Global Critical Infrastructure Protection Market - Size, Share, Trends, & Growth Forecast Report by Services (Consulting, Risk Management and Managed), Security Type (OT and IT) & Region - Industry Forecast From 2026 to 2034

Market Size, 2025

$147.35 BnMarket Estimate, 2026

$152.36 BnMarket Forecast, 2034

$199.08 BnCAGR, 2026–2034

3.4%Global Critical Infrastructure Protection Market Size

The global critical infrastructure protection market was worth USD 147.35 billion in 2025. The global market is predicted to reach USD 152.36 billion in 2026 and USD 199.08 billion by 2034, growing at a CAGR of 3.4% from 2026 to 2034.

Critical infrastructure protection (CIP) encompasses the set of physical, cyber, policy, and operational measures that public and private owners use to ensure continuity, availability and safety of systems deemed essential to society, energy grids, water and wastewater networks, transportation, health care, financial systems and communications. CIP today is a convergence discipline: legacy operational-technology (OT) and control systems intersect with IT and cloud services, raising attack surface and resilience requirements. According to the European Union Agency for Cybersecurity (ENISA), more than 11,000 security events were documented in the latest threat-landscape period, with availability and ransomware among the prime threats to industrial and critical sectors.

MARKET DRIVERS

Rapid escalation of ransomware and OT-focused extortion (100–150 words)

Operational disruption as a revenue stream has shifted adversary calculus: once limited to data theft, many criminal groups now weaponize ransomware against industrial control environments to force payments or cause outages. OT-targeted extortion surged in recent years, Dragos documented a steep increase in ransomware incidents against industrial organizations, reporting a notable number of ransomware attacks on industrial targets in its latest year-in-review, an increase of 87% year-over-year this makes availability protection and secure OT-IT segmentation immediate demand drivers for CIP solutions such as immutable backups, OT monitoring and incident playbooks. The frequency and visibility of such attacks push operators to procure hardened controllers, real-time anomaly detection, and robust incident response retainers.

Rising per-incident financial and operational consequences are driving investment in resilience

CIOs and boardrooms now quantify cyber incidents in operational-loss terms rather than purely reputational risk, which fuels procurement of preventive and resilience capabilities. Industry analysis shows that breaches in industrial sectors are significantly expensive; this high per-incident bill accelerates demand for CIP services such as continuous monitoring, zero-trust access for control networks, and cyber insurance. As firms internalize these potential losses, budgets shift from ad-hoc IT cyber spend to integrated OT/IT resilience programs emphasizing continuity, detection, and recovery.

MARKET RESTRAINTS

Acute skills and talent shortage in cybersecurity and OT disciplines

The human capital deficit constrains the speed and quality of CIP deployments. Globally the cybersecurity workforce gap remains large; ISC2’s workforce studies estimate a multi-million shortfall (roughly 4.7–4.8 million people in recent assessments), and the gap is widening. This scarcity is particularly acute for personnel with combined IT-OT, cloud and industrial control expertise. The result is slower project rollouts, reliance on expensive external service providers, and persistent misconfigurations in ICS/SCADA environments. Organisations must compete for narrow talent pools, invest heavily in upskilling, or adopt managed-service models, each of which alters procurement economics and slows broad adoption of advanced CIP capabilities.

Legacy systems, long equipment lifecycles, and fragile upgrade paths

Critical-infrastructure operators often run equipment with decades-long lifecycles; many ICS devices were designed without security in mind and cannot be patched or isolated easily. These legacy constraints impede the rapid deployment of modern security controls, network segmentation, TLS encryption and endpoint agents are often incompatible with older controllers or interrupt safety-critical processes. Moreover, supply-chain complexity means firmware and vendor patches may be slow or unavailable, forcing operators to adopt compensating controls rather than ideal solutions. This technological inertia increases the operational cost of achieving target risk postures and limits the addressable opportunity for solutions that assume modern, upgradable endpoints.

MARKET OPPORTUNITIES

Demand for managed resilience and pre-incident services

As attacks become faster and more automated, operators increasingly prefer outcome-oriented service models, managed detection & response (MDR) for OT, breach-simulation tabletop services, and pre-ransomware detection notifications over one-off products. Government agencies are also proactively notifying firms about pre-ransomware activity. The institutionalization of pre-incident notification and retained response teams creates recurring revenue streams for service providers and a clear path for private-public collaboration.

Modernisation cycles and convergence spend

Utilities and transport networks face twin pressures: regulatory mandates for resilience and the need to modernize for efficiency (smart grids, sensorized water networks, connected rail signaling). Those modernization programs create natural windows to bake security into new deployments, secure controllers, encrypted telemetry, identity-centric access, and CI/CD pipelines for OT firmware. Vendors that can offer integration-friendly, safety-aware security modules (e.g., microsegmentation appliances certified for industrial use, vendor-agnostic OT threat detection) will capture follow-on spend. Moreover, grant and infrastructure funding in many jurisdictions prioritise resilient modernization, widening addressable budgets for CIP capabilities beyond basic cyber hygiene.

MARKET CHALLENGES

Geopolitical escalation and nation-state targeting

Critical infrastructure increasingly sits at the intersection of crime and geopolitics; nation-state actors and proxies exploit geopolitical tensions to target availability and control functions. Cyber and technology risk is one of the top systemic threats in the near term, which elevates the complexity of defensive planning because adversaries bring long-term reconnaissance, bespoke tooling, and sometimes the ability to mount multi-vector campaigns that combine kinetic and cyber effects. The attribution uncertainty and political sensitivity of some incidents complicate information-sharing and cross-border coordination, and operators must therefore prepare for attacks that exceed the scope of commercial-grade countermeasures.

Interdependencies and cascading failure potential

Modern critical systems are tightly coupled electricity enables telecoms, which enable emergency services and control centers. A localized disruption can cascade rapidly through supply chains and service layers, turning a single-sector outage into a multi-sector crisis. That interdependence raises the technical bar for CIP providers: resilience must be measured in systemic terms, not per-asset. Designing and testing for cascade scenarios requires cross-sector exercises, shared telemetry standards, and escape-hatch architectures (e.g., islanding for grids, manual fallback controls for industrial plants). Achieving such cross-domain resilience is organizationally and technically arduous, demanding greater public-private coordination and investment in interoperable situational awareness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.4% |

| Segments Covered | By Services, Security Type, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | BAE Systems, Airbus Group SE, Honeywell International Inc, General Dynamics Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Company, Teltronic SA, Hexagon AB, Huawei Technologies Co Ltd., Thales Group, Johnson Controls International plc and Motorola Solutions Inc., and Others. |

SEGMENTAL ANALYSIS

By Services Insights

By Security Type Insights

The physical safety and security segment accounted for 56.9% of total CIP spend in 2025, establishing dominance in the security-type breakdown. Enterprises still invest heavily in guarding tangible assets and legacy control environments, where modernization is slow and physical controls remain essential fronts of protection. Many critical sites still operate with long-lived, air-gapped systems and physical controls, which cannot be easily replaced or integrated with digital overlays. The inertia of such systems, combined with safety certifications and operational continuity demands, means physical and control-centric investments continue to attract the majority of spend even as cybersecurity threats multiply.

The cybersecurity in CIP domains segment is expanding annually at 5.9%, representing the fastest-growing slice as attackers increasingly exploit IT-OT convergence points. The expansion of zero-trust baselines and network micro-segmentation products, designed to isolate legacy assets without shutting down plants, is fueling this rapid growth. The shift into hybrid architectures, where OT systems connect to IT and cloud platforms, has multipliedthe attack surface. As industrial systems become targets for ransomware and remote exploitation, demand surges for cybersecurity controls, zero-trust, micro-segmentation, identity-aware access, and real-time IT-OT monitoring, leading to outsized growth in IT-focused CIP investments.

REGIONAL ANALYSIS

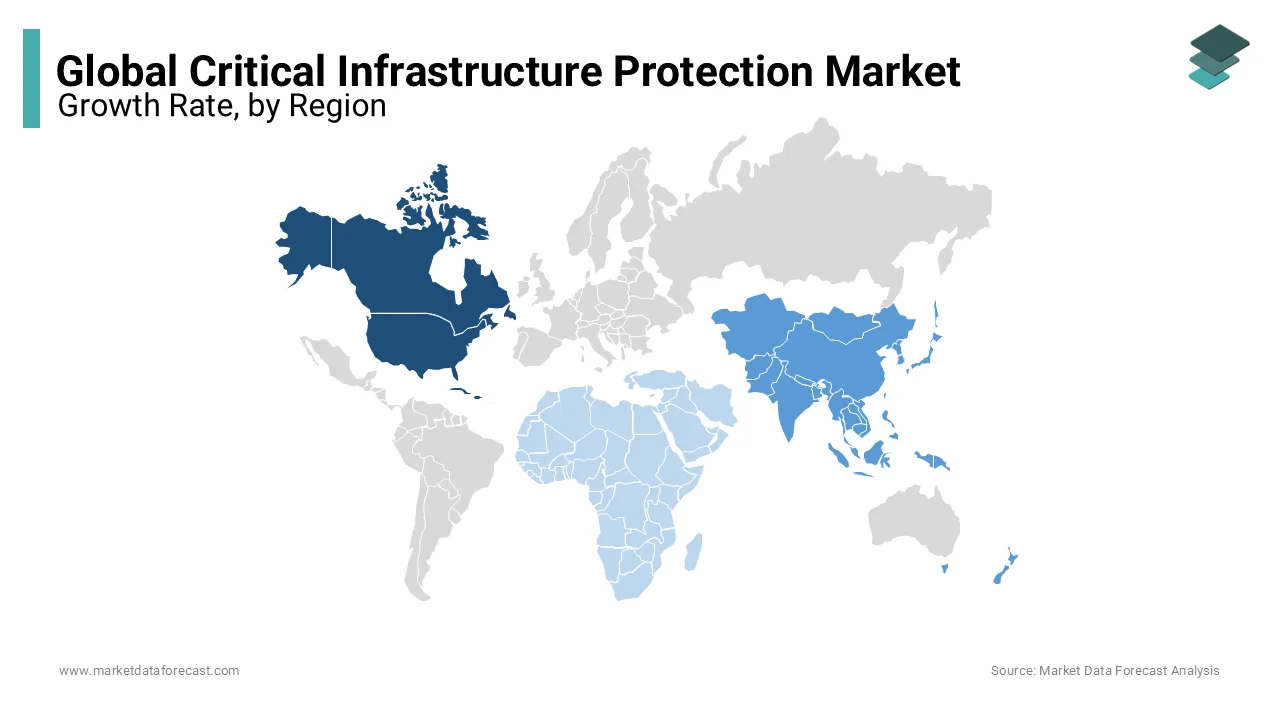

North America Critical Infrastructure Protection Market Insights

North America led the global critical infrastructure protection spectrum by controlling around 38.4 % of the market. This supremacy results from a combination of mature infrastructure assets, high-profile cyber-physical attacks, and aggressive public-private funding. For instance, the U.S. and Canada have allocated substantial budgets toward CIP capabilities and maintain headquarters of many major CIP vendors.

Europe Critical Infrastructure Protection Market Insights

Europe trails closely. Its position is due to stringent regulatory mandates, like the NIS Directive, that require operators of essential services to harden infrastructure. Encryption in grid systems, sensor-based mobility networks, and mandatory cybersecurity resilience programs in energy and transport drive these investments.

Asia Pacific Critical Infrastructure Protection Market Insights

Asia Pacific is the fastest-growing region. Rapid urbanization, smart-city initiatives, and high frequency of natural disasters are pushing governments in China, India and others to embed CIP systems from the start of infrastructure planning, particularly real-time asset monitoring and threat detection in utilities and transport.

Middle East & Africa Critical Infrastructure Protection Market Insights

MEA accounts for a notable share of the market. Its share is anchored by oil & gas security, expansion of smart urban infrastructure, and high-profile mega projects (like NEOM) that mandate next-gen surveillance and resilience systems. Rapid geo-strategic investments and energy-sector modernization underpin this regional demand.

Latin America Critical Infrastructure Protection Market Insights

Latin America remains smaller, but with robust growth pockets. Brazil’s financial systems, especially post-PIX cyber threats, and pipeline monitoring in Mexico are fuelling sectoral CIP spend. Despite a lower absolute share, the region offers high potential in differential niches like financial infrastructure resilience.

KEY MARKET PARTICIPANTS

BAE Systems, Airbus Group SE, Honeywell International Inc., General Dynamics Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Company, Teltronic SA, Hexagon AB, Huawei Technologies Co Ltd., Thales Group, Johnson Controls International plc and Motorola Solutions Inc., and Others.

TOP LEADING PLAYERS IN THE MARKET

Siemens AG

Siemens plays a pivotal role in the Asia-Pacific CIP market by investing heavily in grid modernization and smart-infrastructure projects. Its Indian subsidiary sales increased last year, as the company prioritized transportation systems, renewable energy grid upgrades, and sustainable product labeling via its “Siemens EcoTech” initiative, which resonates well with regional demand for eco-friendly, resilient infrastructure solutions, strongly bolstering its position across Asia’s growing electrification and mobility sectors.

Honeywell International Inc.

Honeywell fortifies its Asia-Pacific footprint through integrated OT-cybersecurity and industrial automation offerings. Its Honeywell Forge Cybersecurity+ platform provides continuous monitoring and real-time threat detection tailored to critical control environments across sectors like energy and manufacturing. At refineries, Honeywell solutions have demonstrably enhanced uptime, system reliability, and safety by aligning industrial network cybersecurity with global standards and enabling 24/7 expert monitoring, cementing its regional strength in CIP delivery.

ABB Ltd.

ABB brings deep operational-technology and automation credentials into the Asia-Pacific CIP space. Its partnerships for instance, with Nozomi Networks deliver combined OT/IoT security solutions that address industrial resiliency, particularly across energy and process sectors. ABB’s legacy in robotics and electrification, coupled with increasing focus on digital grid and automation systems in APAC, positions it as a key provider of holistic automation plus security answers across the region’s evolving critical infrastructure landscapes.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key CIP market players deploy a range of strategic approaches to cement their leadership: strategic regional reinvestment, platform integration, M&A for capability scaling, public-private collaboration, and sustainability-aligned offerings. Siemens, for instance, leverages India’s electrification boom and renewable expansions. Honeywell enhances platform value via integrated digital-cyber offerings like Forge Cybersecurity+. ABB forms OT-security partnerships (e.g., Nozomi) to serve APAC utilities and industries. Additionally, Cisco’s acquisition of Splunk strengthens observability and security convergence. Across the board, companies are aligning CIP solutions with environmental, regulatory, and infrastructure modernization themes to stay ahead of evolving regional needs.

COMPETITIVE LANDSCAPE

The Critical Infrastructure Protection market is characterized by a dynamic interplay of global engineering giants and nimble cybersecurity innovators. Established players like Siemens, Honeywell, and ABB bring deep industrial domain experience, trusted relationships, and expansive APAC footprints. They are increasingly integrating software-defined resilience, zero-trust frameworks, and managed-service models into their offerings. Meanwhile, regional specialists and IT-security disruptors challenge incumbents with niche OT-cyber tools, analytics, and threat-intelligence convergence. The battleground now lies in delivering seamless, scalable, and sustainable protection across converged IT-OT environments. Rapid digitization, regulatory tightening, and high-impact cyber events are pushing demands higher, and the market is evolving from siloed hardware sales toward live, outcome-oriented resilience ecosystems across Asia-Pacific and beyond.

RECENT MARKET DEVELOPMENTS

- March 2024, Cisco acquired Splunk Inc., merging security, observability, AI, and networking capabilities into its portfolio. This unified digital perspective enhances its CIP offerings and strengthens its infrastructure protection posture across sectors.

- March 2025, Fortinet introduced substantial updates to its OT Security Platform at the Gartner Digital Workplace Summit in Singapore. These enhancements deliver advanced visibility, micro-segmentation, and secure connectivity solutions for transport, energy, and manufacturing infrastructures, advancing its CIP relevance in APAC.

- January 2025, a leading oil & gas security services provider launched an AI-driven proactive-threat-detection platform targeted at offshore assets. This innovation underscores the increasing AI infusion into CIP and extends responsive capabilities in high-value sectors.

- August 2025, CISA released thirty-two Industrial Control Systems advisories, including vulnerabilities in Siemens and Rockwell Systems. This high-visibility alert further elevates the urgency for CIP solutions and reinforces vendor roles in patching and monitoring critical systems.

- March 2024, Siemens re-emphasized India as a key growth market, directing investments toward grid upgrades, transportation modernization, and renewable infrastructure, and introduced its “EcoTech” sustainability label for products this dual strategy strengthens its CIP leadership in APAC’s green and smart infrastructure wave.

MARKET SEGMENTATION

This research report on the global critical infrastructure protection market has been segmented and sub-segmented based on the service, security type, and region.

By Services

- Consulting

- Risk Management

- Managed

By Security Type

- Operational Technology (OT)

- Information Technology (IT)

By Region

- North America

- Latin America

- Asia Pacific

- Europe

- Middle East & Africa

Frequently Asked Questions

What specific technologies are gaining traction within the Critical Infrastructure Protection market?

Technologies such as AI-driven analytics, IoT-based security systems, blockchain for secure data management, and biometric access control systems are gaining significant traction due to their effectiveness in enhancing infrastructure security.

How are government initiatives impacting the Critical Infrastructure Protection market globally?

Governments worldwide are implementing various initiatives to bolster critical infrastructure security, including funding programs, regulatory frameworks, and public-private partnerships, thereby driving market growth.

What role do emerging technologies like 5G and smart grids play in shaping the future of Critical Infrastructure Protection?

Emerging technologies such as 5G networks and smart grids introduce new security vulnerabilities, driving the need for innovative protection solutions to safeguard critical infrastructure from evolving threats.

How significant is the role of cybersecurity in Critical Infrastructure Protection, and what measures are being taken to enhance cybersecurity readiness globally?

Cybersecurity plays a pivotal role in Critical Infrastructure Protection, with efforts focused on enhancing threat detection capabilities, implementing robust encryption protocols, and promoting cybersecurity awareness and training programs among infrastructure operators worldwide.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com