Europe Adhesives and Sealants Market Size, Share, Trends And Growth Forecasts Research Report, Segmented By Type, Business, Application and Country – Industry Analysis (2026 to 2034)

Europe Adhesives and Sealants Market Report Summary

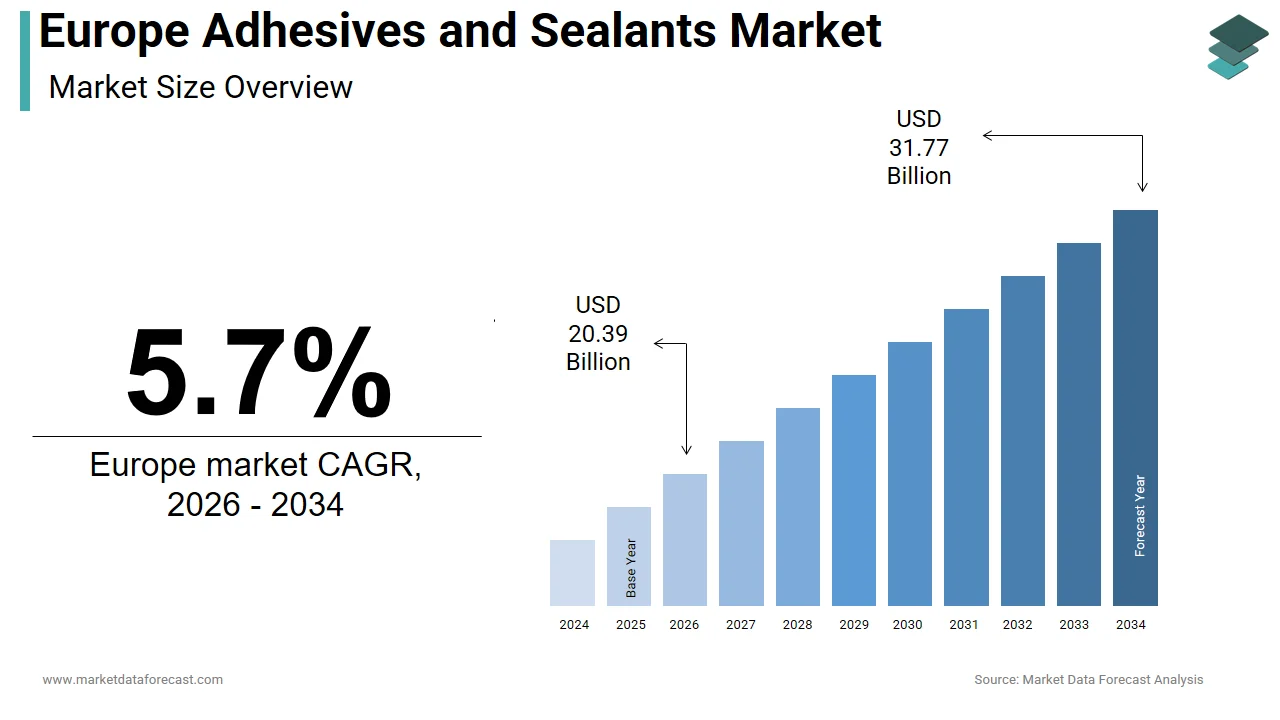

The Europe adhesives and sealants market was valued at USD 19.29 billion in 2025, is anticipated to reach USD 20.39 billion in 2026, and is projected to reach USD 31.77 billion by 2034, growing at a CAGR of 5.7% from 2026 to 2034. Market growth is driven by rising construction and infrastructure activities, increasing demand from the automotive and packaging industries, and expanding applications in renewable energy and electronics manufacturing. The growing preference for lightweight materials, enhanced bonding performance, and sustainable formulations is further supporting market expansion. Additionally, continuous product innovations in water-based, low-VOC, and bio-based adhesives are strengthening adoption across Europe.

Key Market Trends

- Rising demand for high-performance and lightweight bonding solutions in automotive, aerospace, and electronics sectors.

- Increasing adoption of eco-friendly and low-VOC adhesives and sealants to comply with stringent environmental regulations.

- Strong growth in construction and infrastructure development projects, boosting consumption of sealants and structural adhesives.

- Expanding use of reactive and hybrid adhesive technologies for enhanced durability and flexibility.

- Growing investments in research and development to improve thermal resistance, curing speed, and material compatibility.

Segmental Insights

- Based on adhesive resin, the acrylic resins segment dominated the Europe adhesives and sealants market in 2024 by accounting for 37.9% market share. The segment’s dominance is attributed to its strong bonding properties, durability, weather resistance, and wide applicability across construction and industrial sectors.

- Based on adhesive technology, the reactive adhesives segment led the market and held 42.3% share in 2024, driven by high strength, superior chemical resistance, and increasing use in structural bonding applications.

- Based on end user industry, the building and construction segment was the largest, occupying 45.4% market share in 2024, supported by growing demand for sealants and adhesives in residential, commercial, and infrastructure projects.

Regional Insights

The Europe adhesives and sealants market is witnessing steady growth across major economies, supported by industrial expansion, rising construction activity, and increasing investments in sustainable manufacturing practices.

- Germany stood as the top performer in 2024 with 24.4% market share, driven by strong automotive production, advanced manufacturing capabilities, and high demand for industrial adhesives.

- France accounted for 15.8% share in 2024, supported by robust construction activity and expanding packaging and consumer goods industries.

- The United Kingdom holds a notable position, driven by infrastructure modernization, housing development, and growing adoption of high-performance bonding solutions.

Competitive Landscape

The Europe adhesives and sealants market is characterized by the presence of leading multinational manufacturers and regional suppliers with strong technological capabilities and extensive distribution networks. Market players are focusing on developing sustainable formulations, enhancing product performance, and expanding application-specific solutions. Strategic partnerships, capacity expansions, and investments in research and development are strengthening competitive positioning across the region.

Prominent companies operating in the Europe adhesives and sealants market include Sika AG, H.B. Fuller Company, 3M, Arkema, and Henkel AG & Co. KGaA.

Europe Adhesives and Sealants Market Size

The size of the Europe adhesives and sealants market was worth USD 19.29 billion in 2025. The regional market is anticipated to grow at a CAGR of 5.7% from 2026 to 2034 and be worth USD 31.77 billion by 2034 from USD 20.39 billion in 2026.

Adhesives and sealants are engineered bonding and joint-filling materials essential to modern manufacturing, construction, and assembly processes across Europe. Also, adhesives create durable structural or non-structural bonds between substrates while sealants provide elastic barriers against moisture, air, dust, and thermal transfer at interfaces. In Europe, their use is deeply integrated into sectors requiring precision lightweighting and durability, such as automotive, aerospace, building and renovation, electronics and packaging. The regulatory landscape significantly shapes formulation trends, with the European Chemicals Agency enforcing strict controls on volatile organic compounds, isocyanates, and other hazardous substances under REACH and the Construction Products Regulation. According to sources, there is a general shift towards energy-efficient windows using high-performance sealants, which is driven by the EU's Nearly Zero-Energy Building (nZEB) standards, which became mandatory for all new construction in Europe from 2021. This policy has driven high adoption rates of advanced building materials and techniques. Apart from these, European passenger cars contain adhesives primarily for bonding lightweight composites and reducing spot welding. These technical and regulatory imperatives define the Europe adhesives and sealants market not as a commodity segment but as a critical enabler of sustainability, safety, and advanced engineering.

MARKET DRIVERS

Accelerated Building Renovation Driven by EU Energy Efficiency Mandates

The European Union’s ambitious renovation wave initiative is a key accelerator for the Europe adhesives and sealants market. This drives up the demand for them in the construction sector. Launched under the European Green Deal, this policy aims to double the annual energy renovation rate of residential and public buildings to 2 percent by 2030, targeting a 60 percent reduction in building sector emissions. As per the European Commission, the Renovation Wave aims to renovate 35 million building units by 2030. These renovations involve deep retrofits, including insulation, window replacement, and general energy efficiency improvements to reduce energy consumption. Silicone and hybrid polymer sealants are indispensable for bonding external thermal insulation composite systems, while polyurethane foams and acrylic adhesives secure insulation panels to masonry substrates. This regulatory-driven retrofit surge transforms adhesives and sealants from ancillary materials into compliance enablers directly tied to Europe’s decarbonization trajectory.

Lightweighting in Automotive and Transport Manufacturing

The structural integration of adhesives in European automotive and rail manufacturing is intensifying as OEMs pursue aggressive vehicle lightweighting to comply with CO2 emission standards, which fuels the expansion of the Europe adhesives and sealants market. The European Union’s fleet-wide CO2 target of 95 grams per kilometer for new passenger cars enforced since 2020 has compelled manufacturers to replace steel with aluminum composites and high-strength plastics, which cannot be joined effectively by traditional welding. Also, the average aluminum content in European cars increased. This shift necessitates high-strength epoxy and polyurethane structural adhesives capable of distributing stress across dissimilar materials while enhancing crash performance. In the rail sector, the European Railway Agency mandates fire, smoke, and toxicity compliance, driving adoption of intumescent sealants and halogen-free adhesives in interior assemblies.

MARKET RESTRAINTS

Stringent Regulatory Restrictions on Hazardous Chemicals

Mounting burden from evolving chemical regulations that restrict or ban key formulation components essential for performance and cost efficiency slows down the growth of the Europe adhesives and sealants market. Compliance with the new training mandate has disrupted supply chains, particularly among small and medium-sized contractors who lack the resources to implement certification protocols. Apart from these, the EU’s Ecolabel criteria for construction products prohibit volatile organic compound emissions above a level for interior sealants, forcing formulators to adopt more expensive bio-based or waterborne alternatives that may compromise adhesion or cure speed. These regulatory hurdles increase R and D costs, lengthen time to market, and limit formulation flexibility, particularly for niche high-performance applications where substitutes remain technically unproven.

Volatility in Petrochemical Feedstock Prices

Its high vulnerability towards fluctuations in petrochemical raw material costs, as the majority of synthetic polymers, including acrylics, epoxies, polyurethanes and silicones derive from crude oil or natural gas derivatives, obstructs the expansion of the Europe adhesive and sealants market. The vast majority of adhesive resins in the region are derived from petroleum, with critical monomers closely linked to refinery economics and international energy dynamics. As per sources, recent energy crises triggered by geopolitical conflicts have led to significant volatility in raw material pricing, notably affecting production stability within the adhesives industry. Unlike Asian or North American producers with access to low-cost shale gas, European formulators operate at a structural cost disadvantage. This feedstock dependency not only affects pricing stability but also slows the transition to bio-based alternatives.

MARKET OPPORTUNITIES

Expansion of Sustainable and Bio-Based Formulations

The shift toward circular and low-carbon construction and manufacturing is generating major opportunities for bio-based and recyclable formulations, which in turn contribute to the growth of the Europe adhesives and sealants market. The EU Taxonomy for Sustainable Activities and green public procurement criteria are driving adhesive formulators to focus on developing products from renewable materials, including tall oil rosin, lignin, castor oil, and bioethanol. Many new bio-based adhesive products were launched in Europe in recent years, targeting wood construction, packaging, and footwear sectors. In the wood industry, formaldehyde-free adhesives based on tannins or soy proteins now comply with the strictest emission class E1 under EN 717, enabling use in schools and hospitals. Companies have introduced thermally reversible adhesives that dissolve at specific temperatures, allowing mono-material recovery from multilayer laminates. These innovations position sustainable adhesives not as niche alternatives but as strategic enablers of Europe’s circular economy framework.

Growth in Prefabricated and Modular Construction

The rapid adoption of off-site construction methods in the region is creating a key opportunity for the expansion of the Europe adhesives and sealants market. Modular construction reduces on-site labor waste and project timelines while improving quality control, attributes aligned with the EU’s construction sector decarbonization goals. A large number of modular housing units were installed in the European Union. These systems rely on structural adhesives to bond insulated wall panels, floor cassettes, and roof trusses, often replacing mechanical fasteners to maintain thermal continuity and reduce thermal bridging. Furthermore, the precision of factory environments allows the use of reactive hot melt and UV curing adhesives that require controlled conditions, impractical on conventional sites. Modular construction's speed and scalability will boost the demand for industrial-grade bonding and sealing solutions tailored for off-site productivity as the EU directs RRF funds towards social and student housing initiatives.

MARKET CHALLENGES

Intense Competition from Low-Cost Asian Imports

Manufacturers face an escalating burden from competitively priced imports primarily from China, South Korea, and India, which impedes the Europe adhesives and sealants market from growing. These countries benefit from lower production costs, less stringent environmental compliance, and government export subsidies. The price differential is especially disruptive in price-sensitive segments such as general construction and consumer DIY, where brand loyalty is low and procurement decisions are driven by upfront cost. Although the EU maintains anti-dumping duties on certain acrylic and PVAc adhesives from China, these measures do not cover newer product categories like MS polymers or hybrid sealants. European small and medium-sized enterprises (SMEs) that specialize in intermediate-quality products are losing market share, particularly in Southern and Eastern Europe, because public infrastructure contracts there overwhelmingly favor the cheapest bids. This import surge undermines local innovation cycles and threatens the long-term viability of Europe’s specialty chemical manufacturing base.

Technical Complexity in Recycling Adhesive-Bonded Products

The increasing use of high-strength permanent adhesives in multi-material products is a formidable end-of-life challenge that constrains the expansion of the Europe adhesives and sealants market. This technical complexity conflicts with the region’s circular economy ambitions. Modern vehicles, smartphones, and white goods integrate adhesives to bond composites, metals, and plastics into lightweight, durable assemblies, but these bonds resist conventional mechanical or thermal disassembly methods. As per sources, a smaller share of adhesive-bonded electronic waste is effectively separated for material recovery due to the lack of debonding technologies. Reversible adhesives, despite existing, are confined to niche applications because of inherent cost and performance compromises. The qualities that make adhesives valuable in manufacturing currently impede recycling efforts, which poses a systemic challenge to EU sustainability and compliance goals until mandatory debonding standards or design for disassembly protocols are established.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Adhesive Resin, Adhesive Technology, Sealant Resin, End-User Industry, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Sika AG, H.B. Fuller Company, 3M, Arkema, and Henkel AG & Co. KGaA. |

SEGMENTAL ANALYSIS

By Adhesive Resin Insights

The acrylic resins segment continued to dominate the Europe adhesives and sealants market and accounted for a 37.9% share in 2024. Their versatility, rapid curing speed, and excellent resistance to UV aging and temperature fluctuations make them ideal for outdoor construction and automotive applications, which drives the segment's domination. In the building and construction sector, acrylic adhesives are extensively used for bonding cladding panels, insulation boards, and glazing systems where long-term weatherability is critical. Apart from these, acrylic pressure-sensitive adhesives dominate the labeling and packaging industry, which processes billions of consumer packages annually in the European Union. Their compatibility with high-speed converting equipment and recyclability with paper and plastic streams further enhances adoption. Regulatory alignment also plays a role as waterborne acrylic formulations meet the EU’s limits for interior construction adhesives. These performance, regulatory, and industrial integration advantages sustain acrylic resins as the backbone of European adhesive demand.

The epoxy resins segment is anticipated to witness the fastest CAGR of 6.9% from 2025 to 2033. The swift growth of the epoxy resins segment is driven by the expanding use of fiber-reinforced polymers in wind energy infrastructure and electric vehicle manufacturing. Europe added notable gigawatts of onshore and offshore wind capacity in 2023, and each multi-megawatt turbine blade relies on high-strength epoxy adhesives to bond carbon and glass fiber laminates under extreme cyclic loading. A single 100-meter offshore blade can contain kilograms of epoxy adhesive systems. Battery producers specify epoxy systems for cell-to-pack bonding to meet UN ECE R100 safety standards. Furthermore, the EU’s Critical Raw Materials Act prioritizes domestic battery production, reinforcing long-term epoxy demand. These converging clean energy and mobility transitions position epoxy resins as the highest growth vector in the European adhesive landscape.

By Adhesive Technology Insights

The reactive adhesives segment led the Europe adhesives and sealants market and held 42.3% of the regional market share in 2024. The supremacy of the reactive adhesives segment is attributed to their superior structural performance, chemical resistance, and durability in demanding industrial applications. Reactive systems, including polyurethanes, epoxies, silicones, and MS polymers, cure through chemical crosslinking rather than solvent evaporation or cooling, enabling strong bonds across dissimilar substrates such as metal composites and glass. In automotive manufacturing, a share of body in white bonding applications use reactive polyurethane or epoxy adhesives to enable multi-material lightweighting. The technology’s alignment with durability, safety, and sustainability requirements across transport and construction ensures its entrenched position as the preferred bonding method in high-value European manufacturing.

The hot melt adhesives segment is likely to experience the fastest CAGR of 7.2% during the forecast period. The e-commerce boom and the EU’s push for solvent-free free sustainable packaging have largely boosted the expansion of the hot melt adhesives segment. Europe generated billions of e-commerce parcels in 2023, with each requiring rapid case sealing, labeling, and tray forming operations best served by hot melts due to their instantaneous setting and compatibility with automated lines. Major logistics hubs process a large number of parcels daily, relying on ethylene vinyl acetate and polyolefin hot melts for high-speed throughput. Apart from these, the EU Packaging and Packaging Waste Regulation prohibits solvent-borne adhesives in most consumer packaging. Retailers have mandated hot-melt-only assembly for all private label packaging across their European supply chains. Technological advances also enable bio-based hot melts from tall oil and castor oil. These regulatory packaging and sustainability drivers position hot melts as the most dynamic growth segment in adhesive technology.

By End User Industry Insights

The building and construction segment was the largest segment of the Europe adhesives and sealants market and occupied a 45.4% share in 2024. Factors such as the sector’s scale, regulatory intensity, and structural reliance on bonding technologies for modern construction practices drive the growth of the building and construction segment. Prefabricated construction further amplifies demand as modular units use structural adhesives to bond wall and floor panels off-site. Apart from these, the shift toward ceramic and large-format tiles in residential and commercial spaces has increased demand for flexible cementitious and polymer-modified adhesives compliant with EN 12004. These intertwined regulatory, technological, and demographic forces ensure construction remains the cornerstone of adhesive and sealant consumption in Europe.

The aerospace segment is on the rise and is expected to be the fastest-growing segment in the regional market by witnessing a CAGR of 8.1 percent from 2025 to 2033, owing to the rebound in commercial aviation and the strategic emphasis on lightweight composite airframes. Airbus delivered commercial aircraft in 2023, with some of its models comprising composite materials by weight, bonded primarily with film and paste epoxy adhesives that reduce fastener count and improve fatigue resistance. Military aviation also contributes, as the European Defence Fund supports next-generation platforms that will rely heavily on adhesive-bonded stealth structures. Furthermore, stringent fire, smoke, and toxicity requirements under EASA CS drive demand for specialty intumescent and halogen-free sealants in cabin interiors.

COUNTRY LEVEL ANALYSIS

Germany Adhesives and Sealants Market Analysis

Germany stood as the top performer in the Europe adhesives and sealants market and held a 24.4% share in 2024. The country’s dominance is because of its world-class automotive engineering, chemical industry, and precision manufacturing base. Germany hosts the headquarters or major production sites of global adhesive leaders while supplying adhesives to automotive OEMs, which collectively produced millions of vehicles in 2023. The chemical sector alone consumes notable metric tons of industrial adhesives annually for equipment assembly and maintenance, as per VCI data. Construction demand is equally robust, driven by the federal government’s Building Energy Act, which emphasizes stepwise reduction in primary energy use, prompting widespread use of high-performance sealants in window and insulation systems. Furthermore, Germany’s dual vocational training system ensures a skilled workforce capable of handling advanced reactive adhesive applications in industrial settings. These structural, industrial, and regulatory strengths cement Germany’s position as the innovation and volume hub of the European adhesives and sealants landscape.

France Adhesives and Sealants Market Analysis

France is another major country in the Europe adhesive and sealants market and accounted for a 15.8% share in 2024. The demand for adhesives in the country is attributed to its strong aerospace sector, robust housing renovation activity, and expanding renewable energy infrastructure. The packaging industry also contributes significantly, with France generating millions of tons of packaging waste annually, necessitating high-speed hot melt systems for corrugated and carton sealing. These diverse high-value applications across mobility, construction, and logistics sustain France’s strong and balanced adhesive and sealant market.

United Kingdom Adhesives and Sealants Market Analysis

The United Kingdom captured a notable position in the Europe adhesives and sealants market. Despite post-Brexit regulatory divergence, the UK maintains technical alignment with EU construction and transport standards, ensuring continued demand for high-performance products. The housing sector is a major driver, with the government targeting a significant number of new homes annually, requiring extensive use of tile adhesives, structural glazing sealants, and flooring bonding agents. The automotive sector remains significant through premium OEMs like Jaguar Land Rover and Nissan Sunderland, which utilize structural adhesives for lightweight body assembly. Additionally, the UK’s offshore wind capacity reached notable gigawatts in 2023, with each turbine requiring epoxy adhesives for blade and nacelle assembly. These combined construction energy and manufacturing dynamics underpin the UK’s resilient and diversified adhesive consumption profile.

Italy Adhesives and Sealants Market Analysis

Italy gradually expanded in the Europe adhesives and sealants market. The growth of the Italian market is due to its globally recognized ceramics, furniture, and mechanical engineering industries. It produces a notable share of the world’s ceramic tiles, with each square meter requiring specialized cementitious or polymer-modified adhesives for installation. The furniture sector centered in Brianza and Friuli generates billions of euros in annual exports, relying on polyvinyl acetate and hot melt adhesives for wood lamination and edge banding. Apart from these, Italy’s mechanical engineering cluster in Emilia Romagna produces packaging machinery that integrates automated adhesive dispensing systems for global clients. These niche manufacturing strengths, combined with post-pandemic reconstruction efforts, ensure Italy remains a key and distinctive market in Southern Europe.

Netherlands Adhesives and Sealants Market Analysis

The Netherlands is anticipated to grow in the European adhesives and sealants market from 2025 to 2033, owing to high concentration in logistics, packaging, and advanced manufacturing. Companies operate fully automated fulfillment centers using solids hot melts for speed and recyclability. The chemical sector centered in Rotterdam is another key driver, with specialty adhesive producers supplying formulations for semiconductor and life sciences equipment assembly requiring ultra-clean bonding. This unique blend of logistics intensity, chemical innovation, and circular policy makes the Netherlands a high-value and forward-looking market in the European adhesive ecosystem.

COMPETITIVE LANDSCAPE

The Europe adhesives and sealants market features a competitive landscape dominated by multinational chemical companies with strong innovation capabilities and regional manufacturing footprints. Competition is characterized by intense focus on product differentiation through performance, sustainability, and regulatory compliance rather than price alone. Leading firms continuously reformulate products to meet evolving standards such as REACH, EU Ecolabel, and Construction Products Regulation, driving significant R and D investment. The market sees steady consolidation as global players acquire specialty formulators to access advanced chemistries like MS polymers and reversible adhesives. At the same time, pressure from low-cost imports, particularly in the commodity segments, challenges smaller European producers to specialize in high-value applications. The rise of circular economy mandates is reshaping competitive dynamics, with companies racing to commercialize debondable and recyclable adhesive technologies. This environment rewards technical agility, regulatory foresight, and deep integration with end-user industries across automotive construction and packaging sectors.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe adhesives and sealants market include

- Sika AG

- B. Fuller Company

- 3M

- Arkema

- Henkel AG & Co. KGaA

TOP PLAYERS IN THE MARKET

- Henkel is a German multinational with deep roots in the European adhesives and sealants market through its Loctite and Technomelt brands. The company supplies advanced bonding solutions across automotive electronics, construction, and packaging sectors globally. In Europe, Henkel has intensified its focus on sustainable formulations, launching bio-based hot melts and low-emission construction sealants compliant with EU Ecolabel criteria. Recently, the company expanded its production capacity for structural adhesives at its facility in Heidelberg to support electric vehicle battery assembly for European OEMs. Henkel also established a dedicated circular economy lab in Düsseldorf to develop debondable adhesives that facilitate the recycling of multi-material products, aligning with EU regulatory trajectories.

- Sika, a Switzerland-based specialty chemical company, maintains a robust presence in the European adhesives and sealants landscape with a strong emphasis on construction and automotive applications. The company provides high-performance systems for façade bonding, concrete repair, and vehicle lightweighting worldwide. In recent years, Sika has reinforced its European footprint by opening a new R and D center in Stuttgart, focused on fire-resistant sealants for e-mobility and energy-efficient building envelopes. It also launched a suite of CO2-reduced adhesives using recycled raw materials in partnership with BASF, supporting Europe’s net-zero goals. Sika’s integration of digital tools for on-site adhesive performance monitoring further strengthens its service offering to contractors and OEMs across the region.

- Arkema, a French specialty materials producer, plays a pivotal role in the European adhesives and sealants market through its Bostik brand and high-performance polymer platforms. The company is a global leader in hot melt reactive sealants and sustainable bonding technologies, serving packaging, construction, and renewable energy sectors. It also introduced a range of MS polymer sealants for passive house construction certified under Passivhaus Institut standards. Arkema’s strategic collaboration with wind turbine manufacturers to develop epoxy-free bonding solutions for recyclable blades underscores its innovation focus aligned with Europe’s circular transition.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe adhesives and sealants market prioritize sustainability through the development of bio-based, low-VOC, and recyclable formulations to comply with stringent EU chemical regulations. They invest in vertical integration by securing renewable raw material supply chains and expanding production capacity for high-growth applications like electric vehicles and energy-efficient buildings. Strategic acquisitions of niche technology firms enable rapid entry into advanced segments such as debondable adhesives and fire-resistant sealants. Companies also enhance digital capabilities by integrating IoT and AI into adhesive dispensing and performance monitoring systems to deliver value-added services. Lastly, they strengthen regional presence through localized R and D centers focused on meeting country-specific construction and industrial standards across Europe.

MARKET SEGMENTATION

This research report on the Europe adhesives and sealants market has been segmented and sub-segmented into the following categories.

By Adhesive Resin

- Acrylic

- Cyanoacrylate

- Epoxy

- Polyurethane

- Silicone

- VAE / EVA

- Other Resins (Silane-Modified Polymer (SMP), Bio-based Resins, etc.)

By Adhesive Technology

- Hot-Melt

- Reactive

- Solvent-Borne

- UV-Cured

- Water-Borne

By Sealant Resin

- Polyurethane

- Epoxy

- Acrylic

- Silicone

- Other Resins (Polysulfide, SMP Hybrid, etc.)

By End-User Industry

- Aerospace

- Automotive

- Building and Construction

- Footwear and Leather

- Healthcare

- Packaging

- Woodworking and Joinery

- Other End-User Industries (Renewable Energy, Electronics and Appliances, etc.)

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the europe adhesives and sealants market?

Growth is driven by automotive, construction, and renovation demand, plus regulations pushing sustainable, high-performance adhesives in europe

2. Which sectors dominate the europe adhesives and sealants market?

Building and construction lead with nearly 40% market share, with strong contributions from automotive and aerospace sectors in europe

3. How do regulations impact the europe adhesives and sealants market?

EU rules like REACH and VOC limits encourage use of bio-based and low-emission adhesives, fueling innovation in the europe adhesives and sealants market

4. What technologies are common in the europe adhesives and sealants market?

Solvent-based, waterborne, UV-cured, and bio-based adhesives dominate technology choices in the europe adhesives and sealants market

5. Who are key players in the europe adhesives and sealants market?

Major companies include Henkel, Sika AG, Arkema, and Wacker Chemie, driving innovation and market growth in europe adhesives and sealants

6. Why is sustainable adhesive demand rising in the europe adhesives and sealants market?

Energy efficiency goals and environmental policies increase demand for bio-based, recyclable, and low-VOC products in europe adhesives and sealants market

7. How is renovation activity influencing the europe adhesives and sealants market?

The EU renovation wave is boosting demand for adhesives used in insulation, flooring, and window upgrades across europe

8. What role does automotive play in the europe adhesives and sealants market?

Lightweighting and performance enhancements in automotive manufacturing fuel adhesive and sealant demand in europe

9. What are bio-based adhesives in the europe adhesives and sealants market?

Bio-based adhesives use renewable raw materials, meeting europe’s sustainability criteria and reducing carbon footprints in the market

10. How significant is packaging in the europe adhesives and sealants market?

Packaging adhesives see growth from e-commerce and consumer product demand, contributing to the europe adhesives and sealants market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com