Global Benzene Market Size Share, Trends & Growth Forecast Report, Segmented By Derivative, Application, And Region (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa), Industry Analysis From 2025 to 2033

Global Benzene Market Summary

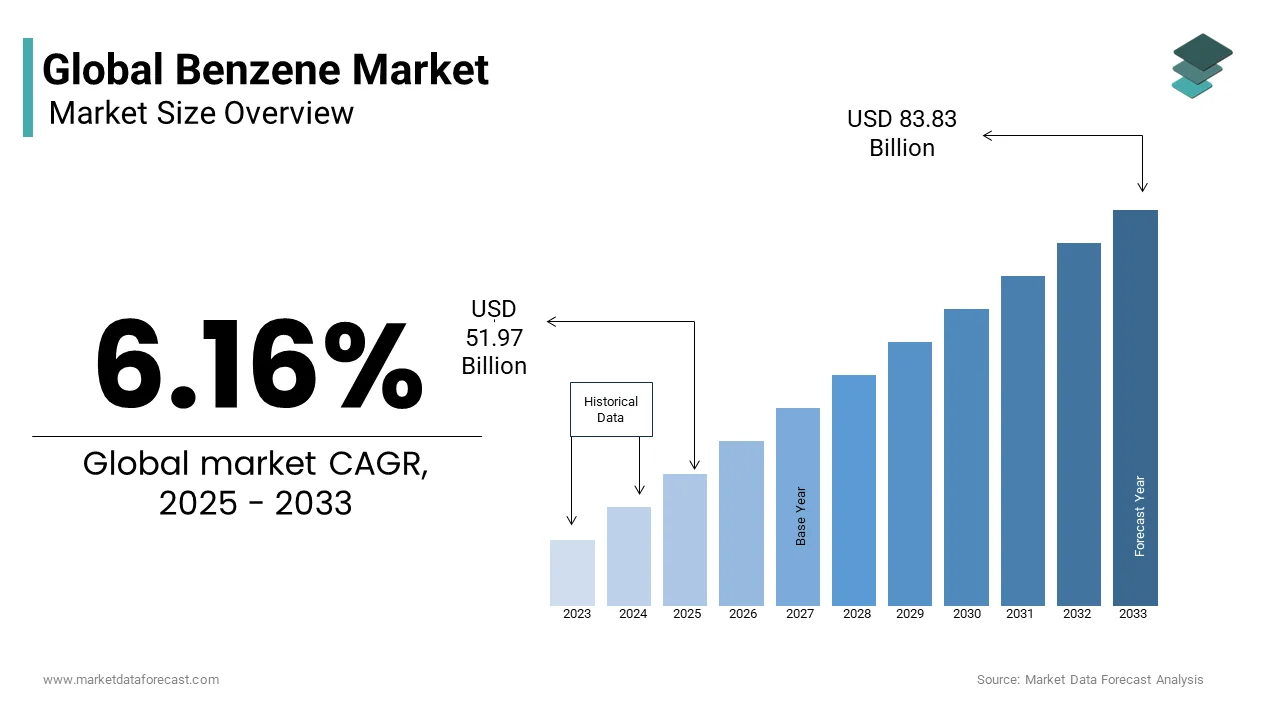

The global benzene market was valued at USD 48.95 billion in 2024, is anticipated to reach USD 51.97 billion in 2025, and is projected to expand to USD 83.83 billion by 2033, growing at a CAGR of 6.16% from 2025 to 2033. The growth of the global benzene market is driven by the rising demand for benzene derivatives in plastics, resins, and synthetic fibers, alongside its growing use in chemical intermediates for pharmaceuticals, automotive, and construction industries. Expanding industrialization in emerging economies and strong demand from the Asia-Pacific further support market growth.

Key Market Trends

- Increasing consumption of benzene derivatives in plastics and synthetic fibers.

- Rising use of cyclohexane for nylon production in textiles and the automotive industries.

- Strong demand for benzene in chemical intermediates, driving applications in resins, detergents, and dyes.

- Expansion of petrochemical capacity in the Asia-Pacific, strengthening regional dominance.

- The industry focuses on process optimization and sustainable production to reduce environmental impact.

Segmental Insights

- By derivative, the cyclohexane segment dominated with a 38.3% share in 2024, reflecting its critical role in nylon and fiber production.

- By application, the chemical intermediates segment accounted for the largest share in 2024, highlighting benzene’s role as a feedstock in multiple industrial processes.

Regional Insights

- Asia-Pacific led the global benzene market in 2024, capturing 58.1% share, supported by rapid industrialization, large-scale petrochemical capacity, and demand from China and India.

- North America shows steady growth, driven by chemical production and robust automotive demand.

- Europe emphasizes sustainable production and demand for specialty chemicals.

- Latin America and the Middle East & Africa are emerging markets, expanding with industrial projects and petrochemical investments.

Competitive Landscape

Leading companies in the global benzene market include Aerosol Aromatics GmbH & Co. KG (Germany), Dow (US), Borealis AG (Austria), BP plc (UK), Exxon Mobil Corporation (US), BASF SE (Germany), SABIC (Saudi Arabia), Repsol (Spain), Royal Dutch Shell Plc (Netherlands), and China Petroleum & Chemical Corporation (China). These players are focusing on capacity expansion, sustainable production technologies, and strategic collaborations to strengthen their global market presence.

Global Benzene Market Size

The global benzene market size was valued at USD 48.95 billion in 2024 and is anticipated to reach USD 51.97 billion in 2025 and USD 83.83 billion by 2033, growing at a CAGR of 6.16% during the forecast period from 2025 to 2033.

Benzene is a fundamental aromatic hydrocarbon primarily derived from crude oil refining and steam cracking processes. Benzene serves as a precursor to a wide array of derivatives, including ethylbenzene, cumene, cyclohexane, and nitrobenzene, which feed into polymers, resins, synthetic fibers, and detergents. The compound’s high reactivity and versatility support its indispensability in manufacturing. According to the United States Environmental Protection Agency, benzene is classified as a known human carcinogen, prompting stringent regulatory oversight across jurisdictions. As per data from the American Petroleum Institute, a portion of benzene produced in the U.S. is utilized in the synthesis of other chemicals, reflecting its foundational role in industrial chemistry. Furthermore, prolonged exposure, even at low concentrations, poses significant health risks, which influence handling protocols and industrial safety standards globally.

MARKET DRIVERS

Expansion of the Plastics and Polymers Industry

The escalating demand for polystyrene and other benzene-derived polymers in packaging, construction, and consumer goods propels the growth of the benzene market. Polystyrene, synthesized via ethylbenzene, a direct benzene derivative, is witnessing robust growth due to its lightweight, insulating, and moldable properties. According to the study, global polystyrene production surpassed 50 million metric tons, with Asia-Pacific accounting for a portion of output. This surge is largely driven by rapid urbanization and rising disposable incomes in emerging economies, particularly India and Indonesia, where the packaging and electrical appliance sectors are expanding. Apart from these, the growing use of expanded polystyrene (EPS) in construction insulation aligns with energy efficiency mandates in Europe and North America.

Rising Demand for Styrene-Butadiene Rubber (SBR) in Automotive Applications

The automotive sector’s reliance on synthetic rubber, particularly styrene-butadiene rubber (SBR), is boosting the growth of the benzene market. SBR, produced using styrene derived from benzene, constitutes a portion of global synthetic rubber consumption, primarily in tire manufacturing. According to the International Organization of Motor Vehicle Manufacturers, over 89 million motor vehicles were produced worldwide in 2023, with China, the United States, and Germany leading output. Each passenger vehicle tire contains approximately a percentage of SBR, which translates to substantial benzene demand. Moreover, the expansion of electric vehicle (EV) fleets, which require specialized low-rolling-resistance tires, further amplifies SBR usage. This shift intensifies the need for high-performance rubber, thereby sustaining benzene’s strategic position in mobility-related chemical value chains.

MARKET RESTRAINTS

Stringent Environmental and Health Regulations

Regulatory crackdowns on benzene emissions and occupational exposure are restraining the growth of the benzene market. Benzene is a volatile organic compound (VOC) and a Group 1 carcinogen, as classified by the International Agency for Research on Cancer. In response, regulatory bodies have imposed strict limits on permissible exposure levels. The European Union has implemented a new occupational exposure limit (OEL) for benzene that has been phased in over several years and is now significantly lower than 1 ppm. In the U.S., the Occupational Safety and Health Administration enforces a permissible exposure limit of 1 ppm, down from 10 ppm in prior decades. Compliance necessitates costly emission control systems and closed-loop processing, which increases operational expenditures.

Volatility in Crude Oil and Feedstock Supply Chains

High sensitivity towards fluctuations in crude oil prices and refinery operations aside, it is degrading the growth of the NZENE market. Benzene is predominantly sourced from catalytic reforming in petroleum refining and pyrolysis gasoline in ethylene production. Geopolitical disruptions, such as the Red Sea shipping crisis, led to an increase in Brent crude prices within three months, as per the study. Such volatility directly impacts benzene production costs and supply stability. Apart from these, shifts in refinery output due to reduced gasoline demand threaten benzene availability. Refineries optimized for diesel or jet fuel yield less reformate, which is the primary source of benzene. Consequently, regions like Western Europe have witnessed a decline in benzene co-production since 2020, according to the research, which forces increased reliance on imports and alternative production routes.

MARKET OPPORTUNITY

Development of On-Purpose Benzene Production Technologies

Emerging on-purpose benzene production methods, such as toluene disproportionation (TDP) and toluene hydrodealkylation (HDA), are setting up new opportunities for the growth of the benzene market. These technologies offer a stable and dedicated output as traditional sources are dwindling due to shifting fuel demand. According to the research, global TDP capacity expanded by metric tons, with major investments in China and Saudi Arabia. These processes achieve benzene yields exceeding, as per the study, which makes them economically viable despite higher capital costs. The ability to adjust production based on aromatic demand rather than gasoline output positions on-purpose facilities as important infrastructure in future chemical parks, particularly in regions aiming for petrochemical self-sufficiency.

Integration with Circular Economy Models in Styrenics Recycling

Advancements in chemical recycling of polystyrene and mixed plastics are setting up new opportunities for the growth of the benzene market. Pyrolysis and depolymerization technologies can recover styrene monomer from post-consumer waste, which can then be reconverted into benzene or used directly in SBR synthesis. According to the research, only a portion of all plastic waste was recycled globally, but chemical recycling capacity is projected to grow by 2030. Companies have demonstrated commercial-scale systems capable of processing notable tons of polystyrene waste annually, yielding a certain level of pure styrene oil. As per the American Chemistry Council, over 30 chemical recycling projects were under development in North America and Europe in 2023, many targeting styrenic feedstocks. This shift reduces reliance on fossil-derived benzene and aligns with corporate sustainability mandates, which creates a secondary supply stream that enhances resource efficiency.

MARKET CHALLENGES

Geopolitical Instability Affecting Key Production Hubs

Major benzene-producing regions, including the Middle East and Eastern Europe, face persistent geopolitical risks that threaten supply continuity, which challenges the growth of the benzene market. The ongoing conflict in Ukraine has disrupted pipeline infrastructure and forced the shutdown of key petrochemical complexes in the region. Similarly, tensions in the Persian Gulf have led to insurance premium hikes for maritime shipments. According to research, there has been an increase in war risk premiums for tankers traversing the Strait of Hormuz in early 2024. These disruptions delay feedstock deliveries and elevate logistics costs, weakening supply chain predictability. As per the study, a portion of the global benzene trade transits through high-risk maritime zones, which amplifies vulnerability to regional conflicts and trade restrictions.

Competition from Bio-Based and Alternative Aromatic Feedstocks

The emergence of renewable aromatics derived from biomass is set to pose a new challenge for the growth of the benzene market. Companies are developing bio-styrene and bio-benzene using lignin and pyrolysis oils, aiming to reduce carbon footprints. According to the research, lignin valorization technologies have achieved pilot-scale production of aromatic chemicals with a portion of carbon efficiency. Virent and Anellotech, for example, have demonstrated catalytic processes converting plant sugars into benzene-like hydrocarbons. Commercial scalability remains limited. Regulatory burden under the EU’s Fit for 55 package, which mandates a 55% reduction in greenhouse gas emissions by 2030, is accelerating investment in bio-alternatives. As per the study, bio-based chemical production in Europe grew annually. Hence, the trajectory signals a potential erosion of market dominance in the coming decades.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.16% |

| Segments Covered | By Derivative, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Aerosol Aromatics GmbH & Co. KG (Germany), Dow (US), Borealis AG (Austria), BP plc (UK), Exxon Mobil Corporation (US), BASF SE (Germany), SABIC (Saudi Arabia), Repsol (Spain), Royal Dutch Shell Plc (Netherlands), China Petroleum & Chemical Corporation (China), among others |

SEGMENTAL ANALYSIS

By Derivative Insights

The cyclohexane segment dominated the benzene derivatives market by capturing 38.3% of global market share in 2024. The growth of the cyclohexane segment is driven by its pivotal role in nylon production, particularly nylon-6 and nylon-6,6, which are indispensable in automotive, textiles, and engineering plastics. Over 90% of cyclohexane produced globally is derived from benzene via catalytic hydrogenation, according to the American Chemical Society. The rising demand for lightweight and durable materials in vehicle manufacturing has accelerated nylon adoption. According to research, nylon components constitute a portion of a typical passenger car’s weight, which enhances fuel efficiency. Apart from these, the textile industry in South and Southeast Asia, where nylon fiber demand grew annually, continues to absorb significant cyclohexane output. This strengthens benzene’s centrality in this value chain, as per the Fiber Economics Bureau. The growth of the cyclohexane segment is further driven by strategic capacity expansions in key manufacturing hubs. The country’s self-sufficiency push in synthetic fibers and engineering resins has led to integrated refinery-petrochemical complexes prioritizing benzene-to-cyclohexane conversion. This convergence of industrial demand and vertical integration in production ensures that cyclohexane remains the dominant derivative.

The ethylbenzene-to-styrene monomer (SM) segment is predicted to witness the highest CAGR of 5.7% from 2025 to 2033 due to the escalating global demand for expanded polystyrene (EPS) and acrylonitrile butadiene styrene (ABS) resins, particularly in construction and electronics. As per the study, EPS insulation usage in new-build residential properties across Europe increased, driven by tightening energy efficiency standards under the EU Energy Performance of Buildings Directive. The material’s thermal resistance and cost-effectiveness make it a preferred choice, directly increasing styrene demand. Simultaneously, the electronics sector’s reliance on high-impact polystyrene (HIPS) and ABS for casings, connectors, and display housings has intensified. These converging applications and new steam cracker projects are synergistically amplifying ethylbenzene demand. This makes it the fastest-growing derivative segment.

By Application Insights

The chemical intermediates segment led the benzene market by capturing a significant share in 2024. The growth of the chemical intermediates segment is driven by benzene’s role as a foundational building block for synthesizing higher-value aromatic compounds such as phenol, aniline, and cumene. Unlike end-use applications, chemical intermediates act as important enablers across multiple downstream industries, which creates a cascading demand effect. Furthermore, the production of cumene, which consumes a portion of global benzene output, feeds directly into phenol and acetone manufacturing, both essential in resins, adhesives, and pharmaceuticals. According to the research, phenol demand grew year-on-year, driven by bisphenol-A (BPA) use in polycarbonate plastics and epoxy coatings. The integration of benzene-based intermediates into complex chemical value chains ensures sustained demand, even amid fluctuations in end-product markets.

The plastics application segment is predicted to witness the highest CAGR of 6.1% during the forecast period, owing to the rising use of polystyrene, polycarbonate, and ABS in packaging, consumer goods, and automotive components. In 2023, global plastics production reached a significant million metric tons, with thermoplastics accounting for a portion of output, according to the research. Moreover, the shift toward lightweight vehicles to meet fuel efficiency standards has increased the use of benzene-derived engineering plastics. Apart from these, innovations in biocompatible plastics for medical devices and 3D printing resins are expanding the application frontier. These factors and the expanding polymerization infrastructure in Southeast Asia and the Middle East are propelling plastics to the forefront of benzene demand growth.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia-Pacific was the top performer in the global benzene market in 2024 and accounted for 58.1% of the global market share in 2024. The domination of Asia Pacific in the global market is primarily driven by the region’s vast manufacturing ecosystem, particularly in China, India, and South Korea, where integrated refineries and petrochemical complexes operate at scale. China alone accounts for a portion of regional demand, driven by its dominance in synthetic fiber, plastic, and rubber production. As per the study, the country produced significant million metric tons of chemical raw materials, with benzene-intensive sectors expanding rapidly. Apart from these, India’s growing automotive and construction industries have increased styrene and phenol consumption, with polymer demand rising annually, as per the research. Government initiatives such as Make in India and the expansion of special economic zones further bolster industrial uptake. As a result, this ensures sustained benzene demand across diverse derivative chains.

North America Market Analysis

North America is the second-largest in the benzene market and accounted for 18.5% of the global market share in 2024, with the United States serving as the primary consumption and production hub. The region benefits from abundant shale-derived feedstocks, which support cost-competitive ethylene production and, consequently, pyrolysis gasoline. In addition, U.S. refineries and crackers produce notable metric tons of benzene, with a portion oriented toward chemical intermediates, according to the study. The resurgence of domestic manufacturing, particularly in automotive and construction, has amplified demand for styrenics and polyurethanes. Furthermore, the Inflation Reduction Act has incentivized investments in clean hydrogen and carbon capture. This enables refiners to upgrade facilities while maintaining aromatic output.

Europe Market Analysis

Europe grew steadily in the global benzene market, with Germany, France, and Italy forming the core of aromatic chemical production. However, the region faces structural challenges due to declining refinery throughput and stringent environmental regulations, leading to a reduction in domestic benzene output since 2020. Despite this, Europe remains a major consumer of benzene-derived intermediates, particularly in high-performance polymers and specialty chemicals. According to a study, the EU produced notable tons of polycarbonate and ABS, largely for automotive and electronics applications. The transition toward circular economy models has also spurred investment in chemical recycling, with pilot plants in the Netherlands and Germany recovering styrene from waste plastics.

Middle East And Africa Market Analysis

Middle East and Africa are expected to be the most lucrative regions in the benzene market, with Saudi Arabia and Iran emerging as key production centers. The region leverages its vast crude oil reserves and low-cost refining infrastructure to produce benzene as a co-product of gasoline and ethylene manufacturing. Saudi Arabia’s Jubail and Yanbu industrial cities host some of the world’s largest integrated complexes, with SABIC and Aramco driving aromatics expansion. Meanwhile, Africa’s benzene demand remains nascent but is growing annually, driven by urbanization and rising detergent and plastic consumption, according to the study. However, limited downstream processing capacity restricts regional value addition, which positions the area more as a supplier than a consumer.

Latin America Market Analysis

Latin America is likely to grow in the benzene market, with Brazil and Mexico representing the primary demand centers. The region’s benzene ecosystem is constrained by aging refineries and limited petrochemical integration, resulting in reliance on imports to meet industrial needs. Brazil consumed large quantities of benzene, mainly for ethylbenzene and cumene production, as per the research. The country’s automotive sector remains a key driver for styrene and polyurethane demand. However, volatility in crude supply and inconsistent energy policies have hindered large-scale investments. Thus, Brazil’s push for bio-based chemicals and ethanol-derived intermediates may open alternative pathways.

COMPETITIVE LANDSCAPE

The benzene market exhibits intense competition shaped by geopolitical dynamics, feedstock accessibility, and regulatory environments. While no single entity dominates globally, regional leaders leverage integrated infrastructure and cost advantages to maintain influence. Competition is less price-driven and more focused on supply reliability, product purity, and compliance with environmental standards. Companies differentiate through technological capabilities, such as advanced extraction and emission control systems, and by offering tailored solutions to downstream industries. Strategic alliances with chemical converters and participation in circular economy initiatives are becoming important competitive levers. The shift toward on-purpose production and investments in low-carbon pathways is redefining competitive boundaries. Emerging players in Asia and the Middle East are challenging traditional Western suppliers by combining scale with lower operating costs, which creates a dynamic and increasingly fragmented competitive landscape.

KEY MARKET PLAYERS

A few of the dominating players in the global benzene market include

- Aerosol Aromatics GmbH & Co. KG (Germany)

- Reliance Industries

- Sinopec

- Dow (US)

- Borealis AG (Austria)

- BP plc (UK)

- Exxon Mobil Corporation (US)

- BASF SE (Germany)

- SABIC (Saudi Arabia)

- Repsol (Spain)

- Royal Dutch Shell Plc (Netherlands)

- China Petroleum & Chemical Corporation (China), among others

Top Players in the Market

- SABIC has established a formidable presence in the Asia Pacific benzene landscape through strategic partnerships and integrated production networks. The company supplies high-purity benzene to key derivatives manufacturers across China, South Korea, and India, supporting growing demand for polycarbonates and styrenics. It has also collaborated with Japanese and Taiwanese firms to develop advanced recycling technologies that reintegrate styrene into the benzene value chain. Its technical service teams work closely with regional customers to optimize feedstock utilization,n which strengthens long-term contracts and supply chain reliability across the Asia Pacific region.

- Reliance Industries has emerged as a pivotal player in the Asia Pacific benzene market through its massive Jamnagar refinery complex, one of the world’s largest integrated refining and petrochemical hubs. The company leverages its scale to produce benzene as a co-product of catalytic reforming, supplying downstream units manufacturing polyester, plastics, and synthetic rubber. The company is also advancing circular economy initiatives by exploring pyrolysis oil integration from plastic waste to supplement fossil-based feedstocks. Its focus on vertical integration, which links benzene to finished goods like textiles and packaging. This enables cost efficiency and market responsiveness. Reliance is expanding its footprint beyond India, which strengthens its role in regional supply chains through strategic export agreements with Southeast Asian processors.

- Sinopec plays a central role in shaping the Asia Pacific benzene market through its extensive refining infrastructure and domestic distribution network. The company operates multiple aromatics complexes across eastern and southern China, supplying benzene to major chemical clusters in Zhejiang, Jiangsu, and Guangdong provinces. It has also deepened collaborations with automakers and electronics manufacturers to ensure a stable supply of styrene and cyclohexane derivatives. Sinopec is actively investing in digital monitoring systems to track benzene emissions and optimize logistics, which aligns with national green manufacturing goals.

Top Strategies Used By The Key Market Participants

Key players in the benzene market are primarily deploying vertical integration, capacity expansion, technology innovation, sustainability initiatives, and strategic partnerships to consolidate their positions. Companies are investing in integrated refining-petrochemical complexes to secure feedstock supply and reduce cost volatility. Expansion of on-purpose benzene production through toluene disproportionation is gaining traction to offset declining co-product availability from refineries. Firms are also adopting advanced process optimization technologies to improve yield and purity. Environmental compliance is driving investments in emission control systems and carbon capture. Apart from these, collaborations with recycling startups and participation in circular economy pilots are emerging as competitive differentiators. Export diversification and long-term off-take agreements with derivative producers are further enhancing market resilience and customer retention across high-growth regions.

MARKET SEGMENTATION

This research report on the global benzene market is segmented and sub-segmented into the following categories.

By Derivative Type

- Alkyl Benzene

- Cumene

- Cyclohexane

- Ethyl Benzene

- Nitro Benzene

- Aniline

- Toluene

- Phenol

- Styrene Others

By Application Type

- Solvent

- Chemical Intermediates

- Surfactants

- Plastics

- Rubber Manufacturing

- Detergent

- Explosives

- Lubricants

- Pesticides

- Anti-Knock Additives

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is benzene, and why does it matter globally?

Benzene is a colorless, flammable liquid hydrocarbon — a foundational building block for plastics, resins, synthetic fibers, and dyes.

Where does benzene come from?

Most benzene is derived as a byproduct of petroleum refining and steam cracking during ethylene production.

Why is the global benzene market so volatile?

Prices swing with crude oil, refinery margins, and regional supply-demand imbalances — especially when crackers shut down or new capacity comes online.

Who are the biggest consumers of benzene?

The chemical industry — especially producers of styrene (for polystyrene and synthetic rubber), cumene (for phenol/acetone), and cyclohexane (for nylon).

Which regions dominate production and consumption?

Asia-Pacific, led by China, is the largest consumer and fastest-growing producer, fueled by domestic petrochemical expansion.

What’s impacting benzene supply chains today?

Refinery reconfigurations (toward diesel/jet fuel), reduced cracker runs during energy crises, and China’s “dual control” energy policies cause supply shocks.

Are there environmental or health concerns affecting the market?

Benzene is a known carcinogen, so workplace exposure limits and emissions controls are tightening globally.

Is benzene being replaced by “greener” alternatives?

Not at scale — its molecular structure is too essential for high-performance polymers. But bio-based benzene (from biomass pyrolysis) is in early R&D.

What’s the future outlook for benzene demand?

But long-term pressure will come from sustainability mandates, material substitution (e.g., bio-polymers), and efficiency gains in conversion processes.

How can businesses navigate the benzene market wisely?

Lock in contracts with integrated petrochemical suppliers, monitor refinery utilization rates, and diversify sourcing regions to hedge against disruptions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com