Europe Fish Oil Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Application, Species And By Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

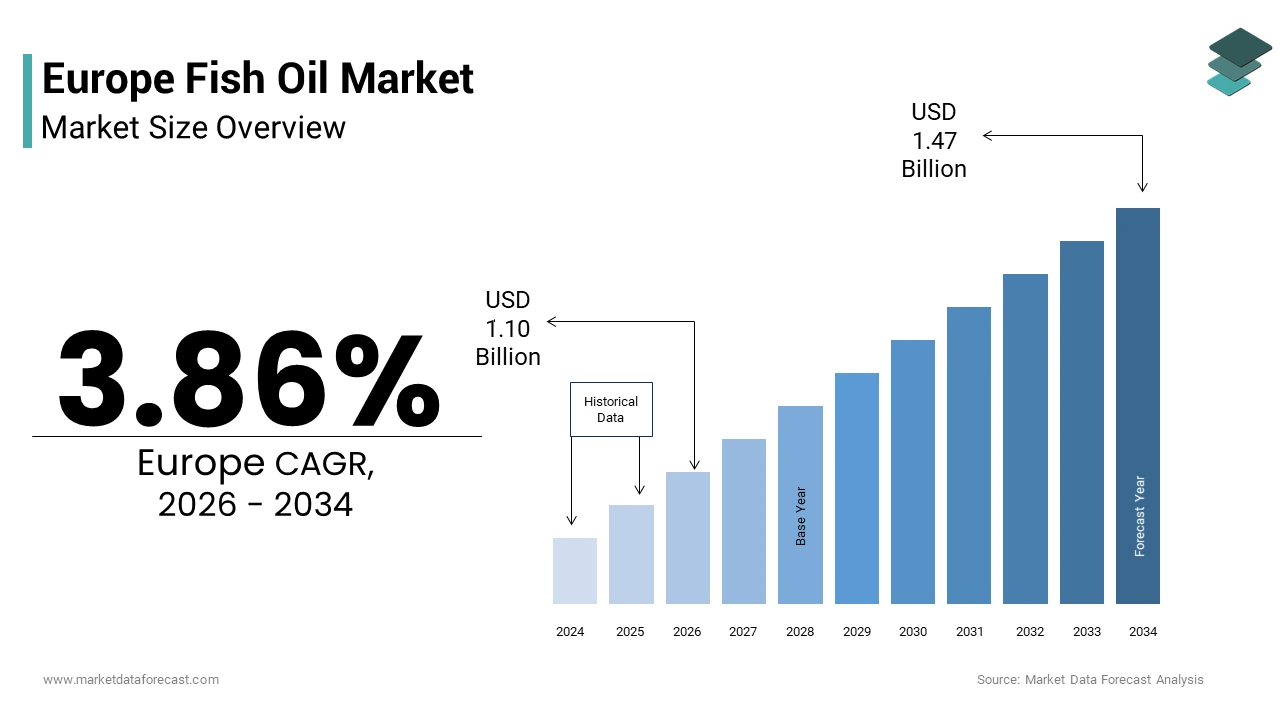

$1.06 BnMarket Estimate, 2026

$1.10 BnMarket Forecast, 2034

$1.47 BnCAGR, 2026–2034

3.86%Europe Fish Oil Market Report Summary

The European fish oil market was valued at USD 1.06 billion in 2025, is estimated to reach USD 1.10 billion in 2026, and is projected to reach USD 1.47 billion by 2034, growing at a CAGR of 3.86% during the forecast period from 2026 to 2034.

The growth of the European fish oil market is driven by the rapid expansion of aquaculture, rising demand for omega-3-rich animal feed, and increasing awareness of fish oil’s nutritional benefits in livestock, pet nutrition, and functional foods. Growing salmon farming activities, the shift toward sustainable feed solutions, and the rising use of fish oil in pharmaceuticals and dietary supplements are further fueling market growth. Additionally, stricter feed quality regulations and traceability standards across Europe are strengthening demand for high-purity fish oil.

Key Market Trends

- Increasing use of fish oil in aquaculture feed formulations to improve fish health, growth rates, and disease resistance.

- Rising demand for omega-3-enriched food and supplements across Europe’s health-conscious population.

- Growing focus on sustainable fisheries and by-product utilization to reduce environmental impact.

- Expansion of salmon farming across Nordic countries is driving raw material consumption.

- Technological advancements in refining and purification to meet pharmaceutical and food-grade standards.

Segmental Insights

- By application, the aquaculture segment was the largest and held 51.9% of the European fish oil market share in 2025.

- This dominance is attributed to the rising production of farmed fish, especially salmon, and the need for nutrient-rich feed to enhance fish growth and immunity.

- By species, the salmon segment accounted for 63.6% of the regional market share in 2025,

driven by Europe’s strong salmon farming industry and the high omega-3 content extracted from salmon processing by-products.

Regional Insights

The European fish oil market is witnessing steady growth across key seafood-producing and processing nations.

- Norway was the largest contributor, holding 28.8% of the European fish oil market share in 2025, driven by its global leadership in salmon farming and fish processing.

- Spain captured the second-largest share, supported by its strong fishing fleet and seafood processing industry.

- Germany commanded a promising share due to growing demand for nutraceuticals, supplements, and pharmaceutical-grade fish oil.

- The United Kingdom is projected to grow at a prominent CAGR, supported by the rising consumption of functional foods and dietary supplements.

- Denmark is expected to hold a notable share owing to its advanced fish processing infrastructure and sustainable marine practices.

Competitive Landscape

The European fish oil market is moderately consolidated, with leading players focusing on sustainable sourcing, advanced refining technologies, and expansion into nutraceutical and pharmaceutical applications. Strategic partnerships with aquaculture producers and investments in eco-friendly extraction processes are key growth strategies.

Prominent players in the European fish oil market include:

Ocean Group Ltd., Croda International plc, GC Rieber, Pelagia AS, BASF SE, DSM, Sürsan, Omega Protein Corporation, TripleNine, and OLVEA Group.

Europe Fish Oil Market Size

The Europe fish oil market was valued at USD 1.06 billion in 2025 and is anticipated to reach USD 1.10 billion in 2026 to USD 1.47 billion by 2034, growing at a CAGR of 3.86% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Fish Oil Market

Fish oil is lipid extract derived primarily from fatty fish such as anchovy, mackerel, herring and sardines used across human nutrition animal feed and pharmaceutical sectors. Unlike generic oils fish oil is valued for its high concentration of long chain omega 3 fatty acids, which are essential nutrients with documented cardiovascular cognitive and anti-inflammatory benefits. According to the European Food Safety Authority, a daily intake of 250 milligrams of EPA and DHA is recommended for heart health, a guideline that influences public health policies and product formulation across the EU. As per Eurostat, a significant share of European households regularly consumes dietary supplements or functional foods containing added omega 3s, which is reflecting deep integration into preventive health practices. Additionally, the European Commission’s Farm to Fork Strategy emphasizes marine resource sustainability, mandating that all fish oil used in EU food and feed must originate from fisheries certified under approved schemes such as the Marine Stewardship Council or EU catch documentation. These regulatory and nutritional frameworks position fish oil not as a commodity but as a strategic health and sustainability asset within Europe’s bioeconomy.

MARKET DRIVERS

EU Health Authority Endorsements and Cardiovascular Disease Prevention Guidelines Drive Consumer Demand

Scientific validation from European regulatory bodies has cemented fish oil as a cornerstone of public health nutrition, which is majorly driving the growth of the European fish oil market. According to the European Food Safety Authority, multiple health claims related to omega 3 fatty acids have been authorized under Regulation EC No 1924/2006, including benefits for heart function, brain health, and vision. Most significantly, EFSA concluded that daily intake of 250 milligrams of EPA and DHA contributes to normal cardiac function, which is a claim permitted on product labels across all 27 member states. This official endorsement directly influences consumer behavior. As per Eurobarometer surveys, a substantial share of EU adults aged 40 and above report taking omega 3 supplements for heart health. The impact is amplified by national health programs; in Sweden, the Public Health Agency includes fatty fish consumption in its dietary guidelines, while in Germany statutory health insurers reimburse omega 3 prescriptions for patients with hypertriglyceridemia. With cardiovascular disease causing over 1.8 million deaths annually in the EU according to the European Heart Network, this regulatory, scientific, and clinical alignment creates sustained and medically validated demand for high purity fish oil across pharmaceutical and nutraceutical channels.

Mandatory Inclusion of Omega 3s in Aquaculture and Livestock Feed Under EU Animal Nutrition Standards

The Europe fish oil market is significantly propelled by regulatory requirements in animal feed formulation, particularly for farmed fish and poultry. According to the European Commission Regulation (EU) 2021/1165, all feeds for salmonids must contain minimum levels of EPA and DHA to ensure nutritional quality and fish welfare. Farmed salmon, which represents the majority of salmon consumed in Europe, requires omega 3 enrichment in feed to replicate wild fish profiles. As per the European Aquaculture Association, EU salmon production exceeded half a million metric tons in 2024, necessitating large volumes of fish oil annually. Similarly, the European Feed Manufacturers Federation mandates DHA enrichment in layer hen diets to produce omega 3 enriched eggs, which is a segment that has shown steady growth. These regulatory and market driven feed standards create a structural and non-discretionary demand base that absorbs a majority of Europe’s fish oil supply, ensuring market stability independent of human supplement trends.

MARKET RESTRAINTS

Overfishing Concerns and Stricter Quotas on Key Pelagic Species Limit Raw Material Supply

The Europe fish oil market faces persistent supply constraints due to ecological pressures on small pelagic fish stocks that serve as primary raw material sources. According to the International Council for the Exploration of the Sea, catches of European anchovy in the Bay of Biscay have declined in recent years due to warming sea temperatures and spawning disruption. In response, the European Commission reduced the 2024 total allowable catch for Norwegian spring spawning herring and for North Sea mackerel, citing precautionary stock assessments. These quotas directly impact fish oil yields. As per the European Fishmeal and Fish Oil Producers Association, raw material availability for European refiners fell year on year. While fisheries are required to operate under MSC or EU sustainability certifications, the biological limits of wild stocks create a hard ceiling on conventional fish oil production. This supply ceiling intensifies competition for raw material and elevates prices, particularly for high EPA grades used in pharmaceutical applications.

Consumer Skepticism Toward Supplement Efficacy and Preference for Whole Food Sources Suppress Mass Market Growth

Despite scientific backing, a segment of European consumers remains unconvinced of the benefits of isolated omega 3 supplements, preferring whole dietary sources, which is further impeding the European fish oil market growth. According to the European Consumer Organisation, many respondents in Germany, France, and Italy believe that eating fatty fish twice a week is superior to taking capsules, with a notable share citing concerns about supplement purity and processing. This skepticism is reinforced by inconsistent messaging. A review published in The Lancet questioned the cardiovascular benefits of omega 3 supplements in low-risk populations, creating public confusion. Consequently, mass market growth is constrained as consumers opt for functional foods like fortified milk or omega 3 enriched eggs rather than standalone supplements. As per Kantar Health Europe, while a majority of households consume omega 3s in some form, only a smaller proportion regularly purchase fish oil capsules. This behavioral gap between nutritional awareness and supplement adoption limits market expansion beyond health conscious and clinically advised segments.

MARKET OPPORTUNITIES

Rise of Algal Oil as a Sustainable Vegan Alternative Creates New Market Segments

The emergence of algal oil is unlocking new consumer groups and application areas previously inaccessible to fish oil, which is a potential opportunity in the European fish oil market. According to the European Algae Biomass Association, algal omega 3 production in the EU has been growing steadily, driven by demand from vegan and vegetarian populations which number in the tens of millions across Europe as per the European Vegetarian Union. Major brands such as Nestlé and Danone have reformulated infant formulas and dairy alternatives with algal oil to meet clean label and allergen free requirements. Crucially, algal oil bypasses fishy aftertaste, oxidation issues, and marine allergen concerns, making it ideal for sensitive applications. As per Euromonitor, many new omega-3 supplement launches in the UK and Netherlands in 2024 featured algal sources. While not a direct substitute in aquaculture, algal oil is capturing high value human nutrition segments, allowing fish oil producers to focus on premium pharmaceutical and feed markets where marine origin remains preferred or mandated.

Integration of Fish Oil Into Medical Nutrition and Prescription Therapies Expands Clinical Applications

The Europe fish oil market is experiencing high value growth through its incorporation into medically supervised nutrition for chronic disease management. According to the European Medicines Agency, high purity ethyl ester formulations of EPA such as icosapent ethyl are approved as adjunctive therapy for severe hypertriglyceridemia. In 2024, the European Society of Cardiology updated its guidelines to recommend prescription omega 3s for patients with cardiovascular disease and elevated triglycerides based on REDUCE-IT trial outcomes showing significant reductions in major adverse cardiac events. Hospitals and pharmacies now dispense these medical grade oils under reimbursement schemes in Germany, France, and Italy. As per IQVIA, prescription omega 3 sales in Europe grew year on year driven by clinical adoption. This shift from wellness to therapy not only commands premium pricing but also ensures demand stability through healthcare system procurement insulated from retail market volatility.

MARKET CHALLENGES

Fragmented Certification and Traceability Standards Across EU Member States Complicate Compliance

The absence of a unified EU framework for fish oil sustainability and purity verification creates operational complexity for producers and brand owners, which is a major challenge to the growth of the European fish oil market. According to the European Commission, while the Common Fisheries Policy mandates catch documentation, national interpretation of “sustainable sourcing” varies significantly. Norway requires full chain of custody MSC certification for fish oil exports to the EU, while Spain accepts regional fishery improvement projects as compliant. Similarly, purity standards for heavy metals and oxidation markers differ; Germany enforces stricter peroxide value limits than Poland under national food safety laws. As per the European Health and Nutrition Association, many fish oil importers maintain multiple certification protocols to satisfy retailer requirements across different countries. This regulatory fragmentation increases testing, documentation, and administrative costs, discouraging small producers and reducing market fluidity despite harmonized EFSA health claims.

Price Volatility Due to Geopolitical Disruptions in Key Supply Regions Affects Cost Stability

Europe’s fish oil supply chain remains vulnerable to external shocks due to heavy reliance on raw material imports from politically sensitive regions. According to the European Fishmeal and Fish Oil Producers Association, a large share of fish oil refined in the EU originates from Peruvian and Chilean anchoveta catches. In 2024, El Niño induced ocean warming caused Peru to suspend its fishing season for several months, which is reducing global fish oil supply and spiking European import prices as per the International Fishmeal and Fish Oil Organization. Additionally, Black Sea port disruptions affected Ukrainian and Russian fish meal exports, which indirectly influence global fish oil pricing through feed market linkages. These instabilities force supplement and feed manufacturers to absorb margin pressure or reformulate with alternative oils, compromising product consistency. Until Europe scales domestic aquaculture byproducts or algal production, the market will remain exposed to climate and geopolitical risks beyond its control.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.86% |

| Segments Covered | By Application, Species, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic,c & Rest of Europe |

| Market Leaders Profiled | Ocean Group Ltd., Croda International plc, GC Rieber, Pelagia AS, BASF SE, DSM, Sürsan, Omega Protein Corporation, TripleNine, OLVEA Group |

SEGMENTAL ANALYSIS

By Application Insights

The aquaculture segment dominated the market by holding 51.9% of the European fish oil market share in 2025. The dominance of aquaculture segment in this regional market is attributed to the EU feed regulations and the scale of farmed fish production. European aquaculture regulations enforce strict nutritional standards to ensure farmed fish replicate the health profile of wild counterparts. According to the European Commission Regulation (EU) 2021/1165, all feeds for salmonids must contain minimum levels of eicosapentaenoic acid (EPA) and docosahexaenoic acid (DHA) to support fish health and human nutritional value. Farmed salmon, which represents the majority of salmon consumed in the EU, requires omega 3 enrichment in feed to maintain flesh quality. Norwegian and Scottish salmon farms operate under these EU aligned standards even when exporting to the bloc, ensuring consistent and non-discretionary demand regardless of human supplement trends.

The human consumption segment is likely to register the fastest growth and is estimated to witness a CAGR of 7.05% over the forecast period. Prescription grade fish oil is gaining clinical traction for treating severe hypertriglyceridemia and cardiovascular risk reduction. According to the European Society of Cardiology, its 2024 guidelines recommend icosapent ethyl for patients with established cardiovascular disease and elevated triglycerides. The European Medicines Agency has approved such products for reimbursement in Germany, France, and Italy where statutory health systems cover high risk patients. As per IQVIA, prescription omega 3 sales in Europe grew year on year with hospital pharmacies and specialty clinics driving adoption. This shift from wellness to therapy creates a high value insulated demand stream less vulnerable to consumer skepticism and retail price competition.

By Species Insights

The salmon segment accounted for 63.6% of the regional market share in 2025. The leading position of salmon segment in the European fish oil market is attributed to the salmon’s high omega 3 retention requirement and dominant position in European aquaculture. Salmon are cold water carnivorous fish that naturally accumulate high levels of omega 3 fatty acids in their flesh, which is a trait that must be preserved in farmed production. According to the Norwegian Institute of Nutrition and Seafood Research, farmed salmon require lipid rich feed with EPA and DHA to maintain flesh quality and consumer health benefits. Unlike omnivorous species such as tilapia which can thrive on plant-based oils, salmon cannot efficiently convert short chain omega 3s from flax or canola into long chain EPA and DHA. As per the University of Stirling, reducing fish oil content in salmon feed significantly lowers final fillet omega 3 levels, which is making it unacceptable for health-conscious European consumers. This biological imperative ensures salmon remains the primary driver of high-grade fish oil demand.

The tilapia segment is the fastest growing and is predicted to register a CAGR of 10.7% over the forecast period. Tilapia farming is gaining traction in controlled recirculating aquaculture systems in Spain, Greece, and Hungary due to its fast growth, low feed conversion ratio, and tolerance to variable water conditions. According to the European Commission’s Directorate General for Agriculture, tilapia production in the EU has been steadily increasing in recent years. While tilapia is omnivorous and can use plant-based oils, its starter and grow out feeds still require fish oil for larval development and immune support. As per the Hellenic Aquaculture Producers Organization, Greek tilapia farms have increased fish oil use to improve survival rates in intensive systems. This emerging production base creates a new and growing demand channel previously insignificant in Europe.

Top Countries In The Market

Norway Fish Oil Market Analysis

Norway dominated the market by holding 28.8% of the regional market share in 2025. The growth of Norway in the European fish oil market is driven by its dual role as the world’s largest salmon producer and a leading fish oil refiner. As per the Norwegian Directorate of Fisheries, Norway remains the top salmon farming nation, with production exceeding one million metric tons annually, requiring significant volumes of fish oil for feed. The country’s proximity to Arctic pelagic fisheries ensures access to high quality raw material, while refineries such as Aker BioMarine and GC Rieber supply pharmaceutical grade oil to EU nutraceutical markets. Additionally, Norway’s stringent feed regulations mandate minimum omega 3 levels, ensuring consistent demand. With the majority of its salmon exported to the EU, Norway functions as both a production and processing hub, making it the undisputed center of Europe’s fish oil ecosystem.

Spain Fish Oil Market Analysis

Spain occupied the second largest share of the European fish oil market in 2025 with demand fueled by its extensive aquaculture industry and growing human supplement consumption. According to the Spanish Ministry of Agriculture, Spain is a leading producer of farmed seabass and seabream, alongside emerging tilapia farms in Andalusia, requiring significant fish oil inputs. Additionally, Spain is among Europe’s largest consumers of dietary supplements per capita, with omega 3s ranking as a top selling category according to IQVIA’s Iberia Health Report. The country’s long coastline and fishing heritage normalize fish-based nutrition, while public health campaigns promote omega 3 intake for cardiovascular protection. This dual demand from animal feed and human health creates a resilient and diversified market less dependent on single sector fluctuations.

Germany Fish Oil Market Analysis

Germany commanded for a promising share of the European fish oil market in 2025 with leadership in high purity pharmaceutical and nutraceutical applications. As per the German Federal Institute for Drugs and Medical Devices, numerous prescriptions and over the counter omega 3 products are approved for cardiovascular and neurological indications. Statutory health insurers reimburse high dose EPA formulations for patients with hypertriglyceridemia, creating a stable medical demand stream. Additionally, Germany’s large pet food industry uses fish oil in premium canine and feline diets for skin and coat health, as confirmed by the German Pet Food Association. As per Euromonitor, German supplement users prioritize certified purity and traceability, driving demand for IFOS and MSC certified oils. This focus on quality, science, and regulation ensures Germany remains a high value anchor market.

United Kingdom Fish Oil Market Analysis

The United Kingdom is predicted to grow at a prominent CAGR in the European fish oil market during the forecast period with strong demand from functional food fortification and pet nutrition sectors. According to the UK Food Standards Agency, infant formulas and dairy products sold in 2024 were widely fortified with DHA from fish oil in compliance with national nutrition guidelines. The country’s pet ownership rate fuels demand for premium pet foods enriched with omega 3s, as per the Pet Food Manufacturers’ Association. Despite Brexit, the UK maintains EFSA aligned health claims and sourcing standards, ensuring continuity in product formulation. The rise of private label fortified foods in retailers such as Tesco and Sainsbury’s further embeds fish oil into everyday consumption patterns, creating broad based stable demand.

Denmark Fish Oil Market Analysis

Denmark is projected to account for a notable share of the European fish oil market over the forecast period. Denmark serves as a pioneer in public health driven fortification. According to the Danish Veterinary and Food Administration, national policy mandates DHA fortification in milk, yogurt, and infant formula, with recent expansions to include other staple foods. This institutional approach ensures near universal omega 3 consumption without relying on supplement adherence. Additionally, Denmark hosts major aquaculture feed producers such as BioMar, which supply fish oil-based formulations to farms across Northern Europe. As per the University of Copenhagen, the Danish population has among the highest average blood omega 3 levels in the EU, well above the cardioprotective threshold. This policy led integration makes Denmark a unique and influential model for systemic fish oil utilization.

COMPETITIVE LANDSCAPE

Competition in the Europe fish oil market is characterized by a dual contest between sustainability credentials and molecular purity. The market is dominated by a handful of integrated refiners who compete not on volume but on certification transparency and application expertise. Barriers to entry are high due to stringent EU regulations on marine sourcing heavy metal limits and health claim substantiation. Competition intensifies around differentiation: pharmaceutical grade players battle on clinical validation and pharmacopoeia compliance while feed segment leaders focus on oxidation stability and feed conversion efficiency. Meanwhile the rise of algal alternatives pressures human nutrition suppliers to justify marine sourcing through superior bioavailability or traceability. Unlike commodity oils success here depends on scientific credibility regulatory alignment and ecosystem partnerships with fisheries feed mills and health brands. As the EU tightens Blue Economy standards and public health policies the competitive landscape increasingly rewards those who embed fish oil within verifiable sustainable and health enhancing value chains.

KEY MARKET PLAYERS

A few of the market players in the Europe fish oil market are

- Ocean Group Ltd.

- Epax

- Croda International plc

- GC Rieber

- Aker BioMarine

- Pelagia AS

- BASF SE

- DSM

- Sürsan

- Omega Protein Corporation

- TripleNine

- OLVEA Group

Top Players In The Market

- Aker BioMarine is a global leader in sustainable marine ingredients with a strong presence in the Europe fish oil market through its Superba krill oil and QRILL feed products. The company contributes significantly to the global omega 3 supply chain by pioneering Antarctic krill harvesting under strict CCAMLR quotas and developing high purity phospholipid bound EPA and DHA. In Europe Aker BioMarine has strengthened its position by expanding its pharmaceutical grade fish oil production facility in Norway and achieving full Marine Stewardship Council certification for its entire supply chain. Recent actions include the launch of its QRILL Aqua line for European salmon farmers seeking sustainable alternatives to traditional fish oil and partnerships with EU nutraceutical brands to develop cardiovascular health formulations aligned with EFSA claims.

- Epax is a premier producer of high concentration omega 3 fatty acids derived from fish oil with deep integration across Europe’s pharmaceutical and nutraceutical sectors. The company supplies EPA and DHA concentrates exceeding 90% purity used in prescription and over the counter cardiovascular and cognitive health products. In Europe Epax has reinforced its market presence by achieving full compliance with the European Pharmacopoeia standards and implementing blockchain based traceability from catch to capsule. It also invested in enzymatic concentration technology that reduces energy use by 30% while maintaining molecular integrity. These actions position Epax as a trusted supplier for science backed health solutions in a market increasingly demanding transparency and clinical efficacy.

- Croda International delivers specialty lipid ingredients including highly refined fish oil derivatives for human nutrition animal health and personal care applications across Europe. The company contributes globally by developing encapsulation and stabilization technologies that enhance omega 3 bioavailability and shelf life. In Europe Croda has strengthened its position by expanding its OmegaPure range of IFOS certified fish oils for infant formula and medical nutrition. It also partnered with European aquaculture feed producers to develop oxidation resistant formulations that maintain EPA and DHA integrity during pelleting. Recent investments in algal oil co processing at its Spanish facility allow integrated marine and vegetarian omega 3 solutions supporting clients’ clean label and sustainability goals.

Top Strategies Used By The Key Market Participants

Key players in the Europe fish oil market prioritize full traceability and sustainability certification through Marine Stewardship Council or EU catch documentation to meet regulatory and consumer expectations. They invest in molecular concentration technologies to produce high purity EPA and DHA exceeding 90% for pharmaceutical applications. Companies expand blockchain or digital batch tracking systems to verify origin purity and compliance with EFSA health claims. Strategic partnerships with aquaculture feed mills and nutraceutical brands ensure integrated solutions from raw material to finished product. Additionally, they diversify into algal or krill-based omega 3s to address vegan demand while maintaining marine oil leadership in feed and high value human health segments.

MARKET SEGMENTATION

This research report on the Europe fish oil market is segmented and sub-segmented into the following categories.

By Application

- Human Consumption

- Aquaculture

- Pet Food

- Others

By Species

-

- Traditional Pelagic and Demersal Species

- Tuna

- Salmon

- Pangasius

- Tilapia

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe fish oil market?

The Europe fish oil market involves the production, processing, and sale of fish oil products used in dietary supplements, animal feed, pharmaceuticals, and nutraceuticals.

Why is the fish oil market growing in Europe?

Growth is driven by rising health awareness, demand for omega-3 supplements, expanding aquaculture, and increased use in pet and livestock nutrition.

What are the main applications of fish oil in Europe?

Fish oil is used in dietary supplements, functional foods, pharmaceuticals, animal feed, aquaculture, and cosmetics.

Which types of fish oil are popular in Europe?

Common types include refined, crude, pharmaceutical-grade, concentrated omega-3, and natural fish oil varieties.

What benefits do fish oil products offer?

Fish oil is valued for heart health, brain function, anti-inflammatory properties, immune support, and improved skin and joint health.

Which countries lead the Europe fish oil market?

Key markets include Norway, Iceland, Denmark, Germany, and the UK, supported by strong fishing industries and supplement demand.

How does regulation impact the Europe fish oil market?

Stringent EU food safety, labeling, and quality standards ensure product purity, safety, and accurate omega-3 content claims.

What are challenges in the Europe fish oil market?

Challenges include supply volatility, sustainability concerns, environmental regulations, fluctuating raw material prices, and competition from plant-based oils.

What trends are shaping the Europe fish oil market?

Trends include sustainable sourcing, traceability initiatives, omega-3 fortified foods, personalized nutrition, and eco-certification.

How does sustainability affect fish oil production?

Sustainability practices such as responsible fishing, MSC certification, and byproduct utilization reduce environmental impact and support long-term supply.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com