- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

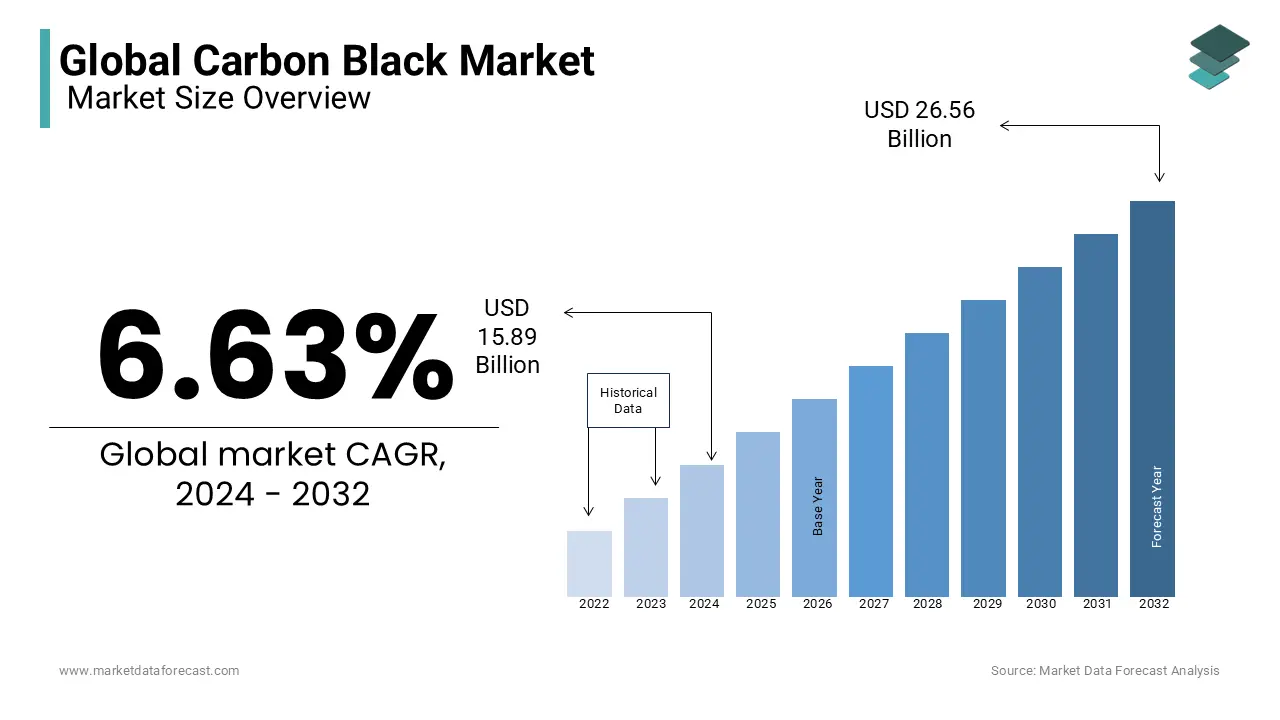

Market Size, 2025

$16.94 BnMarket Estimate, 2026

$18.06 BnMarket Forecast, 2034

$30.18 BnCAGR, 2026–2034

6.63%Global Carbon Black Market Size

The global carbon black market size was valued at USD 16.94 billion in 2025, and is expected to reach USD 30.18 billion by 2034 from USD 18.06 billion in 2026, growing at a CAGR of 6.63% from 2026 to 2034.

Carbon black is a fine particulate material produced through the incomplete combustion of heavy petroleum products or natural gas, engineered to impart reinforcement, UV stability, and electrical conductivity in rubber, plastics, and coatings. As per the study, global carbon black production consumed 13.6 million metric tons of feedstock in 2023. According to research, a portion of all carbon black produced globally is consumed in tire manufacturing, where it enhances tread wear resistance compared to non-reinforced elastomers.

MARKET DRIVERS

Rising Tire Replacement Demand Fuels Market Growth

The relentless global demand for replacement tires, which is fueled by rising vehicle parc and extended mobility in emerging economies is substantially escalating the growth of the carbon black market. The global light vehicle fleet surpassed large number of units, with average tire replacement intervals shortening to thousands of kilometers in high-heat regions like Southeast Asia and the Middle East. Most passenger vehicles globally remain in service for extended lifespans, which necessitates multiple tire replacements over time.

Essential Role in Industrial Rubber Applications Boosts Demand

The structural necessity of carbon black in specialty industrial rubber applications where failure is non-negotiable is escalating the growth of carbon black market. The conveyor belts in U.S. mining operations must withstand hundreds of hours of continuous abrasion, a performance benchmark met only by high-structure N220 and N330 carbon black grades. The American Petroleum Institute mandates carbon black-reinforced elastomers in offshore drilling risers, where elongation at break must exceed under 5,000 psi hydrostatic pressure, a specification unattainable with silica alone. Industrial hoses formulated with high carbon black content demonstrate significantly reduced hydrocarbon permeation by helping to prevent leaks and improve operational safety. Regulatory and safety imperatives, not cost, dictate its irreplaceability in mission-essential sectors.

MARKET RESTRAINTS

Stringent Emission Norms Limit Carbon Black Production

The tightening environmental regulation targeting carbon black’s production emissions and particulate release is restricting the growth of carbon black market. The furnace black producers must now capture most of process emissions up from previously, requiring millions per plant in scrubber retrofits, as per research. Environmental regulations in several regions mandate strict monitoring and control of volatile organic compounds and particulate emissions. Compliance has led to partial capacity reductions in some production areas and increased operational costs by creating financial pressures that are challenging for many producers to absorb.

Silica Substitution in Tires Restrains Market Expansion

The substitution burden from precipitated silica in high-performance tire treads, driven by fuel efficiency mandates is degrading the growth of carbon black market. Silica-reinforced green tires reduce rolling resistance compared to carbon black-dominant compounds, directly improving vehicle MPG. Michelin’s Sustainability Disclosure points out that a portion of its premium passenger tire lines now use hybrid silica-carbon black tread formulations to meet EU Label B ratings. The International Organization for Standardization’s ISO 20859 protocol quantifies hysteresis loss, where silica outperforms, which makes it the default choice for EVs requiring low heat buildup. The erosion of volume growth in the highest-margin segment is due to carbon black's displacement from tread compounds despite its continued dominance in carcass and sidewall layers.

MARKET OPPORTUNITIES

Conductive Carbon Black Powers EV Battery Innovation

The development of conductive carbon black grades for lithium-ion battery electrodes and electromagnetic shielding in electric vehicles is setting up new opportunities for the carbon black market. As per the study, anode slurries require conductive carbon black to ensure electron percolation by translating to 1.8 kg per EV battery pack. High-purity conductive carbon blacks are achieving substantially higher conductivity than conventional grades by enabling thinner electrodes and improved energy density in batteries. These materials are shifting from traditional rubber applications to essential components in electrochemical energy storage due to the rapid growth in electric vehicle production.

Recovered Carbon Black Spurs Circular Economy Growth

Integration into circular economy models via pyrolysis-derived recovery from end-of-life tires generates potential prospects for the carbon black market. As per the research, a portion of global tire waste is now processed via pyrolysis by yielding recoverable carbon black (rCB) per ton of feedstock. Recycled carbon black can partially replace virgin material in tire compounds while preserving most performance and significantly lowering the carbon footprint. Industry standards recognize these sustainable materials, which allows manufacturers to increase recycled content in products. Regulations are pushing for higher recovery and circularity.

MARKET CHALLENGES

Feedstock Price Volatility Impacts Profit Margins

The volatility of feedstock pricing, primarily decant oil and coal tar, challenges the rise of the carbon black market. It constitutes a portion of production cost. As per study, U.S. Gulf Coast decant oil prices surged due to FCC unit maintenance turnarounds, compressing carbon black margins, the lowest in a decade. Supply shortages of key carbon feedstocks have led to increased reliance on imports at higher prices, which creates volatility in material costs. This instability limits long-term contracting, shifts sales toward spot pricing, and exposes manufacturers to unpredictable expenses by complicating budgeting and planning in downstream industries.

Quality Issues in Recovered Carbon Black Limit Adoption

The technical incompatibility of recovered carbon black (rCB) with high-performance applications without extensive reprocessing degrades the growth of the carbon black market. As per the research, only a share of commercially available rCB meets the ash content threshold (<0.5%) required for tire-grade use, the rest contaminated with zinc, sulfur, or char residues from incomplete pyrolysis. Advanced recycling processes can increase the cost of producing recycled carbon black by reducing its price advantage over virgin material. Apart from these, unmodified recycled carbon black may lower performance in critical applications, which restrictes its use to non-structural components.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.63% |

| Segments Covered | By Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Phillips Carbon Black Limited (India), Black Bear Carbon BV (Netherlands), Longxing Chemical Group, Birla Carbon/Thai Carbon Black Public Company Limited (Thailand), Mitsubishi Chemical Corporation (Japan), Pyrolyx AG (Germany), Cabot Corporation (U.S.), Nippon Steel & Sumikin Chemical Co. Ltd. (Japan), OCI Company Ltd. (South Korea), Continental Carbon Company (US) |

SEGMENTAL ANALYSIS

By Type Insights

The furnace black segment dominated the carbon black market share in 2025. The prominence of the furnace black segment is driven by scalability and cost efficiency. As per study, modern furnace reactors yield tons of carbon black per ton of feedstock, with energy recovery systems reducing natural gas consumption. A further driver is performance versatility. Industrial standards classify numerous grades of furnace carbon black for different tire performance needs, from high-abrasion truck treads to low-hysteresis passenger tires. Major manufacturers rely heavily on furnace black because its adjustable structure and surface chemistry provide performance advantages not achievable with older production methods.

The acetylene black segment is on the rise and is expected to grow with a CAGR of 9.7% during the forecast period. The rapid growth of the acetylene black segment is propelled by lithium-ion battery demand. As per research, global EV battery production will require notable metric tons of conductive additives by 2030, a portion of which will be acetylene black due to its superior electrical percolation at 3–5% loading. A different driver is purity requirements. High-purity acetylene blacks with very low ash content are critical for preventing defects in advanced battery anodes.

By Application Insights

The tires segment led the carbon black market by capturing substantial share in 2025. The dominance of the tires segment is attributed to structural necessity. As per the research, tread compounds require carbon black loading to achieve ISO 20859-specified abrasion resistance by translating to passenger tire. A further driver is volume scale. Large tire manufacturers produce hundreds of millions of tires annually, each incorporating several kilograms of carbon black across various components. Even when alternative fillers are used in treads, significant amounts of carbon black remain in non-tread areas, a consumption volume unmatched by any other application segment.

The plastics segment is expected to exhibit a noteworthy CAGR of 8.9% over the forecast period owing to the conductive polymer demand in electric vehicles. According to study, global EV production will require metric tons of antistatic carbon black for battery trays, connectors, and charging housings by 2027. A different accelerant is UV stabilization in agricultural films. A large majority of greenhouse and polymer films now include small percentages of carbon black to extend durability under intense sunlight.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific was the largest region in the carbon black market by occupying 47.3% of share in 2025. The growth of the Asia Pacific in the global market is propelled by tire manufacturing concentration and infrastructure-led rubber consumption. As per study, China produced millions of metric tons of rubber products, consumed domestically in automotive and construction sectors. Tire production continues to expand in several regions, consuming millions of tons of carbon black annually, with the majority sourced from local furnace plants. Rapid growth in export-focused manufacturing hubs has added numerous new production lines, each demanding substantial annual carbon black supply. Feedstock access and proximity to rubber compounding centers cement APAC’s dominance.

North America Market Analysis

North America grew steadily in the carbon black market due to specialty-grade production and battery materials innovation. As per the research, a percentage of North American carbon black capacity is dedicated to acetylene and conductive grades, the highest regional concentration globally. Recent expansions in battery-grade carbon black production have increased supply for large-scale electric vehicle manufacturing. Stringent environmental regulations require significant investment in emission controls, reducing particulate releases. Compliance and labor costs constrain volume growth, but they support premium pricing for high-purity and specialty applications.

Europe Market Analysis

Europe is closely following in the carbon black market with 21.8% share owing to circular economy prominence and silica substitution burden. As per the research, a share of EU tire production now uses hybrid silica-carbon black tread formulations to meet EU Label rolling resistance thresholds. Simultaneously, Europe leads in recovered carbon black (rCB) adoption. Recycled carbon black is increasingly incorporated into a growing share of commercial tire lines. Regional production hubs for specialty carbon blacks continue to dominate supply for high-value applications, including battery additives by reflecting concentrated manufacturing capacity in key industrial markets. Stringent REACH and emissions standards constrain new capacity but drive innovation in purification and recycling.

Latin America Market Analysis

Latin America expanded gradually in the carbon black market which is concentrated in Brazil’s tire and mining sectors. As per research, domestic tire production consumed notable tons of carbon black, a percentage of sourced from local plants using coal tar feedstock. Mining is a important growth vector. Vale mandates carbon black-reinforced conveyor belts for all iron ore operations by specifying N220 grade for abrasion resistance under ISO 4649. Rapid expansion of agricultural plastics is driving strong annual growth in demand for UV-stabilized films.

Middle East & Africa Market Analysis

Middle East & Africa is likely to grow in the carbon black market, with growth anchored in Saudi Arabia’s petrochemical-integrated production and South Africa’s mining rubber demand. As per study, Jubail’s integrated refinery-carbon black complex produces large tons annually, exported to Asia and Europe due to limited local rubber industry. South Africa’s mining sector consumes notable tons/year of N330-grade carbon black for underground conveyor and hose applications, demand growing annually despite mine closures. In several regions, tire retreading industries rely heavily on imported furnace black for recap compounds, consuming substantial annual volumes.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the key players dominating the global carbon black market are

- Phillips Carbon Black Limited (India)

- Black Bear Carbon BV (Netherlands)

- Longxing Chemical Group

- Birla Carbon / Thai Carbon Black Public Company Limited (Thailand)

- Mitsubishi Chemical Corporation (Japan)

- Pyrolyx AG (Germany)

- Cabot Corporation (U.S.)

- Nippon Steel & Sumikin Chemical Co. Ltd. (Japan)

- OCI Company Ltd. (South Korea)

- Continental Carbon Company (U.S.)

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Leading players vertically integrate with refineries to secure feedstock under fixed-price contracts, mitigating volatility. They invest in emission control retrofits ahead of regulatory deadlines to ensure uninterrupted production. Companies establish regional technical centers to co-develop application-specific grades with local OEMs and compounders. Strategic expansions target battery materials hubs near gigafactories to capture premium conductive black demand. Circular economy positioning is prioritized, launching certified rCB lines to align with OEM sustainability KPIs. Digital platforms streamline ordering and logistics, which locks high-volume industrial customers through service differentiation rather than price.

COMPETITION OVERVIEW

The carbon black market is defined by a strategic contest among global integrated producers, regional specialists, and circular economy disruptors, each competing through feedstock security, emission compliance, and application innovation. Incumbents leverage decades of rubber compounding expertise, while challengers exploit battery-grade purity or rCB sustainability credentials. Competition pivots on regulatory resilience, plants lacking scrubbers face shutdowns, not margin burden. Vendor selection is increasingly dictated by proximity to gigafactories, customization agility, and ESG-aligned material passports.

TOP PLAYERS IN THE MARKET

- Birla Carbon operates production facilities across Asia Pacific by supplying furnace and specialty grades to tire, plastics, and battery sectors. The company strengthened its position by launching Purplex, a low-PAH furnace black for Japanese automotive seals compliant. Birla also partnered to co-develop conductive grades for EV battery trays, which embeds its formulations into domestic OEM supply chains while reducing logistics lead times.

- Orion supplies high-purity acetylene and specialty furnace blacks to Asia Pacific’s battery and industrial rubber markets. The company supported its foothold by establishing a technical center in Shanghai to customize N-series grades for Chinese EV gasket and hose manufacturers. Orion also signed a long-term feedstock agreement to secure coal tar supply, which mitigates regional price volatility. Its ISO 14001-certified emissions control systems enable compliance with China’s Ultra-Low Emission standards by avoiding production curtailments.

- Cabot delivers performance-driven carbon blacks for tires, plastics, and lithium-ion batteries across Asia Pacific. Cabot also integrated real-time emissions monitoring across its Malaysia and Indonesia plants to comply with ASEAN environmental directives.

MARKET SEGMENTATION

This research report on the global carbon black market has been segmented and sub-segmented based on type, application, and region.

By Type

- Acetylene

- Furnace

- Channel

- Thermal

- Others.

By Pigment Source

- Ivory Black

- Vine Black

- Lamp Black

- Ivory black

By Application

- Tyres

- Non-Tyre Rubber

- Inks & Coatings

- Plastic

- Others

By Grade

- Standard Grade

- Specialty Grade.

By Region

- North America

- Latin America

- Europe

- Asia Pacific

- Middle East & Africa