Europe Agricultural Adjuvants Market Size, Share, Growth, Trends, And Forecast Report, Segmented By Application, Type, Crop Type, And By Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Agricultural Adjuvants Market Size

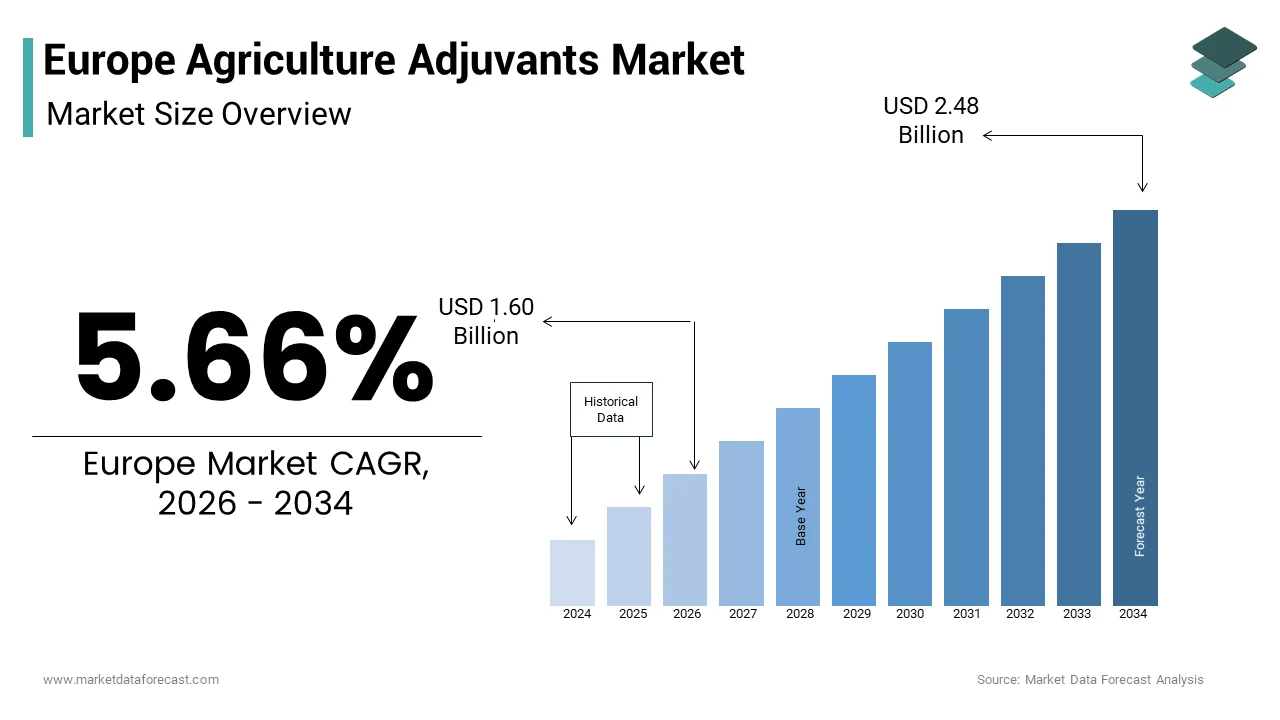

Europe's agricultural adjuvants market size was valued at USD 1.51 billion in 2025 and is anticipated to reach USD 1.60 billion in 2026 to reach USD 2.48 billion by 2034, growing at a CAGR of 5.66% during the forecast period from 2026 to 2034.

Agricultural adjuvants are specialized chemical or biological additives incorporated into pesticide tank mixes to enhance the efficacy, stability, or delivery of active ingredients without possessing intrinsic pesticidal properties themselves. In Europe, these include surfactants, spreaders, stickers, penetrants, and drift reduction agents that optimize spray deposition and foliar uptake under diverse climatic and crop conditions. Their use is increasingly vital as the European Union intensifies restrictions on synthetic pesticide volumes under the Sustainable Use Regulation while maintaining high yield expectations. According to Eurostat, the EU's total Utilised Agricultural Area (UAA) was approximately 157.4 million hectares in 2020, with arable land accounting for the majority (62.3% or 98.1 million hectares). As per research, a portion of field crop protection programs in some of the European countries involve tank-mixed sprays where adjuvant inclusion significantly improves performance consistency. As per the European Commission's Farm to Fork Strategy, the targets are to reduce the use and risk of chemical pesticides and the use of more hazardous pesticides by 50% by 2030, which encourages growers to maximize efficiency per application. This regulatory and agronomic context positions adjuvants not as optional additives but as essential enablers of precision and sustainability in modern European agriculture.

MARKET DRIVERS

Regulatory Pressure to Reduce Pesticide Volumes

Stringent EU policies mandating significant reductions in pesticide use are a primary driver for the growth of the Europe agricultural adjuvants market. According to the European Environment Agency, a directive affects numerous approved active substances currently applied across significant areas of arable land. In response, farmers are turning to adjuvants to enhance the biological activity and foliar retention of reduced dose applications. As per the trials in Germany by the Julius Kühn Institute, using a non-ionic surfactant with less glyphosate provided weed control comparable to a full glyphosate dose alone. Similarly, adjuvants designed to reduce drift can significantly cut down on off-target spray movement, allowing for compliant application near sensitive areas, according to research. Adjuvants are now indispensable for farmers in nations such as the Netherlands and Denmark, where national action plans enforce strict pesticide quotas, which serve as key tools for upholding efficacy, respecting legal limits, and preventing financial penalties.

Expansion of Precision and Low Volume Spraying Technologies

The widespread adoption of precision agriculture equipment in the region is increasing demand for performance-enhancing adjuvants tailored to low-volume and ultra-low volume spray systems, which further accelerates the expansion of the Europe agricultural adjuvants market. According to research, there is a clear trend towards the adoption of advanced spraying technologies such as variable rate application (VRA) and air-assisted nozzles in the EU agricultural sector, driven by a desire to minimize chemical usage and enhance sustainability. These advanced systems often operate at reduced water volumes, typically in the low-volume range of 50-150 liters per hectare, which requires the use of specific adjuvants to ensure uniform droplet size, rapid wetting, and anti-evaporation properties. In response, major adjuvant manufacturers have developed polymer-based stickers and humectant blends that maintain droplet integrity under high wind and solar exposure conditions common in Southern Europe. The EU’s Common Agricultural Policy also allocates funding under its eco schemes for farmers investing in precision technologies, creating a synergistic incentive to adopt both hardware and compatible adjuvants. This technological shift transforms adjuvants from passive additives into active components of digital and sustainable farming ecosystems.

MARKET RESTRAINTS

Complex and Fragmented Regulatory Approval Frameworks

The absence of a unified regulatory pathway for adjuvants across European member states creates significant barriers to product registration and commercialization, and thereby brings down the growth rate of the Europe agricultural adjuvants market. Unlike active pesticide ingredients, which undergo centralized evaluation by the European Food Safety Authority, adjuvants are regulated inconsistently, classified as co-formulants in some countries and as standalone additives in others. According to a study, only a few EU member states maintain explicit national guidelines for adjuvant approval, while others defer to vague interpretations of the Biocidal Products Regulation or REACH. This fragmentation forces manufacturers to navigate separate dossiers with varying toxicological data requirements, causing approval timelines to be several months in countries like Italy and Poland. The resulting uncertainty discourages innovation and limits farmer access to advanced formulations, particularly in Eastern Europe, where regulatory capacity is limited. The market will stay inefficient and fragmented so long as harmonization efforts are incomplete.

Limited Awareness and Technical Knowledge Among End Users

A substantial knowledge gap persists among European farmers regarding the proper selection and use of these adjuvants, which is also an obstacle to the Europe agricultural adjuvants market. According to research, only a percentage of small and medium-scale farmers in the EU could correctly identify the function of common adjuvant types such as non-ionic surfactants or ammonium sulfate-based water conditioners. This lack of understanding often leads to suboptimal tank mixing, either omitting adjuvants entirely or combining incompatible products that reduce efficacy or cause phytotoxicity. Extension services in some European countries report that spray failure cases stem from incorrect adjuvant usage rather than active ingredient resistance. Language barriers and limited access to agronomic advisors in rural regions further exacerbate the problem. Adjuvant compatibility data provided by major agrochemical companies is difficult to use locally due to language and regional applicability gaps. The complete potential of adjuvants to aid sustainable intensification in European agriculture can only be achieved through coordinated education initiatives, specifically those funded by EU rural development programs.

MARKET OPPORTUNITIES

Development of Bio-based and Biodegradable Adjuvant Formulations

The emergence of bio-based adjuvants derived from plant oils, sugars, and microbial metabolites is aligned with the region’s green transition goals and provides an opportunity for the growth of the Europe agricultural adjuvants market. Driven by the EU’s Chemicals Strategy for Sustainability, which aims to eliminate persistent and bioaccumulative substances from agricultural use, companies are investing in rapidly biodegradable alternatives. Companies like Evonik and Croda have launched certified bio-based adjuvant lines compliant with EU Ecolabel standards. The increasing popularity of organic farming suggests a significant rise in demand for ecologically benign aOMRI-listed adjuvants, which fosters a premium market segment where efficacy meets environmental care.

Integration with Digital Farming and Spray Decision Support Systems

The convergence of adjuvant use with digital agronomy platforms offers a major opportunity for the expansion of the Europe agricultural adjuvants market. This integration helps to optimize application timing and formulation selection in real time. Modern farm management software, such as that developed by BASF’s xarvio and Bayer’s Climate FieldView, incorporates adjuvant recommendation engines that analyze wheat, herb, soil moisture a,, nd crop stage data to prescribe optimal tank mix compositions. These systems also log compliance documentation required under national pesticide registries, easing administrative burdens. The EU's promotion of digitalization via CAP Strategic Plans is driving greater funding opportunities for farms implementing integrated decision support tools and precision application hardware. This digital ecosystem transforms adjuvants from static inputs into dynamic variables within data-driven crop protection strategies, enhancing both economic returns and environmental compliance across diverse European growing regions.

MARKET CHALLENGES

Volatility in Raw Material Supply Chains for Synthetic Adjuvants

Supply chain instability driven by energy policy shifts and geopolitical disruptions remains an impediment to the Europe agricultural adjuvants market. The reliance of conventional adjuvant formulations on petrochemical derivatives exposes the European market to significant supply chain instability. Key raw materials such as ethoxylated alcohols and alkylphenol ethoxylates are sourced from refineries in Germany, Belgium, and the Netherlands, which faced production cuts during the 2022 to 2024 energy crisis. According to sources, ethylene oxide, a critical precursor of non-ionic surfactants, experienced price volatility between 2022 and 2023 due to natural gas shortages. This directly impacted adjuvant manufacturers who saw input costs surge without the ability to pass full increases to price-sensitive farmers. As a result, companies have struggled to maintain consistent product availability, particularly in Southern Europe, where smaller distributors lack inventory buffers. The adjuvant industry's formulation consistency and pricing stability will remain susceptible to energy and macroeconomic fluctuations until bio-based alternatives are widely available or regional green hydrogen-based chemical production is established.

Inconsistent Efficacy Data and Lack of Standardized Testing Protocols

The absence of harmonized efficacy evaluation methods for these adjuvants in the region affects grower confidence, impedes scientific validation, and thereby hampers the expansion of the Europe agricultural adjuvants market. Unlike active ingredients, which undergo standardized bioassays under OECD guidelines, adjuvants are tested using diverse methodologies that vary by crop region and application technique. The lack of standardization makes it difficult for extension services to issue reliable recommendations and for regulators to evaluate claims. In countries like Hungary and Bulgaria, farmers often rely on anecdotal evidence, leading to misuse or abandonment after a single trial failure. The absence of universally accepted protocols threatens to polarize the market: large farms may access scientifically backed products, while smallholders rely on unverified offerings, which ultimately hinders the adoption of best practices across the agricultural sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.66% |

| Segments Covered | By Application, Type, Crop Type & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | AkzoNobel N.V., Adjuvant Plus Inc., Clariant International Ltd., Solvay SA, Helena Chemical Company, and Tanatex Chemicals. |

SEGMENTAL ANALYSIS

By Application Insights

In 2024, the herbicides segment remained prominent in the Europe agricultural adjuvants market and held a 42.6% share. Widespread weed pressure in major arable systems and regulatory mandates to maximize herbicide efficiency under reduced dosage regimes have mainly contributed to the prominence of the herbicides segment. According to Eurostat statistics, approximately 98.1 million hectares of EU land were used as arable land in 2020, with cereals and oilseeds being the major crops. As per research, including studies from institutions like the Julius Kühn Institute, the inclusion of non-ionic surfactants improves the efficacy and absorption of herbicides in general, which is a known principle in application technology to optimize performance. Additionally, the EU’s Sustainable Use Regulation prohibits broadcast spraying near waterways unless drift reduction adjuvants are used. Adjuvants are now non-optional in Europe's intensive cropping belts, as effective weed management relies entirely on maximizing herbicide deposition and penetration.

The fungicide application segment is predicted to witness the highest CAGR of 6.8% from 2025 to 2033. The expansion of the fungicide application segment is driven by rising fungal disease pressure linked to climate change and the expansion of high-value horticulture. According to sources, growing seasons in Southern and Central Europe are increasingly warm and humid, creating conditions suitable for plant pathogens. In response, growers are adopting adjuvants that enhance systemic movement and rainfastness of strobilurin and triazole fungicides. As per studies, additives containing organosilicone help fungicides work more effectively on waxy fruit surfaces. The EU’s approval of biofungicides, which often suffer from poor leaf adhesion, has further amplified demand for bio-compatible stickers and penetrants. The expansion of organic fruit and vegetable farming is fostering innovation in products that support biological pest control methods.

By Type Insights

The surfactants segment led the Europe agricultural adjuvants market by capturing a substantial share in 2024. Its fundamental role in reducing surface tension, improving droplet spreading, and enhancing active ingredient penetration across diverse crop protection sprays has fuelled the growth of the surfactants segment. Non-ionic and organosilicone surfactants are particularly critical in herbicide and fungicide tank mixes where waxy or hairy leaf surfaces impede uptake. Their dominance is also supported by compatibility with low-volume spraying systems now used on many large farms in Germany, France, and the Netherlands. Apart from these, surfactants are essential for enabling reduced-dose applications mandated under the Farm to Fork Strategy. Regulatory clarity under REACH also supports their continued use, unlike certain oil-based alternatives facing scrutiny.

The oil adjuvants segment is estimated to register the fastest CAGR of 7.4% over the forecast period, owing to factors such as the shift toward biopesticides and systemic herbicide programs, which require enhanced cuticle penetration. Methylated seed oils and crop oil concentrates improve the uptake of poorly soluble active ingredients, particularly hard-to-wet crops like cereals and legumes. The segment is also gaining traction in organic systems where plant-derived oils like rapeseed and olive oil meet OMRI and EU organic regulation criteria. As per sources, bio-based oil adjuvant production rose with facilities scaling output to meet demand. Furthermore, oil adjuvants offer superior anti-evaporation properties in Mediterranean climates, vital as summer spraying windows narrow due to heat restrictions. Their dual role in efficacy and environmental compliance positions them for sustained expansion.

By Crop Insights

The cereals and oilseeds segment held the leading share of 54.1% of the Europe agricultural adjuvants market in 2024. Their dominance in EU arable land use and high reliance on chemical weed and disease control are among the key factors propelling the growth of the cereals and oilseeds segment. Large-scale mechanized farming in the North European Plain, from eastern France through Germany to Poland, relies on efficient herbicide applications where adjuvants are mandatory to manage resistant weed populations like Alopecurus myosuroides. The European Food Safety Authority lists adjuvant inclusion as a condition for approving many post-emergence herbicides in cereal systems. Adjuvant use is now an embedded part of standardized spray protocols across the bloc’s grain heartland, ensuring consistent volume demand due to average farm sizes exceeding significant hectares in key producing regions.

The fruits and vegetables segment is anticipated to witness the fastest CAGR of 8.1% from 2025 to 2033. The swift expansion of the fruits and vegetables segment is propelled by the expansion of high-value protected cropping and stringent residue limits that necessitate precise and efficient pesticide delivery. Adjuvants that enhance rainfastness and reduce runoff, such as polymer-based stickers, are now standard in vineyards, olive groves, and berry farms. Besides, the organic fruit and vegetable sector, which grew in 20,24, now covers large hectares requiring biocompatible adjuvants or copper and sulfur sprays. The economic premium on quality and compliance ensures sustained adjuvant innovation in this high-margin segment.

COUNTRY ANALYSIS

France Agricultural Adjuvants Market Analysis

France dominated the Europe agricultural adjuvants market by accounting for a 24.7% share in 2024. Its vast arable expanse, intensive crop protection practices, and proactive regulatory enforcement have mainly contributed to the strong demand for agricultural adjuvants in France. The country cultivates millions of hectares of cereals and vineyards, which makes it the EU’s top agricultural producer by value. The country’s strong cooperative farming network, represented by groups like InVivo, facilitates the rapid dissemination of adjuvant best practices through agronomic advisors. Apart from these, France’s leadership in viticulture creates a unique demand for drift control and rainfastness adjuvants in sensitive regions. Public investment in digital spraying tools under the France 2030 plan further integrates adjuvants into precision agriculture workflows, solidifying the nation’s dominant role.

Germany Agricultural Adjuvants Market Analysis

Germany was the next-biggest player in the Europe agricultural adjuvants market by capturing a share of 18.3% in 2024. The German market for agricultural adjuvants is propelled by its advanced farming infrastructure, strict environmental regulations, and command in agrochemical innovation. The Julius Kühn Institute regularly publishes adjuvant efficacy data that informs both farmer decisions and Bayer and BASF product recommendations. Germany’s average farm size of 63 hectares enables cost-effective adoption of low-volume spraying systems that depend on high-performance adjuvants. Furthermore, the country mandates spray drift reduction for all field applications, which has institutionalized the use of polymer-based adjuvants in both conventional and organic sectors. This regulatory and technical ecosystem ensures consistent science-driven adjuvant utilization across German agriculture.

Spain Agricultural Adjuvants Market Analysis

Spain has been noted for experiencing rapid growth in the Europe agricultural adjuvants market, which continues to be driven by its Mediterranean cropping systems, high pest pressure, and leadership in horticultural exports. According to sources, the country produces millions of tons of fruits and vegetables annually, with intensive cultivation in regions like Almería and Murcia covering hectares of greenhouses. The hot arid climate accelerates droplet evaporation, necessitating humectant and anti-desiccant adjuvants to maintain spray efficacy. Additionally, Spain faces increasing resistance in key weeds like Lolium rigidum, um prompting adjuvant inclusion post-emergence herbicide programs for olive and almond orchards. The National Rural Development Programme allocates funding for precision spraying equipment, which inherently requires compatible adjuvants. Spain is expected to rely more heavily on adjuvant-optimized sprays in both open field and protected agriculture as climate change worsens water stress and disease outbreaks.

Italy Agricultural Adjuvants Market Analysis

Italy showed moderate growth in the Europe agricultural adjuvants market. This is due to its diverse cropping systems, which include vineyards, olive groves, and cereal belts that require customized spray solutions. Italy cultivates significant areas of vineyards and olive trees, which traditionally require pest management. The country is implementing stricter rules for pesticide use, including buffer zones near residential areas. Farmers increasingly use drift reduction adjuvants and Integrated Pest Management. Cooperatives support small farms by bundling services and providing recommendations. As per research, improving treatment efficacy allows for lower doses, supporting EU sustainability goals. Italy's organic farming sector is growing, with a notable increase in the area dedicated to these practices. Its dual focus on premium quality and regulatory compliance ensures steady adjuvant adoption across its complex agricultural landscape.

The Netherlands Agricultural Adjuvants Market Analysis

The Netherlands is likely to expand in the Europe agricultural adjuvants market from 2025 to 2033, owing to its globally integrated horticulture sector, precision farming leadership, and stringent environmental governance. The national authorization system requires adjuvant compatibility data for all new pesticide registrations, ensuring science-based adoption. Wageningen University and Research collaborate with companies to develop adjuvants that improve biopesticide rainfastness in high-humidity greenhouse environments. Dutch growers routinely use sensor-based sprayers that adjust adjuvant concentration in real time based on crop canopy density. This data-driven approach, combined with the economic imperative to protect export quality, makes the Netherlands a high-intensity adjuvant market despite its modest land area.

COMPETITIVE LANDSCAPE

The Europe agricultural adjuvants market features a competitive landscape defined by a mix of multinational chemical companies, specialty ingredient suppliers, and regional formulators. Competition is increasingly centered on sustainability performance and regulatory agility rather than price alone. Global players like BASF and Evonik leverage integrated R&D and manufacturing to offer scientifically validated adjuvants that meet stringent EU safety and biodegradability criteria. Meanwhile, niche firms focus on bio-based or organic certified solutions catering to the fast-growing horticultural and organic sectors. The absence of harmonized efficacy testing standards creates opportunities for companies that provide field trial data and extension support to build grower trust. Regulatory complexity under REACH and national pesticide laws acts as a barrier to entry, favoring established firms with compliance expertise. As the EU accelerates its transition toward reduced risk crop protection,n, competition is intensifying around innovation in green chemistry, digital integration, ion and application efficiency, with leading companies positioning adjuvants as essential enablers of precision and sustainable agriculture.

KEY MARKET PLAYERS

The major companies dominating the Agricultural Adjuvants market in this region are

- AkzoNobel N.V.

- BASF SE

- Evonik Industries AG

- Adjuvant Plus Inc.

- Clariant International Ltd.

- Solvay SA

- Helena Chemical Company

- Tanatex Chemicals.

Top Players In The Market

- BASF SE is a global chemical leader with deep integration in the European agricultural adjuvants market through its Crop Protection division. The company develops a comprehensive portfolio of surfactants and oil-based adjuvants designed to enhance the performance of its herbicides, fungicides, and insecticides while supporting EU sustainability mandates. BASF leverages its in-house R&D facilities in LLLimburgerhofe, Germany formulate adjuvants compatible with low-dose and biopesticide applications. Recently, the company launched a new line of biodegradable adjuvants derived from renewable feedstocks certified under EU Ecolabel standards. It also expanded digital advisory tools that recommend adjuvant use based on real-time weather and crop data across its Xarvio platform, strengthening farmer engagement and product stickiness in Western and Central Europe.

- Evonik Industries AG is a Germany-based specialty chemicals company recognized for its advanced adjuvant technologies centered on high-performance surfactants and formulation additives. The company supplies key raw materials and proprietary blends to both agrochemical majors and independent formulators across Europe. Evonik’s TEGO portfolio includes organosilicone and non-ionic surfactants engineered for optimal spray retention and systemic uptake under EU regulatory constraints. It also partnered with agricultural universities to validate adjuvant efficacy in resistant weed scenarios. These initiatives reinforce Evonik’s role as an innovation enabler rather than a direct brand marketer in the European adjuvant value chain.

- Croda International Plc is a UK-headquartered specialty ingredients company that has strategically expanded its presence in the European agricultural adjuvants market through sustainable chemistry. The company’s Crop Care division offers a range of bio-based adjuvants, including methylated seed oils and ethoxylated plant sterols, designed for compatibility with biologicals and reduced risk chemistries. Croda emphasizes green chemistry principles, aligning with the EU’s Chemicals Strategy for Sustainability. It also enhanced its regulatory support services to assist customers with EU MRL and REACH compliance, strengthening its position as a trusted partner for eco-conscious crop protection solutions.

Top Strategies Used By The Key Market Participants

Key players in the Europe agricultural adjuvants market prioritize the development of bio-based and readily biodegradable formulations to align with EU environmental regulations and consumer demand for sustainable farming. Companies invest in R&D to enhance adjuvant compatibility with low-dose pesticides and biologicals, enabling compliance with Farm to Fork reduction targets. Strategic partnerships with agrochemical firms and cooperatives facilitate bundled product offerings and technical support. Firms also integrate adjuvant recommendations into digital farming platforms, providing real-time application guidance based on weather and crop conditions. Regulatory compliance services, including dossier preparation for national approvals, are offered to ease market entry. Additionally, manufacturers expand production capacity for renewable feedstock-based adjuvants in Western Europe to secure supply chains and reduce carbon footprints. These strategies collectively drive adoption while reinforcing regulatory and ecological credibility.

RECENT MARKET NEWS

- In February 202,4, BASF SE introduced its new Lutrol SmartAdjuvant line, a series of bio-based surfactants derived from European rapeseed oil, designed to enhance systemic herbicide uptake while meeting EU Ecolabel biodegradability requirements.

- In October 2023, Evonik Industries AG completed a 20 million euro expansion of its surfactant production unit in Marl, Germany, to increase capacity for TEGO adjuvant formulations used in low-volume spraying systems across Western Europe.

- In May 2024, Croda International Plc launched Ecotrol Plus, an OMRI-listed methylated seed oil adjuvant specifically formulated for organic fruit and vegetable growers in Spain, Italy, and the Netherlands to improve copper fungicide rainfastness.

- In August 2023, BASF integrated adjuvant recommendation algorithms into its xarvio FIELD MANAGER platform, enabling real-time digital guidance for farmers applying herbicides under EU Sustainable Use Regulation constraints.

- In January 2024, Evonik partnered with Wageningen University to publish a multi-country field trial validating the efficacy of its organosilicone adjuvants in reducing glyphosate application rates by 30 percent while maintaining weed control in cereal systems across Germany, France, and Poland.

MARKET SEGMENTATION

This research report on the Europe agricultural adjuvants Market is segmented and sub-segmented into the following categories..

By AApplicationion

- Insecticides

- Herbicides

- Fungicides

- Others

By Type

- Surfactants

- Oil Adjuvants

By Crop Type

- Fruits & Vegetables

- Cereals & Oilseeds

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is driving growth in the Europe Agricultural Adjuvants Market?

The Europe Agricultural Adjuvants Market is expanding due to EU pesticide-use reduction targets (−50% by 2030), rising resistance in weeds/pests, and the need to maximize efficacy of lower-dose, bio-based, and precision-applied products.

How is the Sustainable Use of Pesticides Regulation (SUR) affecting the Europe Agricultural Adjuvants Market?

The proposed SUR (though delayed in 2024) is accelerating demand for performance-enhancing adjuvants—such as drift reducers, penetrants, and tank-mix stabilizers—that help farmers achieve results with less active ingredient in the Europe Agricultural Adjuvants Market.

Which adjuvant types are gaining the most traction?

Non-ionic surfactants (NIS), crop oil concentrates (COC), and anti-foaming/anti-drift polymers lead—especially in herbicide programs for cereals and oilseed rape, where efficacy under low-dose regimes is critical in the Europe Agricultural Adjuvants Market.

Are bio-based adjuvants replacing synthetic ones?

Gradually—plant-derived surfactants (e.g., from rapeseed, sugar beet) and lecithin-based formulations are growing in organic and IPM-certified systems, though performance consistency and cost remain hurdles in the Europe Agricultural Adjuvants Market.

Which countries lead adoption in the Europe Agricultural Adjuvants Market?

France, Germany, Spain, and Italy—where intensive arable and viticulture systems face high pest pressure and strict local restrictions (e.g., dérogations in France)—drive >60% of regional demand in the Europe Agricultural Adjuvants Market.

How do tank-mix compatibility issues influence product choice?

With complex multi-product sprays common (fungicide + insecticide + biostimulant), farmers increasingly select universal adjuvants with pH buffering and suspension properties—making formulation science a key differentiator in the Europe Agricultural Adjuvants Market.

Is there regulatory scrutiny on adjuvant safety?

Yes—while adjuvants themselves aren’t approved as active substances, EFSA now evaluates their impact on toxicity and environmental fate during pesticide dossier reviews, raising compliance burdens in the Europe Agricultural Adjuvants Market.

Are adjuvant suppliers integrating with digital agronomy tools?

Leading players (e.g., Nufarm, Syngenta, Brandt) now offer adjuvant recommendations via spray-app decision engines—linking weather, water hardness, and crop stage to optimize performance in the Europe Agricultural Adjuvants Market.

What role do co-formulated products play?

Pre-mixed formulations (active + adjuvant) are rising—reducing user error and ensuring consistent performance, especially for biopesticides with stability challenges in the Europe Agricultural Adjuvants Market.

What’s the outlook for the Europe Agricultural Adjuvants Market through 2030?

Strong growth (CAGR ~6–8%) is expected, as adjuvants become indispensable “force multipliers” in low-input, high-efficiency farming—positioning them as enablers, not additives, in Europe’s sustainable agriculture transition.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com