Global Diagnostic Imaging Market Size, Share, Trends & Growth Forecast Report By Type (X-Ray, Nuclear Medicine, Ultrasound, MRI, Tomography, Photoacoustic Imaging, Thermography, Tactile Imaging, Elastography, Functional Near-Infrared Spectroscopy and Echocardiography), Application and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2024 to 2033

Global Diagnostic Imaging Market Size

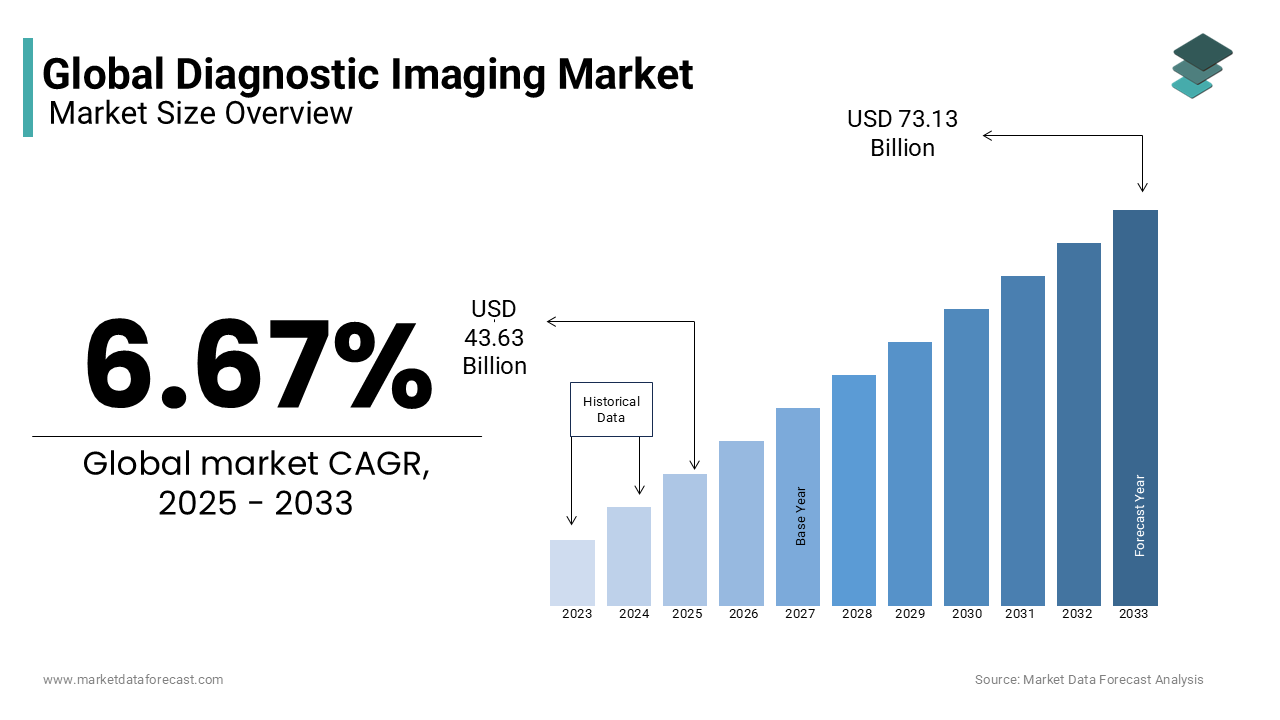

The global diagnostic imaging market is estimated to grow from USD 40.9 billion in 2024 to USD 73.13 billion in 2033, representing a CAGR of 6.67%.

The Diagnostic Imaging is designed to visualize the internal structures of the human body for clinical analysis and medical intervention. This domain includes modalities such as magnetic resonance imaging (MRI), computed tomography (CT), ultrasound, X-ray, and nuclear imaging techniques like positron emission tomography (PET). These tools are indispensable in early disease detection, treatment planning, and monitoring patient outcomes across diverse medical specialties. The integration of digital imaging with hospital information systems has elevated diagnostic precision and workflow efficiency. As per the World Health Organization, over 3.6 billion imaging examinations are conducted globally each year with the centrality of diagnostic imaging in modern healthcare delivery

MARKET DRIVERS

Increasing Prevalence of Chronic Diseases Driving Diagnostic Imaging Demand

The escalating global burden of chronic diseases is driving the growth of the Diagnostic Imaging Market. Cardiovascular disorders, cancer, and neurodegenerative conditions such as Alzheimer’s disease require precise, non-invasive visualization tools for accurate diagnosis and ongoing management. According to the World Health Organization, non-communicable diseases account for 74% of all deaths worldwide, with cardiovascular diseases alone responsible for approximately 17.9 million fatalities annually. Cancer incidence is also surging, with the International Agency for Research on Cancer projecting over 20 million new cases globally each year, necessitating advanced imaging for tumor localization, staging, and treatment monitoring. Hospitals and diagnostic centers are expanding imaging capacity to meet this clinical necessity, with MRI and CT scanners becoming standard in tertiary care facilities.

Technological Advancements Enhancing Imaging Precision and Accessibility

The rapid technological innovation within diagnostic imaging systems is additionally fuelling the growth of the Diagnostic Imaging Market. Modern imaging platforms are increasingly characterized by higher resolution, reduced scan times, and enhanced safety profiles, directly influencing their adoption across healthcare settings. As per the American College of Radiology, over 85% of accredited imaging centers in the U.S. now utilize advanced multi-slice CT technology. Similarly, 3 Tesla MRI systems, offering superior soft-tissue contrast, are being deployed at an accelerating pace; the European Society of Radiology notes that high-field MRI units constitute nearly 60% of new installations in Western Europe

MARKET RESTRAINTS

High Acquisition and Maintenance Costs Constraining Market Expansion

The substantial capital and operational expenditures with resource-limited healthcare systems is restricting the growth of the Diagnostic Imaging Market. In addition to purchase price, ongoing maintenance contracts typically range from 10% to 15% of the initial cost annually, amounting to over $200,000 per year for high-end systems. In low- and middle-income countries, these financial hurdles are even more pronounced. According to the World Health Organization, over 70% of medical imaging devices in sub-Saharan Africa are either obsolete or non-functional due to lack of spare parts and technical expertise. Moreover, the need for continuous staff training and regulatory compliance increases the total cost of ownership.

Regulatory and Radiation Safety Compliance Burdens

Stringent regulatory requirements and growing concerns over ionizing radiation exposure impose significant operational constraints on the deployment and utilization of diagnostic imaging technologies. Modalities such as CT and fluoroscopy involve ionizing radiation, which, when improperly administered, can elevate long-term cancer risks. As per the National Council on Radiation Protection and Measurements, medical imaging accounted for nearly 50% of the total radiation exposure to the U.S. population in 2021, up from just 15% in the early 1980s. In response, regulatory bodies have intensified oversight. Compliance with these standards demands additional staffing, software integration, and quality assurance procedures, increasing administrative and financial burdens.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Image Interpretation

The incorporation of artificial intelligence to enhance accuracy, efficiency, and accessibility of radiological services is substantially to elevate the growth of the Diagnostic Imaging Market. AI-powered algorithms are increasingly capable of detecting abnormalities in medical images with performance levels rivaling or surpassing human radiologists in specific tasks. AI tools can reduce radiologist workload by prioritizing critical cases, with studies from the Mayo Clinic indicating that AI triage systems decrease time-to-diagnosis for acute stroke by up to 30%. Furthermore, AI is facilitating quantitative imaging biomarkers by enabling objective monitoring of disease progression in oncology and neurology. The European Imaging Cancer Care Consortium is leveraging AI to standardize tumor response assessment across 20+ institutions, enhancing clinical trial reliability.

Expansion of Point-of-Care and Portable Imaging Solutions

The emergence of point-of-care and portable imaging technologies access to diagnostic services in non-traditional and underserved settings is additionally surging the growth of the Diagnostic Imaging Market. These compact, often handheld devices are redefining where and how imaging is performed, shifting capabilities from centralized radiology departments to emergency rooms, intensive care units, and remote clinics. The Butterfly iQ+ ultrasound device, for instance, combines a single-probe system with smartphone integration, enabling clinicians to perform cardiac, abdominal, and musculoskeletal assessments at the bedside.

MARKET CHALLENGES

Workforce Shortages in Radiology and Technical Expertise

The global deficit of trained radiologists and technical personnel capable of operating and interpreting advanced imaging systems is limiting the growth of the Diagnostic Imaging Market. According to the World Health Organization, there is a shortfall of over 4.3 million healthcare workers globally, with radiology among the most affected specialties. Even in developed countries, workforce strain is evident; the American College of Radiology projects a deficit of up to 8,500 radiologists in the United States by 2030 due to retirements and increasing service demands. The situation is exacerbated by the complexity of modern imaging modalities, which require specialized training in MRI safety, contrast protocols, and advanced reconstruction techniques. Moreover, the rapid integration of AI tools introduces new competencies, necessitating continuous education in data interpretation and algorithm validation. In rural and remote areas, the scarcity of on-site specialists forces reliance on teleradiology, yet bandwidth limitations and data privacy concerns hinder seamless implementation.

Data Management and Interoperability Challenges in Imaging Systems

The exponential growth in medical imaging data is creating formidable challenges in storage, integration, and interoperability across healthcare ecosystems. A single high-resolution MRI study can generate up to 1 gigabyte of data, and with over 500 million MRI and CT scans performed annually worldwide as per the International Atomic Energy Agency, the cumulative data burden is overwhelming institutional IT infrastructures. Hospitals are increasingly adopting Picture Archiving and Communication Systems (PACS), yet legacy systems often lack compatibility with electronic health records (EHRs), impeding seamless data exchange. The Office of the National Coordinator for Health Information Technology in the United States reports that only 55% of hospitals have achieved full interoperability between imaging systems and EHRs, leading to fragmented patient records and redundant testing. Additionally, the proliferation of AI-driven analytics demands standardized data formats like DICOM and structured reporting, which are inconsistently implemented. The Radiological Society of North America’s 2023 survey revealed that 68% of radiology departments face difficulties in aggregating imaging data for research and quality improvement initiatives due to vendor-specific silos

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Type, Application and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Key Market Players | GE Healthcare, Siemens Healthcare, Toshiba Medical Systems Corporation, Hitachi Medical Corporation, Hologic Inc., and Fujifilm Shimadzu Corporation |

SEGMENTAL ANALYSIS

By Type Insights

The X-ray segment was the largest and held 38.2% of the Diagnostic Imaging Market share in 2024 with its ubiquity, cost-effectiveness, and foundational role in initial clinical assessments across acute and chronic conditions. The sheer volume of X-ray utilization dwarfs other imaging techniques, with over 2.5 billion radiographic examinations conducted annually worldwide, according to the World Health Organization. According to the U.S. Centers for Disease Control and Prevention, chest X-rays alone account for nearly 40% of all radiological procedures in outpatient settings for pneumonia, tuberculosis, and trauma evaluation. Furthermore, digital radiography (DR) systems, which now represent over 70% of new X-ray installations in Europe as per the European Society of Radiology, have enhanced image quality and reduced radiation exposure, revitalizing the modality’s relevance. The integration of AI-driven software for automated fracture detection and lung nodule identification has further extended X-ray’s utility by ensuring its continued primacy despite the rise of advanced alternatives.

The functional near-infrared spectroscopy (fNIRS) segment is lucratively growing with an expected CAGR of 13.6% in the next coming years with its unique ability to monitor cerebral hemodynamics non-invasively by making it particularly valuable in neuroscience and neonatal care. The Children’s Hospital of Philadelphia has implemented fNIRS in neonatal intensive care units to assess oxygenation in preterm infants, reducing the need for repeated MRI scans that require sedation. As per the National Institutes of Health, over 60 clinical trials involving fNIRS were registered between 2020 and 2023, focusing on stroke recovery, autism spectrum disorder, and psychiatric conditions.

By Application Insights

The oncology segment was the largest by occupying 32.2% of the diagnostic imaging market share in 2024 with the indispensable role of imaging in every phase of cancer care from early detection and staging to treatment planning and recurrence monitoring. In oncology, modalities such as PET-CT, MRI, and contrast-enhanced ultrasound are routinely employed, with PET scans alone accounting for more than 2.3 million procedures annually in the United States, according to the Society of Nuclear Medicine and Molecular Imaging. Similarly, low-dose CT lung cancer screening for high-risk individuals recommended by the U.S. Preventive Services Task Force has led to a 20% increase in early-stage lung cancer detection, as demonstrated in the National Lung Screening Trial. The integration of radiomics and AI in tumor characterization has further promoted imaging’s centrality in precision oncology. For instance, the European Organisation for Research and Treatment of Cancer utilizes MRI-based texture analysis to predict treatment response in glioblastoma patients.

The neurology segment is likely to grow at an expected CAGR of 12.8% during the forecast period with the rising prevalence of neurological disorders and the increasing reliance on imaging for early and accurate diagnosis. Stroke alone causes one in six deaths worldwide, as per the World Stroke Organization, necessitating immediate neuroimaging for thrombolytic decision-making. CT and MRI are now standard in acute stroke pathways, with the American Heart Association stating that over 90% of stroke patients in certified stroke centers undergo brain imaging within 25 minutes of arrival. In neurodegenerative diseases, amyloid PET and tau PET imaging have revolutionized Alzheimer’s diagnosis, allowing clinicians to detect pathological changes up to two decades before symptom onset. The FDA-approved amyloid PET tracer florbetapir is used in over 150,000 scans annually in the U.S., facilitating early intervention and clinical trial enrollment. Additionally, advanced MRI techniques such as diffusion tensor imaging (DTI) and functional MRI (fMRI) are being used to map neural networks in traumatic brain injury and multiple sclerosis.

REGIONAL ANALYSIS

North America was the top performer in the global diagnostic imaging market with 37.2% of the share in 2024 with a highly developed healthcare infrastructure, robust reimbursement mechanisms, and early adoption of advanced imaging technologies. Medicare and private insurers cover a broad spectrum of diagnostic procedures by enabling widespread access. According to the Centers for Medicare & Medicaid Services, over 45 million imaging claims in 2022 alone. Moreover, the integration of AI into radiology workflows is most advanced in this region, with institutions like Massachusetts General Hospital deploying AI algorithms for automated lung nodule detection and cardiac risk stratification.

Europe was ranked second by accounting for 28.3% of the diagnostic imaging market share in 2024. Germany, France, and the United Kingdom lead in scanner density, with Germany alone operating over 1,800 MRI units and 2,500 CT scanners, as reported by the Organisation for Economic Co-operation and Development. According to the European Society of Radiology, over 90% of public hospitals in Western Europe are equipped with digital imaging and PACS integration by ensuring seamless data flow. The implementation of the EU’s Medical Device Regulation (MDR) in 2021 has elevated safety and performance benchmarks, which is compelling manufacturers to enhance device transparency and clinical validation. Additionally, cross-border initiatives like the European Imaging Infrastructure (EURO-IMI) are fostering data sharing and AI development in radiology. Sweden and the Netherlands have pioneered national teleradiology networks by reducing diagnostic delays in rural areas.

The Asia-Pacific (APAC) diagnostic imaging market growth is anticipated to grow with prominent CAGR in the next coming years owing to the rising healthcare expenditure, expanding insurance coverage, and government-led modernization of medical infrastructure, countries like China, India, and Japan are accelerating imaging adoption. China operates over 10,000 CT and 20,000 X-ray units, with the National Health Commission planning to install 50,000 additional imaging devices by 2025 under its Healthy China 2030 initiative. India is witnessing a surge in private diagnostic chains such as Dr. Lal PathLabs and Metropolis, which have collectively installed over 1,200 new imaging units since 2020, as reported by the Confederation of Indian Industry. Japan maintains one of the highest MRI densities globally, with 60 MRI units per million people, according to the OECD, supporting its advanced geriatric care system.

Latin America diagnostic imaging market growth is likely to grow with Brazil and Mexico serving as primary growth engines. Private healthcare providers like Grupo Diagnósticos da América have expanded imaging networks across seven countries, performing over 10 million scans annually. Additionally, mobile imaging units are being deployed in rural areas to combat geographic inequities.

The Middle East and Africa (MEA) diagnostic imaging market growth is growing steadily in the coming years. Countries like Saudi Arabia and the United Arab Emirates are investing heavily in healthcare modernization under economic diversification agendas such as Saudi Vision 2030. The UAE operates one of the highest imaging device densities in the region, with 35 CT scanners per million people, according to the Dubai Health Authority. South Africa, despite disparities, performs over 2 million imaging procedures annually, as reported by the Health Professions Council of South Africa. Mobile imaging vans and AI-assisted teleradiology are gaining traction, supported by initiatives from the African Society of Radiology.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Some of the notable companies dominating the global diagnostic imaging market profiled in this report are GE Healthcare, Siemens Healthcare, Toshiba Medical Systems Corporation, Hitachi Medical Corporation, Hologic Inc., and Fujifilm Shimadzu Corporation.

The competitive landscape of the diagnostic imaging market is characterized by intense technological rivalry, strategic consolidation, and rapid innovation. Dominated by established multinational corporations, the market also sees growing influence from regional players and AI-focused startups disrupting traditional imaging workflows. Companies are increasingly shifting from hardware-centric models to integrated solutions that combine advanced imaging systems with AI analytics, cloud connectivity, and lifecycle management services. Differentiation is achieved through superior image resolution, reduced scan times, lower radiation exposure, and enhanced user experience. Geopolitical and economic factors influence regional competition, with local manufacturers in China and India gaining traction through cost-effective alternatives. Regulatory compliance in radiation safety and data privacy, shapes product development timelines and market entry strategies. The expansion of teleradiology and mobile imaging has intensified competition beyond hospital settings, reaching outpatient clinics and rural health centers. Strategic collaborations between imaging vendors and healthcare providers are fostering co-innovation, especially in oncology and neurology applications

Top Players in the Diagnostic Imaging Market

GE HealthCare has maintained a pivotal role in shaping the diagnostic imaging landscape across the Asia Pacific region through its deep integration of advanced technology and localized healthcare solutions. The company has consistently introduced region-specific innovations, such as portable ultrasound systems tailored for rural clinics in India and AI-powered CT platforms deployed in major hospitals in China. In 2023, GE HealthCare launched the Revolution Apex CT scanner in Japan, engineered for high-speed cardiac imaging, reinforcing its focus on precision and efficiency. The company has also expanded its service footprint through digital platforms like AssetPlus, which enables remote monitoring and predictive maintenance of imaging equipment. Collaborations with government health programs in Indonesia and Vietnam have strengthened its public-sector penetration.

Siemens Healthineers has emerged as a transformative force in the Asia Pacific diagnostic imaging market by driving digitalization and precision medicine. The company has deployed its teamplay digital health platform across hospitals in South Korea, Australia, and Thailand, enabling seamless integration of imaging data into clinical workflows. In 2023, Siemens launched the Magnetom Free.Max, a 0.55 Tesla MRI system, in India and Malaysia by offering a cost-effective, low-maintenance alternative ideal for decentralized healthcare settings. The company has also introduced AI-powered tools like AI-Rad Companion in oncology and neurology applications, enhancing diagnostic confidence in major medical centers across Japan and Taiwan. Siemens Healthineers has strengthened its presence through collaborations with local manufacturers and government initiatives, including participation in India’s National Health Mission. The company established a regional innovation hub in Bangalore to accelerate R&D focused on tropical diseases and population-specific imaging needs. Additionally, its training programs for radiographers and technicians in the Philippines and Indonesia have addressed workforce gaps.

Philips has its influence in the Asia Pacific diagnostic imaging market through a patient-centric, value-based approach that emphasizes accessibility and sustainability. The company has introduced compact, AI-integrated systems such as the BlueSeal MRI, which uses minimal helium and is suited for hospitals with limited infrastructure in countries like Thailand and Vietnam. In 2023, Philips launched the EPIQ Elite ultrasound platform in Australia and South Korea, featuring advanced cardiac imaging capabilities and AI-driven workflow optimization. The company has also expanded its Tele-Radiology Services in India, supporting rural clinics with remote diagnostic expertise. Philips has partnered with public health authorities in Indonesia and Malaysia to modernize radiology departments under national digital health initiatives. Its Image Guided Therapy suite has been adopted in leading cardiac centers across Singapore and Japan, enhancing minimally invasive procedures.

Top Strategies Used by the Key Market Participants

Key players in the diagnostic imaging market are deploying multifaceted strategies to consolidate their competitive edge. Product innovation remains central, with companies investing heavily in AI integration, dose reduction, and portable imaging technologies. Strategic partnerships with hospitals, research institutions, and governments enable localized solution development and regulatory alignment. Geographic expansion into emerging economies in Asia Pacific and Latin America, is pursued through joint ventures and localized manufacturing. Mergers and acquisitions are leveraged to acquire niche technologies, especially in AI and software analytics. Companies are also focusing on service-led models, offering predictive maintenance, training, and managed equipment services to increase customer lifetime value. Sustainability initiatives, including energy-efficient systems and reduced rare material usage, align with global ESG trends. Educational outreach and radiologist training programs strengthen professional engagement and brand loyalty.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, GE HealthCare launched the Revolution Apex CT scanner in Japan, a high-performance system designed for ultra-fast cardiac and stroke imaging by enhancing diagnostic precision in care settings and expanding its footprint in advanced imaging solutions across Asia Pacific.

- In May 2023, Siemens Healthineers introduced the Magnetom Free.Max MRI system in India and Malaysia, a low-field, helium-free scanner that reduces operational costs and infrastructure demands by making high-quality MRI accessible to secondary and rural healthcare facilities.

- In September 2023, Philips partnered with the Indonesian Ministry of Health to modernize radiology infrastructure in 50 public hospitals, deploying AI-enabled ultrasound and digital X-ray systems, which is significantly improving diagnostic capabilities in underserved regions.

- In February 2024, Canon Medical Systems received FDA clearance for its Advanced intelligent Clear-IQ Engine (AiCE) 3D deep learning reconstruction technology on its Aquilion CT scanners by enhancing image quality while reducing radiation dose with its technological advancements in precision imaging.

- In June 2024, Fujifilm Healthcare acquired Hitachi’s diagnostic imaging business, integrating its ultrasound and CT portfolios to create a more competitive, full-service imaging division by enabling broader market reach and accelerated innovation in the Asia Pacific region.

MARKET SEGMENTATION

This market research report on the global diagnostic imaging market has been segmented and sub-segmented based on the type, application, and region.

By Type

- X-Rays

- Portable

- Handheld

- Nuclear Medicine

- Scintigraphy

- PET Imaging

- SPECT Imaging

- Ultrasound

- 2D

- 3D

- 4D

- Doppler Imaging

- MRI

- Tomography

- Photoacoustic Imaging

- Thermography

- Tactile Imaging

- Elastography

- Functional Near-Infrared Spectroscopy

- Echocardiography

By Application

- Cardiology

- Oncology

- Neurology

- Orthopedics

- Gastroenterology

- Gynecology

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What was the size of the diagnostic/medical Imaging market worldwide in 2025?

The global diagnostic/medical Imaging market size was valued at USD 43.63 billion in 2025.

Which region is growing the fastest in the diagnostic/medical Imaging market ?

Geographically, the North American diagnostic/medical Imaging market accounted for the largest share of the global market in 2023.

At What CAGR, the global diagnostic/medical Imaging market is expected to grow from 2025 to 2033?

The diagnostic/medical Imaging market is estimated to grow at a CAGR of 6.67% from 2025 to 2033.

Does this report include the impact of COVID-19 on the diagnostic/medical Imaging market?

Yes, we have studied and included the COVID-19 impact on the global diagnostic/medical Imaging market in this report.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com