- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$104 BnMarket Estimate, 2026

$109 BnMarket Forecast, 2034

$157 BnCAGR, 2026–2034

4.63%Europe Flat Glass Market Size

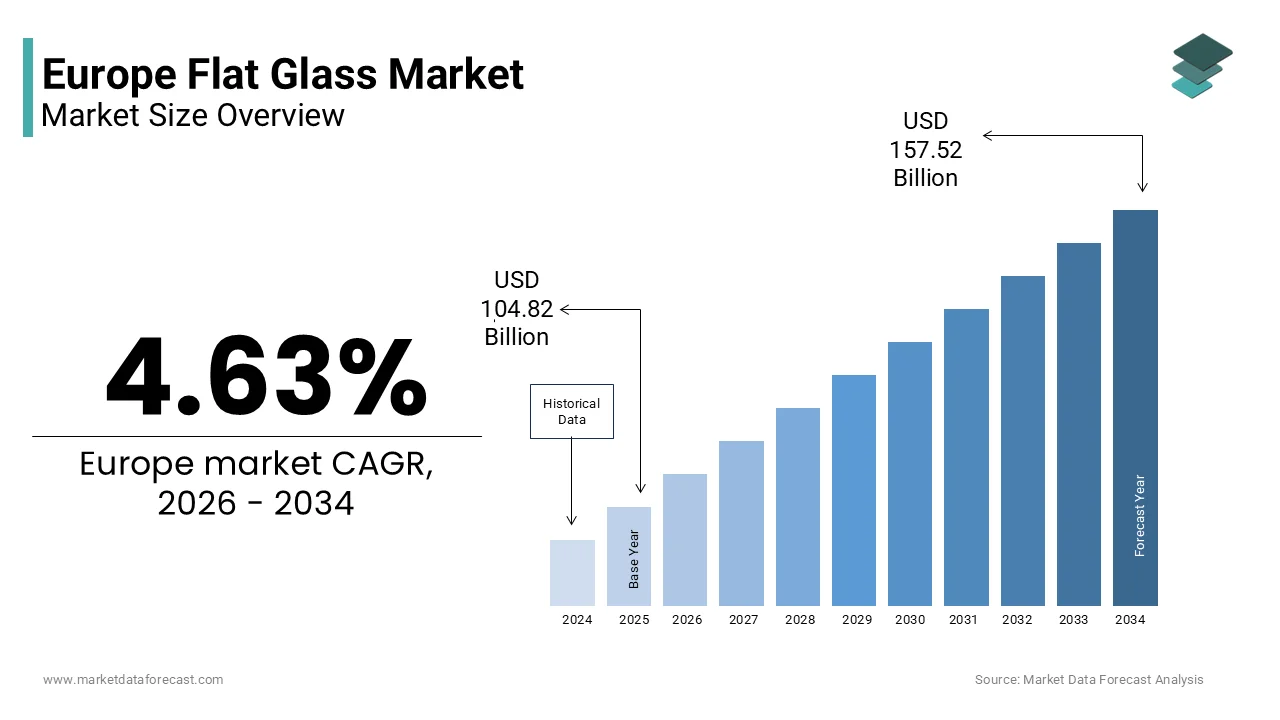

The Europe flat glass market size was valued at USD 104.82 billion in 2025 and is expected to reach USD 157.52 billion by 2034 from USD 109.67 billion in 2026. The Europe flat glass market is predicted to register at a CAGR of 4.63% from 2026 to 2034.

flat glass is a cornerstone of the construction, automotive, and renewable energy industries of Europe and widely used in windows, facades, solar panels, and vehicle glazing. According to the European Union’s Eurostat, the flat glass industry contributes significantly to the EU economy. The demand for flat glass is steadily growing in Europe owing to the urbanization, infrastructure development, and sustainability initiatives. Germany, France, and Italy collectively account for over 60% of the European flat glass market. The construction sector remains the largest consumer of flat glass, representing approximately 70% of total demand, fueled by stringent energy performance regulations such as the EU’s Energy Performance of Buildings Directive (EPBD). This directive mandates the use of energy-efficient glazing solutions, including double and triple-glazed windows, which reduce carbon emissions and improve thermal insulation. Furthermore, the growing adoption of photovoltaic glass in solar energy applications has surged by 12% annually since 2020, as per the International Energy Agency (IEA).

In the automotive sector, the demand for advanced glazing solutions, such as laminated and acoustic glass, has risen due to increasing consumer preferences for safety, noise reduction, and lightweight materials. Additionally, the European Green Deal’s emphasis on decarbonizing industries has spurred innovation in low-carbon flat glass manufacturing processes.

MARKET DRIVERS

Growing Demand for Energy-Efficient Buildings

The increasing demand for energy-efficient buildings is a significant driver of the European flat glass market. The EU’s Energy Performance of Buildings Directive (EPBD) mandates the use of high-performance glazing solutions to reduce energy consumption in residential and commercial structures. According to Eurostat, buildings account for approximately 40% of Europe’s total energy consumption, prompting widespread adoption of double and triple-glazed windows that enhance thermal insulation. In 2022, the integration of energy-efficient glazing systems grew by 8% year-on-year, as reported by the European Environment Agency. These systems help reduce heating and cooling costs by up to 30%, aligning with the EU’s goal of achieving carbon neutrality by 2050. This regulatory push, coupled with rising consumer awareness about sustainability, has significantly bolstered the demand for advanced flat glass products across the region.

Expansion of Solar Energy Infrastructure

The rapid expansion of solar energy infrastructure is another key driver propelling the European flat glass market. Photovoltaic (PV) glass, used in solar panels, has witnessed unprecedented growth due to the EU’s ambitious renewable energy targets under the European Green Deal. The International Energy Agency (IEA) reports that solar energy capacity in Europe expanded by 25% in 2022, with flat glass being a critical component in PV module manufacturing. Furthermore, the European Glass Federation highlights that the demand for photovoltaic glass surged by 12% annually between 2020 and 2023. This growth is fueled by government incentives, such as subsidies for solar installations, and the declining cost of solar technologies. As Europe accelerates its transition to clean energy, the flat glass market is set to benefit from sustained investments in solar infrastructure, reinforcing its pivotal role in the renewable energy ecosystem.

MARKET RESTRAINTS

High Energy Costs in Flat Glass Production

The European flat glass market faces significant challenges due to the high energy costs associated with its manufacturing processes. Flat glass production is energy-intensive, relying heavily on natural gas and electricity, which account for approximately 20-25% of total production costs, as stated by the European Commission. The ongoing energy crisis in Europe, exacerbated by geopolitical tensions, has led to a 60% surge in natural gas prices since 2021, according to Eurostat. This volatility has placed immense pressure on manufacturers, particularly smaller firms, to maintain profitability while adhering to stringent environmental regulations. Additionally, the rising cost of carbon credits under the EU Emissions Trading System (ETS) further compounds the financial burden. These escalating expenses hinder the industry’s ability to invest in innovation and expand production capacities, ultimately restraining market growth.

Stringent Environmental Regulations

Stringent environmental regulations pose another major restraint to the European flat glass market. The EU’s commitment to reducing greenhouse gas emissions under the European Green Deal has imposed strict limits on industrial carbon footprints. According to the European Environment Agency, the flat glass sector contributes approximately 3% of industrial emissions in Europe, prompting regulators to enforce measures such as the Industrial Emissions Directive (IED). While these policies aim to promote sustainability, they often result in increased compliance costs for manufacturers. For instance, investments in low-carbon technologies and emission-reduction systems can raise operational expenses by up to 15%, as reported by the European Glass Federation. Smaller players, in particular, struggle to adapt to these regulatory pressures, leading to reduced competitiveness and slower market expansion amidst the growing focus on decarbonization.

MARKET OPPORTUNITIES

Advancements in Smart Glass Technology

The development and adoption of smart glass technology present a significant opportunity for the European flat glass market. Smart glass, which can dynamically adjust its tint or opacity to control light and heat transmission, is gaining traction due to its energy-saving potential and aesthetic appeal. According to the European Commission, buildings equipped with smart glass can reduce energy consumption by up to 20%, aligning with the EU’s goal of achieving energy-efficient infrastructure. The International Energy Agency (IEA) projects that the global smart glass market will grow at a CAGR of 11% between 2023 and 2030, with Europe leading in innovation and adoption. Government initiatives, such as subsidies for green building technologies, further encourage the integration of smart glass in commercial and residential structures. As demand for sustainable and technologically advanced solutions rises, the flat glass industry is well-positioned to capitalize on this emerging trend.

Expansion in Electric Vehicle (EV) Manufacturing

The rapid growth of the electric vehicle (EV) industry offers another promising opportunity for the European flat glass market. EVs require advanced glazing solutions, including laminated windshields, acoustic glass, and solar roofs, to enhance safety, noise reduction, and energy efficiency. The European Automobile Manufacturers’ Association (ACEA) reports that EV sales in Europe surged by 65% in 2022, accounting for over 20% of total car sales. This shift is driving increased demand for specialized automotive glass, with the European Glass Federation estimating a 10% annual growth in automotive glazing applications through 2026. Additionally, government policies promoting EV adoption, such as tax incentives and investments in charging infrastructure, are accelerating this trend. As Europe strives to become a global leader in EV production, the flat glass market stands to benefit significantly from the expanding automotive sector’s need for innovative and high-performance glass solutions.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Scarcity

The European flat glass market faces significant challenges due to supply chain disruptions and the scarcity of critical raw materials. The production of flat glass relies heavily on materials like silica sand, soda ash, and limestone, which have experienced volatile pricing and limited availability in recent years. According to Eurostat, global supply chain disruptions caused by geopolitical tensions and the aftermath of the COVID-19 pandemic led to a 15% increase in raw material costs for the glass industry in 2022. Additionally, the European Commission highlights that over 60% of key raw materials used in flat glass manufacturing are imported, making the industry vulnerable to trade restrictions and logistical bottlenecks. These challenges hinder production efficiency and increase operational costs, forcing manufacturers to explore alternative sourcing strategies while grappling with potential delays in meeting rising market demand.

Intense Competition from Low-Cost Imports

Intense competition from low-cost imports poses another major challenge to the European flat glass market. The European Glass Federation reports that imports from non-EU countries, particularly China and Turkey, have surged by 25% annually over the past five years, driven by lower production costs and pricing strategies. These imports often undercut domestic manufacturers, creating pricing pressures and eroding profit margins. Furthermore, the European Commission notes that imported flat glass products sometimes fail to meet the region’s stringent quality and environmental standards, leading to concerns about unfair trade practices. While anti-dumping measures have been introduced to mitigate this issue, they have not fully addressed the problem. European manufacturers must now invest in differentiation strategies, such as innovation and sustainability, to compete effectively in an increasingly price-sensitive market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.63% |

| Segments Covered | By Application, Function, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Saint-Gobain S.A., AGC Inc. (formerly Asahi Glass Co., Ltd.), NSG Group (Pilkington), Guardian Glass, Şişecam Group, Euroglas GmbH, Fuyao Glass Industry Group Co., Ltd., Glaston Corporation, Nippon Sheet Glass Co., Ltd. (NSG Group), S.A. Bendheim Ltd., AGP Glass, PPG Industries, Inc., Schott AG, Vitro S.A.B. de C.V., HNG Float Glass Limited, Central Glass Co., Ltd., Cardinal Glass Industries, Abrisa Technologies, Fives Stein, and Others. |

SEGMENTAL ANALYSIS

By Application Insights

The building and construction segment dominated the European flat glass market by holding a 70.8% of the European market share in 2025. The domination of building and construction segment is majorly driven by the stringent EU regulations like the Energy Performance of Buildings Directive (EPBD), which mandate energy-efficient glazing to reduce carbon emissions. The European Environment Agency reports a 10% annual growth in demand for advanced glazing systems, driven by urbanization and renovation projects accounting for 40% of construction activities. This segment’s importance lies in enhancing thermal insulation, reducing energy costs, and supporting Europe’s goal of carbon neutrality by 2050.

The solar energy segment is predicted to be the fastest growing segment and grow at a CAGR of 12.7% over the forecast period. In 2022, solar energy capacity grew by 25%, fueled by the European Green Deal’s renewable energy targets. Photovoltaic glass demand surged 15% annually, as highlighted by the European Glass Federation, due to subsidies and declining solar technology costs. This segment’s rapid growth underscores its role in decarbonizing Europe’s energy mix, with countries like Germany leading solar infrastructure investments, making it vital for achieving sustainability goals.

By Function Insights

The safety glazing segment had the leading share of 35.3% of the European market share in 2025 due to the stringent safety regulations in automotive and construction sectors. Eurostat highlights that safety glazing reduces accidents by providing shatterproof properties, with demand growing at 6% annually. Its importance lies in applications such as laminated windshields, building facades, and fire-resistant windows. The increasing focus on occupant safety and energy-efficient buildings further amplifies its adoption, making it a critical component in modern infrastructure and transportation.

The self-cleaning flat glass segment is projected to witness a CAGR of 9.5% during the forecast period owing to the rising demand for low-maintenance solutions in commercial and residential buildings. Self-cleaning glass, coated with photocatalytic and hydrophilic layers, reduces cleaning costs by up to 40%, as highlighted by Eurostat. Its ability to decompose organic dirt using sunlight aligns with Europe’s sustainability goals, driving adoption in skyscrapers, greenhouses, and solar panels. With urbanization and smart city initiatives expanding, this segment’s role in enhancing efficiency and reducing resource consumption underscores its rapid growth trajectory.

REGIONAL ANALYSIS

Germany held the largest share of the European flat glass market by capturing 307% of the European market share in 2025. The domination of Germany in the European market is primarily attributed to the strong emphasis on energy-efficient buildings, supported by stringent environmental regulations under the German Energy Efficiency Strategy. The country’s robust automotive sector also plays a pivotal role, demanding advanced glazing solutions for safety and lightweight designs. According to the Federal Ministry for Economic Affairs and Climate Action, Germany’s commitment to renewable energy has significantly increased demand for photovoltaic glass, positioning it as a leader in solar infrastructure. This focus on sustainability and innovation solidifies Germany’s dominance in the flat glass market.

France is a prominent regional market for flat glass and is anticipated to hold a substantial share of the European market during the forecast period. The growth of the French market is driven by large-scale renovation projects and urbanization trends. As highlighted by FranceAgriMer, the French government’s initiatives to modernize aging infrastructure and promote green building practices have fueled demand for energy-efficient glazing solutions. Additionally, France’s thriving construction sector, coupled with its focus on reducing carbon emissions, has accelerated the adoption of advanced flat glass products. The country’s strategic investments in sustainable architecture and smart cities further reinforce its position as a key player in the regional market, making it a vital contributor to Europe’s flat glass industry.

The flat glass market in the UK is another lucrative regional segment in the European market. The growth of the UK market is fueled by significant investments in sustainable infrastructure and smart city development, alongside a rising focus on energy-efficient buildings. Post-pandemic recovery has also spurred demand for residential and commercial construction, with renovation projects accounting for a substantial portion of flat glass consumption. The UK’s commitment to achieving net-zero carbon emissions by 2050 has further driven the adoption of innovative glazing solutions, such as low-emissivity and solar control glass, underscoring its importance in the European flat glass landscape.

KEY MARKET PLAYERS

Companies playing a prominent role in the global europe flat glass market include Saint-Gobain S.A., AGC Inc. (formerly Asahi Glass Co., Ltd.), NSG Group (Pilkington), Guardian Glass, Şişecam Group, Euroglas GmbH, Fuyao Glass Industry Group Co., Ltd., Glaston Corporation, Nippon Sheet Glass Co., Ltd. (NSG Group), S.A. Bendheim Ltd., AGP Glass, PPG Industries, Inc., Schott AG, Vitro S.A.B. de C.V., HNG Float Glass Limited, Central Glass Co., Ltd., Cardinal Glass Industries, Abrisa Technologies, Fives Stein, and Others.

MARKET SEGMENTATION

This research report on the Europe flag glass market is segmented and sub-segmented into the following categories.

By Function

- UV Filter flat glass

- Heat insulation flat glass

- Safety glazing

- Soundproofed glazing

- Self-cleaning flat glass

- Ion exchange flat glass

- Others

By Application

- Building and Construction

- Automotive

- Aerospace

- Solar energy

- Electronic appliances

- Furniture

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe