Global Canned Fruits Market Size, Share, Trends & Growth Forecast Report - Segmented By Type (Organic and Inorganic), Form, Distribution Channel, And Region (North America, Europe, APAC, Latin America, Middle East And Africa) - Industry Analysis 2026 to 2034

Market Size, 2025

$12.37 BnMarket Estimate, 2026

$12.78 BnMarket Forecast, 2034

$16.63 BnCAGR, 2026–2034

3.35%Global Canned Fruits Market Report Summary

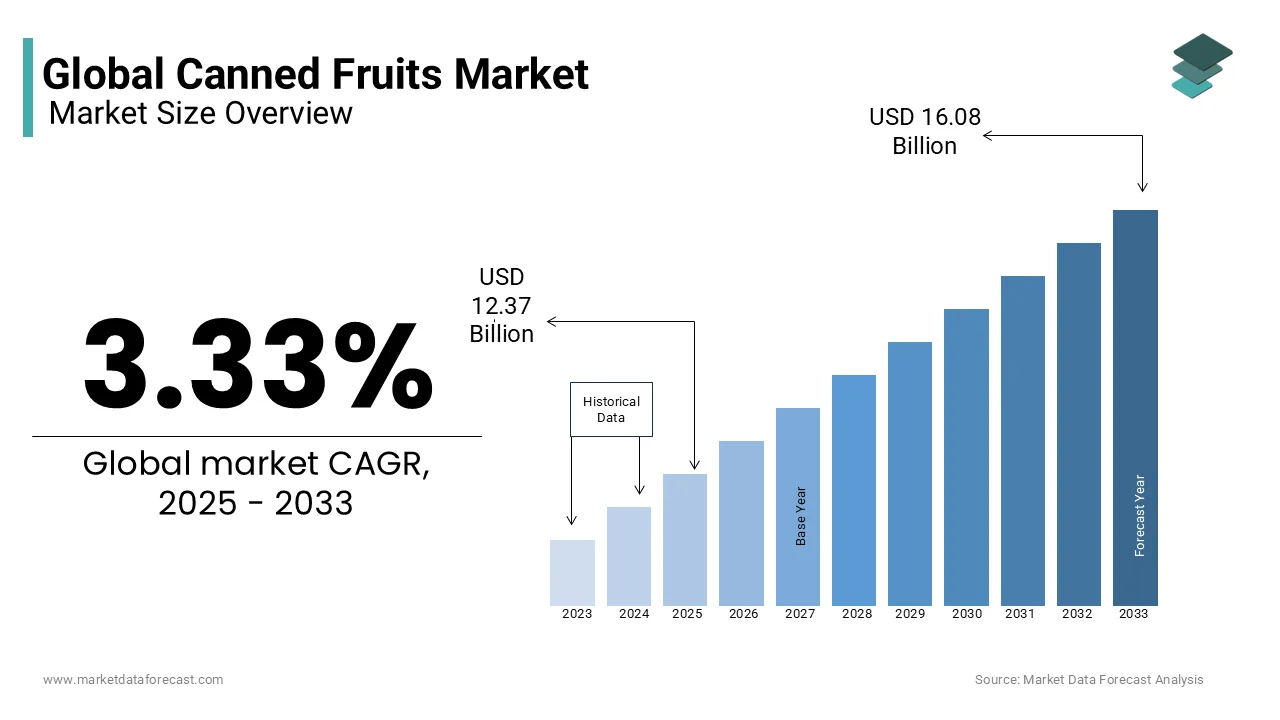

The global canned fruits market was valued at USD 12.37 billion in 2025, is estimated to reach USD 12.78 billion in 2026, and is projected to reach USD 16.63 billion by 2034, growing at a CAGR of 3.35% during the forecast period. Market growth is driven by increasing demand for convenient and long shelf life food products, rising consumption of ready to eat fruits, and expanding retail distribution networks. Canned fruits are widely preferred due to their year round availability, affordability, and ease of storage. The growing demand for convenient food solutions and processed fruit products is further supporting steady global market growth.

Key Market Trends

- Rising demand for convenient and long shelf life fruit products is driving market growth.

- Increasing consumption of ready to eat and processed foods is boosting demand.

- Growing expansion of supermarkets and organized retail channels is supporting market expansion.

- Year round availability of seasonal fruits is enhancing product adoption.

- Innovation in packaging and low sugar fruit preservation is influencing market development.

Segmental Insights

- Based on product type, the peaches segment accounted for 39.9% of the global canned fruits market share in 2025. This dominance is attributed to strong consumer preference and widespread use in desserts and food preparations.

- Based on form, the cut fruits segment held 61.5% of the global canned fruits market share in 2025, driven by convenience and ease of consumption.

- Based on distribution channel, the supermarkets and hypermarkets segment accounted for 58.6% of the global canned fruits market share in 2025, supported by broad product availability and organized retail expansion.

Regional Insights

- The global canned fruits market is experiencing steady growth across regions, supported by convenience food trends and retail development.

- North America was the largest contributor, accounting for 35.7% of the global canned fruits market share in 2025, driven by strong demand for processed foods, established retail infrastructure, and high consumer preference for convenient meal options.

Competitive Landscape

The global canned fruits market is highly competitive, with key players focusing on product quality, packaging innovation, and expansion of distribution networks to strengthen their market position. Companies are investing in healthier formulations, sustainable packaging, and product diversification. Prominent players in the global canned fruits market include Del Monte, ConAgra Foods, Dole Food Company, The Kraft Heinz Company, Seneca Foods, CHB Group, Rhodes Food Group, Conserve, Tropical Food Industries, Kangfa Foods, H.J Heinz, and Ardo.

Global Canned Fruits Market Size

The global canned fruits market size was valued at USD 12.37 billion in 2025, and is expected to reach USD 16.63 billion by 2034 from USD 12.78 billion in 2026, growing at a CAGR of 3.35% between 2026 and 2034.

Canned fruits are preserved fruit products that have been cleaned, sealed in airtight metal cans or jars, and heat-treated to create a shelf-stable product. This market serves as a critical component of the global food supply chain by extending the shelf life of perishable produce and ensuring year round availability regardless of seasonal constraints. The definition of this market extends beyond simple preservation to include value added products such as fruit cocktails diced peaches and tropical mixes that cater to diverse culinary applications in both household and commercial settings. According to the Food and Agriculture Organization (FAO), post-harvest losses for fruits and vegetables in developing regions can reach up to 45-50%. To combat this, the FAO primarily advocates for improved post-harvest management, including cold storage infrastructure, better packaging, and transportation, alongside processing methods like canning and drying. The World Health Organization recommends consuming at least 400g of fruits and vegetables daily to prevent noncommunicable diseases. While canned and frozen fruits are considered suitable alternatives if they contain no added sugar or salt, the WHO does not explicitly emphasize them as a primary solution for urban dietary gaps, often warning instead about the high intake of processed foods in urban environments. As per the United States Department of Agriculture (USDA) and nutritional studies, canned fruits and vegetables are a nutritionally viable alternative to fresh produce. The canning process effectively retains minerals and fat-soluble vitamins (such as A and E), though it can cause significant losses in water-soluble vitamins like Vitamin C and B vitamins due to heat processing. The market is characterized by a complex interplay of agricultural production cycles logistics infrastructure and consumer preferences for convenience. The integration of advanced sterilization technologies ensures product safety while maintaining sensory qualities. This industry acts as a buffer against supply chain disruptions providing stability in food security. The shift toward sustainable packaging and clean label formulations further defines the contemporary landscape of the canned fruits sector aligning with broader environmental and health trends.

MARKET DRIVERS

Rising Demand for Convenience Foods in Urban Households

The accelerating pace of urbanization and the subsequent shift in lifestyle patterns have established that convenience is the main reason for the growth of the canned fruits market. As more individuals migrate to cities the time available for food preparation diminishes leading to a increased reliance on ready to eat and easy to prepare food items. According to the United Nations Department of Economic and Social Affairs, the global urban population is projected to reach 68% by 2050. Observers infer that this urbanization will drive demand for convenient consumer goods, though UN DESA reports focus on sustainable development and infrastructure challenges rather than meal planning behaviors. Canned fruits offer a practical solution for busy professionals and families who seek nutritious options without the labor intensive processes of washing peeling and cutting fresh produce. The International Labour Organization and Eurostat report that average working hours in many developed economies are comparatively low and have declined, with the longest working hours primarily concentrated in developing regions like South Asia and Africa. Retailers have responded by expanding their offerings of single serve cups and family size cans that fit seamlessly into modern refrigerators and pantries. The versatility of canned fruits allows them to be used in breakfast cereals salads desserts and savory dishes enhancing their appeal across various meal occasions. This structural change in consumption habits ensures a steady demand for canned fruits as they provide a reliable and consistent source of nutrition that aligns with the fast paced nature of contemporary urban life.

Extended Shelf Life and Reduction of Food Waste

The ability of canned fruits to maintain quality over extended periods gives a big boost to the canned fruits market. This addresses global concerns regarding food security and waste reduction. Unlike fresh fruits which are highly perishable and susceptible to spoilage canned varieties can be stored for months or even years without significant loss of nutritional value or taste. According to the Food and Agriculture Organization of the United Nations approximately one third of all food produced globally is lost or wasted each year with fruits and vegetables being among the most affected categories. Canning technology effectively mitigates this issue by preserving harvest surpluses and making them available during off seasons or in regions with limited agricultural output. The World Resources Institute highlights that improving food preservation methods is key to achieving sustainable development goals related to hunger and resource efficiency. In developing countries where cold chain infrastructure is often inadequate canned fruits provide a vital means of accessing essential vitamins and minerals year round. The United States Department of Agriculture notes that the thermal processing involved in canning destroys harmful microorganisms ensuring product safety without the need for refrigeration. This logistical advantage reduces the carbon footprint associated with transportation and storage compared to fresh produce that requires constant temperature control. Consequently both consumers and institutional buyers such as schools and hospitals increasingly prefer canned fruits for their reliability and contribution to sustainable food systems.

MARKET RESTRAINTS

Health Concerns Regarding Added Sugars and Preservatives

Growing health consciousness among consumers constrains the growth of the canned fruits market. This is particularly due to perceptions regarding high sugar content and the use of synthetic preservatives. Many traditional canned fruit products are packed in heavy syrups which can significantly increase calorie intake and contribute to metabolic disorders such as obesity and type 2 diabetes. According to the World Health Organization global diabetes rates have risen dramatically with poor dietary habits being a major contributing factor. In response health aware shoppers are increasingly scrutinizing ingredient labels and avoiding products with added sugars or artificial additives. The Centers for Disease Control and Prevention reports that excessive added sugar intake, primarily from sugar-sweetened beverages and snacks, is linked to a higher risk of heart disease and Type 2 diabetes, leading to national recommendations to limit added sugars to less than 10% of total daily calories. Although manufacturers have introduced options packed in water or natural juice these variants often face criticism for altered texture and flavor profiles compared to syrup packed versions. Euromonitor International notes that the clean label movement is gaining traction with consumers demanding minimal processing and transparent sourcing. This trend forces companies to reformulate products which can be costly and may not always meet consumer expectations for taste. The stigma associated with processed foods continues to hinder market growth as educational campaigns by health organizations emphasize the benefits of whole fresh fruits. So, the canned fruits sector must navigate these health perceptions carefully to maintain relevance in a market that increasingly prioritizes wellness and natural ingredients.

Environmental Impact of Packaging Materials

The environmental footprint associated with metal cans and packaging materials is a major factor restraining the growth of the canned fruits market. This challenge grows as sustainability becomes a central concern for consumers and regulators. Traditional steel and aluminum cans require significant energy for production and recycling and if not properly disposed of can contribute to landfill waste and pollution. According to the United Nations Environment Programme plastic and metal waste from food packaging constitutes a major portion of global municipal solid waste. Although metals are recyclable the actual recycling rates vary widely across regions with many cans ending up in landfills due to inadequate waste management infrastructure. The Ellen MacArthur Foundation emphasizes the need for a circular economy where packaging materials are kept in use and regenerated rather than discarded. Consumers are increasingly favoring brands that adopt eco friendly packaging solutions such as biodegradable materials or refillable systems. The European Commission has implemented strict regulations on single use plastics and packaging waste pushing companies to reduce their environmental impact. These regulatory pressures increase compliance costs for manufacturers who must invest in sustainable packaging technologies. Additionally the carbon emissions associated with the transportation of heavy canned goods compared to lighter alternatives like dried or concentrated fruits further exacerbate environmental concerns. As corporate sustainability goals become more ambitious the canned fruits industry faces pressure to innovate its packaging strategies. Failure to address these environmental issues risks alienating environmentally conscious consumers and facing stricter regulatory penalties.

MARKET OPPORTUNITIES

Innovation in Healthy and Organic Product Variants

The development of healthy and organic canned fruit variants offers a significant opportunity for the canned fruits market expansion. This aligns with the growing demand for nutritious and clean label products. Manufacturers can capitalize on this trend by introducing fruits packed in water natural juices or their own juices without added sugars or artificial preservatives. By obtaining organic certifications brands can appeal to health conscious shoppers who are willing to pay a premium for products free from pesticides and synthetic chemicals. The United States Department of Agriculture’s National Organic Program provides a framework for certification that enhances consumer trust and marketability. Additionally the incorporation of functional ingredients such as probiotics or vitamins into canned fruits can create unique value propositions that differentiate products in a crowded market. The International Food Information Council reports that consumers are increasingly interested in functional foods that offer health benefits beyond basic nutrition. Companies can also explore exotic and tropical fruits that are not readily available fresh in certain regions thereby expanding their product portfolios. Collaborations with health experts and nutritionists can help validate the nutritional benefits of these new variants. By focusing on quality and health attributes manufacturers can overcome negative perceptions associated with traditional canned fruits. This strategic shift toward healthier options not only attracts new customer segments but also fosters brand loyalty among existing consumers who prioritize wellness.

Expansion into Emerging Markets with Growing Middle Class

The expansion into emerging markets characterized by a rising middle class and increasing disposable incomes paves the way for the growth of the canned fruits market. As economic conditions improve in regions such as Asia Pacific Latin America and Africa consumers are shifting toward diversified diets that include convenient and processed food items. According to the World Bank the middle class in developing countries is expanding rapidly driving demand for higher quality and varied food products. Canned fruits offer an affordable and accessible way for these consumers to enjoy exotic and out of season fruits that may not be locally available. The Food and Agriculture Organization of the United Nations highlights that urbanization in these regions is leading to changes in shopping habits with supermarkets and hypermarkets becoming dominant retail channels. These modern trade formats facilitate the distribution of packaged goods including canned fruits to a wider audience. Local manufacturers can leverage this trend by establishing production facilities closer to raw material sources thereby reducing costs and ensuring freshness. International brands can enter these markets through partnerships with local distributors who understand regional preferences and regulatory landscapes. The increasing adoption of western dietary habits and the influence of global media further stimulate demand for convenient food options. By tailoring product offerings to local tastes and price points companies can capture significant market share in these high growth regions. This geographic diversification reduces dependence on mature markets and opens new avenues for revenue generation.

MARKET CHALLENGES

Fluctuating Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices and frequent supply chain disruptions are a formidable challenge to the canned fruits market. This affects production costs and profit margins. Fruit crops are highly susceptible to weather conditions pests and diseases which can lead to unpredictable yields and price fluctuations. According to the Intergovernmental Panel on Climate Change extreme weather events such as droughts floods and heatwaves are becoming more frequent impacting agricultural productivity globally. These climatic variations can cause shortages of key fruits such as peaches pineapples and cherries leading to spikes in procurement costs for manufacturers. The World Bank notes that food price inflation has been a persistent issue in recent years driven by supply chain bottlenecks and geopolitical tensions. Additionally disruptions in logistics such as port congestions and shipping delays can hinder the timely delivery of raw materials and finished products. The International Chamber of Commerce highlights that non tariff barriers and trade restrictions further complicate international supply chains. Manufacturers often struggle to pass these increased costs on to consumers who are price sensitive leading to compressed margins. The reliance on seasonal harvests means that any disruption during the picking window can have long lasting effects on inventory levels. To mitigate these risks companies must invest in diversified sourcing strategies and robust supply chain management systems. However these measures require significant capital investment which can be burdensome for smaller players. The inherent unpredictability of agricultural production remains a critical challenge that requires continuous adaptation and resilience.

Intense Competition from Fresh and Frozen Alternatives

Intense competition from fresh and frozen fruit segments is negatively impacting the canned fruits market. These alternatives are perceived as superior in terms of taste, texture, and nutritional value. Advances in cold chain logistics and freezing technologies have made fresh and frozen fruits more accessible and affordable eroding the traditional advantages of canned products. According to the United States Department of Agriculture frozen fruits retain nearly all their nutrients and often have a better texture than canned varieties which can become soft during the heating process. The proliferation of supermarkets and online grocery platforms has improved the availability of fresh produce year round reducing the necessity for canned alternatives. The rise of farm to table movements and local sourcing initiatives further boosts the appeal of fresh fruits. Frozen fruits also offer convenience similar to canned products but without the addition of syrups or preservatives making them a healthier choice. This competitive pressure forces canned fruit manufacturers to innovate and differentiate their products through unique flavors packaging and marketing strategies. However overcoming the entrenched preference for fresh and frozen alternatives remains a significant hurdle. The perception that canned fruits are inferior in quality persists despite improvements in processing techniques. To remain competitive the industry must effectively communicate the benefits of canned fruits such as affordability and shelf stability while addressing quality concerns.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.35% |

| Segments Covered | By Type, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Del Monte, ConAgra Foods, Dole Food Company, The Kraft Heinz Company, Seneca Foods, CHB Group, Rhodes Food Group, Conserve, Tropical Food Industries, Kangfa Foods, H.J Heinz, Ardo, and others. |

SEGMENTAL ANALYSIS

By Type Insights

The peaches segment dominated the global canned fruits market and accounted for a 39.9% share in 2025. This dominance of the segment is driven by its widespread culinary versatility and deep-rooted consumer preference across multiple regions. The fruit is extensively used in both sweet and savory applications ranging from desserts and yogurts to salads and grilled dishes which ensures consistent demand throughout the year. According to the United States Department of Agriculture peaches are among the most consumed stone fruits globally with a significant portion processed into canned formats to extend shelf life beyond the short harvest season. The texture of canned peaches remains firm yet tender making them ideal for various cooking methods without disintegrating. This functional attribute is highly valued by food service providers and home cooks alike. The National Peach Council and various nutritional studies indicate that canned peaches are a reliable source of Vitamin A, Vitamin E, and folate; however, Vitamin C levels are generally lower in canned varieties than in fresh fruit due to thermal processing. In North America and Europe peaches are a staple in household pantries often purchased in bulk during promotional periods. The availability of diverse varieties including yellow and white peaches caters to different taste preferences further broadening the consumer base. Additionally the strong brand recognition of major peach producing regions such as Georgia in the United States and certain provinces in China enhances consumer trust. The established supply chain infrastructure for peaches ensures consistent quality and availability which solidifies their market leadership. Manufacturers continue to innovate with packaging sizes and syrup options to meet evolving consumer needs maintaining the dominance of this segment. The high production volume of peaches coupled with efficient processing infrastructure significantly contributes to their dominance in the canned fruits market. Major producing countries such as China Italy and the United States have developed robust agricultural systems dedicated to peach cultivation ensuring a steady supply of raw materials for canning facilities. This abundance allows for economies of scale in processing which reduces unit costs and makes canned peaches affordable for a wide range of consumers. The advanced processing technologies employed in these regions ensure minimal waste and high retention of sensory qualities. Also, the efficiency of the supply chain from orchard to can reduces lead times and maintains product freshness. Furthermore the seasonal nature of peach harvesting drives the need for preservation making canning the primary method for storing surplus production. This structural alignment between agricultural output and industrial capacity ensures that peaches remain readily available and competitively priced. The continuous investment in processing plants by major food companies further strengthens the market position of canned peaches. The reliability of supply and cost effectiveness make peaches the preferred choice for retailers and consumers sustaining their leading status in the global market.

The mixed fruits segment is predicted to witness the highest CAGR of 4.8% between 2026 and 2034 due to the increasing consumer desire for variety and nutritional diversity. Modern consumers particularly in urban areas seek convenient ways to consume a wide range of fruits without the hassle of purchasing and preparing multiple types. Canned fruit mixes typically include combinations of peaches pears grapes pineapples and cherries offering a balanced blend of flavors and textures. Mixed fruit cans provide an easy solution for adding color and nutrition to breakfast cereals salads and desserts. The World Health Organization recommends consuming at least 400 grams of fruits and vegetables per day and mixed cans help consumers achieve this goal efficiently. The appeal of exotic combinations that may not be readily available fresh in certain regions further drives adoption. For instance tropical fruit mixes featuring mangoes and papayas are gaining popularity in temperate climates. The ability to offer a comprehensive fruit experience in a single purchase appeals to busy families and health conscious individuals. This shift in preference toward diversified and convenient nutritional options fuels the rapid expansion of the mixed fruits segment. The cost effectiveness of mixed fruit cans and their role in reducing food waste appeal strongly to value conscious consumers contributing to the segment's rapid growth. Producing mixed fruit cans allows manufacturers to utilize fruits of varying sizes and slight cosmetic imperfections that might otherwise be discarded if sold as premium single fruit products. According to the Food and Agriculture Organization of the United Nations reducing food loss and waste is a global priority and processing mixed fruits helps maximize the utility of agricultural output. This efficiency translates into lower prices for consumers making mixed fruit cans an affordable option for households managing tight budgets. Mixed cans also reduce the risk of spoilage for consumers who may not consume large quantities of a single fruit type before it goes bad. By providing smaller portions of multiple fruits these products minimize household waste. Retailers often promote mixed fruit cans as budget friendly staples further driving volume sales. The perception of getting more value for money through variety and quantity encourages repeat purchases. Additionally the longer shelf life of canned mixed fruits allows for bulk buying during sales events enhancing savings. This combination of economic benefits and sustainability advantages positions mixed fruits as a rapidly growing segment in the global canned fruits market.

By Form Insights

The cut fruits segment led the canned fruits market and captured a 61.5% share in 2025. This leading position of the segment is attributed to the convenience and ease of consumption they offer. Modern lifestyles characterized by busy schedules and limited time for food preparation have increased the demand for ready to eat formats. Canned cut fruits eliminate these labor intensive steps allowing consumers to enjoy fruit immediately upon opening the container. This convenience is particularly appealing to parents preparing school lunches and individuals seeking quick snacks. Cut fruits are also easier to incorporate into various recipes such as fruit salads yogurt parfaits and baked goods enhancing their utility. The consistent size and shape of canned cuts ensure uniform presentation which is valued in commercial food service settings. The widespread availability of cut fruits in various pack sizes from single serve cups to family cans caters to diverse consumption occasions. This alignment with consumer needs for speed and simplicity solidifies the dominance of the cut fruits segment in the global market. The versatility of cut fruits in culinary applications supports their high demand and leading position in the canned fruits market. Sliced and chunked fruits are integral ingredients in a wide array of dishes ranging from breakfast cereals and smoothies to desserts and savory salads. Chefs appreciate the uniformity of canned cuts which ensures predictable results in recipes. Cut peaches and pears are commonly used in tarts and cobblers while pineapple chunks are essential for pizzas and stir fries. Canned cut fruits also retain their shape well during cooking making them suitable for grilling and baking. This functional reliability makes them a preferred choice for both home cooks and professional chefs. The ability to mix different cut fruits creates visually appealing and nutritious meals enhancing their appeal. Additionally the availability of cut fruits in juice or light syrup allows for healthier preparation methods compared to heavy syrups. The adaptability of cut fruits to various dietary trends and culinary traditions ensures sustained demand. This broad applicability across multiple meal occasions and cuisines reinforces the leadership of the cut fruits segment in the global canned fruits market.

The whole fruits segment is estimated to register the fastest CAGR of 3.9% over the forecast period owing to the trend toward premiumization and aesthetic appeal. Consumers are increasingly seeking high quality visually impressive fruit options for special occasions and gourmet presentations. Whole canned fruits such as pears and peaches are perceived as more luxurious and artisanal compared to cut varieties. Whole fruits are often used in upscale desserts and hospitality settings where appearance is paramount. The intact structure of whole fruits preserves their natural shape and texture enhancing the dining experience. Whole fruits are also preferred for gifting and holiday celebrations where visual impact is important. Manufacturers are responding by offering whole fruits in premium packaging and high quality juices or light syrups. This positioning aligns with the growing demand for indulgent yet convenient food options. The perception of whole fruits as a premium product allows brands to command higher prices and margins. This shift toward quality and aesthetics drives the rapid expansion of the whole fruits segment in the global market. The preservation of superior texture and flavor in whole fruits enhances consumer preference and contributes to the segment's rapid growth. Whole fruits undergo less mechanical processing than cut varieties which helps maintain their structural integrity and natural taste. Consumers who are sensitive to the soft texture of cut canned fruits often prefer whole fruits for their firmer bite. This textural advantage makes whole fruits suitable for applications where structure is important such as poaching or serving as a standalone dessert. The reduced surface area exposed to the packing medium also minimizes flavor leaching ensuring a more intense fruit experience. This quality difference is increasingly recognized by discerning consumers who prioritize taste and texture. The availability of heirloom and specialty varieties in whole form further attracts niche markets. Manufacturers are highlighting these quality attributes in marketing campaigns to differentiate whole fruits from standard cut options. The emphasis on superior sensory experience drives the adoption of whole canned fruits among premium segments. This focus on quality and authenticity sustains the high growth trajectory of the whole fruits segment.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held the majority share of 58.6% of the canned fruits market in 2025. This supremacy of the segment is credited to its extensive product availability and the convenience of one stop shopping. These retail formats offer a wide variety of canned fruit brands types and pack sizes under one roof catering to diverse consumer preferences. The ability to compare prices and read labels in person enhances the shopping experience for value conscious consumers. Supermarkets often feature prominent displays and promotional offers on canned fruits driving impulse purchases and volume sales. The organized layout and categorization of products in supermarkets make it easy for shoppers to locate specific items. Additionally the presence of private label brands alongside national brands provides options for different budget levels. The consistent stock levels and reliable supply chain of supermarkets ensure that canned fruits are always available. This reliability builds consumer trust and loyalty. The integration of loyalty programs and digital coupons further incentivizes purchases in these channels. The dominance of supermarkets and hypermarkets is reinforced by their ability to meet the comprehensive needs of shoppers efficiently. The strong supply chain integration and competitive pricing strategies of supermarkets and hypermarkets significantly contribute to their dominance in the canned fruits market. Large retail chains have established direct relationships with manufacturers and distributors allowing them to negotiate favorable terms and maintain low prices. Supermarkets leverage their purchasing power to offer discounts and bulk deals on canned fruits attracting price sensitive shoppers. The efficient logistics networks of these retailers ensure timely replenishment of stocks reducing the risk of out of stock situations. This price competitiveness makes supermarkets the preferred channel for regular household purchases. Additionally the ability to launch store wide promotions and seasonal campaigns drives traffic and sales volume. The integration of online and offline channels through click and collect services further enhances convenience. Shoppers can order canned fruits online and pick them up at the store combining digital ease with physical accessibility. This omnichannel approach strengthens the position of supermarkets as the leading distribution channel. The combination of low prices wide selection and operational efficiency sustains their market leadership.

However, the online stores segment is anticipated to witness the fastest CAGR of 6.2% between 2026 and 2034. This quick surge of the segment is propelled by increasing digital penetration and the convenience of home delivery. The proliferation of smartphones and high speed internet has made online grocery shopping accessible to a broader audience. Online platforms offer an extensive range of canned fruit products including niche and international brands that may not be available in local stores. The ability to browse reviews and compare prices online empowers consumers to make informed decisions. Home delivery services eliminate the need for physical travel saving time and effort for busy individuals. This convenience is particularly valued by elderly consumers and those with limited mobility. The availability of subscription services for regular deliveries of staple items like canned fruits further enhances customer retention. Online retailers often provide detailed product information and nutritional data aiding health conscious shoppers. The seamless integration of payment gateways and secure transactions builds trust in online shopping. This combination of accessibility variety and convenience drives the rapid expansion of online stores in the canned fruits market. Personalized recommendations and targeted marketing strategies employed by online retailers enhance consumer engagement and drive the rapid growth of this channel. E commerce platforms utilize data analytics to understand consumer preferences and browsing behavior allowing them to offer tailored product suggestions. Online stores send customized emails and notifications about discounts on preferred canned fruit brands encouraging repeat purchases. The ability to create wish lists and save favorite items simplifies the shopping process for returning customers. Social media integration allows brands to reach potential buyers through targeted ads and influencer collaborations. Online retailers also offer bundled deals and cross selling opportunities based on purchase history increasing average order values. The transparency of online reviews and ratings helps build confidence in product quality. Additionally the ease of returning unsatisfactory items reduces purchase risk. These digital enhancements create a engaging and user friendly shopping experience. The focus on personalization and customer-centric services distinguishes online stores from traditional retail channels. This strategic use of technology and data drives the exceptional growth of online stores in the canned fruits distribution landscape.

REGIONAL ANALYSIS

North America Canned Fruits Market Analysis

North America was the top performer in the global canned fruits market and accounted for a 35.7% share in 2025. This growth trajectory of the North American market is supported by high demand for convenience foods and established retail infrastructure. The market position in this region shows a mature consumer base that values shelf stable and nutritious options. The prevalence of dual income households and busy lifestyles drives the preference for ready to eat fruits. Retail giants such as Walmart and Kroger dominate the distribution landscape offering extensive varieties of canned fruits. The trend toward clean label and organic products is gaining traction with consumers seeking healthier options. Manufacturers are responding by introducing fruits packed in water or natural juices. The strong regulatory framework ensures high safety and quality standards. The integration of e commerce platforms has expanded access to specialized and premium canned fruit products. The region benefits from advanced agricultural practices and efficient supply chains. However competition from fresh and frozen alternatives remains a challenge. The market continues to evolve with innovations in packaging and product formulations. The focus on sustainability and health will shape future growth trajectories in North America.

Europe Canned Fruits Market Analysis

Europe followed closely behind in the global canned fruits market and captured a 25.6% share in 2025. This growth of the European market is fuelled by strong environmental regulations and health consciousness. The market status in this region is defined by a preference for sustainable and organic products. Consumers in countries like Germany France and the United Kingdom are increasingly avoiding products with added sugars and artificial preservatives. This has led to a rise in demand for canned fruits packed in natural juices. The region has a well established tradition of fruit preservation particularly in Southern Europe where peaches and apricots are popular. Retailers are focusing on private label organic ranges to meet consumer demands. The European Union’s strict labeling requirements ensure transparency for shoppers. The shift toward plant based diets also boosts fruit consumption. However the market faces challenges from high production costs and regulatory compliance. Innovation in biodegradable packaging is a key area of development. The emphasis on sustainability and health drives the European canned fruits market toward premium and eco conscious segments.

Asia Pacific Canned Fruits Market Analysis

Asia Pacific is moving faster than any other region in the global canned fruits market due to rising disposable incomes and urbanization. This regional market is shifting toward Western diets and convenience foods. The growing middle class in urban areas has greater access to supermarkets and hypermarkets where canned fruits are widely available. The demand for tropical fruits such as pineapples and lychees in canned forms is high both domestically and for export. Cultural factors such as the use of fruits in traditional desserts and festivals also drive consumption. E commerce is rapidly expanding providing access to a wider variety of products. However the market faces challenges from competition with fresh local fruits which are often cheaper. Manufacturers are focusing on affordable pricing and localized flavors. The region offers significant potential for growth as infrastructure improves and consumer awareness increases. The balance between traditional preferences and modern convenience shapes the market dynamics in Asia Pacific.

Latin America Canned Fruits Market Analysis

Latin America witnessed a consistent growth in the global canned fruits market owing to strong agricultural production and export orientation. The region is a major producer of tropical fruits such as pineapples peaches and pears. Domestic consumption is driven by the affordability and shelf stability of canned fruits in regions with varying access to fresh produce. The economic volatility in some countries makes shelf stable foods a practical choice for households. Export markets particularly in North America and Europe drive production volumes. Local manufacturers are improving quality standards to meet international requirements. The rise of modern retail formats in urban centers is increasing availability. However the market faces challenges from infrastructure limitations and economic instability. The focus on value added products and organic certifications offers growth opportunities. The region’s rich biodiversity provides a diverse range of fruit options. The balance between domestic needs and export demands defines the Latin American canned fruits market.

Middle East and Africa Canned Fruits Market Analysis

The Middle East and Africa region is anticipated to expand significantly in the global canned fruits market over the forecast period due to import dependency and growing urbanization. The region relies heavily on imports to meet demand for canned fruits due to limited local processing capacity. In the Middle East high disposable incomes and a large expatriate population drive demand for diverse food products including canned fruits. The hot climate in many parts of the region makes shelf stable foods particularly attractive. Supermarkets in Gulf Cooperation Council countries offer a wide range of imported canned fruits. In Africa the market is fragmented with informal trade playing a significant role. However modern retail is expanding in major cities. The lack of cold chain infrastructure enhances the appeal of canned products. Challenges include high import costs and logistical barriers. Opportunities exist in developing local processing industries. The region’s growth is linked to economic development and infrastructure improvements. The focus on food security and nutrition will drive future market expansion in the Middle East and Africa.

COMPETITIVE LANDSCAPE

The competition in the global canned fruits market is characterized by the presence of established multinational corporations and regional players vying for dominance through product differentiation and price competitiveness. Major companies leverage their extensive distribution networks and brand recognition to maintain strong market positions while smaller firms compete on niche products and local preferences. The market is moderately consolidated with key players controlling significant production capacity. Innovation in healthy formulations such as low sugar and organic variants serves as a primary differentiator. Price wars are common in commoditized segments forcing businesses to optimize costs without compromising quality. The rise of private label brands from major retailers intensifies pressure on branded manufacturers to justify premium pricing. Sustainability credentials including ethical sourcing and eco friendly packaging are increasingly critical for brand loyalty. Regulatory compliance regarding food safety and labeling standards shapes competitive dynamics. Companies must continuously adapt to changing consumer preferences for convenience and health. The integration of digital sales channels offers new avenues for growth and customer engagement. Overall the market demands strategic agility and continuous innovation to sustain profitability amidst fluctuating raw material costs and evolving dietary trends.

KEY MARKET PLAYERS

The key players in the global canned fruits market are

- Del Monte

- ConAgra Foods

- Dole Food Company

- The Kraft Heinz Company

- Seneca Foods

- CHB Group

- Rhodes Food Group

- Conserve

- Tropical Food Industries

- Kangfa Foods

- H.J Heinz

- Ardo

Top Players in the Market

- Del Monte Fresh Produce Inc is a leading global entity in the canned fruits sector renowned for its extensive portfolio of high quality preserved fruit products. The company leverages its vertically integrated supply chain to ensure consistent quality from farm to shelf. Recent strategic initiatives include the expansion of its sustainable sourcing practices and the introduction of eco friendly packaging solutions to meet evolving consumer demands. Del Monte has also invested in digital marketing campaigns to enhance brand visibility and engage with health conscious consumers. By focusing on innovation in product formulations such as reduced sugar options the company strengthens its competitive edge. Their commitment to corporate social responsibility and community engagement further solidifies their reputation. These actions collectively enhance their market presence and drive long term growth in the global canned fruits industry.

- Dole plc stands as a major participant in the global canned fruits market offering a diverse range of tropical and temperate fruit products. The company utilizes its vast global network to source premium fruits ensuring year round availability for consumers. Recent efforts to strengthen its position include the acquisition of strategic assets to expand processing capabilities and distribution reach. Dole has prioritized sustainability by implementing water conservation techniques and reducing plastic usage in packaging. The company actively promotes the nutritional benefits of canned fruits through educational initiatives targeting families and schools. By leveraging data analytics for demand forecasting Dole optimizes inventory management and reduces waste. These strategic moves enhance operational efficiency and brand loyalty. The focus on health and wellness aligns with current consumer trends driving sustained demand for their products across various international markets.

- Conagra Brands Inc contributes significantly to the global canned fruits market through its well known brands such as Hunt’s and Libby’s. The company focuses on delivering convenient and affordable fruit options to households worldwide. Recent actions to bolster its market position include the reformulation of products to reduce added sugars and artificial ingredients. Conagra has expanded its e commerce presence by partnering with online grocery platforms to reach digital native consumers. The company invests in supply chain resilience to mitigate disruptions and ensure consistent product availability. By emphasizing transparency in sourcing and production Conagra builds trust with environmentally conscious shoppers. Their innovative marketing strategies highlight the versatility of canned fruits in modern cooking. These initiatives reinforce their leadership status and drive growth in an increasingly competitive landscape.

Top Strategies Used by Key Market Participants

Key players in the canned fruits market predominantly employ product innovation and sustainability initiatives to maintain competitive advantage. Companies are reformulating products to reduce sugar content and eliminate artificial preservatives aligning with health conscious consumer preferences. Strategic investments in eco friendly packaging such as recyclable cans and biodegradable labels address environmental concerns. Expansion into emerging markets through localized product offerings and distribution partnerships drives volume growth. Digital transformation enhances supply chain efficiency and customer engagement via e commerce platforms. Mergers and acquisitions enable consolidation and access to new technologies or geographic regions. Marketing campaigns emphasize nutritional benefits and convenience to counter negative perceptions of processed foods. Collaborations with retailers for private label production expand market reach. These multifaceted strategies ensure resilience and growth in the dynamic global canned fruits sector.

MARKET SEGMENTATION

This research report on the global canned fruits market has been segmented and sub-segmented based on Type, Distribution channel, & region.

By Type

- Organic Fruits

- Inorganic Fruits

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Retailers

- Online Retails

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the canned fruits market?

The canned fruits market refers to the production, packaging, distribution, and sale of fruits preserved in cans using syrup, juice, or water to extend shelf life.

2. What factors are driving the growth of the canned fruits market?

Market growth is driven by increasing demand for convenient food products, longer shelf life, rising urbanization, and expanding retail distribution networks.

3. What are the most commonly canned fruits?

Commonly canned fruits include peaches, pineapples, pears, apricots, cherries, mixed fruits, and mandarin oranges.

4. Which distribution channels dominate the canned fruits market?

Supermarkets and hypermarkets lead distribution, followed by convenience stores, online retail platforms, and wholesale outlets.

5. How does convenience influence demand for canned fruits?

Canned fruits offer ready to eat options with minimal preparation, making them attractive for busy consumers and food service operators.

6. Who are the key players in the canned fruits market?

The market consists of multinational food processing companies, regional manufacturers, and private label brands supplying retail chains.

7. What role does the food service industry play in market growth?

The food service sector drives demand for canned fruits in desserts, bakery products, salads, and catering applications.

8. Which regions dominate the global canned fruits market?

North America and Europe are significant markets due to high consumption of processed foods and established food processing industries.

9. What challenges does the canned fruits market face?

Challenges include consumer preference for fresh produce, concerns about added sugar content, packaging costs, and supply chain disruptions.

10. What is the future outlook for the canned fruits market?

The market is expected to grow steadily due to increasing demand for long shelf life products, innovation in low sugar options, and expansion in emerging economies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com