Global CAR T Cell Therapy Market Size, Share, Trends & Growth Forecast Report By Target Antigen (CD20, EGFRV III, CD19, HER2, MESO, CD22, BCMA, GD2, CD30, HER1 and CD33), and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 to 2033.

Global CAR T Cell Therapy Market Size

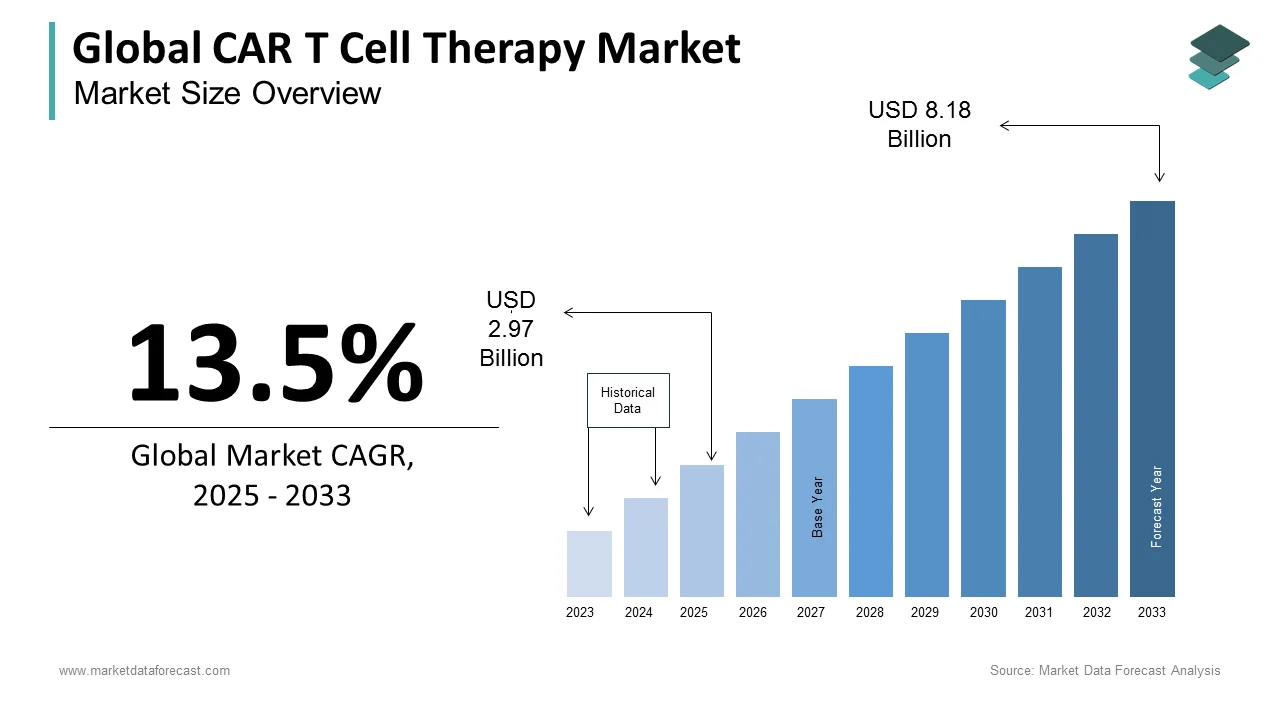

The size of the global CAR T cell therapy market was worth USD 2.62 billion in 2024. The global market is anticipated to grow at a CAGR of 13.5% from 2025 to 2033 and be worth USD 8.18 billion by 2033 from USD 2.97 billion in 2025.

Chimeric Antigen Receptor T-cell (CAR T-cell) therapy represents a transformative modality in oncology, involving the genetic reprogramming of a patient’s own T-cells to target and eliminate malignant cells. This personalized immunotherapy has demonstrated profound efficacy in hematologic malignancies, particularly relapsed or refractory B-cell cancers. About 70,000-85,000 patients globally have undergone autologous CAR T-cell infusions across clinical and commercial settings, according to the International Society for Cell & Gene Therapy. The treatment process involves leukapheresis, ex vivo T-cell modification using viral vectors, expansion, and reinfusion, requiring specialized infrastructure and coordination. The U.S. Food and Drug Administration has approved six CAR T-cell therapies since 2017, with an additional 17 in late-stage trials as per the American Society of Hematology. The therapy’s integration into national cancer care pathways, particularly in high-income countries, reflects a shift toward precision medicine, supported by advancements in gene editing and cellular logistics.

MARKET DRIVERS

Rising Prevalence of Hematologic Cancers Requiring Advanced Therapies

The escalating incidence of refractory hematologic malignancies is a principal catalyst for CAR T-cell therapy adoption. In the United States alone, approximately 86,000 new cases of non-Hodgkin lymphoma were diagnosed in 2023, with 30% progressing to relapsed or refractory stages unresponsive to conventional treatments, as reported by the National Cancer Institute. Similarly, global myeloma diagnoses exceeded 160,000 annually, according to the International Myeloma Foundation, many of whom become eligible for CAR T-cell intervention after second-line treatment failure. This clinical efficacy, combined with limited alternative options, has positioned CAR T-cell therapy as a standard-of-care option, driving demand across academic medical centers and comprehensive cancer networks.

Expansion of Regulatory Approvals and Clinical Trial Success Across Indications

The broadening scope of approved and investigational applications for CAR T-cell therapy is accelerating clinical uptake. Since the first FDA approval of tisagenlecleucel in 2017 for pediatric acute lymphoblastic leukemia (ALL), regulatory greenlights have expanded to include multiple myeloma, follicular lymphoma, and mantle cell lymphoma. Clinical trial data reinforce this momentum: the KarMMa-3 study demonstrated that idecabtagene vicleucel reduced the risk of disease progression or death by 58% in relapsed multiple myeloma patients, as reported by the Mayo Clinic Proceedings. These outcomes have prompted oncologists to integrate CAR T-cell therapy earlier in treatment algorithms. Furthermore, the global clinical trial registry lists about 700-800 active CAR T-cell studies, indicating robust pipeline development and increasing physician familiarity with the modality.

MARKET RESTRAINTS

Prohibitive Treatment Costs and Limited Reimbursement Frameworks

The financial burden associated with CAR T-cell therapy remains a critical barrier to widespread access. Commercial treatments in the U.S. range from $373,000 to $475,000 per infusion, excluding hospitalization, toxicity management, and follow-up care, which can elevate total costs beyond $800,000, as per the Health Care Cost Institute. Despite their clinical value, reimbursement systems in many countries lack standardized coverage policies. In Europe, only a few EU member states fully reimburse approved CAR T-cell therapies. In low- and middle-income nations, the absence of dedicated cell therapy funding mechanisms renders treatment inaccessible to the vast majority of eligible patients. Even in the U.S., payer restrictions and prior authorization hurdles delay treatment for a portion of referred patients. These economic constraints severely limit scalability and equity in delivery.

Complex Manufacturing and Logistics Infrastructure Requirements

The autologous nature of CAR T-cell therapy necessitates a highly sophisticated, time-sensitive production chain that constrains scalability. Each batch is patient-specific, requiring leukapheresis, cryopreservation, shipment to centralized facilities, genetic modification, expansion, and return shipment all within a 16- to 22-day window. As per the Foundation for the Accreditation of Cellular Therapy, 18% of manufacturing attempts fail due to T-cell dysfunction or contamination, leading to treatment cancellation. The reliance on a limited number of GMP-compliant facilities, primarily in North America and Western Europe, exacerbates delays; median vein-to-vein time is 28 days. Geopolitical and logistical disruptions, such as air freight limitations, further jeopardize product integrity. These operational complexities hinder rapid patient access and increase the risk of clinical deterioration during the manufacturing interval, particularly for those with aggressive disease.

MARKET OPPORTUNITIES

Development of Allogeneic "Off-the-Shelf" CAR T-Cell Platforms

The advancement of allogeneic CAR T-cell therapies presents a transformative opportunity to overcome autologous limitations. Unlike patient-specific therapies, allogeneic versions are derived from healthy donors and can be manufactured at scale for immediate use. Companies like Allogene Therapeutics and CRISPR Therapeutics are pioneering this approach, with ALLO-501 demonstrating a 65-75% overall response rate in a Phase II trial for relapsed non-Hodgkin lymphoma. The potential to reduce vein-to-vein time from weeks to days significantly enhances treatment accessibility. Also, several allogeneic CAR T-cell programs are in active clinical development. Furthermore, standardized production could lower costs, making the therapy viable for broader healthcare systems and accelerating global adoption.

Expansion into Solid Tumor Applications Through Target Antigen Innovation

Overcoming the historical inefficacy of CAR T-cell therapy in solid tumors represents a pivotal growth frontier. Recent advances in identifying tumor-specific antigens, such as B7-H3 in pediatric brain cancers and CLDN18.2 in gastric adenocarcinoma, are enabling more precise targeting. At the 2023 Society for Immunotherapy of Cancer conference, data from a Phase I trial of a mesothelin-targeted CAR T-cell therapy showed partial responses in 35% of patients with advanced pancreatic cancer. Additionally, the integration of gene editing tools like CRISPR to enhance T-cell infiltration and persistence in immunosuppressive tumor microenvironments is yielding promising results. As per the MD Anderson Cancer Center, about 100-130 clinical trials are now evaluating CAR T-cell constructs against solid tumors, including glioblastoma, ovarian, and lung cancers. Success in even one major solid tumor indication could exponentially expand the eligible patient pool, fundamentally reshaping the therapy’s clinical footprint.

MARKET CHALLENGES

Management of Severe Treatment-Related Toxicities

The clinical deployment of CAR T-cell therapy is complicated by significant safety risks, particularly cytokine release syndrome (CRS) and immune effector cell-associated neurotoxicity syndrome (ICANS). CRS occurs in up to 77% of recipients, with 12% experiencing grade 3 or higher severity requiring ICU-level care, as per the Journal of Clinical Oncology. ICANS affects approximately 20% of patients, manifesting as confusion, seizures, or cerebral edema. The need for specialized monitoring and rapid intervention limits administration to accredited centers with neurology and critical care support. Although tocilizumab and corticosteroids are used to mitigate CRS, long-term neurological sequelae remain poorly understood, raising concerns about risk-benefit assessment in vulnerable populations.

Immune Escape and Antigen Loss Leading to Disease Relapse

A persistent clinical challenge is the recurrence of malignancy following initial response, often due to antigen-negative tumor escape. In patients treated with CD19-targeted CAR T-cells, up to 50% of relapses involve the loss of CD19 expression on malignant B-cells, as reported by the Dana-Farber Cancer Institute. This phenotypic shift allows tumor cells to evade immune detection despite sustained CAR T-cell persistence. Dual-targeting strategies, such as CD19/CD20 or CD19/CD22 constructs, are being explored to counter this mechanism. Also, bicistronic CAR T-cells reduced antigen escape in pediatric ALL patients. However, tumor heterogeneity and clonal evolution remain formidable obstacles. As per Nature Reviews Clinical Oncology, antigen modulation is now recognized as a dominant resistance pathway, necessitating continuous innovation in target selection and combinatorial approaches to sustain remission.

SEGMENTAL ANALYSIS

By Target Antigen Insights

The CD19-targeted CAR T-cell therapy segment dominated the global market by capturing 53.8% of total revenue in 2024. This preeminence is primarily driven by its well-established clinical validation across multiple B-cell malignancies. CD19 is uniformly expressed on malignant and normal B-cells, making it an ideal target for lymphoid cancers. The U.S. Food and Drug Administration has approved five CD19-directed therapies, including tisagenlecleucel, axicabtagene ciloleucel, and brexucabtagene autoleucel for indications such as diffuse large B-cell lymphoma, follicular lymphoma, and B-cell acute lymphoblastic leukemia. Also,the majority of all CAR T-cell infusions administered globally between 2018 and 2023 targeted CD19. Furthermore, long-term follow-up data from the ELIANA trial demonstrated a 40% event-free survival rate at five years in pediatric ALL patients, reinforcing confidence in its durability. The antigen’s specificity, combined with extensive real-world evidence and integration into national treatment guidelines, solidifies CD19 as the cornerstone of current CAR T-cell applications.

The BCMA (B-cell maturation antigen)-targeted CAR T-cell therapy segment is the fastest-growing segment and is projected to expand at a CAGR of 27.3% from 2025 to 2033. This surge is fueled by the rising unmet need in relapsed or refractory multiple myeloma, a plasma cell disorder affecting over 160,000 individuals annually worldwide, as documented by the International Myeloma Foundation. The approval of idecabtagene vicleucel (Abecma) and cilta-cel (Carvykti) has catalyzed clinical adoption, with the KarMMa-3 trial showing a 73% reduction in progression risk compared to standard regimens, as reported by the Mayo Clinic. Additionally, a portion of multiple myeloma patients become eligible for BCMA-directed therapy after failing two prior lines of treatment. The antigen’s exclusive expression on plasma cells minimizes off-target toxicity, enhancing therapeutic safety. With more than 30 late-stage clinical trials evaluating next-generation BCMA constructs, including dual-targeting and armored CARs, this segment is poised for sustained acceleration.

By Application Insights

The multiple myeloma segment captured the major share of the global CAR T cell therapy market in 2024 and is anticipated to continue its domination throughout the forecast period.

The chronic lymphocytic leukemia segment is expected to grow at a notable CAGR during the forecast period.

The Diffuse large B-cell lymphoma (DLBCL) segment is another lucrative segment and is forecasted to hold a considerable share of the worldwide market during the forecast period.

By Product Insights

The autologous segment is anticipated to lead the CAR T Cell therapy market during the forecast period, owing to several potential competitors.

By Therapies Insights

The axicabtagene ciloleucel (Yescarta) segment is expected to have a notable share of the global CAR T cell therapy market during the forecast period, owing to the developing healthcare infrastructure and growing discretionary expenses.

By End User Insights

The biotechnology and pharmaceutical companies segment had a major share of the CAR T cell therapy market worldwide in 2024. The segment’s domination is expected to continue during the forecast period owing to the advanced research being carried out at the companies.

REGIONAL ANALYSIS

North America CAR T cell Therapy Market Analysis

North America held a commanding position in the CAR T-cell therapy market by accounting for 52.8% of the global share in 2024. The United States, in particular, serves as the epicenter of clinical and commercial deployment, having administered over 22,000 CAR T-cell infusions since 2017, according to the Center for International Blood and Marrow Transplant Research. The country hosts 150-200 FDA-designated treatment centers, each requiring stringent certification for toxicity management and patient monitoring. Medicare and major private insurers now cover all six approved CAR T-cell products, enabling broader access. Academic powerhouses such as the University of Pennsylvania and MD Anderson Cancer Center continue to lead in trial innovation and manufacturing optimization. The presence of key developers like Novartis, Gilead, and Bristol Myers Squibb further consolidates the region’s leadership, supported by robust regulatory pathways and patient advocacy networks that facilitate rapid therapy integration.

Europe CAR T cell Therapy Market Analysis

Europe holds a significant share, with Germany, the United Kingdom, and France emerging as primary hubs for CAR T-cell therapy adoption. The region has seen a year-on-year increase in treatment volumes since 2021. While regulatory approvals through the European Medicines Agency are in place, reimbursement disparities persist. Germany leads in clinical capacity, with 45 certified centers and a national registry tracking post-infusion outcomes. The UK’s National Health Service launched a centralized CAR T-cell program in 2020, standardizing access across England and treating over 1,200 patients by 2023. Additionally, the EU’s Horizon Europe initiative has allocated a substantial share to advance allogeneic CAR T research, fostering innovation. Despite logistical and funding challenges, Europe’s structured healthcare systems and strong research infrastructure support steady market maturation.

Asia Pacific CAR T cell Therapy Market Analysis

The Asia Pacific region accounts for a notable share of the global CAR T-cell therapy market, with China and Australia leading in clinical and regulatory advancement. China has emerged as a powerhouse in CAR T-cell development, with over 300 active clinical trials, more than any other nation, as per the Chinese Clinical Trial Registry. The National Medical Products Administration approved its first domestic CAR T-cell therapy, relma-cel, in 2021 for lymphoma, and by 2023, more than 5,000 patients had received treatment within the public system. Australia, though smaller in scale, has integrated CAR T-cell therapy into its national cancer plan, with 12 accredited centers and full reimbursement under the Pharmaceutical Benefits Scheme. Rising investment in GMP facilities and regional collaboration are accelerating access across the region.

Latin America CAR T cell Therapy Market Analysis

Latin America holds a decent share of the market, with Brazil and Mexico representing the most advanced ecosystems for CAR T-cell therapy. Brazil has taken a pioneering role, launching its first public-sector CAR T-cell program in 2022 at the Hospital das Clínicas in São Paulo, funded by the Ministry of Health. As of 2023, over 300 patients had received therapy through clinical trials or compassionate use programs, according to the Brazilian Society of Bone Marrow Transplantation. Mexico has authorized two CAR T-cell products for commercial use and established three specialized centers in Mexico City and Monterrey. However, high costs and limited manufacturing capabilities restrict scalability. Nonetheless, growing oncology investment and cross-border partnerships with U.S. institutions are laying the foundation for gradual expansion in treatment availability.

Middle East and Africa CAR T cell Therapy Market Analysis

The Middle East and Africa collectively represent a small share of the global market, yet exhibit nascent but strategic growth. Israel stands out as a regional leader, with Sheba Medical Center conducting CAR T-cell trials since 2019 and establishing a national production facility under the “Israel Bio Initiative.” Over 150 patients had been treated by 2023, as per the Israeli Ministry of Health. In South Africa, the University of Witwatersrand initiated a pilot program in 2022 to evaluate feasibility in resource-constrained settings. As per the African Organization for Research and Training in Cancer, fewer than 50 CAR T-cell infusions were performed across the continent by 2023, highlighting access disparities. However, regional interest in biotech sovereignty and partnerships with European and Asian manufacturers suggests potential for future development.

COMPETITIVE LANDSCAPE

Competition in the CAR T-cell therapy market is characterized by a dynamic interplay between multinational pharmaceutical leaders and agile biotech innovators, each vying for dominance in a high-stakes, technically demanding field. While companies like Novartis, BMS, and Gilead control commercialized autologous therapies, a surge of private and publicly traded biotechs, particularly in China and Israel, are advancing novel constructs and allogeneic platforms. The race is not only for market share but for technological supremacy, with differentiation emerging through target selection, safety profiles, and manufacturing efficiency. Regulatory divergence across regions adds complexity, requiring tailored approval and pricing strategies. Moreover, the high cost of therapy and infrastructure demands create barriers to entry, yet also foster collaboration between developers, hospitals, and governments. This competitive environment is accelerating innovation but also intensifying pressure to deliver durable responses, reduce toxicity, and broaden accessibility beyond elite medical centers.

KEY MARKET PLAYERS

Companies playing a leading role in the global CAR T cell therapy market profiled in this report are

- Mustang Bio, Inc.

- Celgene Corporation

- Bluebird Bio, Inc.

- CARsgen Therapeutics, Ltd.

- Novartis International AG

- Legend Biotech

- Sorrento Therapeutics Inc.

- Kite Pharma, Inc.

- Immune Therapeutics

- Bellicum Pharmaceuticals, Inc.

- Pfizer, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Novartis has been a pioneer in CAR T-cell therapy with its FDA-approved product Kymriah (tisagenlecleucel), the first CAR T-cell treatment for pediatric B-cell acute lymphoblastic leukemia and adult diffuse large B-cell lymphoma. In the Asia Pacific region, Novartis has advanced its presence through strategic collaborations with leading cancer centers in Australia, Japan, and South Korea. Novartis also launched a digital patient tracking platform in Japan to monitor post-infusion outcomes, enhancing long-term care coordination. By supporting real-world evidence generation and engaging with regulatory bodies like China’s NMPA, Novartis is accelerating approval pathways and improving therapy accessibility across diverse healthcare systems in the region.

- Bristol Myers Squibb (BMS), through its acquisition of Celgene, gained Yescarta and later Tecartus, two CD19-targeted CAR T-cell therapies with established global footprints. In the Asia Pacific, BMS has intensified its focus on expanding access in Japan and Australia, where both products are commercially approved. The company also initiated a manufacturing feasibility study in Singapore to evaluate regional production, aiming to shorten vein-to-vein timelines. In Australia, BMS worked with state health departments to integrate Yescarta into public hospital networks, ensuring broader patient reach. These initiatives underscore BMS’s commitment to overcoming logistical and economic constraints while reinforcing clinical trust through robust safety monitoring and physician education programs.

- Juno Therapeutics (a Bristol Myers Squibb company), originally an independent innovator in cell therapy, developed cilta-cel (Carvykti), a BCMA-targeted CAR T-cell therapy for multiple myeloma. Although now under BMS, Juno’s R&D legacy continues to influence the company’s Asia Pacific strategy. BMS, leveraging Juno’s technology, initiated clinical trials in China in collaboration with local research institutions to assess efficacy in Asian patient populations. Additionally, the company launched a patient identification program in India to screen eligible myeloma cases for future therapy access. These efforts reflect a targeted expansion model that combines regulatory engagement, localized research, and early-stage patient pathway development to build sustainable market presence.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the CAR T-cell therapy market are deploying a multi-pronged strategic framework to consolidate leadership. Companies are investing heavily in next-generation engineering, including dual-targeting constructs, armored CARs, and gene-edited allogeneic platforms to enhance efficacy and reduce toxicity. Strategic partnerships with academic medical centers and government agencies are being leveraged to expand certified treatment centers and train clinical staff in toxicity management. Firms are also establishing regional manufacturing and logistics hubs to reduce vein-to-vein time and improve scalability. Reimbursement navigation is a critical focus, with companies engaging payers to develop outcome-based pricing models and risk-sharing agreements. Additionally, digital health integration, such as patient monitoring platforms and real-world data registries, is being utilized to demonstrate long-term value and support regulatory submissions across international markets.

GLOBAL CAR T CELL THERAPY MARKET NEWS

- In June 2023, Novartis launched a regional CAR T-cell training academy in Singapore in collaboration with SingHealth, aiming to standardize clinical protocols and expand certified treatment centers across Southeast Asia to strengthen its market presence.

- In February 2024, Bristol Myers Squibb initiated a localized manufacturing feasibility study in Japan to evaluate decentralized production of Yescarta, reducing vein-to-vein time and enhancing supply reliability in the Asia Pacific region.

- In September 2022, Juno Therapeutics, under BMS, commenced Phase III trials of cilta-cel in Chinese patients with relapsed multiple myeloma, marking a strategic expansion into one of the largest emerging markets for advanced cell therapies.

- In January 2023, Novartis introduced a digital patient monitoring platform in Japan for Kymriah recipients, enabling real-time tracking of adverse events and improving post-infusion care coordination to strengthen clinical trust.

- In May 2024, Bristol Myers Squibb partnered with the Australian Genomic Medicine Network to integrate Carvykti into national myeloma treatment pathways, facilitating faster adoption and reimbursement across public healthcare institutions.

REPORT COVERAGE

| Metric | Value |

|---|---|

| Base Year | 2024 |

| Market Size Available | 2024 to 2033 |

| Forecast Period | 2025 to 2033 |

| Quantitative Units | Market Size in USD Billion and CAGR from 2025 to 2033 |

| Various Analyses Included | Global, Regional & Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE; Porter's Five Forces; Competitive Landscape; Investment Opportunities |

| Segments Covered | Target Antigen, Application, Product, Therapies, and Region |

| Key Market Players | Mustang Bio, Inc., Celgene Corporation, Bluebird Bio, Inc., CARsgen Therapeutics, Ltd., Novartis International AG, Legend Biotech, Sorrento Therapeutics Inc., Kite Pharma, Inc., Immune Therapeutics, Bellicum Pharmaceuticals, Inc. and Pfizer, Inc. |

| Regions Analyzed | North America, Europe, APAC, Latin America, Middle East & Africa |

| Countries Covered | U.S, Canada, Mexico, UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Brazil, Argentina, Chile, KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Other Countries |

| Report Format | PDF, Excel, PPT, BI |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

MARKET SEGMENTATION

This research report on the global CAR T Cell therapy market is segmented and sub-segmented based on target antigen, application, product, therapies, and region.

By Target Antigen

- CD20

- EGFRV III

- CD19

- HER2

- MESO

- CD22

- BCMA

- GD2

- CD30

- HER1

- CD33

By Application

- Multiple Myeloma

- Chronic Lymphocytic Leukemia

- Mantle Cell Lymphoma

- Follicular Lymphoma

- Diffuse large B-cell lymphoma

- Acute Lymphoblastic Leukemia

By Product

- Allogeneic

- Autologous

By Therapies

- Axicabtagene ciloleucel (Yescarta)

- Tisagenlecleucel (Kymriah)

By End User

- Cancer Research Centers

- Hospitals

- Academic and Research Institutes

- Pharmaceutical Companies

- Biotechnology Companies

- Contract Research Organizations

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the CAR T Cell Therapy Market and how is it evolving?

The CAR T Cell Therapy Market is a rapidly growing sector focused on innovative cancer treatments using genetically modified T-cells. The market is expanding due to advances in gene editing and increasing cancer prevalence

2. Which types of cancers are primarily targeted in the CAR T Cell Therapy Market?

The CAR T Cell Therapy Market primarily targets hematologic cancers like lymphoma and leukemia, which respond well to this personalized immunotherapy approach

3. What are the major drugs driving the CAR T Cell Therapy Market growth?

Key drugs such as axicabtagene ciloleucel, Kymriah, Yescarta, and Breyanzi are the major contributors to the growth of the CAR T Cell Therapy Market

4. How does gene editing technology impact the CAR T Cell Therapy Market?

Gene editing technology significantly enhances the effectiveness and customization of treatments in the CAR T Cell Therapy Market, enabling precise targeting of cancer cells

5. What factors are fueling the growth of the CAR T Cell Therapy Market globally?

The growth of the CAR T Cell Therapy Market is fueled by rising cancer cases, increased R&D investments, regulatory approvals, and advancements in cell engineering and manufacturing

6. What are the challenges faced by the CAR T Cell Therapy Market?

The CAR T Cell Therapy Market faces challenges such as high treatment costs, side effects, complex manufacturing processes, and regulatory hurdles

7. How does the CAR T Cell Therapy Market vary by region?

The CAR T Cell Therapy Market is dominated by North America with the highest market share, while Europe and Asia-Pacific regions are witnessing rapid growth due to increasing healthcare infrastructure and awareness

8. What role do clinical trials play in the CAR T Cell Therapy Market?

Clinical trials are critical in the CAR T Cell Therapy Market for validating new treatments, improving efficacy, and gaining regulatory approvals

9. How is personalized medicine influencing the CAR T Cell Therapy Market?

Personalized medicine is central to the CAR T Cell Therapy Market, as therapies are customized for each patient's cancer antigen profile, enhancing treatment outcomes

10. What are the typical side effects reported in the CAR T Cell Therapy Market?

Common side effects in the CAR T Cell Therapy Market include cytokine release syndrome and neurotoxicity, which are important considerations for treatment management

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com