Global Echocardiography Market Size, Share, Trends & Growth Forecast Report By Device Type (Cart Based, Handheld), Test Type (Transthoracic Echocardiography, Transesophageal Echocardiography, Stress Echocardiography, Others), Technology (2D, 3D & 4D, Doppler Imaging), End-user (Hospitals & ASCs, Diagnostic Center, Others), and Region (North America, Europe, Asia-Pacific, Middle East & Africa, Latin America) – Industry Analysis, 2026 to 2034

Global Echocardiography Market Size

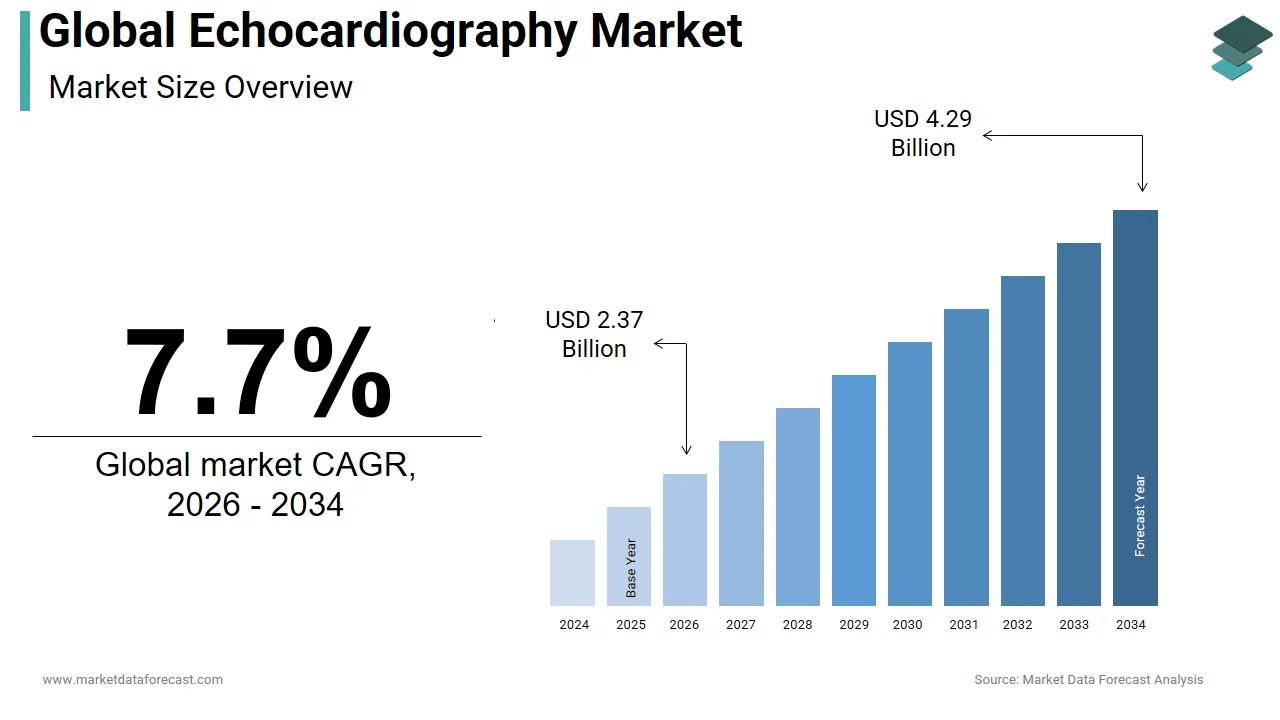

The global echocardiography market was valued at USD 2.20 billion in 2025, is estimated to reach USD 2.37 billion in 2026, and is projected to reach USD 4.29 billion by 2034, growing at a CAGR of 7.7% from 2026 to 2034.

Echocardiography, noninvasive ultrasound visualization of the heart, has become indispensable for diagnosing and managing cardiovascular conditions. This diagnostic method’s real-time imaging capability, absence of radiation, and relative cost-effectiveness drive its adoption across hospitals and outpatient clinics worldwide. Advancements in automation and AI, such as real-time probe guidance and image quality assessment, are expanding access in resource-limited areas, promising improved diagnostic consistency and clinical reach.

MARKET DRIVERS

Escalating Prevalence of Cardiovascular Disease

The global rise in cardiovascular disease (CVD) is a primary demand driver for echocardiography. Echocardiography, being non-invasive and highly informative of structure and function, becomes a frontline imaging tool amid this escalating burden. Its ability to detect valve disorders, ventricular dysfunction, and hemodynamic anomalies in real time positions it as a critical modality in preventive cardiology and acute care. As CVD prevalence grows, so does reliance on echocardiography as both a diagnostic and monitoring asset.

Technological Innovations Enhancing Accessibility

Cutting-edge technologies are reshaping echocardiographic accessibility and quality. Systems offer real-time probe guidance, reducing operator variability and enabling non-experts to achieve accurate imaging, particularly valuable in underserved or primary care settings. AI-driven tools are emerging for automated image-quality assessment and standardization, alleviating reliance on subjective interpretation and enhancing consistency across readings. These advancements lower training thresholds and mitigate inter-observer variability, expanding echocardiography’s reach into diverse clinical environments while maintaining diagnostic reliability.

MARKET RESTRAINTS

High Equipment Costs and Skilled Labor Shortages

Last-mile access to advanced echocardiography systems remains constrained by high capital and operational costs. Sophisticated cart-based units can be prohibitively expensive for rural or budget-limited clinics, while portable versions, though more affordable, may lack advanced features. Additionally, accurate image acquisition and interpretation demand trained sonographers and cardiologists, who are scarce in many regions. Workforce training is often unclear or inadequate, according to professional societies. These twin challenges restrict the equitable deployment of echocardiography and hinder its adoption in under-resourced areas.

Interpretation Variability and Standardization Challenges

Interpreting echocardiograms remains partly subjective, leading to inconsistencies across readers and facilities. Accreditation programs have emerged to mitigate this, yet inter-observer variability persists. Furthermore, newer techniques, such as speckle tracking, suffer from algorithmic and vendor-specific discrepancies, complicating cross-platform comparisons and undermining standardization. Without universal calibration or transparency of analytic methods, reported results may diverge significantly between systems, limiting comparability in multi-center studies and clinical continuity. This inconsistency undermines clinician confidence and scalability.

MARKET OPPORTUNITIES

AI-Enabled Automation and Remote Guidance

AI-driven platforms usher in a new era of remote and semi-autonomous echocardiography. By guiding probes in real time and optimizing image capture, these systems empower primary care providers and non-specialists to perform reliable diagnostic scans. This is especially transformative in underserved or remote regions, where echocardiographic services are scarce. Such tools represent a shift toward democratizing cardiac imaging while preserving quality.

Aging Populations Driving Screening Initiatives

Demographic aging globally is creating new screening imperatives. population echocardiography cohorts, indicate a substantial prevalence (20–30%) of subclinical valve disease in older adults. This demographic shift increases demand for early detection in primary and geriatric care. Early identification of structural heart ailments enables better management, reducing downstream hospitalization and morbidity. Echo-screening programs in aging populations could hence become a foundational pillar in comprehensive cardiac care strategies.

MARKET CHALLENGES

Accreditation Gaps and Workforce Ambiguity

While accreditation programs exist to standardize echocardiographic practice, uptake and governance remain inconsistent globally. Many regions lack clear pathways for training and retaining sonographers, contributing to variability in quality and competency. The British Society of Echocardiography, for instance, notes persistent ambiguity around workforce development, a concern echoed by other professional bodies worldwide. Without structured accreditation and training programs, scaling echocardiography services risks perpetuating inconsistency, undermining diagnostic reliability, and inhibiting broader deployment.

Disparate Standards in Emerging Techniques

Emerging modalities like speckle tracking offer nuanced functional insights, yet their value is eroded by non-standardized algorithms and inconsistent vendor protocols. Each platform implements unique tracking and measurement approaches, with results that may diverge substantially between systems. Without universal reference models or open algorithm disclosure, cross-compatibility and multi-site studies become problematic. Such fragmentation hampers widespread adoption despite scientific potential, limiting these methods to isolated research settings rather than mainstream clinical use.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Device Type, Test Type, Technology, End-User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Market Leaders Profiled | FUJIFILM Holdings Corporation, Koninklijke Philips N.V., Boston Scientific Corporation, Canon Medical Systems Corporation, ESAOTE SPA, CHISON Medical Technologies Co., Ltd, Samsung Electronics Co., Ltd, Siemens Healthineers AG, General Electric Company, and Others. |

SEGMENTAL ANALYSIS

By Device Type Insights

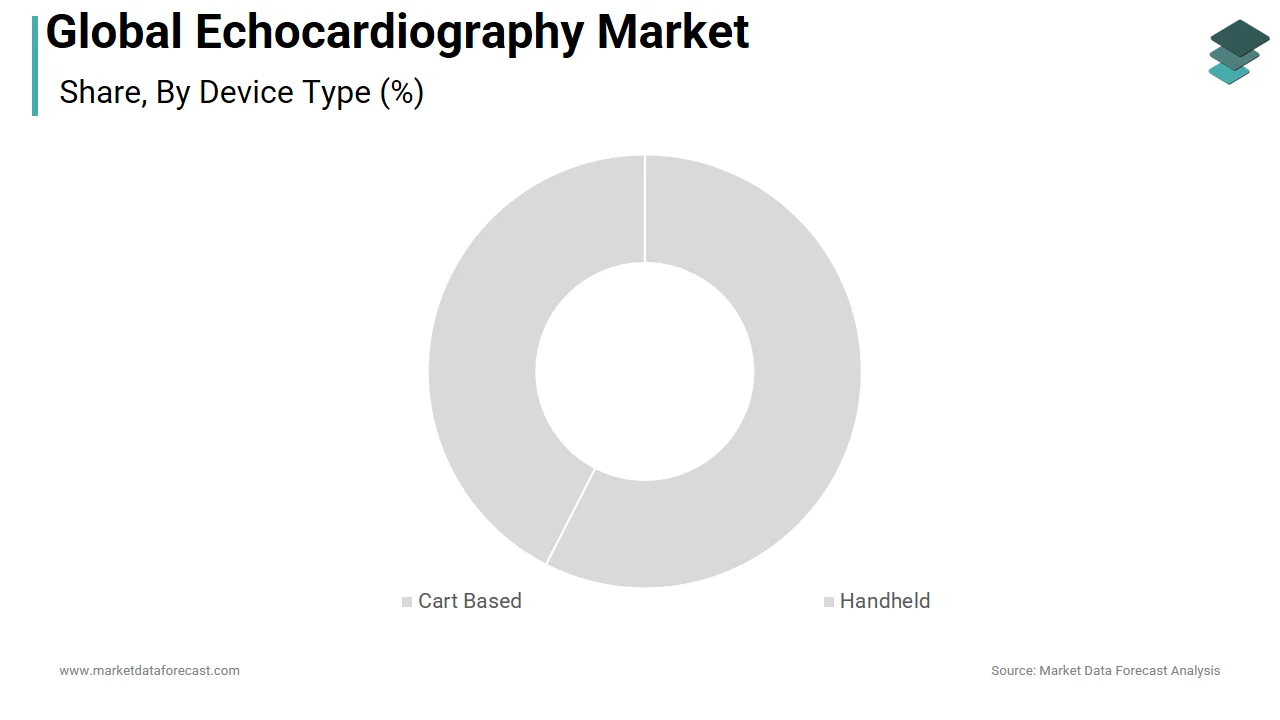

The Cart- or trolley-based echocardiography systems command approximately 65% of the market share in 2024, thanks to their advanced imaging capabilities and prevalence in high-volume healthcare settings. These units support comprehensive diagnostic tasks and display superior imaging quality, making them essential in tertiary hospitals where intricate structural assessments are routine. In fact, over 70% of large hospitals worldwide deploy cart-based systems to manage critical patient loads and ensure diagnostic precision. Manufacturers are enhancing these platforms with AI and cloud integration to further elevate diagnostic accuracy and workflow efficiency.

Cart-based systems remain indispensable due to their superior imaging capabilities and multi-functionality, which are critical in complex cardiovascular diagnostics. Equipped with Doppler, strain analysis, and often 4D imaging, these platforms deliver high-resolution structural and flow assessments, enhancing cardiologists’ ability to detect subtle pathologies. Their physical design supports comprehensive features such as mounted monitors, multiple input ports, and software expandability, making them resilient in high-throughput environments. This robustness underpins their dominance in institutional settings where diagnostic accuracy and throughput are non-negotiable.

Portable or handheld echocardiography is expanding rapidly, achieving around 35% of the market share in 2024. These compact units are increasingly indispensable in remote, point-of-care, and decentralized healthcare settings due to their portability, affordability, and growing feature parity with full-size systems. Approximately 40% of diagnostic centers in developing regions adopted handheld devices in 2024 to bridge diagnostic gaps and extend service reach.

Handheld echocardiography devices are gaining momentum for their ability to deliver rapid, bedside cardiac assessments across diverse care environments emergency departments, community clinics, and home visits. Their integration with telehealth platforms allows remote specialists to interpret scans, bridging expertise gaps in underserved regions. As imaging quality improves, hand-held tools now rival those of larger carts in many applications. This democratization of diagnostic access, enabled by cost-effective technology, is a prime driver of the segment’s swift expansion.

By Test Type Insights

The TTE segment remained the most commonly used modality, though exact share figures are not specified in the sources. Its noninvasive nature, ease of application, and broad diagnostic utility make it the modality of choice across outpatient and inpatient settings. TTE serves as the frontline diagnostic tool for cardiac assessment due to its safety, ease of use, and broad applicability. It enables real-time evaluation of chamber dimensions, pump function, valvular integrity, and hemodynamics without requiring sedation or invasive procedures. The simplicity of probe placement on the chest wall, combined with its immediate read-out and interpretability, allows for rapid decision-making in routine care, from heart failure monitoring to murmur evaluation. These practical advantages cement TTE’s foundational position in clinical cardiology.

The portable/handheld devices segment is the fastest-growing within test-type segmentation due to their adaptability in remote and decentralized care. While specific CAGR isn't given, the trend is clear. As healthcare delivery shifts toward decentralized and home-based models, portable echocardiography, particularly mobile TTE, has become crucial for community-based cardiovascular screening and monitoring. Clinics and ambulatory centers, especially in lower-resource regions, are investing in these devices to enable point-of-care diagnostics without imposing patient burden or referral barriers. Their compact design, coupled with acceptable image quality, allows seamless deployment even in primary care or rural settings, accelerating the modality’s acceptance and growth.

By Technology Insights

The 2D imaging segment dominated the technology landscape by holding 66.3% of the market in 2024. Its cost-efficiency, ease of use, and compatibility with add-on modalities like Doppler and strain analysis secure its position across a wide range of care environments.

2D echocardiography retains its stronghold due to its proven clinical utility, operational simplicity, and well-established role in cardiac diagnostics. It delivers real-time imaging of anatomy and motion with clarity, allowing practitioners to evaluate chamber sizes, wall motion, and basic valvular function reliably. The technology integrates seamlessly into diverse care settings from emergency rooms to community clinics, requiring minimal training and infrastructure. Its compatibility with Doppler and strain enhancements further extends its versatility without complicating workflow or compromising diagnostic consistency.

By End-User Insights

The Hospitals and ASCs segment led the market in 2025. It is due to the sheer volume of cardiovascular procedures and institutional reliance on advanced echocardiographic infrastructure. Hospitals and ASCs remain the backbone of echocardiography utilization, serving large volumes of patients across diagnostic and perioperative contexts. Equipped with trained personnel and imaging infrastructure, these centers rely on echocardiography for preoperative assessments, in-procedure monitoring, and postoperative cardiac evaluations. The efficiency and accuracy of echo-guided decision-making are critical in high-pressure environments where time, quality, and clinical precision are paramount. As cardiac care becomes more procedure-intensive, so does the dependency on robust echocardiographic capability in these settings.

The ambulatory care centers and home care settings segment is emerging rapidly, enabled by portable technologies and shifting care models. The trend toward outpatient management of cardiovascular conditions fuels rising echocardiography demand in diagnostic centers, ASCs, and home care models. Driven by patient preference, cost-containment strategies, and technological innovation, these segments are expanding echocardiographic services beyond hospital walls. Portable devices enable rapid, on-site screening and monitoring, aligning with preventive healthcare objectives. As ancillary cardiac diagnostics decentralize, these users gain prominence as echocardiography’s fastest-growing domain.

REGIONAL ANALYSIS

North America Echocardiography Market Insights

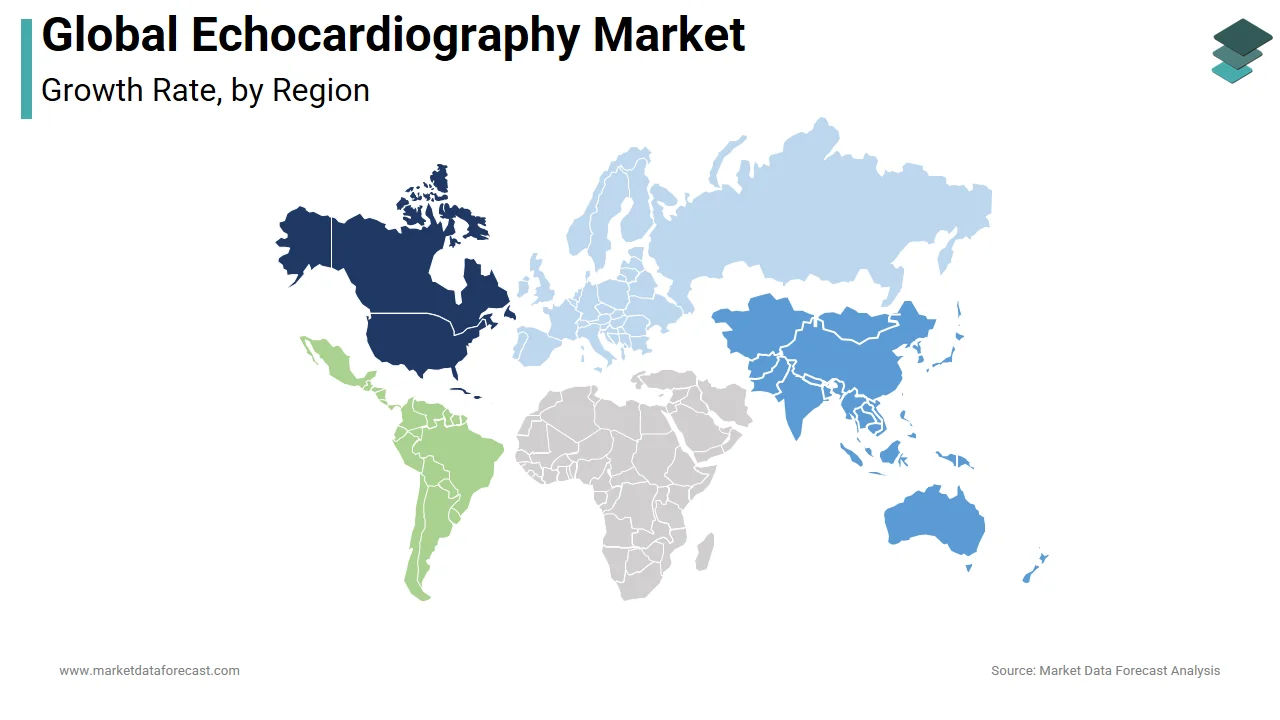

North America remained the largest regional market share at 45.4% in 2024. It is driven by advanced infrastructure, high CVD prevalence, and strong reimbursement frameworks. A notable share of U.S. hospitals with cardiology programs use 3D systems, highlighting mature technology adoption.

Europe Echocardiography Market Insights

Europe is another key player in the market, supported by robust public health systems, preventive cardiology mandates, and favorable reimbursement. For example, Germany reimburses strain echocardiography for cardiomyopathy.

Asia-Pacific Echocardiography Market Insights

Asia-Pacific is the fastest-growing region. Investment in infrastructure, rising CVD burden, and urban healthcare development propel this growth.

Latin America Echocardiography Market Insights

Latin America currently contributes a notable share of the market, with moderate growth supported by urbanization, increasing cardiovascular awareness, and expanding diagnostic access.

Middle East & Africa Echocardiography Market Insights

Middle East & Africa also holds a small share, showing potential tied to healthcare modernization efforts, but is constrained by resource limitations and infrastructural challenges.

KEY MARKET PLAYERS

Some of the noteworthy companies in the global echocardiography market profiled in this report are FUJIFILM Holdings Corporation, Koninklijke Philips N.V., Boston Scientific Corporation, Canon Medical Systems Corporation, ESAOTE SPA, CHISON Medical Technologies Co., Ltd, Samsung Electronics Co., Ltd, Siemens Healthineers AG, General Electric Company, and Others.

TOP LEADING PLAYERS IN THE MARKET

GE Healthcare

GE Healthcare plays a prominent role in the Asia-Pacific echocardiography landscape, with its broad portfolio of cart-based and portable ultrasound systems used across hospitals and clinics. By promoting lightweight systems suitable for remote regions and integrating AI features such as auto-image optimization, the company has enhanced diagnostic access in emerging Asian markets. Its long-standing reputation for product reliability and support infrastructure continues to reinforce its regional positioning.

Philips Healthcare

Philips Healthcare has strengthened its presence in Asia-Pacific through innovation and targeted product launches. This aligns perfectly with the growing demand for automated support in understaffed regions. By localizing training programs and deploying AI-enhanced handheld units in markets like India and Southeast Asia, Philips improves both access and operator efficiency. Their dual focus on smart imaging and regional adaptation reinforces their leadership across varied clinical environments.

Siemens Healthineers

Siemens Healthineers brings decades of imaging heritage into the Asia-Pacific echocardiography arena. The company’s platforms are renowned for high-end image quality and integration with hospital IT systems. By facilitating advanced analytics and remote interpretive workflows in metropolitan and rural centers alike, Siemens supports scalable cardiology services. Their combined legacy of innovation and digital enhancement continues to expand their influence across diverse healthcare ecosystems.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Top echocardiography providers in Asia-Pacific pursue a mix of AI-driven innovation, portability, and localized deployment strategies. GE advances accessibility through FDA-approved portable units; Philips integrates AI to assist real-time diagnostic workflows, reducing dependence on specialized clinicians; and Siemens adopts partnerships to enhance image analysis capabilities. These firms also localize, investing in training, service networks, and distribution tailored to regional needs. Another key strategy is product segmentation: offering both high-end cart systems for tertiary hospitals and cost-effective handheld units for primary care clinics. Together, these strategic moves, innovation, localization, and tiered product offerings enable these players to address cost, competency, and access barriers, ensuring sustained leadership in a dynamic market landscape.

COMPETITION OVERVIEW

Competition in the Asia-Pacific echocardiography market blends historical incumbents with emerging digital challengers. GE, Philips, and Siemens anchor the industry through trusted full-featured systems, regional infrastructure, and global R&D. Their competition centers not just on price or imaging capacity, but also on AI capabilities, portability, and service reliability. Increasingly, mid-sized players and local manufacturers are entering with affordable handheld devices tailored to frontier clinics. Differentiation now hinges on AI integration, system versatility, and regional partnerships. With Asia-Pacific adopting telehealth and point-of-care paradigms, the competitive battleground is shifting from hardware to smart diagnostics and scalable service models.

RECENT MARKET DEVELOPMENTS

- In June 2023, GE Healthcare introduced an FDA-approved portable echocardiography device in the Asia-Pacific market. This innovation is anticipated to broaden the point-of-care cardiac diagnostic reach in remote regions.

- In January 2023, Philips Healthcare launched an AI-powered echocardiography system. This move is expected to enhance real-time diagnostics and operator support across the Asia-Pacific echocardiography market.

- In October 2023, Siemens Healthineers partnered with a leading AI company to improve image analysis for echocardiography. This collaboration is aimed at strengthening diagnostic accuracy in Asia-Pacific cardiovascular care.

- In 2022, Philips expanded its AI-enhanced handheld ultrasound portfolio across Asia-Pacific. This expansion supports increased diagnostic accessibility in decentralized clinical settings.

- In 2021, GE Healthcare augmented its regional training programs for echocardiography operators across Southeast Asia. This initiative is designed to boost system adoption and optimize diagnostic efficiency.

MARKET SEGMENTATION

This research report on the global echocardiography market has been segmented and sub-segmented based on type, product, application, end-user & region.

By Device Type

- Cart Based

- Handheld

By Test Type

- Transthoracic Echocardiography

- Transesophageal Echocardiography

- Stress Echocardiography

- Others

By Technology

- 2D

- 3D & 4D

- Doppler Imaging

By End-user

- Hospitals & ASCs

- Diagnostic Center

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Middle East Africa

- Latin America

Frequently Asked Questions

1. What is the Echocardiography Market?

The Echocardiography Market involves the sale and use of ultrasound imaging systems and related devices for non-invasive visualization and diagnosis of cardiac structure and function in hospitals, clinics, and research centers worldwide

2. Who are the leading companies in the Echocardiography Market?

Major vendors include GE Healthcare, Philips Healthcare, Siemens Healthineers, Canon Medical Systems, Mindray, Fujifilm Sonosite, Samsung Medison, Esaote, Hitachi, and more

3. What drives the growth of the Echocardiography Market?

Key drivers are the rising prevalence of cardiovascular diseases, aging populations, demand for non-invasive diagnostics, efficiency and accuracy of echo, and technology advancements in imaging and AI integration

4. What echocardiography test types are most popular in the market?

Transthoracic echocardiograms are the most commonly performed, followed by transesophageal, stress, and emerging intracardiac echocardiograms

5. How is AI transforming the Echocardiography Market?

AI-powered echo systems support automated image analysis, improved lesion detection, time savings for clinicians, and integration with digital health records and telemedicine

6. What role do portable and handheld echocardiography devices play in the market?

Portable and handheld echo devices are increasing accessibility in emergency, rural, and point-of-care settings, driving broader adoption and innovation

7. How is the echocardiography market segmented by technology?

Technologies include 2D, 3D/4D, Doppler imaging, color-flow imaging, and multi-slice real-time echo, each offering various benefits for clinical applications

8. Which age groups and patient demographics are most impacted in the Echocardiography Market?

Adults and geriatric populations dominate, but the market also includes neonatal, pediatric, and high-risk cardiac patients, especially in specialty centers

9. What trends are shaping the future of the Echocardiography Market?

Trends include the expansion of tele-echocardiography, cloud-based reporting, greater prevalence of AI and 3D imaging, portable device launches, and hybrid diagnostic platforms

10. What are the major challenges in the Echocardiography Market?

Challenges include reimbursement and regulatory complexity, adoption barriers in low-resource areas, device cost, and the need for skilled operators

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com