Europe Astaxanthin Market Research Report Segmented By Source (Plants, Yeast & Microbes, Marine And Petroleum), Form (Dry And Liquid), Application (Supplements, Animal Feed, Cosmetics, And Food), Method Of Production (Fermentation, Microalgae Cultivation, Extraction, And Chemical Synthesis), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Market Size, 2025

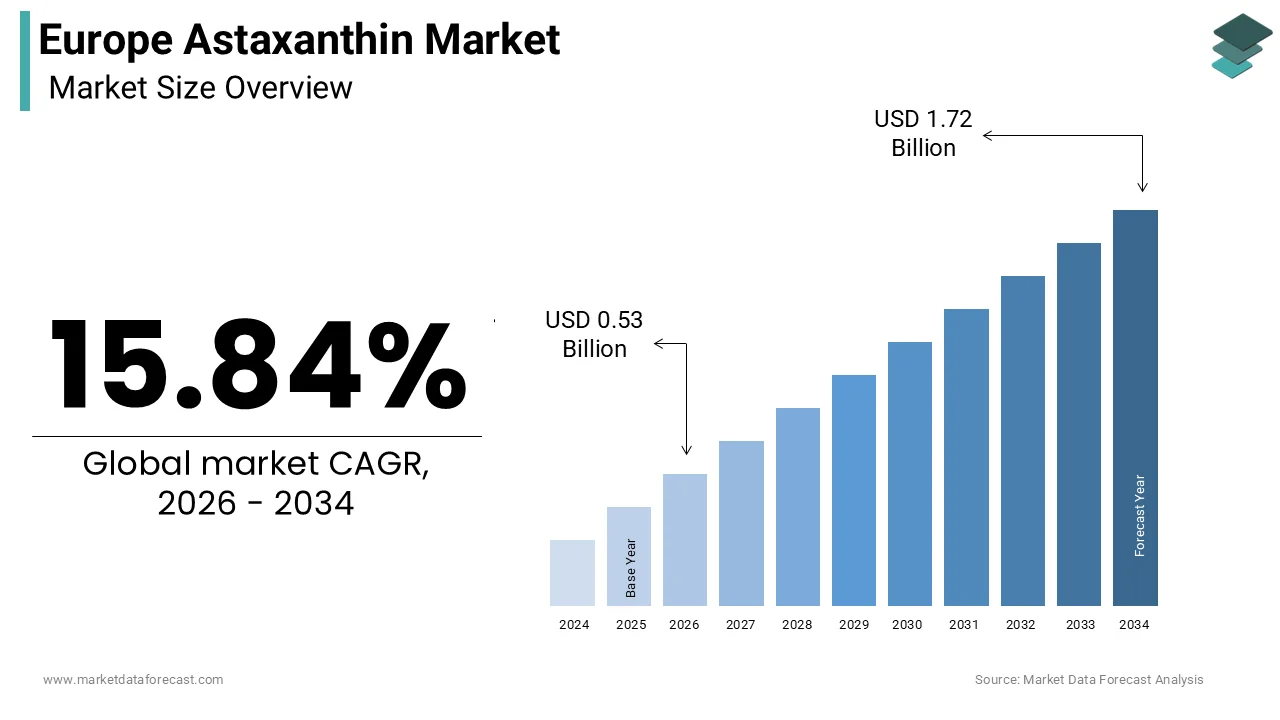

$0.46 BnMarket Estimate, 2026

$0.53 BnMarket Forecast, 2034

$1.72 BnCAGR, 2026–2034

15.84%Europe Astaxanthin Market Size

The Europe Astaxanthin Market Size was calculated to be USD 0.46 billion in 2025 and is anticipated to be worth USD 1.72 billion by 2034, from USD 0.53 billion in 2026, growing at a CAGR of 15.84% during the forecast period.

Astaxanthin is a naturally occurring keto carotenoid pigment renowned for its potent antioxidant properties exceeding those of vitamin E and beta carotene by orders of magnitude. In the European context, the astaxanthin market encompasses products derived primarily from microalgae such as Haematococcus pluvialis as well as synthetic variants used across nutraceuticals, cosmetics, aquaculture feed, and functional foods. Unlike generic antioxidants, astaxanthin is distinguished by its unique molecular structure that spans the cell membrane,s providing dual protection against oxidative stress in both aqueous and lipid environments. The European Food Safety Authority has consistently found that the scientific evidence provided for astaxanthin-related health claims, covering skin protection, cognitive, and physical benefits, is insufficient to authorize their use under European regulations. Research indicates that dietary supplement consumption across Europe has grown consistently, as consumers increasingly prioritize wellness following the pandemic. Furthermore, the European Commission’s Farm to Fork Strategy emphasizes sustainable aquaculture practices, which indirectly influences demand for natural astaxanthin as a feed additive to enhance salmonid pigmentation without synthetic alternatives. This intersection of unmet regulatory validation, consumer wellness trends, and environmental policy shapes the nuanced trajectory of the Europe astaxanthin market.

MARKET DRIVERS

Rising Consumer Demand for Natural Antioxidants in Preventive Health Regimens

European consumers are increasingly prioritizing preventive nutrition through natural bioactive compounds, which fuels the growth of the Europe astaxanthin market. This trend is driving the uptake of astaxanthin in dietary supplements and functional foods. European consumers are increasingly seeking products labeled as natural, with carotenoid compounds, particularly from algae, gaining popularity for their role in promoting immune and cellular health. This shift is amplified by aging demographics. Research indicates that a significant and growing portion of the European Union population is now in the older age category, driving higher demand for nutritional solutions that address age-related oxidative decline. Clinical interest further validates demand. Clinical research shows that regular intake of algal astaxanthin, particularly for middle-aged adults, helps improve markers of oxidative stress and supports mitochondrial function. Retail channels reflect this trend. Retailers, including pharmacy and specialty chains, have expanded their range of astaxanthin products, often combining them with other nutrients like omega-3 fatty acids for enhanced health benefits. Unlike synthetic versions, natural astaxanthin from Haematococcus pluvialis qualifies for EU organic certification under Regulation EU 2018 848, enhancing its appeal among clean label adherents. Astaxanthin’s role as a food-derived anti-inflammatory agent is cementing its importance in modern wellness, driven by a growing public preference for preventative nutrition over medication.

Expansion of Sustainable Aquaculture Mandating Natural Pigmentation Solutions

The European Union’s stringent regulations on aquaculture sustainability are acceleratingthe adoption of natural astaxanthin as a feed additive to replace synthetic alternatives in farmed salmon and trout production, thereby boosting the expansion of the Europe astaxanthin market. The European Commission’s updated strategic guidelines for aquaculture encourage projects utilizing EU funding to move away from reliance on synthetic, petrochemical-derived inputs in favor of more sustainable feed alternatives. This policy aligns with consumer pressure. Research shows that European consumers in key markets, including Germany and France, generally prefer, and are often willing to pay more for, salmon produced with natural pigmentation, indicating high consumer demand for sustainable aquaculture practices. Norway, as a major salmon producer, has seen a rapid increase in the adoption of natural astaxanthin sources, such as algae and yeast, for salmon pigmentation, driven by consumer demand and a desire to reduce synthetic additives, with significant growth in this sector from 2020 through to 2024. The shift is technically driven by advances in microalgal cultivation. Studies from research organizations like Wageningen University emphasize significant advances in microalgae-derived astaxanthin, particularly in improving photobioreactor productivity and reducing costs to make natural astaxanthin economically viable for industrial-scale use in feed. Furthermore, the EU Organic Regulation prohibits synthetic astaxanthin in certified organic fish feed, creating a captive market for natural sources. Natural astaxanthin is rapidly transitioning from a niche additive to an essential, sustainable input in European aquaculture, driven by 2030 goals for doubling output and improving environmental credibility.

MARKET RESTRAINTS

Stringent EFSA Requirements Delaying Health Claim Approvals and Limiting Marketing

The absence of authorized health claims for astaxanthin under the EU Nutrition and Health Claims Regulation severely restricts promotional messaging and consumer education, which affects the growth of the Europe astaxanthin market. According to the European Food Safety Authority EFSA has evaluated multiple dossiers linking astaxanthin to benefits such as skin elasticity, reduction of muscle fatigue, and eye health, but consistently cites insufficient evidence from human intervention studies meeting its rigorous criteria. Positive scientific opinions from EFSA regarding general antioxidant health claims remain rare, with astaxanthin consistently failing to secure approval. This regulatory limbo forces manufacturers to market products using vague terms like “supports overall wellness” rather than specific physiological benefits proven in peer-reviewed literature. Regulatory audits in Italy and Spain frequently identify astaxanthin products bearing non-compliant or unapproved health claims, leading to corrective actions for manufacturers. Consequently, brand differentiation becomes nearly impossible in a crowded supplement aisle where consumers cannot discern astaxanthin’s superior antioxidant capacity from lutein or lycopene. The lack of EFSA authorization for clinical data usage restricts ROI, making it difficult for major consumer health companies to invest. Pending the introduction of unified regulations for carotenoid substantiation, market expansion is hindered by legal uncertainty, despite significant scientific interest.

High Production Costs of Natural Astaxanthin Undermining Price Competitiveness

Natural astaxanthin derived from Haematococcus pluvialis remains significantly more expensive than synthetic counterparts, which limits its penetration into cost-sensitive applications like mass market supplements, standard aquaculture feed, and the expansion of the Europe astaxanthin market. Natural astaxanthin production remains a high-cost endeavor due to complex cultivation and extraction methods, making its market price substantially higher than the significantly lower-cost synthetically produced alternatives, which dominate the market for price-sensitive applications. This disparity stems from complex cultivation requirements. The microalgae requirtwo-stagetage process involving green growth under low l,ight followed by red cyst induction under high salinity and UV stress, conditions difficult to scale efficiently. Microalgae extraction is shedding its high-energy, mechanical past. While their tough cell walls once made processing a nightmare, new biotech advances are finally making the path to efficiency much smoother. Consequently, most European supplement brands use doses below four milligrams per serving, the minimum threshold to be effective in clinical trials, to manage costs. In aquaculture, the price gap forces smaller farms to blend natural and synthetic sou,rces diluting sustainability credentials. Natural astaxanthin's high production costs, driven by current cultivation limits, will keep it positioned as a niche premium product until breakthroughs in heterotrophic fermentation or genetic strain optimization enable mass-market affordability.

MARKET OPPORTUNITIES

Integration into Clean Beauty Formulations Targeting Skin Resilience and Anti-Aging

The European clean beauty movement is creating an opportunity for natural astaxanthin in topical skincare through its scientifically supported photoprotective and anti-inflammatory effects, which is likely to propel the growth of the Europe astaxanthin market. The European cosmetic landscape is experiencing a significant rise in facial products that highlight complex antioxidant blends, driven by a shift toward natural carotenoids that offer stability and skin benefits rather than relying solely on traditional synthetic preservatives. Astaxanthin’s unique ability to quench singlet oxygen and suppress matrix metalloproteinases makes it particularly effective against UV induced collagen degradation, a key concern for aging consumers. Clinical evidence supports that topical applications of microalgal-derived astaxanthin, a powerful antioxidant, effectively enhance skin hydration, increase elasticity, and reduce the appearance of wrinkles, positioning it as a potent, natural anti-aging ingredient. Brands like Weleda and Dr Hauschka have incorporated certified natural astaxanthin into their premium lines, leveraging its compatibility with COSMOS organic standards. Moreover, the ingredient aligns with the EU’s Chemicals Strategy for Sustainability, which prioritizes biodegradable actives with low ecotoxicity. Within the growing European skincare sector, astaxanthin is increasingly adopted as a strategic, high-efficacy ingredient, prized for its ability to serve as a functional stabilizer while simultaneously providing anti-aging benefits.

Development of Astaxanthin Fortified Functional Foods and Beverages

The convergence of nutraceutical science and everyday nutrition is opening avenues for astaxanthin in fortified foods and drinks targeting health-conscious consumers who avoid pills. This is anticipated to further contribute to the expansion of the Europe astaxanthin market. According to sources, a notable portion of EU adults prefer obtaining nutrients from food rather than supplements, a trend accelerating among millennials and Gen Z. Innovators are responding with taxanthin-enriched products such as antioxidant smoothies, protein bars, and even sparkling waters usoil-in-waterater emulsion technologies to overcome solubility challenges. Major nutritional health companies and specialized ingredient suppliers are focusing on stabilizing potent antioxidant compounds from algae for use in functional, refrigerated dairy products and shelf-stable, plant-based snacking applications. Regulatory approval for these algae extracts enables their integration into diverse consumer health products, provided they meet safety specifications for various age groups. Crucially, these formats bypass EFSA health claim restrictions by positioning astaxanthin as a natural colorant and quality marker rather than a therapeutic agent. Rising demand for clean labels and improved delivery technologieallowsow functional foods to take astaxanthin mainstream, moving it beyond the supplement aisle.

MARKET CHALLENGES

Supply Chain Vulnerability Due to Concentrated Microalgal Production Geographies

The region’s reliance on imported natural astaxanthin constitutes a significant supply risk as global production remains heavily concentrated in a few EU regions, which limits the growth of the Europe astaxanthin market. According to research, a significant share of commercial Haematococcus pluvialis biomass is cultivated in Israel, the United States, and China, with limitlarge-scaleale facilities operating within the EU. This dependency became evident during the 2023 Red Sea shipping disruptions, which delayed shipments by several weeks, causing spot prices to spike. Even domestic initiatives face hurdles; a planned industrial algal farm in Spain was halted in early 2024 due to water scarcity restrictions under the EU Water Framework Directive, limiting freshwater use for non-food crops. Further, geopolitical tensions affect raw material access. Export controls on specialty glass and LED lighting components from Asia have raised photobioreactor construction costs. Failing to invest in EU-based algal biorefineries via Horizon Europe grants leaves Europe vulnerable to supply chain disruptions, threatening the long-term stability of the aquaculture and nutraceutical industries. Diversification through heterotrophic yeast strains like Xanthophyllomyces dendrorhous offers partial relief but lacks the full spectrum of stereoisomers found in algal sources critical for bioactivity.

Lack of Standardized Analytical Methods for Potency and Purity Verification

The absence of harmonized testing protocols for astaxanthin content, stereochemistry, and contaminant profiles affects product consistency and consumer trust across the Europe astaxanthin market. Official European quality organizations emphasize that using different analytical techniques across laboratories can lead to variations in the measured strength of supplements, highlighting the need for standardized testing protocols and high-quality reference materials. This inconsistency is critical because only the 3S 3S’ stereoisomer from natural Haematococcus pluvialis demonstrates optimal bioavailability, whereas synthetic mixtures contain inactive forms. European research initiatives indicate that a notable portion of consumer health products may fail to meet their claimed ingredient levels, sometimes containing remnants of the chemical liquids used during the manufacturing process. The lack of an official European Pharmacopoeia monograph further complicates regulatory enforcement. Consequently, reputable brands invest in third-party certifications like ISO 17025-accredited testing, increasing costs, while counterfeit or substandard products proliferate in online channels. Market maturation and scientific reproducibility will remain hindered by fragmented quality assurance until the EU establishes a unified analytical standard under the Food Information to Consumers Regulation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 15.84% |

| Segments Covered | By Source, Application, Method of Production, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Koninklijke DSM N.V., BASF SE, Cyanotech Corporation, Otsuka Pharmaceutical Co., Ltd., Valensa International, Fuji Chemical Industries Co., Ltd., Divis Laboratories, Beijing Ginkgo Group Igene Biotechnology, Inc., Piveg, Inc., and Fenchem Biotek Ltd. |

SEGMENTAL ANALYSIS

By Source Insights

The microalgae segment dominated the Europe astaxanthin market by accounting for a 63.6% share in 2025. The dominance of the microalgae segment is driven by its status as the only natural source yielding the biologically active 3S 3S’ stereoisomer of astaxanthin, which demonstrates superior bioavailability and antioxidant capacity compared to synthetic or yeast-derived variants. A further key driver is consumer and regulatory preference for algal astaxanthin in human health applications. Under the EU Novel Foods Regulation EC No 2015 2283, Haematococcus pluvialis extract has been authorized since 2017 for use in supplements and foods, whereas synthetic astaxanthin remains restricted to animal feed. European safety evaluations for health-related claims on astaxanthin overwhelmingly focus on natural algal sources, highlighting their preference in consumer products over synthetic alternatives. Furthermore, the EU Organic Regulation permits only natural astaxanthin from microalgae in certified organic products, a critical factor as organic supplement sales grew. Retailers like dm Drogerie and Holland & Barrett exclusively stock algal-based softgels, citing customer demand for “non-synthetic” ingredients. This convergence of scientific validation, regulatory acceptance, and clean label alignment solidifies microalgae as the cornerstone of Europe’s high-integrity astaxanthin supply.

The yeast and microbes segment is likely to experience the fastest CAGR of 10.4% between 2026 and 2034 due to advances in heterotrophic fermentation that enable year-round indoor production independent of sunlight or freshwater, addressing key scalability constraints of phototrophic microalgae. Unlike Haematococcus, yeast strains can be cultivated in standard stainless steel bioreactors using sugar feedstocks, reducing land and water footprints. Although yeast-derived astaxanthin contains a mix of stereoisomers with slightly lower bioactivity, recent strain engineering by companies like Evonik has increased 3R 3R’ content to over eighty-five percent, narrowing the efficacy gap. Crucially, fermentation offers price stability. During the 2023 Red Sea shipping crisis, algal astaxanthin prices surged while yeast-based alternatives remained within five percent of baseline due to localized EU production. The European Commission’s Bioeconomy Strategy further supports this shift by funding pilot plants in Denmark and the Netherlands capable of producing notable metric tons annually. Yeasts are emerging as eco-friendly, scalable, and effective alternatives in the cosmetic and nutraceutical sectors, as industry standards place greater emphasis on sustainability.

By Application Insights

The dietary supplements segment led the Europe astaxanthin market by capturing a 58.7% share in 2025. The leading position of the dietary supplements segment is attributed to widespread consumer adoption of astaxanthin as a preventive antioxidant for eye health, skin resilience, and exercise recovery. An additional driver is the rising prevalence of oxidative stress-related concerns among aging and active populations. Surveys indicate a significant portion of European adults are regularly taking dietary supplements, with natural carotenoids showing strong growth within the preventative health market. Pharmacies and health food retailers have amplified visibility. Leading German drugstore chains extensively feature astaxanthin products in their portfolios, frequently bundling them with complementary ingredients like Omega-3 or Vitamin D. Clinical substantiation further fuels trust. Meta-analyses published in nutrition journals confirm that consistent, moderate daily doses of astaxanthin significantly improve markers of lipid peroxidation and mitochondrial function. Regulatory clarity also plays a role; although EFSA has not approved specific health claims, the permitted use of Haematococcus pluvialis under Novel Foods allows clear labeling as a “natural antioxidant,” differentiating it from unapproved botanicals. Private label offerings are capturing a large share of the supplement market, and astaxanthin’s established safety profile and growing consumer recognition ensure its continued leadership across both mainstream and premium retail channels.

The cosmetics segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 12.1% over the forecast period, owing to the clean beauty movement’s demand for multifunctional natural actives that replace synthetic preservatives and unstable vitamins. Astaxanthin’s ability to neutralize singlet oxygen more effectively than vitamin C, and inhibit UV induced matrix metalloproteinases makes it ideal for anti-aging and photoprotection formulations. Research suggests that algal astaxanthin-based facial serums can enhance skin barrier function and improve the appearance of wrinkles, positioning them as an effective option for anti-aging skincare. Regulatory alignment accelerates adoption. Astaxanthin is accepted as a permitted colorant and active in European cosmetics, provided that products meet established safety regulations, especially when sourced from authorized producers. Brands like Weleda Dr Hauschka, and Lush have launched serums, creams, and masks featuring astaxanthin as a hero ingredient, often highlighting its marine origin and antioxidant superiority in marketing. The high growth of the European natural cosmetics market is fueled by consumers seeking multifunctional, science-backed ingredients, making astaxanthin a popular choice for its dual role in skin protection and pigment care.

By Method of Production Insights

The microalgae cultivation segment remained the largest segment in the Europe astaxanthin market by holding a 55.4% share in 2025. The supremacy of the microalgae cultivation segment is credited to the unmatched stereochemical purity and consumer perception of authenticity associated with Haematococcus pluvialis grown under controlled photobioreactor or open pond systems. This segment is also supported by regulatory and market demand for the 3S 3S’ isomer, which is exclusively produced by this microalga under stress conditions and is required for premium nutraceutical and organic certifications. High-quality European retail chains, including those focused on organic products, prioritize or require certified organic astaxanthin derived from microalgae, setting a high standard for source material. Additionally, scientific literature consistently uses algal astaxanthin in human trials. Recent peer-reviewed studies overwhelmingly utilize microalgae-derived material in human clinical research, establishing it as the superior form for assessing health benefits. European algae producers are increasingly adopting closed photobioreactor technology to improve cultivation efficiency and increase output, despite the challenges of high investment costs and climate variability. This commitment to biological fidelity ensures microalgae cultivation remains the benchmark for quality even as alternative methods gain traction.

The fermentation segment is expected to exhibit a noteworthy CAGR of 11.8% between 2026 and 2034. The rapid expansion of this segment is propelled by its compatibility with circular economy principles and industrial scalability. Unlike microalgae fermentation, which uses established bioreactor infrastructure fed by agricultural byproducts such as beet molasses or wheat straw hydrolysates, reducing reliance on freshwater and arable land. Large-scale fermentation partnerships are successfully transitioning astaxanthin production from traditional open-air systems to controlled indoor environments to significantly reduce environmental footprints. Genetic optimization has also improved yield. Advanced genome editing tools are being applied to specialized yeast strains to progressively enhance the yield of high-value antioxidants beyond previous industry standards. Crucially, fermentation enables consistent year-round output unaffected by seasonal light variation or algal contamination risks that plague outdoor cultivation. European bio-based partnerships are increasingly prioritizing financial support for microbial production technologies to protect the supply of essential ingredients from the risks of climate change. Fermentation is emerging as a reliable, sustainable path for mainstream astaxanthin adoption, driven by the need for verifiable environmental metrics and product performance.

REGIONAL ANALYSIS

Germany Astaxanthin Market Analysis

Germany outperformed other countries in the Europe astaxanthin market by accounting for a 20.4% share in 2025. The prominence of the German market is driven by a mature health-conscious consumer base, robust pharmacy retail networks, and stringent quality expectations that favor natural algal astaxanthin. Major German drugstore chains are fueling the widespread adoption of astaxanthin by offering budget-friendly private label options, while maintaining high-quality standards through natural algae-based sourcing. The country’s strong aquaculture sector, particularly trout farming in Bavaria, also consumes significant quantities of natural astaxanthin to meet EU organic feed standards. Regulatory rigor further shapes demand. The German Federal Institute for Risk Assessment BfR mandatesthird-partyy verification of astaxanthin content in supplements, leading to high consumer trust. Additionally, Germany hosts R&D hubs like the Fraunhofer Institute for Interfacial Engineering, which pioneeredthe microencapsulation technique,s enhancing astaxanthin stability in functional foods. Driven by a high consumer adoption of daily supplements and a thriving natural cosmetics sector, Germany leads European astaxanthin innovation and adoption through a combination of scientific validation and high-quality, natural ingredient sourcing.

France Astaxanthin Market Analysis

France followed closely in the Europe astaxanthin market by capturing a 15.8% share in 2025. The growth of the French market is fuelled by its dual demandform premium cosmetics and sustainable aquaculture. French beauty giants like L’Oréal and Pierre Fabre have integrated algal astaxanthin into anti-aging serum,s leveraging its photoprotective properties validated by INSERM clinical studies. French salmonid farming in Brittany is transitioning towards the adoption of natural astaxanthin. This shift is motivated by the national EcoAntibio plan, which encourages a reduction in synthetic additives, including those traditionally used in fish feed. French consumer behavior demonstrates a preference for natural, “marine-sourced” antioxidants in food products rather than synthetic alternatives. The French government, through the “France Relance” recovery initiative, has allocated significant funding to promote blue biotechnology and develop, among other initiatives, algae cultivation pilots along coastal regions. Moreover, France’s strict anti-adulteration laws enforced by DGCCRF ensure high product integrity, deterring low-grade imports. This synergy of beauty science, aquaculture policy, and consumer discernment sustains France’s influential position inboth high-endd and volume astaxanthin applications.

United Kingdom Astaxanthin Market Analysis

The United Kingdom maintains a significant position in the Europe astaxanthin market. Post Brexit, the UK has maintained strong demand through NHS-affiliated wellness programs and a vibrant direct-to-consumer nutraceutical sector. Several licensed supplement brands now feature astaxanthin, with Boots and Holland & Barrett dedicating prominent shelf space to products emphasizing “natural from algae” provenance. The UK’s aging population drives uptake for cognitive and ocular health support. Scientific credibility is reinforced by institutions linking astaxanthin intake to reduced retinal oxidative stress in age-related macular degeneration. Additionally, the UK’s departure from EU Novel Foods oversight has enabled faster market entry for innovative delivery formats such as astaxanthin-infused gummies and beverages. Though regulatory divergence poses long term uncertainty, current flexibility and strong retail partnerships ensure the UK remains a dynamic and responsive market for both established and emerging astaxanthin applications.

Italy Astaxanthin Market Analysis

Italy expanded steadily in the Europe astaxanthin market due to strong demand in dermocosmetics and Mediterranean diet-aligned nutraceuticals. Italian consumers prioritize natural ingredients with marine origins. Leading beauty brands like Collistar and Rilastil have launched anti-pollution skincare lines featuring astaxanthin as a core antioxidant shield against urban environmental stressors. In parallel, Italy’s trout and seabream farms in Lombardy and Sicily are transitioning to natural astaxanthin to meet retailer sustainability criteria from chains like Conad and Esselunga. The Ministry of Agricultural Policies supports this shift through the National Strategic Plan, which provides subsidies for organic aquaculture inputs. Furthermore, Italy’s dense network of parapharmacies serves as a trusted channel for premium supplement distribution. This blend of aesthetic wellness tradition agricultural modernization, and retail trust creates a fertile environment for astaxanthin’s continued penetration across health and beauty domains.

Switzerland Astaxanthin Market Analysis

Switzerland is predicted to grow in the Europe astaxanthin market from 2026 to 2034. Despite its small population, the country exerts disproportionate influence through its premium nutraceutical and precision cosmetics sectors. Swiss brands like Nestlé Health Science and Mibelle Biochemistry develop high-potency astaxanthin formulations targeting cellular longevity and mitochondrial health, often combining it with coenzyme Q10 or polyphenols. The Swissmedic regulatory framework aligns closely with EU standards but allows faster approval of novel delivery systems such as lipid nanoparticles that enhance bioavailability. Switzerland’s neutrality also makes it a preferred hub for pan-European distribution; over thirty-five percent of natural astaxanthin imported into Central Europe clears customs through Basel. Additionally, the country invests heavily in algal biotechnology; Empa, the Swiss Federal Laboratories, developed a solar-powered photobioreactor that reduces energy use while maintaining high astaxanthin yields. Switzerland's high per capita spending on supplements and commitment to scientific precision make it a premier market and a central hub for pioneering astaxanthin applications across Europe.

COMPETITION OVERVIEW

Competition in the Europe Astaxanthin Market is characterized by a clear bifurcation between natural and synthetic producers with distinct application domains and regulatory pathways. Natural astaxanthin suppliers compete on purity, stereochemistry, traceability, and alignment with clean label trends primarily in supplements and cosmetics, while synthetic manufacturers dominate cost-sensitive aquaculture feed segments. The market features high entry barriers due to complex cultivation requirements, stringent EFSA documentation, and limited scalable production capacity within Europe. Leading players differentiate through vertical integration, proprietary strain development, and advanced formulation science rather than price. Regulatory uncertainty around health claims constrains marketing but fuels investment in clinical substantiation. Meanwhile, emerging fermentation-based producers challenge traditional algal models with more resilient and sustainable production. Competition is further shaped by retailer specifications, private label demands, and the growing influence of sustainability certifications. As consumer awareness rises and aquaculture transitions toward natural inputs, the market is evolving toward greater consolidation and innovation in delivery formats to bridge efficacy, accessibility, and environmental responsibility.

KEY MARKET PLAYERS

A few major players of the Europe astaxanthin market include

- Koninklijke DSM N.V

- BASF SE

- Cyanotech Corporation

- Otsuka Pharmaceutical Co., Ltd

- Valensa International

- Fuji Chemical Industries Co., Ltd

- Divis Laboratories

- Beijing Ginkgo Group Igene Biotechnology, Inc

- Piveg, Inc

- Fenchem Biotek Ltd

Top strategies used by the key market participants

Key players in the Europe Astaxanthin Market focus on securing regulatory approvals under EU Novel Foods and organic certification to validate natural sourcing claims. They invest in advanced delivery technologies such as microencapsulation and lipid carriers to enhance bioavailability and stability in diverse applications. Companies expand European warehousing and technical support to ensure supply chain reliability and rapid response to customer needs. Strategic collaborations with cosmetic and nutraceutical brands enable co-development of science-backed formulations. Additionally, they emphasize sustainability through renewable energy, water recycling, and carbon footprint reduction to align with EU green policies and consumer expectations.

Leading Players in the Europe Astaxanthin Market

- Algatech is a leading producer of natural astaxanthin derived from Haematococcus pluvialis microalgae cultivated in closed photobioreactors in Israel, with strong distribution across Europe. The company supplies high-purity astaxanthin to premium nutraceutical, cosmetic, and aquaculture clients under its AstaPure brand, known for consistent 3S 3S’ stereochemistry and organic certification. It also partnered with German and French skincare laboratories to develop topical formulations targeting urban skin stress. These initiatives reinforce its global reputation for quality while deepening integration into Europe’s clean label and sustainable beauty ecosystems.

- BASF is a major global chemical company that produces synthetic astaxanthin primarily for the European aquaculture feed market under its Carophyll Pink brand. Despite regulatory bans on human consumption, BASF’s product remains vital for producing the characteristic pink color in farmed salmon across major production regions like Norway, Scotland, and Chile. The company also strengthened its technical support services for European feed mills, ensuring precise dosing and regulatory compliance. BASF sustains its position as a key enabler of sustainable, large-scale aquaculture through ongoing advancements in feed efficiency and environmental impact, even as natural alternatives gain popularity.

- Cyanotech is a US-based pioneer in natural astaxanthin production, supplying its BioAstin Hawaiian Astaxanthin to European health and wellness markets through strategic partnerships with supplement brands and distributors. The company’s algae are grown in open pond systems in Hawaii, yielding a full spectrum of carotenoids alongside astaxanthin, which enhances synergistic antioxidant effects. It also collaborated with Swiss and UK retailers to launch co branded product,s emphasizing traceability and solar-powered cultivation. Cyanotech reinforces its status as a trusted authority in the EU by bridging the gap between heritage-grade quality and innovative delivery systems.

MARKET SEGMENTATION

This research report on the Europe astaxanthin market has been segmented and sub-segmented based on source, application, method of production, and region.

By Source

- Plants

- Yeast & Microbes

- Marine

- Petroleum

By Application

- Supplements

- Animal Feed

- Cosmetics

- Food

By Method of Production

- Fermentation

- Microalgae Cultivation

- Extraction

- Chemical Synthesis

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe Astaxanthin Market?

Rising demand for natural antioxidants, increasing health awareness, growing nutraceutical consumption, and expanding use in cosmetics and aquaculture are major growth drivers.

2. Why is astaxanthin gaining popularity in Europe?

European consumers increasingly prefer natural and clean-label ingredients that support preventive healthcare, skin health, and wellness applications.

3. Which source segment dominates the Europe Astaxanthin Market?

Natural astaxanthin derived from microalgae such as Haematococcus pluvialis holds the largest market share due to strong consumer preference for natural products

4. What are the major applications of astaxanthin in Europe?

Astaxanthin is widely used in dietary supplements, cosmetics, aquaculture feed, pharmaceuticals, food and beverages, and animal nutrition products.

5. How is the nutraceutical industry supporting market growth?

Growing demand for antioxidant supplements and preventive healthcare products is increasing the use of astaxanthin in nutraceutical formulations

6. Why is astaxanthin used in cosmetics?

Astaxanthin is valued for its antioxidant and anti-aging properties, making it popular in skincare and personal care products.

7. What role does aquaculture play in the Europe Astaxanthin Market?

Astaxanthin is widely used in aquaculture feed to improve pigmentation, growth, and health of salmon, trout, and shrimp.

8. What challenges does the Europe Astaxanthin Market face?

High production costs, complex extraction methods, regulatory compliance, and raw material price fluctuations are major market challenges.

9. Which distribution channels are important in the market?

Pharmacies, specialty nutrition stores, online retail platforms, health stores, and direct sales channels are major distribution platforms.

10. What is the future outlook for the Europe Astaxanthin Market?

The market is expected to witness strong growth due to rising demand for natural antioxidants, expanding supplement consumption, and increasing applications in skincare and aquaculture industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com