Europe Fresh Herbs Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Culinary Herbs, Medicinal Herbs, Aromatic Herbs), Category, Distribution Channel, And Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech, Republic Rest Of Europe) - Industry Analysis (2026 To 2034)

Europe Fresh Herbs Market Report Summary

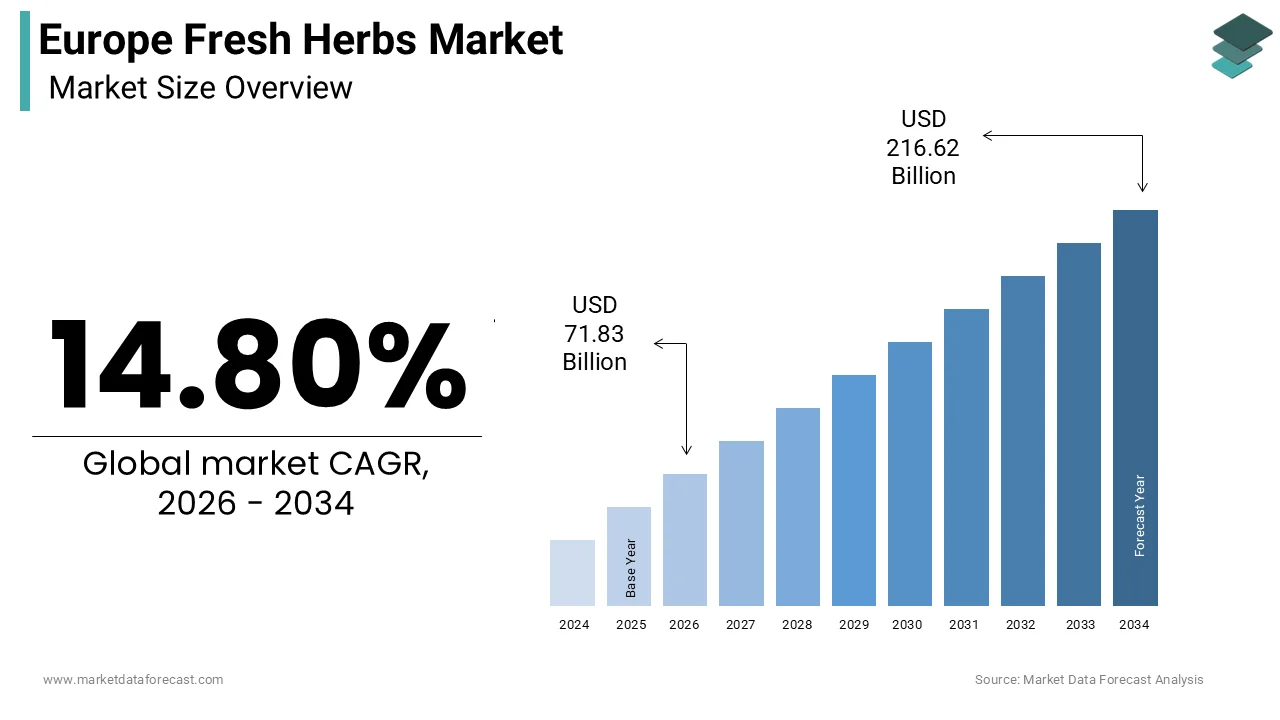

The Europe fresh herbs market was valued at USD 62.57 billion in 2025 and is projected to reach USD 216.62 billion by 2034, growing from USD 71.83 billion in 2026 at a CAGR of 14.80% during the forecast period. Market growth is driven by increasing consumer preference for fresh and natural ingredients, rising demand for healthy and organic foods, expanding use of herbs in culinary applications, and growing adoption of fresh herbs by the foodservice industry. Advances in greenhouse cultivation, vertical farming, and sustainable agricultural practices are further supporting market expansion.

Key Market Trends

- Rising demand for fresh, organic, and sustainably grown herbs.

- Increasing use of fresh herbs in home cooking and foodservice applications.

- Growing consumer preference for clean-label and natural food ingredients.

- Expansion of controlled-environment agriculture and greenhouse cultivation.

- Rising investments in precision farming and sustainable herb production.

Segmental Insights

- Based on Type, the culinary herbs segment dominated the Europe fresh herbs market in 2025 due to their widespread use in traditional and contemporary European cuisines. Growing consumer interest in fresh flavors, healthy cooking, and gourmet food preparation continues to support segment growth.

- Based on Category, the conventional herbs segment accounted for the largest share of the market in 2025, owing to their affordability, extensive availability, and strong presence across supermarkets, hypermarkets, and foodservice establishments.

- Based on Distribution Channel, the supermarkets and hypermarkets segment dominated the Europe fresh herbs market in 2025 due to their broad product assortment, established retail networks, and convenience of one-stop shopping.

Regional Insights

- Germany held a leading position in the Europe fresh herbs market in 2025, supported by strong demand for organic produce, advanced retail infrastructure, and increasing consumer preference for sustainable and locally sourced herbs.

- France maintained a significant market share due to its rich culinary heritage, extensive agricultural production, and strong demand for premium fresh herbs in households and restaurants.

- Italy remained a key market owing to its Mediterranean cuisine, extensive herb cultivation, and growing consumption of fresh herbs in domestic cooking and food processing.

- The United Kingdom accounted for a notable share of the market, driven by a diverse consumer base, expanding retail distribution, and increasing demand for fresh and organic culinary ingredients.

- Spain played a major role in the Europe fresh herbs market as one of the region's leading producers and exporters of Mediterranean herbs, supported by favorable climatic conditions and strong agricultural output.

- The Netherlands maintained a strategic position due to its advanced greenhouse farming technologies, efficient logistics infrastructure, and role as a major distribution hub for fresh produce across Europe.

- Sweden is expected to witness steady growth, driven by increasing health awareness, rising demand for organic foods, and strong consumer interest in sustainable agriculture.

- Denmark is projected to experience healthy growth due to high organic food consumption, innovative retail practices, and growing demand for locally sourced fresh herbs.

- Switzerland held a premium position in the market, supported by high consumer purchasing power, strong demand for premium-quality herbs, and strict food quality standards.

- Turkey remained a significant producer and exporter of fresh herbs, benefiting from favorable growing conditions, rich culinary traditions, and expanding export opportunities across Europe.

- The Czech Republic is expected to witness gradual market growth, supported by increasing consumer awareness of healthy diets, expanding retail availability, and rising demand for locally produced herbs.

- The Rest of Europe, including Poland, Austria, Belgium, and Portugal, contributes significantly to the regional market through increasing herb cultivation, expanding retail distribution, and growing consumer demand for fresh culinary herbs.

Competitive Landscape

The Europe fresh herbs market is highly competitive, with companies focusing on sustainable cultivation, greenhouse production, organic certification, and innovative farming technologies. Market participants are investing in advanced breeding techniques, controlled-environment agriculture, product quality improvement, and expansion of distribution networks to strengthen their competitive positions.

Key players operating in the Europe fresh herbs market include Bayer AG, Syngenta Group, BASF SE, Groupe Limagrain, Bejo Zaden B.V., Enza Zaden, Rijk Zwaan Zaadteelt en Zaadhandel B.V., Sakata Seed Corporation, Takii & Co., Ltd., HM.CLAUSE, KWS SAAT SE & Co. KGaA, Vilmorin & Cie, East-West Seed, Johnny's Selected Seeds, and Thompson & Morgan.

Europe Fresh Herbs Market Size

The Europe fresh herbs market size was calculated at USD 62.57 billion in 2025 and is anticipated to reach USD 216.62 billion by 2034, from USD 71.83 billion in 2026, growing at a CAGR of 14.80% during the forecast period.

The fresh herbs are aromatic leafy plants that are utilized primarily for culinary, medicinal, and aesthetic purposes. These botanical products are distinct from dried herbs due to their perishable nature and requirement for cold chain logistics to maintain potency and flavor profiles. The consumption patterns in this region are deeply rooted in traditional Mediterranean cuisines, where fresh ingredients are preferred over processed alternatives. Many European households purchase fresh produce at least once a week, indicating a strong baseline demand for perishable agricultural goods. According to the study, the average annual consumption of vegetables and legumes in Western Europe stands at 130 kilograms per capita, providing a substantial base for herb integration into daily diets. Consumer awareness regarding nutritional benefits has surged with studies from the European Food Safety Authority confirming that fresh herbs contain higher concentrations of antioxidants compared to their dried counterparts. This biological advantage drives preference among health-conscious demographics.

MARKET DRIVERS

Rising Consumer Preference for Healthy and Organic Culinary Ingredients

The escalating demand for healthy and organic culinary ingredients is amplifying the growth of the Europe fresh herbs market. Consumers across the continent are increasingly prioritizing wellness and nutritional value in their dietary choices, leading to a significant shift away from processed foods toward whole, natural ingredients. Fresh herbs are recognized for their rich content of vitamins, minerals, and antioxidants, which contribute to overall health and disease prevention. This trend is particularly pronounced among millennials and Generation Z consumers, who actively seek transparency in food sourcing and production methods. The integration of fresh herbs into daily meals allows individuals to enhance flavor without adding excessive salt or unhealthy fats aligning with public health recommendations. Furthermore, the rise of plant-based diets has amplified the need for flavorful alternatives to meat and dairy products, with fresh herbs playing a pivotal role in creating satisfying vegetarian and vegan dishes. Retailers have responded by expanding their organic sections and offering certified fresh herb varieties that command premium prices. This consumer behavior is supported by extensive marketing campaigns from health organizations that emphasize the anti-inflammatory and digestive benefits of herbs like mint and ginger.

Expansion of the Food Service Industry and Gourmet Dining Trends

The rapid expansion of the food service industry, coupled with evolving gourmet dining trends, is additionally accelerating the growth of the Europe fresh herbs market. Restaurants, cafes, and catering services increasingly incorporate fresh herbs into their menus to differentiate their offerings and appeal to discerning customers, who value authenticity and high-quality ingredients. Chefs and culinary professionals prefer fresh herbs over dried variants due to their superior aroma, vibrant color, and intense flavor profile, which are essential for creating visually appealing and tasty dishes. The popularity of international cuisines, such as Italian, Thai, and Mexican, has further diversified the range of herbs required, including basil, cilantro, lemongrass, and oregano. Tourism activities in Europe contribute significantly to the hospitality sector, with millions of visitors seeking authentic local dining experiences that heavily feature fresh regional produce. Additionally, the rise of fast casual dining concepts has increased the volume of fresh herb usage as these establishments focus on quick service without compromising on ingredient quality. Supply chains have adapted to meet the consistent needs of commercial kitchens, ensuring the timely delivery of perishable goods. The emphasis on farm-to-table initiatives by many upscale restaurants also drives direct partnerships with local herb growers, reducing transit time and preserving freshness.

MARKET RESTRAINTS

High Perishability and Complex Cold Chain Logistics Requirements

The inherent high perishability of fresh herbs, coupled with complex cold chain logistics requirements, is impeding the growth of the Europe fresh herbs market. Fresh herbs have a short shelf life, often lasting only a few days after harvest if not stored under optimal conditions of temperature and humidity. Maintaining these conditions throughout the supply chain from farm to retail shelf requires sophisticated infrastructure and continuous monitoring, which increases operational costs substantially. Temperature fluctuations during transportation can lead to wilting, discoloration, and loss of aromatic compounds, rendering the product unsellable. Small and medium-sized farmers often lack the financial resources to invest in advanced refrigeration technologies and controlled atmosphere storage facilities, limiting their ability to access distant areas. The carbon footprint associated with refrigerated transport is significantly higher than that of ambient shipping, raising sustainability concerns among environmentally conscious stakeholders. Furthermore, labor shortages in the logistics sector exacerbate delays in delivery schedules, increasing the risk of spoilage. Retailers face challenges in managing inventory levels accurately, leading to either stockouts or excess waste. The stringent regulatory standards for food safety in the European Union require meticulous documentation and tracking, which adds administrative burdens to suppliers. These logistical complexities result in higher retail prices for fresh herbs, potentially deterring price-sensitive consumers.

Stringent Regulatory Compliance and Pesticide Residue Limits

The stringent regulatory compliance and strict limits on pesticide residues are also inhibiting the growth of the Europe fresh herbs market. The European Union enforces rigorous standards under the Maximum Residue Levels regulation, which dictates the allowable amounts of pesticide residues in food products to protect consumer health. Compliance with these regulations requires farmers to adopt integrated pest management strategies and reduce reliance on chemical pesticides, which can be costly and technically demanding. The regular monitoring programs detect non-compliance in a small but significant percentage of herb samples, leading to product recalls and financial penalties for suppliers. The complexity of navigating varying national regulations within member states adds another layer of difficulty for exporters and distributors. Small-scale growers often struggle to afford the certification processes and laboratory testing required to prove compliance, thereby limiting their market access. Additionally, the increasing consumer demand for organic and residue-free herbs forces conventional farmers to transition to organic farming practices, which involve a three-year conversion period during which yields may decline, and costs increase. The lack of harmonized interpretation of regulations across different European countries can create trade barriers and inconsistencies in market entry requirements. These regulatory pressures necessitate continuous investment in training technology and quality control systems, placing a financial burden on market participants.

MARKET OPPORTUNITIES

Integration of Vertical Farming and Controlled Environment Agriculture

The integration of vertical farming and controlled environment agriculture presents a transformative opportunity for the Europe fresh herbs market by addressing land scarcity and climate variability. Urbanization in Europe has led to limited availability of arable land near major consumption centers, prompting innovators to adopt space-efficient farming techniques. Vertical farms utilize stacked layers in controlled indoor environments, allowing for year-round production of fresh herbs regardless of external weather conditions. According to the European Association for Vertical Farming, the sector has seen a 30 percent annual growth rate in installed capacity over the past five years, driven by technological advancements and investment interest. These systems use significantly less water than traditional agriculture, with some facilities reporting up to 95 percent reduction in water usage through recirculation systems. The proximity of vertical farms to urban markets reduces transportation distances, thereby lowering carbon emissions and ensuring fresher products reach consumers faster. Major cities such as Berlin, Paris, and London have witnessed the emergence of commercial vertical farming operations supplying local supermarkets and restaurants. Data from the Joint Research Centre of the European Commission highlights that controlled environment agriculture can increase yield per square meter by up to 10 times compared to open field farming. This efficiency attracts investors looking for sustainable and scalable agricultural solutions. Furthermore, the ability to precisely control nutrients and light spectra enables the production of herbs with enhanced flavor profiles and nutritional content. As energy costs stabilize and renewable energy sources become more accessible, the economic viability of vertical farming improves. This technological shift offers a resilient supply chain model that mitigates risks associated with climate change and seasonal fluctuations, positioning it as a key growth avenue for the market.

Growth of E-Commerce Platforms and Direct-to-Consumer Models

The rapid growth of e-commerce platforms and direct-to-consumer models offers a substantial opportunity for expanding the reach and accessibility of the Europe fresh herbs market. Digital transformation in the grocery sector has enabled consumers to purchase fresh produce online with increasing confidence due to improved logistics and packaging solutions. According to Eurostat, the share of individuals aged 16 to 74 who bought goods or services online in the European Union reached 74 percent in recent years, indicating a robust digital adoption rate. Specialty online retailers and subscription services now offer curated boxes of fresh herbs delivered directly to households, ensuring convenience and a consistent supply. These platforms often provide detailed information about the origin, farming practices, and nutritional benefits of the herbs, appealing to informed consumers. The direct-to-consumer model eliminates intermediaries, allowing farmers to retain a larger portion of the profit margin while offering competitive prices to buyers. Data from the European E-Commerce Association shows that online food and personal care sales grew by 15 percent annually, driven by changing consumer habits post-pandemic. Mobile applications facilitate easy ordering and personalized recommendations, enhancing customer engagement and loyalty. Additionally, social media marketing plays a crucial role in educating consumers about the uses and benefits of various herbs, driving impulse purchases and trials. Partnerships between tech companies and local growers enable real-time inventory management and reduced waste through predictive analytics. This digital ecosystem supports niche players and artisanal producers who can reach broader audiences without the need for extensive physical retail presence. The convenience factor, combined with transparent sourcing information, strengthens consumer trust and fosters long-term relationships between producers and buyers in the digital marketplace.

MARKET CHALLENGES

Vulnerability to Climate Change and Extreme Weather Events

The vulnerability of fresh herb production to climate change and extreme weather events constitutes a major challenge for the Europe fresh herbs market. Rising temperatures, unpredictable rainfall patterns, and increased frequency of droughts and floods disrupt agricultural cycles and reduce crop yields. According to the European Environment Agency, climate-related extremes have caused significant economic losses in the agricultural sector, with some regions experiencing up to a 20 percent reduction in crop productivity during severe weather years. Herbs such as basil and cilantro are particularly sensitive to temperature fluctuations and water stress, requiring precise growing conditions that are becoming harder to maintain outdoors. Soil degradation and erosion further complicate cultivation efforts, reducing the fertility of land traditionally used for herb farming. Data from the Intergovernmental Panel on Climate Change indicates that Southern Europe is projected to face heightened water scarcity, affecting irrigation capabilities essential for herb growth. Farmers face increased uncertainty in planning planting schedules and harvesting timelines, leading to supply inconsistencies and price volatility. The cost of implementing adaptive measures such as irrigation systems and shade structures places additional financial pressure on producers, especially smallholders. Moreover, the spread of new pests and diseases due to warmer climates threatens crop health, requiring more intensive management practices. These environmental stresses compromise the quality and quantity of fresh herbs available in the market. Retailers and consumers experience the downstream effects through sporadic availability and higher prices. Addressing these climatic challenges requires significant investment in research and development of resilient crop varieties and sustainable farming practices. Without effective adaptation strategies, the long-term stability of the fresh herbs supply chain remains at risk, impacting market growth and food security.

Intense Price Competition from Substitute Products

Intense price competition from substitute products such as dried herbs, frozen herbs, and herb pastes poses a persistent challenge to the Europe fresh herbs market. Consumers often perceive dried and frozen alternatives as more cost-effective and convenient due to their longer shelf life and ease of storage. According to the European Retail Forum, private label brands offering dried herb mixes have gained significant market share due to their affordability and widespread availability in supermarkets. Frozen herbs retain much of their nutritional value and flavor while eliminating the risk of rapid spoilage, making them an attractive option for busy households. Data from market analysis firms indicates that the dried herbs segment continues to dominate in terms of volume sales due to its lower price point and versatility in cooking. Herb pastes and oils also provide ready-to-use solutions that appeal to consumers seeking convenience without the preparation effort required for fresh herbs. The economic downturns and inflationary pressures in Europe have made price sensitivity a key factor in purchasing decisions, leading many consumers to opt for cheaper substitutes. Retailers frequently promote discounted deals on dried and frozen products, further intensifying the competitive landscape. Fresh herb producers struggle to justify premium pricing when alternatives offer similar culinary utility at a fraction of the cost. Marketing efforts to highlight the superior taste and health benefits of fresh herbs often fail to overcome the immediate financial considerations of budget-constrained shoppers. This substitution effect limits the growth potential of the fresh herbs segment, particularly in mass market channels. Producers must continuously innovate in packaging and value addition to differentiate their offerings and justify the higher price tag associated with fresh produce in a highly competitive retail environment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 14.80% |

| Segments Covered | By Type, Category, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Bayer AG, Syngenta Group, BASF SE, Groupe Limagrain, Bejo Zaden B.V., Enza Zaden, Rijk Zwaan Zaadteelt en Zaadhandel B.V., Sakata Seed Corporation, Takii & Co., Ltd., HM.CLAUSE, KWS SAAT SE & Co. KGaA, Vilmorin & Cie, East-West Seed, Johnny's Selected Seeds, Thompson & Morgan |

SEGMENTAL ANALYSIS

By Type Insights

Culinary herbs constitute the leading segment in the Europe fresh herbs market due to their integral role in daily cooking across diverse European cuisines. The region boasts a rich gastronomic heritage where ingredients like basil, parsley, thyme and rosemary are staples rather than optional additives. According to the European Commission, food consumption patterns indicate that over 80 percent of households in Southern and Western Europe use fresh herbs at least three times a week. This high frequency of usage is supported by the widespread popularity of Mediterranean diets, which emphasize fresh plant-based ingredients for both flavor and health benefits. Data from the Food and Agriculture Organization of the United Nations reveals that Europe produces approximately 40 percent of the global supply of culinary herbs such as oregano and marjoram. The dominance is further reinforced by the tourism industry, which exposes consumers to authentic regional dishes, thereby increasing demand for specific herb varieties upon returning home. Retailers respond by dedicating significant shelf space to fresh culinary herbs, often placing them near produce sections to encourage impulse buys. The versatility of these herbs allows them to be used in salads, soups, main courses, and garnishes, making them indispensable in professional and home kitchens alike. As per Eurostat, the value of vegetable production, including herbs, in the European Union exceeded 60 billion euros recently, highlighting the economic significance of this sector. The consistent demand ensures that culinary herbs remain the primary revenue generator within the fresh herbs category, driving continuous investment in cultivation and distribution infrastructure.

The expansion of the culinary herbs segment is significantly supported by the rise of home cooking trends and the digitalization of recipes through social media and cooking apps. During and after the pandemic, many Europeans developed new cooking skills, leading to increased experimentation with flavors and ingredients. According to a survey by the International Food Information Council, 65 percent of European consumers reported cooking more meals at home compared to pre-pandemic levels. This shift has driven demand for fresh ingredients that elevate simple dishes with minimal effort. Digital platforms such as Instagram and TikTok feature millions of posts related to herbal cuisine, inspiring users to purchase specific herbs like cilantro, mint, and dill. Data from Statista indicates that food-related content engagement on social media in Europe grew by 25 percent annually, creating a direct link between online inspiration and offline purchasing behavior. Supermarkets have capitalized on this trend by offering recipe cards and bundled herb packs that simplify meal preparation. Additionally, the availability of fresh herbs in convenient packaging formats such as living pots allows consumers to keep plants alive longer, reducing waste and encouraging repeated use. The European Retail Forum notes that retailers who integrate digital recipe suggestions with in-store herb displays see a 15 percent increase in sales volume. This synergy between digital content and retail strategy sustains the growth of culinary herbs as consumers seek to replicate restaurant-quality meals at home using fresh aromatic ingredients.

Medicinal herbs represent the fastest growing segment in the Europe fresh herbs market driven by an increasing consumer preference for natural remedies and preventive healthcare solutions. As individuals seek alternatives to synthetic pharmaceuticals for minor ailments such as colds, digestive issues, and stress, the demand for fresh medicinal herbs like chamomile, peppermint, and lemon balm has surged. According to the World Health Organization, approximately 40 percent of the population in developed countries uses some form of traditional medicine, including herbal treatments. In Europe, this trend is supported by robust regulatory frameworks that recognize the efficacy of certain herbal preparations. Data from the European Medicines Agency shows that the number of registered traditional herbal medicinal products has increased by 20 percent in the last five years, reflecting growing acceptance and standardization. Consumers are particularly drawn to fresh herbs because they retain higher concentrations of active compounds compared to dried or processed forms. The aging population in Europe also contributes to this growth as older adults increasingly manage chronic conditions through lifestyle and dietary adjustments. A study published by the European Journal of Public Health indicates that 30 percent of adults aged 50 and above regularly consume herbal teas or infusions made from fresh ingredients. This demographic shift, combined with rising health consciousness among younger generations, creates a broad base for market expansion. Retailers are responding by expanding their wellness sections to include fresh medicinal herbs, often accompanied by educational materials on their health benefits. The integration of these herbs into daily wellness routines ensures sustained high growth rates for this segment.

The rapid growth of the medicinal herbs segment is further accelerated by innovation in product formats and their integration into functional beverages and wellness products. Manufacturers and retailers are developing convenient ways to consume medicinal herbs, such as ready-to-drink herbal infusions, cold-pressed juices with added mint or ginger, and smoothie blends. According to the European Beverage Association, the functional beverage market in Europe grew by 12 percent annually, with herbal ingredients being a key driver of this expansion. Fresh herbs are perceived as premium ingredients that enhance the nutritional profile and taste of these drinks, appealing to health-conscious consumers. Data from Mintel reveals that 45 percent of European consumers are willing to pay more for beverages that offer additional health benefits, such as immunity-boosting or relaxation properties. This willingness to pay supports the higher price point of fresh medicinal herbs compared to conventional produce. Additionally, spa wellness centers and yoga studios are incorporating fresh herbal teas and treatments into their offerings, creating new distribution channels beyond traditional retail. The European Spa Association reports that 60 percent of spa facilities now feature locally sourced herbal ingredients in their menus, enhancing the authenticity and appeal of their services. These innovative applications diversify the usage of medicinal herbs beyond home remedies, embedding them into broader lifestyle and wellness contexts. The convenience and perceived efficacy of these modern formats drive repeat purchases and attract new customer segments, ensuring that medicinal herbs continue to outpace other segments in growth rate.

By Category Insights

Conventional herbs hold the leading position in the Europe fresh herbs market primarily due to their affordability and wide accessibility in mainstream retail channels. Most consumers prioritize cost and convenience when purchasing perishable goods, making conventionally grown herbs the default choice for the majority of households. According to Eurostat, conventional agriculture accounts for over 90 percent of total agricultural production in the European Union, ensuring a steady and abundant supply of fresh herbs at competitive prices. Supermarkets and hypermarkets dominate the retail landscape, and they predominantly stock conventional herbs due to lower procurement costs and higher profit margins. Data from the European Retail Forum indicates that private-label conventional herbs are among the top-selling produce items due to their low price points. The established supply chains for conventional herbs are highly efficient, allowing for consistent availability year-round regardless of seasonal variations. Farmers benefit from economies of scale and established relationships with large distributors, which reduces operational risks. Furthermore, the lack of strict certification requirements for conventional herbs lowers barriers to entry for growers, enabling a larger number of suppliers to participate in the market. This competition keeps prices stable and attractive to budget-conscious consumers. The European Commission notes that while organic farming is growing, it still represents a niche segment compared to the vast volume of conventional produce. Consequently, conventional herbs remain the backbone of the market, serving the mass consumer base that values practicality and economic efficiency in their weekly grocery shopping routines.

The dominance of the conventional herbs segment is reinforced by well-established supply chains and consistent quality standards that ensure consumer trust and reliability. Decades of optimization have resulted in robust logistics networks that minimize spoilage and maintain freshness from farm to fork. According to the European Logistics Association, the efficiency of cold chain operations for conventional produce has improved significantly, reducing waste rates to below 10 percent. This reliability is crucial for retailers who need to maintain consistent stock levels to meet daily demand. Conventional farming practices utilize standardized protocols for irrigation, fertilization, and pest control, which result in uniform product appearance and size. This consistency is preferred by commercial buyers such as restaurants and catering services that require predictable ingredient quality for menu planning. Data from the European Food Safety Authority shows that conventional herbs strictly adhere to maximum residue limits, ensuring safety for consumption. Regular inspections and testing protocols provide an additional layer of assurance for consumers who may be concerned about food safety. The familiarity of conventional brands and packaging also plays a role in maintaining market share as shoppers tend to stick with known quantities. Retailers invest heavily in promoting conventional herbs through prominent shelf placement and promotional campaigns, further cementing their position. The combination of logistical efficiency, product consistency, and regulatory compliance creates a stable environment that supports the continued leadership of conventional herbs in the European market.

Organic herbs are the fastest growing segment in the Europe fresh herbs market, driven by surging consumer demand for health-conscious and environmentally sustainable products. Shoppers are increasingly aware of the potential health risks associated with pesticide residues and are willing to pay a premium for certified organic options. According to the European Commission, the organic food market in the EU has grown by 10 percent annually, reaching a value of 41 billion euros. This growth is particularly strong in the fresh produce category, where consumers perceive immediate health benefits. Data from the Research Institute of Organic Agriculture indicates that sales of organic herbs have increased by 15 percent year on year, outpacing the overall market growth. Environmental concerns also play a significant role as consumers seek to support farming practices that protect biodiversity and soil health. Organic certification guarantees that no synthetic pesticides or fertilizers were used, which aligns with the values of eco-conscious buyers. The European Green Deal aims to increase the share of organic farmland to 25 percent by 2030, providing policy support and incentives for farmers to transition to organic methods. This political backing enhances the visibility and credibility of organic products in the marketplace. Retailers are expanding their organic sections and introducing dedicated branding for organic herbs to capture this growing segment. The combination of health benefits, environmental ethics, and policy support creates a powerful momentum that drives the rapid expansion of organic herbs in Europe.

The rapid growth of the organic herbs segment is facilitated by a premium pricing strategy and enhanced brand differentiation that attracts high-value consumers. Organic herbs command higher prices due to the increased labor and certification costs associated with organic farming, but consumers perceive this as a reflection of superior quality and safety. According to Nielsen data, organic products typically carry a price premium of 20 to 30 percent compared to conventional equivalents, yet sales volumes continue to rise. This indicates a resilient customer base that prioritizes quality over cost. Brands that specialize in organic herbs invest in storytelling and transparency, highlighting their farming practices and commitment to sustainability. This emotional connection fosters loyalty and encourages repeat purchases. Data from the European Organic Certifiers Council shows that the number of certified organic operators has increased by 8 percent annually, indicating a growing supply base capable of meeting rising demand. Retailers leverage this differentiation by creating exclusive organic lines and partnering with local organic farms to offer unique varieties. The perception of organic herbs as a luxury or wellness item appeals to affluent demographics who are less sensitive to price fluctuations. Marketing campaigns emphasize the purity and potency of organic herbs, further justifying the higher cost. As disposable incomes rise and health awareness deepens, the appeal of premium organic products strengthens, ensuring that this segment continues to grow at the fastest rate in the market.

By Distribution Channel Insights

Supermarkets and hypermarkets constitute the leading distribution channel for the Europe fresh herbs market due to the convenience of one-stop shopping and the wide variety of products they offer. Consumers prefer these large retail formats because they can purchase fresh herbs alongside other grocery items, saving time and effort. According to Eurostat, supermarkets account for over 50 percent of total food retail sales in the European Union, making them the primary touchpoint for most shoppers. These stores dedicate significant floor space to fresh produce sections where herbs are prominently displayed, often in living pots or pre-packaged containers to maintain freshness. The ability to offer a wide range of herb varieties, including common and exotic types, allows supermarkets to cater to diverse culinary preferences. Data from the European Retail Forum indicates that customers visit supermarkets an average of 1.5 times per week, ensuring frequent exposure to fresh herb promotions. The economies of scale enjoyed by large retail chains enable them to negotiate better prices with suppliers, passing some savings to consumers. Additionally, supermarkets invest in advanced cold chain infrastructure to minimize spoilage and ensure high-quality products reach the shelves. Loyalty programs and digital apps further enhance customer engagement by offering personalized discounts on fresh produce. The combination of convenience, variety, competitive pricing, and consistent quality makes supermarkets and hypermarkets the dominant channel for fresh herb distribution in Europe.

The leadership of supermarkets and hypermarkets is strengthened by strategic shelf placement and integrated marketing campaigns that drive sales volume for fresh herbs. Retailers place herbs in high traffic areas near entranceways or alongside complementary items such as vegetables, meats, and cheeses to stimulate impulse purchases. According to a study by the Point of Purchase Advertising International, effective in-store displays can increase sales by up to 20 percent. Supermarkets frequently run promotional campaigns featuring fresh herbs as part of meal deals or seasonal themes, encouraging consumers to try new varieties. Data from Kantar Worldpanel shows that promotional activities in supermarkets lead to a 15 percent uplift in fresh produce sales during campaign periods. The integration of digital signage and recipe suggestions near herb sections educates consumers on usage ideas, further boosting demand. Private label brands offered by supermarkets provide affordable options that compete effectively with branded products. The consistent availability of fresh herbs throughout the year builds consumer trust and habit formation. Retailers also collaborate with suppliers to ensure timely restocking and minimize out-of-stock situations. The use of data analytics helps supermarkets optimize inventory levels based on historical sales patterns, reducing waste and maximizing profitability. These strategic operational and marketing efforts ensure that supermarkets and hypermarkets remain the primary channel for fresh herb distribution, capturing the largest share of consumer spending in the European market.

Online retail is the fastest-growing distribution channel for the Europe fresh herbs market, enabled by widespread digital adoption and improved last-mile delivery services. The convenience of ordering fresh produce from home and having it delivered quickly has attracted a growing number of consumers, especially in urban areas. According to Eurostat, the percentage of individuals in the EU who bought goods or services online reached 74 percent in recent years, reflecting a significant shift in shopping behavior. Specialized online grocery platforms and mainstream retailers have invested heavily in cold chain logistics to ensure that fresh herbs arrive in optimal condition. Data from the European E-Commerce Association indicates that online grocery sales grew by 20 percent annually, driven by the demand for convenience and safety. The ability to browse a wider selection of herbs, including rare and exotic varieties, appeals to culinary enthusiasts who may not find them in local stores. Subscription models offering regular deliveries of fresh herbs provide predictability and reduce the effort of weekly shopping. The integration of mobile apps allows users to track orders and receive notifications about fresh arrivals, enhancing the customer experience. As delivery times shorten and fees decrease, the barrier to entry for online fresh produce shopping lowers. This technological advancement, combined with changing consumer lifestyles, ensures that online retail continues to expand at the fastest rate in the distribution channel segment.

The rapid growth of online retail is further supported by personalization and transparency features that enhance consumer trust and engagement. Online platforms provide detailed information about the origin, farming practices, and nutritional benefits of each herb, allowing consumers to make informed choices. According to a survey by McKinsey, 70 percent of consumers expect personalized experiences from retailers, which online platforms can deliver through algorithms that suggest products based on past purchases. This level of customization increases customer satisfaction and loyalty. Data from BrightLocal shows that 88 percent of consumers trust online reviews as much as personal recommendations, highlighting the importance of social proof in online shopping. Retailers use customer feedback to improve product quality and service delivery, creating a virtuous cycle of improvement. Virtual tours of farms and live chats with growers add a layer of authenticity that bridges the gap between producer and consumer. The ability to compare prices and read detailed descriptions empowers shoppers to find the best value for their money. Online retailers also offer flexible payment options and easy return policies, reducing the perceived risk of buying perishable goods digitally. These features create a compelling value proposition that attracts new customers and retains existing ones, driving the sustained high growth of the online retail channel for fresh herbs in Europe.

REGIONAL ANALYSIS

Germany Fresh Herbs Market Analysis

Germany holds a prominent position in the Europe fresh herbs market, characterized by a strong emphasis on quality, sustainability, and organic consumption. As the largest economy in Europe, Germany has a highly developed retail sector that supports the widespread availability of fresh herbs. According to the Federal Ministry of Food and Agriculture, Germany has the largest organic market in Europe with sales exceeding 15 billion euros annually. This robust demand for organic products extends to fresh herbs, where consumers prioritize pesticide-free and locally sourced options. The country’s dense network of supermarkets and discounters ensures that fresh herbs are accessible to a broad demographic. Data from Statista indicates that German households spend an average of 300 euros per year on fresh vegetables and herbs, reflecting a high level of engagement with fresh produce. The popularity of home gardening is also significant, with many Germans growing their own herbs on balconies and in gardens. This cultural inclination towards self-sufficiency complements retail sales. Government initiatives promoting sustainable agriculture and healthy eating further support market growth. The presence of major retail chains like Aldi and Lidl drives competition and innovation in herb packaging and preservation technologies. Germany’s central location in Europe also makes it a hub for herb distribution, facilitating trade with neighboring countries. The combination of high purchasing power, environmental awareness, and efficient retail infrastructure ensures that Germany remains a key driver of the European fresh herbs market.

France Fresh Herbs Market Analysis

France occupies a central role in the Europe fresh herbs market, driven by its renowned culinary heritage and strong agricultural base. French cuisine relies heavily on fresh herbs such as thyme, rosemary, tarragon, and parsley, making them essential ingredients in daily cooking. According to the French Ministry of Agriculture, France is one of the leading producers of aromatic plants in Europe, with significant output from regions like Provence. The country’s farmers' markets and specialty stores play a vital role in distributing fresh herbs directly to consumers, fostering a culture of freshness and quality. Data from INSEE shows that French consumers spend approximately 20 percent of their food budget on fresh produce, including herbs. The popularity of traditional dishes such as ratatouille and bouillabaisse ensures consistent demand for specific herb varieties. Tourism also contributes to the market as visitors seek authentic culinary experiences featuring local herbs. The French government supports agricultural diversity through subsidies and protection of geographical indications, which helps maintain the quality and reputation of French herbs. Retailers in France are increasingly adopting organic practices to meet consumer expectations. The integration of herbs into gourmet dining and home cooking sustains a vibrant market. France’s influence on European culinary trends ensures that its herb consumption patterns impact the broader regional market. The combination of cultural pride, agricultural strength, and consumer sophistication keeps France at the forefront of the fresh herbs sector.

Italy Fresh Herbs Market Analysis

Italy maintains an influential position in the Europe fresh herbs market due to its status as a global culinary powerhouse and major producer of Mediterranean herbs. Basil, oregano, rosemary, and sage are staples in Italian cooking, driving high domestic consumption and export volumes. According to ISTAT, the Italian agricultural sector produces significant quantities of fresh herbs, particularly in the southern regions where climate conditions are ideal. The concept of km zero or local sourcing is deeply embedded in Italian food culture, encouraging consumers to buy fresh herbs from local markets and farms. Data from Coldiretti indicates that over 60 percent of Italians prefer locally produced food items, including herbs. The popularity of pizza, pasta, and sauces ensures that fresh herbs are used frequently in both home and restaurant settings. Italy’s tourism industry also boosts demand as visitors explore regional cuisines rich in herbal flavors. The Italian government promotes agricultural sustainability through initiatives that support small-scale farmers and organic certification. Retailers in Italy emphasize freshness and quality, often displaying herbs in open bins to allow customers to select specific bunches. The strong emotional connection between food and identity in Italy sustains high demand for authentic fresh ingredients. Italy’s contribution to European culinary trends ensures that its herb varieties remain popular across the continent. The combination of a favorable climate, cultural tradition, and agricultural expertise secures Italy’s leading role in the fresh herbs market.

United Kingdom Fresh Herbs Market Analysis

The United Kingdom holds a significant share in the Europe fresh herbs market, characterized by a diverse consumer base and a strong retail sector. British cuisine has evolved to incorporate a wide range of international flavors, increasing the demand for various fresh herbs such as cilantro, mint, and basil. According to the Department for Environment, Food and Rural Affairs, the UK imports a substantial portion of its fresh herbs to meet year-round demand. The prevalence of supermarkets and online grocery services ensures widespread accessibility. Data from Kantar Worldpanel shows that UK households purchase fresh herbs regularly, with a growing preference for living pots that extend shelf life. The rise of vegetarian and vegan diets in the UK has further boosted herb consumption as these diets rely on herbs for flavor enhancement. The UK government supports sustainable farming through environmental land management schemes, which encourage herb cultivation. Retailers focus on convenience, offering pre-washed and chopped herbs to save time for busy consumers. The multicultural nature of British society drives demand for exotic herbs used in Asian, African, and Middle Eastern cuisines. London serves as a major distribution hub, facilitating trade with European and global suppliers. The combination of dietary trends, retail innovation, and cultural diversity ensures that the UK remains a key market for fresh herbs in Europe. Continued investment in local production aims to reduce reliance on imports and enhance sustainability.

Spain Fresh Herbs Market Analysis

Spain plays a vital role in the Europe fresh herbs market as a major producer and exporter of Mediterranean herbs. The country’s favorable climate allows for year-round cultivation of parsley, cilantro, mint, and rosemary, making it a key supplier to Northern European markets. According to the Spanish Ministry of Agriculture, Spain is one of the largest producers of fresh herbs in the EU, with significant exports to France, Germany, and the UK. Domestic consumption is also high due to the importance of herbs in traditional Spanish dishes such as gazpacho and paella. Data from MAPA indicates that the value of herb production in Spain has grown steadily, driven by both domestic and international demand. The prevalence of local markets and ferias ensures that fresh herbs are readily available to consumers. Spanish farmers are increasingly adopting sustainable practices to meet European environmental standards. The tourism sector in Spain boosts demand for fresh herbs as restaurants cater to visitors seeking authentic local cuisine. Retailers in Spain emphasize freshness and affordability, offering a wide variety of herbs at competitive prices. The country’s strategic location facilitates efficient logistics and distribution to other European countries. Spain’s agricultural expertise and climatic advantages position it as a critical supplier in the European fresh herbs supply chain. Continued investment in technology and sustainability ensures long-term competitiveness.

Netherlands Fresh Herbs Market Analysis

The Netherlands holds a strategic position in the Europe fresh herbs market due to its advanced agricultural technology and role as a distribution hub. Although not a traditional consumer of large quantities of fresh herbs compared to Mediterranean countries, the Netherlands is a major producer and exporter thanks to its sophisticated greenhouse industry. According to Statistics Netherlands, the country is a leading exporter of agricultural products, including herbs, leveraging its logistics infrastructure to serve the entire European market. Dutch growers utilize controlled environment agriculture to produce high-quality herbs year-round, regardless of external weather conditions. Data from Wageningen University highlights the efficiency of Dutch horticulture in minimizing water and energy usage. The presence of major flower and plant auctions facilitates the trading of fresh herbs alongside ornamental plants. Retailers in the Netherlands focus on innovation, offering novel packaging and herb varieties. The country’s central location and excellent transport links make it an ideal entry point for herbs imported from outside Europe. Dutch consumers are increasingly interested in organic and sustainable products, driving local production shifts. The integration of technology in farming ensures consistent quality and supply. The Netherlands’ role as a logistical and technological leader supports the stability and growth of the European fresh herbs market.

Sweden Fresh Herbs Market Analysis

Sweden occupies a niche but growing position in the Europe fresh herbs market, driven by strong sustainability values and increasing culinary interest. Swedish consumers prioritize organic and locally sourced products, aligning with national environmental goals. According to Statistics Sweden, the sales of organic food products have increased significantly, with fresh herbs being a notable category. The short growing season in Sweden encourages the use of indoor farming and imports during the winter months. Data from the Swedish Board of Agriculture indicates a rise in local herb production using hydroponic systems. Retailers in Sweden emphasize transparency and ethical sourcing, appealing to conscious consumers. The popularity of Nordic cuisine, which incorporates herbs like dill and chives, supports domestic demand. Swedish households are willing to pay premium prices for high-quality and sustainable herbs. The government supports agricultural innovation through grants and research initiatives. The compact retail market allows for efficient distribution and minimal waste. Sweden’s focus on sustainability and quality sets a benchmark for other Northern European markets. The combination of environmental awareness and culinary exploration drives steady growth in the Swedish fresh herbs sector.

Denmark Fresh Herbs Market Analysis

Denmark holds a progressive position in the Europe fresh herbs market characterized by high organic penetration and innovative retail practices. Danish consumers are among the most likely in Europe to purchase organic products, including fresh herbs. According to Statistics Denmark, the organic market share in Denmark is one of the highest globally, exceeding 10 percent of total food sales. This strong preference supports local farmers who adopt organic methods. The country’s compact size facilitates efficient distribution from farm to table. Data from the Danish Agricultural Agency shows steady growth in herb production driven by domestic demand. Retailers in Denmark focus on minimal packaging and sustainability, appealing to eco-conscious shoppers. The popularity of New Nordic Cuisine has renewed interest in traditional herbs such as sorrel and woodruff. Danish households value freshness and quality, often purchasing herbs from local markets and specialty stores. The government supports sustainable agriculture through policy incentives. The high level of consumer education regarding food origins and impacts drives demand for transparent supply chains. Denmark’s leadership in organic consumption influences broader European trends. The combination of policy support, consumer awareness, and retail innovation ensures a robust market for fresh herbs.

Switzerland Fresh Herbs Market Analysis

Switzerland maintains a premium position in the Europe fresh herbs market, driven by high purchasing power and strict quality standards. Swiss consumers prioritize quality, freshness, and sustainability, often preferring locally produced herbs. According to the Federal Statistical Office, Switzerland has a high per capita expenditure on food, including fresh produce. The mountainous terrain limits large-scale agriculture but supports niche high-value herb production. Data from Agroscope indicates a growing interest in organic and biodynamic farming methods. Retailers in Switzerland, such as Migros and Coop, emphasize local sourcing and organic certification. The popularity of traditional Swiss dishes incorporating herbs like chives and parsley sustains domestic demand. Tourism in the Alpine regions boosts sales of local herbal products. Swiss consumers are willing to pay higher prices for guaranteed quality and ethical production. The country’s strict regulatory framework ensures high safety standards. The focus on precision and quality in Swiss agriculture results in superior herb products. Switzerland’s market serves as a benchmark for premium quality in Europe. The combination of wealth, quality consciousness, and local tradition supports a stable and high-value fresh herbs market.

Turkey Fresh Herbs Market Analysis

Turkey holds a significant and unique position in the Europe fresh herbs market as a major producer and exporter with a rich culinary tradition. Although geographically partly in Asia, Turkey is a key supplier to European markets due to its proximity and favorable climate. According to the Turkish Statistical Institute, Turkey is one of the world’s largest producers of fresh herbs, including parsley, mint, and dill. Domestic consumption is very high as herbs are integral to Turkish cuisine. Data from the Ministry of Agriculture and Forestry shows substantial export volumes to European countries. Turkish farmers benefit from low production costs and favorable weather conditions allowing for competitive pricing. The country’s strategic location facilitates quick transport to European markets. Retailers in Turkey offer a wide variety of fresh herbs at affordable prices. The growing middle class in Turkey is increasing demand for diverse and high-quality herbs. Government support for agricultural exports enhances market access. Turkey’s role as a supplier complements European production, especially during off-seasons. The combination of production capacity, culinary culture, and logistical advantage makes Turkey a critical player in the European fresh herbs supply chain.

Czech Republic Fresh Herbs Market Analysis

The Czech Republic holds a developing position in the Europe fresh herbs market characterized by growing consumer interest in healthy eating and local produce. According to the Czech Statistical Office, the demand for fresh vegetables and herbs has increased as consumers become more health-conscious. The country has a strong tradition of home gardening, which supplements retail purchases. Data from the Ministry of Agriculture indicates a rise in local herb production, particularly in organic formats. Retailers in the Czech Republic are expanding their fresh produce sections to include a wider variety of herbs. The popularity of traditional Czech dishes using herbs like dill and parsley supports domestic demand. Economic growth has increased purchasing power, allowing consumers to buy more premium products. The government supports sustainable agriculture through EU-funded programs. The central location of the Czech Republic facilitates trade with neighboring countries. Local markets remain popular for purchasing fresh herbs directly from farmers. The combination of traditional habits and modern health trends drives steady market growth. The Czech Republic’s market is evolving towards greater diversity and quality in fresh herb consumption.

Rest of Europe Fresh Herbs Market Analysis

The Rest of Europe segment includes countries such as Poland, Austria, Belgium, and Portugal, which collectively contribute significantly to the Europe fresh herbs market. These countries exhibit diverse consumption patterns influenced by local cuisines and economic conditions. According to Eurostat, the aggregate demand for fresh herbs in these regions is growing, driven by urbanization and health awareness. Poland has a large agricultural sector producing significant quantities of herbs for domestic use and export. Austria shares similarities with Germany in its preference for organic and high-quality products. Belgium serves as a logistical hub with a strong retail sector. Portugal benefits from a Mediterranean climate supporting year-round herb production. Data from national statistical offices in these countries indicates steady growth in fresh produce sales. Local traditions in each country dictate specific herb preferences, such as coriander in Portugal and chives in Poland. Retailers in these markets are adopting best practices from larger European economies to improve quality and availability. The diversity of the Rest of Europe segment provides resilience and opportunities for niche products. Collective growth in these countries supports the overall expansion of the European fresh herbs market.

COMPETITION OVERVIEW

The competition in the Europe garden seeds market is characterized by the presence of several large multinational corporations alongside numerous regional and local players who cater to specific consumer preferences. Major global companies leverage their extensive research and development capabilities to introduce innovative seed varieties that boast improved germination rates, disease resistance, and aesthetic appeal. These firms often engage in strategic acquisitions to consolidate their market position and expand their product offerings across different European countries. Regional players compete by focusing on niche segments such as heirloom varieties, organic seeds and plants adapted to local climatic conditions, which appeals to environmentally conscious consumers. The market is highly fragmented with intense competition driving continuous innovation in seed technology and packaging solutions. Price competitiveness remains a key factor, particularly in the mass market segment, where private label brands offered by large retail chains exert significant pressure on branded products. Companies differentiate themselves through strong branding, educational content, and digital engagement strategies that connect with hobbyist gardeners and professional landscapers. Regulatory compliance regarding genetic modification and pesticide use also shapes competitive dynamics as firms navigate complex legal frameworks. The overall landscape is dynamic with participants constantly adapting to shifting consumer trends towards sustainability and home food production.

KEY MARKET PALYERS

A few major players of the Europe garden seeds market include

- Bayer AG

- Syngenta Group

- BASF SE

- Groupe Limagrain

- Bejo Zaden B.V

- Enza Zaden

- Rijk Zwaan Zaadteelt en Zaadhandel B.V

- Sakata Seed Corporation

- Takii & Co., Ltd

- HM.CLAUSE

- KWS SAAT SE & Co. KGaA

- Vilmorin & Cie

- East-West Seed

- Johnny's Selected Seeds

- Thompson & Morgan

Top Strategies Used by Key Market Participants in the Europe Garden Seeds Market

Key players in the Europe garden seeds market primarily focus on product innovation through the development of hybrid and genetically improved varieties that offer higher yields and disease resistance. Companies invest heavily in research and development to create seeds that are adaptable to changing climate conditions and suitable for urban gardening trends. Strategic mergers and acquisitions are frequently employed to expand geographic reach and diversify product portfolios, allowing firms to access new customer segments and technologies. Partnerships with local distributors and retailers enhance market penetration and ensure efficient supply chain management. Digitalization is another critical strategy where companies utilize online platforms and mobile applications to engage directly with consumers, providing personalized gardening advice and seed recommendations. Sustainability initiatives such as organic seed certification and eco-friendly packaging are increasingly adopted to meet consumer demand for environmentally responsible products. Educational campaigns and community gardening projects help build brand loyalty and raise awareness about the benefits of homegrown produce. These combined strategies enable market participants to maintain a competitive advantage and drive growth in the dynamic European garden seeds sector.

Leading Players in the Europe Fresh Herbs Market

- Bayer Crop Science is a global leader in agricultural innovation with significant involvement in the European fresh herbs sector through its advanced seed technologies and crop protection solutions. The company focuses on developing high-yielding herb varieties that are resistant to diseases and pests, ensuring consistent quality for farmers. Recently, Bayer has intensified its efforts in sustainable agriculture by launching digital farming platforms that help growers optimize resource use and improve crop health. These initiatives strengthen their market position by providing comprehensive support to herb producers across Europe. The company collaborates with local distributors to ensure widespread availability of its premium seeds and biological control products. By integrating data-driven insights with traditional farming practices, Bayer enhances productivity and sustainability in the fresh herbs supply chain. Their commitment to research and development drives continuous improvement in herb cultivation techniques, benefiting the entire industry.

- Syngenta Group is a major contributor to the Europe fresh herbs market, offering a wide range of high-performance seeds and crop care products. The company emphasizes innovation in plant breeding to create herb varieties with superior flavor, aroma, and shelf life. Syngenta recently expanded its portfolio of organic-compatible solutions catering to the growing demand for chemical-free produce in Europe. They have invested heavily in biological pest control methods, which align with stringent European regulatory standards. The company works closely with farmers to provide technical assistance and training on best practices for herb cultivation. Syngenta’s strategic partnerships with retailers and distributors ensure efficient delivery of their products to end consumers. Their focus on sustainability and resilience helps growers adapt to climate challenges while maintaining high-quality standards. This approach solidifies their reputation as a trusted partner in the European fresh herbs industry.

- BASF Agricultural Solutions plays a crucial role in the Europe fresh herbs market by providing innovative crop protection and seed treatment technologies. The company develops specialized solutions that enhance the growth and vitality of fresh herbs, ensuring robust yields and premium quality. BASF recently launched new biological fungicides that protect herbs from common diseases without harming the environment. These products support the transition towards more sustainable farming practices favored by European consumers. The company engages in extensive research to understand the specific needs of herb growers and tailor their offerings accordingly. BASF collaborates with agricultural experts to promote integrated pest management strategies that reduce chemical usage. Their digital tools help farmers monitor crop health and make informed decisions. By focusing on innovation and sustainability, BASF strengthens its position as a key enabler of success in the European fresh herbs sector.

RECENT HAPPENINGS NEWS IN THE EUROPE GARDEN SEEDS MARKET

- In March 2024, Bayer Crop Science launched a new line of organic certified vegetable seeds specifically designed for home gardens in Western Europe to meet rising demand for chemical-free produce and strengthen its sustainable portfolio.

- In June 2023, Syngenta Group acquired a smaller regional seed breeder in Southern France to expand its variety of heat-tolerant herb and vegetable seeds, enhancing its adaptation to climate change impacts.

- In September 2023, BASF Agricultural Solutions introduced a digital platform for amateur gardeners in Germany, providing personalized seed recommendations and care tips to increase customer engagement and brand loyalty among urban consumers.

- In January 2024, KWS SAAT SE partnered with several major European online retailers to streamline the direct-to-consumer sales channel for its premium flower and vegetable seeds, improving accessibility and convenience.

- In November 2023, Rijk Zwaan opened a new research facility in the Netherlands focused on developing disease-resistant leafy green and herb varieties to support sustainable farming practices and secure long-term supply stability.

MARKET SEGMENTATION

This research report on the Europe fresh herbs market has been segmented and sub-segmented based on type, category, distribution channel, and region.

By Type

- Culinary Herbs

- Medicinal Herbs

- Aromatic Herbs

By Category

- Convectional

- Organic

By Distribution Channel

- Supermarkets / Hypermarkets

- Specialty Stores

- Online Retail

- Farmers’ Markets

- Convenience Stores

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the current size and growth outlook of the Europe garden seeds market?

The Europe garden seeds market was valued at USD 71.83 billion in 2026 and is projected to reach USD 216.62 billion by 2034, expanding at a CAGR of 14.80% during the forecast period. Market growth is supported by increasing home gardening activities, rising demand for organic produce, growing urban agriculture, and continuous advancements in hybrid and disease-resistant seed varieties across Europe.2

2. Which countries are leading the Europe garden seeds market?

Germany currently represents one of the largest markets for garden seeds in Europe due to its strong gardening culture and well-established horticulture sector. France, the United Kingdom, Italy, Spain, and the Netherlands also contribute significantly to regional demand through expanding home gardening, commercial landscaping, greenhouse cultivation, and investments in sustainable agriculture and seed innovation.

3. What are the major trends shaping the Europe garden seeds market?

The Europe garden seeds market is being transformed by several long-term trends, including growing demand for organic and non-GMO garden seeds, rising adoption of hybrid and climate-resilient seed varieties, expansion of urban gardening and vertical farming, increased consumer preference for home-grown vegetables and herbs, and advancements in seed breeding technologies that improve germination rates, disease resistance, and crop productivity. These trends continue to drive product innovation and sustainable growth across the European seed industry.

4. What factors are driving demand in the Europe garden seeds market?

The Europe garden seeds market is primarily driven by increasing consumer awareness of healthy eating, rising interest in home food production, government initiatives promoting sustainable agriculture, and growing investments in horticulture. Climate-resilient seed development, improved seed quality, expanding e-commerce distribution channels, and higher spending on residential landscaping are further supporting market expansion throughout Europe.

5. Which seed types account for the largest share of the Europe garden seeds market?

Vegetable seeds account for the largest share of the Europe garden seeds market, driven by the increasing popularity of kitchen gardens, organic farming, and self-sufficient food production. Flower seeds, herb seeds, ornamental plant seeds, and lawn grass seeds also represent significant segments, supported by rising investments in landscaping, urban green spaces, and recreational gardening across European countries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com