- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

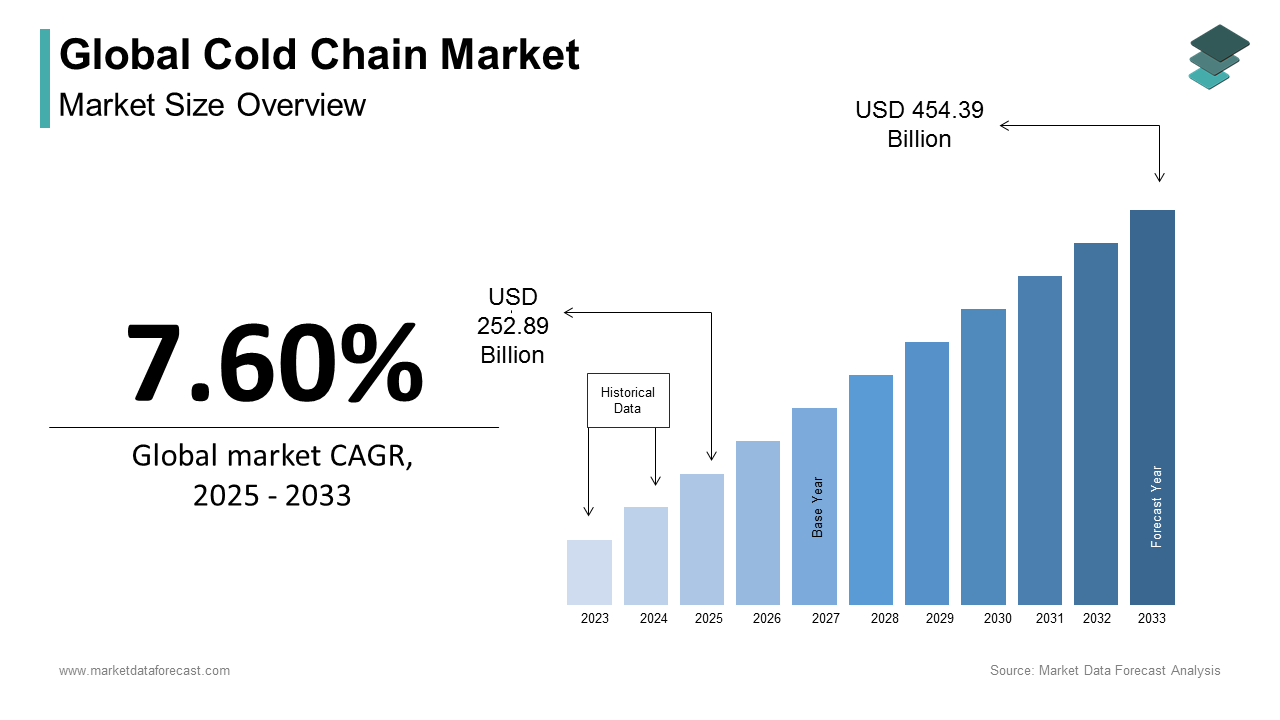

Market Size, 2025

$252.89 BnMarket Estimate, 2026

$272.11 BnMarket Forecast, 2034

$488.93 BnCAGR, 2026–2034

7.6%Global Cold Chain Market Summary

The global cold chain market was valued at USD 252.89 billion in 2025 and is projected to reach USD 272.11 billion in 2026 and further expand to USD 488.93 billion by 2034, growing at a CAGR of 7.6% from 2026 to 2034. The growth of the global cold chain market is driven by rising demand for perishable food products, increasing pharmaceutical and vaccine distribution requirements, and growing international trade of temperature-sensitive goods. Advancements in refrigeration technologies and strong investments in logistics infrastructure are also accelerating market expansion.

Key Market Trends

- Growing adoption of automated storage and retrieval systems (ASRS) to enhance efficiency.

- Rising demand for pharmaceutical cold chain logistics, especially for biologics and vaccines.

- Expansion of e-commerce and online grocery platforms is fueling cold chain delivery services.

- Increased emphasis on energy-efficient and sustainable refrigeration solutions.

- Strategic investments in emerging markets to strengthen supply chain networks.

Segmental Insights

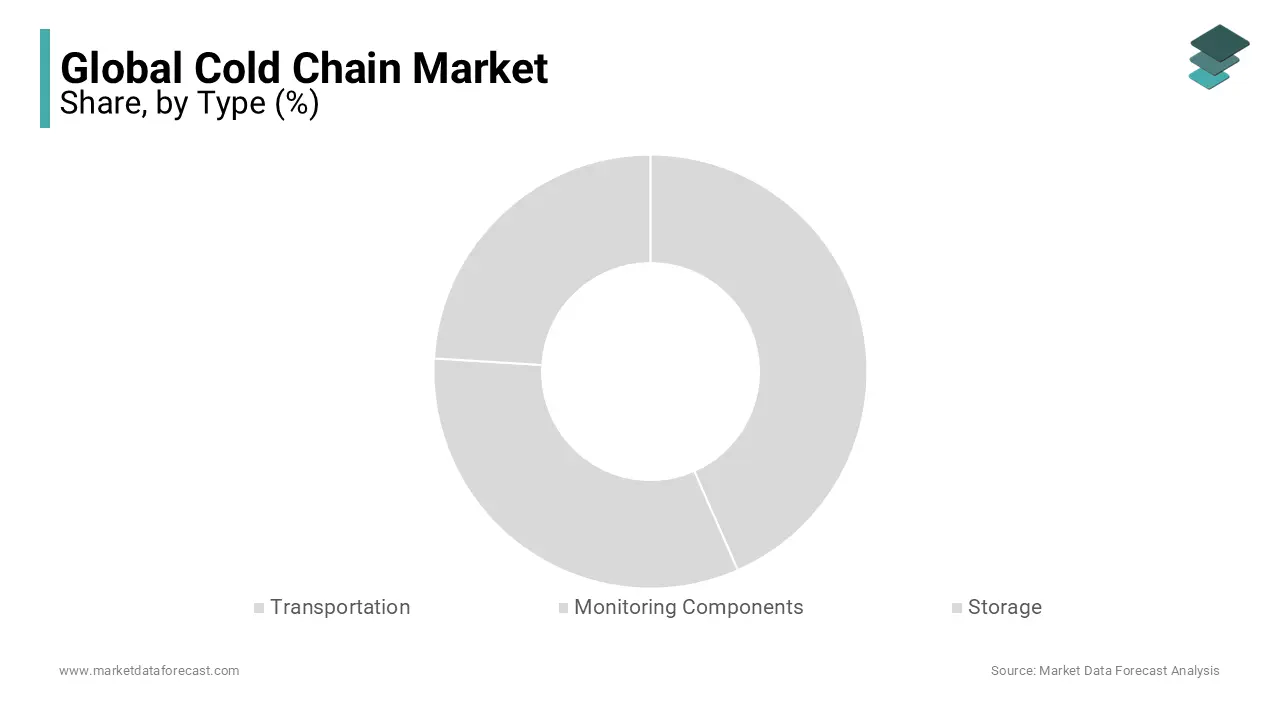

- Based on type, the storage segment dominated the global cold chain market in 2025 with a 48.3% share, supported by growing demand for refrigerated warehouses.

- Based on temperature type, the chilled segment held the largest share at 57.6% in 2025, reflecting its role in preserving dairy, fruits, and beverages.

- Based on application, the dairy and frozen desserts segment led the market in 2025, capturing 32.1% of the share, driven by increasing consumption of frozen foods and ready-to-eat products.

Regional Insights

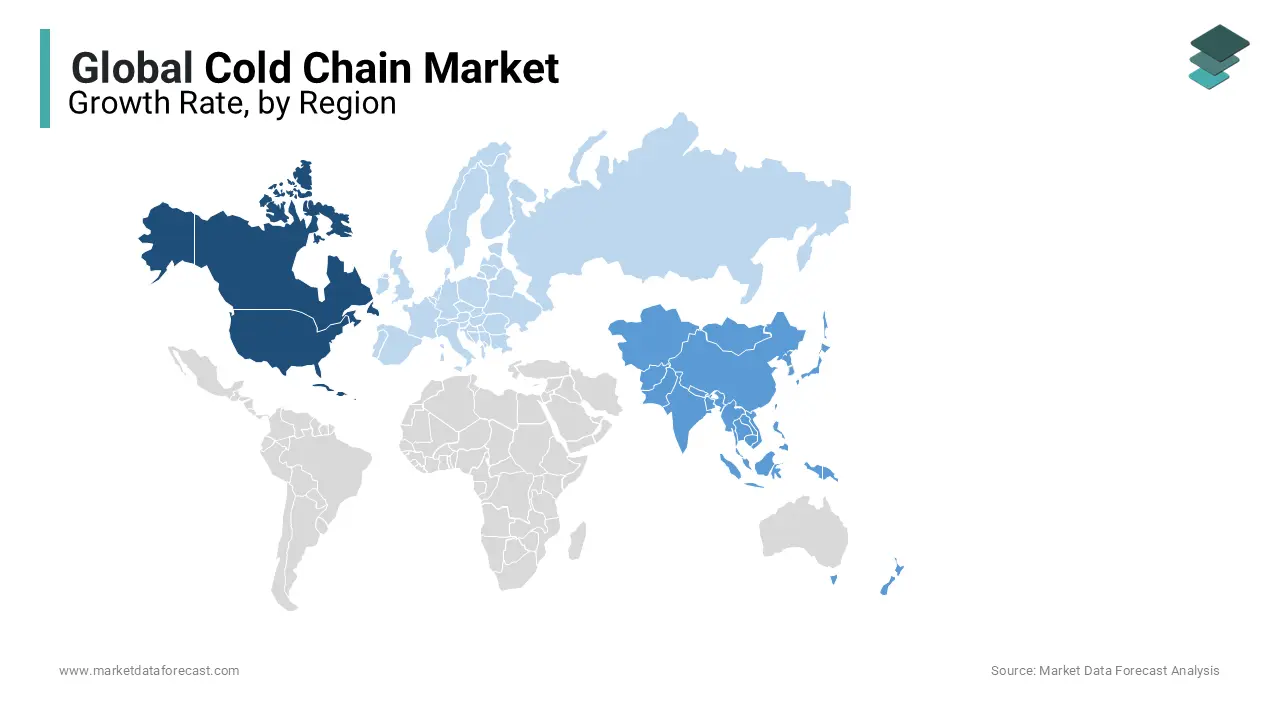

- North America dominated the global cold chain market with a 31.3% share in 2025, backed by advanced logistics infrastructure, strong foodservice demand, and pharmaceutical storage needs.

- Europe showed significant adoption, driven by stringent food safety regulations and sustainability initiatives.

- Asia-Pacific is anticipated to witness the fastest growth, led by rising urbanization, booming e-commerce, and higher demand for perishable goods.

- Latin America is expanding steadily with increasing exports of seafood, fruits, and meat.

- Middle East & Africa are emerging markets, supported by investments in food imports and healthcare cold chain logistics.

Competitive Landscape

Leading players in the global cold chain market include Lineage Logistics, AGRO Merchant, Priority Freezer, ITC Ltd, Henningsen, Americold Logistics, Burris Logistics, Nichirei Logistics, Kloosterboer, VersaCold Logistics, Weekly Warehouse, and Swire Refrigeration. Companies are focusing on network expansion, energy-efficient technologies, and strategic partnerships to strengthen their market presence worldwide.

Global Cold Chain Market Size

The global cold chain market size was assessed to be USD 252.89 billion in 2025. The global market is further expected to reach USD 488.93 billion by 2034 from USD 272.11 billion in 2026, growing at a compound annual growth rate (CAGR) of 7.60% during the forecast timeline.

The Cold Chain system relies on refrigerated production, storage, and transportation maintained within specific thermal ranges typically between -25°C and +25°C, which is depending on the product category. According to the Food and Agriculture Organization of the United Nations, approximately 14% of the world’s food is lost between post-harvest and retail due to inadequate temperature management, with the Asia-Pacific region accounting for a significant share of these losses.

MARKET DRIVERS

Growing Demand for Temperature-Sensitive Pharmaceuticals

The proliferation of biopharmaceuticals and advanced therapeutics has fundamentally altered the structural demands on the cold chain ecosystem, which is fuelling the growth of the Cold Chain Market. The need for specialized cold chain infrastructure capable of maintaining thermal integrity across long distances is prompting the growth of the market. Pfizer-BioNTech’s vaccine, requiring storage at -70°C, necessitated over 200,000 specialized thermal shippers globally during initial distribution phases, according to the World Health Organization. Additionally, the World Bank indicates that 3 billion people lack consistent access to essential medicines, many of which are temperature-sensitive, thereby increasing pressure on governments and logistics providers to invest in resilient cold chain networks. In emerging markets like Indonesia and Nigeria, where immunization coverage gaps persist due to cold chain deficiencies, the expansion of temperature-controlled logistics is now a public health priority.

Rising Consumption of Perishable and Frozen Foods

The transformation in dietary patterns across urban populations is driving the growth of the Cold Chain Market. As per the United Nations Economic and Social Commission for Asia and the Pacific, the region’s frozen food market volume grew by 8.3% annually between 2018 and 2022, fueled by rising disposable incomes, dual-income households, and the proliferation of organized retail and e-grocery platforms. This shift reflects a broader trend where convenience, food safety, and extended shelf life are prioritized over traditional fresh-market procurement. The U.S. Department of Agriculture notes that nearly 85% of dairy products and 90% of seafood in developed economies move through temperature-controlled supply chains, illustrating the indispensability of cold logistics in modern food systems. Furthermore, the global ready-to-eat meals market, which heavily relies on frozen distribution, is expected to surpass USD 200 billion by 2027, according to the Food and Agriculture Organization.

MARKET RESTRAINTS

High Energy Consumption and Operational Costs

The exorbitant energy demand associated with temperature-controlled logistics is restricting the growth of the cold chain market. Refrigerated warehouses and transport units consume significantly more power than their ambient counterparts; refrigerated trucks use up to 30% more fuel than dry freight vehicles, as documented by the International Energy Agency. In the European Union, cold storage facilities account for approximately 15% of total industrial electricity consumption, according to Eurostat. This energy intensity translates into high operational expenditures, with cooling systems representing nearly 40% of total logistics costs in temperature-sensitive supply chains, as noted by the World Bank’s Sustainable Energy for All initiative.

Fragmented Infrastructure in Emerging Economies

A cold chain scalability lies in the fragmented and underdeveloped infrastructure across many developing regions. In countries like Vietnam, Pakistan, and Kenya, cold chain networks remain highly decentralized, with limited integration between storage, transportation, and last-mile delivery. In India, despite the presence of over 8,000 cold storage facilities, most are designed solely for potatoes and lack multi-commodity capabilities or reefer truck connectivity, as stated by the Indian Council of Agricultural Research. This siloed structure inhibits end-to-end temperature control, particularly for high-value exports such as berries, seafood, and cut flowers. Rural areas are especially affected over 60% of farmers in Sub-Saharan Africa lack access to refrigerated transport, according to the Food and Agriculture Organization, forcing reliance on informal, unregulated channels. Additionally, the absence of standardized monitoring protocols and real-time tracking systems exacerbates inefficiencies.

MARKET OPPORTUNITIES

Integration of IoT and Real-Time Monitoring Technologies

The advent of Internet of Things (IoT) technology is creating new opportunities for the growth of cold chain market. Companies like Maersk and DHL have integrated smart containers equipped with IoT sensors across 70% of their temperature-sensitive shipments, reducing spoilage incidents by up to 45%, as reported by the International Air Transport Association. The U.S. Department of Commerce notes that IoT-enabled cold chain solutions can improve energy efficiency by 20–30% by optimizing cooling cycles based on real-time data. Furthermore, regulatory bodies are increasingly mandating digital monitoring India’s Food Safety and Standards Authority now requires temperature logging for all interstate shipments of dairy and meat products.

Expansion of E-Grocery and Direct-to-Consumer Models

The rapid ascent of online grocery platforms and direct-to-consumer (D2C) food delivery services has created a structural shift in cold chain demand dynamics. Consumers in urban centers increasingly expect same-day or next-day delivery of fresh and frozen foods, necessitating agile, last-mile temperature-controlled logistics. In Singapore, over 40% of households now purchase perishables online at least once a month, according to the Monetary Authority of Singapore. This trend compels retailers and logistics providers to invest in urban cold hubs, refrigerated micro-fulfillment centers, and electric refrigerated vans. For instance, Alibaba’s Hema Fresh operates over 300 smart supermarkets in China, each backed by a cold storage and distribution network capable of delivering fresh seafood and meat within 30 minutes. The World Economic Forum estimates that last-mile cold logistics will grow by 12.5% annually through 2027, driven by urbanization and changing consumption habits. In India, BigBasket and JioMart have deployed over 15,000 refrigerated delivery vehicles to serve metropolitan markets.

MARKET CHALLENGES

Vulnerability to Climate Change and Environmental Regulations

Cold chain operations are increasingly exposed to the physical and regulatory impacts of climate change, posing a significant strategic challenge. Rising ambient temperatures, particularly in tropical regions, escalate the energy required to maintain refrigerated environments. According to the Intergovernmental Panel on Climate Change, the average global temperature has risen by 1.1°C since pre-industrial times, with South Asia experiencing a 0.7°C increase per decade since 1980, complicating cold storage efficiency. In regions like the Persian Gulf, where summer temperatures exceed 50°C, refrigerated trucks face thermal stress, leading to compressor failures and product spoilage. The International Institute of Refrigeration warns that for every 1°C rise in ambient temperature, refrigeration systems consume an additional 2–3% energy. Simultaneously, stringent environmental regulations are phasing out high-global-warming-potential (GWP) refrigerants. The Kigali Amendment to the Montreal Protocol mandates a 80% reduction in hydrofluorocarbon (HFC) use by 2047, affecting over 70% of commercial refrigeration systems globally, as per the United Nations Environment Programme.

Workforce Skill Gaps in Cold Chain Management

The shortage of skilled professionals capable of managing complex, technology-driven logistics systems is limiting the growth of the cold chain market. The operation of modern cold chains requires expertise in refrigeration engineering, data analytics, regulatory compliance, and supply chain optimization skills that are in short supply in emerging markets. According to the International Labour Organization, over 60% of logistics technicians in Southeast Asia lack formal training in temperature-controlled logistics, which is leading to improper handling, equipment misuse, and temperature deviations. According to the European Cold Chain Association, improper loading practices such as blocking air vents in refrigerated trailers account for nearly 25% of temperature excursions due to inadequate training.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.60% |

| Segments Covered | By Type, Type Temperature, Application, and Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Lineage Logistics, AGRO Merchant, Priority Freezer, ITC Ltd, Henningsen, Americold Logistics, Burris Logistics, Nichirei Logistics, Kloosterboer, VersaCold Logistics, Weekly Warehouse, and Swire Refrigeration |

SEGMENTAL ANALYSIS

By Type Insights

The storage segment dominated the global cold chain market by capturing 48.3% of the share in 2025 with the foundational role of temperature-controlled warehousing in preserving product integrity across extended supply chains. Cold storage facilities serve as nodes for consolidation, buffering, and distribution for perishable food and pharmaceuticals. As per the Food and Agriculture Organization, over 1.3 billion tonnes of food require temperature-controlled storage annually, with fruits, vegetables, and dairy constituting the largest volumes. In India, the Ministry of Food Processing Industries reports that the country’s cold storage capacity has expanded to 41 million metric tonnes, yet only 30% of it is equipped for dynamic temperature modulation with the need for modernization. Another pivotal factor is the expansion of centralized distribution hubs in e-commerce and pharmaceutical logistics. Amazon’s fulfillment network in the U.S. includes over 200 temperature-controlled warehouses, as disclosed in its 2023 logistics sustainability report.

The monitoring components segment is projected to grow with a prominent CAGR of 14.6% during the forecast period with the growing imperative for real-time visibility and compliance in temperature-sensitive logistics. These systems enable continuous data logging of temperature, humidity, and shock exposure, ensuring adherence to standards such as the FDA’s Drug Supply Chain Security Act. For instance, UNICEF’s drone delivery program in Malawi uses blockchain-integrated sensors to verify vaccine conditions throughout transit. Another catalyst is regulatory tightening; the European Medicines Agency now mandates electronic monitoring for all investigational medicinal products in clinical trials. Additionally, the U.S. Department of Agriculture reports that 92% of high-value seafood exporters utilize GPS-enabled temperature loggers to meet import requirements in Japan and the EU.

By Temperature Type Insights

The chilled temperature segment was the largest and held 57.6% of the cold chain market share in 2025 owing to the vast volume of pharmaceuticals and fresh perishables requiring stable, above-freezing conditions. Vaccines, insulin, and biologic drugs constitute a major portion of chilled logistics, with the global biopharmaceutical market surpassing USD 380 billion in 2023, according to the International Federation of Pharmaceutical Manufacturers & Associations. In China, the Ministry of Commerce reports that chilled meat sales grew by 18% year-on-year in 2023, reflecting shifting consumer preferences toward fresher, minimally processed options. Furthermore, the expansion of chilled ready meals in urban markets has intensified demand—Japan’s convenience store sector alone sells over 3 billion chilled bento boxes annually, as noted by the Japan Frozen Food Association.

The frozen temperature segment is lucratively to grow with an expected CAGR of 12.8% from 2026 to 2034 due to the rapid expansion of the frozen food industry and the emergence of ultra-low temperature (ULT) logistics for advanced therapeutics. In South Korea, frozen meal consumption rose by 21% between 2021 and 2023, driven by single-person households and time-constrained urban professionals, according to Statistics Korea. Another major factor is the rise of mRNA and cell-based therapies, which require storage at -70°C or lower. The World Health Organization reports that over 1.5 billion doses of ultra-cold chain vaccines were distributed globally in 2023, necessitating specialized freezers and dry vapor shippers. Pfizer’s distribution network alone deployed more than 500,000 ULT freezers worldwide during the pandemic, as confirmed in its 2023 supply chain transparency report.

By Application Insights

The dairy and frozen desserts segment held 32.1% of the cold chain market share in 2025 with the intrinsic perishability of milk, cheese, yogurt, and ice cream, all of which require uninterrupted refrigeration from production to consumption. Global milk production reached 926 million tonnes in 2023, with over 70% of it passing through temperature-controlled logistics, according to the Food and Agriculture Organization. Another factor is the expansion of frozen dessert consumption in emerging markets.

The fruits and vegetables segment is expected to grow with an expected CAGR of 13.4% from 2026 to 2034 owing to the increasing global trade in fresh produce and rising awareness of post-harvest losses due to inadequate cold storage. Kenya’s horticulture sector, a major exporter of green beans and avocados to Europe, relies on over 120 refrigerated cargo flights weekly, according to the Kenya Airports Authority. Another key driver is urban consumer demand for out-of-season and exotic produce; China imported USD 12.7 billion worth of fresh fruits in 2023, a 19% increase from the previous year, as reported by the General Administration of Customs. The U.S. Department of Agriculture notes that 80% of imported fresh produce enters via temperature-controlled ports. Additionally, the rise of farm-to-table and organic movements has intensified the need for traceable, refrigerated logistics.

REGIONAL ANALYSIS

North America Cold Chain Market Analysis

North America was the top performer of the cold chain market by capturing 31.3% of share in 2025 with its highly integrated logistics infrastructure, stringent regulatory environment, and high consumer demand for perishable goods. The Food and Drug Administration’s Food Safety Modernization Act mandates comprehensive cold chain controls for high-risk foods, driving compliance investments. Walmart’s cold chain fleet grew by 22% in 2023 to support its same-day grocery delivery expansion, as disclosed in its corporate logistics update. The region also leads in pharmaceutical cold chain logistics, handling over 40% of global clinical trial shipments, according to the Biotechnology Innovation Organization. According to the Environmental Protection Agency, 60% of new cold warehouses in California now incorporate LED lighting and variable-speed refrigeration compressors to reduce energy use.

Europe Cold Chain Market Analysis

Europe was positioned second by holding 28.2% of the cold chain market share in 2025. The region’s strength lies in its harmonized regulatory framework, dense transportation network, and high standards for food and drug safety. The European Union’s Cold Chain Directive mandates continuous temperature monitoring for all perishable goods in transit, ensuring traceability from farm to fork. According to the European Environment Agency, over 90% of fresh meat and 85% of dairy products in the EU are transported under refrigerated conditions. The pharmaceutical sector is another key contributor; Switzerland, home to major biotech firms, exports over CHF 90 billion worth of temperature-sensitive medicines annually, according to Swissmedic.

Asia Pacific Cold Chain Market Analysis

The growth of the Asia Pacific is primarily driven by its vast population, rapid urbanization, and escalating demand for food safety and healthcare access. China operates over 10,000 cold storage facilities, with a total capacity exceeding 150 million cubic meters, according to the China Logistics Information Center. India’s cold chain infrastructure, though underdeveloped, is expanding rapidly; the Ministry of Road Transport reports a 35% increase in reefer truck registrations between 2021 and 2023. Japan maintains one of the most advanced cold chain networks, with 98% of fresh food deliveries monitored via IoT sensors, as stated by the Japan Refrigeration and Air Conditioning Industry Association. The rise of e-grocery platforms like Meituan and BigBasket is transforming last-mile logistics, necessitating urban cold lockers and refrigerated two-wheelers. The World Bank estimates that improving cold chain coverage in Southeast Asia could reduce food losses by USD 15 billion annually. Additionally, the region is a major exporter of seafood and fruits; Thailand’s Department of International Trade reports that 70% of its mango exports require chilled logistics.

Latin America Cold Chain Market Analysis

Latin America is having steady growth as a major exporter of perishable agricultural goods, including berries, coffee, and beef, necessitating reliable cold logistics. However, infrastructure gaps persist; the Economic Commission for Latin America and the Caribbean notes that only 40% of refrigerated trucks are equipped with real-time monitoring systems. Argentina’s dairy sector, producing 11 billion liters of milk annually, faces spoilage rates of up to 15% due to inadequate cold storage, according to the National Institute of Agricultural Technology. Urbanization is a key growth driver; Mexico City’s e-grocery market expanded by 33% in 2023, as stated by the Mexican Association of Online Commerce.

Middle East and Africa Cold Chain Market Analysis

The Middle East and African market growth is likely to be driven with the rising investments in cold chain infrastructure to reduce food import dependency. Saudi Arabia’s Vision 2030 includes a USD 3.5 billion investment in agri-logistics, according to the Ministry of Environment, Water and Agriculture. The UAE operates the largest cold storage hub in the region, with Jebel Ali Free Zone housing over 1.2 million square meters of temperature-controlled space, as stated by Dubai Customs. Nigeria’s National Bureau of Statistics reports that only 15% of dairy farms have cold storage, leading to high spoilage. Zipline’s drone delivery network in Rwanda transports blood and vaccines under cold conditions to remote clinics, completing over 500,000 deliveries by 2023, as confirmed by the Rwandan Ministry of Health.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a dominating role in the global cold chain market include Lineage Logistics, AGRO Merchant, Priority Freezer, ITC Ltd, Henningsen, Americold Logistics, Burris Logistics, Nichirei Logistics, Kloosterboer, VersaCold Logistics, Weekly Warehouse, and Swire Refrigeration. Henningsen Cold Storage is an international cold chain company that provides the necessary services, such as warehouses, sole suppliers, transportation facilities, and transportation providers.

The competitive landscape of the cold chain market is characterized by a dynamic interplay of logistics giants, specialized freight operators, and technology innovators, all striving to capture growing demand for temperature-sensitive supply chains. As industries such as pharmaceuticals, e-grocery, and biotechnology place greater emphasis on product integrity, companies are differentiating themselves through technological sophistication, regulatory expertise, and global reach. The market is witnessing a shift from basic refrigerated transport to integrated, data-driven cold chain ecosystems that emphasize traceability, resilience, and sustainability. Incumbents are under pressure to modernize legacy systems while new entrants leverage digital platforms to offer agile, on-demand solutions. Competition is further intensified by the need for compliance with evolving international standards, particularly in healthcare logistics. Regional players are expanding cross-border capabilities to challenge global leaders, while strategic acquisitions and partnerships are reshaping market hierarchies. The emphasis on reducing carbon footprint is also influencing competitive strategy, with firms adopting green refrigerants and energy-efficient technologies. Ultimately, success in this space hinges on the ability to deliver seamless, secure, and intelligent cold chain solutions across complex, fragmented, and rapidly evolving supply networks.

TOP PLAYERS IN THE MARKET

United Parcel Service (UPS)

UPS has established itself as a dominant force in the global cold chain market by integrating advanced temperature-controlled logistics with a vast international network. The company’s dedicated healthcare logistics division, UPS Healthcare, specializes in handling sensitive pharmaceuticals, vaccines, and clinical trial materials requiring stringent thermal management. UPS operates specialized cold chain hubs equipped with real-time monitoring, refrigerated storage, and contingency protocols to ensure product integrity. Its investment in cold chain innovation includes temperature-sensitive packaging solutions and strategic partnerships with biotech firms.

DSV Panalpina

DSV, following its acquisition of Panalpina, has emerged as a leading global logistics provider with a robust cold chain offering tailored to pharmaceuticals, food, and high-value perishables. The company integrates air, sea, and road freight under a unified cold chain framework, ensuring seamless temperature control across multimodal transport. DSV’s expertise lies in its dedicated pharma logistics units, which operate certified facilities compliant with GDP and GDP Annex 1 standards. The company emphasizes end-to-end visibility, utilizing digital platforms for real-time monitoring and risk mitigation. Its global footprint enables customized cold chain solutions for clients in biotechnology, retail, and healthcare. DSV’s operational agility and focus on quality assurance have made it a preferred partner for time- and temperature-sensitive cargo.

C.H. Robinson

C.H. Robinson leverages its vast global network and non-asset-based logistics model to deliver comprehensive cold chain solutions across food, retail, and pharmaceutical sectors. The company excels in orchestrating temperature-controlled shipments through a broad carrier network, enabling flexibility and responsiveness in dynamic supply chains. Its proprietary technology platform, Navisphere, provides clients with real-time shipment visibility, predictive analytics, and compliance tracking, enhancing control over cold chain integrity. C.H. Robinson places strong emphasis on supplier vetting, risk management, and regulatory adherence, particularly for cross-border pharmaceutical and perishable food transport. Its consultative approach allows clients to tailor cold chain strategies to specific operational needs. Through continuous innovation in digital logistics and strategic partnerships with cold storage providers, C.H. Robinson maintains a pivotal role in shaping efficient, resilient, and scalable temperature-controlled supply chains worldwide.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

One of the primary strategies employed by leading players in the cold chain market is the integration of digital monitoring and IoT-enabled tracking systems across logistics networks. Companies are embedding smart sensors and cloud-based platforms into shipments to provide real-time visibility of temperature, humidity, and location, ensuring compliance and minimizing spoilage risks. This digital transformation enhances transparency, enables predictive interventions, and strengthens client trust in supply chain integrity.

Another key approach is the expansion of specialized infrastructure, including temperature-controlled warehouses, cold distribution hubs, and refrigerated transport fleets. Firms are investing in multi-zone storage facilities and energy-efficient refrigeration technologies to accommodate diverse product requirements, from frozen seafood to ultra-cold vaccines. These assets improve operational reliability and allow for scalability in high-demand regions.

Strategic partnerships and collaborations also play a crucial role in strengthening market presence. Companies are forming alliances with pharmaceutical manufacturers, food retailers, and technology providers to co-develop tailored cold chain solutions. These collaborations facilitate regulatory alignment, accelerate innovation, and extend service reach into emerging markets by enhancing competitiveness and service differentiation

RECENT HAPPENINGS IN THE MARKET

- In March 2025, UPS announced the expansion of its cold chain facility in Louisville, Kentucky, enhancing its temperature-controlled storage and distribution capabilities for pharmaceutical clients. This development strengthens UPS’s healthcare logistics network in North America and supports the growing demand for clinical trial and vaccine shipments.

- In January 2025, DSV launched a dedicated cold chain corridor between Singapore and Rotterdam, integrating air and sea freight under continuous temperature monitoring. This initiative improves transit reliability for high-value perishables and biopharmaceuticals moving between Asia and Europe.

- In February 2025, C.H. Robinson introduced an upgraded version of its Navisphere platform with advanced cold chain analytics, enabling clients to monitor thermal performance and optimize routing in real time. This enhancement reinforces its digital in temperature-sensitive logistics.

- In May 2025, Kerry Logistics partnered with a Singapore-based biotech firm to establish a GDP-compliant cold storage hub for cell and gene therapy products. The collaboration supports the region’s growing life sciences sector with specialized handling and distribution.

- In April 2025, Lineage Logistics opened a fully automated, energy-efficient cold storage facility in Sydney, incorporating AI-driven inventory management and solar-powered refrigeration. This facility marks a strategic entry into the Asia-Pacific market with sustainable cold chain infrastructure.

MARKET SEGMENTATION

This research report on the global cold chain market has been segmented and sub-segmented based on type, type temperature, application, and region.

By Type

- Transportation

- Monitoring Components

- Storage

By Type Temperature

- Chilled

- Frozen

By Application

- Fruits and vegetables

- Fruit pulp and concentrates

- Dairy Products

- Meat and seafood

- Processed foods

- Bakery and confectionery

- Pharmaceuticals

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa