Europe Biological Control Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Microbials, Entomopathogenic nematodes), And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Europe Biological Control Market Report Summary

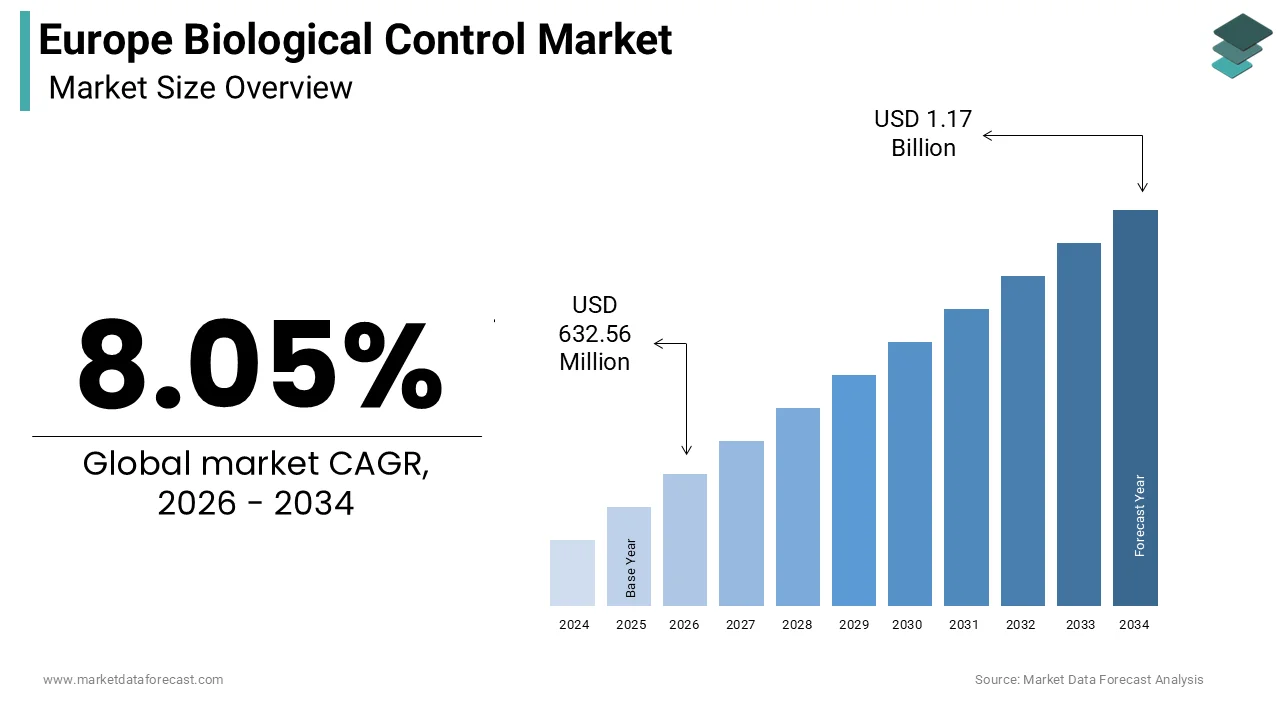

The Europe biological control market was valued at USD 585.43 million in 2025 and is projected to reach USD 1.17 billion by 2034, growing from USD 632.56 million in 2026 at a CAGR of 8.05% during the forecast period. Market growth is driven by increasing adoption of sustainable crop protection solutions, stringent regulations on chemical pesticide usage, expanding organic farming, and rising demand for environmentally friendly pest management practices. Advancements in microbial technologies, integrated pest management (IPM), and biological crop protection products are further supporting market expansion.

Key Market Trends

- Rising adoption of microbial biological control products across agriculture.

- Increasing demand for sustainable and residue-free crop protection solutions.

- Growing implementation of integrated pest management (IPM) practices.

- Expansion of organic farming and environmentally friendly agricultural practices.

- Rising investments in research and development of biological crop protection technologies.

Segmental Insights

- Based on Type, the microbials segment dominated the Europe biological control market in 2025 by accounting for the largest market share. The segment's growth is driven by its high efficacy against a broad spectrum of pests and diseases, ease of application, compatibility with sustainable farming practices, and increasing adoption in organic agriculture.

Regional Insights

- Germany dominated the Europe biological control market in 2025, supported by advanced agricultural practices, strong regulatory support for sustainable farming, and widespread adoption of integrated pest management solutions.

- France is expected to witness significant market growth during the forecast period as farmers increasingly adopt biological crop protection products to comply with sustainability regulations and reduce reliance on synthetic pesticides.

- Spain is projected to strengthen its position in the European biological control market due to extensive greenhouse cultivation, intensive horticultural production, and growing adoption of biological pest management solutions.

- Italy is anticipated to experience steady market growth, supported by the expansion of organic farming, increasing investment in sustainable agriculture, and rising demand for biological crop protection products.

- The United Kingdom is expected to witness increasing adoption of biological control products over the forecast period, driven by environmental land management initiatives, sustainable farming policies, and growing emphasis on reducing chemical pesticide use.

Competitive Landscape

The Europe biological control market is highly competitive, with companies focusing on microbial innovations, beneficial insects, integrated pest management solutions, and sustainable crop protection technologies. Market participants are investing in research and development, strategic partnerships, and product innovation to strengthen their competitive positions.

Key players operating in the Europe biological control market include BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, Koppert Biological Systems, Biobest Group, Andermatt Biocontrol, Certis Belchim, Bioline AgroSciences, FMC Corporation, Novonesis, Valent BioSciences, UPL Ltd., De Sangosse, and CBC (Europe) S.r.l

Europe Biological Control Market Size

The Europe biological control market size was calculated at USD 585.43 million in 2025 and is anticipated to reach USD 1.17 billion by 2034, from USD 632.56 million in 2026, growing at a CAGR of 8.05% during the forecast period.

Biological control is the strategic utilization of living organisms, including predators, parasitoids, pathogens, and competitors, to suppress pest populations in agricultural and horticultural systems. This approach represents a fundamental shift from chemical dependency toward ecological balance, leveraging natural mechanisms to manage crop threats. The European Union has positioned itself at the forefront of this transition through comprehensive legislative frameworks that prioritize environmental sustainability and human health. According to Eurostat, the sales volume of chemical pesticides in the EU decreased by 14% between 2011 and 2021, indicating a structural decline in synthetic reliance. The Farm to Fork Strategy explicitly targets a 50% reduction in the use and risk of chemical pesticides by 2030, creating an imperative for effective non-chemical alternatives. As per the Research Institute of Organic Agriculture FiBL, organic farmland in the European Union reached 10.9% of total agricultural area, with countries like Austria exceeding 25% coverage. This expansion necessitates robust biological solutions as synthetic inputs are prohibited in certified organic production. Furthermore, the European Food Safety Authority continues to withdraw approvals for numerous active substances due to safety concerns, leaving significant gaps in pest management portfolios. The market is characterized by high innovation rates in microbial fermentation and macrobial rearing technologies. With increasing consumer awareness regarding food safety and residue-free produce, biological control agents have evolved from niche products to essential components of integrated pest management strategies across the continent.

MARKET DRIVERS

Regulatory Withdrawal of Synthetic Active Substances

The systematic withdrawal of approvals for synthetic chemical active substances is mainly driving the growth of the European biological control market. Regulation EC No 1107/2009 mandates rigorous safety assessments for all plant protection products, which is leading to the non-renewal of many conventional chemicals that fail to meet current environmental and health standards. According to the European Commission, a significant number of previously approved pesticide active substances have been withdrawn from the market in the last decade due to failures in meeting safety criteria. Specific bans on neonicotinoids and other broad-spectrum insecticides have created significant voids in pest management strategies, particularly for crops like sugar beets, oilseed rape, and maize. Farmers are compelled to seek compliant alternatives to avoid legal penalties and maintain production levels. The Sustainable Use of Pesticides Directive further reinforces this trend by requiring member states to prioritize non-chemical methods in their National Action Plans. As per data from the European Environment Agency, agricultural runoff containing pesticide residues remains a critical water quality issue, prompting stricter local regulations in vulnerable zones. This regulatory pressure ensures that biological control agents are not merely optional but increasingly mandatory components of modern crop protection programs, which is driving consistent demand growth among both organic and conventional growers seeking to remain compliant with evolving legislative frameworks.

Consumer Demand for Residue-Free and Organic Produce

Escalating consumer preference for food products free from synthetic pesticide residues and certified organic goods is further contributing to the European biological control market expansion. Health-conscious consumers are increasingly scrutinizing food labels and sourcing practices, willing to pay premium prices for produce grown using sustainable and natural methods. According to the European Commission, the retail market for organic food in the EU reached 56.5 billion euros in 2023, demonstrating robust growth and consumer commitment to organic principles. Organic farming standards strictly prohibit the use of synthetic chemical pesticides, making biological control agents indispensable for managing pest and disease pressures in these systems. Major retail chains and supermarkets across Europe have established strict private standards for maximum residue levels, often lower than legal limits, pushing suppliers to adopt biological crop protection strategies. As per a study by the European Consumer Organisation, over 70% of Europeans consider environmental impact and health safety when purchasing food products. This market pull encourages conventional farmers to adopt reduced-risk inputs like biological controls to access premium market segments and maintain buyer relationships. The visibility of biological controls as safe and natural solutions enhances brand value for food producers, creating a strong economic incentive for their adoption. This consumer-driven transformation of the food supply chain ensures sustained growth for biological control manufacturers catering to high-value crop sectors.

MARKET RESTRAINTS

Higher Cost Structure Compared to Synthetic Alternatives

The elevated cost of biological control agents relative to conventional synthetic pesticides is hampering the expansion of the European biological control market. Biological products often require more complex manufacturing processes involving live organism cultivation, stringent quality control, and specialized storage conditions, which drive up production expenses. According to industry cost analyses, biological control treatments can be 20% to 30% more expensive per hectare than standard chemical applications, depending on the crop and pest pressure. For large-scale conventional farmers operating on thin margins, this price differential presents a substantial financial barrier, especially when synthetic options remain available and affordable. The need for repeated applications to maintain efficacy further increases labor and material costs, exacerbating the total expense. As per agricultural economic studies, small and medium-sized farms lack the financial buffer to absorb these higher input costs without guaranteed yield improvements or premium market access. Government subsidies for synthetic fertilizers and pesticides in certain member states distort the pricing landscape, making it difficult for biological alternatives to compete on a level playing field. Although long-term benefits, such as improved soil health and resistance management, exist, the immediate cash flow impact discourages many growers from switching. This economic constraint slows the transition rate among conventional growers who recognize the environmental benefits but cannot justify the short-term financial outlay required for integrating biological controls into their regular pest management programs.

Limited Shelf Life and Complex Storage Requirements

The inherent biological nature of biological control agents imposes strict limitations on shelf life and storage conditions, which complicates logistics and distribution across Europe and impedes the regional market growth. Unlike stable chemical formulations, live microorganisms require specific temperature, humidity, and light conditions to maintain viability and efficacy during transport and warehousing. Most predatory insects and mites have a shelf life of only a few days to weeks, requiring rapid delivery from manufacturer to field, which challenges existing supply chain infrastructure. According to supply chain assessments, inconsistent cold chain facilities in rural areas lead to significant product mortality and reduced field performance, undermining farmer confidence. Fungal and bacterial agents are also sensitive to extreme temperatures and UV exposure, requiring specialized packaging and handling protocols that increase operational costs. As per distributor reports, product wastage due to improper storage or delayed delivery remains a persistent issue affecting profitability and reliability. Farmers often hesitate to invest in biological inputs when faced with uncertainty regarding organism viability at the time of application, preferring the predictable potency of chemical pesticides. The lack of standardized preservation technologies across different formulation types creates variability in product quality, further complicating inventory management for retailers. These logistical hurdles restrict the geographic reach of manufacturers and limit the availability of biological control agents in remote agricultural regions, thereby restraining overall market penetration and growth potential.

MARKET OPPORTUNITIES

Integration with Precision Agriculture and Digital Monitoring

The convergence of biological control agents with precision agriculture technologies offers a substantial opportunity for the European biological control market. Advanced sensors, drones, and digital monitoring platforms enable growers to track pest populations and environmental conditions in real time, allowing for targeted and timely deployment of biological agents. According to the European Commission, the adoption of digital tools in farming is accelerating, with over 30% of farms in the European Union utilizing some form of precision agriculture technique. Integrating biological control release schedules with predictive pest models helps farmers apply agents when pest thresholds are reached and environmental conditions favor organism survival, maximizing efficacy and minimizing waste. Drone-based dispersal systems offer novel delivery methods for releasing predatory mites or applying microbial sprays over large areas, reducing labor costs and improving coverage uniformity. As per industry trends, the synergy between biological inputs and digital data enhances the credibility of biological controls among tech-savvy younger farmers who prioritize measurable outcomes. This technological integration also facilitates traceability and documentation required for organic certification and sustainability reporting, adding value to the overall farming operation. By leveraging precision technology, manufacturers and service providers can offer comprehensive pest management solutions that address traditional limitations of consistency and timing, driving broader adoption of biological controls in modern intensive agriculture.

Expansion into Protected Cultivation and Greenhouse Systems

The extensive protected cultivation sector in Europe, particularly in countries like Spain, the Netherlands, and Italy, is expected to continue expanding its adoption of biological solutions over the next few years. Greenhouses and tunnel farming create controlled environments where temperature, humidity, and light can be optimized for the survival and activity of beneficial organisms, making them ideal settings for biological pest management. According to industry reports, over 60% of greenhouse tomato and pepper production in Europe uses integrated pest management strategies dominated by biological controls. The closed nature of these systems prevents the escape of released agents and minimizes interference from weather conditions, ensuring higher efficacy compared to open field applications. High-value crops grown in protected environments are highly susceptible to pests such as whiteflies, thrips, and spider mites, which can cause rapid crop loss if not managed effectively. Biological control agents offer a safe and efficient solution that avoids chemical residues on premium produce destined for export markets with strict maximum residue limits. As per market analysis, the density of greenhouse production allows for economies of scale in biological control application, making it cost-competitive with chemical alternatives. The growing investment in vertical farming and urban agriculture further expands the addressable market for biological control solutions. This alignment with high-tech sustainable farming practices positions biological control agents as essential tools for the future of European protected horticulture, which is also driving sustained market growth.

MARKET CHALLENGES

Variable Efficacy Due to Environmental Sensitivity

The susceptibility of biological control agents to fluctuating environmental conditions poses a significant challenge to their consistent performance and reliability in European agricultural settings. Unlike synthetic chemicals, which provide predictable knockdown effects regardless of weather, biological agents require specific temperature, humidity, and light levels to thrive and exert control. For instance, predatory mites may become inactive below certain temperatures, while fungal pathogens require high humidity to infect pest populations. According to agronomic studies, efficacy rates of biological control agents can vary significantly between seasons and regions, leading to unpredictable results that frustrate farmers accustomed to chemical certainty. Climate change exacerbates this issue by introducing more extreme weather events, such as heatwaves or heavy rains, that can wash away or kill beneficial organisms. As per field trial data, inconsistent performance during critical pest outbreaks can lead to crop damage and economic losses, discouraging growers from relying solely on biological methods. The complexity of matching specific agent strains to local microclimates requires advanced technical knowledge that many farmers lack. Extension services often struggle to provide site-specific recommendations due to limited localized data, leaving growers to experiment at their own risk. This variability creates a perception of unreliability that hinders widespread adoption among risk-averse conventional farmers who prioritize immediate and guaranteed pest suppression over long-term ecological benefits.

Complex Regulatory Approval Processes for Novel Strains

Navigating the complex and lengthy regulatory approval process for new biological control agents remains a major challenge for manufacturers seeking to introduce innovative strains to the European market. While the EU supports low-risk products, the authorization procedure under Regulation EC No 1107/2009 requires extensive data on efficacy, safety, and environmental impact, which can be costly and time-consuming to generate. According to the European Crop Protection Association, the average time to register a new biologically active substance can exceed 3 to 5 years, with costs ranging from 5 to 10 million euros. This lengthy timeline delays product commercialization and reduces the window for patent protection, discouraging investment in research and development, particularly for small and medium-sized enterprises. The lack of harmonization in data interpretation across member states further complicates the process, creating market fragmentation and additional administrative burdens. As per industry feedback, the uncertainty surrounding regulatory outcomes and potential changes in data requirements creates financial risks for developers. Additionally, the periodic re-evaluation of approved substances adds ongoing compliance costs for manufacturers. Until the regulatory framework becomes more streamlined and predictable for biologicals, the pace of innovation and market entry will remain constrained, limiting the diversity of products available to farmers and slowing the replacement of less sustainable chemical alternatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.05% |

| Segments Covered | By Type, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, Koppert Biological Systems, Biobest Group, Andermatt Biocontrol, Certis Belchim, Bioline AgroSciences, FMC Corporation, Novonesis, Valent BioSciences, UPL Ltd., De Sangosse, CBC (Europe) S.r.l. |

SEGMENTAL ANALYSIS

By Type Insights

The microbials segment accounted for the dominant share of the European market in 2025 due to its exceptional versatility and applicability across a wide range of agricultural systems, including open field crops, horticulture, and protected cultivation. This category encompasses bacteria, fungi, and viruses that target specific pests and diseases, offering solutions for both insect control and pathogen suppression. According to industry data, microbials account for over 60% of the total biological control market value in Europe, reflecting their widespread adoption. The ability of microbial agents such as Bacillus thuringiensis and Trichoderma species to be applied using standard spraying equipment makes them highly compatible with existing farming practices, reducing the barrier to entry for conventional growers. As per agronomic studies, microbial formulations can be integrated into tank mixes with certain fertilizers and other compatible inputs, allowing for efficient application schedules. This operational ease is particularly valued in large-scale arable farming where labor efficiency is critical. Furthermore, microbials offer broad-spectrum activity against multiple pest species, providing comprehensive protection in complex cropping environments. The extensive research backing the efficacy of established microbial strains builds trust among farmers and agronomists, ensuring consistent demand. The scalability of microbial production also allows manufacturers to meet the high volume requirements of major European crops such as wheat, maize, and potatoes, solidifying their dominant position in the market.

However, the entomopathogenic nematodes segment is estimated to register the fastest CAGR of 14.4% over the forecast period in the European market, owing to their superior efficacy against difficult-to-control soil-borne pests. These microscopic worms specifically target larvae of insects such as weevils, grubs, and root maggots, which are often inaccessible to foliar sprays and resistant to many chemical treatments. According to research from leading agricultural universities, entomopathogenic nematodes can achieve mortality rates exceeding 80% in targeted pest populations when applied correctly. The increasing prevalence of soil-borne pests due to monoculture practices and climate change creates an urgent demand for effective biological solutions. As per field trials in major vegetable-producing regions, nematode applications have shown significant reductions in crop damage and yield losses compared to untreated controls. The ability of nematodes to seek out and infect hosts within the soil profile offers a unique advantage over other biological agents that rely on contact or ingestion. This targeted action minimizes impact on non-target organisms and preserves beneficial soil biodiversity. The growing awareness of soil health and the negative impacts of chemical nematicides further accelerates adoption. Farmers are increasingly recognizing nematodes as a reliable tool for integrated pest management in high-value crops such as strawberries, carrots, and ornamental plants, fueling rapid market expansion.

REGIONAL ANALYSIS

Germany Biological Control Market Analysis

Germany led the market in Europe in 2025 and is set to maintain its leadership position in the regional market through the steady integration of advanced digital tools and biological inputs over the coming years. The country holds a prominent position in the Europe biological control market, driven by its advanced agricultural technology sector and strong commitment to environmental sustainability. The country is a leader in organic farming adoption, with over 10% of its agricultural land under organic management, creating substantial demand for biological inputs. German farmers are increasingly integrating precision agriculture tools with biological control applications to optimize efficacy and comply with strict environmental regulations. The Federal Ministry of Food and Agriculture provides significant financial support for sustainable farming practices, including the adoption of biocontrol agents. The presence of major agrochemical companies and research institutions in Germany fosters innovation in microbial formulation technologies, enhancing product efficacy and market acceptance. The country's robust distribution network ensures the wide availability of biological control products across diverse farming regions. Consumer demand for organic and sustainably produced food in Germany is among the highest in Europe, driving retailers to source from farms using biological inputs. This market pull, combined with a regulatory push, establishes Germany as a key growth engine for the biological control market in the region.

France Biological Control Market Analysis

France is expected to witness significant growth in its biological control adoption as farmers transition toward sustainable practices over the next few years. France stands as a major contributor to the Europe biological control market, characterized by its extensive agricultural land and strong policy support for agroecological transitions. The country is one of the largest agricultural producers in the European Union, with significant areas dedicated to cereals, wine grapes, and vegetables, all of which are potential users of biological controls. The French Ecophyto Plan aims to reduce pesticide use by 50%, indirectly promoting the adoption of biological inputs that enhance plant health and reduce dependency on chemical protections. According to the French Ministry of Agriculture, the area under organic farming has reached over 2.9 million hectares, which drives demand for compliant pest management solutions. French farmers are increasingly aware of the benefits of soil health management, leading to greater interest in microbial inoculants and predatory insects. The country hosts several leading biological control manufacturers and research centers that develop strains suited to local soil conditions. Government subsidies for organic conversion and sustainable practices provide financial incentives for farmers to adopt biocontrols. The strong cooperative structure in French agriculture facilitates knowledge sharing and bulk purchasing of bio inputs, accelerating market penetration.

Spain Biological Control Market Analysis

Spain is poised to strengthen its role as a hub for biological pest management in intensive cultivation systems during the next few years. Spain is a key player in the Europe biological control market, particularly known for its intensive horticulture and protected agriculture sectors. The country is a major exporter of fresh fruits and vegetables to the rest of Europe, requiring high standards of produce quality and safety that drive the adoption of residue-free production methods. Biological control agents are widely used in Spanish greenhouses and open field vegetable production to control pests such as whiteflies and thrips without chemical residues. According to the Ministry of Agriculture, Fisheries and Food, Spain has seen significant growth in organic farming areas, particularly in regions like Andalusia and Catalonia. The arid and semi-arid conditions in many parts of Spain make efficient pest management critical, as biological controls offer targeted control with minimal water usage. The intensive nature of Spanish horticulture allows for frequent monitoring and adjustment of pest control inputs, facilitating the integration of biocontrols into precision farming systems. Export markets impose strict maximum residue limits, compelling Spanish growers to minimize chemical input use. Government initiatives promoting sustainable water and nutrient management support the adoption of biological alternatives.

Italy Biological Control Market Analysis

Italy is anticipated to see rising demand for biological agents as its organic sector continues to expand over the next few years. Italy occupies a significant share of the Europe biological control market, driven by its diverse agricultural landscape and high-value specialty crop production. The country is a leading producer of fruits, vegetables, and wine, sectors that are increasingly adopting organic and sustainable practices to meet premium market demands. Italian farmers face challenges related to climate change-induced disease pressure, making effective biological control agents highly relevant. According to ISMEA data, Italy has one of the largest organic farming areas in the European Union, with over 2 million hectares under organic management. This extensive organic sector creates a ready market for biological pest control agents that are permitted under organic certification standards. The Mediterranean climate in many parts of Italy supports year-round cultivation, allowing for multiple applications of biocontrols and sustained demand. Italian consumers are highly conscious of food quality and origin, driving retailers to prefer suppliers using sustainable production methods. The government supports agroecological initiatives through national rural development programs, providing funding for the adoption of innovative biological inputs. The presence of numerous small and medium-sized farms in Italy favors the use of cost-effective and easy-to-apply biocontrols.

United Kingdom Biological Control Market Analysis

The United Kingdom is likely to experience increased uptake of biological solutions as new environmental land management incentives take full effect in the coming years. The United Kingdom maintains a steady presence in the Europe biological control market, influenced by its post Brexit agricultural policies and strong organic sector. The UK government has introduced the Environmental Land Management scheme, which rewards farmers for adopting sustainable practices, including the use of biological inputs that improve soil health and reduce chemical reliance. According to the Department for Environment, Food and Rural Affairs, the UK has a well-established organic farming community, with consumer demand for organic products remaining robust despite economic fluctuations. British farmers are increasingly focused on regenerative agriculture principles, which emphasize soil biology and minimal chemical intervention, creating favorable conditions for biocontrol adoption. The country's temperate climate supports a wide range of crops, including cereals, oilseeds, and vegetables, all of which can benefit from biological pest control. Research institutions in the UK are actively studying the efficacy of microbial inoculants in local soil conditions, providing evidence-based recommendations to farmers. The retail sector in the UK is highly competitive, with major supermarkets committing to sustainable sourcing standards that encourage the use of biocontrols. Although the market size is smaller compared to continental giants, the UK offers high-value opportunities due to its advanced agricultural knowledge base.

COMPETITION OVERVIEW

The competition in the Europe biological control market is characterized by intense rivalry between specialized biological firms and diversified agrochemical giants. Specialized companies differentiate themselves through deep technical expertise, superior strain selection, and dedicated customer support tailored to specific regional needs. Multinational corporations compete by leveraging established distribution networks, financial resources, and integrated product portfolios that combine biological and conventional solutions. Innovation serves as the primary battleground with participants racing to develop more stable formulations, broader spectrum agents, and compatible application technologies. Regulatory compliance creates significant entry barriers favoring established players with resources to navigate complex authorization processes. Price competition remains moderate as buyers prioritize efficacy and reliability over cost alone due to the living nature of these products. Strategic alliances and mergers frequently reshape the competitive landscape as companies seek complementary technologies and market access. Regional variations in pest pressures and cropping systems allow niche players to maintain strong local positions despite global consolidation. Ultimately, success depends on demonstrating consistent field performance, providing robust technical guidance, and maintaining reliable supply chains for perishable biological agents across diverse European agricultural environments.

KEY MARKET PLAYERS

A few major players of the Europe biological control market include

- BASF SE

- Bayer AG

- Syngenta Group

- Corteva Agriscience

- Koppert Biological Systems

- Biobest Group

- Andermatt Biocontrol

- Certis Belchim

- Bioline AgroSciences

- FMC Corporation

- Novonesis

- Valent BioSciences

- UPL Ltd

- De Sangosse

- CBC (Europe) S.r.l

Top Strategies Used by Key Market Participants

Key players in the Europe biological control market primarily employ strategic acquisitions and partnerships to rapidly expand their product portfolios and geographic reach. Companies invest heavily in research and development to improve formulation stability and extend shelf life, addressing critical logistical barriers. Manufacturers increasingly integrate digital monitoring tools with biological products to enable precision application and demonstrate measurable efficacy to skeptical growers. Strategic collaborations with seed companies allow for the incorporation of microbial treatments directly into planting materials, simplifying adoption for farmers. Regulatory navigation remains a core strategy with firms dedicating resources to secure approvals under evolving EU frameworks. Educational initiatives and technical support services are prioritized to bridge knowledge gaps and build trust among conventional growers transitioning from chemical inputs. Production capacity expansion through facility upgrades ensures reliable supply chains for perishable biological agents. These multifaceted strategies collectively strengthen market positions and drive the widespread integration of biological control solutions across European agriculture.

Leading Players in the Europe Biological Control Market

- Koppert Biological Systems is a foundational leader in the European biological control sector, specializing in natural pest management and pollination solutions. The company maintains extensive production facilities across the continent to supply predatory mites and beneficial insects for protected cultivation. Koppert recently expanded its research capabilities to develop climate-resilient strains adapted to changing European weather patterns. They actively collaborate with universities to validate product efficacy under local conditions, ensuring reliability for growers. Their comprehensive technical support network educates farmers on integrated pest management protocols, bridging the knowledge gap between chemical and biological methods. This commitment to science-based solutions strengthens their reputation as a trusted partner for sustainable agriculture throughout Europe.

- Biobest Group NV plays a pivotal role in the European market by offering a diverse portfolio of biological control agents and bumblebee pollination services. The company focuses on delivering high-quality macrobials and microbials tailored for horticultural applications across Southern and Northern Europe. Biobest recently invested in automated rearing technologies to enhance production consistency and meet rising demand for biological alternatives. They launched new digital monitoring tools that integrate with farm management systems, allowing precise application timing. By strengthening distribution partnerships in key agricultural regions, Biobest ensures timely product availability, which is critical for live organisms. Their continuous innovation in formulation stability addresses logistical challenges, reinforcing their competitive position in the dynamic European landscape.

- Syngenta Crop Protection AG leverages its global agricultural expertise to advance biological control solutions within the European market through strategic integration and acquisition. The company combines conventional and biological offerings to provide holistic crop protection strategies for both organic and conventional farmers. Syngenta recently acquired specialized biocontrol firms to expand its microbial pipeline and accelerate product development cycles. They utilize their vast agronomic advisory network to promote biological inputs alongside precision farming technologies, enhancing adoption rates. By investing in local manufacturing and regulatory compliance, Syngenta navigates complex European approval processes efficiently. Their ability to scale production and offer bundled solutions positions them as a major driver of mainstream biological control adoption across diverse cropping systems in the region.

MARKET SEGMENTATION

This research report on the Europe biological control market has been segmented and sub-segmented based on type and region.

By Type

- Microbials

- Entomopathogenic nematodes

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe biological control market?

The market is driven by increasing demand for sustainable agriculture, strict regulations on chemical pesticides, growth in organic farming, and rising adoption of integrated pest management (IPM) practices.

2. Which type of biological control product holds the largest market share?

Microbial biological control products, including bacteria, fungi, and viruses, account for a significant share due to their effectiveness against a wide range of crop pests and diseases.

3. Which crop type generates the highest demand for biological control products?

Fruits and vegetables account for the greatest demand because these high-value crops require effective pest management while meeting stringent food safety standards.

4. What are the major applications of biological control products?

Biological control products are widely used for pest control, disease management, greenhouse cultivation, field crops, horticulture, and organic farming.

5. What role does integrated pest management (IPM) play in the market?

IPM combines biological, cultural, mechanical, and chemical methods to achieve sustainable pest control, making biological control products an essential component of modern crop protection strategies.

6. Which distribution channels dominate the Europe biological control market?

Agricultural distributors, cooperatives, direct sales to commercial farms, and online agricultural supply platforms are the primary distribution channels.

7. What challenges does the Europe biological control market face?

Challenges include higher product costs, shorter shelf life, varying field performance under different climatic conditions, and limited farmer awareness in some regions.

8. What technological advancements are shaping the Europe biological control market?

Advances in microbial formulations, precision agriculture, biotechnology, drone-based application systems, and digital crop monitoring are improving the effectiveness of biological control solutions.

9. What opportunities exist in the Europe biological control market?

Growing demand for residue-free food, increasing investment in sustainable agriculture, expanding greenhouse cultivation, and continuous innovation in biopesticides create significant growth opportunities.

10. What is the future outlook for the Europe biological control market?

The market is expected to experience strong growth over the coming years, supported by stricter environmental regulations, increasing adoption of sustainable farming practices, ongoing product innovation, and rising demand for eco-friendly crop protection solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com