Europe Cookware Market Size, Share, Trends & Growth Forecast Report – Segmented By Product Type (Core Cookware, Specialized Cookware, Accessories), Material, End User, Distribution Channel, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Cookware Market Size

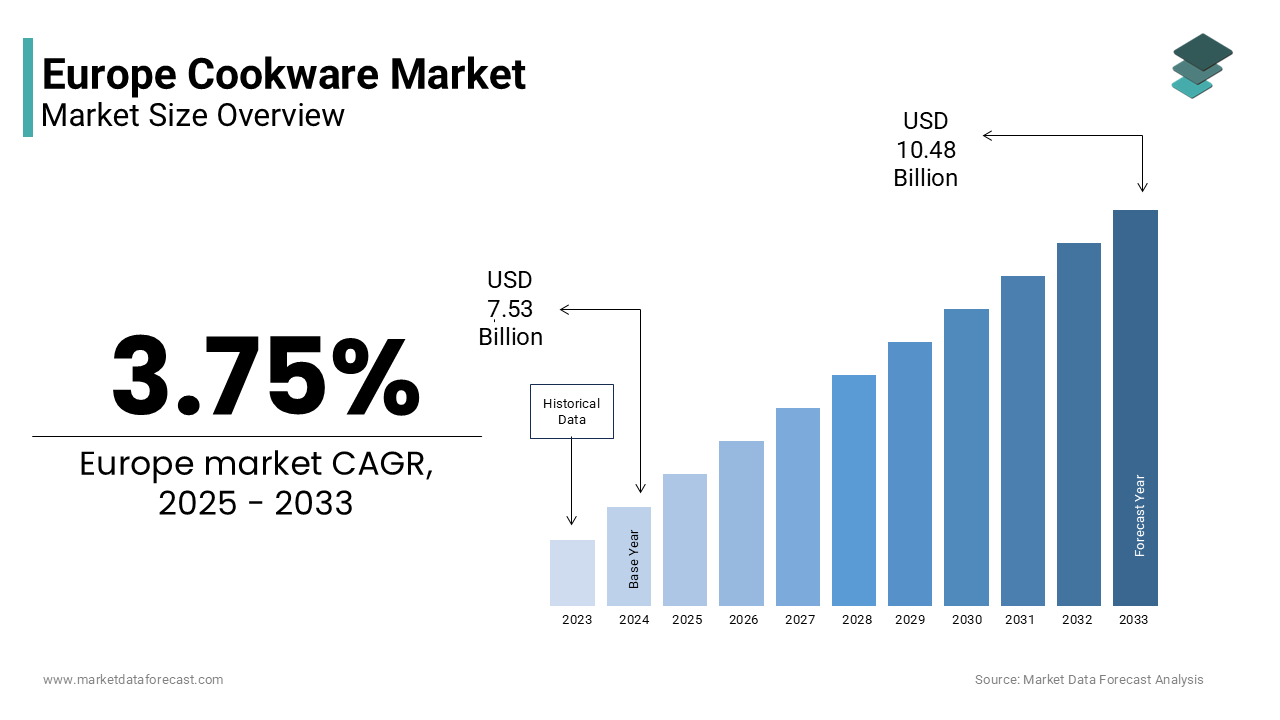

The Europe cookware market size was valued at USD 7.53 billion in 2024 and is projected to reach USD 10.48 billion by 2033 from USD 7.81 billion in 2025, growing at a CAGR of 3.75%.

The cookware is a diverse array of pots, pans and kitchen utensils designed for domestic and professional culinary use, characterised by strong regional preferences, material innovation, and evolving consumer expectations around health, sustainability, and design. Many European households reported replacing at least one cookware item annually by reflecting both wear and intentional upgrades. The European Chemicals Agency has intensified oversight of non-stick coatings, leading to a 40% decline in perfluorooctanoic acid-based products since 2020, according to the source. Concurrently, the European Committee for Standardisation maintains rigorous testing protocols under EN 12983 for thermal shock resistance, handle stability, and metal migration. Household cooking frequency remains robust, with some adults in France, Italy, and Spain preparing meals at home five or more times per week, as documented by the study. This cultural resilience, combined with regulatory evolution and material science advancements, defines the contemporary European cookware landscape as a convergence of heritage and innovation.

MARKET DRIVERS

Revival of Home Cooking and Culinary Tradition Fuels Premium Cookware Demand

The sustained resurgence of home cooking across Europe, amplified by post-pandemic behavioural shifts and cost-of-living pressures, has significantly elevated demand for durable, high-performance cookware. The revival of home cooking and culinary tradition fuels premium cookware demand,, is majorly fuelling the growth of the European cookware market. According to some sources, 74% of adults in Southern Europe cook at home at least five times per week, with similar trends emerging in Germany and the Netherlands, where home meal preparation increased by 18% between 2022 and 2024. This habitual engagement translates into greater scrutiny of cookware functionality, with consumers prioritising even heat distribution, ergonomic design, and longevity over disposable alternatives. Similarly, France’s artisanal cast iron and enamelled cookware segment is reflecting a preference for heirloom quality pieces linked to regional cuisine. The rise of food literacy through digital platforms further educates consumers on material performance, pushing them toward premium investments. This cultural reanchoring of cooking as both necessity and craft sustains a resilient demand for high-calibre cookware independent of short-term economic fluctuations.

Strict EU Regulations on Food Contact Materials Accelerate Shift to Safer Coatings

European Union legislation governing food contact materials has become a decisive driver of product innovation, and consumer preference is another attribute in leveraging the growth of the European cookware market. Regulation (EC) No 1935 2004 and its amendments require all materials intended to contact food to be inert and non-migratory under normal use conditions. The European Chemicals Agency banned perfluorooctanoic acid and related substances in non-stick coatings, leading to a near-complete phase-out across major brands. PFOA-based cookware sales in the EU declined by 40% between 2020 and 2024, replaced by ceramic, titanium diamond-infused alternatives, as per the recent survey. Companies like Tefal and WMF now prominently label their products as “PFOA free” and “EU compliant,” using third-party certifications from bodies like TÜV Rheinland to validate safety claims.

MARKET RESTRAINTS

High Import Dependency on Asian Manufacturing Increases Supply Chain Vulnerability

The heavy reliance on imports from China, Turkey, and Vietnam, by creating structural vulnerabilities to geopolitical tensions, shipping disruptions, and quality inconsistencies, is restraining the growth of the European cookware market. This dependency became particularly evident during the 2021-2022 global logistics crisis when container shortages caused lead times to stretch from six to 16 weeks, forcing retailers like Carrefour and Tesco to ration stock. Even post-pandemic, quality control remains a challenge. Turkish exports have grown as an alternative, yet they too face scrutiny under the EU’s General Product Safety Regulation. Local manufacturers such as Le Creuset and Fissler struggle to scale due to higher labour and energy costs, limiting domestic resilience.

Premiumization and Material Innovation Inflate Retail Prices Beyond Mass Market Reach

The shift toward high-performance materials, such as tri-ply stainless steel, forged aluminium, and ceramic reinforced coatings, has significantly increased average cookware prices, pricing out budget-conscious consumers. The premiumization and material innovation inflate retail prices beyond mass is additionally hindering the growth of the European cookware market. A mid-range stainless steel cookware set that cost 120 euros in 2020 now averages 210 euros in 2024, according to some data, which is driven by raw material inflation and compliance costs. While premium brands thrive in urban centres, affordability remains a barrier in Eastern and Southern Europe, where disposable income is lower. In Romania and Greece, over 60% of households still rely on basic uncoated aluminium or thin-gauge steel, as per the survey. This polarisation creates a two-tier market.

MARKET OPPORTUNITIES

Growth of Sustainable and Circular Cookware Models Opens New Consumer Segments

The emergence of circular economy principles in kitchenware is unlocking innovative business models centred on repairability, recyclability, and material transparency i,, escalating new opportunities for the growth of the European cookware market. European consumers increasingly favour brands that offer lifetime guarantees, take-back programs, and fully recyclable construction. Le Creuset’s “Forever Guarantee” covers cracks, hi, and defects indefinitely, with over 120000 pieces repaired or replaced across Europe in 2024. The EU Ecodesign for Sustainable Products Regulation, set to apply to cookware by 2027, will mandate durability labelling and disassembly instructions, accelerating this trend. Startups like Made In Cookware now offer modular sets with replaceable handles and bases, reducing waste.

Rise of Direct-to-Consumer and Experience-Based Retail Enhances Brand Loyalty

Cookware brands are bypassing traditional retail channels to build direct relationships with consumers through e-commerce, experiential showrooms, and culinary content. The rise of direct-to-consumer and experience-based retail enhances brand loyalty is gearing up the growth of the European cookware market. Companies like Staub and De Buyer operate branded boutiques in Paris, Berlin,n, and Milan that double as cooking studios, hosting workshops with chefs to demonstrate product performance. This model enables richer data collection on cooking habits, informing product development and personalised marketing. Crucially, it allows brands to communicate material provenance, manufacturing ethics, and care instructions directly elements often lost in mass retail.

MARKET CHALLENGES

Greenwashing and Lack of Standardised Sustainability Claims Undermine Consumer Trust

The absence of harmonised EU standards for environmental labelling has led to widespread greenwashing, eroding consumer confidence is a challenge for the growth of the European cookware market. Terms like “eco-friendly,” “green,” and “sustainable” are used without third-party verification, confusing buyers and diluting credible claims. The German Federal Office of Consumer Protection issued warnings against 17 brands for falsely claiming “plastic-free packaging” when internal components used synthetic films. This credibility gap not only penalises honest brands but also slows the adoption of truly circular innovations, as scepticism overrides intent.

Fragmented National Preferences Hinder Pan-European Product Standardisation

The deep fragmentation by national culinary traditions is leading to divergent product expectations that complicate unified design and inventory strategies, which is another factor inhibiting the growth of the European cookware market. French consumers prefer heavy enamelled cast iron for slow braising, while Italians favour lightweight copper or aluminium for precise sauce control. Germans demand induction compatibility and dishwasher safety, whereas Scandinavians prioritise minimalist design and stackability. According to the European Kitchenware Association, a single cookware brand must maintain at least six distinct product lines to meet core national preferences. This localisation increases R and D costs and limits economies of scale. For instance, a pan optimised for French gas stoves may not distribute heat evenly on German induction hobs, necessitating separate engineering.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.75% |

| Segments Covered | By Product Type, Material, End User, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Le Creuset, Tefal/T-fal, Mauviel, De Buyer, Fissler, WMF Group, Zwilling J.A. Henckels, Bialetti, Ballarini, Agnelli, Kuhn Rikon, BK Cookware, Samuel Groves, Stellar Cookware |

SEGMENTAL ANALYSIS

By Product Type Insights

The core cookware segment accounted in holding 63.4% of the European cookware market share in 2024. Core cookware items experience consistent wear from daily use, leading to predictable replacement cycles. In countries with high home cooking frequency, such as Italy and Spain, many adults prepare hot meals daily. Retailers like IKEA and Carrefour, core items represent 75% of cookware unit sales, driven by their status as essential kitchen staples. Unlike specialised,, these products serve multiple functions, making them non-discretionary even during economic downturns.

Stricter EU regulations on food contact materials are accelerating the replacement of older or non-compliant core cookware. The European Chemicals Agency’s 2023 enforcement of PFOA and PFOS bans rendered millions of legacy non-stick pans obsolete, prompting consumers to upgrade to ceramic or titanium reinforced alternatives. Germany’s Federal Institute for Risk Assessment documented an increase in consumer inquiries about coating safety in 20 24, directly correlating with higher sales of certified stainless steel and enamelled core sets. Brands like WMF and Tefal now embed QR codes linking to material safety data sheets satisfying EU transparency mandates. This regulatory push transforms routine replacements into quality upgrades,s, favouring certified durable core cookware over low-cost imports.

The specialised cookware segment is swiftly emerging at an anticipated CAGR of 9.7% throughout the forecast period. European consumers are increasingly experimenting with international recipes, leading to demand for culturally specific cookware. Retailers like John Lewis in the UK are seeing an increase in tagines and couscousiers, fueled by North African food popularity. As per the European Food Information Council, Europeans aged 18 to 35 cook at least one non-native cuisine weekly. Manufacturers respond with region-specific designs such as De Buyer’s Moroccan-style tagines or Scanpan’s induction-compatible woks. This culinary globalisation turns niche items into mainstream purchases as authenticity becomes a cooking aspiration. Platforms like Instagram, TikTok, and YouTube have transformed specialised cookware into aspirational tools showcased in viral cooking videos. A single recipe video featuring a Le Creuset oval roaster can generate thousands of units in sales across Europe within weeks, as reported by the European Digital Commerce Federation. Brands collaborate with food influencers for live demonstrations, such as Staub’s “Sunday Roast” series, driving direct conversions. This digital word of mouth accelerates adoption beyond traditional culinary boundaries.

By Material Insights

The stainless steel segment was the largest by accounting for 35.4% of the European cookware market share in 2024. Stainless steel is inherently inert, non-reactive, and free from chemical coatings, making it fully compliant with Regulation (EC) No 1935 2004 on materials intended to come into contact with food. In contrast, non-stick and aluminium cookware face increasing scrutiny with RAPEX alerts in 2024 involving coating or metal leaching issues. Hospitals, schools and public kitchens across Germany and the Nordic countries mandate stainless steel for this reason. Stainless steel is associated with professional kitchens and culinary excellence, particularly in France, Germany, and Scandinavia. Brands like Demeyere and Fissler leverage this perception, offering multi-ply constructions with aluminium cores for even heating while maintaining stainless exteriors.

The ceramic and glass cookware segment is expected to witness a CAGR of 11.2% throughout the forecast period. As the EU phases out per- and polyfluoroalkyl substances, consumers are turning to ceramic glazed and tempered glass cookware as inherently safe alternatives. Ceramic coatings contain no PFOA, PFO, S or PTFE and are derived from natural minerals, such as silicon dioxide. Brands like GreenPan and Berndes saw triple-digit growth in Germany and the Netherlands, where chemical sensitivity is a top purchase concern. Ceramic and glass cookware aligns with contemporary European preferences for minimalist and multifunctional kitchenware. Tempered glass lids and pastel-hued ceramic pots double as serving dishes, reducing the need for additional tableware. The Nordic Swan Ecolabel certifies several ceramic lines for low environmental impact duringproductionp pealinto sustainability-minded consumers. Retailers like Habitat and Muuto showcase ceramic cookware as lifestyle objects, not just tools. This fusion of function and form transforms ceramics from a niche alternative into a design-led growth engine.

By End User Insights

The residential segment was the largest by capturing 58.3% of the European cookware market share in 2024. Consumers value the ability to assess weight balance, handle ergonomic features, and finish in person before buying premium cookware. Speciality retailers like Le Creuset boutiques and De Buyer showrooms offer live demonstrations, allowing customers to experience heat distribution and sound factors impossible to convey online. In Germany and France, over 80% of high-end cookware is still sold offline. Kitchen speciality stores provide expert advice on material compatibility, ty stove, and care instructions for complex purchases. Staff at stores like Williams Sonoma Europe undergo certified training on metallurgy and heat dynamics, enabling personalised recommendations.

By Distribution Channel Insights

The online distribution segment is likely to grow at an anticipated CAGR of 14.3% throughout the forecast period. Digital native brands like Made In and Our Place leverage storytelling video tutorials and chef collaborations to build loyalty without physical stores. These brands use data analytics to personalise offers and predict reorder cycles for items like non-stick pans. Online platforms excel for routine or budget-conscious purchases where price comparison and delivery convenience outweigh tactile evaluation. During 202energy costsspikedd, as German consumers increasingly bought basic pots online to replace damaged items quickly. Subscription models for replacement sets and AI-powered “cookware fit” quizzes further enhance digital relevance. This accessibility ensures online channels capture volume and younger demographics even as offline retains a premium share.

REGIONAL ANALYSIS

Germany Cookware Market Analysis

Germany was the top performer of the European cookware market by holding 22.3% of share in 2024. The growth of the market in this country is driven by the consumer preference for precision-engineered, durable cookware that aligns with the national ethos of quality and functionality. Over 78% of households own at least one multi-ply stainless steel or forged aluminium set, as per GfK, with brands like WM, F Fissler and Silit commanding strong loyalty. The country’s strict adherence to LFGB food safety standards ensures that only rigorously tested materials gain market acceptance. Induction cooking penetration exceeds 85% requiring magnetic base compatibility, ty which German manufacturers natively support. Additionally, the rise of “Kochbox” meal kits has increased demand for versatile core cookware as consumers replicate professional recipes at home.

France Cookware Market Analysis

The French cookware market was ranked second by holding 19.8% of share in 2024. French consumers view cookware as an extension of gastronomic identity, with heritage brands like Le Creuset, Staub and De Buyer embedding regional cooking techniques into product design. The country’s “Appellatid'Origineine Contrôlée” mindset extends to kitchenware, with consumers favouring locally made pieces that support terroir-based cuisine. In 2024, the French Ministry of Culture included traditional cookware making in its intangible cultural heritage list, reinforcing national pride. Copper remains popular in professional and affluent homes despite its cost due to superior thermal responsiveness.

Italy Cookware Market

The Italian cookware market is likely to grow at an anticipated CAGR throughout the forecast period. Italian cookware preferences are shaped by regional cuisines that require precise temperature control fosautéau, pasta, and seafoodAluminiummum and cop p,e r core stainless steel dominate due to rapid heat conduction, essential for risotto and tomato sauces. Brands like Lagostina and Ballarini thrive by offering induction-compatible non-stick lines that meet modern needs while honouring tradition. Southern Italy shows strong demand for terracotta and ceramic for slow cooking, while the north prefers professional-grade stainless. Steeleel The “Made in Italy” label also boosts exports with Italian design recognised for elegance and function.

United Kingdom Cookware Market Analysis

The United Kingdom cookware market is likely to grow eventually during the forecast period. Post Brexit and cost of living pressures have increased home meal preparation, with 69% of UK adults cooking five or more times weekly. This shift revived interest in durable cookware after years of reliance on ready meals. British consumers favour multifunctional sets that save space in smaller urban kitchens. Brands like Tower and Salter gained share with affordable non-stick and stainless steel premium imports from Le Creuset cater to aspirational buyers. The “Great British Bake Off” effect also spurred demand for oven-safe dishes and roasters.

Spain Cookware Market Analysis

Spain's cookware market growth is likely to grow at the fastest CAGR in next coming years. Spanish households prioritise cookware for communal and traditional dishes such as paella, seafood stews and tapas. Family gatherings and outdoor cooking drive demand for large-diameter shallow pans and grill plates. In 2024, sales of induction-compatible paella pans grew by 31% as households upgrade stoves. Southern regions favour earthenware for slow cooking, while urban centres adopt stainless steel for versatility. Spanish brands like Magefesa and San Ignacio combine local craftsmanship with modern safety standards, gaining export traction.

COMPETITIVE LANDSCAPE

Competition in the European cookware market is defined by a three-tier structure comprising global premium brands, regional heritage manufacturers,, rs and low-cost importers. Premium players such as WF, Le Creuset, and Tefal dominate through material innovation, regulatory compliance and strong brand narratives rooted in national culinary identity. They compete on durability performance and trust rather than price, leveraging certifications from TÜV Bureau Veritas and EU food safety bodies to differentiate from commoditised alternatives. Mid-tier brands focus on functional value with induction-ready sets and modular designs targeting urban households with space constraints. Meanwhile, budget segments are flooded with Asian imports, often lacking proper compliance documentation, triggering RAPEX alerts and consumer awareness. The rise of direct-to-consumer models challenges traditional retail with immersive digital storytelling, while offline speciality stores retain influence through tactile experience and expert advice. Increasingly, competition hinges on the ability to balance heritage authenticity with modern demands for safe, sssustainabconvenient highlya ghly fragmented yet culturally rich market.

KEY MARKET PLAYERS

Some of the notable key players in the European cookware market are

- Le Creuset

- Tefal / T-fal

- Mauviel

- De Buyer

- Fissler

- WMF Group

- Zwilling J.A. Henckels

- Bialetti

- Ballarini

- Agnelli

- Kuhn Rikon

- BK Cookware

- Samuel Groves

- Stellar Cookware

Top Players in the Market

- WMF Group is a German premium cookware manufacturer renowned for its high-quality stainless steel and pressure cookers sold across Europe and globally. The company contributes to international standards in food safety and material innovation through its participation in European Committee for Standardisation working groups. WMF operates production facilities in Germany and Portugal, ensuring compliance with EU food contact regulations while maintaining craftsmanship. In 20,24, the company launched its “Cuisine Pro” line featuring induction optimised tri-ply construction with fully encapsulated aluminium cores and ergonomic stay cool handles. It also enhanced its sustainability profile by introducing packaging made from 100% recycled paper certified by the Forest Stewardship Council. These initiatives reinforce WMF’s reputation for technical excellence and regulatory alignment in premium kitchenware.

- Le Creuset is a French iconic brand specialising in enamelled cast iron cookware with a strong presence in Europe and worldwide distribution across 60 countries. The company is globally recognised for its artisanal casting process and vibrant colour palettes that blend functionality with design. Le Creuset supports circular economy principles through its lifetime warranty and repair program, which replaced over 120000 defective pieces across Europe. The brand also deepened its digital engagement by launching interactive cooking masterclasses in partnership with Michelin chefs, streamed to customers in 15 European markets. In Le Creuset introduced a new line of stoneware featuring lead-free glazes compliant with the latest EU ceramic safety directives, further strengthening its position as a trusted heritage brand committed to modern safety and sustainability standards.

- Tefa, a flagship brand of France-based GroupeSEB, is a leading innovator in non-stick and everyday cookware with extensive reach across European households and global markets. The company plays a pivotal role in advancing safer coating technologies, having phased out all PFOA and PFOS from its products since 2020, ahead of EU regulatory deadlines. Tefal introduced its “Ingenio” modular system featuring detachable handles for space-saving storage and oven compatibility certified under EN 12983 standards. It also expanded its eco-conscious “Initio” range made with 100% recycled aluminium and ceramic non-stick coatings validated by Bureau Veritas. Through partnerships with retailers' e-commerce platforms, Tefal continues to drive accessibility while embedding EUU food safety and environmental compliance into mainstream cookware design.

Top Strategies Used by the Key Market Players

Key players in the European cookware market emphasise material safety and regulatory compliance by proactively eliminating PFAS and adopting EU-certified non-stick alternatives such as ceramic and titanium reinforced coatings. They invest in premiumization through multi-ply construction, induction compatibility, and ergonomic design to justify higher price points and foster brand loyalty. Companies leverage heritage storytelling and culinary partnerships to reinforce authenticity, ty particularly in France, Italy, and Germany, where cooking tradition influences purchasing. Direct-to-consumer channels are expanded via immersive digital content, including recipe videos and live chef ddemdemonstrationsdrive engagement and reduce reliance on third-party retailers. Sustainability is integrated through lifetime guarantees, recycled materi ndandlplastic-freeeee packagng,, aligning with EU Ecodesign and circular economy mandates. Offline retail remains vital through speciality boutiques offering tactile experiences and expert guidance, especially for high involvement purchases. These strategies collectively address Europe’s unique blend of safetconsciousnessses,, cultural identity and environmental responsibility.

MARKET SEGMENTATION

This research report on the European cookware market has been segmented and sub-segmented based on categories.

By Product Type

- Core Cookware

- Specialized Cookware

- Accessories

By Material

- Stainless Steel

- Aluminium

- Cast Iron

- Carbon Steel

- Copper

- Ceramic/Glass

- Silicone

- Other Coated Substrates

By End User

- Residential

- Commercial

By Distribution Channel

- Offline Retail

- Online

- B2B / Direct Sales

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe cookware market?

Growth is driven by increasing home cooking trends, rising disposable incomes, premiumization of kitchenware, and strong demand for durable and non-toxic cookware materials.

2. Which countries dominate the cookware market in Europe?

Germany, France, the United Kingdom, and Italy are the leading markets due to strong culinary culture, high consumer spending on kitchenware, and the presence of premium brands.

3. What types of cookware are commonly used in Europe?

Common product types include core cookware (pots, pans, skillets), specialized cookware (woks, roasters, grills), and accessories such as lids and handles.

4. Which materials are most popular in the Europe cookware market?

Stainless steel, aluminium, cast iron, carbon steel, copper, ceramic/glass, silicone, and coated substrates are widely used across households and commercial kitchens.

5. What is the biggest end-user segment in the Europe cookware market?

Residential users make up the largest segment, supported by lifestyle trends such as home cooking, baking, and kitchen upgrades.

6. How is the commercial sector influencing cookware demand?

Hotels, restaurants, and catering services drive demand for durable, heat-resistant, and professional-grade cookware.

7. What distribution channels are most common for cookware sales in Europe?

Cookware is sold through offline retail stores, online marketplaces, and B2B/direct sales channels for commercial buyers.

8. What impact has premium cookware had on the European market?

Demand for high-end cookware brands has increased as consumers seek long-lasting products with superior performance and safety features.

9. Which cookware segment is experiencing the fastest growth?

Specialized cookware and non-stick coated products are growing quickly due to rising interest in diverse cooking styles and convenience.

10. What is the future outlook for the Europe cookware market?

The market is expected to grow steadily, driven by innovation in materials, expansion of e-commerce, and increasing consumer preference for premium and sustainable cookware.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com