Europe Auto Parts Market Size, Share, Trends, and Growth Analysis Report, Segmented by Component, Deployment, Enterprise Size, End-use, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

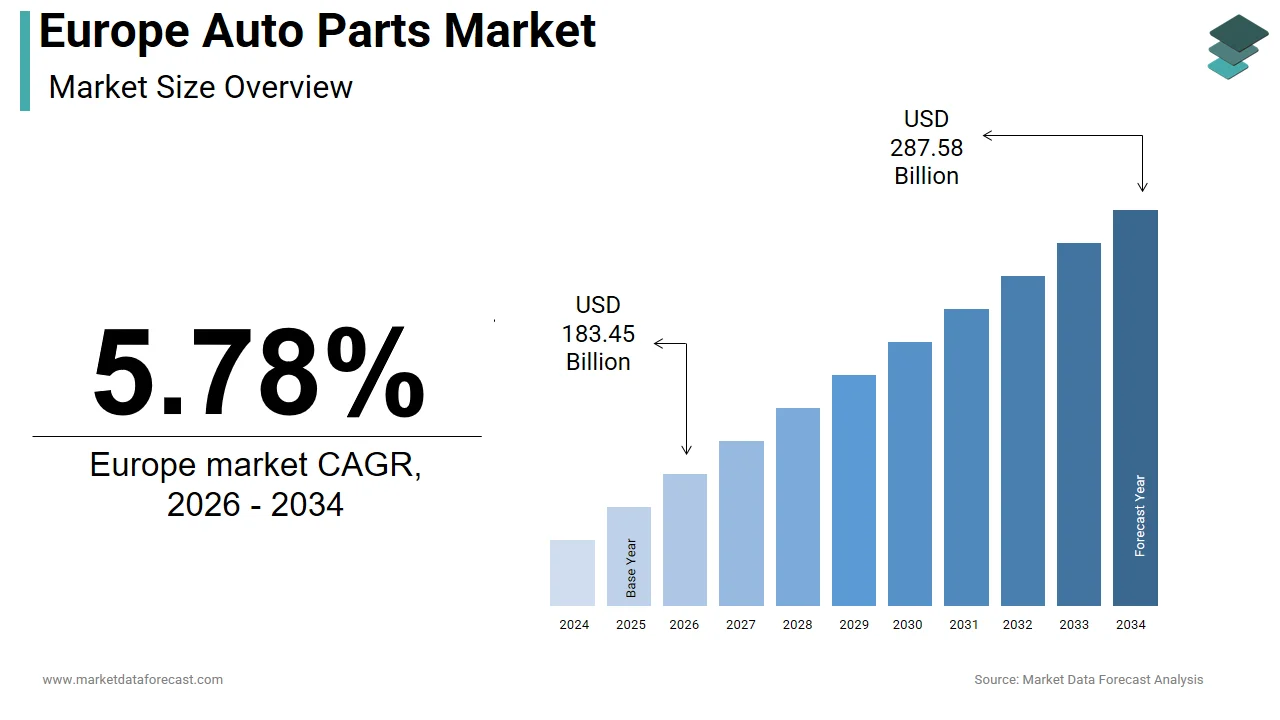

$173.43 BnMarket Estimate, 2026

$183.45 BnMarket Forecast, 2034

$287.58 BnCAGR, 2026–2034

5.78%Europe Auto Parts Market Report Summary

The Europe auto parts market was valued at USD 173.43 billion in 2025, is estimated to reach USD 183.45 billion in 2026, and is projected to reach USD 287.58 billion by 2034, growing at a CAGR of 5.78% from 2026 to 2034. Market growth is driven by the strong presence of automotive manufacturing hubs, increasing vehicle production, and rising demand for replacement parts and maintenance services. Auto parts include a wide range of components such as engine systems, braking systems, electrical components, and body parts that support vehicle manufacturing and aftermarket services. The ongoing transition toward electric vehicles, advancements in automotive technologies, and expansion of automotive supply chains are further supporting market expansion across Europe.

Key Market Trends

- Increasing demand for advanced automotive components and electronic systems.

- Growing adoption of electric vehicle components and battery-related parts.

- Rising demand for aftermarket replacement parts due to aging vehicle fleets.

- Expansion of automotive manufacturing and supplier networks across Europe.

- Increasing focus on lightweight materials and energy-efficient vehicle components.

Segmental Insights

- Based on end user, the OEM segment held a prominent share of the Europe auto parts market in 2025, driven by strong demand from automotive manufacturers for high-quality components used in vehicle production.

- Based on distribution channel, the offline distribution channel segment dominated the market in 2025, supported by the widespread presence of authorized dealerships, service centers, and traditional auto parts retailers.

Regional Insights

The Europe auto parts market is witnessing steady growth across major automotive manufacturing countries due to strong industrial capabilities and expanding vehicle production.

- Germany was the top performer in the regional market in 2025, driven by its world-leading automotive industry, strong supplier ecosystem, and major automotive OEM presence.

- France ranked second in the Europe auto parts market in 2025, supported by strong automotive production and established automotive component manufacturers.

- Italy is expected to experience notable growth due to its specialized supplier network and the increasing demand for replacement parts driven by an aging vehicle fleet.

Competitive Landscape

The Europe auto parts market is characterized by strong competition among global automotive component manufacturers and regional suppliers. Market players are focusing on product innovation, integration of advanced automotive technologies, and expansion of electric vehicle component portfolios. Strategic partnerships with automotive manufacturers, investments in research and development, and expansion of supply chains are shaping competitive dynamics across the region.

Prominent companies operating in the Europe auto parts market include 3M Co., AISIN Corp., Akebono Brake Industry Co. Ltd., Autoliv Inc., BorgWarner Inc., Brembo Spa, Bosch Group, Forvia SE, General Motors Co., HELLA GmbH and Co. KGaA, Hyundai Motor Co., Lear Corp., Magna International Inc., Marelli Holdings Co. Ltd., Robert Bosch GmbH, Schaeffler AG, Tenneco Inc., The Goodyear Tire and Rubber Co., Toyota Motor Corp., Valeo SA, ZF Friedrichshafen AG, and Marelli Holdings.

Europe Auto Parts Market Size

The size of the Europe auto parts market was worth USD 173.43 billion in 2025. The regional market is anticipated to grow at a CAGR of 5.78% from 2026 to 2034 and be worth USD 287.58 billion by 2034 from USD 183.45 billion in 2026.

The auto parts are the replacement of components used in passenger vehicles, commercial vehicles, and two-wheelers. This includes mechanical, electrical, electronic, and structural elements, ranging from engine systems and braking components to advanced driver assistance sensors and battery modules. Europe hosts over 13,000 automotive suppliers employing more than 2 million people, as per the European Automobile Manufacturers Association. The region’s vehicle parc exceeds 260 million units with an average age of 12.1 years, according to Eurostat 2025 data, indicating robust demand for maintenance and replacement parts. Furthermore, the EU’s End of Life Vehicles Directive requires 95% of each vehicle to be recovered or recycled by 2035, compelling manufacturers to design parts for disassembly and reuse. These structural and regulatory dynamics position the Europe auto parts market not merely as a support sector but as a critical enabler of mobility, sustainability, and industrial innovation.

MARKET DRIVERS

Accelerated Electrification Mandates Drive Demand for High Voltage Components

The EU’s binding phase out of internal combustion engine vehicles by 2035 has triggered unprecedented investment in electric powertrain infrastructure, which is propelling the growth of Europe auto parts market. Every new battery electric vehicle requires approximately 80 kilograms of specialized high voltage components, including inverters, DCDC converters, on-board chargers, and battery management systems, as per the research. Tier one suppliers like Bosch and Valeo have retooled legacy plants to produce silicon carbide-based power electronics, which offer 10% greater energy efficiency than traditional silicon variants. This systemic shift is not incremental but transformative, converting the auto parts market from a mechanical domain into an electrified digital ecosystem.

Rising Vehicle Age Intensifies Aftermarket Replacement Demand

The aging vehicle fleet requires replacement parts, as older cars require more frequent maintenance and component renewal. The average age of light-duty vehicles in the EU reached 12.1 years in 2025, according to Eurostat, surpassing the 10 year threshold, where failure rates for critical systems like suspension, steering, and exhaust double. In Italy, over 45% of registered vehicles are older than 12 years, as per ISTAT, leading to a 28% increase in independent workshop visits between 2022 and 2024. Similarly, Poland reported a 33% rise in brake pad and shock absorber sales in 2024, driven by its 14.3 year average vehicle age as documented by the Polish Automotive Industry Association. Unlike new vehicle production, which is shifting to electric platforms, the aftermarket remains dominated by internal combustion models, ensuring continued demand for conventional parts. This demographic inertia provides a stable revenue base for distributors and repair networks even as OEMs pivot toward future technologies.

MARKET RESTRAINTS

Stringent Right to Repair Legislation Disrupts OEM-Controlled Supply Chains

The EU’s Right to Repair Directive, enacted in 2023, mandates that automakers provide independent repairers with full access to diagnostic tools, software updates, and spare parts for up to 15 years after a model’s launch. While intended to empower consumers, this regulation has fragmented OEM spare parts strategies and eroded captive channel margins. In 2024, Volkswagen Group reported a 12% decline in its authorized dealer parts revenue due to third-party workshops sourcing identical components through alternative channels as per its annual financial disclosure. Compliance costs are also substantial, where Stellantis invested 85 million euros in 2025 to develop a secure digital parts portal meeting EU interoperability standards, according to company statements. Moreover, the requirement to stock parts for 15 years strains inventory management, particularly for discontinued models with low turnover. These operational complexities are forcing manufacturers to rethink lifetime value models and explore service-based revenue streams beyond hardware sales.

Geopolitical Fragmentation of Critical Raw Material Supply

The acute vulnerability due to its dependence on imported minerals essential for both conventional and electric components is additionally limiting the growth of Europe auto parts market. Over 90% of the EU’s cobalt and 98% of its rare earth elements used in electric motors and sensors are sourced from China and the Democratic Republic of Congo, as per the European Commission’s Raw Materials Act assessment. The 2024 export restrictions imposed by China on gallium and germanium, key for semiconductor production, delayed the rollout of next-generation ADAS systems by 6 to 8 weeks across multiple German and French OEMs, according to the VDA German Automotive Industry Association. Similarly, Russia’s control over 25% of global palladium supply used in catalytic converters caused exhaust system costs to spike by 18% in 2023, as per the European Environment Agency.

MARKET OPPORTUNITIES

Circular Remanufacturing Gains Traction Under Eco Design Rules

The revised Eco Design for Sustainable Products Regulation now requires all automotive components to be designed for durability, reparability, and remanufacturing by 2027. This factor is attributed to creating new opportunities for the growth of Europe auto parts market. A remanufactured part uses 85% less energy and generates 80% fewer emissions than a new equivalent, according to the Joint Research Centre of the European Commission. In Sweden, Volvo Cars’ remanufacturing program recovered over 22 000 engines and gearboxes in 2024, achieving a 92% functional equivalence rate as verified by its sustainability report. Meanwhile, Germany’s ZF Group operates Europe’s largest remanufacturing hub in Friedrichshafen, processing 150 000 transmissions annually with a 30% cost advantage over new units. These closed-loop systems not only reduce environmental impact but also create resilient secondary supply chains insulated from raw material volatility.

Integration of AI-Driven Predictive Maintenance Platforms

Automotive suppliers are embedding artificial intelligence into vehicle components to enable real-time health monitoring and predictive failure alerts. Bosch’s Smart Sensor Suite, deployed in over 3 million European vehicles by 2025, analyzes vibration, temperature, and load patterns to forecast bearing or brake wear up to 6,000 kilometers in advance as per internal telemetry data. This capability transforms the parts market from reactive replacement to proactive service, triggering automatic part orders and workshop bookings. Continental’s AI-powered tire pressure monitoring system reduced unscheduled roadside failures by 41% in a 2024 pilot across Dutch logistics fleets, according to the company’s mobility division. As 5G connectivity expands, these intelligent components will feed data into centralized platforms, allowing insurers, fleet operators, and retailers to optimize inventory and service scheduling. This evolution positions auto parts not as static hardware but as dynamic nodes in a connected mobility ecosystem.

MARKET CHALLENGES

Semiconductor Shortages Expose Fragile Electronics Dependency

The global semiconductor supply instability is ascribed to be a challenge for the growth of Europe auto parts market. Modern vehicles contain between 1,400 and 3,000 chips, depending on automation level, and the average lead time for automotive-grade microcontrollers remains at 22 weeks, as per the European Semiconductor Industry Association in early 2025. In 2024, production delays at NXP’s Hamburg fab due to power grid fluctuations caused a three-week halt in ABS module deliveries, affecting BMW and Mercedes assembly lines, as reported by Handelsblatt. The EU’s Chips Act aims to boost regional capacity, but its 2030 target of 20% global semiconductor production still leaves Europe reliant on Asian foundries for advanced nodes. Until vertical integration or strategic stockpiling mechanisms are implemented, electronic component shortages will remain a systemic risk disrupting everything from infotainment to safety systems.

Skills Gap in Electrified and Digital Component Servicing

The rapid transition to electric and software-defined vehicles has created a severe shortage of technicians qualified to handle high-voltage systems and over-the-air diagnostics. The skills gap in electrified and digital component servicing is also hindering the growth of Europe auto parts market. The European Automobile Manufacturers Association estimates a deficit of 500,000 certified EV technicians by 2027. Germany’s dual education system has expanded mechatronics apprentice ships, but the pipeline remains insufficient to meet demand from both OEMs and aftermarket networks. Bosch alone trained 12,000 technicians in 2025, yet this covers less than 5% of Europe’s workshop base as per its training division. Without urgent investment in vocational curricula and safety accreditation, this human capital gap will constrain vehicle uptime and undermine consumer confidence in new mobility technologies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Deployment, Enterprise Size, End-use, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Amazon.com, Inc., CleanWhale GmbH, Rentokil Initial plc, Rollins, Inc., Dwyer Franchising LLC (Drain Doctor), Aquevo, 1st Online Solutions Limited, Hello Services Ltd., Checkatrade, Helpling, Homelike, DSP Drainage and Plumbing Ltd., Flo-Well Drainage and Plumbing Limited, Le Marche Home Services, and Others. |

SEGMENTAL ANALYSIS

By End User Insights

The OEM segment accounted in holding 58.2% of the Europe auto parts market share in 2024. OEMs maintain long-term contractual relationships with tier one suppliers, ensuring consistent high-volume orders tied to vehicle production schedules. In 2024, Germany produced 3.1 million passenger cars, according to the German Federal Motor Transport Authority, requiring over 150 million individual components per year from certified suppliers. These parts must meet exacting specifications under ISO TS 16949 quality standards and are often co-engineered during vehicle development. For instance, every Volkswagen ID series vehicle integrates over 200 electrically actuated components sourced exclusively from pre-qualified OEM partners, as documented in the company’s 2024 supply chain report. This deep integration creates a captive ecosystem where aftermarket alternatives cannot compete on fitment or warranty compliance, especially for safety-critical systems like airbags and electronic stability control modules.

EU type approval regulations grant OEMs exclusive rights to supply certain safety and emissions-related parts for the first three years or 100,000 kilometers of a vehicle’s life. During this period, independent repairers must source these components directly from manufacturers or authorized distributors. In 2025, France’s Directorate General for Competition Policy, Consumer Affairs, and Fraud Control confirmed that most of all brake calipers and exhaust gas recirculation valves installed in vehicles under warranty were OEM-supplied. This legal framework ensures steady revenue streams for OEM-aligned channels and delays aftermarket penetration until vehicles age beyond initial ownership cycles.

The aftermarket segment is projected to expand at a CAGR of 6.8% from 2025 to 2033. Europe’s light-duty vehicle parc now averages 12.1 years, according to Eurostat 2025 data, with over 40% of vehicles exceeding 12 years of age. These older models are no longer under manufacturer warranty and are increasingly maintained through independent workshops that rely on cost-effective aftermarket parts. In Poland, where the average vehicle age is 14.3 years, aftermarket part sales grew by 11.2% in 2024, as per the study. The EU’s Right to Repair Directive has mandated full access to diagnostic software and technical documentation for independent garages since 2023. Platforms like TecAlliance and Autodata now provide real-time part cross-referencing and installation guides to over 180,000 European workshops, as per their 2025 user metrics. In Spain, over 65% of independent garages reported increased confidence in installing non-OEM ADAS sensors in 2024 due to standardized calibration protocols released under EU interoperability rules, as confirmed by the Spanish Federation of Automotive Trade Associations. This institutional support is dismantling OEM monopolies and accelerating aftermarket adoption across previously restricted categories.

By Distribution Channel Insights

The offline distribution channel segment held a prominent share of the Europe auto parts market in 2025. Professional repair shops require same-day or next-hour access to parts to maintain workflow efficiency and customer satisfaction. In Germany, over 85% of independent workshops source more than 60% of their parts from local physical warehouses operated by groups like AutoDoc and Bilstein, as per a 2024 survey. These outlets maintain extensive SKUs and offer technical consultation on site capabilities that online platforms cannot replicate for complex diagnostics. The average downtime cost for a commercial fleet vehicle is 280 euros per hour, according to the study, by making rapid physical access to alternators, fuel pumps, or turbochargers economically non-negotiable for professional users. For safety-critical components, such as brake master cylinders or steering racks, mechanics prefer inspecting parts in person before installation. Physical distributors mitigate this through certified packaging, authorized dealer status, and return policies that build long term trust. In Sweden, major chains like Mekonomen operate over 400 service-integrated stores, where parts can be tested and installed on premises, a model that combines retail assurance with technical validation unavailable in pure e-commerce environments.

The online distribution channel is expected to witness the fastest CAGR of 12.3% from 2025 to 2033. Leading e-retailers like Mister Auto and Oponeo use machine learning algorithms to predict regional demand and pre-position inventory in micro-fulfillment centers. In 2025, Oponeo reduced average delivery time to 14 hours in urban France by deploying AI-driven demand forecasting that analyzes vehicle registration data, seasonal failure patterns, and weather conditions as per company logistics disclosures. These platforms also offer VIN-specific part matching, eliminating compatibility errors that plagued early online adoption. Younger car owners in cities like Berlin, Amsterdam, and Copenhagen are increasingly performing basic maintenance themselves using online tutorials and mobile diagnostics. Platforms respond with value-added services such as installation videos, AR-guided assembly, and chat-based technical support.

COUNTRY LEVEL ANALYSIS

Germany Auto Parts Market Analysis

Germany was the top performer in the Europe auto parts market by holding 22.3% of the market share in 2024 with its dense manufacturing base and engineering excellence. The country hosts over 700 automotive suppliers, including global leaders like Bosch, ZF, and Mahle employing more than 850,000 people, as per the study. Germany produced 3.1 million passenger cars in 2024, requiring a continuous flow of high precision components, many of which are exported as original equipment. The federal government’s 2025 Mobility Transition Fund allocated 2.3 billion euros to support SMEs in developing electric and hydrogen-compatible parts, reinforcing domestic innovation. Additionally, Germany’s robust independent repair sector, comprising over 38,000 workshops, ensures strong aftermarket demand for premium replacement components that match OEM quality standards.

France Auto Parts Market Analysis

France held second position by holding 16.3% of the Europe auto parts market share in 2024, with the strong policy-driven electrification and domestic manufacturing. The nation’s Automotive Recovery Plan has invested over 8 billion euros since 2020 to localize battery and powertrain component production, as confirmed by the French Ministry of Economy and Finance. Renault’s Douai gigafactory alone will produce 400,000 electric motors annually by 2026, creating downstream demand for inverters and thermal management systems. France also enforces strict anti-counterfeiting laws, with customs seizing 1.2 million fake auto parts in 2024, according to the Directorate General of Customs and Indirect Taxes, protecting both consumers and legitimate manufacturers.

Italy Auto Parts Market Analysis

Italy auto parts market growth is likely to grow with its specialized supplier network and aging vehicle fleet. The country is home to over 12,000 automotive SMEs concentrated in the Emilia, Romagna, and Piedmont regions, producing high-performance components for luxury and racing brands, as per Confindustria’s 2025 industrial census. Simultaneously, Italy’s average vehicle age of 12.8 years is the highest in Western Europe, which fuels robust aftermarket demand with brake and suspension part sales growing by 9.4% in 2024. Companies like Brembo and Marelli leverage this duality by supplying both Ferrari and Lamborghini and millions of everyday commuters.

United Kingdom Auto Parts Market Analysis

The United Kingdom auto parts market growth is expected to have prominent growth opportunities in foreseen years with its strong aftermarket culture and post Brexit trade adaptations. The British vehicle parc exceeds 39 million units with an average age of 9.2 years, driving consistent replacement demand. Online retailers like Euro Car Parts and Halfords have expanded same-day delivery networks to over 500 locations by enabling rapid response to workshop needs. The UK’s Vehicle Certification Agency also maintains rigorous type approval standards, ensuring that aftermarket parts meet safety benchmarks comparable to EU regulations, thereby preserving consumer trust in non-OEM components.

Spain Auto Parts Market Analysis

Spain auto parts market growth is likely to grow with its role as a manufacturing hub and growing domestic demand. Major OEMs, including SEAT, Stellantis, and Ford, operate integrated plants that source over 60% of components locally, creating a resilient supplier ecosystem. Additionally, Spain’s warm climate accelerates wear on cooling and exhaust systems, leading to 15% higher replacement rates for radiators and catalytic converters compared to Nordic countries, as documented by the Spanish Institute for Automotive Research. Government incentives for scrappage and EV adoption are further stimulating both new and replacement part markets across urban and rural regions.

COMPETITIVE LANDSCAPE

The Europe auto parts market exhibits a highly stratified yet intensely competitive structure dominated by a few multinational tier one suppliers alongside thousands of specialized SMEs. At the apex, Bosch ZF and Continental set global benchmarks in technology and scale, while mid-tier players like Valeo and Marelli compete through niche expertise in lighting, thermal systems, or cockpit electronics. Simultaneously, a vast network of independent manufacturers supplies cost-effective alternatives for the aftermarket, particularly in Southern and Eastern Europe. Competition is no longer confined to price or quality but extends to software capabilities, sustainability credentials, and speed of innovation. Regulatory pressures, including the EU’s Right to Repair Directive and End of Life Vehicles Regulation, have leveled the playing field for smaller players but raised compliance costs across the board. Meanwhile, the shift to electric and autonomous vehicles is redrawing value chains, favoring those with semiconductor partnerships and AI talent.

KEY MARKET PLAYERS

The leading companies operating in the Europe auto parts market include:

- 3M Co.

- AISIN Corp.

- Akebono Brake Industry Co., Ltd.

- Autoliv Inc.

- BorgWarner Inc.

- Brembo Spa

- Bosch Group

- Forvia SE

- General Motors Co.

- HELLA GmbH and Co. KGaA

- Hyundai Motor Co.

- Lear Corp.

- Magna International Inc.

- Marelli Holdings Co. Ltd.

- Robert Bosch GmbH

- Schaeffler AG

- Tenneco Inc.

- The Goodyear Tire and Rubber Co.

- Toyota Motor Corp.

- Valeo SA

- ZF Friedrichshafen AG

- Marelli Holdings

TOP PLAYERS IN THE MARKET

- Bosch Group is a German multinational engineering and technology company that serves as a cornerstone of the global automotive supply chain. It supplies advanced components ranging from electronic control units and braking systems to electric powertrain modules and hydrogen fuel cell stacks. Bosch plays a critical role in shaping vehicle safety and electrification standards worldwide through its R and D investments and participation in international regulatory bodies. In recent years, Bosch has accelerated its transition toward software-defined mobility by launching its own operating system for electric vehicles and expanding its AI-driven predictive maintenance platforms.

- ZF Friedrichshafen AG is a leading German supplier of driveline and chassis technology with a strong footprint in both conventional and electric mobility systems. The company is globally recognized for its advanced transmissions, active safety systems, and autonomous driving solutions deployed across passenger and commercial vehicles. ZF contributes significantly to global decarbonization efforts through its scalable electric axle drives and regenerative braking technologies. It inaugurated a dedicated e-mobility campus in Saarbrücken, Germany, focused on integrated electric drivetrains and software-defined vehicle architectures, aligning with Europe’s zero-emission vehicle mandates and global OEM electrification roadmaps.

- Marelli Holdings is an Italy-Japan headquartered automotive supplier specializing in lighting systems, cockpit electronics, thermal management, and electric vehicle components. The company leverages its dual heritage to serve a diverse portfolio of European, Asian, and American automakers with localized engineering support. Marelli is a key enabler of vehicle personalization and human-machine interface innovation through its adaptive LED lighting and smart surface technologies. Recently, the company expanded its thermal management capabilities to support high-performance battery cooling in premium EVs and established a circular economy lab in Turin to develop remanufactured electronic control units. These initiatives position Marelli at the intersection of sustainability, digitalization, and user-centric design in the evolving auto parts landscape.

MARKET SEGMENTATION

This research report on the Europe auto parts market has been segmented and sub-segmented into the following categories.

By Component

- Software

- Services

By Deployment

- Cloud

- On-premises

By Enterprise Size

- Small & Medium Enterprises

- Large Enterprises

By End-use

- Automotive & Transportation

- Manufacturing

- Aerospace & Defense

- BFSI

- Energy & Utilities

- Retail & E-commerce

- Healthcare

- IT & Telecommunication

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe auto parts market?

The Europe auto parts market manufactures engine, brake, and transmission components for OEMs and repairs. Passenger cars dominate demand across Western Europe.

How does the Europe auto parts market function?

The Europe auto parts market functions through OEM supply chains and independent aftermarket distributors. Digital platforms streamline parts ordering regionally.

What drives growth in the Europe auto parts market?

EV adoption drives the Europe auto parts market alongside aging vehicle fleets. Emission regulations boost demand for advanced aftermarket components.

Which countries lead the Europe auto parts market?

Germany dominates the Europe auto parts market through manufacturing strength. France and Italy follow with robust automotive production ecosystems.

What segments define the Europe auto parts market?

Engine and powertrain parts lead the Europe auto parts market alongside braking systems. Electrical components grow rapidly with vehicle electrification.

How does regulation shape the Europe auto parts market?

EU safety standards govern the Europe auto parts market ensuring component reliability. Emission directives favor the adoption of lightweight materials.

What role does aftermarket play in the Europe auto parts market?

Aftermarket sustains the Europe auto parts market, serving vehicle repairs and maintenance. Independent workshops drive replacement parts demand.

What trends influence the Europe auto parts market?

Electrification transforms the Europe auto parts market requiring battery and motor components. Remanufacturing gains traction for sustainability.

What challenges face the Europe auto parts market?

Supply chain disruptions challenge the Europe auto parts market though localization helps. Asian competition pressures pricing strategies.

How has EV transition impacted the Europe auto parts market?

EV growth reshapes the Europe auto parts market prioritizing power electronics over engines. Battery components create new supply opportunities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com