Europe Fresh Figs Market Size, Share, Trends & Growth Forecast Report – Segmented By Varietal (Kadota, Calimyrna, Black Mission, Celeste, Panache), Cultivation Method, Distribution Channel, Packaging, Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Fresh Figs Market Report Summary

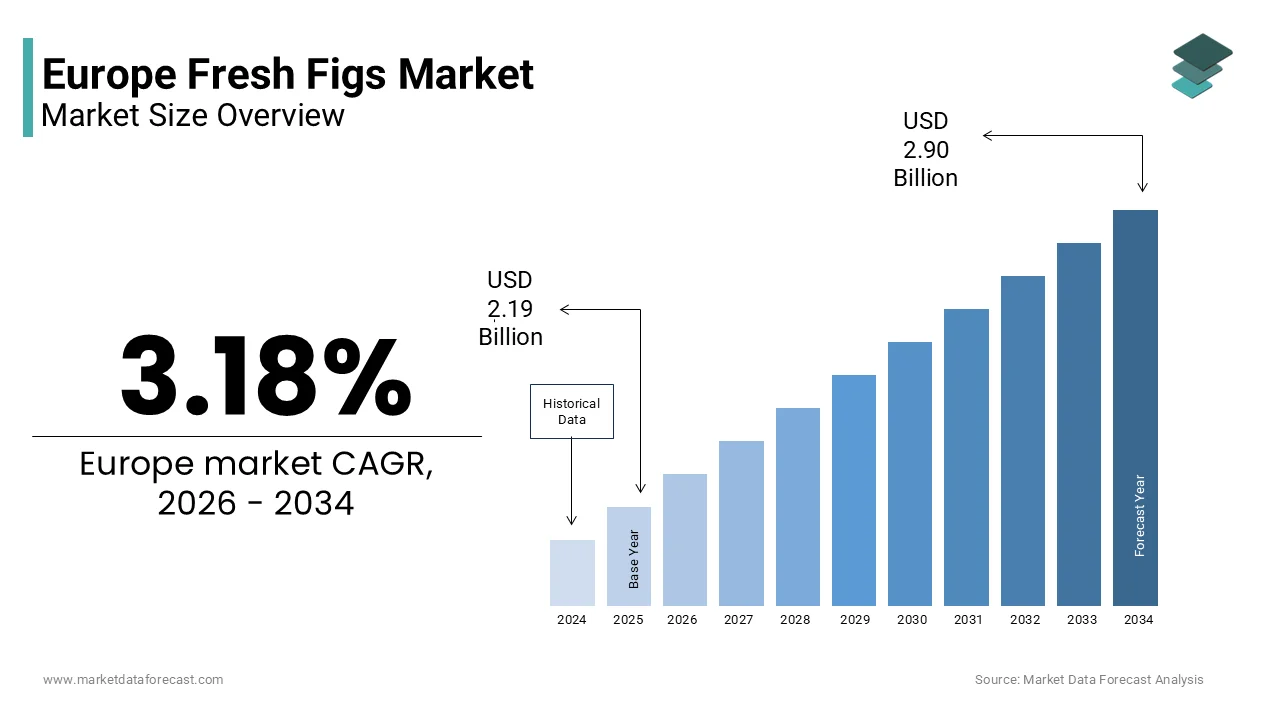

The Europe fresh figs market was valued at USD 2.19 billion in 2025, is estimated to reach USD 2.26 billion in 2026, and is projected to reach USD 2.90 billion by 2034, growing at a CAGR of 3.18% during the forecast period from 2026 to 2034. The growth of the Europe fresh figs market is driven by increasing consumer preference for fresh and nutritious fruits, rising demand for Mediterranean diets, and growing awareness of the health benefits of figs. Expanding retail distribution networks, increasing consumption of premium fresh produce, and advancements in cultivation and post-harvest handling techniques are further supporting market growth. Additionally, rising demand for natural, minimally processed foods is contributing to the steady expansion of the fresh figs market across Europe.

Key Market Trends

-

Rising consumer preference for fresh, nutritious, and naturally sweet fruits is driving demand for fresh figs across Europe.

-

Growing popularity of Mediterranean diets is supporting increased consumption of fresh figs in households and foodservice establishments.

-

Advancements in cultivation, irrigation, and post-harvest handling technologies are improving fruit quality and shelf life.

-

Expanding organized retail and premium fresh produce sections are increasing the availability of fresh figs.

-

Growing demand for healthy snacks and functional foods is creating new opportunities for fresh fig producers.

Segmental Insights

-

Based on varietal, the Black Mission variety segment dominated the Europe fresh figs market in 2025. The segment's leadership is attributed to its rich honey-like flavor, deep purple skin, high nutritional value, and strong consumer preference across European markets.

-

Based on cultivation method, the conventional cultivation segment held the largest share of the Europe fresh figs market in 2025. The segment's dominance is driven by established farming practices, higher production volumes, and widespread commercial cultivation across major fig-producing countries.

-

Based on distribution channel, the retail stores segment accounted for the largest share of the Europe fresh figs market in 2025. The segment's growth is supported by immediate product availability, consumer preference for physical inspection of fresh produce, and the extensive presence of supermarkets and specialty grocery stores.

Regional Insights

-

The Europe fresh figs market is witnessing steady growth due to increasing consumption of healthy fruits, expanding premium produce markets, and improvements in agricultural practices.

-

Spain dominated the Europe fresh figs market in 2025. The country's leadership is supported by favorable climatic conditions, extensive fig cultivation, advanced water management strategies, and strong export capabilities.

-

Turkey remains a significant supplier to the European market due to its large-scale fig production, high-quality fruit, and established export infrastructure.

Competitive Landscape

The Europe fresh figs market is moderately competitive, with producers and distributors focusing on product quality, sustainable cultivation practices, and expansion of distribution networks to strengthen their market positions. Companies are investing in improved farming techniques, post-harvest technologies, and strategic partnerships to meet the growing demand for premium fresh figs across retail and foodservice sectors. Key players operating in the Europe fresh figs market include Dole plc, NatureSweet, Fresh Del Monte Produce Inc., Chiquita Brands International Sàrl, Athos Agricola S.A., Mission Produce, Inc., Alara Agri, Isik Tarim A.S., Hadley Fruit Orchards, Inc., Roland Foods LLC, Earl's Organic Produce, Fresca Group, and Valley Fig Growers, Inc.

Europe Fresh Figs Market Size

The Europe fresh figs market size was valued at USD 2.19 billion in 2025 and is projected to reach USD 2.90 billion by 2034 from USD 2.26 billion in 2026, growing at a CAGR of 3.18 %.

Fresh figs are ripe Ficus carica fruits characterized by their delicate skin and sweet granular interior. This sector is distinct from the dried fig trade due to the extreme perishability and seasonal nature of the fresh product. Fresh figs are prized for their unique texture and nutritional profile, offering high levels of dietary fiber, potassium, and antioxidants. According to Eurostat, the European Union imports substantial quantities of fresh fruit from Mediterranean partner countries, with figs representing a growing niche within this category. The consumption patterns are heavily influenced by cultural traditions in Southern Europe, where figs have been a staple for millennia, while Northern European markets view them as exotic premium items. Climate change impacts are altering production zones, with traditional growers in Spain and Italy facing water stress challenges that affect yield consistency. In Europe, the demand for locally sourced organic produce is rising, with organic retail sales in the EU reaching 49.5 billion euros in 2024 as per the Organic Research Centre. This shift supports sustainable fig farming practices. Retailers are increasingly stocking fresh figs during the late summer and early autumn seasons, capitalizing on consumer interest in seasonal eating. The market dynamics are shaped by the balance between domestic production in Mediterranean states and imports from Turkey and North Africa to meet year round expectations.

MARKET DRIVERS

Rising Consumer Preference for Nutrient Dense Superfoods

The escalating demand for nutrient dense superfoods is majorly contributing to the expansion of the Europe fresh figs market as consumers actively seek natural sources of essential vitamins and minerals. Fresh figs are rich in dietary fiber, calcium, and magnesium, making them an attractive option for health conscious individuals aiming to improve digestive health and bone density. The European Society for Clinical Nutrition and Metabolism emphasizes the importance of increasing fruit and vegetable intake to combat chronic diseases, with recommendations suggesting at least 400 grams of fruits and vegetables per day. Fresh figs provide a convenient and delicious way to meet these dietary goals without added sugars or processing. The antioxidant properties of figs, particularly in darker varieties, appeal to consumers interested in anti-aging and cellular protection. As per Deloitte, 64% of European consumers indicate that over the past 12 months they have become more interested in learning about the influence of food on their health. This trend is particularly strong among Millennials and Gen Z consumers who are well informed about nutritional science. Social media influencers and nutritionists frequently highlight figs as a versatile ingredient for smoothies, salads, and snacks, further boosting their popularity. The natural sweetness of figs also makes them an ideal substitute for refined sugars in healthy desserts, aligning with the broader movement against added sugar consumption. As public health campaigns continue to promote plant based diets, the perception of fresh figs as a wholesome and beneficial food item drives sustained demand across diverse demographic groups in Europe.

Culinary Renaissance and Gourmet Food Trends

The culinary renaissance and the growing popularity of gourmet food trends is further fuelling the Europe fresh figs market growth by elevating the status of figs from a simple snack to a sophisticated gastronomic ingredient. High end restaurants and bistros across Europe increasingly feature fresh figs in seasonal menus, pairing them with artisanal cheeses, cured meats, and balsamic reductions to create complex flavor profiles. The influence of Mediterranean cuisine, which celebrates fresh and simple ingredients, has spread throughout the continent, encouraging chefs to experiment with figs in both savory and sweet dishes. Food festivals and culinary exhibitions often showcase fig based recipes, educating consumers on diverse preparation methods beyond raw consumption. The rise of home cooking enthusiasts, accelerated by digital platforms, has led to a surge in searches for fig recipes. Consumers are eager to replicate restaurant quality meals at home, driving retail sales of fresh figs during peak seasons. The aesthetic appeal of fresh figs also plays a crucial role, as visually striking dishes are highly shared on social media, which is creating a viral effect that boosts demand. Specialty food retailers respond by offering premium varieties such as Black Mission and Brown Turkey figs, catering to discerning palates. This integration into high end dining and home gourmet experiences transforms fresh figs into a symbol of culinary sophistication, driving consistent growth in the market.

MARKET RESTRAINTS

Extreme Perishability and Short Shelf Life

The extreme perishability and short shelf life of fresh figs is impeding the fresh figs market growth in Europe, which is also limiting their availability and increasing supply chain costs. Fresh figs have delicate skin and high moisture content and making them highly susceptible to bruising, mold, and fermentation if not handled with extreme care. The post-harvest life of a fresh fig is typically only two to three days at room temperature, requiring rigorous cold chain management from farm to fork. For instance, high perishability and cold chain gaps act as a significant barrier, particularly for routes between the Mediterranean and the European Union. This high waste factor discourages smaller grocery stores from stocking fresh figs, restricting their presence to larger supermarkets with advanced refrigeration infrastructure. The need for rapid turnover means that retailers must carefully manage inventory to avoid overstocking, which can result in unsold produce being discarded. Consumers often hesitate to purchase fresh figs due to concerns about freshness and potential internal spoilage that is not visible externally. This uncertainty reduces impulse buying and limits market penetration. Additionally, the short harvesting window in many European regions creates periods of scarcity, forcing reliance on imports that may suffer from longer transit times and reduced quality. These logistical challenges constrain the volume of fresh figs that can be efficiently distributed, which is keeping prices higher and accessibility lower compared to more durable fruits.

Climate Vulnerability and Water Scarcity Issues

Climate vulnerability and water scarcity issues pose significant restraints on the Europe fresh figs market by threatening production stability and yield quality. Fig trees, while drought tolerant to some extent, require consistent watering during fruit development to ensure size and sweetness. Southern European countries, which are the primary producers of fresh figs in the region, are experiencing increasingly frequent heatwaves and prolonged droughts. According to the European Environment Agency, water stress affects over 20% of the EU territory, impacting agricultural productivity severely. In Spain and Italy, key fig producing regions have faced irrigation restrictions due to depleted reservoirs, leading to smaller fruit sizes and lower overall harvest volumes. These climatic disruptions cause price volatility and supply inconsistencies, making it difficult for retailers to maintain steady stock levels. Farmers are forced to invest in expensive irrigation technologies or switch to more resilient crops, reducing the area dedicated to fig cultivation. Furthermore, extreme weather events such as heavy rains during harvest can cause fruit splitting and fungal infections, rendering crops unmarketable. The unpredictability of weather patterns complicates long term planning for growers and distributors. As climate change intensifies, the risk of crop failure increases, threatening the sustainability of local fresh fig production. This environmental pressure forces greater reliance on imports from non-European regions, which may not meet the same quality or sustainability standards expected by European consumers, thereby restraining market growth.

MARKET OPPORTUNITIES

Expansion of Organic and Sustainable Farming Practices

The expansion of organic and sustainable farming practices presents a substantial opportunity for the Europe fresh figs market as consumers increasingly prioritize environmentally friendly and chemical free produce. Organic figs command a premium price due to the rigorous standards required for certification, which prohibits the use of synthetic pesticides and fertilizers. As per the Organic Research Centre, the European organic market continues to grow, with retail sales in the EU reaching 49.5 billion euros in 2024. This trend creates a lucrative niche for fig growers who adopt agroecological methods that enhance soil health and biodiversity. Organic figs are perceived as safer and healthier, appealing to health conscious families and individuals with sensitivities to chemical residues. Retailers are expanding their organic fruit sections, providing dedicated shelf space for certified organic figs during the season. Direct to consumer models, such as community supported agriculture and farmers markets, allow growers to sell organic figs directly to buyers, ensuring fair prices and building customer loyalty. Sustainability certifications also open doors to export opportunities within Europe, where regulatory support for green agriculture is strong. Governments offer subsidies and technical assistance to farmers transitioning to organic practices, reducing financial barriers. By positioning fresh figs as a symbol of sustainable luxury, producers can differentiate their products in a competitive market. This alignment with consumer values and regulatory incentives drives growth in the organic segment, offering higher profit margins and long term viability for fig cultivators.

Integration into Premium Health and Wellness Products

The integration of fresh figs into premium health and wellness products offers a promising opportunity for the regional market expansion. Food manufacturers are developing innovative products such as fig infused yogurts, energy bars, and functional beverages that leverage the natural sweetness and nutritional benefits of figs. Fresh fig purees and extracts are being used as natural sweeteners in clean label products, replacing artificial additives and refined sugars. This application appeals to consumers seeking transparent and wholesome ingredients. Collaborations between fig growers and health food brands can lead to exclusive product lines that highlight the origin and quality of the fruit. Additionally, the spa and cosmetics industries are exploring fig extracts for their moisturizing and antioxidant properties, creating cross sector demand. Wellness retreats and luxury hotels incorporate fresh figs into detox menus and spa treatments, enhancing their brand image and attracting affluent clients. The versatility of figs allows for creative product development that caters to specific dietary needs, such as gluten free and vegan options. By expanding into value added products, the fresh figs market can reduce dependency on seasonal fresh sales and create year round revenue streams. This innovation drives consumer engagement and opens new distribution channels in health stores and online wellness platforms.

MARKET CHALLENGES

Labor Shortages in Agricultural Sector

Labor shortages in the agricultural sector present a major challenge to the Europe fresh figs market by hindering efficient harvesting and increasing production costs. Fig harvesting is labor intensive as the fruit must be picked by hand to prevent bruising and ensure optimal ripeness. Many European countries face a declining agricultural workforce due to urbanization and an aging farmer population. According to the European Commission, the agricultural sector struggles to attract young workers, leading to reliance on seasonal migrant labor. Recent geopolitical events and pandemic related restrictions have disrupted the flow of seasonal workers, causing delays in harvesting and significant crop losses. Without timely picking, figs overripen and fall, becoming unsellable. The scarcity of labor drives up wages, increasing the cost of production and final retail prices. Mechanization of fig harvesting is limited due to the delicate nature of the fruit, leaving growers dependent on manual labor. This vulnerability exposes the supply chain to disruptions and inefficiencies. Small scale farmers are particularly affected as they lack the resources to compete for labor with larger agribusinesses. The resulting inconsistency in supply affects retailer confidence and consumer availability. Addressing this challenge requires policy interventions to improve working conditions and attract domestic workers, but progress is slow. Until labor stability is achieved, the fresh figs market will face ongoing operational hurdles.

Complex Regulatory Standards for Imports

Complex regulatory standards for imports pose a significant challenge to the Europe fresh figs market by creating barriers to entry and increasing compliance costs for non EU suppliers. The European Union enforces strict maximum residue limits for pesticides and stringent phytosanitary requirements to protect consumer health and local ecosystems. Importers must provide detailed documentation and undergo rigorous inspections at border control points, which can delay shipments and increase the risk of spoilage for perishable goods like fresh figs. According to the European Commission, numerous consignments of fresh fruits are rejected annually due to non-compliance with safety standards. These rejections result in financial losses and damage to supplier reputations. Navigating the evolving regulatory landscape requires significant investment in testing and certification, which can be prohibitive for small exporters from developing countries. Changes in trade policies and tariffs further complicate the import process, affecting pricing and availability. Domestic producers benefit from fewer regulatory hurdles, but they cannot meet total demand, leading to reliance on imports that face these barriers. The complexity of compliance discourages new suppliers from entering the market, limiting competition and variety. Retailers must carefully vet their supply chains to ensure compliance, adding administrative burdens. These regulatory challenges restrict the flow of fresh figs into Europe, which is impacting market growth and consumer choice.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.18% |

| Segments Covered | By Varietal, Cultivation Method, Distribution Channel, Packaging, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Dole plc, NatureSweet, Fresh Del Monte Produce Inc., Chiquita Brands International Sàrl, Athos Agricola S.A., Mission Produce, Inc., Alara Agri, Isik Tarim A.S., Hadley Fruit Orchards, Inc., Roland Foods LLC, Earl's Organic Produce, Fresca Group, and Valley Fig Growers, Inc. |

SEGMENTAL ANALYSIS

By Varietal Insights

The black mission variety segment held the major share of the European market in 2025 due to its rich, honey like flavor and deep purple skin which appeals strongly to European consumers. This variety is widely recognized for its intense sweetness and jammy texture, which is making it ideal for both fresh consumption and culinary applications such as pairing with cheeses or incorporating into desserts. The visual appeal of the dark skin contrasts beautifully with the pink interior, enhancing its popularity in high end gastronomy and social media driven food trends. Chefs prefer this variety for its ability to retain structure when grilled or roasted, adding versatility to menu planning. Consumer surveys indicate that a majority of fig buyers in France and Germany specifically seek out dark skinned varieties for their perceived richness and premium quality. The widespread availability of Black Mission figs in major supermarket chains during the peak season ensures consistent consumer access. Its adaptability to various climate conditions in Mediterranean growing regions allows for stable supply volumes. The strong brand recognition of Black Mission figs as a premium product drives repeat purchases and establishes it as the default choice for many shoppers unfamiliar with other varietals.

On the other hand, the panache variety segment is anticipated to register the fastest CAGR in the European market over the forecast period owing to its unique striped appearance and gourmet appeal. The distinctive green and yellow striped skin makes it visually striking, which is attracting attention in specialty stores and high end restaurants. Chefs and food stylists favor Panache figs for their artistic value in plating, leading to increased visibility on social media platforms. The novelty factor drives curiosity among consumers who are eager to try new and exotic fruit varieties. This digital exposure translates into higher retail demand as shoppers seek to replicate professional dishes at home. Specialty retailers in urban centers like London and Paris have expanded their stock of Panache figs to meet this growing interest. The limited availability of this variety creates a sense of exclusivity, encouraging premium pricing and early adoption by trendsetters. As consumers become more adventurous in their food choices, the demand for visually unique produce like Panache figs continues to rise rapidly. This aesthetic differentiation positions Panache as a standout choice in the competitive fresh fruit market.

By Cultivation Method Insights

The conventional cultivation segment dominated the market with the major share of the regional market in 2025 and is estimated to remain the leading method in the Europe fresh figs market over the forecast period due to its cost efficiency and well established supply chains. Traditional farming methods allow for higher yields per hectare compared to organic or hydroponic systems, resulting in lower production costs. This economic advantage translates to affordable retail prices, making conventional figs accessible to a broader consumer base. The majority of fig imports from Turkey and North Africa are conventionally grown, ensuring a steady supply throughout the season. According to international trade statistics, a high proportion of fresh figs sold in European supermarkets are produced using conventional methods. The familiarity of conventional farming practices among growers reduces operational risks and ensures consistent quality. Distributors rely on the predictable volume of conventional harvests to plan logistics and inventory. The established infrastructure for pesticide application and fertilization supports large scale production needed to meet mass market demand. While consumer interest in organic options is growing, price sensitivity keeps conventional figs as the primary choice for most households. The economies of scale achieved by large commercial farms further reinforce the dominance of this segment. Retailers prioritize conventional figs for their reliability and margin stability. This structural advantage ensures that conventional cultivation continues to lead the market despite emerging alternatives.

On the other end, the organic cultivation segment is the fastest growing segment in the Europe fresh figs market and is expected to showcase the fastest CAGR in the European market during the forecast period owing to the growing consumer demand for chemical free and environmentally friendly produce. European shoppers are increasingly concerned about pesticide residues in fresh fruits, leading to a shift toward organic options. According to the European Commission, the organic food market has shown consistent growth, with fresh fruits being a key category. Organic figs are perceived as safer and healthier, appealing to families and health conscious individuals. Retailers are expanding their organic sections to meet this demand, offering certified organic figs during the season. The willingness of consumers to pay a premium for organic certification supports market growth. Surveys indicate that many organic buyers prioritize fruits that are free from synthetic chemicals. This trend is particularly strong in Northern European countries where environmental awareness is high. The transparency of organic labeling builds trust and encourages trial. As education on the benefits of organic farming spreads, more consumers are likely to switch from conventional to organic figs. This shift in preference drives the rapid expansion of the organic segment.

By Distribution Channel Insights

The retail stores segment led the market by holding the leading share of the European market in 2025 due to immediate accessibility and consumer trust in physical inspection. Shoppers prefer to select fresh figs personally to check for ripeness and quality, a process that is difficult to replicate online. Supermarkets and grocery chains offer a wide variety of figs, allowing consumers to compare prices and varieties easily. According to retail data, over 75% of fresh fig sales occur in physical stores, reflecting the importance of tactile selection. The presence of figs in prominent produce sections increases visibility and impulse purchases. Retailers often provide sampling opportunities, encouraging trial and educating consumers on usage. The established reputation of major supermarket brands assures customers of food safety and quality standards. Regular shoppers integrate fig purchases into their weekly grocery routines, ensuring steady demand. The convenience of one stop shopping for all household needs supports the dominance of retail stores. Promotional displays and seasonal campaigns further boost sales during peak periods. This direct interaction with the product builds consumer confidence and loyalty.

However, the online retailers segment is estimated to record a prominent CAGR in the European market during the forecast period due to the convenience of home delivery services. Busy consumers appreciate the ability to order fresh produce online and have it delivered to their doorstep, saving time and effort. The growth of e commerce grocery platforms has made fresh figs more accessible to those who cannot visit physical stores regularly. According to industry analysis, online grocery sales in Europe have grown by 20% annually, with fresh fruits being a significant category. The ease of browsing and comparing different fig varieties online enhances the shopping experience. Subscription services offer regular deliveries of seasonal fruits, including figs, ensuring consistent supply for households. The ability to schedule deliveries at convenient times adds to the appeal. Younger demographics are particularly inclined toward online shopping for its speed and flexibility. The expansion of last mile delivery networks has improved the reliability of fresh produce shipments. This convenience factor drives rapid adoption of online channels for fresh fig purchases.

REGIONAL ANALYSIS

Spain Fresh Figs Market Analysis

Spain held the dominant share of the European market in 2025 and is expected to maintain its market dominance in the coming years due to its commitment to advanced water management strategies. Spain is one of the largest producers and exporters in the region. The country’s favorable climate allows for extensive cultivation of high quality figs, particularly in regions like Extremadura and Andalusia. Spanish figs are renowned for their sweetness and size, making them highly sought after in international markets. As per agricultural statistics, Spain produces tens of thousands of tonnes of fresh figs annually, supplying a significant portion of European demand. The government supports modernization of irrigation systems to combat water scarcity, ensuring sustainable production. Spanish exporters have established strong relationships with retailers across Northern Europe, leveraging efficient logistics networks. The domestic market also consumes a substantial amount of fresh figs, driven by traditional culinary preferences. Local festivals celebrate the fig harvest, promoting cultural appreciation and consumption. The focus on quality certifications enhances the reputation of Spanish figs globally. Spain’s strategic location facilitates quick transport to key European markets. Its leadership in production and export solidifies its central role in the regional market.

Italy Fresh Figs Market Analysis

Italy is likely to see steady growth over the next few years as it further aligns with sustainable farming directives and occupies a prestigious position in the Europe fresh figs market characterized by its diverse varieties and strong culinary heritage. Italian figs, such as the Dottato and Brogiotto, are prized for their unique flavors and textures. The country produces approximately 50,000 tonnes of fresh figs annually, with significant contributions from regions like Calabria and Campania. Italian consumers have a deep cultural connection to figs, using them in traditional desserts and savory dishes. The emphasis on local and seasonal produce supports domestic sales. Italy is also a major exporter of premium figs to neighboring countries, capitalizing on its reputation for quality. The integration of figs into the Mediterranean diet promotes regular consumption. Government initiatives support organic farming, increasing the availability of certified organic figs. Italian retailers feature fresh figs prominently during the autumn season. The country’s focus on gastronomic excellence drives demand for high quality varieties. Italy’s combination of tradition and innovation sustains its strong market presence.

France Fresh Figs Market Analysis

France is projected to see continued investment in precision systems as national environmental standards tighten and maintains a significant position in the Europe fresh figs market driven by its gourmet culture and demand for premium produce. French consumers value the aesthetic and flavor qualities of fresh figs, integrating them into high end cuisine. The country imports a substantial volume of figs to supplement domestic production, which is concentrated in the southern regions. According to trade data, France is one of the top importers of fresh figs in Europe, sourcing from Spain and Turkey. The popularity of figs in patisserie and cheese pairings boosts retail sales. French retailers focus on offering diverse varieties to cater to discerning palates. The trend toward organic and locally sourced foods supports domestic growers. Parisian markets are known for their high quality fresh produce, including exotic fig varieties. The influence of French culinary traditions spreads across Europe, driving demand for premium figs. France’s role as a trendsetter in gastronomy enhances the status of fresh figs. Its sophisticated market dynamics support steady growth.

Germany Fresh Figs Market Analysis

Germany is expected to experience significant technological advancements and increased adoption of digital irrigation tools in the coming years and holds a growing position in the Europe fresh figs market characterized by increasing health consciousness and import dependence. As a non producing country for significant volumes, Germany relies heavily on imports from Mediterranean states. German consumers are increasingly incorporating figs into their diets for their nutritional benefits. The retail sector offers a wide range of fresh figs, with a focus on organic options. According to import statistics, Germany imports over 30,000 tonnes of fresh figs annually. The demand for convenient and healthy snacks drives sales in supermarkets. Online grocery platforms are expanding their fresh fruit offerings, including figs. German shoppers prioritize quality and sustainability, influencing supplier practices. The rise of veganism supports the consumption of plant based foods like figs. Retailers educate consumers on the benefits of figs through marketing campaigns. Germany’s strong economy supports premium pricing for high quality produce. Its role as a major importer influences regional trade flows.

United Kingdom Fresh Figs Market Analysis

The United Kingdom is poised for consistent market expansion as farmers adapt to changing climate conditions over the next few years and occupies a notable position in the Europe fresh figs market driven by culinary trends and import reliance. The UK does not produce fresh figs commercially, relying entirely on imports from Spain, Turkey, and other regions. British consumers have embraced figs as a gourmet ingredient, influenced by media and celebrity chefs. Retailers such as Waitrose and Marks and Spencer offer premium fresh figs during the season. According to trade data, the UK imports approximately 25,000 tonnes of fresh figs annually. The demand for exotic fruits is strong in urban centers. The trend toward healthy eating boosts fig consumption. Online grocery services facilitate access to fresh figs for busy consumers. The UK market is sensitive to price and quality fluctuations. Trade adjustments have impacted supply chains, but demand remains resilient. The cultural appreciation for Mediterranean cuisine supports steady growth. The UK’s role as a key importer shapes market dynamics.

COMPETITIVE LANDSCAPE

The competition in the Europe fresh figs market is characterized by a mix of large international importers and specialized regional producers who compete on quality freshness and sustainability credentials. Major players leverage their extensive distribution networks to ensure wide availability and consistent supply throughout the season. Smaller niche producers differentiate themselves by offering unique heirloom varieties and organic certifications that appeal to discerning consumers. Price competition is moderate due to the premium nature of fresh figs but intensifies during peak harvest periods when supply is abundant. Innovation in packaging and preservation technology serves as a key differentiator among competitors seeking to reduce waste and enhance shelf life. Regulatory compliance regarding pesticide residues and food safety standards creates high entry barriers favoring established operators with robust quality control systems. Collaboration between growers and retailers often defines the market dynamics as they work together to promote consumption and educate consumers. Geographic specialization allows Southern European producers to dominate local markets while importers control flows from North Africa and Turkey. Overall competitiveness hinges on balancing operational efficiency with high quality standards and sustainable practices in this sensitive perishable goods sector.

KEY MARKET PLAYERS

Some of the notable key players in the Europe fresh figs market are

- Dole plc

- Nature Sweet

- Fresh Del Monte Produce Inc.

- Chiquita Brands International Sàrl

- Athos Agricola S.A.

- Mission Produce, Inc.

- Alara Agri

- Isik Tarim A.S.

- Hadley Fruit Orchards, Inc.

- Roland Foods LLC

- Earl's Organic Produce

- Fresca Group

- Valley Fig Growers, Inc.

Top Players in the Market

- Nature Sweet has established a significant presence in the European fresh figs market by focusing on premium quality and sustainable cultivation practices. The company supplies high grade fresh figs to major retail chains across the continent, emphasizing consistent flavor and texture. Recent actions include the expansion of their greenhouse facilities in Southern Europe to extend the harvesting season and reduce reliance on imports. Nature Sweet also launched a traceability program that allows consumers to scan codes on packaging to learn about the origin and farming methods of their figs. This transparency builds trust and aligns with consumer demand for ethical sourcing. The company collaborates with local agronomists to optimize water usage and minimize environmental impact. By prioritizing quality control and sustainability Nature Sweet strengthens its reputation as a reliable supplier of premium fresh produce in the competitive European market.

- Mission Produce contributes to the Europe fresh figs market through its extensive global supply chain and expertise in perishable fruit logistics. Although primarily known for avocados the company has diversified its portfolio to include high value fruits like fresh figs. They leverage their advanced cold chain infrastructure to ensure that figs arrive at European destinations in optimal condition. Recent initiatives involve partnering with specialized growers in Turkey and Spain to secure exclusive access to premium varieties such as Black Mission and Calimyrna. Mission Produce also invests in ripening technology that enhances the shelf life of fresh figs during transit. Their strategic alliances with European distributors enable efficient market penetration and consistent availability. By applying their logistical excellence to the fig sector Mission Produce ensures high quality standards and strengthens its position as a key player in the European fresh fruit industry.

- Fresca Group plays a vital role in the Europe fresh figs market by acting as a leading importer and distributor of specialty fruits. The company sources fresh figs from diverse growing regions to provide year round availability to retailers and food service providers. Fresca Group focuses on building strong relationships with growers to ensure consistent quality and fair trade practices. Recent actions include the development of branded packaging solutions that highlight the nutritional benefits and culinary uses of fresh figs. They also participate in international food exhibitions to showcase new varieties and educate buyers on proper handling techniques. The group invests in digital platforms that streamline ordering and inventory management for their clients. By combining sourcing expertise with marketing innovation Fresca Group enhances the visibility and appeal of fresh figs. Their commitment to quality and service reliability strengthens their market position across multiple European countries.

Top Strategies Used by Key Market Participants

Key players in the Europe fresh figs market employ strategies focused on supply chain optimization and product differentiation to maintain competitive advantages. Companies invest in advanced cold chain technologies to minimize spoilage and extend the shelf life of highly perishable fresh figs. Strategic partnerships with local growers in Mediterranean regions ensure consistent supply and adherence to quality standards. Brands emphasize organic certification and sustainable farming practices to appeal to health conscious and environmentally aware consumers. Marketing efforts highlight the unique flavor profiles and culinary versatility of specific fig varieties to drive consumer interest. Retailers collaborate with suppliers to create attractive packaging that protects the fruit while enhancing visual appeal. Diversification of sourcing regions helps mitigate risks associated with climate variability and seasonal fluctuations. Digital traceability systems are implemented to provide transparency and build consumer trust. These multifaceted approaches enable participants to navigate logistical challenges while capturing growth in both retail and food service segments across the diverse European landscape.

MARKET SEGMENTATION

This research report on the Europe fresh figs market has been segmented and sub-segmented based on categories.

By Varietal

- Kadota

- Calimyrna

- Black Mission

- Celeste

- Panache

By Cultivation Method

- Conventional

- Organic

- Hydroponic

By Distribution Channel

- Retail Stores

- Wholesale Markets

- Online Retailers

- Direct-to-Consumer

By Packaging

- Fresh Bulk

- Fresh Packed

- Dried

- Preserved

By Application

- Fresh Consumption

- Processed Foods

- Beverages

- Pharmaceuticals

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the current size of the Europe fresh figs market?

The Europe fresh figs market is witnessing steady growth, driven by rising consumer demand for fresh, nutritious fruits and increasing awareness of their health benefits.

2. What factors are driving the growth of the Europe fresh figs market?

Growing health consciousness, increasing consumption of fresh fruits, expanding retail distribution, and rising demand for organic produce are key factors driving market growth.

3. Which countries are the major producers of fresh figs in Europe?

Turkey, Spain, Greece, Italy, and Portugal are among the leading producers and suppliers of fresh figs serving the European market.

4. Which fig variety is most popular in the Europe fresh figs market?

Black Mission figs are among the most popular varieties due to their sweet taste, rich nutritional profile, and wide consumer acceptance.

5. How is the organic fresh figs segment performing in Europe?

The organic segment is growing rapidly as consumers increasingly prefer chemical-free and sustainably cultivated fruits.

6. Which distribution channel dominates the Europe fresh figs market?

Retail stores, including supermarkets and hypermarkets, account for the largest share due to their wide product availability and strong consumer reach.

7. What are the major applications of fresh figs?

Fresh figs are primarily consumed as fresh fruit and are also used in processed foods, beverages, bakery products, and pharmaceutical applications.

8. What challenges does the Europe fresh figs market face?

The market faces challenges such as the short shelf life of fresh figs, seasonal production, supply chain complexities, and fluctuating weather conditions.

9. What is the future outlook for the Europe fresh figs market?

The market is expected to experience steady growth over the coming years, supported by increasing consumer preference for healthy foods, expanding organic cultivation, and improvements in cold-chain logistics.

10. Which trends are shaping the Europe fresh figs market?

Growing demand for organic figs, sustainable packaging, premium fruit offerings, and direct-to-consumer sales are key market trends.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com