Global ENT Devices Market Size, Share, Trends, COVID-19 Impact & Growth Analysis Report – Segmented By Product (Diagnostic Devices, Surgical Devices, Hearing Aids, Hearing Implants, Co2 Lasers, Image-Guided Surgery Systems), Devices, End-User & Region – Industry Analysis From 2026 to 2034

Global ENT Devices Market Report Summary

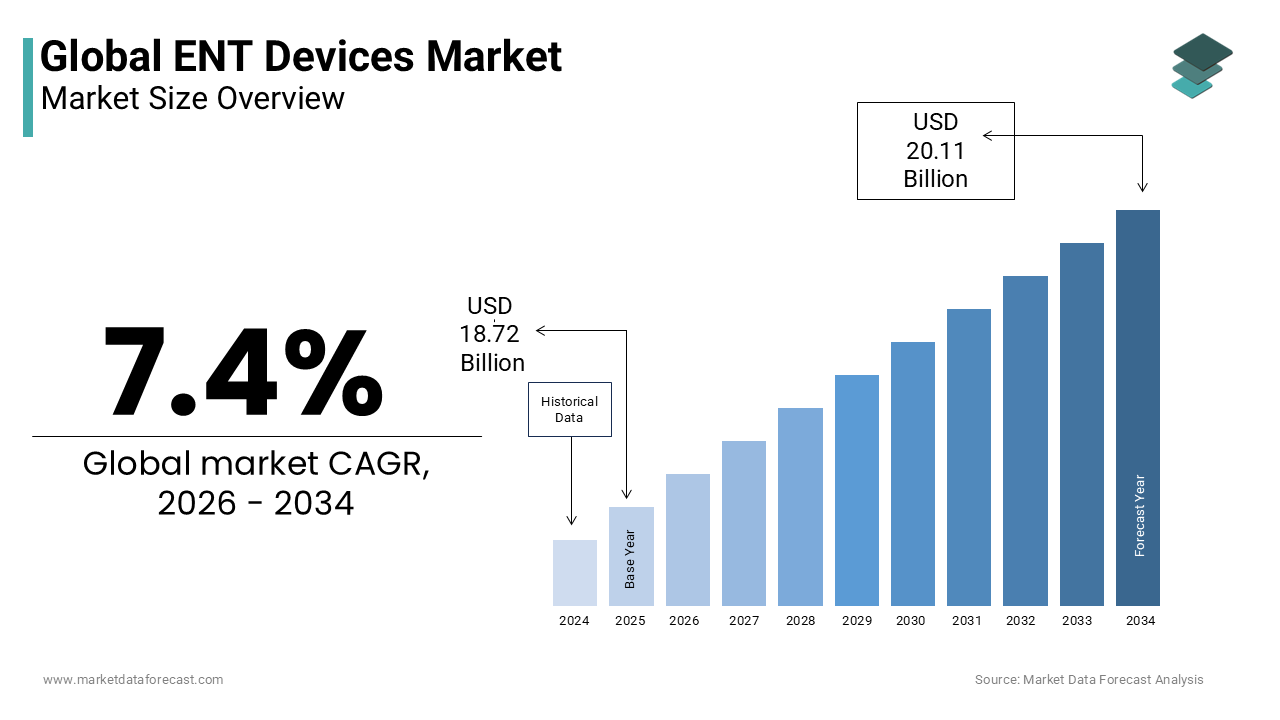

The global ENT devices market was valued at USD 18.72 billion in 2025 and is anticipated to reach USD 20.11 billion in 2026 from USD 35.60 billion by 2034, growing at a CAGR of 7.4% during the forecast period from 2026 to 2034. The growth of the global ENT devices market is driven by the increasing prevalence of hearing disorders, chronic respiratory diseases, and sinus-related conditions, coupled with the growing aging population worldwide. Rising demand for minimally invasive ENT procedures, expanding adoption of advanced diagnostic and surgical technologies, and increasing awareness regarding early diagnosis and treatment of ear, nose, and throat disorders are further accelerating market growth. Moreover, advancements in image-guided surgery systems, artificial intelligence-enabled diagnostic tools, robotic-assisted ENT procedures, and tele-audiology solutions are supporting the expansion of the global ENT devices market.

Key Market Trends

-

Rising adoption of minimally invasive endoscopic ENT procedures.

-

Increasing utilization of image-guided surgical navigation systems for complex ENT surgeries.

-

Growing demand for advanced digital hearing aids and implantable hearing devices.

-

Rising integration of artificial intelligence in ENT diagnostics and surgical planning.

-

Increasing expansion of tele-ENT services supported by portable diagnostic devices.

Segmental Insights

- Based on product, the hearing aids segment dominated the global ENT devices market and accounted for 32.3% of the market share in 2025. The dominance of the segment is attributed to the rising prevalence of age-related hearing loss, increasing awareness regarding hearing rehabilitation, growing availability of over-the-counter hearing aids, and continuous technological advancements including Bluetooth connectivity and AI-powered sound processing.

- The image-guided surgery systems segment is projected to witness the fastest CAGR of 9.5% during the forecast period owing to the increasing complexity of ENT surgeries, growing adoption of minimally invasive procedures, rising demand for surgical precision, and expanding reimbursement support for navigated surgical interventions.

- Based on device type, the endoscopes segment accounted for 60.6% of the global ENT devices market share in 2025. The growth of the segment is driven by increasing utilization in sinus surgery, laryngoscopy, otology procedures, early cancer detection, and routine ENT diagnostics. Advancements in high-definition imaging, 4K visualization, and narrow-band imaging technologies continue to strengthen segment demand.

- The hearing screening devices segment is anticipated to register the fastest CAGR of 8.4% during the forecast period due to expanding newborn hearing screening programs, increasing public health awareness regarding early hearing loss detection, growing adoption of portable wireless screening devices, and rising government initiatives supporting preventive healthcare.

- Based on end user, the hospitals and ambulatory settings segment dominated the global ENT devices market owing to the increasing number of ENT surgical procedures, growing adoption of advanced surgical technologies, expanding outpatient ENT care services, and rising investments in hospital infrastructure.

- The ENT clinics segment is expected to witness significant growth during the forecast period due to increasing patient preference for specialized ENT care, expanding private specialty clinics, growing availability of advanced diagnostic equipment, and rising demand for same-day minimally invasive ENT procedures.

Regional Insights

- North America dominated the global ENT devices market in 2025 and accounted for 39.1% of the global market share. The region's leadership is driven by advanced healthcare infrastructure, high prevalence of hearing impairment and chronic sinus disorders, strong reimbursement systems, and widespread adoption of innovative ENT diagnostic and surgical technologies. Continuous investments in medical research and rapid technological adoption further strengthen regional market growth.

- Europe held the second-largest share of the global ENT devices market owing to its aging population, strong public healthcare systems, increasing prevalence of hearing disorders, widespread implementation of newborn hearing screening programs, and growing adoption of minimally invasive ENT surgical procedures. Stringent regulatory standards continue to support high-quality device adoption across the region.

- Asia Pacific is projected to witness the fastest growth during the forecast period due to rapidly expanding healthcare infrastructure, increasing healthcare expenditure, rising awareness regarding ENT disorders, growing government investments in hospital modernization, and expanding access to advanced diagnostic and surgical technologies across China, India, Japan, and Southeast Asian countries.

- Latin America continues to maintain steady growth due to improving healthcare infrastructure, increasing ENT disease awareness, expanding private healthcare investments, and growing demand for advanced hearing care and minimally invasive surgical solutions.

- The Middle East & Africa is expected to experience notable growth during the forecast period owing to increasing healthcare modernization initiatives, rising investments in specialty hospitals, growing adoption of advanced diagnostic equipment, and expanding access to hearing healthcare services across emerging economies.

Competitive Landscape

The global ENT devices market is highly competitive and characterized by the presence of multinational medical device manufacturers and specialized ENT technology providers competing through technological innovation, product quality, clinical performance, and strategic partnerships. Leading companies are focusing on developing advanced hearing solutions, image-guided navigation systems, robotic-assisted surgical platforms, artificial intelligence-powered diagnostics, and minimally invasive ENT technologies. Strategic acquisitions, investments in research and development, expansion into emerging markets, and collaborations with healthcare institutions continue to strengthen market positioning across the global ENT devices industry. Growing emphasis on precision medicine, digital healthcare integration, and patient-centered care continues to intensify competition within the market. The key players operating in the global ENT devices market include Johnson & Johnson Services, Inc., Stryker Corporation, Zimmer Biomet Holdings, Inc., Orthofix Medical Inc., B. Braun Melsungen AG, Medtronic plc, NuVasive, Inc., Globus Medical, Inc., ATEC Spine, Inc., Captiva Spine, Inc., SeaSpine Holdings Corporation, Spinal Elements, Inc., Spine Wave, Inc., Spineology Inc., and Xtant Medical Holdings, Inc.

Global ENT Devices Market Size

The global ENT devices market was worth USD 18.72 billion in 2025. The global market is expected to reach USD 35.60 billion by 2034 from USD 20.11 billion in 2026, rising at a CAGR of 7.4% from 2026 to 2034.

ENT devices are designed to aid in the treatment and diagnostic procedures for the ears, nose and throat. An ENT specialist uses these devices to help the patient with different problems in these parts of the body. These instruments are regularly used in surgeries and treatment procedures such as aural forceps and nasal forceps. An otolaryngologist is a trained professional who is educated in the use of these devices and assists in the application. Some of the most common instruments in the ENT industry are the Nasal Speculum, Tongue depressor, Laryngeal mirrors and others.

ENT devices are a specialized array of diagnostic, surgical, and therapeutic instruments designed to address disorders of the ear, nose, and throat. This sector includes essential tools, such as otoscopes, endoscopes, laryngoscopes, hearing aids, and advanced surgical navigation systems that facilitate precise intervention in complex anatomical regions. The clinical necessity for these devices is underscored by the high global prevalence of sensory impairments and chronic respiratory conditions. According to the World Health Organization, over 5% of the world’s population, equivalent to 430 million people, suffer from disabling hearing loss, creating an enduring demand for diagnostic audiology equipment and rehabilitative technologies. As per data from the Centers for Disease Control and Prevention, the burden of chronic rhinosinusitis affects approximately 12% of the adult population in the United States alone, necessitating frequent endoscopic evaluations and surgical interventions. The rising incidence of head and neck cancers also drives the adoption of advanced imaging and minimally invasive surgical tools. As per the Global Burden of Disease Study, upper respiratory infections remain among the top causes of morbidity globally, particularly in pediatric populations, ensuring consistent utilization of basic ENT diagnostic instruments in primary care settings. Technological advancements have shifted the paradigm toward minimally invasive procedures, with robotic-assisted surgery gaining traction for complex skull base operations. Regulatory bodies, such as the U.S. Food and Drug Administration, continue to refine guidelines for device safety and efficacy, emphasizing the importance of precision engineering. This convergence of demographic pressures, disease prevalence, and technological innovation defines the current landscape, positioning ENT devices as critical components in modern otolaryngology practice and patient quality of life improvement.

MARKET DRIVERS

Escalating Prevalence of Chronic Respiratory and Sinus Disorders Fuels Diagnostic Demand

The rising global incidence of chronic respiratory conditions, particularly chronic rhinosinusitis and allergic rhinitis is one of the major factors propelling the growth of the ENT devices market. These conditions necessitate frequent diagnostic evaluations using rigid and flexible endoscopes, as well as surgical interventions involving powered instrumentation and image-guided systems. According to the American Academy of Otolaryngology-Head and Neck Surgery, chronic rhinosinusitis affects approximately 12.5% of the adult population in the United States, translating to millions of patients requiring regular clinical monitoring and potential surgical management. This substantial patient pool drives consistent demand for high-resolution visualization tools that enable precise assessment of sinus anatomy and pathology. Furthermore, environmental factors, such as increasing air pollution and allergen exposure, exacerbate these conditions, leading to higher recurrence rates and prolonged treatment courses. As per data from the World Health Organization, ambient air pollution contributes to millions of premature deaths annually, with respiratory diseases being a significant contributor, thereby intensifying the need for effective ENT diagnostics. The complexity of sinus surgery often requires advanced navigation systems to avoid critical structures, prompting healthcare facilities to invest in sophisticated technological solutions. Additionally, the growing preference for minimally invasive procedures reduces recovery times and hospital stays, making endoscopic sinus surgery a preferred option. This clinical shift ensures sustained utilization of specialized ENT instruments, fostering innovation in device design to enhance procedural efficiency and patient outcomes in managing pervasive respiratory ailments.

Increasing Burden of Hearing Loss Drives Adoption of Audiology and Implantable Devices

The escalating global burden of hearing impairment significantly propels the demand for audiological diagnostic equipment and implantable hearing solutions within the ENT devices sector. Age-related hearing loss, noise-induced damage, and congenital conditions create a vast demographic requiring comprehensive auditory assessment and rehabilitation. According to the World Health Organization, over 700 million people globally are projected to have disabling hearing loss by 2050, representing a nearly twofold increase from current figures. This demographic trend underscores the urgent need for advanced audiometers, tympanometers, and otoacoustic emission testing devices in both clinical and screening settings. As per data from the National Institute on Deafness and Other Communication Disorders, only about 16% of adults aged 20 to 69 who could benefit from hearing aids have ever used them, indicating a significant untapped market potential driven by increasing awareness and improved insurance coverage. Technological advancements in digital signal processing have enhanced the clarity and comfort of these devices, encouraging wider acceptance among patients. The integration of tele-audiology platforms also facilitates remote monitoring and adjustment, expanding access to care in underserved regions. Consequently, the rising prevalence of hearing disorders, coupled with technological innovations and improved accessibility, creates a robust and growing demand for specialized audiological ENT devices worldwide.

MARKET RESTRAINTS

High Capital Expenditure and Reimbursement Limitations Restrict Adoption

The substantial financial burden associated with acquiring advanced ENT equipment is a significant barrier to market penetration, particularly in smaller healthcare facilities and developing regions. Sophisticated technologies, such as image-guided surgical navigation systems, robotic platforms, and high-definition endoscopic towers, require significant upfront investment, often exceeding hundreds of thousands of dollars per unit. According to the Center for Healthcare Quality and Payment Reform, over 20% of rural hospitals in the United States are at risk of closing due to financial pressure, severely limiting their capacity to purchase capital-intensive ENT devices despite clinical need. As per data from the Centers for Medicare and Medicaid Services, reimbursement rates for certain endoscopic sinus procedures have remained stagnant or declined when adjusted for inflation over the past decade, discouraging investment in next-generation instrumentation. This economic pressure forces many clinics to rely on older, less efficient technology or refer complex cases to larger centers, fragmenting care delivery. According to data from the World Bank, out-of-pocket health expenditure remains high in low- and middle-income countries, meaning the cost of advanced ENT diagnostics and implants is often prohibitive for patients. Consequently, the misalignment between device costs and available financial resources stifles widespread adoption, preventing equitable access to state-of-the-art otolaryngology care and slowing overall market growth despite clear clinical benefits.

Shortage of Specialized Otolaryngologists Limits Procedural Volume

A critical shortage of trained otolaryngologists and allied ENT professionals significantly constrains the utilization and demand for specialized medical devices across global healthcare systems. Advanced ENT equipment requires highly skilled operators to perform complex diagnostics and surgeries safely and effectively, and without sufficient personnel, devices remain underutilized regardless of availability. According to the Association of American Medical Colleges, the United States faces a projected shortfall of up to 86,000 physicians by 2036, with surgical specialties being severely affected by workforce gaps. According to notes from the National Rural Health Association, this deficit is even more acute in rural and underserved areas, where the ratio of ENT specialists to the population can be less than 1 per 100,000 people. The lengthy training period required to master modern ENT technologies further exacerbates the bottleneck, as new graduates must navigate steep learning curves for robotic and navigation systems. As per findings from the World Health Organization, many low-income countries have fewer than one ENT specialist per million inhabitants, rendering advanced device deployment practically unfeasible. This human resource crisis creates a fundamental cap on procedural volumes, meaning that even if devices are affordable and available, the lack of qualified practitioners prevents their integration into routine care. Until training pipelines expand and retention improves, this workforce limitation will continue to suppress the realized potential of the ENT devices market.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Diagnostic Precision and Surgical Planning

The incorporation of artificial intelligence into ENT devices is a promising opportunity for the ENT devices market. AI algorithms can process high-resolution endoscopic images to detect early-stage pathologies, such as subtle mucosal changes indicative of malignancy, with greater accuracy than human observation alone. According to a study published in JAMA Otolaryngology-Head and Neck Surgery, AI-assisted diagnostic tools have demonstrated high diagnostic accuracy in identifying chronic rhinosinusitis patterns, significantly reducing misdiagnosis rates. As per data from the National Institutes of Health, the adoption of AI-driven planning software has significantly reduced operative times in complex sinus procedures, enhancing hospital efficiency and patient throughput. Furthermore, machine learning models can predict post-operative complications based on pre-operative imaging, allowing clinicians to tailor interventions more effectively. According to guidelines from the International Federation of Otorhinolaryngological Societies, AI integration facilitates standardized training for residents, accelerating proficiency in using advanced devices. Consequently, the convergence of computational power with otolaryngological instrumentation offers a pathway to highly personalized care, driving demand for intelligent devices that deliver superior diagnostic insights and procedural safety, thereby expanding market potential in both academic and community healthcare settings.

Expansion of Tele-ENT Services Drives Demand for Portable Home Diagnostic Devices

The rapid growth of telemedicine creates significant opportunities for the development and deployment of portable, patient-operated ENT diagnostic devices that facilitate remote consultations. As healthcare systems increasingly shift toward decentralized care models, there is a rising need for compact otoscopes, digital stethoscopes, and hearing assessment tools that patients can use at home under virtual guidance. According to the American Telemedicine Association, telehealth utilization experienced a massive baseline increase following recent global health disruptions, establishing a lasting precedent for remote management of minor ear, nose, and throat issues. As per findings from the World Health Organization, telemedicine can improve access to specialist care in rural areas where ENT specialists are scarce, potentially reaching millions of underserved patients. Furthermore, the integration of these devices with electronic health records enables seamless data sharing, enhancing continuity of care. According to reports from the Federal Communications Commission, expanded broadband access supports the reliable transmission of high-quality medical imagery, making remote diagnostics increasingly viable. This shift not only reduces unnecessary clinic visits but also empowers patients to monitor chronic conditions, like tinnitus or recurrent infections, creating a new revenue stream for device manufacturers focused on consumer-centric, connected health solutions.

MARKET CHALLENGES

Stringent Regulatory Approval Processes Delay Market Entry and Innovation

The rigorous regulatory landscape governing medical devices is a significant challenge to the ENT devices market, particularly for novel technologies requiring extensive clinical validation. Obtaining clearance from bodies such as the U.S. Food and Drug Administration or the European Commission involves complex pre-market submissions, prolonged review periods, and substantial financial investment. According to the FDA, the average time for 510(k) clearance can range from several months to over a year, while Premarket Approval for high-risk Class III devices, such as certain cochlear implants, often takes three to five years. As per data from the Advanced Medical Technology Association, the cost of bringing a new medical device to market in the United States can exceed $30 million, creating a high barrier to entry for smaller innovators. The implementation of the European Union’s Medical Device Regulation has further intensified these requirements, mandating more robust clinical evidence and post-market surveillance. This regulatory burden delays the commercialization of innovative solutions, such as robotic-assisted surgical systems, limiting patient access to cutting-edge treatments. Furthermore, inconsistent regulatory standards across different global regions force manufacturers to navigate fragmented compliance frameworks, increasing operational complexity. According to statements from the World Health Organization, regulatory harmonization remains incomplete, leading to disparities in device availability. Consequently, the time and capital required to meet these stringent standards restrict the pace of innovation and market expansion, particularly for startups lacking the resources of established multinational corporations.

Risk of Surgical Complications and Device-Associated Infections Impacts Adoption

The inherent risks associated with invasive ENT procedures, including potential surgical complications and device-associated infections, which is further challenging the global market expansion. Despite advancements in minimally invasive techniques, procedures involving the skull base or inner ear carry risks of nerve damage, cerebrospinal fluid leaks, or hearing loss. According to the Agency for Healthcare Research and Quality, surgical site infections account for approximately 20% of all healthcare-associated infections, with head and neck surgeries being highly susceptible due to the proximity to contaminated areas like the nasal cavity. As per findings published in Otolaryngology–Head and Neck Surgery, complication rates for endoscopic sinus surgery, while generally low, can lead to significant morbidity if critical structures are injured, prompting cautious adoption of new instruments. Additionally, the reuse of certain ENT instruments, if not properly sterilized, poses cross-contamination risks. According to recommendations from the Centers for Disease Control and Prevention, strict sterilization protocols are emphasized, but lapses in hospital compliance can result in outbreaks, damaging trust in specific device brands. These safety concerns necessitate rigorous training and quality control measures, increasing operational costs for healthcare facilities. Fear of litigation and adverse outcomes may also deter surgeons from adopting newer, less proven technologies, thereby slowing market penetration for innovative ENT devices despite their potential clinical benefits.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Devices, End-User & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Johnson & Johnson Services, Inc. (DePuy Synthes), Stryker, Zimmer Biomet, Orthofix Medical, Inc., B. Braun Melsungen AG, Medtronic, NuVasive, Inc., Globus Medical, ATEC Spine, Inc., Captiva Spine, Inc., SeaSpine, Spinal Elements, Inc., Spine Wave, Inc., Spineology, Inc., and Xtant Medical Holdings, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The hearing aids segment dominated the market by holding 32.3% of the global market share in 2025. The growth of the hearing aids segment in the global market is majorly driven by the escalating global prevalence of age-related hearing loss and significant technological advancements in device miniaturization. The primary factor underpinning this dominance is the demographic shift toward an aging population, which is disproportionately affected by presbycusis. According to the World Health Organization, nearly 2.5 billion people globally will have some degree of hearing loss by 2050, with over 700 million requiring rehabilitation, creating a vast and expanding user base for hearing aids. This demographic trend is particularly pronounced in developed regions. As per data from the National Institute on Deafness and Other Communication Disorders, approximately one in three adults between the ages of 65 and 74 has disabling hearing loss in the United States alone. Furthermore, recent regulatory changes, such as the U.S. Food and Drug Administration’s approval of over-the-counter hearing aids, have democratized access by reducing costs and eliminating the need for professional fitting for mild-to-moderate cases. This policy shift has significantly lowered barriers to entry, encouraging earlier adoption among consumers who previously delayed treatment due to expense or stigma. Additionally, the integration of Bluetooth connectivity and artificial intelligence for noise cancellation has enhanced user experience, making modern hearing aids desirable consumer electronics rather than just medical necessities. These converging factors ensure that hearing aids remain the most lucrative product segment, supported by robust demand and increasing social acceptance.

On the other end, the image-guided surgery systems segment is projected to register the highest CAGR of 9.5% during the forecast period in the global market owing to the increasing complexity of otolaryngological procedures and the critical need for precision in anatomically constrained areas. The principal driver accelerating this expansion is the rising adoption of minimally invasive endoscopic sinus and skull base surgeries, where real-time navigation is essential to avoid damage to critical structures such as the optic nerve and carotid artery. According to the American Academy of Otolaryngology-Head and Neck Surgery, the volume of functional endoscopic sinus surgeries has increased significantly in recent decades, reflecting a broader clinical shift toward image-guided interventions. As per findings from the Journal of Neurosurgery, the use of IGS in complex skull base tumor resections has reduced complication rates by up to 30% compared to traditional methods, demonstrating clear clinical value that justifies high capital investment. Furthermore, technological advancements in augmented reality and electromagnetic tracking have improved the accuracy and ease of use of these systems, making them accessible to a wider range of surgeons. According to policy rollouts from the Centers for Medicare and Medicaid Services, the agency has expanded reimbursement codes for navigated procedures, alleviating financial burdens on healthcare providers. This combination of improved patient outcomes, regulatory support, and technological sophistication positions IGS systems as the fastest-growing segment, as hospitals increasingly prioritize safety and efficiency in high-risk ENT surgeries.

By Device Type Insights

The endoscopes segment captured the leading share of 60.6% of the global market in 2025. The dominance of endoscopes segment in the global market is attributed to their indispensable role in both diagnostic evaluation and minimally invasive surgical interventions. According to the American Academy of Otolaryngology-Head and Neck Surgery, endoscopic sinus surgery is now the gold standard for treating chronic rhinosinusitis, a condition affecting millions globally, ensuring consistent high-volume utilization of rigid and flexible endoscopes. As per data from the Centers for Disease Control and Prevention, upper respiratory infections and chronic sinus issues remain among the most common reasons for physician visits, necessitating routine endoscopic examinations for accurate diagnosis. Furthermore, technological advancements, such as high-definition 4K imaging and narrow-band illumination, have enhanced the detection of early-stage malignancies and subtle mucosal changes, expanding the clinical utility of these devices. According to the World Health Organization, head and neck cancers are increasingly prevalent due to lifestyle factors, requiring precise endoscopic biopsy and staging. Additionally, the versatility of endoscopes allows them to be used across various subspecialties, including laryngology and otology, broadening their application scope. This multifaceted utility, combined with the ongoing shift toward outpatient surgical centers where efficiency is paramount, solidifies the endoscope segment’s leading position, supported by robust demand from both hospital systems and private practices seeking optimal diagnostic and therapeutic outcomes.

However, the hearing screening devices segment is anticipated to showcase a CAGR of 8.4% during the forecast period in the global market owing to the stringent public health mandates for newborn hearing screening and increasing awareness of pediatric auditory health. According to the World Health Organization, early identification and management of hearing loss can significantly improve language development and educational outcomes, prompting governments worldwide to mandate screening protocols. As per data from the Centers for Disease Control and Prevention, nearly all babies born in United States hospitals are screened for hearing loss before discharge, creating a sustained institutional demand for automated auditory brainstem response and otoacoustic emission devices. Furthermore, the rising prevalence of noise-induced hearing loss among adolescents and young adults has expanded the target demographic beyond neonates, driving adoption in schools and occupational health settings. According to data from the National Institute on Deafness and Other Communication Disorders, a significant percentage of children aged 6 to 19 years have permanent damage to their hearing from excessive noise exposure, necessitating regular monitoring. Technological innovations, such as portable, wireless screening tools integrated with electronic health records, have streamlined the testing process, making large-scale screening campaigns more feasible. This regulatory support, combined with growing public health emphasis on preventive care, positions hearing screening devices as the fastest-growing segment in the ENT market.

REGIONAL ANALYSIS

North America ENT Devices Market Analysis

North America held 39.1% of the global market share in 2025 and is poised to drive the global marketplace with superior tech-integrations and a highly responsive healthcare model over the next few years. The United States serves as the primary engine of this growth, characterized by a high prevalence of chronic ENT conditions and robust reimbursement mechanisms for complex procedures. According to the Centers for Disease Control and Prevention, chronic sinusitis affects millions of Americans annually, necessitating frequent diagnostic endoscopies and surgical interventions using image-guided systems. The region benefits from significant federal funding for medical research. As per data from the National Institutes of Health, billions are invested annually in health research, fostering innovation in robotic surgery and hearing implants. Furthermore, the aging population contributes to sustained demand. According to projections from the U.S. Census Bureau, all baby boomers will be older than 65 by 2030, expanding the user base for hearing aids and cochlear implants. The presence of major industry players who continuously introduce technologically superior products ensures that North America remains at the forefront of market development. Strict regulatory standards enforced by the Food and Drug Administration also guarantee high product quality, reinforcing consumer trust and maintaining steady sales volumes across both clinical and consumer segments, thereby solidifying its leadership in the global ENT landscape.

Europe ENT Devices Market Analysis

Europe occupied the second-largest share of the global market in 2025 due to the stringent regulatory frameworks and a rapidly aging demographic profile that increases susceptibility to sensory impairments. The implementation of the Medical Device Regulation by the European Union has standardized safety and performance requirements, ensuring high-quality ENT products across member states while raising barriers for substandard entries. According to Eurostat, over 21% of the EU population is aged 65 or older, a segment with higher incidence rates of hearing loss and head and neck cancers requiring specialized diagnostic and therapeutic devices. Germany, France, and the United Kingdom are key contributors, boasting well-established public healthcare systems that prioritize comprehensive ENT care and early intervention programs. According to the World Health Organization, Europe faces a significant burden of chronic respiratory diseases, driving consistent demand for endoscopic evaluation tools in hospital settings. The region’s strong emphasis on minimally invasive surgery has accelerated the adoption of advanced navigation systems and powered instrumentation. Additionally, government initiatives promoting universal newborn hearing screening have bolstered the market for pediatric audiology devices. This combination of regulatory rigor, demographic pressure, and technological adoption sustains Europe’s prominent position, fostering a market characterized by high-value, precision-oriented diagnostic and surgical instruments that meet strict clinical efficacy standards.

Asia Pacific ENT Devices Market Analysis

The Asia Pacific theater will function as a vital growth engine through volume-driven demands and public health modernizations over the next few years. Countries like China, India, and Japan are leading this expansion through significant government investments in hospital modernization and private sector participation in specialty care. According to data from the World Bank, health expenditure in East Asia and the Pacific has grown at an average annual rate of 8% over the past decade, reflecting improved access to diagnostic tools and surgical options.

COMPETITIVE LANDSCAPE

The competition in the ENT devices market is characterized by intense rivalry among established multinational corporations and specialized niche players, driven by rapid technological advancements and increasing demand for precision diagnostics. Major competitors differentiate themselves through innovation in surgical navigation, robotic assistance, and miniaturized hearing implants, while competing on brand reputation and clinical support services. The market sees frequent strategic alliances and acquisitions as companies seek to expand their product portfolios and geographic reach, particularly in high-growth regions like Asia Pacific. Regulatory compliance and quality standards serve as significant barriers to entry, favoring incumbents with robust infrastructure and established clinical data. However, emerging players focusing on cost-effective solutions and tele-audiology platforms are gaining traction by offering accessible alternatives to traditional high-end devices. Price competition remains moderate in the surgical segment but is more pronounced in consumer hearing aids. The dynamic landscape requires continuous investment in research and development to keep pace with evolving clinical needs and digital integration trends, ensuring that only agile and innovative organizations sustain long-term competitiveness in this critical specialty care sector.

KEY MARKET PARTICIPANTS

Companies currently dominating the global ENT devices market and profiled include

- Johnson & Johnson Services, Inc. (DePuy Synthes)

- Stryker

- Zimmer Biomet

- Orthofix Medical, Inc.

- B. Braun Melsungen AG

- Medtronic

- NuVasive, Inc.

- Globus Medical

- ATEC Spine, Inc.

- Captiva Spine, Inc.

- SeaSpine

- Spinal Elements, Inc.

- Spine Wave, Inc.

- Spineology, Inc.

- Xtant Medical Holdings, Inc.

TOP COMPANIES

Medtronic plc

Medtronic maintains a robust presence in the Asia Pacific ENT devices market through its comprehensive portfolio of surgical navigation systems and powered instrumentation. The company actively strengthens its position by collaborating with regional hospitals to implement advanced image-guided surgery protocols, enhancing procedural precision for complex sinus and skull base operations. Recent initiatives include expanding training centers in key hubs like Singapore and India, ensuring surgeons are proficient in utilizing their latest robotic-assisted technologies. Medtronic also focuses on strategic partnerships with local distributors to improve supply chain efficiency and product accessibility across diverse healthcare settings. By integrating digital health solutions that facilitate pre-operative planning and post-operative monitoring, the company addresses the growing demand for minimally invasive procedures. This commitment to education and technological innovation solidifies Medtronic’s reputation as a trusted partner for otolaryngologists seeking to improve patient outcomes and operational efficiency throughout the rapidly evolving Asia Pacific healthcare landscape.

Cochlear Limited

Cochlear Limited dominates the Asia Pacific hearing implant sector by delivering innovative cochlear implant systems and bone conduction devices tailored to diverse patient needs. The company has significantly expanded its footprint through localized manufacturing facilities in Australia and China, ensuring cost-effective production and faster delivery times. Recent actions include launching next-generation implants with enhanced connectivity features, allowing seamless integration with smartphones and assistive listening devices popular in the region. Cochlear actively collaborates with governments and non-profit organizations to support newborn hearing screening programs and subsidize implant surgeries in underserved communities. Their extensive clinical support network provides continuous rehabilitation services, crucial for long-term user success. By prioritizing affordability and accessibility while maintaining high technological standards, Cochlear effectively addresses the rising prevalence of hearing loss in aging Asian populations, reinforcing its leadership in restoring auditory function and improving quality of life for thousands of patients across the Asia Pacific region.

Olympus Corporation

Olympus Corporation leverages its expertise in optical technology to provide high-quality rigid and flexible endoscopes widely used in ENT diagnostics and surgery across Asia Pacific. The company strengthens its market position by continuously innovating its visualization systems, introducing 4K and 3D imaging capabilities that enhance diagnostic accuracy for subtle mucosal pathologies. Recent strategies involve establishing dedicated demonstration labs in major cities like Tokyo and Shanghai, allowing clinicians to experience advanced endoscopic techniques firsthand. Olympus also partners with regional medical associations to promote standardized training protocols for endoscopic sinus surgery, fostering skill development among local practitioners. Their focus on durability and ergonomic design appeals to high-volume hospital settings seeking reliable equipment. By integrating artificial intelligence for real-time lesion detection, Olympus stays at the forefront of diagnostic innovation. This combination of superior optical performance, educational support, and technological advancement ensures Olympus remains a preferred choice for ENT specialists demanding precision and clarity in their daily clinical practice throughout the Asia Pacific market.

Top strategies used by the key market participants

Key players in the ENT devices market primarily employ strategies centered on technological innovation, strategic acquisitions, and geographic expansion. Companies invest heavily in research and development to create advanced image-guided systems, robotic surgical platforms, and smart hearing aids that integrate with digital health ecosystems. Mergers and acquisitions are frequently utilized to acquire niche technologies or expand product portfolios, particularly in audiology and minimally invasive surgery. Collaborations with academic institutions and professional societies facilitate clinical validation and surgeon training, enhancing product adoption. Manufacturers also focus on penetrating emerging markets in Asia Pacific and Latin America by establishing local manufacturing units and distribution networks to reduce costs. Additionally, emphasizing value-based care through improved patient outcomes and reduced recovery times helps secure favorable reimbursement policies. These multifaceted approaches enable companies to maintain competitive advantages, address diverse clinical needs, and capitalize on the growing global demand for precise and efficient ENT diagnostic and therapeutic solutions.

RECENT MARKET HAPPENINGS

- In February 2022, Baylis Medical Company Inc. was acquired by Boston Scientific Corporation. Baylis Medical Company Inc. provides trans septal access solutions, guidewires, sheaths and dilators for catheter-based left-heart procedures are now under Boston Scientific Corporation and the company aims to bring forth advanced research and development with this acquisition.

- In June 2022, ShengWang was acquired by Demant. Demant achieved full ownership of ShengWang, the top network of hearing aid clinics in China, by acquiring the remaining 80% of its shares.

- In January 2022, the Livio AI Edge, a new hearing aid from Starkey Hearing Technologies, utilizes artificial intelligence to enhance hearing capabilities and can keep track of an individual's physical and cognitive well-being.

- In February 2021, the LATERA nasal implant was granted clearance by the FDA. This implant is designed to provide support to the lateral nasal wall and alleviate nasal airway obstruction.

MARKET SEGMENTATION

This research report on the global ENT devices market has been segmented and sub-segmented based on product, devices, end-user & region.

By Product

- Diagnostic Devices

- Surgical Devices

- Hearing Aids

- Hearing Implants

- Co2 Lasers

- Image-Guided Surgery Systems

By Device Type

- Endoscopes

- Hearing Screening Devices

By End-User

- Home Use

- Hospitals and Ambulatory Settings

- ENT Clinics

By Region

- North America

- Asia Pacific

- Europe

- Latin America

- The Middle East and Africa

Frequently Asked Questions

Which region is growing the fastest in the global ENT devices market ?

Geographically, the North American ENT devices market accounted for the largest share of the global market in 2024.

At What CAGR, the global ENT devices market is expected to grow from 2025 to 2033?

As per our research report, the global ENT devices market size is projected to be USD 30.70 billion by 2032.

Does this report include the impact of COVID-19 on the ENT devices market ?

Yes, we have studied and included the COVID-19 impact on the global ENT devices market in this report.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com