Europe Cloud Gaming Market Size, Share, Trends & Growth Forecast Report – Segmented By Platform (PC, Mobile, Console, Smart TV), Game Type, Service Model, User Type, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Cloud Gaming Market Report Summary

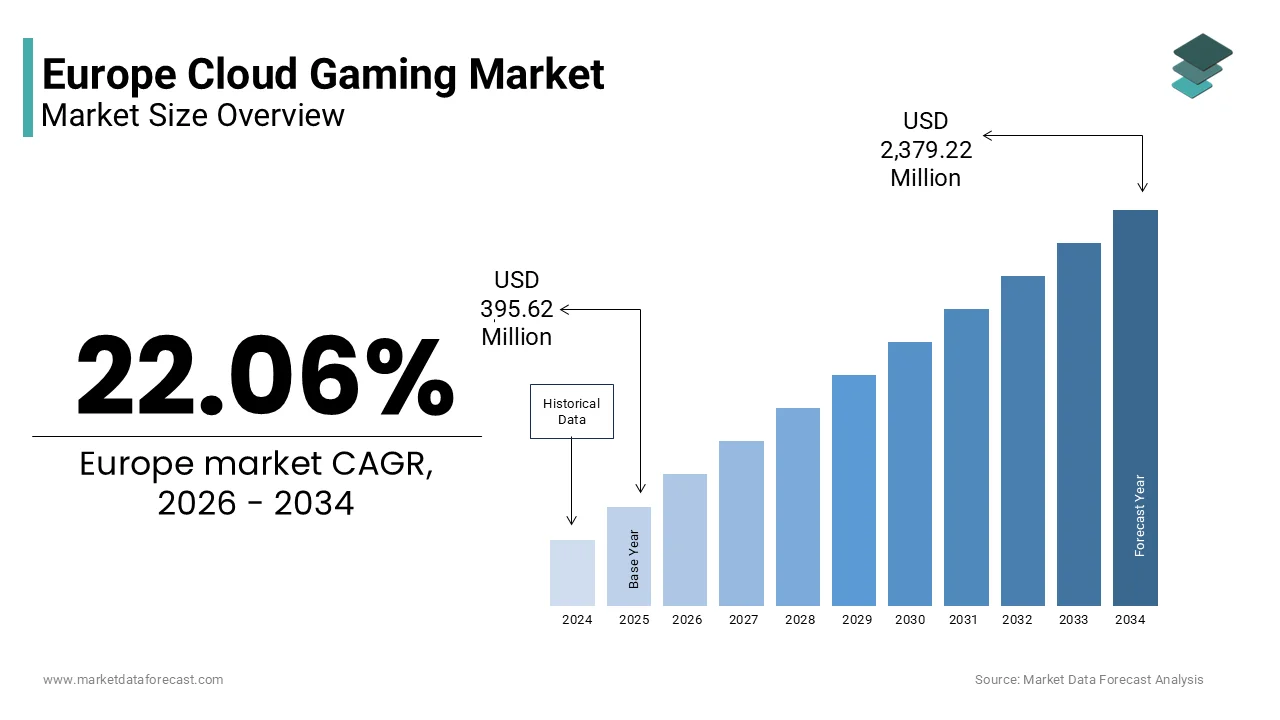

The Europe cloud gaming market was valued at USD 395.62 million in 2025 and is estimated to reach USD 482.89 million in 2026, with projections indicating growth to USD 2,379.22 million by 2034, expanding at a CAGR of 22.06% during the forecast period. Market growth is primarily driven by increasing broadband penetration, widespread adoption of 5G networks, and rising demand for device-agnostic gaming experiences. The growing popularity of subscription-based gaming services, advancements in cloud infrastructure, and increasing acceptance of mobile and casual gaming are further accelerating market expansion across Europe.

Key Market Trends

-

Rapid adoption of cloud gaming platforms fueled by 5G rollout and improved low-latency streaming technologies.

-

Rising popularity of mobile cloud gaming as smartphones become a primary gaming device for European users.

-

Strong shift toward subscription-based cloud gaming services offering cost-effective access to large game libraries.

-

Growing engagement from casual gamers seeking instant, hardware-free gaming experiences.

-

Increasing investments by major technology and gaming companies to enhance cloud infrastructure and content delivery.

Segmental Insights

- Based on platform, the mobile segment dominated the Europe cloud gaming market by accounting for 42.4% of the regional market share in 2025. This dominance is attributed to high smartphone penetration, ease of access, and the convenience of playing high-quality games without dedicated gaming hardware.

- Based on game type, the action games segment is expected to witness a robust CAGR of 19.04% over the forecast period, driven by strong user demand for immersive, multiplayer, and fast-paced gaming experiences supported by cloud technology.

- Based on service model, the subscription-based segment held the largest share of 65.5% of the Europe cloud gaming market in 2025. The segment’s leadership is supported by affordable monthly pricing, access to extensive game libraries, and increasing consumer preference for on-demand entertainment services.

- Based on user type, the casual gamers segment led the market by capturing 51.5% of the regional market share in 2025, reflecting the growing appeal of cloud gaming among non-hardcore players seeking flexible and low-commitment gaming options.

Regional Insights

- The Europe cloud gaming market is experiencing strong growth across major countries, supported by advanced digital infrastructure, high internet speeds, and growing gaming communities.

- The United Kingdom dominated the European cloud gaming market in 2025, accounting for 20.6% of the regional market share. This leadership is driven by high consumer spending on digital entertainment, early adoption of cloud technologies, and the strong presence of global gaming and technology providers.

Competitive Landscape

The Europe cloud gaming market is moderately competitive, with the presence of global technology giants and specialized cloud gaming providers focusing on platform innovation, content partnerships, and service expansion. Key players are investing heavily in improving streaming quality, reducing latency, and expanding game libraries to strengthen user engagement. Strategic collaborations with telecom operators and game developers are also shaping market competition. Prominent companies operating in the Europe cloud gaming market include Google Stadia, Microsoft xCloud, NVIDIA GeForce Now, Sony PlayStation Now, Amazon Luna, Shadow, Vortex Cloud Gaming, LiquidSky, GameFly, Parsec, Boosteroid, Playkey, Blacknut, Ubitus, and Blade SAS.

Europe Cloud Gaming Market Size

The Europe cloud gaming market size was valued at USD 395.62 million in 2025 and is projected to reach USD 2,379.22 million by 2034 from USD 482.89 million in 2026, growing at a CAGR of 22.06%.

Cloud gaming represents a paradigm shift in digital entertainment and is enabling users to stream high-fidelity video games directly from remote data centres without relying on local hardware. This model leverages high-speed broadband infrastructure and edge computing to deliver console-quality experiences on smartphones, tablets and low-end PCs. As of 2025, high-speed broadband coverage in Europe continues to expand, with fixed networks capable of delivering download speeds of at least 100 megabits per second reaching most households, according to the European Commission’s 2025 broadband progress report. The European Union’s Digital Decade initiative aims to ensure that all urban and major rural areas benefit from gigabit connectivity by 2030, which will further expand the addressable user base. Concurrently, European consumers are increasingly shifting toward subscription-based digital content consumption, with more than one-third of gamers in Western Europe subscribing to at least one gaming service in 2025, according to Ampere Analysis. Regulatory developments also play a role, as the EU’s Data Act establishes clear frameworks for data portability and interoperability, potentially reducing vendor lock-in and encouraging multi-platform game libraries. These converging infrastructural, behavioural, and policy dynamics position cloud gaming not merely as a niche service, but as a structural evolution in Europe’s digital leisure economy.

MARKET DRIVERS

Proliferation of 5G Mobile Networks Enabling On the Go High Fidelity Gaming

The rapid rollout of 5G networks across Europe is a critical catalyst for cloud gaming adoption, drastically reducing latency and increasing bandwidth for mobile devices. Unlike 4G, which typically delivers 30 to 50 milliseconds round-trip latency, 5G networks in urban centres now achieve significantly lower response times, according to the European Telecommunications Standards Institute. This threshold is essential for real-time gameplay, where inputs must register instantly to maintain immersion and competitive fairness. As per the European Commission, more than three-quarters of the EU population had access to 5G coverage by the end of 2025, with countries like Finland, Sweden, and the Netherlands having exceedingly high urban penetration. This infrastructure supports cloud gaming on smartphones and tablets without the need for Wi-Fi tethering, unlocking new usage scenarios during commuting or travel. Furthermore, 5G’s network slicing capability allows telecom operators to allocate dedicated virtual channels with guaranteed quality of service for gaming traffic, a feature already deployed by Orange in France and Deutsche Telekom in Germany. According to the International Data Corporation, hundreds of millions of 5 G-enabled smartphones are in active use across Europe, priming the installed base for frictionless cloud gaming on the move and transforming mobile devices into portable high-end consoles.

Rising Popularity oCross-Platformrm Play and Game Continuity

European gamers increasingly demand seamless continuity across devices, which is allowing them to start a session on a console, continue on a laptop during lunch, and finish on a smartphone while commuting. This factor is also contributing to the expansion of the European cloud gaming market. Cloud gaming uniquely fulfils this expectation by centralising game state and rendering in the cloud, eliminating hardware dependency. According to the Entertainment Software Association of Europe, a majority of regular gamers aged 18 to 34 consider cross-platform progression a deciding factor when choosing a game or service, which reflects a behavioural shift toward fluid digital lifestyles. Major publishers such as Ubisoft and CD Projekt Red have responded by designing titles with cloud native architectures that sync player progress in real time. As per Microsoft’s European operations briefing, Xbox Cloud Gaming integrated with Windows 11 ensures that saved states update quickly across devices, a feature used by millions of European Xbox Game Pass subscribers. This convergence of consumer expectations, publisher support, and platform interoperability creates a self-reinforcing cycle where cloud gaming becomes the default delivery mechanism fonext-generationon interactive entertainment in Europe.

MARKET RESTRAINTS

Persistent Latency and Network Stability Issues in Rural and Suburban Areas

Despite advances in urban broadband, cloud gaming faces significant headwinds in non-metropolitan Europe due to inconsistent network performance and elevated latency, which is significantly hampering the European cloud gaming market expansion. According to the European Environment Agency’s 2025 connectivity assessment, many rural households still rely on fixed wireless or legacy DSL connections with average round-trip latencies exceeding acceptable thresholds for cloud gaming. Even in suburban zones, network congestion during peak evening hours can cause jitter spikes that disrupt frame pacing, leading to input lag and visual stuttering. As per the Body of European Regulators for Electronic Communications, millions of European households experience broadband speeds that fluctuate widely between daytime and nighttime, which is undermining consistent gaming experiences. While fibre deployment is accelerating, the European Court of Auditors noted in 2024 that just over half of the EU’s rural population is covered by full fibre infrastructure, with Eastern member states lagging significantly. These disparities create a digital leisure divide where cloud gaming remains a premium urban privilege, limiting mass market scalability and forcing providers to implement regional content throttling or session queuing, which degrades user satisfaction and retention.

Stringent Data Privacy Regulations Increasing Operational Complexity

The European cloud gaming market operates under one of the world’s most rigorous data governance regimes, with the General Data Protection Regulation imposing strict constraints on player data collection, storage, and cross-border transfer. Every gameplay session generates large volumes of behavioural telemetry, including biometric inputs from adaptive triggers, eye tracking, and voice commands, all classified as personal data under EU jurisprudence. According to the European Data Protection Board, cloud gaming providers must obtain explicit consent for each data processing purpose and ensure that biometric datasets are stored within EU jurisdiction, necessitating costly local data centre investments. Microsoft, for instance, operates dedicated Azure cloud gaming regions in Ireland and Germany to comply, while smaller entrants such as GeForce NOW rely on third-party EU-based infrastructure partners, which can increase latency as measured by the Fraunhofer Institute for Secure Information Technology. Moreover, as per the Digital Services Act, gaming platforms must provide real-time transparency on algorithmic content recommendations, disclosing how match-making or game suggestions are generated. These compliance burdens elevate operational costs and delay feature rollouts, particularly for global players adapting standardised architectures to Europe’s fragmented regulatory landscape.

MARKET OPPORTUNITIES

Integration with Public Cloud Infrastructure for Scalable Game Hosting

European cloud gaming is unlocking new scalability through deeper integration with hyperscaler public cloud platforms such as Amazon Web Services, Microsoft Azure, and Google Cloud, which is a promising opportunity in the European cloud gaming market. These infrastructures offer elastic compute resources that can dynamically scale during game launches or esports events, which is eliminating the need for fixed capacity investments. As per the European Cloud Partnership, most new cloud gaming startups in Europe now deploy entirely on public cloud stacks, leveraging pre-certified compliance modules for GDPR and the EU Cybersecurity Act. Microsoft’s Azure PlayFab service, for instance, provides turnkey multiplayer backend solutions used by hundreds of European game studios, including UK-based Hello Games and Sweden’s Hazelight Studios. The hyperscalers are also investing in edge locations, and AWS opened its sixth European edge facility in Warsaw in 2024 to support low-latency game streaming for Central and Eastern Europe. This ecosystem enables developers to focus on content creation rather than infrastructure, accelerating time to market and fostering innovation in genres such as cloud native multiplayer and persistent world simulations that were previously cost-prohibitive.

Expansion of Cloud Gaming into Education and Professional Training Simulations

Beyond entertainment, cloud gaming technology is gaining strategic traction in European education and professional upskilling through immersive simulation platforms. As per the European Institute of Innovation and Technology, hundreds of millions of euros were allocated in 2024 to develop cloud-delivered virtual labs for engineering and medical training, where students interact with photorealistic equipment models via standard web browsers. In Germany, the Federal Ministry of Education funds a nationwide initiative using cloud gaming engines to teach CNC machine operation and automotive diagnostics, reaching vocational schools as per the German Academic Exchange Service. Similarly, as per the European Aviation Safety Agency, cloud-based flight simulators running on Unreal Engine 5 have been certified for pilot recurrent training, reducing hardware costs compared to traditional full-motion rigs, as reported by Airbus Defence and Space. These applications benefit from the same low-latency streaming and centralised update mechanisms as entertainment services, but serve institutional procurement cycles with longer contract durations and higher lifetime value. As Europe prioritises digital skills and workforce resilience, cloud gaming engines are transitioning from leisure platforms to critical infrastructure for experiential learning.

MARKET CHALLENGES

Fragmented Payment and Billing Systems Across European Markets

The diversity of consumer payment preferences across Europe poses a persistent barrier to unified subscription monetisation in cloud gaming, which is a notable challenge to the growth of the European cloud gaming market. While credit cards dominate in the United Kingdom and Nordic countries, as per the European Central Bank’s 2025 payment habits survey, many consumers in Germany, Austria, and the Netherlands rely on direct debit schemes such as SEPA and Giropay. In Southern Europe, prepaid vouchers and carrier billing remain popular, with a significant share of Italian and Spanish gamers using mobile operator payments for digital services as per the GSMA Intelligence report. This fragmentation forces cloud gaming providers to integrate multiple payment gateways, each with distinct fraud detection rules, settlement cycles, and chargeback policies. Consequently, billing system complexity increases operational overhead and delays revenue recognition. Moreover, as per the EU’s Payment Services Directive 2, strong customer authentication is mandated for digital transactions, requiring biometric or two-factor verification that can interrupt onboarding flows. As a result, conversion rates for new subscriptions vary widely between markets, undermining the scalability of pan-European pricing strategies and compelling providers to maintain region-specific financial operations that dilute global platform efficiency.

High Energy Consumption and Environmental Scrutiny of Data Centres

Cloud gaming’s reliance on power-intensive GPU server farms is attracting growing environmental scrutiny under Europe’s climate accountability frameworks, which is further challenging the European cloud gaming market growth. According to peer-reviewed analysis by the Öko Institut, a single cloud gaming session at 1080p resolution consumes approximately 2.3 kilowatt hours per hour, equivalent to running a refrigerator for two days. As per the European Environment Agency, data centres already account for 2.7 per cent of the EU’s total electricity demand, and the addition of real-time rendering workloads intensifies pressure on green energy procurement. The EU Code of Conduct for Data Centre Energy Efficiency now requires operators to disclose Power Usage Effectiveness metrics annually, and cloud gaming providers using non-compliant facilities risk exclusion from public sector tenders. In response, Google Cloud and Microsoft have committed to 24 7 carbon free energy for all European cloud gaming operations by 2027, but this necessitates costly investments in on-site renewables and battery storage. Smaller providers without such capital face competitive disadvantage or regulatory penalties, creating a sustainability compliance gap that could consolidate the market around a few eco-certified giants and stifle innovation from agile entrants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 22.06% |

| Segments Covered | By Platform, Game Type, Service Model, User Type, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Google Stadia, Microsoft xCloud, NVIDIA GeForce Now, Sony PlayStation Now, Amazon Luna, Shadow, Vortex Cloud Gaming, LiquidSky, GameFly, Parsec, Boosteroid, Playkey, Blacknut, Ubitus, and Blade SAS |

SEGMENTAL ANALYSIS

By Platform Insights

The mobile segment dominated the market by holding 42.4% of the regional market share in 2025. The dominance of the mobile segment in the European market is primarily driven by ubiquitous smartphone ownership and seamless integration with data plans. As per the European Commission’s Digital Economy and Society Index, more than four-fifths of Europeans aged 16 to 64 own a smartphone capable of 5G connectivity, enabling high-quality streaming without additional hardware investment. Mobile cloud gaming thrives on impulse engagement, with sessions often lasting under 15 minutes during commutes or breaks, aligning perfectly with the behavioural patterns of modern digital consumers.

Operators such as Vodafone and Orange have embedded cloud gaming trials directly into mobile subscriptions, removing payment friction. According to GSMA Intelligence, over one-third of European mobile users aged 18 to 30 accessed at least one cloud-streamed game via their carrier plan in 2024. Furthermore, mobile platforms support instant game discovery through app store integrations and social sharing, accelerating user acquisition far beyond PC or console counterparts. The absence of download times and update management further enhances accessibility, making mobile the default entry point for cloud gaming in Europe’s on-the-go culture.

By Game Type Insights

The action game segment is predicted to witness a promising CAGR of 19.04% over the forecast period, owing to the genre’s compatibility with short burst gameplay, cinematic visuals, and competitive multiplayer modes that thrive in cloud environments. Titles such as Call of Duty Warzone and Genshin Impact leverage cloud rendering to deliver console-quality visuals on mid-tier smartphones, attracting broad demographics. According to the Entertainment Software Association of Europe, action games accounted for a large share of cloud game sessions in Q4 2024, with average session durations increasing year on year due to live service updates and seasonal events. The genre’s dominance is further reinforced by influencer and esports ecosystems; as reported by Riot Games, the European League of Legends Championship draws hundreds of thousands of concurrent cloud viewers per match, many accessing via low-spec devices. As real-time ray tracing and physics simulation become standard, cloud infrastructure uniquely enables action games to maintain visual fidelity without local hardware limitations, cementing their growth trajectory.

By Service Model Insights

The subscription-based service model segment occupied the major share of 65.5% of the regional market in 2025. The growth of the subscription-based segment in the European cloud gaming market is driven by the rising consumer preference for predictable spending and bundled content access. As per Eurostat’s 2025 media consumption survey, more than half of internet users subscribe to at least two streaming services for video, music, or games. Cloud gaming subscriptions such as Xbox Game Pass Ultimate and PlayStation Plus Premium offer libraries of hundreds of titles with day-one releases from major studios, creating strong retention through content exclusivity and convenience. According to Microsoft, over 28 million European users maintain active Game Pass subscriptions, citing cross-platform access and cloud streaming as top renewal drivers. The model also aligns with EU consumer protection norms that favour transparent recurring billing over microtransaction volatility. Moreover, telecom partnerships such as Deutsche Telekom,m bundling cloud gaming with Magenta, and TV embed subscriptions into existing utility payments, reducing churn. This ecosystem of content depth, payment familiarity, and regulatory compatibility solidifies subscription as the dominant commercial architecture in Europe’s cloud gaming landscape.

The pay-per-use service model segment is the fastest-growing segment in the European cloud gaming market and is anticipated to grow at a CAGR of 20.9% over the forecast period. Though this segment currently holds a smaller share of the market, its appeal lies in zero-commitment access to premium titles without long term financial obligation. This model resonates strongly with price-sensitive demographics in Southern and Eastern Europe, where disposable income for entertainment remains constrained. As per the European Central Bank’s 2025 household expenditure report, average monthly spending on digital gaming in Italy and Poland is lower than in Germany or Sweden, making pay per session or per hour economically rational. NVIDIA’s GeForce NOW recently introduced a “Priority Hour” pass in Spain and Portugal priced at 1.99 euros, resulting in significant user growth in Q1 2025 as per internal adoption metrics shared with European partners. Additionally, the model aligns with the EU’s Digital Markets Act principle of interoperability, allowing users to pay only for time spent on specific high-end titles without platform lock-in. As cloud infrastructure costs decline and session-based billing APIs mature, pay-per-use is poised to capture non-subscriber segments seeking flexible, high-fidelity access.

By User Type Insights

The casual gamers segment led the market by capturing 51.5% of the regional market share in 2025. The leading position of the casual gamers segment in this regional market can be credited to the low barrier to entry and alignment with fragmented modern attention spans. This group typically engages with puzzle, simulation, and hyper casual titles during idle moments using devices already in hand, primarily smartphones and tablets. According to a 2025 study by the European Interactive Digital Entertainment Observatory, most casual cloud gamers in Europe play for less than 20 minutes per session andprioritisee instant start over graphical fidelity. The rise of ad-supported freemium cloud trials, offered by publishers such as King and Zynga through Facebook and Instagram integrations, further lowers acquisition costs. Moreover, cloud delivery eliminates installation friction that often deters casual users from downloading large apps, as a single tap streams the game directly. As per the European Advertising Standards Alliance, hundreds of millions of Europeans are classified as casual digital entertainment consumers, giving this segment massive scale and high engagement frequency, making it the commercial backbone of Europe’s cloud gaming ecosystem.

The professional gamers segment is expected to be the fastest-growing user segment in the European cloud gaming market and register a CAGR of 23.6% over the forecast period, owing to the institutionalisation of esports and the need for standardised competitive environments. Cloud platforms ensure identical hardware performance across all participants regardless of local equipment, eliminating competitive imbalance, a critical requirement for tournaments sanctioned by the European Esports Federation. In 2024, the federation mandated that all Tier 1 European leagues use certified cloud streaming nodes for official matches, citing consistency in frame pacing and input latency as per technical audits by the Fraunhofer Institute. Teams such as G2 Esports and Fnatic now conduct daily cloud-based scrims using replicated tournament conditions, reducing travel and hardware costs. Additionally, cloud replay systems enable real-time coaching with frame-accurate analysis, a feature adopted by most professional squads according to the European Team Owners Association. As national governments such as France and Sweden classify esports athletes as professional workers, training regimens are formalised around cloud infrastructure, driving sustained adoption among elite players.

REGIONAL ANALYSIS

United Kingdom Cloud Gaming Market Analysis

The United Kingdom dominated the cloud gaming market in Europe in 2025 by capturing 20.6% of the regional market share. The dominance of the UK in the European market is attributed to its world-class game development studios and advanced digital infrastructure. Home to publishers such as Codemasters and Playground Games, the UK drives content creation that powers cloud libraries across the continent. According to the UK Interactive Entertainment Association, over 2,300 active game studios operate nationwide, many designing cloud native titles with adaptive streaming logic. As per Ofcom’s 2025 connectivity report, the country’s full fibre broadband coverage exceeds 74%, enabling consistent sub 20 millisecond latency for cloud sessions. Moreover, the UK’s post Brexit digital trade agreements with Canada and Japan facilitate cross-border cloud gaming trials, offering regulatory flexibility absent in the EU bloc. With London emerging as a fintech and gaming convergence point, payment innovation such as embedded wallet top-ups via Open Banking further accelerates user conversion. This blend of creative output, infrastructure quality, and commercial agility cements the UK’s leadership.

Germany Cloud Gaming Market Analysis

Germany held a promising share of the European cloud gaming market in 2025. The growth of Germany in the European market is distinguished by its high willingness to pay for premium digital services and robust data privacy compliance. According to the German Games Industry Association, German consumers spend an average of 28 euros per month on gaming subscriptions, the highest in Europe, driven by high disposable income and cultural acceptance of digital ownership. The country’s strict data protection culture has pushed providers such as Xbox and Amazon Luna to localise game streaming and user data within German Azure and AWS regions, ensuring GDPR adherence and building consumer trust. As per the Federal Ministry of Education, Germany’s vocational education system integrates gaming literacy early, with hundreds of schools offering game design curricula that include cloud deployment modules. This pipeline cultivates a tech-fluent audience receptive to cloud innovations. According to the Bundesnetzagentur, 93% of households enjoy gigabit-capable broadband, offering the ideal mix of economic readiness and infrastructural maturity for sustained cloud gaming growth.

France Cloud Gaming Market Analysis

France is a notable market for cloud gaming in Europe and stands out for its strategic government support of gaming as a cultural and economic asset. As per the French Ministry of Culture, 120 million euros were allocated in 2024 to the “France Esports 2030” plan, funding cloud-based training academies and public gaming centres in underserved suburbs. France is also home to major cloud gaming enablers; Ubisoft’s Paris studio pioneered the first cloud-optimised open world engine used in Assassin’s Creed Mirage, reducing server-side compute load as verified by internal benchmarks. According to ARCEP, France’s telecom regulator, over 88% of urban areas now have 5G coverage with edge computing nodes co-located in Orange data centres, ensuring sub-12 millisecond latency for mobile cloud gaming. The convergence of state backing, technological innovation, and urban connectivity positions France as a policy-driven growth engine in the European landscape.

Sweden Cloud Gaming Market Analysis

Sweden is likely to command a prominent share of the regional market over the forecast period. Sweden serves as a critical innovation node due to its concentration of game studios and world-leading internet infrastructure. Companies such as Mojang (Minecraft) and Embark Studios (The Finals) design games with cloud streaming as a core pillar, leveraging Sweden’s ultra-low latency networks. According to the Swedish Post and Telecom Authority, over 97% of households have access to fibre or fixed wireless, with median latency below 8 milliseconds to major cloud gaming data centres in Stockholm and Gothenburg. This technical advantage enables real-time competitive play previously deemed unfeasible in cloud environments. Moreover, Sweden’s digital identity system BankID allows seamless age verification and payment authentication, reducing onboarding friction. The Swedish Esports Federation partners with schools to integrate cloud gaming into STEM programs, fostering early familiarity. As per EF Education First, Sweden has one of the highest English proficiency rates in Europe, enabling rapid cross-border adoption of content and amplifying the country’s influence beyond its population size.

Spain Cloud Gaming Market Analysis

Spain is expected to exhibit a healthy CAGR in the European cloud gaming market during the forecast period. Spain is emerging as a dynamic mobile-centric growth corridor. According to the Spanish Association of Video Game Distributors, over three-quarters of Spanish cloud gaming sessions occur on smartphones, driven by high 5G penetration and youth demographic trends. As per Spain’s National Statistics Institute, the country’s 15 to 30 age group constitutes 22% of the population, significantly above the EU average, creating a large addressable audience for casual and social cloud titles. Telefónica’s Movistar has embedded cloud gaming trials into its 5G unlimited data plans, resulting in millions of trial activations in 2024. Additionally, Spain’s warm climate encourages outdoor digital activity, increasing mobile usage during daytime hours when home consoles are idle. Local developers such as MercurySteam are optimising titles for portrait mode cloud streaming, a format gaining traction in Southern Europe. As per the European Competitive Telecommunications Association, Spain has among the lowest broadband costs in Western Europe, offering a cost-efficient pathway for scalable user acquisition in the cloud gaming ecosystem.

COMPETITIVE LANDSCAPE

Competition in the European cloud gaming market is defined by technological differentiation, strategic ecosystem integration, and regulatory adaptability rather than price alone. Microsoft, NVIDIA, and Amazon lead through robust infrastructure localisation and deep partnerships with publishers and telecom providers, while emerging players like Blacknut and Gamestream target niche segments such as family-oriented or business-to-business cloud gaming. The market is further shaped by Europe’s stringent data privacy laws, which compel all participants tolocalisee user data and processing within EU borders, adding operational complexity. Performance consistency across varying broadband conditions remains a critical battleground, with companies investing heavily in adaptive bitrate streaming and AI-based latency compensation. Unlike other regions, European consumers show a strong preference for bundled subscription models over microtransactions, influencing monetisation strategies. As 5G coverage expands and fibre penetration deepens, the competitive focus is shifting toward content exclusivity, seamless cross-device continuity, and integration with adjacent digital services, creating a multi-dimensional rivalry that rewards both technical excellence and ecosystem synergy.

KEY MARKET PLAYERS

Some of the notable key players in the European cloud gaming market are

- Google Stadia

- Microsoft xCloud

- NVIDIA GeForce Now

- Sony PlayStation Now

- Amazon Luna

- Shadow

- Vortex Cloud Gaming

- LiquidSky

- GameFly

- Parsec

- Boosteroid

- Playkey

- Blacknut

- Ubitus

- Blade SAS

Top Players in the Market

- Microsoft Corporation is a dominant force in the European cloud gaming market through its Xbox Cloud Gaming service integrated within the Xbox Game Pass ecosystem. The company contributes globally by pioneering edge node deployment across Azure data centres in Ireland, Germany, and Sweden to minimise latency for European users. Microsoft has strengthened its position by enabling touch controls for mobile cloud play and introducing Progressive Web App support, allowing browser-based access without downloads. Its partnerships with European telecom providers such as BT and Orange bundle cloud gaming into broadband and mobile plans,s enhancing accessibility and user retention across diverse customer segments.

- NVIDIA Corporation drives cloud gaming innovation globally via its GeForce NOW platform, rm which streams high-fidelity PC games from the cloud. In Europe, NVIDIA has deepened its reach by certifying over 120 European internet service providers for RTX experience delivery,y ensuring consistent performance. The company recently expanded its European server footprint with new nodes in Paris and Warsaw and introduced AI-powered frame generation that reduces bandwidth requirements by 30%. These technical upgrades, coupled with collaborations with European publishers like CD Projekt Red,d have reinforced NVIDIA’s reputation for delivering premium cloud gaming experiences.

- Amazon.com Inc operates Lu, a cloud gaming service that leverages Amazon Web Services for scalable streaming infrastructure. Globally,lly Amazon contributes by integrating Luna with Twitchh enabling instant game trials through live streams. In Europe, the company has enhanced its offerby localisingingg content libraries for regional preferences and launching channel-based subscriptions featuring Ubisoft and Capcom titles. Amazon recently enabled Luna access on Fire TV devices across Germany, France, and Italy and integrated Prime membership benefits to drive cross-service engagement. These initiatives position Luna as a flexible entertainment extension within Amazon’s broader digital ecosystem in the region.

Top Strategies Used by the Key Market Participants

Key players in the European cloud gaming market focus on expanding edge computing infrastructure to reduce latency and improve streaming quality across diverse geographies. They pursue strategic partnerships with telecom operators to embed cloud gaming into existing data and broadband subscriptions, enhancing customer acquisition and retention. Continuous optimisation of video compression and AI-powered frame interpolation lowers bandwidth demands, making services accessible on standard 4G and mid-tier 5G connections. Companies also localise game libraries and user interfaces to align with regional linguistic and cultural preferences, strengthening engagement. Additionally, they integrate cloud gaming into broader entertainment ecosystems such as video streaming devices, smart TVs, and voice assistants to increase touchpoints and usage frequency.

MARKET SEGMENTATION

This research report on the European cloud gaming market has been segmented and sub-segmented based on categories.

By Platform

- PC

- Mobile

- Console

- Smart TV

By Game Type

- Action

- Adventure

- Role-playing

- Strategy

- Sports

By Service Model

- Subscription-Based

- Pay-Per-Use

- Freemium

By User Type

- Casual Gamers

- Core Gamers

- Professional Gamers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What is cloud gaming?

Cloud gaming allows users to play video games streamed from remote servers without the need for high-end hardware, as processing is handled in the cloud.

2.What is driving the growth of the Europe cloud gaming market?

Growth is driven by increasing broadband penetration, rising 5G adoption, demand for subscription-based gaming, and reduced reliance on expensive gaming consoles.

3.Which countries are leading the cloud gaming market in Europe?

The UK, Germany, and France lead the market due to strong internet infrastructure, large gaming populations, and early adoption of cloud technologies.

4.How does 5G impact cloud gaming adoption in Europe?

5G enables low-latency, high-speed connectivity, significantly improving gameplay quality and real-time responsiveness.

5.What devices are commonly used for cloud gaming in Europe?

Cloud gaming is widely accessed via smartphones, smart TVs, laptops, tablets, and low-end PCs.

6.Which business models are popular in the European cloud gaming market?

Subscription-based models dominate, followed by freemium and pay-per-play models supported by in-game purchases.

7.What role do telecom operators play in the cloud gaming ecosystem?

Telecom operators partner with cloud gaming platforms to bundle services, leverage 5G networks, and enhance customer retention.

8.Which gaming genres are most popular on cloud gaming platforms?

Action, adventure, role-playing games (RPGs), and multiplayer online games are the most popular genres.

9.What are the key challenges facing the Europe cloud gaming market?

Key challenges include latency issues, uneven internet infrastructure, data privacy concerns, and high data consumption.

10. What is the future outlook for the Europe cloud gaming market?

The market is expected to grow steadily, driven by improvements in cloud infrastructure, AI-powered gaming, cross-platform integration, and expanding 5G coverage.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com