Global CDMO Market Size, Share, Trends & Growth Forecast Report By Service (CMO and CRO) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global CDMO Market Size

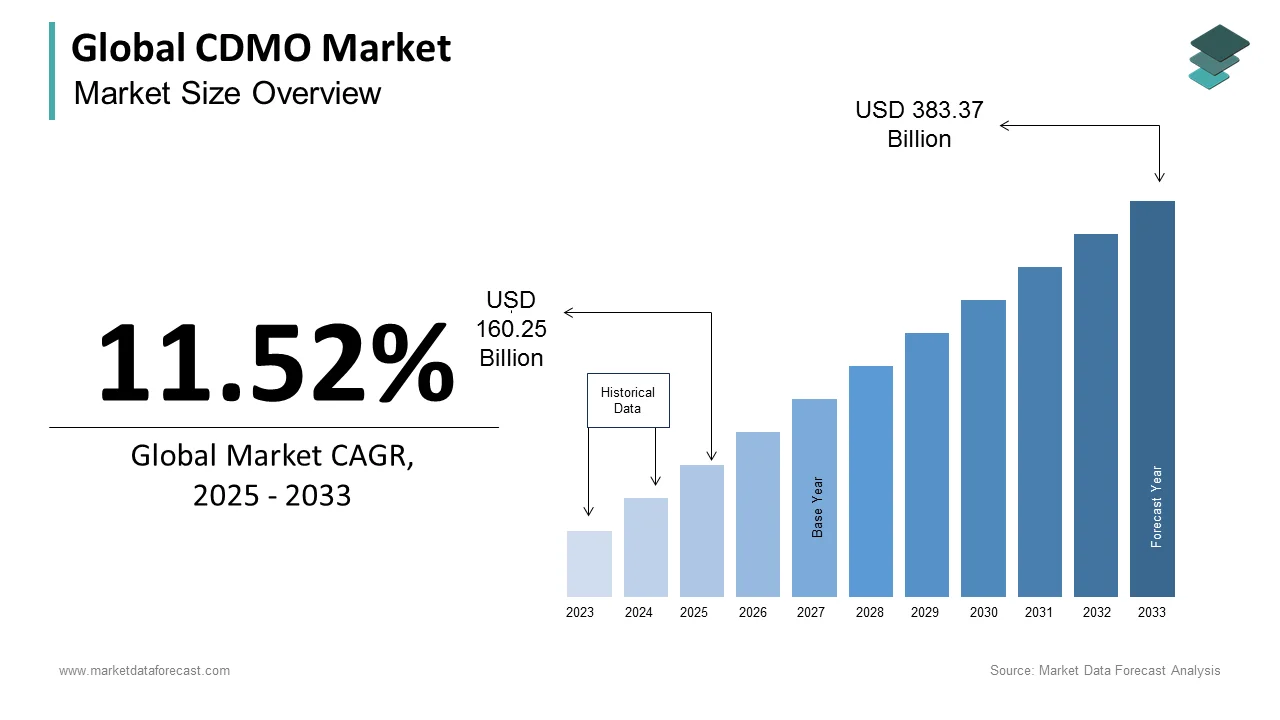

The size of the global CDMO market was worth USD 143.70 billion in 2024. The global market is anticipated to grow at a CAGR of 11.52% from 2025 to 2033 and be worth USD 383.37 billion by 2033 from USD 160.25 billion in 2025.

Contract Development and Manufacturing Organization (CDMO) are comprises specialized entities that provide integrated services in drug development, process optimization, and commercial-scale manufacturing for biopharmaceutical companies. These organizations support the transformation of therapeutic candidates, from small molecules to complex biologics and cell and gene therapies, into clinically viable and regulatory-compliant products. The sector has become indispensable due to the rising complexity of therapeutics, particularly in monoclonal antibodies and mRNA-based platforms. This integration underscores a structural shift in the industry toward outsourced expertise, driven by cost efficiency, technological specialization, and accelerated development timelines.

MARKET DRIVERS

Increasing R&D Outsourcing by Biopharmaceutical Firms to Optimize Innovation Pipelines

Pharmaceutical and biotech companies are increasingly delegating development and manufacturing functions to CDMOs to enhance operational agility and focus on core innovation. According to the Tufts Center for the Study of Drug Development, the average cost to bring a new drug to market exceeds $2.3 billion, prompting firms to outsource non-core activities to reduce capital expenditure. Mid-sized biotechs, lack in-house manufacturing infrastructure and rely heavily on CDMO partnerships for clinical trial material production. Additionally, the rise of niche therapies, such as antisense oligonucleotides and viral vectors, requires specialized expertise that only a subset of CDMOs possess. This dependency has elevated CDMOs from service providers to strategic partners, with long-term agreements becoming commonplace to ensure supply continuity and regulatory alignment.

Proliferation of Complex Therapeutic Modalities Requiring Specialized Manufacturing Expertise

The surge in advanced therapeutics, including antibody-drug conjugates (ADCs), mRNA vaccines, and cell and gene therapies, has amplified demand for CDMOs with niche technical capabilities. These modalities involve intricate processes such as aseptic fill-finish, viral vector production, and lipid nanoparticle formulation, which require GMP-compliant facilities and highly trained personnel. According to the Alliance for Regenerative Medicine, over 1,300 cell and gene therapy programs were in clinical development globally in 2023. Furthermore, the complexity of ADCs, combining cytotoxic agents with monoclonal antibodies, demands precise conjugation technologies available at fewer facilities worldwide. This scarcity of expertise positions specialized CDMOs as critical enablers of next-generation medicine commercialization.

MARKET RESTRAINTS

Geopolitical and Supply Chain Vulnerabilities in Global Manufacturing Networks

The CDMO industry’s reliance on geographically dispersed supply chains exposes it to disruptions from trade tensions, regulatory divergence, and logistical bottlenecks. Active pharmaceutical ingredient (API) production is heavily concentrated in China and India, which supply over 65% of global intermediates. Additionally, the European Medicines Agency has intensified inspections of Asian manufacturing sites, resulting in an increase in compliance-related delays. These vulnerabilities undermine delivery timelines and increase operational risk, particularly for time-sensitive oncology and rare disease programs. The lack of redundant manufacturing capacity in Western nations further exacerbates dependency, limiting the sector’s resilience to global shocks.

Escalating Regulatory Scrutiny and Compliance Burdens Across Jurisdictions

CDMOs face mounting regulatory complexity as global health authorities enforce stricter quality and traceability standards. The U.S. FDA issued warning letters to contract manufacturers between 2018 and 2023, with related to data integrity and process validation failures. In emerging markets, inconsistent regulatory frameworks create additional hurdles. These compliance challenges increase audit preparation costs and delay product approvals. Moreover, the shift toward real-time release testing and continuous manufacturing requires substantial capital investment, disproportionately affecting smaller CDMOs lacking the financial or technical infrastructure to adapt swiftly.

MARKET OPPORTUNITIES

Expansion of mRNA and Nucleic Acid-Based Therapeutics Manufacturing Infrastructure

The success of mRNA vaccines during the pandemic has catalyzed sustained investment in nucleic acid-based therapeutic platforms, creating a high-growth niche for CDMOs. Also, over 50 mRNA-based candidates are now in clinical trials for cancer, infectious diseases, and genetic disorders. The demand for lipid nanoparticle (LNP) formulation and cryogenic fill-finish capabilities has outpaced supply. Companies like Catalent and Lonza have invested majorly since 2021 to expand mRNA capacity. In 2023, Moderna partnered with Samsung Biologics to establish a dedicated mRNA production facility in South Korea, signaling a trend toward strategic CDMO alliances. This infrastructure development not only supports pandemic preparedness but also enables scalable production of personalized cancer vaccines and rare disease therapies, positioning forward-looking CDMOs at the forefront of a transformative therapeutic wave.

Adoption of Digital Twins and AI-Driven Process Optimization in Manufacturing

The integration of artificial intelligence and digital twin technology is revolutionizing CDMO operations by enhancing process predictability and reducing development timelines. Digital twins—virtual replicas of manufacturing processes, allow CDMOs to simulate bioreactor performance, optimize yield, and preempt deviations before physical runs. According to the Massachusetts Institute of Technology’s Center for Biomedical Innovation, AI-driven modeling can reduce process development time and improve batch consistency. Also, Thermo Fisher Scientific deployed machine learning algorithms across its biologics CDMO network. These advancements enable predictive maintenance, real-time quality control, and adaptive process control, transforming CDMOs into data-intelligent partners capable of delivering higher reliability and faster time-to-market for complex therapeutics.

MARKET CHALLENGES

Talent Shortage in Specialized Biomanufacturing and Process Sciences

The CDMO sector faces a critical shortage of skilled professionals in bioprocessing, regulatory affairs, and analytical development, constraining expansion and innovation. Europe faces a similar gap. Academic programs are not producing graduates at a sufficient pace, and on-the-job training remains time-intensive. This talent scarcity increases operational risk, slows project timelines, and limits the ability of CDMOs to scale rapidly in response to client demand, particularly in emerging therapeutic areas.

Capacity Constraints in High-Potent and Cell & Gene Therapy Manufacturing

Despite rising demand, the CDMO market faces acute capacity shortages in high-potency APIs and advanced therapy medicinal products (ATMPs). In cell and gene therapy, the vein-to-vein model necessitates decentralized or flexible manufacturing, mot of CDMO suites are designed for batch processing, limiting scalability. According to the Cell & Gene Therapy Catapult, global demand for viral vector manufacturing capacity exceeds supply, with lead times stretching beyond severalmonths. This bottleneck delays clinical trials and commercial launches, particularly for rare disease therapies with small patient pools but high development costs. Furthermore, the capital intensity of building BSL-2+ and closed-system facilities deters new entrants and slows industry-wide capacity expansion, creating a persistent imbalance between demand and operational readiness.

SEGMENTAL ANALYSIS

By Service Insights

The Contract Manufacturing Organization (CMO) services segment was the largest segment in the CDMO market and accounted for 65.3% of the global share in 2024. This dominance is primarily driven by the escalating demand for commercial-scale production of biologics and complex small molecules. In USA, a significant portion of new molecular entities approved in 2023 required specialized formulation or aseptic manufacturing, capabilities predominantly outsourced to CMOs. The rising cost of in-house facility development has prompted pharmaceutical firms to leverage external manufacturing capacity. Also, outsourcing manufacturing reduces capital risk compared to internal builds. Furthermore, the global expansion of biosimilar pipelines has intensified reliance on CMOs with regulatory-compliant facilities in multiple jurisdictions, reinforcing their central role in the supply chain.

The Contract Research Organization (CRO) services segment is the fastest-growing within the CDMO market projected to grow at a CAGR of 12.6% from 2025 to 2033. This acceleration is fueled by the increasing complexity of early-stage drug development and the need for integrated development-to-manufacturing pathways. Biotech firms, particularly those in the preclinical and Phase I stages, are prioritizing CRO-led process development, analytical testing, and formulation optimization to de-risk later manufacturing. A large share of emerging biotechs now engage CROs for cell line development and upstream process characterization before transitioning to manufacturing partners. The integration of AI-driven pharmacokinetic modeling and high-throughput screening has further enhanced CRO value, reducing development timelines. This seamless transition from research to production positions CROs as pivotal enablers of speed and efficiency in the modern drug development lifecycle.

REGIONAL ANALYSIS

North America CDMO Market Analysis

North America held the leading position in the global CDMO market by capturing 43.5% of total revenue in 2024. The United States, as the regional epicenter, hosts the highest concentration of integrated CDMOs with end-to-end capabilities, including Catalent, Lonza’s U.S. divisions, and Thermo Fisher Scientific. The country’s robust regulatory framework, supported by the FDA’s Emerging Technology Program, encourages innovation in continuous manufacturing and real-time release testing. Additionally, the presence of a dense biotech cluster in Massachusetts, California, and North Carolina drives consistent demand for clinical and commercial manufacturing. Federal funding through the Biomedical Advanced Research and Development Authority (BARDA) has also bolstered domestic capacity for pandemic-responsive therapeutics, reinforcing North America’s position in high-complexity, regulated manufacturing.

Europe CDMO Market Analysis

Europe maintains a significant market share, with Germany, Switzerland, and the United Kingdom serving as core hubs for high-quality biopharmaceutical manufacturing. Switzerland, home to major CDMO sites operated by Lonza and Siegfried, contributes disproportionately to the region’s output, producing a portion of all outsourced biologics in Europe. The EU’s centralized approval system through the European Medicines Agency facilitates multi-country market access, enhancing the attractiveness of European CDMOs for global clients. Germany’s strong engineering base supports advanced aseptic fill-finish and ADC manufacturing. Despite Brexit-related regulatory divergence, the UK retains a competitive edge through specialized facilities in Cambridge and Glasgow, particularly in viral vector and mRNA production, supported by public-private initiatives like the Medicines Manufacturing Innovation Centre.

Asia Pacific CDMO Market Analysis

The Asia Pacific region is also a key player in the global CDMO market, with China and South Korea emerging as strategic manufacturing gateways. China has rapidly expanded its CDMO infrastructure, with large number of contract manufacturers now offering services ranging from API synthesis to biologics fill-finish, as documented by the China Pharmaceutical Industry Association. The country’s 14th Five-Year Plan includes incentives for domestic biopharma outsourcing, accelerating facility development. South Korea, though smaller in scale, has gained recognition for high-yield monoclonal antibody production. Japan’s CDMO sector is highly regulated but technologically advanced, with Fujifilm Diosynth Biotechnologies operating one of the world’s largest single-site biologics plants. The region’s cost efficiency, combined with improving regulatory alignment with ICH guidelines, is driving increased outsourcing from Western biotechs seeking scalable, compliant capacity.

Latin America CDMO Market Analysis

Latin America holds a notable share of the global CDMO market, with Brazil and Mexico representing the most developed ecosystems. Brazil’s market is anchored by Eurofarma and Aché Laboratórios, which have expanded into contract services for generics and biosimilars. The country produced a substantial volume of doses of biologics for domestic and regional use. Mexico has attracted foreign investment through its proximity to the U.S. and participation in USMCA, enabling faster supply chain integration. CDMO capacity in Mexico is increasingly focused on oral solids and sterile injectables, with several facilities certified under FDA or EMA standards. However, limited expertise in biologics and gene therapy manufacturing restricts high-end service offerings. Despite these constraints, growing government support for local pharmaceutical production is fostering gradual modernization and regional collaboration.

Middle East and Africa CDMO Market Analysis

The Middle East and Africa collectively represent a small share of the global CDMO market, yet exhibit emerging strategic importance. Israel stands out as a regional leader, with a concentration of biotech startups and CDMOs specializing in niche formulations and peptide synthesis. The Weizmann Institute and Tel Aviv University have spun off several process development firms now engaged in international partnerships, as noted by the Israeli Biotech Federation. The UAE has made significant investments in pharmaceutical sovereignty, launching the Abu Dhabi-based Bioproduction Facility in 2023 to support mRNA and viral vector manufacturing for regional distribution. South Africa hosts the continent’s most advanced GMP facilities, with Biovac Institute producing vaccines under technology transfer agreements.

COMPETITIVE LANDSCAPE

Competition in the CDMO market is intensifying as global leaders and regional specialists vie for dominance across therapeutic complexity and geographic reach. The sector is characterized by a tiered structure: multinational CDMOs with integrated capabilities compete on scale, regulatory expertise, and technological sophistication, while niche players differentiate through specialization in high-potency drugs, cell and gene therapies, or rapid-response platforms. The rise of biologics and personalized medicine has elevated the importance of technical precision, leading to consolidation among mid-tier firms unable to invest in next-generation infrastructure. Client loyalty is increasingly tied to reliability, speed, and regulatory success rates rather than cost alone. Moreover, the shift toward regionalized manufacturing—driven by supply chain resilience and government incentives—is reshaping competitive dynamics, with countries like South Korea, Singapore, and Ireland emerging as strategic hubs. This evolving landscape demands continuous innovation, operational agility, and deep client integration to sustain long-term advantage.

KEY MARKET PLAYERS

The major players operating in the global CDMO market profiled in this report are

- Metrics

- AMRI (Albany Molecular Research Inc.)

- Famar

- WuXi AppTec

- Asymchem

- Porton

- Lonza

- Catalent

- Patheon

- Siegfried

- Recipharm

- Strides Shasun

- Piramal

TOP LEADING PLAYERS IN THE MARKET

- Lonza has established a significant footprint in the Asia Pacific CDMO landscape through strategic investments and localized innovation. The company operates a state-of-the-art biologics manufacturing facility in Visp, Singapore, which commenced commercial production in 2023 and supports both monoclonal antibodies and mRNA-based therapeutics. Lonza strengthened its regional presence by launching a digital process optimization hub in Shanghai, enabling real-time collaboration with Chinese biotechs on upstream development. Lonza also initiated a training alliance with the National University of Singapore to cultivate bioprocessing talent, addressing regional skill gaps. These initiatives underscore its commitment to integrating technological excellence with regional adaptability, positioning Lonza as a preferred partner for complex molecule development across the Asia Pacific.

- Catalent has deepened its engagement in the Asia Pacific market by expanding its formulation and fill-finish capabilities in Japan, Australia, and India. Catalent also acquired a peptide manufacturing site in Japan to enhance its sterile product offerings and strengthen access to the Japanese regulatory pathway. The company launched a patient-centric drug delivery program in collaboration with Australian biotechs, focusing on oral thin films and inhalation systems. Additionally, Catalent integrated AI-driven stability modeling into its Asia Pacific development centers, reducing formulation timelines by up to 30%. These advancements reflect a strategic pivot toward high-value, differentiated services that align with the region’s growing innovation in specialty pharmaceuticals and personalized medicine.

- Samsung Biologics has emerged as a dominant force in biologics manufacturing within the Asia Pacific, leveraging South Korea’s advanced infrastructure and government-backed biopharma initiatives. The company completed construction of its fourth biomanufacturing plant (Plant 4) in Incheon in 2023, increasing its total capacity. Samsung Biologics has secured long-term supply agreements with multiple U.S. and European biopharma firms, positioning South Korea as a global export hub for monoclonal antibodies. Its adoption of continuous manufacturing and digital twin technology has set new benchmarks in yield and consistency, attracting clients seeking speed, scale, and regulatory reliability in a geopolitically stable environment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the CDMO market are deploying vertical integration, technological differentiation, and geographic expansion to solidify their competitive standing. Companies are acquiring or building end-to-end capabilities that span process development, clinical manufacturing, and commercial-scale production to reduce client dependency on multiple vendors. Investment in advanced modalities, such as ADCs, mRNA, and viral vectors, ais accelerating, with firms establishing dedicated suites to capture high-margin segments. Digital transformation is a critical enabler, with AI-driven process modeling, real-time analytics, and blockchain-based supply chain tracking enhancing efficiency and compliance. Strategic partnerships with biotechs and academic institutions are being leveraged to co-develop novel platforms and secure early-stage pipeline access. Additionally, CDMOs are expanding into emerging markets through joint ventures and regulatory harmonization initiatives to diversify supply chains and meet regionalization demands driven by geopolitical and pandemic resilience considerations.

GLOBAL CDMO MARKET NEWS

- In January 2023, Lonza launched a digital process optimization center in Shanghai, enabling real-time data exchange with biotech clients across China and enhancing development efficiency to strengthen its market presence.

- In August 2023, Catalent commissioned a new aseptic fill-finish line at its Hyderabad facility, expanding capacity for biosimilars and oncology drugs to meet rising demand in the Asia Pacific region.

- In December 2022, Samsung Biologics completed Plant 4 in Incheon, adding 200,000 liters of biologics manufacturing capacity and reinforcing its position as a global-scale production leader.

- In May 2024, Catalent acquired a peptide manufacturing site in Japan, broadening its sterile product portfolio and strengthening regulatory access in one of Asia’s most advanced pharmaceutical markets.

- In March 2023, Lonza initiated a bioprocessing talent development program with the National University of Singapore, addressing workforce shortages and deepening its regional integration in the Asia Pacific CDMO market.

REPORT COVERAGE

| Metric | Value |

|---|---|

| Base Year | 2024 |

| Market Size Available | 2024 to 2033 |

| Forecast Period | 2025 to 2033 |

| Quantitative Units | Market Size in USD Billion and CAGR from 2025 to 2033 |

| Various Analyses Included | Global, Regional & Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE; Porter's Five Forces; Competitive Landscape; Investment Opportunities |

| Segments Covered | Service and Region |

| Key Market Players | Metrics, AMRI, Famar, WuXi AppTech, Asymchem, Porton, Lonza, Catalent, Patheon, Siegfried, Recipharm, Strides Shasun, and Piramal |

| Regions Analyzed | North America, Europe, APAC, Latin America, Middle East & Africa |

| Countries Covered | U.S, Canada, Mexico, UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Brazil, Argentina, Chile, KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Other Countries |

| Report Format | PDF, Excel, PPT, BI |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

MARKET SEGMENTATION

This research report on the global CDMO market has been segmented and sub-segmented based on the service and region.

By Service

- CMO

- Finished Product Manufacturing

- Injectables

- Solid Dosage Forms

- Others (Semisolids/Liquid, Powder)

- API Manufacturing

- Packaging

- Finished Product Manufacturing

- CRO

- Preclinic

- Clinic

- Laboratory Services

- Discovery

By Region

- North America

- Europe

- Asia-pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the CDMO Market?

The CDMO Market involves organizations providing comprehensive drug development and manufacturing services to pharmaceutical and biotechnology companies, spanning research to commercial production

2. Which regions dominate the CDMO Market?

North America is the largest market with around 39% share in 2024, followed by Europe; Asia Pacific is rapidly growing due to increasing pharma R&D and manufacturing outsourcing

3. What services do CDMOs provide?

Services include drug formulation, clinical trial manufacturing, analytical testing, commercial product manufacturing, packaging, and regulatory support

4. Who are the key players in the CDMO Market?

Leading companies include Lonza Group, Catalent, Samsung Biologics, WuXi Biologics, Charles River Labs, and Thermo Fisher Scientific

5. How is AI impacting the CDMO Market?

AI streamlines drug development, optimizes processes, reduces cycle time, and enhances data analysis for manufacturing scale-up

6. What sectors within pharma drive CDMO growth?

Demand for biologics, personalized medicine, oncology therapies, and gene and cell therapies drives CDMO outsourcing

7. How did COVID-19 affect the CDMO Market?

The pandemic accelerated vaccine manufacturing outsourcing and highlighted the need for flexible, scalable contract manufacturing

8. What technological innovations are influencing CDMOs?

Continuous manufacturing, advanced analytics, green chemistry, digital twins, and automated process control are leading innovations

9. What challenges does the CDMO Market face?

Challenges include regulatory complexity, capacity constraints, technology investments, supply chain risks, and rising competition

10. How is the CDMO Market segmented by product type?

Segments include small molecules, biologics, advanced therapies, vaccines, and consumer health products

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com