Europe Compression Garments and Stockings Market Size, Share, Trends & Growth Forecast Report By Product Type, By Application, By End User, and By Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$0.82 BnMarket Estimate, 2026

$0.86 BnMarket Forecast, 2034

$1.32 BnCAGR, 2026–2034

5.51%Europe Compression Garments and Stockings Market Size

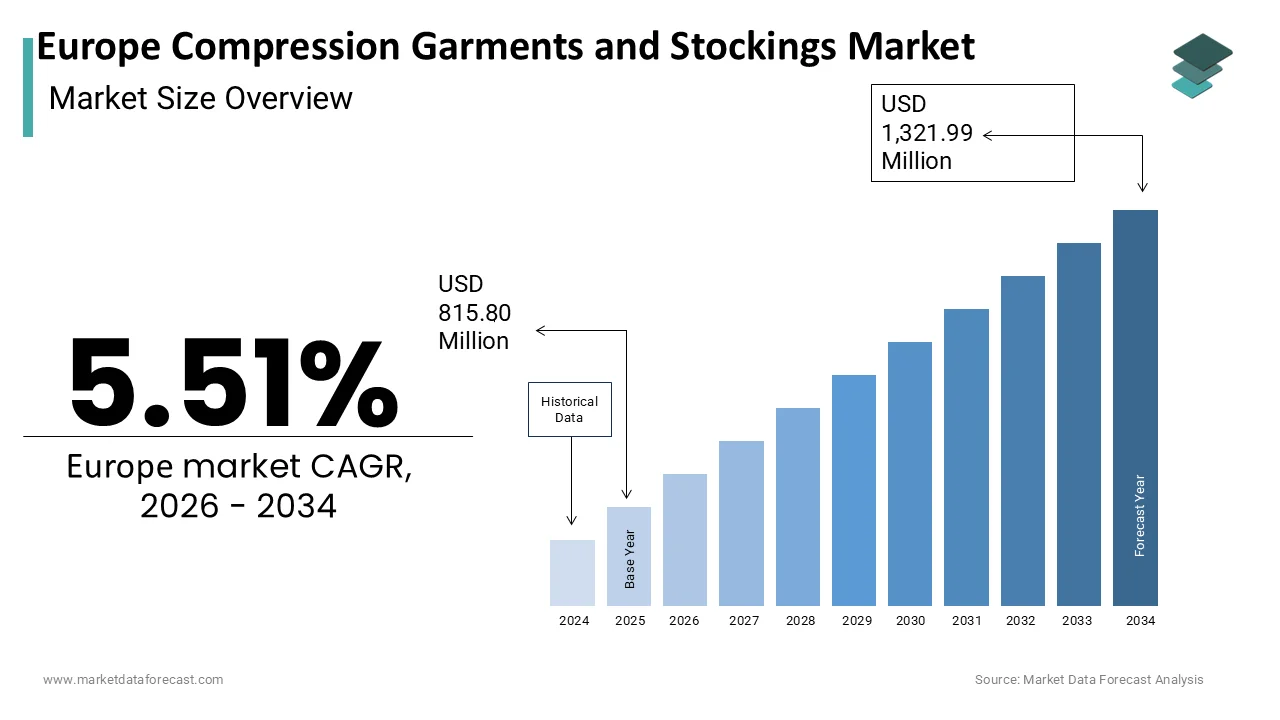

The Europe Compression Garments and Stockings Market is projected to grow from USD 815.80 million in 2025 to USD 860.75 million in 2026 and reach USD 1,321.99 million by 2034, registering a CAGR of 5.51% from 2026 to 2034.

Compression garments and stockings refer to specialized elastic textile products engineered to apply graduated pressure on the limbs primarily to enhance venous return,n prevent blood pooling, and reduce the risk of thromboembolic events. These medical devices are classified under Class I or Class IIa in the European Union Medical Device Regulation, depending on their intended use and pressure gradient. Their application spans clinical settings such as post-surgical recovery and chronic venous insufficiency management, as well as preventive use in high-risk populations, long-haul travelers, and pregnant women. According to the European Society for Vascular Surgery (ESVS), studies indicate a high prevalence of chronic venous disease (CVD), with risk increasing with age. Furthermore, the World Health Organization estimates that venous thromboembolism accounts for a significant number of hospitalizations annually across the EU, making prophylactic compression a critical component of public health strategy. The aging demographic structure exacerbates demand as per Eurostat, 21.3 percent of the EU population was aged 65 or older in 202,3, a figure projected to reach 29 percent by 2050. This epidemiological shift, coupled with heightened clinical awareness and updated hospital protocols for thrombosis prevention, continues to anchor the therapeutic relevance of compression therapy in European healthcare systems.

MARKET DRIVERS

Rising Prevalence of Venous Disorders Fuels Clinical Demand

The escalating burden of chronic venous disease and related complications constitutes a major accelerator for the Europe compression garments and stockings market growth. According to the European Society for Vascular Surgery, approximately 40 percent of women and 25 percent of men in Europe suffer from some form of venous insufficiency with symptoms ranging from leg swelling to venous ulcers. This condition is particularly prevalent in aging populations and those with sedentary lifestyles, both of which are increasingly common across the continent. Eurostat notes that 28 percent of European adults report sitting for more than seven hours per day outside of work hours, which significantly elevates venous stasis risk. In clinical practice, compression therapy remains the first-line non-invasive intervention for managing these conditions, with guidelines from the National Institute for Health and Care Excellence in the United Kingdom recommending its use for all patients with varicose veins and edema. Hospitals across Germany, France, and Italy have institutionalized compression stocking protocols for postoperative and immobile patients following evidence that such measures reduce deep vein thrombosis incidence, as per sources. The integration of these guidelines into national healthcare pathways ensures consistent prescription volumes and reinforces the medical necessity of compression products beyond cosmetic or lifestyle applications.

Integration of Compression Therapy into Hospital Thromboprophylaxis Protocols

The systematic adoption of mechanical thromboprophylaxis in European hospitals has fuelled the expansion of the Europe compression garments and stockings market. This institutionalization stems from robust clinical evidence showing that mechanical compression reduces venous thromboembolism risk when used alone and even more when combined with pharmacological agents. The European Commission’s Patient Safety Initiative has further reinforced this practice by including venous thromboembolism prevention as a core quality indicator for hospital accreditation. Besides, the United Kingdom’s National Health Service procures millions of pairs annually under centralized tenders to ensure protocol compliance across trusts. These systemic procurement mechanisms create stable, recurring demand insulated from consumer market fluctuations. Moreover, updated guidelines from the European Wound Management Association now recommend compression as essential in venous ulcer healing protocols, further expanding clinical indications and solidifying the role of these garments within evidence-based care pathways.

MARKET RESTRAINTS

Patient Non-Compliance Due to Discomfort and Poor Fit

Patient non-compliance restrains the growth of the Europe compression garments and stockings market. This is because of physical discomfort and inadequate sizing. As per studies, a considerable proportion of patients tend to discontinue use of certain dermatological or wearable treatments within the initial weeks, primarily due to discomfort factors such as skin irritation, overheating, or challenges in application. Standard off-the-shelf products often fail to accommodate anatomical variations, particularly in elderly patients who may have edema, a joint deformity, or an irregular limb.b The non-adherence not only diminishes therapeutic outcomes but also increases the risk of complications such as ulcer recurrence or post-thrombotic syndrome. Custom-knit options are available, but their high cost and lack of public reimbursement make them inaccessible for most people in member states. The effectiveness of compression therapy is hindered by patient dropout, which will persist until scalable personalized fitting becomes possible with technologies like 3D scanning and adaptive textiles.

Stringent Regulatory Classification Under EU MDR Increases Time to Market

The implementation of the European Union Medical Device Regulation has introduced significant compliance hurdles for manufacturers that hold back the expansion of the Europe compression garments and stockings market. Unlike previous directives, the MDR classifies many graduated compression products as Class IIa medical devices requiring rigorous clinical evaluation, technical documentation, ion, and notified body oversight. According to research, many legacy compression products underwent reclassification in 2021, necessitating new conformity assessments. This regulatory recalibration has extended the average time to market by several months. Smaller European manufacturers, particularly those in Southern and Eastern Europe, lack the internal resources to navigate the complex documentation demand, post-market surveillance plans, and unique device identification implementation. Consequently, several niche brands have exited the market or limited their portfolios to Class I items with lower pressure gradients, which may not meet clinical needs. The regulation also mandates greater transparency in performance claims, compelling companies to generate new clinical data for even well-established products.

MARKET OPPORTUNITIES

Expansion of Telehealth Enables Remote Fitting and Follow-Up

The rapid adoption of digital health services for addressing longstanding barriers related to accessibility and adherence offers new opportunities for the growth of the Europe compression garments and stockings market. According to studies, many EU member states reimburse teleconsultations for chronic disease management, including venous disorders. This infrastructure enables vascular specialists to conduct virtual assessments, prescribe appropriate compression levels, nd coordinate with certified fitters via video. Companies have launched digital fitting platforms that use AI-powered limb measurement tools, allowing patients to self-scan their legs using smartphone cameras. These platforms integrate with electronic health records, ensuring continuity of care and automatic prescription renewal. In Sweden and the Netherlands, national wound care programs have piloted remote monitoring where patients upload weekly photos of their legs, enabling clinicians to adjust compression strategies in real time. This digital integration not only improves compliance but also expands market reach to rural mobility-limited populations who previously faced logistical challenges in accessing fitting services.

Growing Emphasis on Preventive Care in Occupational Health Programs

Workplace wellness initiatives in the region are increasingly incorporating compression garments as a preventive measure for employees in high-risk occupations, which is setting up new opportunities for the expansion of the Europe compression garments and stockings market. According to sources, prolonged standing or sitting is prevalent in sectors such as healthcare, retail, logistics, and aviation,n with millions of workers exposed to venous risk factors daily. In addition, France’s National Health Insurance reimburses Class I compression hosiery for pregnant women employed in standing jobs following evidence that early intervention reduces edema and varicose vein progression. The United Kingdom’s Health and Safety Executive updated its guidelines in 2023 to recommend employer-provided compression wear for workers with more than four hours of static posture per shift. These policy shifts transform compression garments from reactive medical devices into proactive occupational health tools. Corporate procurement programs with companies like Lufthansa and Carrefour distributing branded compression socks to frontline staff further normalize usage and drive volume.

MARKET CHALLENGES

Lack of Standardized Pressure Measurement Across Products

The absence of uniform methodologies for measuring and labeling graduated pressure, which affects clinical reliability and consumer trust, thereby hinders the growth of the Europe compression garments and stockings market. Although the European standard EN 12718 defines testing protocols for compression hosiery, actual pressure delivery varies significantly based on fabric elasticity, knitting technique, and limb geometry. According to research, not all commercially available Class II stockings consistently deliver the labeled 23 to 32 mmHg pressure range during real-world wear due to factors like fabric fatigue and improper sizing. This variability complicates clinical decision-making as physicians cannot be certain of the therapeutic dose being administered. The European Wound Management Association has called for dynamic in vivo pressure monitoring to replace static bench testing, yet no regulatory mandate exists. Consequently, patients may receive subtherapeutic compression leading to treatment failure or excessive pressure causing skin breakdown, particularly in elderly or diabetic individuals. The use of pressure-mapping systems in development is not mandatory for CE marking, though it is a practice adopted by some manufacturers. The significant discrepancy between the stated and actual compression of medical devices will continue to be a major clinical and commercial problem until the EU mandates harmonized performance validation via real-time biomechanical assessment.

Limited Reimbursement for Advanced or Customized Products

Reimbursement policies across Europe, which often restrict coverage to basic, off-the-shelf models, limit access to advanced or personalized solutions that could improve outcomes and impede the expansion of the European compression garments and stockings market. According to studies, national health systems in some European countries, like Spain, Italy, and Poland, use cost-containment measures such as fixed price caps for certain classes of medical devices, including compression stockings. Custom knit garments, which offer superior fit for patients with lymphedema or severe deformities, are rarely covered outside Germany and the Nordic countries. The financial barrier disproportionately affects low-income and elderly populations who are most vulnerable to venous complications. Moreover, newer technologies such as temperature-regulating or antimicrobial textiles are classified as comfort enhancements rather than medical necessities, excluding them from public funding. The market's focus on low-cost generics, which can hinder therapeutic effectiveness and patient quality of life, is a direct result of outdated reimbursement frameworks that fail to account for long-term cost savings from better adherence and fewer complications.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End User and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Leonisa, Inc., Medical Z, 2XU Pty. Ltd, 3M, BSN Medical, Medi GmbH & Co KG, Nouvelle, Inc., Santemol Group Medical. |

SEGMENTAL ANALYSIS

By Product Insights

The compression stockings segment was the leading segment in the Europe compression garments and stockings market by capturing a substantial share in 2025. The growth of the compression stockings segment is attributed to their widespread clinical adoption as a first-line intervention for venous disorders and thromboprophylaxis. Their standardized design, ease of use, and established reimbursement pathways make them the default choice across hospitals and outpatient settings. In addition, their integration into national clinical guidelines for deep vein thrombosis prevention also drives the growth of this segment. According to sources, many surgical protocols in EU hospitals use knee-length compression stockings for perioperative patients. The simplicity of stocking application compared to full garments also enhances patient compliance, particularly among elderly users who constitute the majority of chronic venous disease cases. Furthermore, national health systems in Germany, France, and the United Kingdom maintain centralized procurement contracts for Class I and Class II stockings, ensuring consistent volume demand and market stability.

The compression segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 9.4% from 2025 to 2022 due to rising demand for customized solutions in complex lymphatic and post-surgical care. Unlike standardized stockings, these garments, such as sleeveless vests and pantyhose, are engineered for anatomical precision in managing conditions that affect a large number of people. Their growth is further accelerated by advancements in seamless knitting and adaptive textile technologies that improve comfort and wearability. In oncology settings where secondary lymphedema is a common consequence of breast or pelvic cancer treatment, compression therapy is a critical and widely accepted treatment for lymphedema associated with cancer. Some countries have expanded public reimbursement to cover custom-fitted garments following mastectomy, with national health agencies recognizing their role in reducing long-term disability costs. Besides, the aesthetic and functional improvements in modern compression garments have broadened their appeal beyond clinical use into post-cosmetic surgery recovery, where demand has surged due to rising aesthetic procedure volumes. This convergence of medical necessity and patient-centric design fuels sustained double-digit growth.

By Application Insights

The varicose veins segment led the Europe compression garments and stockings market and occupied 47.1% of the regional market share in 2025. High prevalence of chronic venous insufficiency and its recognition as a progressive medical condition rather than a cosmetic concern has largely contributed to the expansion of the varicose veins segment. According to research, millions of adults in the EU exhibit clinical signs of venous reflux, with women affected at nearly twice the rate of men due to hormonal and pregnancy-related factors. National health systems across Europe classify compression therapy as a first-line conservative treatment before considering invasive procedures. The United Kingdom’s National Institute for Health and Care Excellence guidelines recommend a stepped approach for symptomatic varicose veins, prioritizing more effective interventional procedures. Moreover, in Germany, a doctor can prescribe medical compression stockings, and SHI will cover the cost for up to two pairs per year for diagnosed cases. The aging population further amplifies demand as venous valve deterioration is age-associated with notable prevalence in individuals over 65. Moreover, public awareness campaigns have destigmatized venous disease and encouraged early intervention. This combination of clinical validation policy support and demographic trends solidifies varicose veins as the cornerstone application segment.

The oncology segment is expected to exhibit a noteworthy CAGR of 11.2% over the forecast period, owing to the increasing incidence of cancer-related lymphedema and the integration of supportive care into comprehensive cancer treatment pathways. According to sources, a significant number of new cancer cases were diagnosed in Europe in 2023, with breast and prostate cancers, known to carry a high lymphedema risk, accounting for a portion of diagnoses. In addition, some countries have implemented mandatory lymphedema risk assessments within months of cancer surgery with immediate garment prescription for high-risk patients. Furthermore, the EU allocates funding for rehabilitation services that include certified lymphedema therapists who prescribe custom compression solutions. The oncology segment is set to grow rapidly beyond traditional venous applications, a shift driven by increasing policy support for survivorship care and the standardization of early detection protocols.

By End User Insights

The hospitals segment held the largest share of 41.5% of the Europe compression garments and stockings market. Their central role in acute care thromboprophylaxis and surgical recovery protocols propels the growth of the hospitals segment. The institutionalization of mechanical compression in perioperative and intensive care units creates consistent high-volume demand. According to studies, many hospitals in the EU have formal venous thromboembolism prevention bundles that include graduated compression stockings for immobile patients. In Germany, hospitals perform major orthopedic surgeries, each requiring extended postoperative compression. National procurement frameworks further consolidate hospital purchasing power with centralized tenders covering millions of units yearly. Apart from these, hospitals serve as primary referral points for chronic venous disease diagnosis, with vascular departments prescribing initial compression therapy before transitioning patients to outpatient care. The integration of compression protocols into hospital accreditation standards by bodies ensures compliance and sustained usage. This structural embedding within acute care workflows makes hospitals the most stable and dominant end-user channel despite the rise of alternative distribution models.

The online sales segment is predicted to witness the highest CAGR of 13.6% from 2025 to 2033. The rapid growth of the online sales segment is fueled by digital health adoption, evolving reimbursement models, and consumer preference for convenience. According to research, a notable share of EU citizens used health services in 2023, including teleconsultations and online medical product ordering. National health systems are adapting to this shift, with countries enabling e-prescriptions for compression products that can be fulfilled through certified online pharmacies. Companies have launched direct-to-consumer e-commerce platforms featuring virtual fitting assistants and AI-powered size recommendations. These tools address historical barriers like improper fit and improve adherence. Moreover, the post-pandemic acceleration in home-based care has normalized self-management of chronic conditions, with patients increasingly responsible for replenishing their own compression supplies. Online channels are set to disrupt traditional distribution hierarchies, driven by the increasing regulatory recognition of digital therapeutics and the expansion of e-health services across the EU.

COUNTRY LEVEL ANALYSIS

Germany Compression Garments And Stockings Market Analysis

Germany outperformed other regions in the Europe compression garments and stockings market by accounting for 24.1% share in 2025. The dominance of Germany is due to its robust healthcare infrastructure, the high prevalence of venous and lymphatic disorders, and comprehensive reimbursement policies. The country has the highest number of certified lymphedema therapists in Europe, with practitioners recognized by the German Lymphology Society, ensuring widespread access to specialized compression care. Statutory health insurance covers both standard and custom compression products for diagnosed conditions, including up to six garment changes per year for lymphedema patients. According to research, chronic venous disease affects millions of Germans, with prevalence rising sharply after age 50. Germany also hosts leading manufacturers SuMedis, Medii, and Bauerfeind, whose R and D investments in seamless knitting and andpressure-mappingg technologies set industry benchmarks. This ecosystem of clinical expertise, policy support, and domestic innovation cements Germany’s position as the region’s most mature and influential market.

France Compression Garments And Stockings Market Analysis

France followed closely in the Europe compression garments and stockings market by capturing 17.4% share in 2025. The growth of France is attributed to strong public health initiatives and high patient awareness of venous health. The French National Health Insurance reimburses compression stockings at a share for conditions like varicose veins and post-thrombotic syndrome, with full coverage for pregnant women and lymphedema patients. According to sources, a notable number of compression prescriptions are issued annually, which reflects deep integration into primary care. The country also pioneered national awareness campaigns which reach a large number of citizens yearly and reduce stigma around venous disease. France’s aging population amplifies demand as venous insufficiency prevalence exceeds. The presence of global players like Thuasne and local cooperatives ensures product diversity and competitive pricing. This blend of preventive public health policy, universal access, and demographic pressure sustains France’s leadership in therapeutic compression adoption.

United Kingdom Compression Garments And Stockings Market Analysis

The United Kingdom grew steadily in the Europe compression garments and stockings market, with evidence-based clinical guidelines and centralized procurement through the National Health Service. The UK also leads in wound care integration with district nursing teams routinely applying compression bandaging followed by stocking transition in community settings. Despite Brexit, the Medicines and Healthcare products Regulatory Agency maintains alignment with the EU MDR standardsensuring product safety and availability. The aging population, a share aged 65 or older, further fuels the need as venous leg ulcers affect people. Recent NHS Long Term Plan investments in community vascular services aim to reduce hospital admissions through early compression intervention. This systematic embedding within both acute and community care pathways ensures sustained market relevance.

Italy Compression Garments And Stockings Market Analysis

Italy gradually expanded in the Europe compression garments and stockings market because of high venous disease prevalence and regionalized healthcare delivery. According to research, a portion of adults exhibit clinical signs of chronic venous insufficiency, with rates exceeding in southern regions due to genetic and lifestyle factors. Italy also has a strong tradition of artisanal hosiery manufacturing, with companies producing high-quality medical-grade products. The rise in oncology-related lymphedema, driven by improved cancer survival rates, has expanded demand for custom garments, especially in northern regions with advanced cancer centers. Apart from these, Italy’s warm climate increases summer edema complaints, prompting seasonal over-the-counter purchases. This mix of clinical need, artisanal supply, and policy modernization supports steady market growth.

Netherlands Compression Garments And Stockings Market Analysis

The Netherlands is predicted to grow in the Europe compression garments and stockings market from 2025 to 20,33, owing to its integrated care model, Elsa, a digital health leader, and early adoption of lymphedema prevention protocols. The Dutch Healthcare Authority includes compression garments in the basic insurance package with no co-payment for diagnosed conditions, ensuring near universal access. According to sources, many breast cancer centers implement preoperative lymphedema risk assessment with immediate garment prescription for high-risk patients. The country also leads in telehealth-enabled compression management with platforms like ThromboDynamix, allowing remote monitoring of patient adherence and edema progression. Moreover, the Netherlands serves as a European logistics and innovation hub for global manufacturers, facilitating rapid product updates and clinical trials. This TThiforward-lookingecosystem positions the country as a model for next-generation compression care delivery.

COMPETITIVE LANDSCAPE

The Europe compression garments and stockings market features a competitive landscape defined by the coexistence of established medical device manufacturers and specialized regional players. Competition centers less on price and more on clinical validation, product innovation,n and integration into national healthcare protocols. Leading companies differentiate through advanced knitting technology, custom fit solutions, and digital health capabilities that improve patient adherence and outcomes. Regulatory complexity under the EU Medical Device Regulation has raised entry barriers favoring incumbents with robust quality management systems while pressuring smaller brands to consolidate or exit. Reimbursement policies vary significantly across countries, creating fragmented demand patterns that require localized commercial strategies. Despite this, the market is gradually shifting to value-based models where long-term therapeutic efficacy and cost savings drive procurement decisions. Emerging opportunities in oncology, lymphedema, and preventive care are attracting cross-sectoralnvestment, further intensifying competition through technological convergence and service bundling.

KEY MARKET PLAYERS

Notable companies leading the europe compression garments and stockings market profiled in the report are

- Leonisa, Inc.

- Medical Z

- 2XU Pty. Ltd

- 3M

- BSN Medical

- Medi GmbH & Co KG

- Nouvelle, Inc.

- Santemol Group Medical.

TOP LEADING PLAYERS IN THE MARKET

- Medi GmbH & Co KG is a leading German manufacturer of medical compression products with a strong footprint across Europe and global markets. The company specializes in custom-fitted compression garments for lymphedema, venous disorders, and post-surgical recovery, leveraging advanced seamless knitting and 3D scanning technologies. Medi has reinforced its position through strategic investments in digital health, including the launch of its Medii Scan app, which enables accurate self-measurement using smartphone cameras. It also partnered with European lymphedema clinics to integrate its products into standardized care pathways, enhancing clinical adoption and patient outcomes across the continent.

- Sigvaris Group, headquartered in Switzerland, nd is a globally recognized innovator in graduated compression therapy with deep roots in the European market. The company offers a comprehensive portfolio spanning medical stockings for venous insufficiency to lifestyle compression for travel and sports. Sigvaris has strengthened its European presence by aligning its product development with EU Medical Device Regulation requirements and investing in sustainable manufacturing practices. The company also enhanced its telehealth integration by collaborating with digital health platforms in France and the Netherlands to enable virtual fittings and e-prescriptions, supporting accessibility and adherence.

- Bauerfeind AG, a German medical technology company, is renowned for its high precision compression garments and orthopedic supports used in both clinical and performance settings. The company contributes significantly to the global market through its emphasis on biomechanical research and patient-centric design. In Europe, Bauerfeind has deepened its engagement with hospital networks by providing certified training programs for vascular care professionals. Its commitment to clinical validation through partnerships with academic hospitals further solidifies its reputation for evidence-based solutions.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe compression garments and stockings market employ several core strategies to sustain competitive advantage. They prioritize regulatory compliance by aligning product portfolios with the European Union Medical Device Regulation to ensure market access and patient safety. Companies invest in digital transformation through virtual fitting tools, telehealth integration,n and smart textiles that enhance adherence and data collection. Strategic collaborations with hospitals, lymphedema clinics, and national health systems embed their products into standardized care pathways. Sustainability initiatives use eco-friendly materials and circular design principles, addressing evolving consumer and policy expectations. Finally, they expand training and certification programs for healthcare professionals to reinforce clinical trust and proper product application across diverse care settings.

MARKET SEGMENTATION

This research report on the europe compression garments and stockings market has been segmented and sub-segmented into the following categories.

By Product

- Compression garments

- Compression stocking

By Application

- Varicose veins

- Wound care

- Burns

- Oncology

By End User

- Hospitals

- ASCs

- Clinics

- Online sales

- Healthcare

By Country

- UK

- France,

- Spain,

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic & Rest of Europe

Frequently Asked Questions

1. How is the Europe Compression Garments and Stockings Market segmented by product type?

The Europe Compression Garments and Stockings Market is segmented into compression stockings, compression garments, and anti-embolism stockings for diverse medical needs.

2. What are the main applications of compression garments in the Europe market?

In Europe, the Compression Garments and Stockings Market is primarily applied in medical uses such as varicose vein treatment, orthopedic recovery, and sports performance support.

3. Which countries lead the Europe Compression Garments and Stockings Market?

Germany, France, the UK, and Italy are key contributors to the Europe Compression Garments and Stockings Market due to advanced healthcare infrastructure and high product adoption.

4. How do compression levels affect the Europe Compression Garments and Stockings Market?

The Europe Compression Garments and Stockings Market includes products with varying compression levels like mild, moderate, firm, and extra-firm to address different medical conditions.

5. What materials are commonly used in compression garments in Europe?

The Europe Compression Garments and Stockings Market features materials such as nylon, spandex, cotton, microfiber, bamboo fiber, and moisture-wicking fabrics to enhance comfort and effectiveness.

6. How important is online distribution in the Europe Compression Garments and Stockings Market?

Online distribution channels are increasingly important for the Europe Compression Garments and Stockings Market, improving accessibility and consumer convenience.

7. What role does aging population play in the Europe Compression Garments and Stockings Market?

Aging population significantly boosts demand in the Europe Compression Garments and Stockings Market due to increased prevalence of chronic venous insufficiency and need for preventive healthcare.

8. How are sports and fitness influencing the Europe Compression Garments and Stockings Market?

The sports and fitness sectors contribute to the Europe Compression Garments and Stockings Market growth by driving demand for performance-enhancing compression wear.

9. What innovations are shaping the Europe Compression Garments and Stockings Market?

Innovation in the Europe Compression Garments and Stockings Market includes breathable fabrics, smart sensor integration, and advanced compression technology for improved patient outcomes.

10. How does regulatory environment impact the Europe Compression Garments and Stockings Market?

Strict regulatory standards in Europe ensure quality and safety in the Compression Garments and Stockings Market, particularly for medical-grade products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com