Global Cold Storage Market Size, Share, Trends & Growth Forecast Report By Construction Type (Bulk Storage, Production Stores and Ports), Temperature (Chilled and Frozen), Application (Processed Foods, Dairy Products, Fruits and Vegetables, Meat and Seafood, and Pharmaceuticals), Warehouse Type (Public, Private and Semi-Private), And Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis (2026 to 2034)

Global Cold Storage Market Size

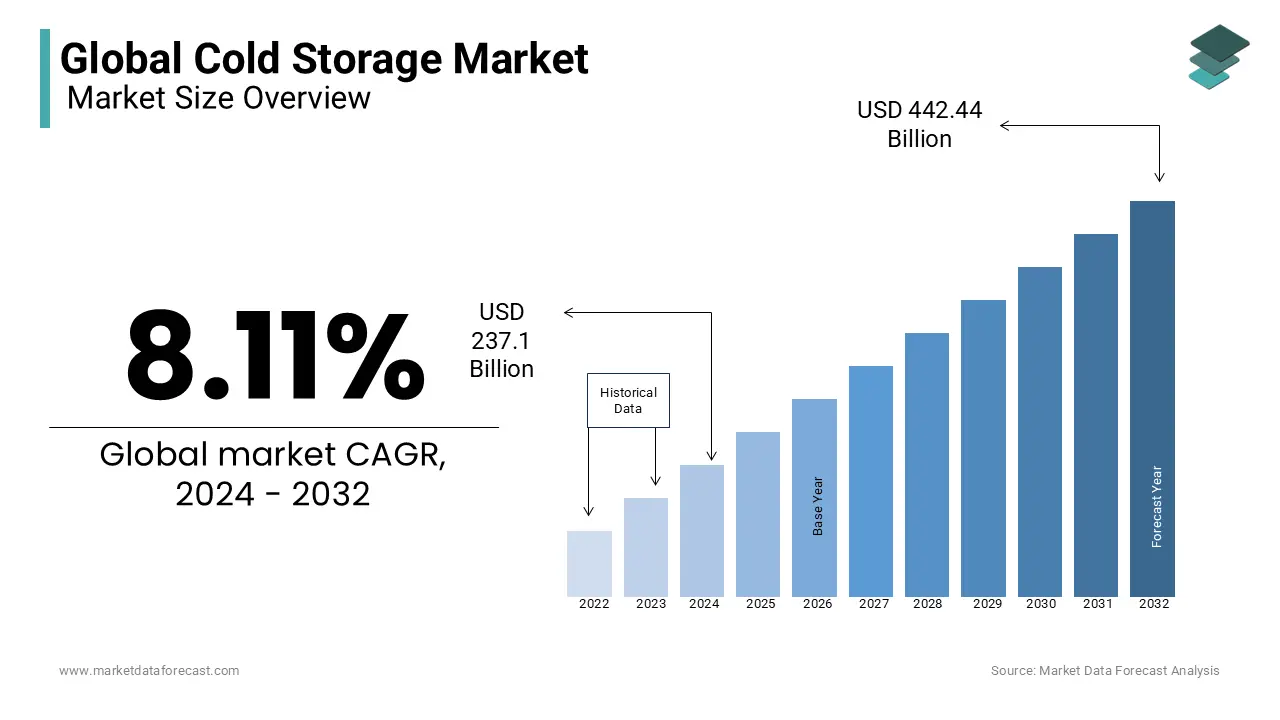

The size of the global cold storage market was valued at USD 256.43 billion in 2025 and is predicted to grow at a CAGR of 8.11% from 2026 to 2034 and be worth USD 517.33 billion by 2034 from USD 277.23 billion in 2026.

The Cold Storage is a temperature-controlled warehousing and logistics infrastructure essential for preserving the quality and safety of perishable goods across the supply chain. These facilities, operating at precise low temperatures, are critical for sectors such as food and beverage, pharmaceuticals, and biotechnology, where thermal integrity directly impacts product efficacy and shelf life. As per the World Health Organization, over 50% of vaccines in low-income countries are compromised due to temperature deviations during storage and transport. The expansion of e-grocery platforms and the rise of ready-to-eat meals have further intensified demand for reliable cold storage.

MARKET DRIVERS

Rising Demand for Perishable and Temperature-Sensitive Food Products

The increasing global consumption of perishable food items such as dairy, seafood, meat, and fresh produce, which require uninterrupted refrigeration to maintain safety and quality is escalating the growth of the cold storage market. As per the U.S. Department of Agriculture, global per capita meat consumption has risen from 34.5 kg in 2000 to 43.8 kg in 2022, with the highest growth observed in Asia and Africa. In China, the Ministry of Commerce reports that the volume of refrigerated food transported increased by 18% annually between 2018 and 2023, driven by urbanization and rising disposable incomes. Additionally, the popularity of ready-to-cook and frozen meals has escalated; in the U.S., frozen food sales reached $70 billion in 2023, a 12% increase from 2020, according to the American Frozen Food Institute.

Expansion of the Pharmaceutical and Biologics Supply Chain

The growing complexity and scale of temperature-sensitive pharmaceutical logistics for vaccines, biologics, and cell-based therapies is additionally to fuel the growth of the cold storage market. According to the World Health Organization, over 30% of biopharmaceutical products require storage between 2°C and 8°C, while advanced therapies like mRNA vaccines and CAR-T cells demand ultra-low temperatures as low as -70°C. In India, the National Health Mission deployed over 40,000 solar-powered cold chain equipment units to maintain vaccine potency in off-grid regions.

MARKET RESTRAINTS

High Energy Consumption and Operational Costs

The substantial energy demand required to maintain consistent low temperatures, which is leading to elevated operational expenses and environmental concerns. In the European Union, the European Commission reports that cold storage facilities contribute approximately 4% of the region’s total industrial CO₂ emissions, which is prompting stricter energy efficiency regulations under the Energy Performance of Buildings Directive. In India, the Bureau of Energy Efficiency found that 30–40% of a cold storage facility’s lifecycle cost is attributed to energy, discouraging investment in regions with unreliable or expensive power supply. The use of conventional refrigerants like R-404A, which have high global warming potential, further complicates compliance with the Kigali Amendment to the Montreal Protocol. While energy-efficient compressors and insulation materials are available, their high upfront costs limit adoption among small operators.

Fragmented Infrastructure in Emerging Economies

The lack of integrated and standardized infrastructure in many developing regions, which is resulting in inefficient supply chains and high spoilage rates is limiting the growth of the cold storage market. The absence of centralized cold hubs, inconsistent power supply, and limited technical expertise hinder the development of scalable solutions. These structural gaps not only increase waste but also discourage private investment, as fragmented ownership and regulatory inconsistencies make large-scale cold chain development economically unviable without substantial public sector intervention.

MARKET OPPORTUNITIES

Adoption of Sustainable Refrigeration Technologies

The transition toward eco-friendly refrigerants and energy-efficient systems, is solely to pose new opportunities for the growth of the cold storage market. According to the United Nations Environment Programme, the phase-down of hydrofluorocarbons (HFCs) under the Kigali Amendment could prevent up to 0.5°C of global warming by 2100, incentivizing the adoption of natural refrigerants like ammonia, CO₂, and hydrocarbons. The U.S. Environmental Protection Agency’s GreenChill program has partnered with major retailers to install transcritical CO₂ systems, reducing refrigerant emissions by 80% in participating stores. Additionally, advancements in vacuum insulation panels and smart defrost controls have reduced energy consumption by up to 30%, as demonstrated in pilot projects by the Global Cold Chain Alliance. These innovations not only lower carbon footprints but also reduce long-term operational costs, positioning sustainable cold storage as a strategic investment for both environmental compliance and economic resilience.

Integration of IoT and Digital Monitoring Systems

The integration of Internet of Things (IoT) technologies to enhance visibility, control, and compliance is also to elevate the growth of the cold storage market in coming years. As per the GS1 Global Healthcare Serialization Report, over 70% of pharmaceutical distributors now use IoT-enabled temperature loggers to ensure real-time monitoring and data integrity during storage and transit. In the food sector, companies like Maersk and Lineage Logistics have deployed wireless sensors in over 80% of their cold warehouses by enabling remote alerts for temperature deviations and predictive maintenance, as reported by the World Shipping Council.

MARKET CHALLENGES

Ensuring Resilience Against Climate Change and Power Instability

The increasing vulnerability of temperature-controlled facilities to climate change and unreliable power infrastructure is ascribed to bolster the growth of the cold storage market. According to the Intergovernmental Panel on Climate Change, the frequency of extreme heat events has doubled since the 1980s, placing additional thermal load on refrigeration systems and increasing the risk of system failure. As per a 2023 study by the International Renewable Energy Agency, 45% of cold storage facilities in sub-Saharan Africa operate with backup generators, significantly increasing operational costs and carbon emissions.

Workforce Shortage and Technical Skill Gaps

The shortage of skilled technicians capable of installing, maintaining, and repairing advanced refrigeration systems may also inhibit the growth of the cold storage market. According to the International Institute of Refrigeration, there is a global deficit of over 500,000 trained refrigeration engineers, with the most acute shortages in Africa and South Asia. In Nigeria, the Institute of Refrigeration and Air Conditioning Engineers reports that fewer than 2,000 certified technicians serve a population of over 200 million, leading to prolonged equipment downtime and inefficient operations. In the U.S., the Environmental Protection Agency mandates Section 608 certification for handling refrigerants, yet a 2023 report by the Air-Conditioning, Heating, and Refrigeration Institute found a 20% decline in new certifications over the past five years.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.11% |

| Segments Covered | By Construction type, Temperature, Application, Warehouse Type, And Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Agro Merchants Group, Burris Logistics, Americold Logistics LLC, Wabash National Corporation, Preferred Freezer Services, Lineage Logistics Holding LLC, Nichirei Logistics Co., Ltd. Barloworld Limited, VersaCold Logistics Services, Henningsen Cold Storage, Nordic Logistics and United States Cold Storage. |

SEGMENTAL ANALYSIS

By Construction Type Insights

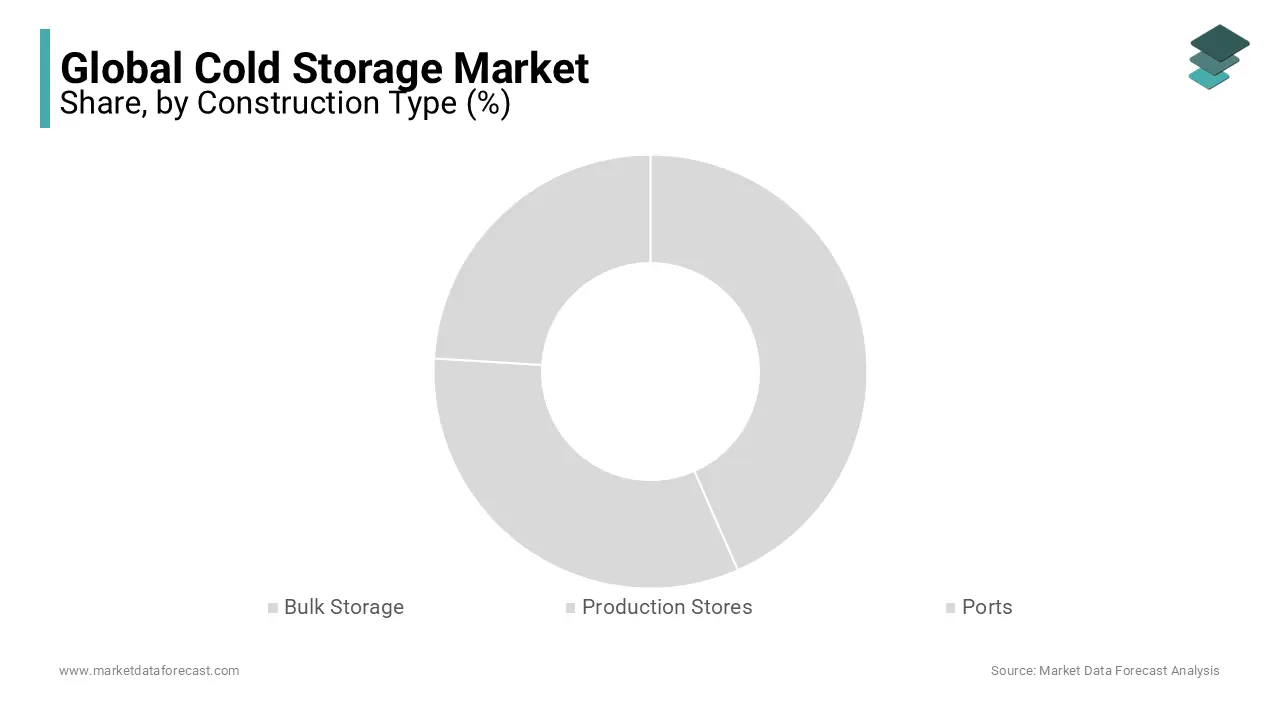

The bulk storage segment was accounted in holding 48.3% of the cold storage market share in 2025 with the need for centralized, high-capacity warehousing to support large-scale agricultural and food supply chains. These facilities serve as critical nodes in national and international trade, enabling inventory buffering, price stabilization, and export readiness. In India, the Ministry of Food Processing Industries reports that bulk storage capacity has increased to 38 million metric tons, yet demand continues to outpace supply, particularly for fruits, vegetables, and dairy. The expansion of organized retail and e-grocery platforms has further intensified the need for regional bulk hubs capable of handling seasonal surpluses.

The port-based cold storage segment is projected to grow at a CAGR of 10.7% during the forecast period with the escalating volume of temperature-sensitive cargo in global trade, particularly perishable foods and pharmaceuticals. According to the World Trade Organization, refrigerated container (reefer) shipments grew by 9.3% annually between 2018 and 2023, outpacing overall container traffic. The U.S. Food and Drug Administration mandates that 100% of imported seafood be stored under controlled temperatures, driving investment in port-side cold facilities. Additionally, the rise of global vaccine distribution has heightened demand for temperature-monitored storage at international gateways.

By Temperature Insights

The frozen segment was the largest and held 58.3% of the cold storage market share in 2025 with the long-term preservation requirements of key commodities such as frozen meat, seafood, and ready-to-eat meals, which must be stored at or below -18°C to maintain safety and texture. According to the U.S. National Fisheries Institute, over 75% of globally traded seafood is transported and stored in frozen form, with countries like Norway and Thailand relying on frozen storage for 90% of their export volumes. According to the American Meat Institute, 85% of beef and pork exports are frozen in the US, which is requiring uninterrupted cold chain integrity.

The chilled segment is anticipated to grow at a CAGR of 9.4% in the next coming years owing to the rising consumer preference for fresh, minimally processed foods and the expansion of urban retail networks that prioritize short-shelf-life products. The rapid rise of e-grocery platforms has further amplified demand; in China, Alibaba’s Freshippo and JD.com’s 7FRESH require last-mile chilled logistics, with over 80% of deliveries occurring within 24 hours of harvest or production. According to the Indian Brand Equity Foundation, India’s chilled food market is expanding at 15% annually, fueled by urbanization and working populations seeking convenience. Additionally, the pharmaceutical sector increasingly relies on chilled storage (2–8°C) for biologics and insulin, with the World Health Organization estimating that over 50% of temperature-sensitive medicines require this range.

By Application Insights

The meat and seafood segment was the largest and held 32.1% of the cold storage market share in 2025 with the perishable nature of animal proteins, which require strict temperature control from slaughter or harvest to retail. According to the U.S. Department of Agriculture, over 90% of beef, pork, and poultry in the U.S. is stored at sub-zero temperatures to prevent microbial growth and extend shelf life. Additionally, rising protein consumption in emerging markets is driving demand; the International Food Policy Research Institute states that per capita meat consumption in sub-Saharan Africa has increased by 30% since 2010.

The pharmaceuticals segment is projected to expand at a CAGR of 11.2% from 2026 to 2034 with the increasing production and distribution of biologics, vaccines, and personalized medicines that require strict thermal control. According to the World Health Organization, over 30% of pharmaceutical products globally are temperature-sensitive, with mRNA vaccines like those for COVID-19 requiring storage at -70°C. The COVAX initiative distributed over 1.9 billion doses by 2023, many of which relied on ultra-low temperature freezers and cold boxes, as reported by Gavi, the Vaccine Alliance.

By Warehouse Type Insights

The private warehouse segment was accounted in holding 52.3% of the cold storage market share in 2025 owing to the large food producers, retailers, and pharmaceutical companies investing in proprietary cold storage to ensure supply chain control, quality assurance, and brand integrity. In the U.S., companies like Tyson Foods and Nestlé operate extensive private cold networks, with Tyson alone managing over 200 temperature-controlled facilities, as per its 2023 sustainability report. Walmart has built a dedicated cold chain infrastructure across its U.S. and Chinese operations, enabling direct farm-to-store logistics for perishables.

The public cold storage segment is expected to grow at a CAGR of 9.8% from 2026 to 2034, which is government initiatives to reduce food waste and support smallholder farmers in developing economies. As per Nigerian Ministry of Agriculture, public cold storage investment has reduced tomato spoilage from 50% to 28% in key farming regions. In Indonesia, the Ministry of Trade has launched a national cold chain program, allocating $1.2 billion to build public refrigerated warehouses in 34 provinces. According to the Food and Agriculture Organization, public facilities can reduce post-harvest losses by up to 35% in low-income countries. These warehouses are often subsidized, multi-tenant, and strategically located near production zones, enabling small producers to access markets.

REGIONAL ANALYSIS

North America Cold Storage Market Insights

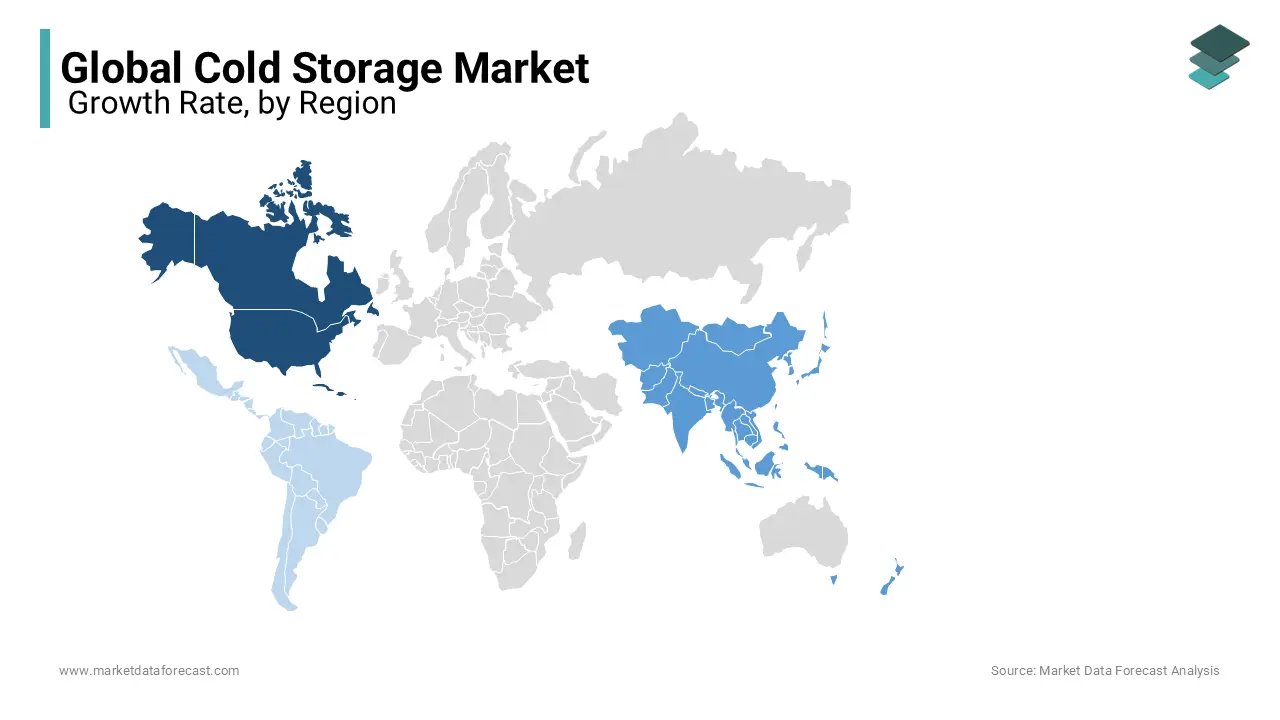

North America was the top performer in the cold storage market by capturing 35.4% of share in 2025 with the advanced logistics infrastructure, stringent food safety regulations, and high consumer demand for fresh and frozen products. The FDA’s Food Safety Modernization Act mandates strict temperature controls across the supply chain, which is driving investment in compliant facilities. Canada has expanded its cold storage network in British Columbia and Quebec to support seafood and dairy exports, with the Canadian Food Inspection Agency reporting a 22% increase in refrigerated warehouse certifications since 2020. The rise of e-grocery platforms like Instacart and Amazon Fresh has further intensified demand for urban cold fulfillment centers. Additionally, the U.S. Department of Energy supports the adoption of low-GWP refrigerants through tax incentives, accelerating the transition to sustainable cold chain solutions.

Europe Cold Storage Market Insights

Europe holds the second-largest share of the cold storage market, accounting for approximately 28% in 2023, as documented by Eurostat. The region’s market is characterized by a highly integrated cold chain, supported by cross-border trade, harmonized regulations, and advanced logistics. The European Commission reports that over 90% of perishable food transported within the EU is temperature-controlled, with reefer truck fleets exceeding 150,000 units. The Netherlands, home to the Port of Rotterdam, serves as a major cold distribution hub, handling 25% of Europe’s refrigerated cargo. Germany operates over 1,200 cold storage facilities, many integrated with automated sorting systems for e-commerce, as per the German Logistics Association. The EU’s Green Deal and F-Gas Regulation are driving the adoption of natural refrigerants, with Denmark and Sweden leading in CO₂-based systems. The European Environment Agency notes that cold storage energy efficiency has improved by 18% since 2015 due to regulatory pressure. With rising demand for organic and fresh foods, and the expansion of meal-kit services, Europe’s cold storage infrastructure continues to evolve toward sustainability, digitalization, and seamless cross-border connectivity.

Asia Pacific Cold Storage Market Insights

The Asia Pacific region accounts for approximately 24% of the global cold storage market, as reported by the Asian Development Bank, and is experiencing the fastest infrastructure development. China, India, and Japan are leading the expansion, driven by urbanization, rising incomes, and government-backed cold chain initiatives. In China, the Ministry of Commerce reports that cold storage capacity has grown to over 200 million cubic meters, with a 12% annual increase since 2020. India’s National Centre for Cold-chain Development estimates that cold chain investment has surged to $15 billion since 2018, focusing on rural pre-cooling and reefer transport. Japan’s aging population has increased demand for chilled ready-to-eat meals, with the Ministry of Health noting a 14% rise in chilled food sales between 2020 and 2023. Australia’s cold storage network has expanded to support high-value exports of dairy and seafood, with the Australian Bureau of Agricultural and Resource Economics reporting a 20% increase in refrigerated warehouse space since 2021. With e-commerce and food delivery booming, APAC is transforming into a dynamic, high-demand market for modern cold storage solutions.

Latin America Cold Storage Market Insights

Latin America holds a 9% share of the global cold storage market, as per the Inter-American Development Bank, with Brazil, Mexico, and Chile leading regional development. Despite challenges, the region is expanding cold infrastructure to support agricultural exports and urban food security. Brazil’s Ministry of Agriculture reports that cold storage capacity for poultry and beef has increased by 18% since 2020, driven by export demand. Mexico’s cold chain covers only 35% of its perishable output, but the government’s ProMéxico program has allocated $800 million to expand refrigerated warehousing. Chile, a major fruit exporter, maintains over 1.2 million m³ of cold storage for grapes and berries, with 90% of exports shipped under temperature control, as per the Chilean Fruit Exporters Association. However, the Pan American Health Organization notes that only 40% of vaccines in rural areas are stored under compliant conditions. Power instability and fragmented logistics remain barriers. Nevertheless, rising middle-class consumption and export-oriented agriculture are driving investment, positioning Latin America as a market with significant growth potential.

Middle East and Africa Cold Storage Market Insights

The Middle East and Africa collectively account for 4% of the global cold storage market, as reported by the African Development Bank, but are witnessing strategic expansion due to food import dependency and climate vulnerabilities. The UAE has emerged as a regional cold chain hub, with Jebel Ali Port housing over 500,000 m² of temperature-controlled storage, as per the Dubai Multi Commodities Centre. Saudi Arabia’s Vision 2030 includes a $2.5 billion investment in cold chain infrastructure to reduce food imports. In South Africa, the Department of Agriculture reports that cold storage capacity has increased by 15% since 2020 to support fruit exports. Nigeria loses over $4 billion annually in post-harvest waste, prompting the government to launch the National Cold Chain Strategy in 2023. The World Bank estimates that cold storage could reduce food loss by 30% across Sub-Saharan Africa. With rising urban populations and climate risks, the region is prioritizing cold storage as a tool for resilience, trade, and public health, signaling a transformative shift in infrastructure development.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a major role in the global cold storage market include Agro Merchants Group, Burris Logistics, Americold Logistics LLC, Wabash National Corporation, Preferred Freezer Services, Lineage Logistics Holding LLC, Nichirei Logistics Co., Ltd. Barloworld Limited, VersaCold Logistics Services, Henningsen Cold Storage, Nordic Logistics and United States Cold Storage.

The cold storage market is witnessing intensified competition shaped by technological differentiation, sustainability mandates, and evolving supply chain demands. Established players compete not only on capacity and location but also on operational sophistication, including automation, energy efficiency, and digital integration. The race to achieve net-zero emissions has pushed firms to adopt eco-friendly refrigerants and renewable energy, with regulatory pressures in Europe and Asia accelerating this shift. In the Asia-Pacific region, competition is further intensified by the entry of local logistics firms offering cost-effective solutions, challenging multinational operators on pricing and agility. The rise of e-grocery and direct-to-consumer food models demands urban cold fulfillment centers, prompting companies to develop compact, high-density warehouses near metropolitan areas. Pharmaceutical cold storage has become a high-stakes battleground, with firms investing in ultra-low temperature facilities for biologics and cell therapies. Mergers, joint ventures, and public-private partnerships are increasingly common, enabling shared infrastructure and risk mitigation. Customer expectations for real-time visibility, compliance reporting, and minimal spoilage are redefining service standards. As climate change and food security concerns grow, the competitive landscape is shifting toward resilient, intelligent, and sustainable cold chain ecosystems that can adapt to global disruptions while ensuring product integrity from origin to end-user.

TOP PLAYERS IN THE MARKET

Lineage Logistics

Lineage Logistics has emerged as a transformative force in the cold storage market, with a growing footprint across the Asia-Pacific region through strategic investments and technological integration. The company operates advanced temperature-controlled warehouses equipped with automated storage and retrieval systems, significantly enhancing operational efficiency. In Australia, Lineage expanded its Melbourne facility in 2023 to support growing demand from food exporters and e-grocery providers. It has also partnered with local logistics firms in Japan and South Korea to integrate its cold chain solutions into last-mile delivery networks. Lineage’s adoption of AI-driven warehouse management systems optimizes energy use and reduces spoilage. By prioritizing sustainability—using CO₂ refrigeration and solar energy—the company aligns with regional environmental goals. Its focus on digitalization, including real-time monitoring and blockchain-enabled traceability, strengthens trust among food and pharmaceutical clients. Through these initiatives, Lineage is redefining cold chain reliability and scalability in dynamic Asia-Pacific markets.

United States Cold Storage (USCS)

United States Cold Storage has strategically extended its influence into the Asia-Pacific market by leveraging its expertise in high-integrity temperature control and pharma-grade storage. While historically focused on North America, USCS has intensified its advisory and technology transfer collaborations with cold chain operators in India, Thailand, and Vietnam, supporting the development of GDP-compliant facilities for vaccine and biologics storage. In 2023, the company launched a knowledge-sharing initiative with Indian cold storage developers to implement energy-efficient ammonia-based refrigeration systems. USCS has also contributed to training programs for refrigeration technicians in Southeast Asia, addressing critical skill gaps. Its emphasis on HACCP and FDA-aligned protocols has made its operational model a benchmark for emerging markets. By sharing best practices in automation, inventory management, and compliance, USCS is playing a pivotal role in modernizing cold chain infrastructure across the region, particularly in pharmaceutical and export-oriented food sectors.

Snowman Logistics (Now Emergent Logistics)

Emergent Logistics, formerly Snowman Logistics, is a pioneering cold chain solutions provider in India and a key contributor to the development of organized cold storage infrastructure across South Asia. The company operates one of the largest integrated cold chain networks in the region, spanning warehousing, refrigerated transport, and value-added services. In 2023, it expanded its facilities in Gujarat and Andhra Pradesh to support seafood and dairy exporters, integrating solar-powered refrigeration to reduce carbon emissions. The company has also partnered with state governments to establish rural pre-cooling centers, reducing post-harvest losses for small farmers. Emergent’s adoption of IoT-enabled monitoring systems ensures real-time temperature tracking across its network. By collaborating with e-commerce platforms and food processors, it has strengthened the cold chain link between production zones and urban consumers. Its focus on sustainability, scalability, and rural inclusion positions it as a critical enabler of India’s agricultural modernization and regional cold storage advancement.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the cold storage market are deploying multifaceted strategies to solidify their competitive edge. Expansion through strategic acquisitions and greenfield developments enables rapid geographic reach, particularly in high-growth regions like Asia-Pacific. Companies are investing heavily in automation, integrating robotic systems and AI-driven warehouse management to enhance throughput and reduce labor dependency. Sustainability is a core focus, with firms adopting natural refrigerants like CO₂ and ammonia, installing solar panels, and optimizing energy use to comply with global climate regulations. Digital transformation is accelerating, with IoT sensors, blockchain, and cloud-based platforms enabling real-time temperature monitoring and end-to-end traceability. Strategic partnerships with food producers, pharmaceutical firms, and governments ensure long-term contracts and infrastructure alignment. Additionally, firms are diversifying service offerings to include value-added services such as blast freezing, packaging, and labeling. Workforce training and compliance with international standards like GDP and HACCP further strengthen credibility. These strategies collectively enhance operational resilience, customer trust, and long-term scalability in an increasingly complex cold chain landscape.

RECENT HAPPENINGS IN THE MARKET

- In January 2022, Lineage Logistics acquired NewCold, a Netherlands-based automated cold storage provider, enhancing its technological capabilities in robotics and energy-efficient warehousing for expansion into Asia-Pacific markets.

- In June 2022, Emergent Logistics launched a solar-powered cold storage facility in Vijayawada, India, reducing grid dependency and operational emissions while supporting local agricultural supply chains.

- In March 2023, Lineage Logistics partnered with Mitsubishi Logistics to develop integrated cold chain solutions in Japan, combining automation expertise with regional distribution networks.

- In September 2023, United States Cold Storage introduced a digital cold chain compliance platform used in advisory projects across Southeast Asia, improving temperature monitoring and regulatory adherence for pharmaceutical clients.

- In February 2025, Emergent Logistics expanded its refrigerated transport fleet by 30% in South India, strengthening last-mile connectivity for dairy and seafood producers supplying urban retail and export markets.

MARKET SEGMENTATION

This research report on the global cold storage market has been segmented and sub-segmented based on construction type, temperature, application, warehouse type, & region.

By Construction Type

- Bulk Storage

- Production Stores

- Ports

By Temperature

- Chilled

- Frozen

By Application

- Processed Foods

- Dairy Products

- Fruits and Vegetables

- Meat and Seafood

- Pharmaceuticals

By Warehouse Type

- Public

- Private

- Semi-Private

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is cold storage?

Cold storage refers to temperature-controlled facilities used to preserve perishable goods like food, pharmaceuticals, and chemicals.

2. What is driving the growth of the cold storage market?

Rising demand for frozen and packaged foods, e-commerce grocery sales, and growth in the pharmaceutical sector.

3. Which region dominates the cold storage market?

North America leads, while Asia-Pacific is the fastest-growing due to expanding food supply chains.

4. What role does technology play in cold storage?

Automation, IoT sensors, and AI-based monitoring improve energy efficiency and inventory management.

5. What challenges does the cold storage market face?

High energy costs, infrastructure investment requirements, and lack of skilled workforce.

6. Who are the major players in the cold storage market?

Key companies include Lineage Logistics, Americold Logistics, NewCold, Nichirei Logistics, and DHL Supply Chain.

7. What is the role of cold chain logistics in pharmaceuticals?

It ensures vaccines, biologics, and temperature-sensitive medicines are stored and transported safely.

8. What is the future outlook for the cold storage market?

The market is expected to expand significantly with advancements in automation and rising global food trade.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com