Europe Application Security Market Size, Share, Trends & Growth Forecast Report By Deployment, Type, Enterprise Type, End User, and By Country (Germany, France, United Kingdom, Italy, Spain & Rest of Europe) – Industry Analysis and Forecast, 2025 to 2033

Europe Application Security Market Summary

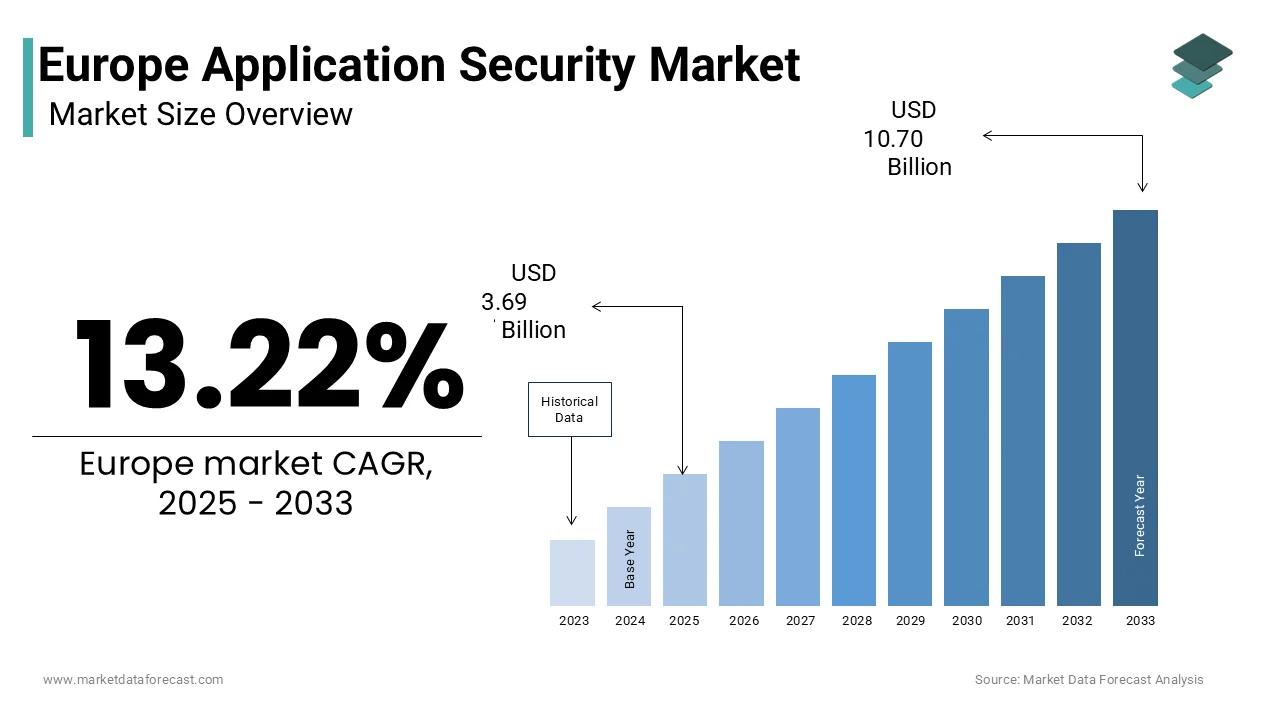

Europe application security market was valued at USD 3.50 billion in 2024, is estimated to reach USD 3.69 billion in 2025, and is projected to reach USD 10.70 billion by 2033, growing at a CAGR of 13.22% from 2025 to 2033, driven by enforcement of the EU Cyber Resilience Act and NIS2 Directive, rapid expansion of cloud-native and API-driven applications, rising application-layer cyberattacks, and mandatory secure-by-design software requirements across critical sectors.

Market Highlights

- 2024 value: USD 3.50 billion

- 2025 (est): USD 3.69 billion

- 2033 forecast: USD 10.70 billion

- CAGR (2025–2033): 13.22%

Quick growth drivers

- Enforcement of the EU Cyber Resilience Act and NIS2 Directive mandating secure development, SBOMs, and vulnerability disclosure.

- Accelerated adoption of cloud-native, microservices, and API-centric architectures expanding the application attack surface.

- Rising frequency of application-layer breaches involving insecure APIs and third-party components.

- Mandatory DevSecOps integration across BFSI, healthcare, and public sector software procurement.

- Rapid growth of digital public services, fintech, and e-government platforms across Europe.

Principal restraints

- Acute shortage of skilled application security and DevSecOps professionals across EU member states.

- Fragmented security tooling leading to alert fatigue and poor interoperability.

- High operational burden of multi-tool integration within CI/CD pipelines.

- Limited security maturity among SMEs despite regulatory trickle-down.

High-value opportunities

- Adoption of AI-driven vulnerability prioritization and autonomous remediation platforms.

- Expansion of secure software development academies and developer certification programs.

- Growth of cloud-based, subscription-driven application security platforms for SMEs.

- Public–private partnerships supporting secure-by-design software ecosystems.

Key operational challenges

- Escalating API and software supply-chain attacks exploiting third-party dependencies.

- Difficulty maintaining continuous SBOM visibility across transitive dependencies.

- Legal ambiguity around cross-border liability and incident reporting timelines.

- Balancing development speed with mandatory security controls under EU regulations.

Fastest-growing segments

- Mobile application security: 16.06% CAGR — mobile banking, telehealth, digital therapeutics.

- SMEs (enterprise type): 17.7% CAGR — regulatory pressure + affordable cloud tools.

- Healthcare (end user): 18.4% CAGR — EHRs, telemedicine, connected health apps.

- Cloud deployment: dominant (68.5% share in 2024).

Regional leadership & dynamics

- Germany (25.8% share): strict compliance enforcement, strong industrial and BFSI demand.

- France: public sector digitization and national cybersecurity mandates.

- United Kingdom: fintech-driven demand and mature cloud security adoption.

- Italy & Spain: fast-growing adoption across government, healthcare, and manufacturing.

What wins commercially

- Regulation-ready platforms aligned with Cyber Resilience Act and NIS2.

- Deep CI/CD and developer-tool integrations enabling frictionless security.

- AI-powered remediation reducing false positives and MTTR.

- EU-based data residency and compliance assurance for public sector and BFSI clients.

Top strategic ask for executives

Invest in AI-driven DevSecOps platforms, expand secure-coding talent pipelines, strengthen SBOM and supply-chain visibility, and align product roadmaps tightly with EU cybersecurity legislation to secure long-term market leadership.

Leading players

Synopsys · Checkmarx · Veracode · Fortify (OpenText) · Qualys · Rapid7 · IBM · Cisco · Palo Alto Networks · CrowdStrike · Snyk · GitLab · Salt Security

Europe Application Security Market Size

The Europe application security market was valued at USD 3.50 billion in 2024, is estimated to reach USD 3.69 billion in 2025, and is projected to grow to USD 10.70 billion by 2033, registering a CAGR of 13.22% from 2025 to 2033.

Application security includes technologies, processes,s and services designed to protect software applications from vulnerabilities, threats, and data breaches throughout their development and operational lifecycle. This includes static and dynamic analysis, software composition assessment, penetration testing, and runtime protection mechanisms embedded within web, mobile, e-commerce, and cloud native applications. The market is fundamentally shaped by Europe’s stringent regulatory environment and the digitalization of critical services. According to the European Union Agency for Cybersecurityapplication-layerer exploits such as injection flaws, insecure APIs, and misconfigured third-party components remain among the leading causes of cyber incidents reported by essential entities in 2024. As per the European Commission, the Cyber Resilience Act mandates that all software placed on the EU market from 2025 must undergo security testing, vulnerability disclosure, and software bill of materials documentation, reinforcing compliance obligations. Furthermore, data from the European Banking Federation highlights that financial institutions manage extensive API ecosystems, often numbering in the thousands per institution, which indicates the scale of the attack surface. This convergence of regulatory mandates, persistent application-layer vulnerabilities, and expansive API usage justifies application security as both a legal requirement and an operational imperative across public and private sectors.

MARKET DRIVERS

Enactment of the EU Cyber Resilience Act and NIS2 Directive

The introduction of the EU Cyber Resilience Act and the revised NIS2 Directive has become the most significant regulatory catalyst for application security adoption across European enterprises and software vendors, which is primarily driving the application security market growth in Europe. As per the European Commission, all developers placing software on the EU market from 2025 must implement secure development practices, provide a software bill of materials, and establish vulnerability handling processes. According to the European Union Agency for Cybersecurity, 72% of critical infrastructure operators reported at least one application-level breach in 2023, with 68% linked to unpatched open-source libraries or insecure APIs. The Cyber Resilience Act imposes direct legal liability on manufacturers for security flaws, making secure coding and continuous testing non-discretionary. In response,e Germany’s Federal Office for Information Security now requires all public sector software suppliers to submit an attestation of static and dynamic application security testing. This regulatory shift transforms application security from a best practice into a binding requirement for market access and legal compliance across the European digital economy.

Accelerated Adoption of Cloud Native and API Driven Architectures

The rapid transition to microservices, serverless functions,s and API centric application design has exponentially expanded the attack surface, requiring embedded security controls throughout the software lifecycle, which is further boosting the expansion of the European application security market. According to Eurostat, 87% of EU enterprises used cloud computing services in 2024, with over 75% deploying customer-facing applications in public or hybrid environments. As per the European Cloud Partnership, containerized application deployments grew by 48% year on year in 2023, increasing dependency on third-party libraries and interconnected services. The European Banking Authority reports that financial institutions manage an average of 1,200 APIs each, making them prime targets for broken object-level authorization and excessive data exposure. This architectural complexity outpaces traditional perimeter defenses, necessitating integrated security within DevOps pipelines. Consequently, 71% of large European enterprises now embed automated scanning tools in their CI/CD workflows as noted by the European Institute of Innovation and Technology, ensuring that security scales with development velocity rather than impedes it.

MARKET RESTRAINTS

Acute Shortage of Skilled Application Security Professionals

A critical deficit of cybersecurity talent with specialized expertise in secure coding,g penetration testing, ng and DevSecOps significantly constrains effective implementation across European organizations, which is impeding the European application security market growth. According to the European Union Agency for Cybersecurity, Europe faces a shortfall of over 320,000 cybersecurity professionals, with less than 18% possessing advanced application security competencies. As per the European Centre for the Development of Vocational Training, only 14 EU member states offer formal certification pathways in application security, leading to inconsistent skill levels. In Southern and Eastern Europe, the gap is more acute, with 68% of IT teams lacking dedicated application security roles, relying instead on overburdened network security staff. This shortage delays vulnerability remediation, with the average time to fix critical flaws in web applications exceeding 70 days according to a study by ENISA. Without urgent investment in education, upskilling, and automation, Europe’s regulatory ambitions for secure software will remain hampered by operational incapacity despite strong policy intent.

Fragmentation of Security Tooling and Lack of Interoperability

The proliferation of disparate point solutions for static analysis, dynamic testing,g and software composition assessment has created toolchain fragmentation that undermines cohesive security programs, which is hampering the regional market expansion. According to the European Institute for Digital Innovation, 76% of European enterprises use 3 or more security testing tools from different vendors, resulting in alert fatigue, inconsistent risk scoring, and manual correlation efforts. As per the European Cybersecurity Organisation, many legacy tools lack native integration with modern CI/CD platforms such as GitLab, Azure DevOps, or GitHub Actions, forcing developers to bypass scans due to performance bottlenecks. In France and Italy, ly 60% of development teams reported disabling security checks during peak release cycles to avoid pipeline delays. Furthermore, the absence of standardized APIs across vendors prevents unified dashboards and automated remediation workflows. This operational friction dilutes the effectiveness of security investments and fosters a culture of compliance over genuine risk reduction, particularly in mid-sized firms with limited DevOps maturity.

MARKET OPPORTUNITIES

Integration of AI-Driven Threat Intelligence and Autonomous Remediation

The deployment of artificial intelligence to enhance vulnerability detection prioritization and automated remediation is a high-growth opportunity in the European application security market. According to the European Institute of Innovation and Technology, AI-powered platforms reduced false positive rates by 42% and cut mean time to remediate critical flaws by 55% in pilot programs across financial and healthcare sectors in 2024. As per the International Telecommunication Union, machine learning models trained on European threat telemetry can now predict exploitation likelihood for newly disclosed CVEs with 90% accuracy, enabling risk-based patching. Vendors like Snyk and Checkmarx have integrated generative AI to suggest context-aware code fixes directly within developer IDEs. Furthermore, the EU’s Horizon Europe program allocated €38 million in 2024 to fund research on autonomous security agents that can validate and deploy patches in containerized environments without human intervention. These innovations align with the EU’s vision for self-healing digital infrastructure under the Cyber Resilience Act.

Expansion of Secure Software Development Academies and Public-Private Partnerships

The growing emphasis on developer upskilling offers a structural opportunity to embed security at the source through formalized education and certification ecosystems, which is a lucrative opportunity for the European market. According to the European Commission, over 29 million software developers operate in the EU, yet fewer than 14% have received formal secure coding training. In response, the EU launched the Cyber Skills Academy in 20,23 partnering with industry leaders such as SAP Sie, men,mens and Thales to deliver standardized curricula on OWASP Top 10 mitigation and secure architecture design. As per the European Association of Software Architects, national initiatives in Germany and Finland now mandate secure coding modules in all computer science degrees accredited after 2024. Companies like GitLab and Microsoft have open-access labs offering hands-on application security challenges aligned with ENISA guidelines. Furthermore, the revised Cybersecurity Act incentivizes firms to certify developers through tax credits, creating a virtuous cycle of competence and compliance. This foundational investment addresses the root cause of vulnerabilities rather than merely treating symptoms.

MARKET CHALLENGES

Escalating Sophistication of API and Software Supply Chain Attacks

The increasing complexity and interconnectivity of modern applications have made APIs and third-party dependencies prime vectors for high-impact breaches across Europe, which is challenging the application security market growth in Europe. According to the European Union Agency for Cybersecurity, API related incidents accounted for 70% of web application breaches in 2024, with attackers exploiting broken object-level authorization and excessive data exposure. As per the European Banking Authority, a single compromised open-source library in a payment processing SDK led to the exfiltration of 2.5 million customer records across 5 EU banks in early 2024. The SolarWinds-style supply chain compromise remains a top concern, with 44% of European software vendors unable to fully inventory their transitive dependencies per a 2024 ENISA assessment. While the Cyber Resilience Act mandates software bills of materials, many organizations lack tools to continuously monitor for newly disclosed vulnerabilities in their dependency trees. This asymmetry between attack sophistication and defensive visibility creates systemic risk that cannot be addressed by perimeter controls alone.

Ambiguity in Cross-Border Liability and Incident Reporting Obligations

Despite harmonized frameworks like NIS2, significant legal uncertainty remains in how application security incidents are reported and liability allocated across EU jurisdictions, particularly for multinational software vendors, which is also challenging the expansion of this regional market. According to the European Data Protection Supervisor, inconsistent interpretations of “significant impact” under NIS2 have led to divergent reporting timelines, with Germany requiring notification within 24 hours while Spain allows 72 hours. As per European Court of Justice rulings in 2024, liability for third-party component vulnerabilities remains legally contested, with developers arguing they cannot be held accountable for upstream open-source flaws. This uncertainty discourages proactive disclosure and complicates breach response coordination. Furthermore, cloud providers and software vendors often dispute responsibility for misconfigurations in shared environments, creating gaps in accountability. Until binding guidance clarifies roles across the software value chain, no organizations will prioritize legal defensibility over collaborative defense,nse undermining the collective resilience envisioned by EU cybersecurity policy.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Deployment, Type, Enterprise Type, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Synopsys, Inc., Checkmarx Ltd., Veracode, Inc. (an Acquired Security business – Thoma Bravo), Fortify (Micro Focus International plc), Qualys, Inc., Rapid7, Inc., IBM Corporation, Cisco Systems, Inc., Palo Alto Networks, Inc., CrowdStrike Holdings, Inc., Trend Micro Incorporated, McAfee Corp., Sophos Group plc, WhiteHat Security, Inc. (NTT Security), Tenable, Inc., Secure Code Warrior, Snyk Ltd., GitLab Inc., Salt Security |

SEGMENTAL ANALYSIS

By Deployment Insights

The cloud deployment segment occupied 68.5% of the European application security market share in 2024 due to the continent’s rapid shift toward cloud‑native development and regulatory alignment with secure‑by‑default architectures. As per Eurostat, 42.5% of EU enterprises purchased cloud computing services in 2023, with adoption highest among large firms. The European Cloud Partnership notes that cloud‑based application security platforms offer automatic updates, real‑time threat intelligence, and seamless integration with DevOps pipelines features critical for agile enterprises. The EU Cyber Resilience Act explicitly encourages certified cloud security services that provide software bills of materials and vulnerability disclosure. National cybersecurity agencies in Germany and France now mandate cloud security posture management for all public sector SaaS deployments. This convergence of technological necessity and regulatory preference has made the cloud the default deployment model for application security across financial, healthcare, and e‑government sectors.

By Type Insights

The web application security segment led the market by holding 60.95% of the European market share in 2024. The pervasive reliance on web interfaces across banking, e‑commerce, public services, and enterprise portals is fuelling the expansion of the web application security segment in this regional market. As per ENISA, web applications were the attack vector in 72% of reported breaches in 2023, with injection flaws and broken authentication topping the risk list. The European Banking Federation confirms that all major EU banks now enforce real‑time web application firewalls and automated penetration testing for internet‑facing portals following the 2022 DORA regulation. National e‑government platforms in Estonia and Denmark integrate continuous web security scanning as part of their sovereignty strategy. Furthermore, the revised NIS2 Directive requires operators of essential services to conduct quarterly web vulnerability assessments, institutionalizing web security as a compliance function across critical infrastructure.

The mobile application security segment is the fastest-growing type segment and is projected to grow at a CAGR of 16.06% over the forecast period, owing to the exponential growth in mobile banking, telehealth, and enterprise productivity apps handling sensitive personal and financial data. As per Eurostat, 92% of EU adults used mobile banking or payment apps in 2024, with transaction volumes doubling since 2021. The European Data Protection Supervisor reported that over 40% of GDPR breach notifications in 2023 involved insecure mobile applications leaking health or location data. In response, the European Medicines Agency now requires all digital therapeutics and patient monitoring apps to undergo mobile‑specific penetration testing before authorization. Financial regulators in France and the Netherlands mandate runtime application self‑protection and jailbreak detection for consumer finance apps.

By Enterprise Type Insights

The large enterprises segment captured 68.4% of theEuropeane application security market in 2024. The leading position of the large enterprises segment in this regional market can be credited to its complex digital footprints, stringent regulatory obligations, and mature cybersecurity budgets. As per the European Cybersecurity Organisation, 94% of large EU firms operate more than 500 custom applications with an average of 1,200 active APIs each, creating vast attack surfaces. The European Commission’s NIS2 Directive requires operators of essential services—primarily large utilities, banks, and transport firms—to implement continuous application security testing and incident response plans by October 2025. National strategies in Germany and Sweden mandate annual third‑party audits of internet‑facing software. Their in‑house DevOps teams integrate advanced tools like interactive application security testing and software composition analysis into CI/CD pipelines.

The SMEs segment is the fastest-growing enterprise segment and is predicted to witness a CAGR of 17.7% over the forecast period, owing to digitalization, regulatory trickle‑down, and affordable cloud‑based security services. As per the European Commission, over 23 million SMEs operate in the EU, with 67% offering digital services post‑pandemic. The EU Cyber Resilience Act requires software vendors to secure products by design, indirectly compelling SMEs that develop or customize applications to adopt security testing. National cybersecurity centers in the Netherlands and Finland subsidize SME security assessments via public‑private partnerships. Vendors like Snyk and Veracode now offer tiered pricing and automated remediation guides tailored to teams with limited expertise.

By End User Insights

The BFSI segment dominated the market with 28.5% of the European application security market share in 2024. Financial institutions manage high‑value digital assets and face strict mandates. As per the European Banking Authority, all credit institutions must comply with DORA, mandating penetration testing, code reviews, and third‑party risk assessments. The European Central Bank reported cyber incidents targeting banking applications rose by 47% in 2023, with API abuse and credential stuffing as leading tactics. National regulators in France, Germany, and the UK require real‑time web application firewalls, anomaly detection, and secure coding certifications.

The healthcare segment is the fastest-growing end‑user segment and is anticipated to record a CAGR of 18.4% over the forecast period due to the rapid digital transformation of patient care, rising cyber threats, and new EU health data regulations. As per the European Health Data Space initiative, over 80% of EU hospitals now use electronic health records, telemedicine platforms, and connected medical devices. The European Data Protection Supervisor reported healthcare was the second most targeted sector for ransomware in 2023, with attackers exploiting vulnerable patient portals. The revised Medical Devices Regulation classifies health software as medical devices requiring cybersecurity risk assessments and surveillance.

COUNTRY LEVEL ANALYSIS

Germany Application Security Market Analysis

Germany led the European application security market and had 25.8% of the regional market share in 2024. The dominance of Germany in the European market is attributed to its role as a technology and industrial hub. The country’s demand is driven by secure software development practices, particularly in manufacturing, automotive, and financial services. Germany accounts for a significant share due to its strong enterprise base and regulatory environment. Market status is expansionary, supported by strict compliance requirements under GDPR and increasing cyber threats targeting industrial systems. Driving factors include the rise of cloud adoption, digital transformation in Mittelstand companies, and government initiatives to strengthen cybersecurity resilience. Germany’s role is reinforced by investments in DevSecOps and secure coding practices, which are making it a cornerstone of Europe’s application security growth.

France Application Security Market Analysis

France held a promising share of the regional application security market in 2024 and is supported by its large financial services and public sector demand. The country’s role is significant, with enterprises adopting application security solutions to comply with GDPR and national cybersecurity frameworks. Market status is growth-oriented, with France investing in secure digital infrastructure and expanding its cybersecurity workforce. Driving factors include rising cyberattacks on healthcare and government systems, increased adoption of cloud services, and emphasis on secure application development. France’s position is also defined by its leadership in EU cybersecurity policy, which encourages the adoption of advanced testing tools such as SAST and DAST. This combination of regulatory strength and sectoral demand secures France’s place as a growth engine in the European application security market.

United Kingdom Application Security Market Analysis

The United Kingdom maintains a steady position in the European application security market, with demand concentrated in financial services, retail, and government sectors. Market status is stable but expanding, supported by strong regulatory frameworks and investments in secure application development. Driving factors include the UK’s emphasis on protecting critical infrastructure, rising cyber threats, and the adoption of cloud‑based application security solutions. The UK’s role is reinforced by its advanced fintech ecosystem, which requires robust security testing and compliance. The UK remains a consistent contributor, which is ensuring resilience and innovation in secure application practices.

Italy Application Security Market Analysis

Italy holds a prominent position in the European application security market, combining demand from manufacturing, healthcare, and government sectors. Market status is growth-oriented, with Italy investing in secure application development to support digital transformation. Driving factors include rising cyber threats, EU compliance requirements, and the adoption of cloud services. Italy’s role is reinforced by its emphasis on secure coding practices and investments in cybersecurity training. The country’s balanced demand across multiple sectors ensures its position as a reliable growth contributor within the European application security market.

Spain Application Security Market Analysis

Spain has carved out a dynamic position in the European application security market, distinguished by its rapid growth trajectory. Market status is expansionary, with strong adoption in financial services, retail, and government applications. Driving factors include rising cyberattacks, government initiatives to strengthen cybersecurity, and the adoption of cloud‑based solutions. Spain’s role is further strengthened by its emphasis on secure digital transformation, positioning the country as a rising star in the regional market.

COMPETITIVE LANDSCAPE

Competition in the European application security market is defined by a dynamic interplay between global cybersecurity giants, specialized DevSecOps innovators,s and open source security vendors. Incumbents leverage deep regulatory expertise, seamless integration with enterprise tools, ins and professional services to maintain dominance in large BFSI and government accounts. Simultaneously,usly agile startups differentiate thrAI-poweredwered analytics, developer-friendly interfaces, and subscription-based pricing that appeals to digital native firms and SMEs. The market is intensifying as the EU Cyber Resilience Act imposes legal liability on software producers, creating urgency for embedded security. However,r fragmentation persists due to varying national interpretations of compliance and inconsistent DevSecOps maturity across industries. Cloud migration and API proliferation expand the addressable market, yet toolchain complexity and talent shortages constrain effective deployment. Success increasingly hinges on balancing automation with human expertise while ensuring solutions are both technically robust and legally defensible under Europe’s evolving digital sovereignty regime.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe application security market include

- Synopsys, Inc.

- Checkmarx Ltd. (a private company)

- Veracode, Inc. (an Acquired Security business – part of Thoma Bravo)

- Fortify (Micro Focus International plc)

- Qualys, Inc.

- Rapid7, Inc.

- IBM Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- CrowdStrike Holdings, Inc.

- Trend Micro Incorporated

- McAfee Corp.

- Sophos Group plc

- WhiteHat Security, Inc. (a NTT Security Company)

- Tenable, Inc.

- Trend Micro Incorporated

- Secure Code Warrior

- Snyk Ltd.

- GitLab Inc.

- Salt Security

TOP LEADING PLAYERS IN THE MARKET

- Checkmarx Ltd is a leading force in the European application security market, offering a comprehensive suite of static application security testing and software composition analysis solutions. Headquartered in Israel,l the company serves major financial, healthcare, re and government institutions across Europe and operates globally in over 50 countries. Checkmarx actively contributes to secure coding standards through partnerships with European cybersecurity agencies and participation in ENISA working groups. Recently,tly Checkmarx enhanced its AI-powered Codebashing platform with interactive secure coding lessons tailored to OWASP Top 10 risks in European regulatory contexts. It also launched a dedicated cloud instance compliant with EU data residency requirements, enabling seamless integration for public sector clients. These actions reinforce its position as a trusted enabler of developer-centric security in highly regulated environments.

- Synopsys Inc plays a pivotal role in the European application security market through its Black Duck and Coverity platforms, which provide advanced software composition analysis and static testing for complex enterprise applications. As a global leader, Synopsys integrates application security into the full software development lifecycle,e serving automotive, financial,ial and industrial clients across Europe and beyond. The company collaborates with EU standardization bodies to align its tools with the Cyber Resilience Act and NIS2 Directive requirements. Recently, Synopsys introduced an automated SBOM validation module that maps dependencies against ENISA vulnerability databases in real time. It also expanded its European professional services team to supportlarge-scalee DevSecOps transformations in Germany and France. These initiatives strengthen its ability to deliver end-to-end security for mission-critical software supply chains.

- Micro Focus, now operating under OpenText, significantly influences theEuropeane application security market through its Fortify suite, which delivers dynamic, static, and runtime application security testing capabilities. The company supports large enterprises and public sector organizations across the U, Germany, and the Nordics in meeting stringent compliance mandates. OpenText leverages its European data centers to ensure application security testing adheres to GDPR and EU data sovereignty principles. Recently,ntly OpenText integrated Fortify with its broader DevOpsAI-powered analytics platform, enabling risk-based vulnerability prioritization aligned with European threat intelligence feeds. It also launched a managed application security service for SMEs in partnership with national cybersecurity centers in the Netherlands and Belgium. These moves enhance accessibility and compliance for diverse customer segments while reinforcing its commitment to secure digital transformation in Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European application security market prioritize alignment with EU regulatory frameworks such as the Cyber Resilience Act and NIS2 Directive by embedding mandatory requirements like software bills of materials and vulnerability disclosure into their platforms. They invest heavily in AI-driven automation to reduce false positives, accelerate remediation,n and integrate seamlessly into DevOps pipelines. Companies expand cloud-based offerings with EU data residency to address sovereignty concerns while lowering entry barriers for SMEs. Strategic partnerships with national cybersecurity agencies, educational institutions, and industry consortia enhance credibility and drive secure coding adoption. Furthermore, they develop vertical-specific solutions for BFSI, healthcare, and government sectors that address unique compliance and tlandscapess ensuring relevance and resilience in critical infrastructure.

MARKET SEGMENTATION

This research report on the europe application security market is segmented and sub-segmented into the following categories.

By Deployment

- Cloud

- On-premise

By Type

- Web Application Security

- Mobile Application Security

By Enterprise Type

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

By End User

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- IT & Telecom

- Retail & E-commerce

- Government

- Others

By Country

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Application Security Market?

Key drivers for the Europe Application Security Market include GDPR compliance, the Cyber Resilience Act, and rapid cloud adoption across BFSI, healthcare, and manufacturing sectors.

Increasing cyberattacks and government initiatives like the UK's National Cyber Strategy boost demand for AI-powered threat detection and zero-trust models.

2. Who are the top players in the Europe Application Security Market?

Leading companies in the Europe Application Security Market include Checkmarx, Veracode, Synopsys, Palo Alto Networks, and Snyk, offering SAST/DAST tools tailored to EU regulations.

These vendors dominate through DevSecOps integrations and partnerships with European firms for compliance-focused solutions.

3. What is SAST in the Europe Application Security Market?

Static Application Security Testing (SAST) scans source code for vulnerabilities in the Europe Application Security Market without execution, ideal for early DevSecOps integration.

Widely adopted in Germany and France for compliance with BSI standards and GDPR, it helps identify issues like SQL injection proactively.

4. How does GDPR impact the Europe Application Security Market?

GDPR mandates robust data protection, fueling the Europe Application Security Market by requiring secure app development and runtime protection across EU nations.

Fines for breaches drive investments in RASP and IAST, with the UK and Germany leading in enforcement and solution adoption.

5. What role does cloud play in Europe Application Security Market?

Cloud deployment dominates the Europe Application Security Market, with hybrid solutions addressing DORA requirements for financial apps and scalable threat protection.

Europe's sovereign cloud push enhances adoption in SMEs and large enterprises alike.

6. What is DAST in the Europe Application Security Market?

Dynamic Application Security Testing (DAST) simulates attacks on running apps in the Europe Application Security Market, uncovering runtime vulnerabilities like XSS.

Essential for compliance in retail and healthcare sectors under EU cyber acts

7. How does AI influence the Europe Application Security Market?

AI enhances threat detection and anomaly flagging in the Europe Application Security Market, supporting zero-trust and predictive security.

Germany's BSI initiatives promote AI-driven tools for manufacturing and automotive apps.

8. What are challenges in the Europe Application Security Market?

Challenges in the Europe Application Security Market include skills shortages, legacy system integration, and varying national regulations.

Solutions focus on automated DevSecOps and managed services to address SME adoption barriers.

9. Which verticals dominate Europe Application Security Market?

BFSI, IT & Telecom, and healthcare lead the Europe Application Security Market, with manufacturing gaining traction via secure IoT apps.

Government mandates ensure high penetration across these sectors.

10. What is RASP in Europe Application Security Market?

Runtime Application Self-Protection (RASP) embeds security into apps for real-time threat blocking in the Europe Application Security Market.

Popular in fintech for GDPR-aligned protection against exploits.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com