Europe Automotive Aftermarket Market Size, Share, Trends & Growth Forecast Report, Segmented By Replacement Type, Service Channel, Distribution Channel, Certification and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$144.68 BnMarket Estimate, 2026

$153.87 BnMarket Forecast, 2034

$251.79 BnCAGR, 2026–2034

6.35%Europe Automotive Aftermarket Market

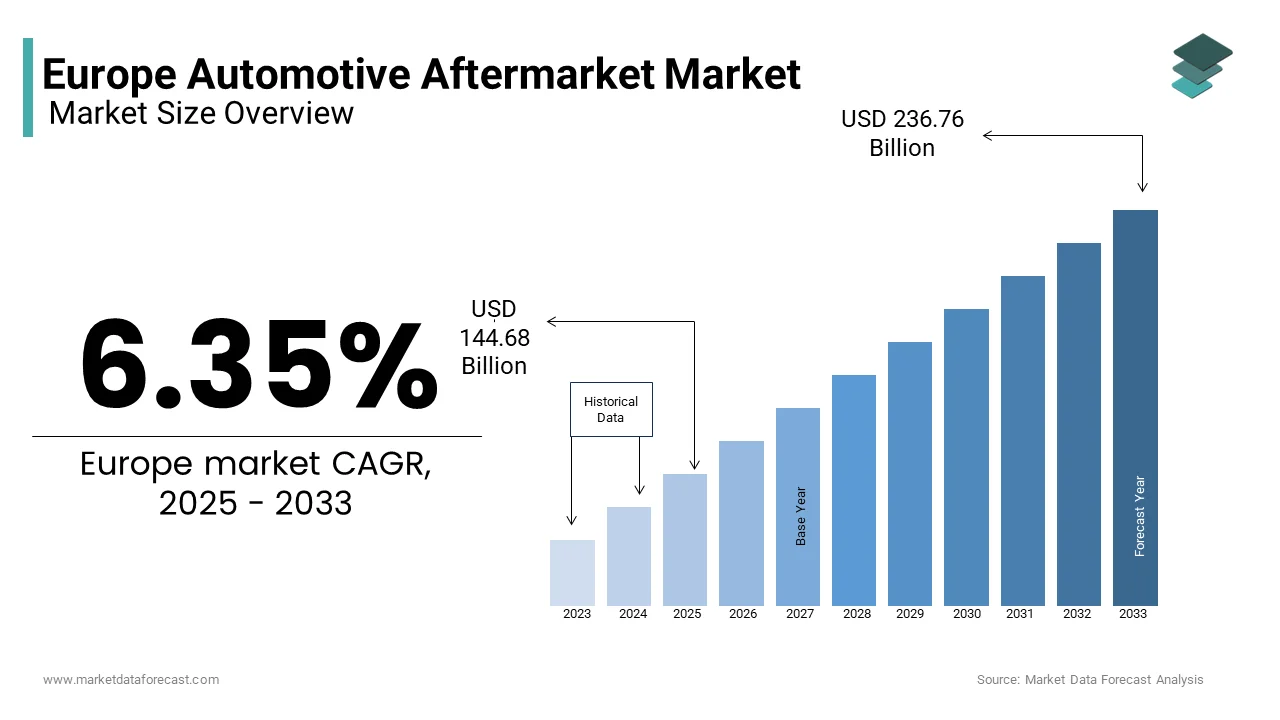

The European automotive aftermarket market size was valued at USD 144.68 billion in 2025 and is projected to grow from USD 153.87 billion in 2026 to USD 251.79 billion by 2034, at a CAGR of 6.35% (2026–2034). The market is expanding due to the aging vehicle fleet, increasing demand for vehicle customization, and the growth of digital sales channels across Europe.

Key Market Trends

- Rising demand for electric vehicle aftermarket parts and services.

- Growing penetration of e-commerce platforms in auto parts distribution.

- Increasing consumer preference for Do-It-For-Me (DIFM) services.

- Expansion of data-driven predictive maintenance solutions in vehicle servicing.

Segmental Insights

- Based on replacement parts, the tyres segment dominated with 28.3% share in 2024, driven by replacement cycles and rising demand for high-performance tyres.

- Based on service channel, the DIFM (Do-It-For-Me) segment captured a prominent share in 2024 as professional service centers remain the preferred option for vehicle owners.

- Based on distribution channel, the wholesalers & distributors segment led the market with 58.6% share in 2024, benefitting from strong networks and supply chain integration.

- Based on certification, the Uncertified parts segment accounted for the largest share at 47.6% in 2024, as cost-sensitive customers increasingly opt for affordable alternatives.

Regional Insights

- Germany led the European automotive aftermarket with a 21.3% share in 2024, supported by its large automotive industry base.

- France and the UK are showing strong growth, driven by rising e-commerce adoption and premium service providers.

- Southern and Eastern Europe are witnessing accelerating demand due to vehicle aging trends and expanding repair networks.

Competitive Landscape

Key companies in the Europe automotive aftermarket market include Continental AG, ZF Friedrichshafen AG, HELLA KGaA Hueck & Co., ThyssenKrupp AG, Mahle GmbH, Delphi Tech, Valeo Group, Faurecia, Gestamp, Magna International Inc., and Lear Corp. Bosch stands as the largest automotive aftermarket company in Europe, employing 400,000 people across 440 companies in 60 countries, and generating USD 91.8 billion in revenue.

Europe Automotive Aftermarket Market Size

The European automotive aftermarket market size was valued at USD 144.68 billion in 2025. The European market size is anticipated to reach USD 153.87 billion in 2026 from USD 251.79 billion by 2034, growing at a CAGR of 6.35% during the forecast period from 2026 to 2034.

The Automotive Aftermarket is the distribution and installation of vehicle parts, components, and services for passenger cars and light commercial vehicles post-original equipment manufacturer (OEM) production. It includes replacement parts, maintenance, repair, and customization solutions provided through independent workshops, dealership service centers, and retail chains. As of 2023, the average age of the passenger car fleet across the European Union exceeded 12.7 years, as reported by the European Automobile Manufacturers’ Association (ACEA), indicating a growing reliance on repair and maintenance rather than new vehicle acquisition. This aging fleet is a structural underpinning of aftermarket demand, as vehicles beyond their warranty periods require more frequent servicing and part replacements.

MARKET DRIVERS

Expanding Vehicle Fleet Age and Prolonged Ownership Cycles

The rising average age of the passenger car fleet directly correlates with increased maintenance and component replacement frequency. As of 2023, the average age of cars in Europe reached 12.7 years, according to the European Automobile Manufacturers’ Association (ACEA), marking a steady upward trend from 10.5 years in 2013. This aging reflects prolonged vehicle ownership, driven by economic pressures and improved vehicle durability. Older vehicles require more frequent replacement of wear-and-tear components such as brakes, exhaust systems, and suspension parts. Additionally, as vehicles exit OEM warranty periods, typically after three to five years, consumers increasingly turn to independent service providers and non-OEM parts to reduce costs.

Rising Prevalence of Vehicle Inspections and Regulatory Compliance Requirements

Mandatory vehicle inspection regimes are additionally expected to enhance the growth of the Europe Automotive Aftermarket market. As of 2023, over 180 million vehicles in the EU were subject to these inspections, as reported by the European Commission’s Directorate-General for Mobility and Transport. Failures in these tests, particularly related to emissions, lighting, brakes, and tire conditions, necessitate immediate repairs, directly stimulating aftermarket activity. For instance, Germany’s KBA reported that in 2022, nearly 18% of all HU inspections failed, with brake system defects being the most common issue, affecting over 4.1 million vehicles. Similarly, in France, UTAC noted that 22% of vehicles failed their initial technical inspection, with exhaust and emission control systems being the primary contributors.

MARKET RESTRAINTS

Increasing Reliability and Durability of Modern Vehicles

The enhanced reliability and extended service intervals of modern vehicles, which reduce the frequency of part replacements and maintenance visits, are limiting the growth of the Europe Automotive Aftermarket market. Contemporary automobiles, particularly those manufactured after 2015, incorporate advanced materials, precision engineering, and predictive diagnostics that significantly prolong component lifespans. Furthermore, OEMs have extended standard warranties from three to five years, and in some cases up to seven years, as seen with brands like Hyundai and Kia, which limits early aftermarket access. Bosch Automotive Aftermarket division noted in its 2023 service trends report that average service intervals for engine oil changes have increased from 15,000 km to over 30,000 km in many new models, effectively halving maintenance frequency. Additionally, the integration of sealed-for-life components in electric and hybrid vehicles further diminishes demand for traditional consumables.

Stringent Intellectual Property and Technical Access Barriers

The restrictive access to vehicle repair data, diagnostic software, and proprietary components controlled by OEMs is also limiting the growth of the Europe Automotive Aftermarket market. According to the European Association of Automotive Suppliers (CLEPA), over 60% of repair-related data is either partially or fully restricted by manufacturers, which limits the ability of third-party workshops to perform comprehensive servicing. This issue is particularly acute with advanced driver assistance systems (ADAS) and connected vehicle technologies, where recalibration requires OEM-specific tools. A 2023 study by the European Competition Network (ECN) revealed that 74% of independent garages reported delays in accessing software updates, averaging 4.8 weeks behind dealership availability.

MARKET OPPORTUNITIES

Expansion of Digital Platforms and E-Commerce in Aftermarket Distribution

The digitization of procurement and service delivery channels is creating new opportunities for the growth of the Europe Automotive Aftermarket. Major players such as Bosch Automotive Aftermarket, Euro Car Parts, and Amazon Automotive have invested heavily in digital marketplaces that offer real-time inventory, technical compatibility checks, and same-day delivery. In Germany, the online share of aftermarket parts sales exceeded 30% in 2023, driven by B2B platforms like TecAlliance and Hella Gutmann Solutions, which integrate cataloging and ordering systems directly into workshop management software. Additionally, the adoption of AI-powered diagnostic tools and mobile service apps enables remote troubleshooting and part recommendations, enhancing customer engagement. According to Statista, the number of active users on automotive e-commerce platforms in Europe surpassed 48 million in 2023, with a compound annual growth rate of 14.3% since 2020.

Growth in Hybrid and Plug-In Vehicle Aftermarket Services

The electric vehicles (EVs) reduce demand for traditional mechanical components with the rising fleet of hybrid and plug-in hybrid electric vehicles (PHEVs), which is expected to boost the growth of the Europe Automotive Aftermarket market. As of 2023, hybrid vehicles accounted for 18.7% of new car registrations in the EU, totaling over 2.9 million units, according to the European Environment Agency (EEA). The European Association of Automotive Suppliers (CLEPA) estimates that the service complexity of PHEVs is approximately 35% higher than that of conventional vehicles, generating demand for trained technicians and certified repair equipment. High-voltage battery degradation, for instance, becomes an issue after 8–10 years, with studies by the Fraunhofer Institute indicating that 22% of PHEV batteries show capacity loss exceeding 20% by 2028. This creates a growing market for battery diagnostics, refurbishment, and replacement services. Furthermore, the lack of standardized recycling and second-life frameworks means that independent players can develop reverse logistics and remanufacturing capabilities.

MARKET CHALLENGES

Workforce Shortage and Skills Gap in Technical Expertise

The acute shortage of skilled technicians capable of servicing increasingly complex vehicle systems is hindering the growth of the Europe Automotive Aftermarket market. Eurostat data from 2023 indicates that the EU faces a deficit of over 145,000 qualified automotive technicians, with Germany alone reporting a shortfall of 28,000 mechanics. This gap is exacerbated by an aging workforce; nearly 42% of active automotive technicians in Europe are over the age of 50, as per the European Centre for the Development of Vocational Training (Cedefop). A 2023 report by the European Automotive Skills Forum revealed that only 37% of independent workshops have at least one technician certified in high-voltage system repair. This deficiency limits their ability to service hybrid and electric vehicles, pushing consumers toward OEM dealerships. The situation is further complicated by the lack of standardized training curricula across EU member states, despite the European Commission’s efforts under the Pact for Skills initiative. Bosch’s 2023 technician survey found that 68% of garages delayed investments in new diagnostic equipment due to insufficient staff expertise.

Proliferation of Counterfeit and Substandard Automotive Parts

The widespread circulation of counterfeit and substandard components, with regard to the integrity and safety, also hinders the growth of the Europe Automotive Aftermarket market. According to Europol’s 2023 Intellectual Property Crime Report, automotive parts ranked among the top five most commonly counterfeited goods in the EU, with seizures of fake brake pads, filters, and lighting units increasing by 38% between 2021 and 2023. In Italy, the Guardia di Finanza confiscated over 1.2 million counterfeit automotive components in 2022, many originating from illicit supply chains in Eastern Europe and Asia. A study by TÜV Rheinland in 2023 found that 27% of non-OEM brake pads tested in independent workshops across Central Europe did not comply with minimum friction and wear requirements. The economic impact is substantial: the European Intellectual Property Office (EUIPO) estimated that counterfeit automotive parts cost the legitimate industry over €4.3 billion annually in lost revenue and warranty claims. Moreover, the rise of unregulated online marketplaces has facilitated the distribution of these goods, with platforms like AliExpress and eBay facing repeated scrutiny from national enforcement agencies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.35% |

| Segments Covered | By Replacement Type, Service Channel, Distribution Channel, Certification, and Region. |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Continental AG (Germany), ZF Friedrichshafen AG (Germany), HELLA KGaA Hueck & Co. (Germany), ThyssenKrupp AG (Germany), Mahle GmbH (Germany), Delphi Tech (UK), Valeo Group (France), Faurecia (France), Gestamp (Spain), Magna International Inc (Canada), Lear Corp (US), and Others. |

SEGMENTAL ANALYSIS

By Replacement Part Insights

The tyres segment accounted in holding 28.3% of the Europe Automotive Aftermarket market in 2024, which is significantly reinforced by legal and climatic requirements across Europe that mandate seasonal tyre changes. In countries such as Germany, Austria, and Sweden, winter tyre laws require vehicles to be equipped with approved cold-weather tyres during specific months, effectively doubling the replacement frequency for a large portion of the fleet. According to the German Federal Road Research Institute (BASt), over 38 million vehicles in Germany were fitted with winter tyres in 2023, with an average replacement cycle of every 4–5 years or 40,000 km. Additionally, the EU’s tyre labelling regulation (EU No 2020/740) has heightened consumer awareness regarding rolling resistance, wet grip, and noise levels, prompting upgrades to higher-performance models.

The turbocharger segment is expected to grow with a CAGR of 7.2% during the forecast period, with the near-ubiquity of turbocharged petrol and diesel engines in modern European passenger cars. According to data from Bosch Mobility Solutions, over 78% of new petrol vehicles registered in the EU in 2023 were equipped with turbocharged engines, up from just 32% in 2013. This technological shift, aimed at reducing CO₂ emissions through engine downsizing, has created a vast installed base of turbo-dependent vehicles entering high-mileage phases where turbo failure becomes increasingly likely. The average service life of a turbocharger is between 120,000 and 150,000 km, and with the average European vehicle accumulating over 13,000 km annually (as per Eurostat), a growing number are reaching wear thresholds.

By Service Channel Insights

The DIFM (Do-It-For-Me) channel segment accounted for a prominent share of the Europe Automotive Aftermarket market in 2024. Modern automobiles are now rolling computers, which are integrating hundreds of electronic control units (ECUs), advanced driver assistance systems (ADAS), and proprietary software that require specialized tools and expertise for servicing. According to a 2023 study by the German Association of the Automotive Industry (VDA), over 90% of new vehicles sold in Europe feature ADAS functionalities such as adaptive cruise control and lane-keeping assist, which demand recalibration after even minor front-end repairs. This level of sophistication is beyond the capability of most DIY enthusiasts. Bosch Automotive Aftermarket data indicates that 74% of independent workshops now use OEM-level diagnostic scanners, compared to just 42% in 2018, highlighting the professionalization of the service ecosystem. Furthermore, incorrect calibration or software flashing can void warranties or compromise safety, deterring consumers from self-repair.

The OE (Original Equipment) service delegation segment is projected to expand at a CAGR of 6.8% from 2025 to 2033. Automotive manufacturers are deploying embedded telematics and over-the-air (OTA) updates to maintain post-sale control over vehicle servicing. As per data from McKinsey, over 85% of new vehicles delivered in Europe in 2023 were equipped with embedded connectivity modules that monitor vehicle health and automatically schedule service appointments with OEM networks.

By Distribution Channel Insights

The wholesalers & distributors segment was the largest by accounting for 58.6% of the Europe Automotive Aftermarket market share in 2024. Wholesalers maintain a strategic advantage through their extensive network of regional depots and just-in-time delivery capabilities, which cater to the operational needs of over 280,000 independent repair workshops across Europe, according to the Federation of Independent European Distributors (FIED). These workshops, which handle the majority of non-warranty repairs, rely on wholesalers for rapid access to a broad inventory of parts, often requiring same-day delivery. Euro Car Parts, a leading wholesale distributor, operates over 130 branches in the UK and Ireland alone, enabling 95% of orders to be fulfilled within 24 hours.

The Retailers segment is growing lucratively with an estimated CAGR of 7.5% from 2025 to 2033.

Automotive retailers are increasingly adopting hybrid physical-digital models that allow consumers to browse, order, and collect parts in-store or via mobile apps. As per Statista, online parts sales through OEM and independent retailer platforms grew by 19% in 2023, with click-and-collect options accounting for 44% of transactions. BMW’s Parts Online platform, available in 27 European markets, saw a 31% increase in retail part sales in 2023, driven by transparent pricing and compatibility assurance. Additionally, repair shops are transforming into retail hubs, selling maintenance kits, wiper blades, and cabin filters directly to customers during service visits.

By Certification Insights

The uncertified parts segment was the largest and held 47.6% of the Europe Automotive Aftermarket market share in 2024, with the economic considerations, particularly in insurance-led repairs. According to the European Insurance and Occupational Pensions Authority (EIOPA), over 62% of collision repairs in Germany, France, and Italy in 2023 were processed through insurance claims, with insurers actively promoting the use of uncertified parts to reduce claim payouts. A 2023 study by the German Insurance Association (GDV) found that using uncertified body parts could reduce repair costs by up to 38% compared to OEM equivalents. This financial incentive encourages body shops to source from non-certified suppliers, especially for low-risk components such as bumpers, mirrors, and trim.

The Certified Parts segment is expanding at a CAGR of 8.1% from 2025 to 2033. European regulators are intensifying scrutiny on part certification to ensure road safety and emissions integrity. The EU’s 2021 revision of the Roadworthiness Directive mandates that replacement parts affecting safety or emissions, such as ECUs, catalytic converters, and ADAS sensors, must meet ECE approval standards. As per the European Agency for Safety and Health at Work, vehicles fitted with non-compliant parts are 2.3 times more likely to fail technical inspections. In France, UTAC reported a 29% increase in part-related inspection failures linked to uncertified components between 2020 and 2023, which is prompting authorities to mandate certified replacements.

COUNTRY-LEVEL ANALYSIS

Germnay Automotive Aftermarket Market Analysis

Germany was the top performer in the Europe Automotive Aftermarket market with 21.3% of share in 2024, with its status as Europe’s largest automotive market, with over 48 million registered passenger vehicles—the highest in the EU. Germany’s dense network of independent workshops, numbering over 62,000, supports a highly fragmented yet efficient service ecosystem. According to the German Federal Ministry for Economic Affairs, the average vehicle age in Germany reached 10.8 years in 2023, with over 12 million vehicles exceeding 15 years, creating sustained demand for repairs. The presence of major OEMs like Volkswagen, BMW, and Mercedes-Benz further amplifies aftermarket activity, as their extended service networks and proprietary technologies generate high-value repair opportunities.

France Automotive Aftermarket Market Analysis

France was positioned second by accounting for 16.8% of the Europe Automotive Aftermarket market share in 2024, with a large vehicle parc of 40.2 million passenger cars and a growing preference for independent repairers. As per the French Ministry of Transport, over 70% of vehicles aged 7–12 years are serviced outside dealership networks, driven by cost efficiency and proximity. The UTAC technical inspection agency reported that 23% of vehicles failed their 2023 contrôle technique, with lighting and suspension defects being the most common, generating demand for replacement parts. Furthermore, France’s push toward green mobility has increased the complexity of servicing Euro 6-compliant diesel and hybrid vehicles, creating opportunities for specialized workshops. The Italian Automotive Aftermarket market is expected to grow with the highest CAGR from 2025 to 2033. The ACI (Italian Automobile Club) reported that 41% of vehicles in 2023 were over 15 years old, particularly in southern regions where new car ownership remains low. Italy’s decentralized repair market, comprising over 55,000 independent garages, thrives on cost-effective servicing, often using non-OEM parts. The mandatory “revisione” inspection, required every two years after the fourth year of ownership, drives recurring demand. ISTAT data shows that 21% of inspections in 2023 led to immediate repairs.

United Kingdom Automotive Aftermarket Market Analysis

United Kingdom Automotive Aftermarket market is also gaining huge traction due to the growth opportunities. As per the Driver and Vehicle Standards Agency (DVSA), over 24 million MOT tests were conducted in 2023, with 32% failing, the highest in Europe, due to worn tyres, faulty lights, and exhaust issues. This high failure rate ensures consistent demand for replacement parts and services. The UK’s mature e-commerce infrastructure has also accelerated online parts sales, with platforms like Euro Car Parts and Amazon Automotive capturing over 25% of retail transactions.

Spanish Automotive Aftermarket Market Analysis

The Spanish Automotive Aftermarket market has potentially a prominent growth opportunity with 31.8 million registered vehicles and an average age of 13.1 years in Western Europe. Economic constraints, particularly among younger demographics, have increased reliance on affordable servicing, with 68% of repairs conducted at independent workshops.

COMPETITIVE LANDSCAPE

KEY MARKET PARTICIPANTS

Companies playing a key role in the Europe automotive aftermarket market include

- Continental AG

- ZF Friedrichshafen AG

- HELLA KGaA Hueck & Co.

- ThyssenKrupp AG

- Mahle GmbH

- Delphi Tech

- Valeo Group

- Faurecia

- Gestamp

- Magna International Inc.

- Lear Corp.

- Bosch

The world's largest service provider employs 400,000 people and operates 440 companies in 60 countries, generating $91.8 billion in revenue.

The competitive landscape of the Europe Automotive Aftermarket is characterized by a dynamic interplay between global OEM-affiliated suppliers, independent distributors, and emerging digital disruptors. Incumbent manufacturers leverage their engineering heritage, brand trust, and technical expertise to maintain dominance in high-value component segments, particularly in powertrain and safety systems. At the same time, independent networks are gaining ground by offering cost-effective alternatives and localized service models that resonate with price-sensitive consumers and small repair businesses. The rise of digital platforms has intensified rivalry, enabling faster access to parts, real-time diagnostics, and transparent pricing, which erodes traditional margins and forces players to differentiate through value-added services. Brand credibility, technical support, and integration into workshop workflows have become differentiators, replacing mere product availability as competitive levers. Additionally, the increasing complexity of modern vehicles has created a knowledge gap that companies are striving to fill through training, certification, and digital tooling. As OEMs tighten control over software and diagnostics, independent players are forming alliances and cooperative networks to preserve market access and ensure fair competition.

Top Players In The Market

- Bosch Automotive Aftermarket operates as a pivotal force in the European aftermarket landscape, leveraging its legacy in engineering excellence and technological innovation. The division delivers a comprehensive portfolio of replacement parts, diagnostic equipment, and service solutions, catering to both independent workshops and retail networks. Bosch’s influence extends beyond product supply, as it actively shapes service standards through training initiatives, digital integration platforms, and technical support ecosystems. Its commitment to quality and compatibility has established deep trust among technicians and consumers, reinforcing its position as a preferred partner in vehicle maintenance.

- ZF Aftermarket, a division of ZF Friedrichshafen AG, plays an important role in advancing driveline, chassis, and safety system solutions within the European aftermarket. Known for its premium-tier brands such as Sachs, Boge, and LUK, the company delivers high-performance components that meet stringent technical and durability benchmarks. ZF distinguishes itself through integrated engineering expertise, offering not only replacement parts but also technical documentation, repair guidelines, and digital service tools that enhance workshop efficiency.

- ERA Motors, a pan-European independent aftermarket network, has emerged as a key facilitator of parts distribution and workshop collaboration. Built on a cooperative model, ERA Motors unites a vast network of regional distributors and service centers, enabling localized responsiveness with centralized procurement advantages. The company excels in delivering a broad range of components—from consumables to powertrain parts while emphasizing technical support and training for its partners. Its agility in adapting to regional regulatory and consumer demands allows it to compete effectively with larger OEM-aligned entities. ERA Motors places strong emphasis on digital transformation, integrating e-commerce platforms and inventory management systems to streamline operations.

Top Strategies Used By Key Market Participants

- One of the most prominent strategies employed by leading players is the integration of digital service ecosystems that connect workshops, parts suppliers, and end users through unified platforms. Companies are investing in cloud-based diagnostic tools, real-time inventory access, and AI-driven repair recommendations to enhance service accuracy and efficiency. These digital ecosystems not only improve customer retention but also position providers as indispensable partners in the repair workflow. By embedding their solutions into daily workshop operations, firms secure long-term engagement and reduce dependency on price-based competition.

- Another key approach is the expansion of technical training and certification programs for independent mechanics. As vehicle systems grow more complex, manufacturers and distributors are establishing academies and online learning modules to upskill technicians in areas such as ADAS calibration, hybrid system servicing, and software diagnostics. This strategy strengthens brand loyalty, ensures proper installation of proprietary components, and elevates service quality across the independent channel, thereby reinforcing trust in non-OEM networks.

- Another strategy involves the development of remanufactured and sustainable product lines to align with environmental regulations and circular economy principles. Companies are investing in reverse logistics, core return programs, and reconditioning facilities to offer high-quality alternatives to new parts. This not only reduces waste and resource consumption but also appeals to cost-conscious consumers and insurers seeking economical yet reliable solutions, thereby expanding market reach while supporting long-term sustainability goals.

RECENT MARKET NEWS

- In April 2024, Bosch Automotive Aftermarket launched a new digital service platform integrating real-time diagnostic support and parts compatibility verification for independent workshops across Europe by enhancing its technical engagement with repairers.

- In February 2024, ZF Aftermarket introduced an expanded remanufacturing program for transmission components in Germany, which is reinforcing its commitment to sustainability and circular economy principles in the powertrain segment.

- In January 2024, ERA Motors formed a strategic partnership with a Nordic automotive distributor to extend its network coverage into Sweden and Finland by strengthening its pan-European presence.

- In March 2024, Bosch Automotive Aftermarket initiated a technician certification initiative in Italy, which is offering advanced training on hybrid vehicle systems to support the growing service demand for electrified powertrains.

- In May 2024, ZF Aftermarket unveiled a new digital catalog system integrated with major European workshop management software by streamlining part selection and ordering for service providers.

MARKET SEGMENTATION

This research report on the Europe automotive aftermarket market has been segmented and sub-segmented based on the following categories.

By Replacement Part

- Battery

- Tyre

- Filters

- Brake Parts

- Turbochargers

- Body Parts

- Wheels

By Service Channel

- DIFM (Do it for Me)

- DIY (Do it Yourself)

- OE (Delegating to OEMs)

By Distribution Channel

- Wholesalers & Distributors

- Retailers (OEMs and Repair Shops)

By Certification

- Certified Parts

- Genuine Parts

- Uncertified Parts

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe automotive aftermarket market?

The Europe automotive aftermarket market includes parts, components, and services sold for vehicle maintenance, repair, performance upgrades, and accessories after initial sale by the OEM.

Why is the automotive aftermarket important?

The aftermarket supports vehicle longevity, safety, performance, and customization, offering cost-effective solutions for maintenance and repairs across passenger and commercial vehicles.

What drives growth in the Europe automotive aftermarket market?

Market growth is driven by increased vehicle parc age, higher miles driven, extended vehicle lifespans, rising demand for maintenance services, and growth in e-commerce parts sales.

What types of products are in the automotive aftermarket?

Key products include replacement parts (brakes, filters, belts), lubricants, tires, batteries, performance parts, body repair components, and accessories.

How do channels for aftermarket sales differ?

Aftermarket sales occur through independent repair shops, dealership service centers, auto parts retailers, online platforms, and DIY consumer purchases.

What role does vehicle age play in the market?

Older vehicles typically require more routine maintenance and part replacement, driving consistent aftermarket demand as new car sales fluctuate.

How is e-commerce shaping the automotive aftermarket?

E-commerce expands access to parts and accessories, direct-to-consumer pricing, fast delivery, product reviews, and comparison tools that improve purchasing convenience.

What trends are shaping the Europe automotive aftermarket?

Top trends include digital parts catalogs, online fitting bookings, telematics-based maintenance reminders, performance upgrades, and sustainability in parts recycling.

What challenges does the market face?

Challenges include complexity of modern vehicle systems, rising costs of genuine parts, aftermarket-OEM competition, and the shift toward electric vehicles with fewer moving parts.

How are regulations influencing the market?

EU rules on warranty rights, data access, emissions standards, and safety compliance impact aftermarket operations and parts sourcing.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com