Europe Farm Management Software Market Size, Share, Trends & Growth Forecast Report By Function, Deployment, End User, and By Country (Germany, France, Netherlands, United Kingdom, Spain, Rest of Europe) – Industry Analysis and Forecast, 2025 to 2033

Europe Farm Management Software Market Summary

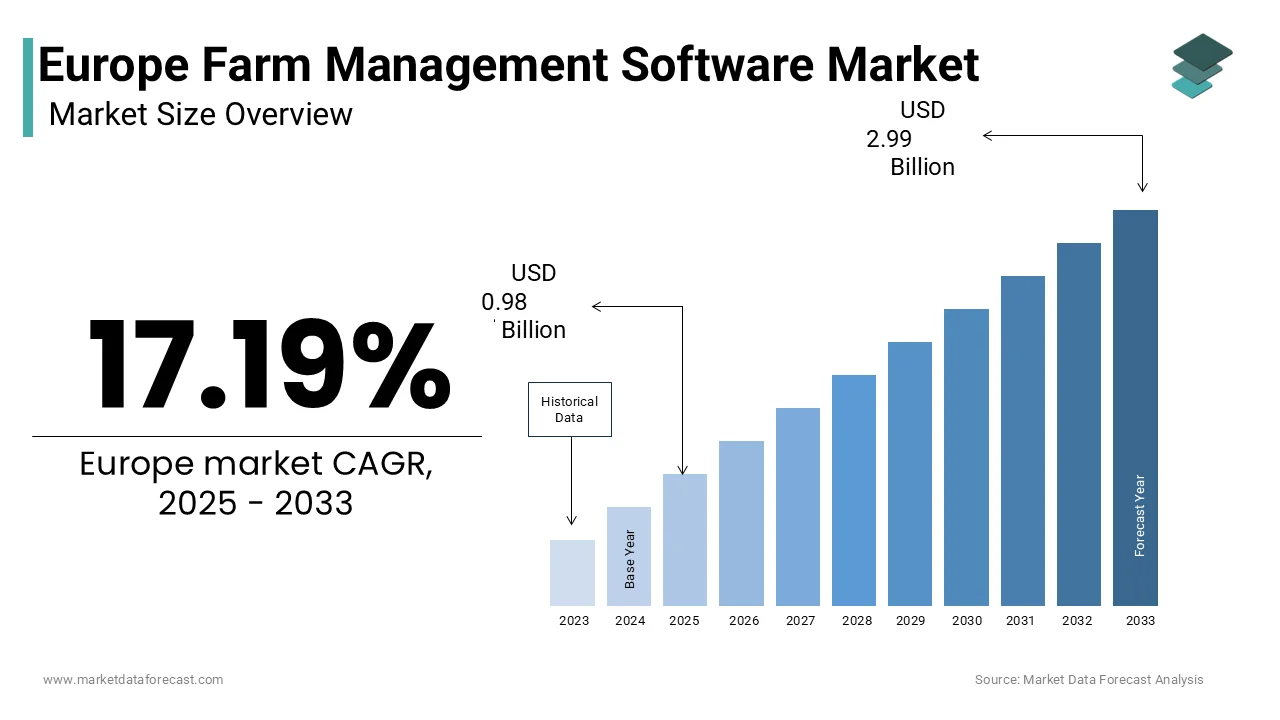

The Europe farm management software market was valued at USD 0.84 billion in 2024, is estimated to reach USD 0.98 billion in 2025, and is projected to grow at a CAGR of 17.19% from 2025 to 2033, reaching USD 2.99 billion by 2033, driven by EU CAP digital compliance mandates, precision agriculture adoption, and Green Deal–aligned sustainability reporting.

Market Snapshot

- 2024 Market Size: USD 0.84 billion

- 2025 Estimate: USD 0.98 billion

- 2033 Forecast: USD 2.99 billion

- CAGR (2025–2033): 17.19%

Quick Growth Drivers

- Mandatory digital record-keeping under EU CAP eco-schemes

- Rapid uptake of precision farming tools (GPS, VRA, soil sensors)

- Expansion of organic farming under Farm to Fork targets

- EU-backed agricultural data spaces and digital subsidy portals

- Rising demand for traceability and environmental compliance

Principal Restraints

- Fragmented data standards (limited ISOBUS compliance)

- Proprietary machinery ecosystems restricting interoperability

- Low digital literacy among aging farmers

- Inconsistent rural broadband and mobile connectivity

High-Value Opportunities

- Compliance-integrated platforms aligned with EU Green Deal rules

- Digital tools for carbon farming, soil health, and nutrient tracking

- Growth of farmer-owned data cooperatives

- SaaS solutions enabling ESG and supply-chain traceability

- AI-driven predictive agronomy and advisory services

Key Market Challenges

- Rising cybersecurity risks in cloud-based farm systems

- Lack of mandatory security standards for agri-software

- Exposure to data breaches during critical crop cycles

- Persistent digital divide between large farms and smallholders

Fastest-Growing Segments

- Remote Crop & Soil Monitoring: 16.9% CAGR — satellites, drones, AI

- Cloud & SaaS Deployment: 15.2% CAGR — low cost, scalability

- Agribusiness End Users: 18.4% CAGR — traceability & ESG needs

Regional Leadership & Dynamics

- Germany (20.1%) — strict nutrient rules, strong software–subsidy integration

- France (17.2%) — centralized digital agriculture platforms

- Netherlands — high-intensity precision farming, IoT leadership

- United Kingdom — outcome-based subsidies driving digital proof

- Spain — water stress accelerating irrigation and compliance software

What Wins Commercially

- Deep integration with CAP and national subsidy systems

- Mobile-first, offline-capable interfaces for rural users

- Open APIs for machinery and data interoperability

- Built-in carbon, soil, and biodiversity accounting

- Strong data security and ownership controls

Top Strategic Ask for Executives

- Embed regulatory logic directly into farm workflows

- Prioritize interoperability and open data standards

- Invest in AI-driven compliance and predictive agronomy

- Design for low-connectivity and low-literacy environments

- Partner with cooperatives and agribusinesses for scale

Leading Players

Some of the companies that are playing a dominating role in the Europe farm management software market include

John Deere, Trimble, AGCO, CNH Industrial, SAP, Microsoft, IBM, Bayer (Climate Corporation), Topcon, Agrivi, Agworld, 365FarmNet, Agroptima, Farmflo

Europe Farm Management Software Market Size

The europe farm management software market was valued at USD 0.84 billion in 2024, is expected to reach USD 0.98 billion in 2025, and is projected to grow at a CAGR of 17.19% from 2025 to 2033 and reach USD 2.99 billion by 2033.

Farm management software refers to digital platforms that integrate data from field operations, machinery, weather, er satellites, and regulatory databases to optimize agricultural decision making across crop planning, input application, labor scheduling,g and compliance reporting. Unlike generic enterprise tools,s these solutions are purpose-built for the agronomic and policy environment of the European Union, where sustainability metrics and traceability are as critical as yield. According to sources, the number of agricultural holdings across the EU has been steadily declining, while the average farm size has consequently increased over time. The European Commission's Digital Europe Programme is actively funding initiatives to develop a common European agricultural data space, fostering secure data exchange and supporting data-driven innovation within the sector. Furthermore, the EU's Farm to Fork Strategy includes ambitious targets for significantly expanding organic farming across Europe. The strategy also encourages greater transparency and improved data management, including for environmental metrics like pesticide use and nutrient balances, with efforts underway to implement digital record-keeping systems for these purposes. These regulatory and structural conditions position farm management software not as a luxury but as an essential utility for European farmers navigating ecological transition and market complexity.

MARKET DRIVERS

Mandatory Digital Record Keeping Under EU Agri-Environmental Schemes Is Driving Adoption

The Common Agricultural Policy’s conditionality requirements now compel farmers to maintain detailed digital records of fertilizer application, crop rotations, ns and pesticide usage to qualify for subsidies, which in turn drives the growth of tEuropeanope farm management software market. The European Union's Common Agricultural Policy (CAP) increasingly ties significant portions of direct aid to environmental and climate objectives, such as eco-schemes and sustainable nutrient management, requiring robust compliance and reporting from farmers. In Germany, there is a growing adoption of certified digital farm management software among farmers to efficiently manage and automate environmental reporting requirements, such as those related to fertilizer usage regulations (Düngeverordnung). France has developed an advanced platform, such as the "MesParcelles" system, which integrates with various commercial software providers to streamline the digital submission of farm data and simplify the administrative process for receiving national CAP payments. The digitalization of farm compliance procedures, utilizing software, is significantly reducing the administrative burden and time commitment for farmers compared to traditional manual record-keeping methods, as highlighted in various analyses and reports on agricultural efficiency. This administrative burden reduction, combined with audit accuracy, ensures that adoption is no longer optional but a prerequisite for financial viability in the EU subsidy ecosystem.

Integration of Precision Agriculture Technologies Is Enabling Data-Driven Input Optimization

European farmers are increasingly deploying GPS-guided machinery, variable rate applicators, and soil moisture sensors that generate terabytes of operational data requiring centralized software for interpretation and action. This further boosts the expansion of theEuropeane farm management software market. The adoption of technology allowing seamless data exchange between implements and farm management platforms is becoming commonplace in new tractors across the European Union. Farmers in the Netherlands operate within a stringent regulatory environment concerning nitrogen application, increasingly using farm management software to precisely model and adjust nutrient inputs to meet strict environmental standards. Research from leading agricultural institutions demonstrates that farms utilizing integrated software solutions can significantly reduce nitrogen over-application while sustainably maintaining or improving crop yields. The use of software-controlled drip irrigation systems in Spain is expanding widely across significant agricultural areas, leading to substantial improvements in water conservation for crops such as almonds and olives. This convergence of hardware connectivity, regulatory limits,s and agronomic intelligence transforms software from record-keepingng tool into a core productivity engine.

MARKET RESTRAINTS

Fragmented Data Standards Hinder Interoperability Across Platforms and Machinery

A lack of universal data protocol is causing significant inefficiencies in data exchange between software providers, equipment brands, and government systems, despite technological advances, which hampers the growth of the European farm management software market. A large majority of commercial farm software in the European Union does not fully comply with the ISO 11783 ISOBUS standard for machinery integration, which commonly results in significant manual data re-entry and an increased risk of errors in farm management. Moreover, a substantial majority of farmers utilizing multiple digital tools have reported experiencing widespread compatibility problems when attempting to transfer essential data, such as field boundaries or yield information, between different technology platforms. This fragmentation is exacerbated by proprietary formats from major machinery manufacturers such as John Deere’s Operations Center and Claas’ Telematics, which restrictthird-partyy access without paid middleware. Consequently, it is revealed that a notable share of users operate two or more software systems simultaneously, increasing training costs and reducing decision coherence. Interoperability will continue to be a significant challenge until the EU mandates open architecture via initiatives such as the Common European Agricultural Data Space (CEADS).

Limited Digital Literacy Among Aging Farming Populations Constricts Effective Utilization

The demographic profile of the region’s farming community poses a persistent barrier to software adoption, with digital fluency lagging behind technological availability, and thereby hinders the expansion of tEuropeanope farm management software market. Data from previous years indicates that the average age of farm holders across the EU tends to be older, with a majority of holders being over the age of 55. This demographic typically utilizes smartphones and cloud services less frequently than the general population. Reports from EU rural networks suggest that older farmers generally express less confidence in utilizing advanced digital farming software features, such as those related to variable rate application or satellite data analysis, compared to younger farmers. Within Southern and Eastern European regions that have less developed digital infrastructure, broadband coverage in agricultural areas is often insufficient in several member states, including Greece, Romania, and Bulgaria, which generally hinders real-time connectivity for farming operations. Even when software is adopted, ed usage often remains superficial, restricted to basic record keeping rather than predictive analytics. The potential of digital agronomy in Europe will remain untapped without targeted reskilling, simplified interfaces, and localized support.

MARKET OPPORTUNITIES

EU Green Deal Policy Alignment Creates Demand for Compliance Integrated Platforms

The European Green Deal’s legislative cascade, including the Sustainable Use of Pesticides Regulation nutrient action plans and carbon farming initiatives, generates potential opportunities for tEuropeanope farm management software market. This software embeds regulatory logic directly into operational workflows. Large-scale agricultural operations are transitioning toward mandatory digital record-keeping for the application of crop protection products. These digital logs are expanding to include precise environmental variables, such as localized weather data and the designation of protected buffer zones. Agricultural technology providers are integrating regulatory databases and automated mapping features into their software to assist with compliance verification. New legislative frameworks are shifting focus toward the systematic monitoring of soil health indicators, such as organic matter content. The industry is increasingly utilizing satellite-based observation tools, confirmed by physical sampling, to automate the tracking of soil and vegetation metrics. The adoption of these digital management systems is expected to decrease the frequency of administrative errors and subsequent financial penalties for producers. This policy-driven software necessity transforms vendors from service providers into compliance partners, enabling them to capture value through regulatory assurance rather than just productivity gains.

Expansion of Agricultural Data Cooperatives Is Unlocking Collective Intelligence

A nascent but accelerating trend in the region involvesfarmer-ownedd data cooperatives that pool anonymized field data to generate regional agronomic insights while retaining ownership rights, which provide fresh prospects for the European farm management software market. Agricultural regulations are increasingly mandating digital record-keeping for land management activities, specifically concerning the application of plant protection products and environmental conditions during use. Technology providers are integrating regulatory databases and automated mapping features into their management platforms to help operators align with legal standards. Proposed environmental legislation suggests a transition toward systematic monitoring of soil quality indicators, such as organic matter content. Software solutions are evolving to analyze remote sensing data alongside physical soil samples to provide more consistent oversight of land health. The shift toward digital compliance frameworks is expected to lower the frequency of administrative errors and subsequent financial assessments for agricultural enterprises. This collective intelligence approach not only enhances individual farm resilience but also creates scalable data assets that inform public policy and supply chain transparency, making farm management software a conduit for community-based agronomic innovation rather than isolated optimization.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Cloud-Based Agricultural Systems Raise Operational Risks

The transition of farm management to cloud infrastructure and the integration of IoT devices broadens the attack surface for cyber threats, heightening concerns regarding the integrity of data and maintaining operational continuity. This negatively impacts the growth of the European farm management software market. Reported instances of malicious digital events impacting agricultural technology systems have seen a significant increase. The frequency of unauthorized access and data copying incidents within the sector has more than doubled over two years. A recent compromise of a widely used agricultural data management platform has shown that operational data, including planting schedules and supply chain information, can be exposed. Such incidents have demonstrably affected the critical initial stages of the growing season for numerous farming operations across a broad region. Unlike financial or healthcare systems, farm software often lacks mandatory cybersecurity certification and operates on legacy protocols with weak authentication. The European Commission’s Cyber Resilience Act will soon require digital products to meet baseline security standards,s but transition timelines leave current systems exposed. Farmers, rs particularly those using integrated machinery control,rol are vulnerable to spoofed guidance signals or manipulated variable rate prescriptions that could cause crop damage or regulatory non-compliance. Systemic disruption threatens EU agriculture's digital transformation as long as security isn't built in from the start.

Uneven Access to High-Speed Connectivity Limits Real-Time Functionality in Rural Areas

The reality of rural connectivity continues to impede the full functionality of cloud-dependent farm management software, despite EU ambitions for universal broadband. These further challenge the expansion of the European farm management software market. Rural regions exhibit a noticeable discrepancy in access to high-capacity fixed broadband compared to more developed areas. High-speed connectivity levels appear significantly lower in specific territories characterized by intensive agricultural activity. Mobile network availability on cultivated land remains inconsistent, which may impact the reliability of digital tools. Infrastructure limitations can lead to periodic interruptions in the synchronization of data from field-based equipment. Agricultural operations that depend on constant cloud access face potential operational challenges due to service instability. Connectivity gaps in remote terrain are observed to delay the transmission of automated alerts and monitoring data. The EU's Digital Europe Programme has not significantly boosted satellite internet adoption among remote farms; cost and latency barriers continue to hinder widespread use, even with available subsidies. This digital divide forces farmers to rely on offline modes that lack predictive analytics or regulatory updates, thereby fragmenting the market between connected commercial farms and digitally isolated smallholders.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Function, Deployment, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | John Deere (Deere & Company), Trimble Inc., AGCO Corporation, CNH Industrial N.V., SAP SE, Microsoft Corporation, IBM Corporation, Granular, Inc. (a Microsoft subsidiary), Raven Industries, Inc. (CNH Industrial), Climate Corporation (Bayer AG), FarmLogs (Envestnet | Yodlee), AgriWebb, AgJunction Inc., Topcon Positioning Systems, Inc., DottyVibes SAS, Agrivi d.o.o., FarmWizard Ltd., CropIn Technology Solutions Pvt. Ltd., TE-FOOD (blockchain farm management solutions), Agworld Inc. |

SEGMENTAL ANALYSIS

By Function Insights

The precision farming segment was the largest in the European farm management software market by capturing a 38.6% share in 2024. The supremacy of the precision farming segment is driven by the need to optimize input use under tightening environmental regulations. The European Commission’s Farm to Fork Strategy caps synthetic nitrogen application across the EU and mandates integrated pest management, compelling farmers to adopt variable rate technology guided by software analytics. A significant majority of cultivated land within the region now employs machinery guided by satellite positioning systems. These advanced systems frequently utilize detailed application maps that are generated by common data management platforms. In one specific country, agricultural operations employing precision technology modules have shown a measurable decrease in the amount of a particular fertilizer applied beyond optimal levels. In another nation, regulations require detailed logs of crop protection chemical use, a requirement that is streamlined through the use of precision software that factors in specific field characteristics and localized weather conditions. This convergence of regulatory compliance, agronomic efficiency,y and machinery interoperability ensures precision farming remains the core functional pillar of digital agriculture in Europe.

The remote crop and soil monitoring segment is estimated to register the fastest CAGR of 16.9% from 2025 to 2033 due to the integration of satellite imagery,ery drone analytics, and AI-driven anomaly detection into routine agronomic workflows. A significant number of farms across Europe are utilizing satellite data to monitor vegetation indices at a high resolution with frequent updates. The application of remote sensing in areas facing water scarcity enables more efficient irrigation scheduling over a substantial area of specific permanent crops. There is a trend toward integrating ground-based moisture sensors with cloud-based data management systems, which has been observed to mitigate the negative impacts of heatwaves and drought on crop yields. Additionally, the EU’s Carbon Farming Initiative will soon require baseline soil organic carbon measurements, data that remote monitoring platforms can now estimate using hyperspectral algorithms validated by the Joint Research Centre. This ability to deliver real-time ecological intelligence without field visits positions remote monitoring as the vanguard of scalable, sustainable agronomy.

By Deployment Insights

The cloud and SaaS segment held the majority share of the European farm management software market in 2024. The leading position of the cloud and SaaS segment is attributed to its low upfront cost, automatic updates,s and seamless integration with mobile and machinery ecosystems. New software adoptions show a strong preference for subscription models. This trend is linked to compatibility with smartphone-based field scouting and real-time data synchronization from IoT sensors. Cloud platforms are particularly important for farms lacking IT infrastructure for on-premises systems, allowing access without managing local servers. In one European region, most farms using digital tools rely on cloud platforms that connect directly to subsidy portals and cooperatives. Upcoming cybersecurity regulations favor centralized cloud architectures over fragmented local servers. This combination of accessibility, regulatory alignment, and ecosystem connectivity makes SaaS the default deployment model for Europe’s digital agrarian transition.

The Cloud & SaaS segment is also anticipated to witness the fastest CAGR of 15.2% during the forecast period as it evolves beyond basic record keeping into predictive and prescriptive analytics powered by artificial intelligence. A substantial financial investment has been directed towards the development of cloud-native models designed to forecast pest outbreaks, optimize harvest timing, and simulate carbon sequestration scenarios. A nationwide initiative successfully migrated a significant number of farms to a unified software platform, facilitating real-time environmental balance validation against national thresholds. A national geodatabase now offers open APIs, which allow commercial software vendors to automatically populate field boundaries and crop codes, significantly streamlining their onboarding processes. The European Data Act’s provisions on data portability further strengthen SaaS appeal by ensuring farmers can switch providers without losing historical records. Cloud platforms, leveraging improved connectivity from rural 5G and satellite internet, are increasingly delivering edge computing capabilities, for example, processing drone images on mobile devices, to blend immediacy with central intelligence. This trajectory transforms SaaS from a cost-efficient alternative into the central nervous system of future farming.

By End User insights

The farmers segment led the European farm management software market by accounting for a significant share in 2024, as digital tools become essential for day-to-day operational and compliance tasks. Across various regions, there has been a noticeable increase in the use of digital submission methods for agricultural program records. Software solutions are automating key administrative tasks within agricultural management, including the mapping of fields, logging of input data, and documentation for environmental programs. A significant pattern is the widespread adoption of specialized software for real-time nutrient management planning on larger farming operations. The use of integrated applications has become a prevalent practice for managing and tracking specific livestock-related metrics to ensure adherence to regional guidelines. The rise of smartphone penetration further enables direct adoption without intermediaries. This grassroots reliance on software for both productivity and regulatory survival ensures farmers remain the primary end user segment.

The agribusiness companies segment is likely to experience the fastest CAGR of 18.4% from 2025 to 2033, owing to its need to ensure supply chain traceability,y sustainability compliance,ce and input efficiency across contracted grower networks. Agricultural sourcing strategies are increasingly defined by the necessity to verify the environmental origins of raw materials to ensure regulatory compliance. The integration of digital tracking and geolocation tools is becoming a standard requirement for documenting the land-use history of commodities. Collaborative data-sharing platforms are facilitating the exchange of agronomic information between growers and buyers to support value-added market claims. Farm management software is being utilized to monitor production practices, such as livestock health interventions and land management, to meet evolving retail expectations. Agribusinesses are increasingly embedding lifecycle assessment capabilities into their procurement processes to prepare for broader transparency mandates across the food supply chain. This shift transforms farm software fromfarmer-centricric tool into a B2B compliance and value creation infrastructure linking field to fork.

COUNTRY LEVEL ANALYSIS

Germany Farm Management Software Market Analysis

Germany dominated the European farm management software market and captured a 20.1% share in 2024. The dominance of the German market is driven by its dense network of medium-scale arable and livestock farms operating under some of the EU’s strictest environmental regulations. A significant majority of agricultural holdings fall within a specific operational size that correlates strongly with the use of digital solutions for managing nutrients and manure effectively. Initiatives designed to integrate software with farming machinery and subsidy systems have been widely funded, resulting in the development and use of large-scale, accessible platforms by a considerable number of farms. A prevalent pattern has emerged where farms receiving certain environmental payments utilize certified software to automatically produce reports required for regulatory compliance, suggesting a streamlined reporting process. Furthermore, Germany hosts major software developers like 365FarmNet and AgriCon, as well as R and D centers for global players such as John Deere,e ensuring continuous innovation aligned with national agronomic priorities.

France Farm Management Software Market Analysis

France was the next prominent player in the European farm management software market by holding a 17.2% share in 2024. The growth of the French market is propelled by its centralized digital agriculture strategy and strong integration between public infrastructure and private software. A national geospatial system provides a core infrastructure that facilitates the movement of information between agricultural software used commercially and the support payment application process. A substantial majority of farms requesting certain support payments submit their necessary documentation through authorized digital systems. Efforts to reduce pesticide use have encouraged the uptake of platforms that offer functions like real-time spray logs and mapping of protective buffer zones. Across various agricultural technical sites, a network of demonstration farms highlights how different software systems and machinery from various manufacturers can work together effectively. This public-private synergy creates a uniquely cohesive digital ecosystem that accelerates scalable adoption beyond early adopters.

Netherlands Farm Management Software Market Analysis

The Netherlands is another key player in the European farm management software market due to its intensive horticulture and dairy sectors that demand high precision in resource management. A significant majority of farms across the country incorporate digital tools to manage resource optimization, including water, nutrients, and energy. Operations within controlled environments consistently show leadership in the extensive integration of the Internet of Things technology. A widespread program facilitates dairy farms in evaluating their nitrogen efficiency by using shared software dashboards. A vast majority of pig and poultry operations demonstrate compliance with environmental standards, using dedicated software applications to automatically manage metrics related to manure storage and appropriate land application timing. Moreover, the Netherlands hosts Wageningen University’s Digital Farming Lab, which collaborates with startups like FarmMobile to develop AI models for disease prediction in potato and tulip crops. This fusion of regulatory pressure,re-cooperative structures, and agritech innovation positions the Netherlands as a high-intensity digital farming leader.

United Kingdom Farm Management Software Market Analysis

The United Kingdom grew steadily in the European farm management software market owing to its post Brexit agricultural policy shift toward public money for public goods under the Environmental Land Management scheme. According to sources, thousands of English farms enrolled in the Sustainable Farming Incentive must submit digital records of soil health, hedgerow management,t and integrated pest control to receive payments. This has driven rapid adoption of platforms which auto generate compliance evidence from field activities. The UK’s Agricultural Technology Strategy has also funded the Farm Data Standards initiative to ensure interoperability between software providers and government portals. Despite leaving the EU, the UKoutcome-basedsed subsidy model creates a unique demand for software as a verification layer between ecological action and public funding.

Spain Farm Management Software Market Analysis

Spain is anticipated to expand in the European farm management software market from 2025 to 2033 due to water stress and the need for efficient irrigation across its millions of hectares of arable land. Large-scale agricultural territories are increasingly characterized by persistent water availability challenges, necessitating more formal oversight of resource extraction. Administrative frameworks have evolved to require digital authorization for water usage alongside the maintenance of detailed consumption logs. Technological solutions now facilitate the automated transmission of data from irrigation infrastructure to regional water management authorities. Regulatory shifts have linked the adoption of digital record-keeping practices to eligibility for environmental and economic support programs. Additionally, Spain’s fruit and vegetable cooperatives require digital traceability for pesticide residues and harvest dates to meet EU and UK retailer standards. This confluence of environmental constraint, export compliance, and policy enforcement is rapidly digitizing Spain’s diverse agricultural landscape.

COMPETITIVE LANDSCAPE

Competition in the European farm management software market is shaped by the dual imperatives of regulatory compliance and agronomic utility in a landscape of small to medium farms operating under increasingly stringent environmental rules. Unlike other regions where yield optimization dominates the value proposition, European vendors must first solve the problem of digital proof for subsidies,s eco schemes, and input limits. This has fostered a bifurcated competitive field; a handful of pan-European platforms with deep policy integration coexist with dozens of localized solutions tailored to national laws, language, and crop systems. Interoperability remains a key battleground as the EU pushes for a Common Agricultural Data Space, while cybersecurity, data ownership,p and usability for older farmers constrain adoption. Competition is less about features and more aboutrueet accuracy, and seamless linkage to public and private gatekeepers of income and market access,s making the European market uniquely complex and policy-driven.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe farm management software market include

- John Deere (Deere & Company)

- Trimble Inc.

- AGCO Corporation

- CNH Industrial N.V.

- SAP SE

- Microsoft Corporation

- IBM Corporation

- Granular, Inc. (a Microsoft subsidiary)

- Raven Industries, Inc. (CNH Industrial)

- Climate Corporation (Bayer AG)

- FarmLogs (Envestnet | Yodlee)

- AgriWebb

- AgJunction Inc.

- Topcon Positioning Systems, Inc.

- DottyVibes SAS

- Agrivi d.o.o.

- FarmWizard Ltd.

- CropIn Technology Solutions Pvt. Ltd.

- TE-FOOD (blockchain farm management solutions)

- Agworld Inc.

TOP LEADING PLAYERS IN THE MARKET

- 365FarmNet is a leading European farm management software provider headquartered in Germany with deep integration into the continent’s regulatory and machinery ecosystems. The platform enables farmers to manage field records, machinery data, and compliance documentation in a single interface aligned with EU Common Agricultural Policy requirements. It supports seamless data exchange with major tractor and implement brands through ISOBUS and partners with national authorities in Germany,ny Fr, aFrance and Austria for direct subsidy reporting. This policy-aligned functionality and open interoperability have positioned 365FarmNet as a benchmark for public-private digital agriculture collaboration across Europe and a reference model for global compliance-driven farm software design.

- Agroptima is a Spain-based farm management software company specializing in mobile-first solutions for permanent crop and smallholder farmers across Southern Europe. Its platform combines offline-capable field logging, GPS mapping,g and real-time compliance tracking, tailored to water and pesticide regulations in drought-prone regions. Agroptima’s strength lies in the intuitive smartphone interface that requires minimal training, making it accessible to aging and digitally inexperienced farm holders. It also partnered with cooperatives like Almendras de Andalucía to embed traceability workflows from harvest to export. Agroptima's success in achieving scale across fragmented agricultural landscapes highlights the importance of localized software design, demonstrating how prioritizing usability, regulatory relevance, and regional customization can inform strategies for other emerging markets globally.

- Farmflo is a UK-headquartered agri software platform known for its modular architecture that serves both arable livestock and livestock farms with a strong emphasis on post Brexit Environmental Land Management compliance. The company’s platform automates evidence collection for the UK’s Sustainable Farming Incentive, including soil health,h hedgerow management, and integrated pest control logs. Farmflo also offers APIs for agribusinesses,s enabling grain buyers, rs dairy processors, and input suppliers to access verified sustainability data from contracted growers. Its dual focus on public policy alignment and B2B data sharing reflects an ext-generation model where farm software acts as both a compliance utility and a value creation channel, influencing global trends in outcome-based agricultural payments and supply chain transparency.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe farm management software market pursue strategies centered on deep integration with national subsidy and environmental compliance systems development of mobile first offline capable interfaces for rural users partnerships with machinery manufacturers for seamless data exchange creation of carbon and biodiversity accounting modules aligned with EU Green Deal policies and collaboration with cooperatives agribusinesses and retailers to embed farm data into supply chain traceability frameworks.

MARKET SEGMENTATION

This research report on the europe farm management software market is segmented and sub-segmented into the following categories.

By Function

- Precision Farming

- Remote Crop & Soil Monitoring

- Farm Planning & Management

- Livestock Monitoring

- Others

By Deployment

- Cloud & SaaS

- On-Premise

By End User

- Farmers

- Agribusiness Companies

- Cooperatives

- Others

By Country

- Germany

- France

- Netherlands

- United Kingdom

- Spain

- Rest of Europe

Frequently Asked Questions

1. What are the key segments in the Europe Farm Management Software Market?

Key segments include precision farming, livestock management, aquaculture, and smart greenhouses, with precision holding the largest share at 49.78%. Deployment splits into cloud-based (dominant), on-premise, and hybrid; solutions cover software, consulting, and managed services for farms of all sizes.

2. What drives growth in the Europe Farm Management Software Market?

Growth drivers include precision agriculture, sustainable practices, and EU CAP incentives for digital tools like GPS tractors and AI analytics. Cloud scalability and IoT for real-time data reduce costs and boost yields, with livestock management seeing high demand.

3. What is precision farming in the Europe Farm Management Software Market?

Precision farming, the top segment (49.78% share), uses software for site-specific crop management via drones, satellite imagery, and automated irrigation in the Europe Farm Management Software Market, enhancing yields and sustainability across medium-large farms.

4. How does cloud-based software impact the Europe Farm Management Software Market?

Cloud-based dominates due to affordability, scalability, and mobile access for real-time farm data in the Europe Farm Management Software Market. It supports integration for supply chain and accounting, aiding small farms under EU digital subsidies.

5. What role does livestock management play in the Europe Farm Management Software Market?

Livestock management leads applications, offering monitoring, health tracking, and efficiency tools in the Europe Farm Management Software Market. It drives growth via broad uses in dairy and meat sectors, aligning with EU eco-friendly policies.

6. What are market trends in the Europe Farm Management Software Market?

Trends feature AI, IoT, and data analytics for sustainable farming, with 15.5% CAGR to 2031. Focus on managed services and hybrid models supports regulatory compliance and resource optimization in precision and greenhouse apps.

7. Who are the top players in the Europe Farm Management Software Market?

Top players provide precision and livestock solutions, though specifics vary; market leaders innovate in cloud agritech amid 17.6% growth. Competition centers on EU-compliant features for farmers and enterprises.

8. What challenges exist in the Europe Farm Management Software Market?

Challenges include high costs for small farms, data privacy under GDPR, and skill gaps, yet offset by subsidies in the Europe Farm Management Software Market promoting adoption for sustainability.

9. How does the EU CAP affect the Europe Farm Management Software Market?

EU CAP mandates digital records and funds precision pilots (€700M), boosting the Europe Farm Management Software Market via subsidies for software in crop rotation and pest management.

10. How to choose farm management software in Europe?

Select based on farm size, cloud vs. on-premise, and features like precision analytics in the Europe Farm Management Software Market; prioritize EU-compliant scalability for growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com