Europe Agrochemicals Market Size, Share, Trends And Growth Forecast Research Report, Segmented By Type, Application Type And Country (United Kingdom, France, Spain Germany And Italy, Russia, Sweden, Denmark, Switzerland, Netherlands And Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$45.43 BnMarket Estimate, 2026

$46.90 BnMarket Forecast, 2034

$60.53 BnCAGR, 2026–2034

3.24%Europe Agrochemicals Market Size

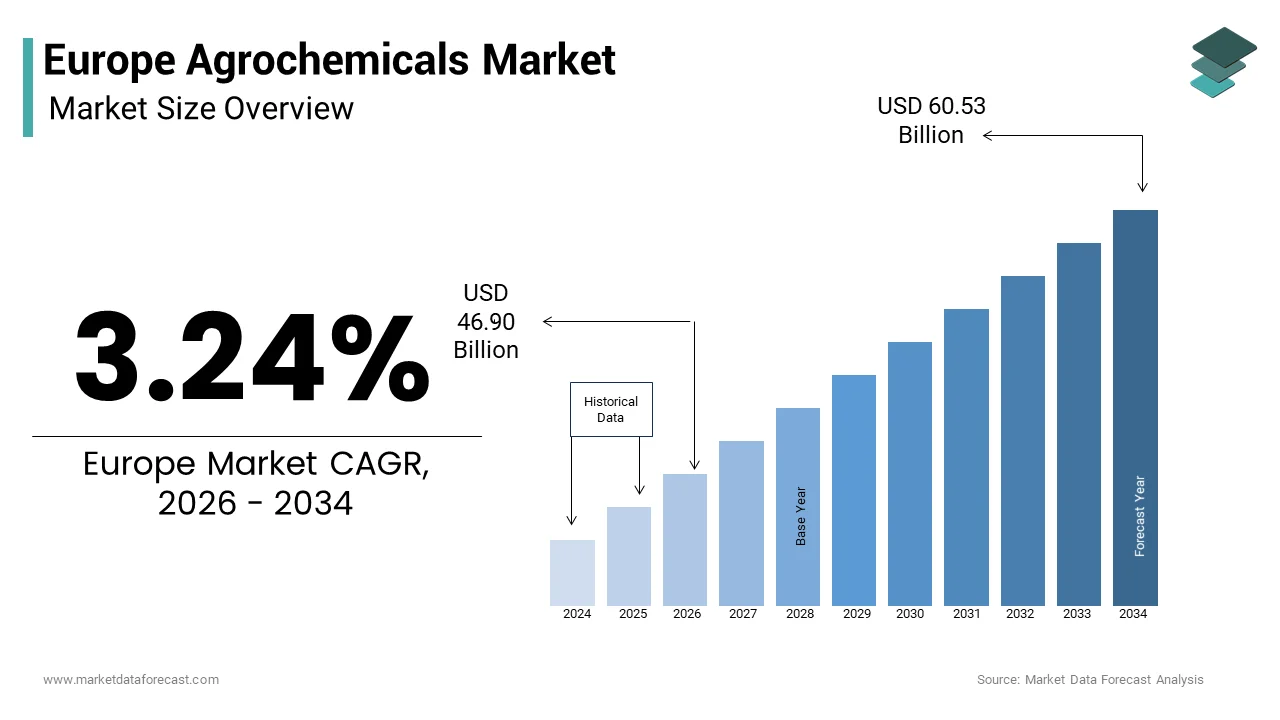

The European agrochemicals market size was valued at USD 45.43 billion in 2025 and is anticipated to reach USD 46.90 billion in 2026, and reach USD 60.53 billion by 2034, growing at a CAGR of 3.24% during the forecast period from 2026 to 2034.

The agrochemicals market is estimated to be one of the most crucial segments of agro-inputs, owing to the intensifying commercial farming of high-value crops to meet the growing diversified food demand. As such, agrochemicals are witnessing a significant demand since farmers are resolute in attaining nutritious and high-quality crop production.

The growth of the European agrochemicals market is majorly driven by factors such as a wide range of pest control applications of agrochemicals and decreasing arable land. This market is also propelled by factors such as meticulous research & partaking of intellectual property rights and increasing R&D investments.

However, issues such as strict regulatory structures in the EU and the toxicity of these substances towards the environment are the major restraints for the market growth in this region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.24% |

| Segments Covered | By Type, Application, And By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, & Rest of Europe |

| Market Leaders Profiled | Bayer Crop Science, Dow-DuPont, Syngenta AG, BASF SE, Agrium Inc., Monsanto Company, Israel Chemicals Ltd., Yara International ASA, Mosaic Company, and Sociedad Química Y Minera S.A. |

SEGMENT ANALYSIS

By Type Insights

Nitrogenous fertilizers lead the agrochemical market based on type. However, the demand for pesticides is increasing at a high rate, given the growing frequency of numerous pests and diseases. Currently, the pesticide market is being spearheaded by herbicide products, trailed by fungicides and insecticides.

By Application Insights

By application, grains & cereals lead the market for Agrochemicals, a nd this trend is anticipated to remain during the forecast period.

COUNTRY ANALYSIS

Demand for agrochemicals in Europe is estimated to grow at a sluggish rate, mainly due to market maturity and regulatory restrictions. However, the development of crops such as oilseeds and sugarcane is mainly anticipated due to the broadening applications, such as feed, fuel, and other industrial applications, which in turn drives the market in this region.

KEY MARKET PLAYERS

The market for agrochemicals is extremely consolidated and streamlined, owing to the domination of the market by a handful of companies. Some of the major companies dominating this market are

- Bayer Crop Science.

- Dow-DuPont

- Syngenta AG

- BASF SE

- Agrium Inc.

- Monsanto Company

- Israel Chemicals Ltd.

- Yara International ASA

- Mosaic Company

- Sociedad Química Y Minera S.A.

MARKET SEGMENTATION

This research report on the European agrochemicals market is segmented and sub-segmented into the following categories

By Type

- Fertilizers

- Nitrogenous

- Phosphate

- and Potassic

- Pesticides

- organophosphates

- pyrethroids

- biopesticides

- Plant Growth Regulators

- Auxins

- Cytokinins

- Adjuvants

- Activator Adjuvants

- Utility Adjuvants

By Application

- Crop Based

- Oil seeds

- Fruits & Vegetables

- Grains & Cereals

- Non-Crop Based

- Turf & Ornamental Grass

- others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe agrochemicals market?

It refers to the regional industry focused on crop protection products and agricultural chemicals used to enhance yield, control pests, and improve farm productivity.

What products are included in agrochemicals?

Fertilizers, herbicides, insecticides, fungicides, and plant growth regulators are the primary categories within the agrochemicals market.

What factors are driving growth in the Europe agrochemicals market?

Increasing food demand, limited arable land, and the need for higher agricultural efficiency are key growth drivers.

Why are crop protection chemicals important for European farmers?

They help minimize crop losses caused by weeds, pests, and diseases while ensuring consistent agricultural output.

How do environmental regulations influence agrochemical usage in Europe?

Strict EU policies encourage safer formulations, reduced chemical residues, and sustainable application practices.

Are biological and eco-friendly agrochemicals gaining adoption?

Yes, farmers are increasingly adopting bio-based and low-toxicity solutions aligned with sustainable farming goals.

Which crops contribute most to agrochemical demand?

Cereals, oilseeds, fruits, vegetables, and specialty crops generate significant agrochemical consumption.

How does climate variability affect agrochemical demand?

Changing weather patterns increase pest pressure and disease outbreaks, raising the need for effective crop protection solutions.

What role does precision agriculture play in agrochemical application?

Digital farming tools help optimize dosage and timing, reducing waste and improving environmental efficiency.

How are farmers balancing productivity with sustainability?

Integrated pest management and targeted chemical use help maintain yields while reducing ecological impact.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com