Global Electric Two-Wheeler Market Size, Share, Trends & Growth Forecast Report – Segmented By Vehicle Type (Electric Scooter/Moped, Electric Motorcycle), Battery Type, Voltage Type, Peak Power, And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Global Electric Two-Wheeler Market Size

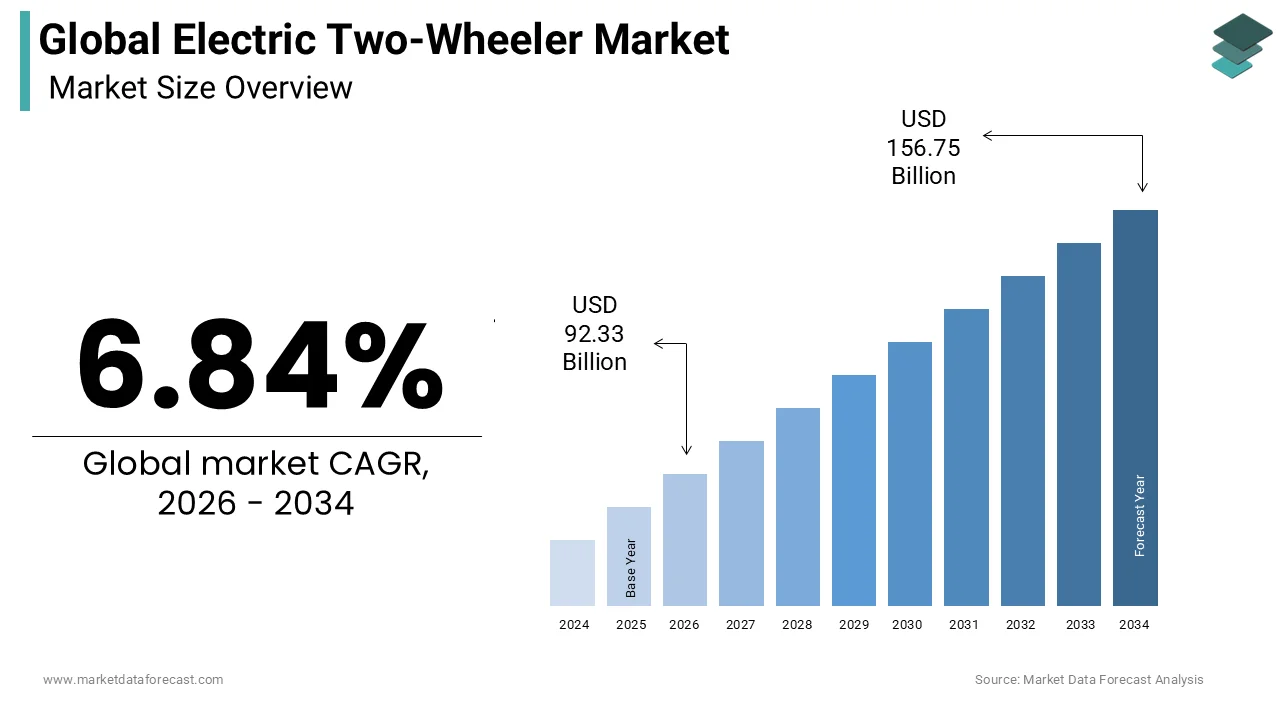

The global electric two-wheeler market size was calculated at USD 86.42 billion in 2025 and is anticipated to reach USD 156.75 billion by 2034, from USD 92.33 billion in 2026, growing at a CAGR of 6.84% during the forecast period.

An Electric Two-Wheeler (E2W) is a personal vehicle powered by an electric motor and a rechargeable battery instead of a traditional petrol engine. These vehicles utilize electric motors powered by rechargeable lithium-ion or lead acid batteries to deliver zero-emission transportation solutions that align with global sustainability goals. The segment has gained significant traction due to rising fuel costs and increasing environmental awareness among consumers, particularly in densely populated regions where traffic congestion and air quality are critical concerns. According to the International Energy Agency, global sales of electric two- and three-wheelers reached 10 million units, making up approximately 15% of the total market share. In Europe, the adoption rate is accelerating as cities implement low-emission zones and promote active mobility infrastructure. As per Eurostat data, more than 75% of the European Union population resides in urban areas (cities, towns, and suburbs), providing a massive addressable market for agile electric vehicles. The integration of smart connectivity features, such as mobile app integration and over-the-air updates, further enhances user experience and vehicle management capabilities. Governments across various jurisdictions are introducing subsidies and tax incentives to lower the upfront cost barrier for buyers. This regulatory support, combined with technological advancements in battery energy density and charging speed, is reshaping the competitive landscape. Manufacturers are increasingly focusing on modular designs and swappable battery systems to address range anxiety and improve convenience for daily commuters, thereby establishing electric two-wheelers as a cornerstone of future urban mobility ecosystems.

MARKET DRIVERS

Stringent Environmental Regulations Drive Adoption of Zero-Emission Vehicles

Governments worldwide are implementing rigorous emission standards and urban access restrictions that compel consumers and fleet operators to transition from fossil fuel-powered two-wheelers to electric alternatives, which boosts the growth of the electric two-wheeler market. Policies such as the European Green Deal aim to reduce greenhouse gas emissions by at least 55 percent by 2030 compared to 1990 levels, which directly impacts the automotive sector, including two-wheeler manufacturers. According to the European Environment Agency, transport accounts for approximately 25 percent of total greenhouse gas emissions in the European Union, prompting strict regulatory measures to curb pollution from internal combustion engines. Many major cities, including Paris, London, and Madrid, have established low-emission zones where high-polluting vehicles face hefty fines or outright bans, thereby creating a favorable environment for electric two-wheelers. As per data from the International Council on Clean Transportation, over 30 cities globally have announced plans to phase out internal combustion engine vehicles within the next decade. These regulatory frameworks not only discourage the purchase of traditional motorcycles but also provide financial incentives such as purchase subsidies and reduced registration fees for electric models. The cumulative effect of these policies is a significant shift in consumer preference toward cleaner mobility options. Manufacturers are responding by expanding their electric portfolios to comply with these mandates while capitalizing on government-supported demand. This regulatory push serves as a primary catalyst for market growth, ensuring that electric two-wheelers become an integral part of compliant urban transportation networks.

Rising Fuel Prices Enhance the Economic Viability of Electric Mobility

The volatility and sustained increase in gasoline and diesel prices significantly enhance the total cost of ownership advantage of E2Ws, which further propels the expansion of the electric two-wheeler market. This makes them an economically attractive option for daily commuters. As global energy markets face geopolitical tensions and supply chain disruptions, fuel costs have surged, placing a financial burden on users of conventional internal combustion engine vehicles. Studies show that consumer retail gasoline prices across multiple European nations frequently surpass 1.80 euros per liter, driving consumers toward more economical transport options. In contrast, electricity prices remain relatively stable, and the cost per kilometer for charging an electric two-wheeler is substantially lower than refueling a gasoline-powered counterpart. As per the European Commission, household electricity prices in the EU averaged around 0.28 euros per kilowatt hour,r which translates to minimal running expenses for electric vehicle users. This disparity in operational costs becomes particularly pronounced for high-mileage users such as delivery riders and daily commuters who rely on two-wheelers for their livelihood. The ability to charge at home using standard outlets further reduces dependency on public infrastructure and associated costs. Consequently, consumers are increasingly viewing electric two-wheelers as a prudent financial investment that offers long-term savings despite potentially higher upfront purchase prices. This economic incentive drives widespread adoption across various demographic segments, particularly in price-sensitive markets where operational efficiency is paramount.

MARKET RESTRAINTS

Limited Charging Infrastructure Hinders Convenience and Range Confidence

The insufficient deployment of public charging stations remains a critical restraint for the electric two-wheeler market. This lack of infrastructure limits widespread adoption, particularly for long-distance travel and users without private parking. Unlike four-wheeled electric vehicles, which benefit from growing fast charging networks, two-wheelers often rely on slower standard charging methods that require prolonged connection times. According to the European Alternative Fuels Observatory, the density of public charging points in many European regions remains inadequate to support the growing fleet of electric two-wheelers, especially in rural and suburban areas. As per data from the International Energy Agency, while urban centers are seeing improvements in infrastructure coverage, the peripheral regions lag significantly, creating range anxiety among potential buyers. The lack of standardized charging connectors and incompatible socket types further complicates the user experience, forcing riders to carry multiple adapters or rely solely on home charging. This limitation restricts the utility of electric two-wheelers for intercity travel and reduces their appeal to consumers who require flexible mobility options. Additionally, the time required to fully charge a battery can range from three to eight hours, depending on the charger capacity, which is impractical for users needing a quick turnaround during the day. Until a robust and universally accessible charging network is established, the perceived inconvenience will persist. Consequently, this will continue to deter a significant portion of the market from transitioning away from conventional fuel-based transportation solutions.

High Initial Purchase Cost Deters Price-Sensitive Consumers

The elevated upfront cost of E2Ws compared to their internal combustion engine equivalents is a significant barrier to entry for many consumers, which hampers the expansion of the electric two-wheeler market. This trend is particularly visible in price-sensitive markets. The high cost is primarily attributed to the expensive battery packs, which constitute a substantial portion of the total vehicle price. According to BloombergNEF, the average cost of lithium-ion battery packs has decreased over the years, but remains a significant component of electric vehicle manufacturing expenses, impacting final retail pricing. The European Association of Motorcycle Manufacturers (ACEM) highlights that up-front cost premiums for electric two-wheelers relative to combustion models can present barriers for budget-focused consumers. Although total cost of ownership calculations favor electric models due to lower running and maintenance costs, the initial capital outlay remains a decisive factor for many households. Government subsidies help mitigate this gap, but they are often temporary, subject to eligibility criteria, and vary significantly across regions, creating uncertainty for buyers. Furthermore, the perceived risk of battery degradation and replacement costs adds to the hesitation among consumers who are unfamiliar with electric vehicle technology. Financing options for electric two-wheelers are also less developed compared to traditional vehicles, limiting accessibility for those who cannot afford lump-sum payments. Until manufacturing efficiencies and economies of scale drive down production costs, high initial prices will continue to restrain mass market adoption. As a result, the penetration of electric two-wheelers will remain limited to early adopters and environmentally motivated segments.

MARKET OPPORTUNITIES

Expansion of Battery Swapping Networks Enhances Operational Efficiency

The development and deployment of battery swapping infrastructure offer a transformative opportunity for the electric two-wheeler market. This approach addresses charging time constraints and range limitations. Battery swapping allows users to exchange depleted batteries for fully charged ones at dedicated stations in a matter of minutes, thereby eliminating long waiting periods associated with plug-in charging. Research from the World Economic Forum shows that battery swapping reduces fleet downtime to minutes, saving over 90% of traditional charging time for delivery and ride-hailing services. As per the International Energy Agency, several Asian and European cities are piloting large-scale swapping networks that support interoperability between different vehicle brands through standardized battery designs. This model not only improves user convenience but also lowers the upfront cost of vehicles since batteries can be leased separately rather than purchased outright. Companies like Gogoro and Niu are leading this initiative by establishing extensive swapping station networks that cater to thousands of daily users. The scalability of this approach enables rapid expansion into dense urban areas where space for charging infrastructure is limited. Furthermore, battery swapping facilitates better grid management by allowing centralized charging during off-peak hours, reducing strain on electrical networks. As technology matures and standardization efforts gain momentum, battery swapping is poised to become a mainstream solution. It will accelerate electric two-wheeler adoption by offering a seamless and efficient energy replenishment experience for diverse user groups.

Integration of Smart Connectivity Features Creates New Revenue Streams

The incorporation of advanced connectivity and Internet of Things technologies into E2Ws opens new avenues for value-added services and enhanced user engagement, which is anticipated to accelerate the expansion of the electric two-wheeler market. Modern electric two-wheelers are increasingly equipped with telematics systems that enable real-time tracking, remote diagnostics, over-the-air software updates, and integration with smartphone applications. According to research, connected vehicle services are expected to generate billions in revenue globally as manufacturers shift from selling hardware to providing ongoing digital services. As per the European Telecommunications Standards Institute, the adoption of 5G technology will further enhance data transmission speeds, enabling more sophisticated features such as predictive maintenance, augmented reality navigation, and vehicle-to-infrastructure communication. These capabilities allow manufacturers to offer subscription-based services, including insurance packages, security alerts, and performance optimization tools that create recurring revenue streams. Additionally, connectivity enables fleet operators to monitor vehicle usage patterns, optimize routing, and improve asset utilization, leading to greater operational efficiency. The data collected from connected vehicles also provides valuable insights for product development and personalized marketing strategies. By leveraging smart connectivity, manufacturers can differentiate their offerings in a crowded market and build stronger relationships with customers through continuous digital interaction. This technological evolution transforms electric two-wheelers from simple transportation devices into intelligent mobility platforms that offer comprehensive solutions for modern urban living.

MARKET CHALLENGES

Safety Concerns Related to Battery Thermal Management Persist

Safety issues associated with lithium-ion batteries, particularly the risk of thermal runaway and fires, are a significant challenge to consumer confidence and growth in the electric two-wheeler market. High-profile incidents involving battery explosions have raised alarms among regulators and users, prompting stricter safety standards and testing protocols. According to the National Fire Protection Association, lithium-ion battery fires are difficult to extinguish and can release toxic gases, presenting serious hazards in residential and commercial settings. Manufacturers must invest heavily in advanced battery management systems that monitor temperature, voltage, and current in real time to prevent overheating and short circuits. However, balancing safety with cost and weight remains a complex engineering challenge, especially for affordable two-wheeler models. The lack of uniform global safety standards creates confusion for consumers and complicates compliance for manufacturers operating in multiple markets. Additionally, the disposal and recycling of damaged batteries require specialized facilities to prevent environmental contamination and fire risks. Apprehension regarding battery reliability continues to hinder widespread acceptance and slow down the transition to electric two-wheelers. This hesitation will persist until consistent safety performance is demonstrated and communicated effectively to the public.

Supply Chain Vulnerabilities for Critical Raw Materials

The dependence on scarce and geographically concentrated raw materials, such as lithium, cobalt, and nickel, for battery production creates significant supply chain vulnerabilities for the electric two-wheeler market. Geopolitical tensions, trade restrictions, and mining constraints in key producing regions can disrupt the availability of these essential components, leading to production delays and price volatility. The International Energy Agency projects that global lithium demand will multiply up to 15 times over the coming decades under aggressive net-zero scenarios. As per the United States Geological Survey, a few countries dominate the production of these critical minerals, making the supply chain susceptible to political instability and export controls. This concentration risk forces manufacturers to seek alternative sourcing strategies and invest in vertical integration, which requires substantial capital and long lead times. Additionally, ethical concerns regarding mining practices in certain regions add another layer of complexity, requiring companies to implement rigorous supply chain auditing and sustainability certifications. Fluctuations in raw material prices directly impact battery costs and consequently vehicle pricing, affecting competitiveness against internal combustion engine alternatives. Diversifying supply sources and developing alternative battery chemistries, such as sodium ion or solid-state technologies, are potential mitigation strategies, but these solutions are still in early stages of commercialization. The industry remains exposed to external shocks that can impede growth and stability. This vulnerability persists until a more resilient and diversified supply chain is established.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.84% |

| Segments Covered | By Vehicle Type, Battery Type, Voltage Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, the Middle East and Africa, And Latin America |

| Market Leaders Profiled | Tesla, Inc., BYD Company Ltd., Yadea Group Holdings Ltd., NIU Technologies, Gogoro Inc., Ather Energy, Hero MotoCorp Ltd., TVS Motor Company, Ola Electric Mobility Ltd., Vmoto Limited, Silence Urban Ecomobility, Energica Motor Company S.p.A., Zero Motorcycles, Horwin Global, Mahindra Last Mile Mobility Limited |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The electric scooter and moped segment was the largest in the global electric two-wheeler market and occupied a commanding share in 2025. This supremacy of the segment was supported by its suitability for short-distance urban commuting and last-mile connectivity. These vehicles offer a practical and cost-effective solution for navigating congested city streets where parking space is limited and traffic flow is slow. Sources confirm that lightweight electric scooters and mopeds dominate global two-wheeler sales because of their affordability and ease of use across a wide demographic. The compact design allows users to bypass traffic jams and utilize dedicated bike lanes, which are increasingly available in major metropolitan areas across Europe and Asia. Furthermore, the lower licensing requirements for low-speed mopeds in many jurisdictions make them accessible to younger riders and those without full motorcycle licenses. The integration of removable batteries enables users to charge at home or the office, eliminating the need for public charging infrastructure. This convenience factor, combined with lower maintenance costs compared to internal combustion engines, makes electric scooters the preferred choice for daily commuters. Manufacturers are continuously improving battery range and motor efficiency to meet the demands of urban mobility, thereby reinforcing the dominance of this segment in the global market landscape.

However, the electric motorcycle segment is projected to register the highest CAGR over the forecast period due to advancements in high-performance battery technology and increasing consumer interest in premium electric mobility. Unlike scooters, electric motorcycles offer superior power, torque, and handling characteristics that appeal to enthusiasts and long-distance riders seeking an exhilarating driving experience. Ongoing improvements in lithium-ion battery energy density have substantially increased the average range of electric motorcycles, making them increasingly viable for longer intercity travel. Major manufacturers such as Zero Motorcycles and Energica are launching models with ranges exceeding 200 kilometers on a single charge, addressing previous concerns about range anxiety. Studies show an upward trend in electric motorcycle adoption as enthusiast acceptance grows and more premium models hit the market. The development of fast charging networks capable of delivering an 80 percent charge in under 30 minutes further enhances the practicality of these vehicles for touring and recreational use. Additionally, government incentives for zero-emission vehicles often extend to higher-value motorcycles, encouraging adoption among affluent consumers. The aesthetic appeal and technological sophistication of electric motorcycles also attract a new generation of riders who prioritize sustainability without compromising on performance. Hence, this segment is poised for rapid expansion as technology matures and consumer perceptions shift toward electric performance machines.

By Battery Type Insights

The lithium-ion battery segment dominated the electric two-wheeler market and accounted for a substantial share in 2025. This dominance of the segment was driven by its high energy density, lightweight nature, and longer cycle life compared to alternative technologies. These attributes enable manufacturers to produce vehicles with greater range and better acceleration while keeping the overall weight manageable for agile handling. According to the Department of Energy, lithium-ion batteries offer an energy density of approximately 250 watt hours per kilogram, which is significantly higher than lead acid alternatives, allowing for compact battery packs that do not compromise vehicle design. As per data from the International Renewable Energy Agency, the cost of lithium-ion batteries has decreased by nearly 90 percent over the past decade, making them increasingly affordable for mass market electric two-wheelers. The ability to withstand thousands of charge-discharge cycles ensures longevity and reduces the total cost of ownership for consumers. Furthermore, lithium-ion batteries support fast charging capabilities, which are essential for commercial applications such as delivery services where downtime must be minimized. The widespread adoption of this technology by major automotive and electronics industries has created a robust supply chain that benefits electric two-wheeler manufacturers through economies of scale. Continuous research into solid-state and other advanced lithium chemistries promises even greater safety and performance improvements in the future. Therefore, the dominance of lithium-ion batteries is sustained by their unmatched combination of efficiency, durability, and decreasing cost structures.

By Voltage Type Insights

In 2025, the 48V to 60V voltage segment held the majority share of the electric two-wheeler market as it offers an optimal balance between performance cost and regulatory compliance for most urban commuting scenarios. This voltage range provides sufficient power for speeds up to 45 kilometers per hour, which aligns with legal limits for mopeds and light electric vehicles in many countries without requiring a full motorcycle license. Under European Union Regulation No 168/2013, light electric two-wheelers with small powertrains qualify for the L1e-B category, which benefits from simplified regional registration and licensing paths. As per data from the International Organization for Standardization, this voltage range allows for the use of standard industrial components and controllers, which are readily available and cost-effective to manufacture. The moderate voltage level also reduces the risk of electrical hazards, making it safer for everyday users and easier to maintain. Manufacturers can achieve adequate torque for hill climbing and acceleration while keeping battery pack sizes manageable for easy removal and charging. This segment appeals to a broad customer base, including students, office workers, and delivery personnel who require reliable and efficient transportation for daily tasks. The widespread availability of 48V and 60V chargers further supports this dominance by ensuring convenient charging options at home and workplaces. Consequently, this voltage range remains the industry standard for mass market electric scooters and mopeds, driving its continued leadership in the global market.

But the greater than 96V voltage segment is registering the fastest growth, owing to the rising demand for high-performance electric motorcycles capable of competing with internal combustion engine counterparts. Higher voltage systems enable the use of more powerful motors that deliver superior torque and top speeds, appealing to enthusiasts and professional riders. According to the Society of Automotive Engineers, voltage levels above 96V allow for more efficient power transmission with lower current requirements, reducing heat generation and improving overall system efficiency. These vehicles often feature advanced thermal management systems and sophisticated battery management software to handle the higher energy loads safely. The adoption of fast charging technologies is also more prevalent in this segment, as high-voltage architectures support rapid energy replenishment, minimizing downtime for long-distance travel. Regulatory changes in several regions are also expanding the definition of eligible electric motorcycles, allowing higher voltage models to access roads previously restricted to gasoline-powered bikes. This trend is further supported by the development of specialized charging infrastructure capable of handling high power outputs. Therefore, the greater than 96V segment is expanding rapidly as technology advances and consumer preferences shift toward high-performance electric mobility solutions.

REGIONAL ANALYSIS

Asia Pacific Electric Two-Wheeler Market Analysis

Asia Pacific led the global electric two-wheeler market and captured a significant share in 2025. This leading position of the segment was attributed to its vast manufacturing capabilities and high consumer adoption rates, particularly in China, India, and Southeast Asia. Driven by proactive government support and a demand for cleaner urban transport, the Asia Pacific region accounts for approximately 80% of global electric two- and three-wheeler sales. A study confirms that China remains the world's largest market for electric two-wheelers, recording nearly 7 million new sales units in recent years. India is also witnessing rapid growth with government initiatives like the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles scheme, providing substantial subsidies to buyers and manufacturers. As per data from the Asian Development Bank, urbanization rates in the region are increasing, leading to severe traffic congestion and air pollution, which electric two-wheelers help alleviate. The presence of major battery manufacturers in countries like Japan, South Korea, and China ensures a stable and cost-effective supply chain for critical components. Additionally, the popularity of food delivery and ride-hailing services has created a robust commercial demand for durable and efficient electric scooters. Local manufacturers are continuously innovating to produce affordable models tailored to regional preferences and road conditions. Thus, Asia Pacific remains the epicenter of electric two-wheeler activity, influencing global trends through scale innovation and aggressive policy interventions.

Europe Electric Two-Wheeler Market Analysis

Europe exhibits robust growth in the electric two-wheeler market, fueled by stringent environmental regulations and a cultural shift toward sustainable urban mobility. The European Union’s Green Deal and various national bans on internal combustion engines in city centers are accelerating the transition to electric alternatives. Studies show that the European electric two-wheeler sector is maintaining a strong compound annual growth rate, reflecting robust consumer demand for eco-friendly micromobility. Countries like France, Germany, and Italy are leading this trend with generous purchase incentives and investments in cycling infrastructure. Also, the Urban Access Regulations in Europe network shows hundreds of cities have implemented low-emission zones that restrict access for polluting vehicles, inherently boosting demand for electric scooters and mopeds. The region is also seeing a rise in shared mobility services that utilize electric two-wheelers for last-mile connectivity, enhancing their visibility and accessibility. Manufacturers are focusing on premium designs and smart connectivity features to appeal to discerning European consumers who value quality and technology. Additionally, the development of standardized charging networks across borders is improving convenience for cross-country travelers. Europe’s commitment to sustainability and urban livability ensures its continued importance in the global electric two-wheeler market, particularly for high-value and technologically advanced segments.

North America Electric Two-Wheeler Market Analysis

North America experiences steady expansion in the global electric two-wheeler market due to increasing environmental awareness and supportive state-level policies. The United States and Canada are seeing rising adoption of electric scooters and motorcycles, particularly in urban areas where traffic congestion is a major concern. Research shows that sales of electric two-wheelers in North America are growing rapidly as consumers increasingly look to replace passenger vehicles for short commutes. State governments in California, New York, and Washington are offering tax credits and rebates to encourage the purchase of zero-emission vehicles. As per data from the United States Department of Transportation, infrastructure investments are improving bike lanes and parking facilities, making electric two-wheelers a safer and more viable option. The presence of innovative startups and established automotive brands entering the electric two-wheeler space is expanding product choices and driving competition. Additionally, the gig economy has spurred demand for electric delivery vehicles among courier services looking to reduce operational costs. While adoption rates lag behind Asia and Europe, the market is gaining momentum as charging infrastructure expands, and consumer perceptions shift. North America’s focus on innovation and sustainability positions it for significant future growth in the electric two-wheeler sector.

Latin America Electric Two-Wheeler Market Analysis

Latin America is a promising region in the electric two-wheeler market, with potential for significant growth driven by economic factors and urbanization trends in countries like Brazil, Mexico, and Colombia. Rising fuel prices and traffic congestion in major cities are prompting consumers and businesses to consider electric alternatives for cost-effective mobility. According to the Economic Commission for Latin America and the Caribbean, the urban population in the region exceeds 80 percent, creating a large addressable market for compact electric vehicles. Governments are beginning to introduce incentives and pilot programs to promote electric mobility, although adoption is still in early stages compared to other regions. As per the Inter American Development Bank, infrastructure challenges remain, but investments in renewable energy and smart grid technologies are laying the groundwork for future expansion. Local assembly plants are being established to reduce costs and tailor products to regional needs, such as rugged terrain and varying road conditions. The delivery sector is also showing interest in electric scooters to improve efficiency and reduce emissions in dense urban centers. While financial constraints and limited charging infrastructure pose challenges, the long-term potential is significant as economic conditions improve and awareness grows. Latin America represents a frontier market with opportunities for manufacturers willing to invest in local partnerships and adaptive solutions.

Middle East and Africa Electric Two-Wheeler Market Analysis

The Middle East and Africa region is likely to expand notably in the electric two-wheeler market due to infrastructure development and economic diversification efforts. Countries such as South Africa, Morocco, and the United Arab Emirates are initiating projects to promote sustainable transport and reduce reliance on fossil fuels. According to the African Development Bank, industrialization and urbanization are driving demand for efficient mobility solutions, although the market remains small compared to other regions. Governments are exploring policies to support electric vehicle adoption, including tax exemptions and pilot projects for electric buses and two-wheelers. As per data from the Gulf Cooperation Council, countries are investing in smart city initiatives that include provisions for electric mobility infrastructure. The high temperatures in some parts of the region pose technical challenges for battery performance, requiring specialized thermal management solutions. However, the abundance of solar energy offers opportunities for sustainable charging solutions that align with regional renewable energy goals. Limited local manufacturing capabilities mean most vehicles are imported, keeping prices high, but international brands are beginning to explore local assembly options. As infrastructure improves and awareness increases, the Middle East and Africa present long-term opportunities for electric two-wheeler manufacturers seeking new growth markets.

COMPETITION OVERVIEW

The competition in the electric two-wheeler market is characterized by intense rivalry among established automotive manufacturers and innovative startups striving to capture the growing demand for sustainable urban mobility. Major players compete based on battery technology range, performance, and price positioning to attract diverse consumer segments. The shift toward electrification has lowered entry barriers, allowing new entrants to disrupt traditional markets with novel business models such as battery swapping and subscription services. Companies differentiate themselves through unique design aesthetics, smart connectivity features, and robust after-sales support networks. Strategic alliances with technology firms and energy providers are crucial for developing comprehensive ecosystems that address charging infrastructure gaps. Price wars are common in mass market segments, particularly in the Asia Pacific, where affordability drives purchasing decisions. Meanwhile, premium segments focus on performance and brand prestige to justify higher costs. Regulatory compliance and adherence to safety standards also play a significant role in competitive positioning as governments impose stricter norms. Ultimately, success depends on the ability to innovate continuously, optimize supply chains, and build strong brand loyalty in a rapidly evolving landscape where technological advancements occur frequently, and consumer preferences shift toward convenience and sustainability.

KEY MARKET PLAYERS

A few major players of the global electric two-wheeler market include

- Tesla, Inc

- BYD Company Ltd

- Yadea Group Holdings Ltd

- NIU Technologies

- Gogoro Inc

- Ather Energy

- Hero MotoCorp Ltd

- TVS Motor Company

- Ola Electric Mobility Ltd

- Vmoto Limited

- Silence Urban Ecomobility

- Energica Motor Company S.p.A

- Zero Motorcycles

- Horwin Global

- Mahindra Last Mile Mobility Limited

Top Strategies Used by the Key Market Participants

Key players in the electric two-wheeler market primarily focus on strategic partnerships and collaborations to expand charging infrastructure and enhance battery technology. Companies invest heavily in research and development to improve energy density and reduce charging times for a better user experience. Expansion into emerging markets through local manufacturing facilities helps reduce costs and comply with regional regulations effectively. Many firms are adopting direct-to-consumer sales models supplemented by digital platforms to streamline purchasing and service processes. Sustainability initiatives such as using recycled materials and establishing battery recycling programs are increasingly common to meet environmental standards. Product diversification, including high-performance motorcycles and affordable scooters, allows manufacturers to cater to varied consumer segments. Continuous innovation in smart connectivity features like mobile app integration and over-the-air updates enhances vehicle functionality and customer engagement significantly.

Leading Players in the Global Electric Two-Wheeler Market

- Yadea Group Holdings Limited stands as a global leader in the electric two-wheeler industry with a strong presence in both domestic and international markets. The company focuses on producing high-quality electric scooters and motorcycles that cater to diverse consumer needs, ranging from urban commuting to recreational riding. Recently, Yadea has intensified its research and development efforts to enhance battery efficiency and integrate smart connectivity features into its vehicles. They have expanded their manufacturing facilities in Europe and Southeast Asia to better serve regional demands and reduce logistics costs. This strategic geographic expansion allows Yadea to respond quickly to local market trends and regulatory requirements. By prioritizing innovation in motor technology and design aesthetics, Yadea continues to strengthen its brand reputation and customer loyalty globally. Simultaneously, it maintains a competitive edge through cost-effective production methods and robust distribution networks.

- Hero MotoCorp Ltd is a prominent player in the electric two-wheeler segment, leveraging its extensive experience in the internal combustion engine market to transition toward electrification. The company has launched several electric scooter models under its Vida brand, targeting urban consumers seeking sustainable mobility solutions. Hero MotoCorp has invested heavily in building a comprehensive charging infrastructure network across India to address range anxiety and improve user convenience. They have also partnered with technology firms to develop advanced battery management systems and digital platforms for vehicle monitoring. These initiatives demonstrate their commitment to creating an ecosystem that supports electric vehicle adoption beyond just manufacturing. Hero MotoCorp utilizes its vast dealer network and service centers to ensure widespread availability and after-sales support. Consequently, this widespread infrastructure strengthens their market position and accelerates consumer trust in their electric offerings.

- Gogoro Inc is a pioneer in the electric two-wheeler market, known for its innovative battery-swapping technology and smart scooter designs. The company operates an extensive network of swapping stations that allow users to exchange depleted batteries for fully charged ones in seconds, thereby eliminating long charging times. Gogoro has recently expanded its operations into new markets, including Europe and North America, through strategic partnerships with local distributors and energy providers. They continue to refine their artificial intelligence-driven platform, which optimizes battery usage and predicts maintenance needs for enhanced reliability. By focusing on sustainability and user experience, Gogoro attracts environmentally conscious consumers and commercial fleet operators. Their open platform approach encourages collaboration with other manufacturers to standardize battery formats, further solidifying their role as a key enabler of widespread electric two-wheeler adoption globally.

MARKET SEGMENTATION

This research report on the global electric two-wheeler market has been segmented and sub-segmented based on vehicle type, battery type, voltage type, peak power, and region.

By Vehicle Type Insights

- Electric Scooter/Moped

- Electric Motorcycle

By Battery Type Insights

- Lithium-Ion

- Sealed Lead Acid (SLA)

By Voltage Type Insights

- <48V

- 48-60V

- 61-72V

- 73-96V

- >96V

By Peak Power Insights

- <3 kW

- 3-6 kW

- 7-10 kW

- >10 kW

By Region

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

Frequently Asked Questions

1. What is driving the growth of the global electric two-wheeler market?

Growing environmental awareness, supportive government incentives, rising fuel prices, and advancements in battery technology are the major growth drivers.

2. Which type of electric two-wheeler dominates the market?

Electric scooters dominate the market due to their affordability, ease of use, and popularity for daily urban commuting.

3. Which battery technology is most commonly used in electric two-wheelers?

Lithium-ion batteries are the most widely used because they offer higher energy density, faster charging, and longer lifespan than lead-acid batteries.

4. Which region leads the global electric two-wheeler market?

The Asia-Pacific region leads the market, driven by high adoption in countries such as China, India, and Taiwan.

5. What are the main applications of electric two-wheelers?

They are primarily used for personal commuting, commercial deliveries, ride-sharing services, and fleet operations.

6. What factors are encouraging consumers to switch to electric two-wheelers?

Lower operating costs, reduced maintenance requirements, government subsidies, and zero tailpipe emissions encourage consumers to adopt electric two-wheelers.

7. What challenges does the electric two-wheeler market face?

Key challenges include limited charging infrastructure in some regions, battery replacement costs, range anxiety, and supply chain disruptions.

8. Which distribution channels are commonly used for electric two-wheelers?

Manufacturers sell through dealerships, exclusive brand stores, online platforms, and direct-to-consumer channels.

9. What technological trends are shaping the electric two-wheeler market?

Key trends include smart connectivity, IoT-enabled vehicle monitoring, AI-based battery management systems, regenerative braking, and improved battery performance.

10. What is the future outlook for the global electric two-wheeler market?

The market is expected to grow steadily over the coming years, supported by continuous technological innovation, expanding charging infrastructure, favorable government policies, and increasing consumer preference for sustainable transportation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com