten-Free and Alternative Grain Segments

The expansion into gluten-free and alternative grain segments presents a significant opportunity for the bagels market. The prevalence of celiac disease and gluten sensitivity has created a dedicated consumer base seeking safe and delicious alternatives. According to the Celiac Disease Foundation, approximately 1 in 100 people worldwide, which includes roughly 3 million people in the United States, have celiac disease. Additionally, many consumers choose gluten-free diets for perceived health benefits, driving broader market demand. Manufacturers are innovating with flours such as almond, coconut, cassava, and chickpea to create bagels that mimic the texture and taste of traditional wheat versions. As per Mintel, launches of gluten-free bakery products increased by 18% in 2024. These innovations allow brands to tap into a high-growth niche with less competition than the saturated traditional segment. Alternative grains such as quinoa and spelt also appeal to health-conscious consumers looking for nutrient-dense options. The development of improved binding agents and fermentation techniques has enhanced the quality of gluten-free bagels, reducing the crumbly texture often associated with these products. Retailers are dedicating more shelf space to free-from categories, reflecting this growing demand. Online direct-to-consumer channels also provide an effective platform for reaching niche audiences. By diversifying their product portfolios to include these specialized options, companies can capture new revenue streams and enhance brand loyalty among health-focused consumers. This strategic shift aligns with broader trends towards personalized nutrition and dietary inclusivity.

Innovation in Flavor Profiles and Functional Ingredients

Innovation in flavor profiles and the incorporation of functional ingredients offer substantial opportunities for the global bagels market expansion. Consumers are increasingly seeking novel and exciting taste experiences beyond traditional plain or sesame bagels. Incorporating ingredients such as everything seasoning, jalapeño, cheddar, blueberries, and cinnamon raisin attracts diverse consumer preferences. According to the Specialty Food Association, sales of specialty baked goods with unique flavors grew by 10% in 2024. Furthermore, the integration of functional ingredients such as protein, fiber, probiotics, and vitamins transforms bagels into health-promoting snacks. Protein-enriched bagels appeal to fitness enthusiasts and those seeking satiety. As per the Global Wellness Institute, the functional food market is expanding rapidly, with consumers willing to pay a premium for added health benefits. Collaborations with chefs and food influencers can help launch trendy flavors that generate buzz and social media engagement. Limited edition releases create a sense of urgency and exclusivity, driving trial and repeat purchases. Seasonal flavors such as pumpkin spice in autumn or peppermint in winter align with holiday traditions and boost sales during specific periods. The use of natural colorants from vegetables and fruits enhances visual appeal while maintaining clean label standards. These innovations keep the product category fresh and relevant, attracting younger demographics who value experimentation. By continuously evolving their offerings, manufacturers can sustain consumer interest and drive growth in a mature market.

MARKET CHALLENGES

Intense Competition from Substitute Breakfast Items

Intense competition from substitute breakfast items is a major challenge to the bagel market. Consumers have a wide array of convenient breakfast options, including croissants, muffins, toast, oatmeal, and breakfast sandwiches. These alternatives often compete directly with bagels for share of stomach and wallet. According to the National Coffee Association, 65% of Americans drink coffee daily, often paired with a pastry or bread product. The rise of healthy breakfast trends such as smoothie bowls and yogurt parfaits further diverts consumption away from carbohydrate-heavy options. Fast food chains and café franchises aggressively promote their breakfast menus featuring proprietary items that may exclude traditional bagels. In the United States, the quick-service restaurant sector saw a 12% increase in breakfast sales in 2024, as per QSR Magazine. This competitive landscape forces bagel producers to constantly innovate and market their products effectively to maintain relevance. Price competition is also fierce, with private label brands offering lower-priced alternatives that erode brand loyalty. The perception of bagels as less healthy compared to options like oatmeal or fruit also limits their appeal among health-conscious consumers. Additionally, the saturation of the bakery market means that shelf space is highly contested. Retailers prioritize high-turnover items, which may disadvantage slower-moving specialty bagel varieties. Overcoming this competition requires strong branding and clear communication of unique value propositions.

Supply Chain Disruptions and Logistics Challenges

Supply chain disruptions and logistics challenges present ongoing difficulties for the bagels market. The perishable nature of fresh bagels necessitates efficient and reliable distribution networks to ensure product quality upon arrival. Any disruption in transportation due to labor strikes, fuel shortages, or extreme weather can lead to significant waste and stockouts. According to the American Trucking Associations, the trucking industry faced a shortage of 80,000 drivers in 2024, impacting delivery schedules. These logistical bottlenecks increase lead times and costs for manufacturers and retailers. The reliance on just-in-time inventory systems makes the supply chain vulnerable to unexpected delays. Furthermore, the complexity of sourcing diverse ingredients such as seeds, nuts, and dried fruits from multiple suppliers adds layers of risk. Geopolitical tensions and trade policies can affect the availability and cost of imported ingredients. In 2024, global shipping rates remained volatile, as per the Drewry World Container Index, affecting international supply chains. For small and medium-sized bakeries, these challenges are particularly acute as they lack the resources to build redundant supply networks. Temperature control during transit is critical to prevent staleness and mold growth, requiring specialized packaging and refrigerated transport. These additional requirements increase operational costs and environmental footprint. Ensuring consistent product availability amidst these uncertainties is a persistent challenge that requires robust risk management strategies and investment in supply chain resilience.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.68% |

| Segments Covered | By Type, Application,n, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | BAB Inc., Thomas’ Bagels, Panera Bread Company, McDonald’s, Bruegger's Bagel Bakery, Dunkin’ Donuts, Einstein Noah Restaurant Group, Hostess Brands, George Weston Ltd., Aryzta Americas, Kettleman’s Bagel Company, and Flowers Foods |

SEGMENTAL ANALYSIS

By Type Insights

The fresh bagels segment led the market by holding 60.6% of the global market share in 2025. The dominance of the fresh bagels segment in the global market is primarily driven by consumer preference for superior texture and taste, which are characteristic of freshly baked products. Fresh bagels offer a crisp crust and chewy interior that frozen or pre-packaged alternatives often struggle to replicate. According to the American Bakers Association, fresh bakery items account for the majority of bread product sales due to their perceived quality and freshness. The proliferation of artisanal bakeries and café chains has reinforced this preference by making high-quality fresh bagels readily available in urban centers. In the United States, the number of independent bakeries increased by 9% in 2024, as per the National Association of Retail Bakers. These establishments emphasize traditional boiling and baking methods that enhance flavor and appeal to discerning customers. The sensory experience of purchasing warm, fresh bagels creates an emotional connection with consumers that packaged goods cannot match. Furthermore, fresh bagels are often viewed as a premium product, justifying higher price points. Retailers prioritize fresh bakery sections to drive foot traffic and impulse purchases. The immediacy of consumption aligns with breakfast and snack habits where freshness is paramount. This combination of sensory appeal, cultural tradition, and retail strategy ensures that fresh bagels remain the dominant choice for consumers seeking authenticity and quality in their daily dietary routines.

However, the frozen bagels segment is anticipated to record a CAGR of 9.4% over the forecast period in the global bagels market, owing to the increasing demand for convenience and extended shelf life among busy households. Frozen bagels allow consumers to stockpile products and enjoy them at their convenience without frequent trips to the bakery. According to the American Frozen Food Institute, sales of frozen bakery products increased by 12% in 2024, driven by their versatility and ease of storage. Advances in freezing technology have significantly improved the quality of frozen bagels, preserving their texture and flavor upon reheating. Quick freeze techniques prevent large ice crystals from forming, which maintains the structural integrity of the bread. Major retail chains have expanded their frozen bakery sections, offering a wide variety of flavors and brands. In Canada, the availability of frozen bagels in supermarkets grew by 15% in 20,24 as per Statistics Canada data. The rise of remote work has also contributed to this trend as consumers seek efficient breakfast solutions that can be prepared quickly at home. Toasting frozen bagels is a simple process that fits seamlessly into morning routines. Additionally, frozen bagels reduce food waste as consumers can thaw only what they need. This practicality, combined with improving quality standards, positions frozen bagels as a preferred option for modern families seeking a balance between convenience and quality.

By Application Insights

The supermarkets segment led the market by capturing 51.9% of the global market share in 2025 due to the extensive distribution networks and one-stop shopping convenience that supermarkets offer. Consumers prefer purchasing bagels alongside other grocery items such as cream cheese, fruits, and beverages, making supermarkets the most logical destination. According to the Food Marketing Institute, 85% of consumers prefer buying bakery items during their regular grocery shopping trips. Supermarkets provide a wide selection of brands, types, and price points catering to diverse consumer preferences. Private label brands offered by supermarket chains provide affordable alternatives that attract budget-conscious shoppers. In the United States, private label bakery sales grew by 7% in 2024 as per Nielsen IQ data. The prominent placement of bakery sections near store entrances enhances visibility and encourages impulse buys. Supermarkets also invest in in-store bakeries that produce fresh bagels daily, enhancing the perception of quality. Loyalty programs and promotional discounts further drive sales within this channel. The ability of supermarkets to manage large volumes efficiently ensures consistent availability and competitive pricing. This accessibility and variety make supermarkets the primary channel for bagel distribution, reaching a broad demographic across urban and suburban areas. The integration of online grocery shopping and delivery services has further strengthened this channel, allowing consumers to order bagels along with their weekly groceries.

On the other hand, the food service segment is experiencing the fastest growth in the global bagels market and is expected to grow at a CAGR of 10.4% over the forecast period, owing to the increasing popularity of café culture and the demand for ready-to-eat breakfast options. Coffee shops and quick service restaurants are expanding their menus to include gourmet bagel sandwiches and specialty toppings. According to the National Restaurant Association, limited service restaurants saw a 10% increase in breakfast sales in 2024. Bagels serve as a versatile base for both sweet and savory creations, appealing to a wide range of tastes. The rise of mobile ordering and delivery platforms has made it easier for consumers to access food service bagels conveniently. Apps like Uber Eats and DoorDash reported a 20% increase in breakfast orders in 2024 as per their annual reports. Corporate cafeterias and university dining halls are also incorporating bagels into their offerings, recognizing their popularity among students and employees. The social aspect of visiting cafés drives frequency of purchase as consumers combine coffee with bagel snacks. Innovation in menu items, such as avocado toast on bagels or smoked salmon combinations, attracts younger demographics. Food service providers leverage branding and ambiance to create experiential dining that justifies premium pricing. This dynamic environment fosters rapid adoption of new trends and flavors, driving sustained growth in the food service channel.

REGIONAL ANALYSIS

North America Bagels Market Analysis

North America captured the dominant position in the global bagels market by accounting for 45.7% of the global market share in 2025. The region is the birthplace of the modern bagel culture, particularly in cities like New York and Montreal, where the product is deeply embedded in local culinary traditions. According to the United States Department of Agriculture, per capita consumption of wheat-based bakery products remains high, supporting steady demand. The presence of major bagel chains and independent artisanal bakeries ensures widespread availability and variety. In Canada, the influence of French and British baking traditions has merged with Jewish deli culture, creating a unique market landscape. As per Statistics Canada, the bakery sector contributes significantly to the food manufacturing industry with consistent year-over-year growth. The trend towards premiumization is evident as consumers seek out authentic boiled and baked bagels over mass-produced alternatives. Health consciousness is driving innovation with whole grain, gluten-free, and protein-enriched options gaining traction. The robust infrastructure for dairy production supports the popular pairing of bagels with cream cheese and other spreads. Retailers and food service providers continuously innovate with seasonal flavors and limited edition offerings to maintain consumer interest. The strong economic stability and high disposable income in the region enable consumers to spend on premium bakery items. North America continues to set trends in flavor and format, influencing global markets through its established brands and culinary influence.

Europe Bagels Market Analysis

Europe occupied a promising share of the global bagels market in 2025. While traditionally dominated by bread rolls and croissants, the bagel has gained popularity as a convenient and versatile breakfast option. According to Eurostat, the bakery products market in Europe has seen steady growth, driven by urbanization and changing lifestyle habits. Western European countries such as the United Kingdom, Germany, and France are leading the adoption of bagels in mainstream diets. The influence of American café chains has introduced bagels to a wider audience, familiarizing consumers with the product. In the United Kingdom, the number of coffee shops offering bagel sandwiches increased by 11% in 2024, as per the British Coffee Association. Eastern European countries are also witnessing growth as international retail brands expand their presence. The demand for healthy and organic bakery products is rising, prompting manufacturers to introduce whole wheat and multigrain bagels. As per the European Bakery Association, sales of healthy bakery items grew by 8% in 2024. The regulatory environment in Europe emphasizes clean labels and sustainable sourcing, which influences product development. Local bakeries are adapting traditional recipes to include bagels, appealing to tourists and locals alike. The cultural acceptance of diverse bread types facilitates the integration of bagels into daily meals. Europe continues to evolve as a key market driven by health trends and international culinary influences.

Asia Pacific Bagels Market Analysis

The Asia Pacific region is an emerging market for bagels and is estimated to witness a prominent CAGR in the global bagels market during the forecast period. The rapid urbanization and the adoption of Western dietary habits among the growing middle class are propelling the market expansion in the Asia-Pacific region. In countries like Japan, South Korea, and China, bagels are perceived as a trendy food item. According to the Japan Bakery Association, imports and local production of Western-style breads, including bagels, increased by 9% in 2024. International coffee chains and fast food outlets have played a crucial role in introducing bagels to Asian consumers. The convenience of bagels aligns with the fast-paced lifestyles in major metropolitan areas. In China, the expansion of international bakery brands has increased awareness and availability of bagels. As per the China Bakery Association, the premium bakery segment is growing rapidly, with consumers willing to pay for quality and brand reputation. Local manufacturers are experimenting with Asian inspired flavors such as red bean, matcha, and sesame to cater to local palates. The rise of e-commerce and food delivery platforms has made bagels more accessible to younger consumers. Health consciousness is also driving demand for whole-grain and low-sugar options. Government initiatives to support the food processing industry encourage local production and innovation. Asia Pacific offers significant growth potential as consumer preferences continue to evolve towards diverse and convenient food options.

Latin America Bagels Market Analysis

Latin America is predicted to account for a notable share of the global bagels market during the forecast period, owing to gradual adoption and niche appeal. The presence of international hotel chains and expatriate communities that introduce bagels to the local population is further contributing to the Latin American market growth. In countries like Brazil and Mexico, urban centers are seeing an increase in specialized bakeries and cafés offering bagels. According to the Brazilian Bakery Industry Association, the consumption of specialty breads has grown by 6% annually. The economic recovery in several Latin American countries is boosting disposable income, allowing consumers to explore premium food options. Local producers are beginning to manufacture bagels using indigenous ingredients such as corn and quinoa to create unique variations. As per the Mexican Ministry of Economy, imports of bakery machinery have increased, indicating investment in local production capabilities. The tourism sector contributes to demand as visitors seek familiar breakfast options. Social media influences young consumers to try new food trends, including bagels paired with local cheeses and meats. The lack of widespread traditional bagel culture means that education and marketing are essential for growth. Retailers are slowly expanding their imported and local bagel offerings in major cities. While the market is smaller compared to North America and Europe, it presents opportunities for early entrants to establish brand loyalty. The potential for growth lies in adapting products to local tastes and leveraging urban dining trends.

Middle East and Africa Bagels Market Analysis

The Middle East and Africa are predicted to showcase steady growth in the global bagels market during the forecast period. The urbanization and the influence of international hospitality and retail brands in Gulf Cooperation Council countries are propelling the bagels market growth in the Middle East and Africa. In the United Arab Emirates and Saudi Arabia, the presence of global coffee chains and hotels has introduced bagels to affluent consumers. According to the Saudi Food and Drug Authority, the import of bakery products has increased by 7% in 2024, reflecting growing demand. The expatriate population plays a significant role in driving consumption as they seek familiar food items. Local bakeries are beginning to produce bagels to cater to this demand, often incorporating regional flavors such as zaatar and dates. In South Africa, the retail sector is expanding its range of international bakery items in upscale supermarkets. As per Stats SA, the food and beverage sector continues to grow, supported by a rising middle class. The hot climate favors indoor dining and café culture, where bagels are popular breakfast items. Religious and cultural dietary laws influence product formulation, with halal certification being essential for market entry. The region offers opportunities for growth as infrastructure improves and consumer awareness increases. Investment in local production facilities is expected to rise as demand stabilizes. The market remains small but holds potential for expansion as Western dietary habits continue to spread.

COMPETITION OVERVIEW

The competition in the bagel market is characterized by a fragmented landscape with a mix of large multinational corporations, regional chains, and independent artisanal bakeries. Major players leverage economies of scale and extensive distribution networks to dominate the retail packaged segment, while smaller establishments compete on quality and uniqueness in the fresh bakery sector. Price competition is intense, particularly in the supermarket aisle, where private label brands offer lower cost alternatives. Differentiation through branding, flavor innovation, and health benefits is crucial for maintaining market share. The rise of health consciousness has prompted companies to reformulate products with whole grains and reduced sodium to appeal to wellness-oriented consumers. Digital platforms have lowered barriers to entry, allowing small bakeries to reach wider audiences through direct-to-consumer sales. Strategic partnerships with coffee shops and delivery services enhance accessibility and convenience for customers. Retailers play a pivotal role by deciding shelf space allocations, which influence brand visibility. The threat of substitute products such as croissants, muffins, and toast adds pressure on bagel producers to continuously innovate. Overall, the market remains dynamic with companies striving to balance tradition with modern consumer demands for convenience and health.

KEY MARKET PLAYERS

A few major players of the global bagels market include

- BAB Inc

- Thomas’ Bagels

- Panera Bread Company

- McDonald’s

- Bruegger's Bagel Bakery

- Dunkin’ Donuts

- Einstein Noah Restaurant Group

- Hostess Brands

- George Weston Ltd

- Aryzta Americas

- Kettleman’s Bagel Company

- Flowers Foods

Top Strategies Used by Key Market Participants

Key players in the bagel market primarily employ product innovation and digital engagement strategies to maintain a competitive advantage. Companies frequently introduce new flavors and healthy alternatives, such as gluten-free or protein-enriched options, to cater to evolving dietary preferences. This diversification helps capture niche market segments and drives trial among health-conscious consumers. Digital transformation is another critical strategy, with firms investing in mobile apps and loyalty programs to enhance customer retention. Personalized marketing through data analytics allows brands to target specific demographics effectively. Expansion into food service channels via partnerships with coffee chains and hotels increases brand visibility and consumption occasions. Sustainability initiatives, including eco-friendly packaging and responsible sourcing, are increasingly used to build brand equity and appeal to environmentally aware shoppers. Operational efficiency improvements through automation and supply chain optimization reduce costs and ensure consistent product quality. These combined approaches enable companies to adapt to market dynamics and sustain growth in a mature industry.

Leading Players in the Market

- Einstein Bros. Bagels operates as a prominent chain in the United States, specializing in freshly baked bagels and proprietary cream cheese blends. The company focuses on delivering a consistent premium experience through its extensive network of retail locations. Recently, the brand has invested in digital transformation by enhancing its mobile application and loyalty program to improve customer engagement and retention. Einstein Bros. emphasizes operational efficiency by optimizing supply chain logistics to ensure product freshness across all outlets. The company actively introduces limited-time offers featuring seasonal flavors to drive foot traffic and generate buzz. Its commitment to community involvement and local sourcing strengthens brand loyalty. By leveraging data analytics, the company tailors marketing campaigns to specific demographic preferences. These strategic initiatives reinforce its position as a leader in the quick-service restaurant segment. The brand continues to expand its catering services, targeting corporate clients and events. This diversified approach ensures sustained relevance and growth in a competitive bakery landscape.

- Bruegger's Bagels is a key player known for its authentic New York-style bagels, boiled and baked daily in-store. The company prioritizes quality ingredients and traditional baking methods to differentiate itself from mass-produced competitors. Bruegger's has recently focused on menu innovation by introducing healthier options such as whole-grain and gluten-free bagels. The brand enhances its digital presence through improved online ordering systems and partnerships with third-party delivery platforms. This expansion increases accessibility for consumers seeking convenient breakfast solutions. Bruegger's also invests in employee training programs to ensure high service standards and product consistency. The company engages in sustainable practices by reducing waste and sourcing responsible ingredients. Strategic renovations of existing stores create modern, inviting atmospheres that appeal to younger demographics. Collaborations with local suppliers support community economies and enhance product authenticity. These efforts strengthen brand reputation and customer trust. Bruegger's continues to adapt to changing consumer preferences while maintaining its core identity. This balance of tradition and innovation drives long-term success in the specialty bakery sector.

- Thomas' Brands, a subsidiary of Bimbo Bakeries US, dominates the retail packaged bagel segment with widespread distribution across North America. The company leverages its massive scale to offer affordable and accessible bagel products in supermarkets and convenience stores. Thomas' has recently expanded its product portfolio to include artisanal-inspired varieties and plant-based options. The brand invests heavily in marketing campaigns that highlight versatility and convenience for home consumption. Innovations in packaging technology extend shelf life while maintaining texture and flavor quality. Thomas collaborates with retailers to optimize shelf placement and promotional strategies. The company focuses on sustainability initiatives such as recyclable packaging and energy-efficient manufacturing processes. By utilizing advanced data analytics, Thomas' identifies emerging trends and adjusts production accordingly. Its strong brand recognition ensures a loyal customer base and repeat purchases. The integration of digital coupons and social media engagement further drives sales. Thomas continues to lead the packaged segment by balancing cost efficiency with product quality. This strategic approach solidifies its position as a household name in the bagel category.

MARKET SEGMENTATION

This research report on the global bagels market has been segmented and sub-segmented based on type, application,n, and region.

By Type

- Fresh and Frozen Bagels

- Pre-Packaged Bagels

By Application

- Supermarkets

- Food Service

- Convenience store

- Other

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What factors are driving growth in the bagels market?

Growth drivers include rising demand for convenient breakfast foods, expanding retail distribution, product innovations, and increasing café and bakery culture.

2. What are the key distribution channels for bagels?

Retail supermarkets/hypermarkets, convenience stores, bakery cafés, online grocery platforms, and specialty stores are major channels.

3. What trends are shaping the bagels market?

Trends include artisanal and premium bagels, health-oriented options (whole grain, low-calorie), frozen bagels, and flavor innovations.

4. How does consumer preference influence product offerings?

Consumers are seeking healthier, organic, and premium varieties, along with convenient ready-to-eat and frozen options.

5. What are the health benefits of bagels?

Bagels provide carbohydrates for energy and can offer fiber and whole grains when made from whole wheat or multigrain flour.

6. What challenges does the bagels market face?

Challenges include price competition, perishability, maintaining freshness, and pressure to innovate in a saturated baked goods market.

7. How important is branding in the bagels market?

Strong branding helps differentiate products, build loyalty, and communicate quality and flavor uniqueness.

8. What impact does online retail have on the bagels market?

Online grocery sales and home delivery platforms have expanded market reach and convenience, especially for frozen and packaged bagels.

9. What role do bakery cafés play in market growth?

Bakery cafés and quick-service restaurants promote bagel consumption through fresh offerings and menu diversification.

10. Who are the key players in the bagels market?

Major players include Einstein Bros. Bagels, Bruegger’s Bagels, Thomas’ (Bimbo Bakeries), Lender’s Bagels (J.M. Smucker), Dave’s Killer Bread, and various regional artisanal bakeries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com