Europe Hearing Aid Market Size, Share, Trends & Growth Forecast Report By Hearing Loss, Product, End-User & Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis (2026 to 2034)

Market Size, 2025

$2.8 BnMarket Estimate, 2026

$3 BnMarket Forecast, 2034

$5.19 BnCAGR, 2026–2034

7.1%Europe Hearing Aid Market Size

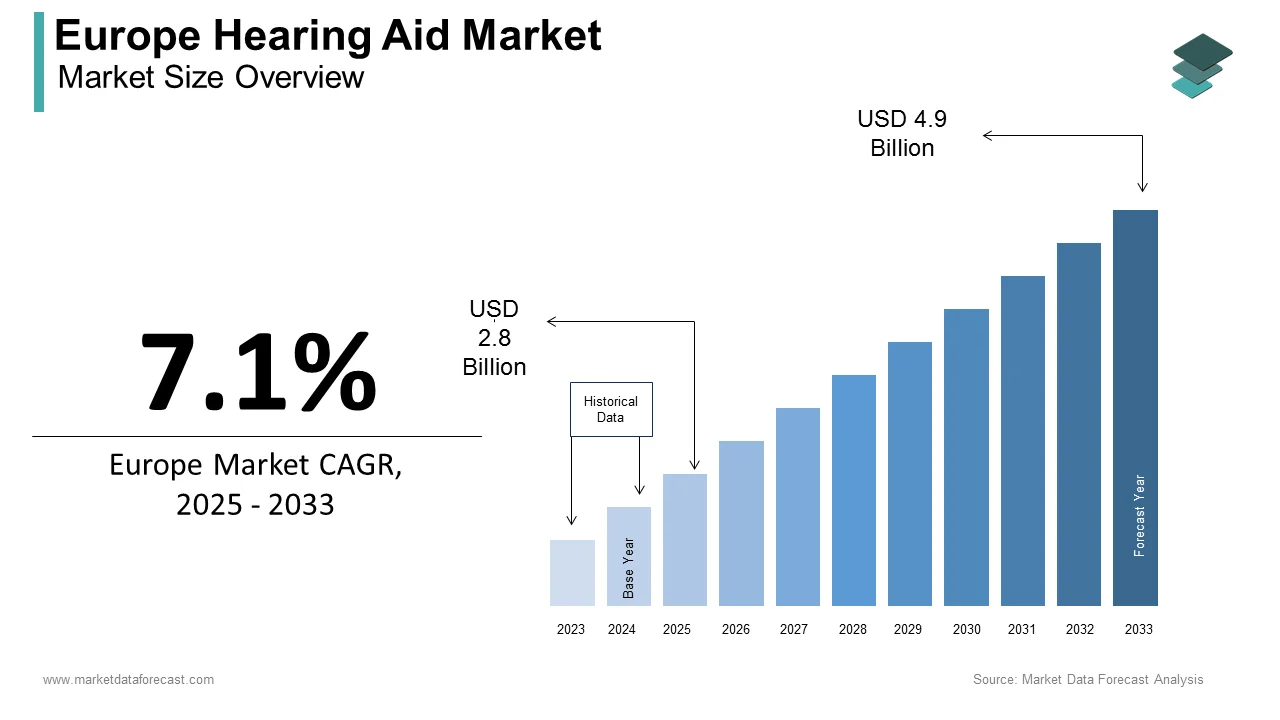

The hearing aid market size in Europe was valued at USD 2.8 billion in 2025. The European market is predicted to grow at a CAGR of 7.1% from 2026 to 2034 and be valued at USD 3 billion in 2026 and USD 5.19 billion by 2034.

The hearing aid is an electroacoustic device designed to amplify sound for individuals with sensorineural or conductive hearing impairment. These devices range from basic analog units to advanced digital systems featuring wireless connectivity artificial intelligence driven noise reduction and rechargeable batteries. Universal newborn hearing screening is now implemented in 25 out of 27 EU member states as confirmed by the European Centre for Disease Prevention and Control ensuring early detection and intervention.

MARKET DRIVERS

Aging Population and Rising Prevalence of Age-Related Hearing Loss Drive Sustained Demand

The aging population is substantially prompting the growth of Europe hearing aid market. According to Eurostat, 29.4 % of the European Union’s population was aged 60 or older in 2023 and this proportion is projected to exceed 33 % by 2035. This irreversible sensorineural condition results from cumulative degeneration of cochlear hair cells and auditory nerve pathways necessitating lifelong amplification support. National health systems respond through structured audiology pathways with countries like Germany and Sweden mandating hearing assessments as part of routine geriatric care.

Expansion of Universal Newborn and School Age Hearing Screening Programs Fuels Early Intervention

The systematic implementation of early hearing detection and intervention programs across Europe is creating a steady pipeline of pediatric and adolescent hearing aid users who require lifelong device support, which is additionally fuelling the growth of Europe hearing aid market. According to the European Environment Agency, over 12 million young Europeans aged 15 to 35 are at risk of permanent hearing damage due to unsafe listening practices. Early identification not only initiates immediate device use but also establishes long term patient pathways with regular device upgrades every four to six years.

MARKET RESTRAINTS

Stigma and Low Awareness Continue to Suppress Help Seeking Behavior

The technological advances and public health initiatives social stigma and limited awareness of hearing loss consequences is restricting the growth of Europe hearing aid market. According to a 2023 pan European survey by the European Federation of Hard of Hearing People only 38 % of adults with measurable hearing impairment had sought professional help with many perceiving hearing aids as symbols of aging frailty or disability. Moreover, public health messaging has historically focused on vision and cardiovascular health with hearing receiving minimal attention in national wellness campaigns.

Fragmented Reimbursement Policies Limit Access in Southern and Eastern Europe

While Western and Northern European countries offer robust public funding for hearing aids significant disparities persist in Southern and Eastern Europe where reimbursement is partial inconsistent or absent. In Romania and Bulgaria public funding covers less than 20 % of device costs forcing patients to pay out of pocket for even basic models which average 800 to 1200 euros as per national health ministry price benchmarks. This financial barrier results in stark adoption gaps with hearing aid penetration rates below 25 % in these regions compared to over 50 % in Germany and the Netherlands as documented by the European Hearing Instrument Manufacturers Association. Even where partial reimbursement exists bureaucratic delays and restricted device formularies discourage uptake. The lack of harmonized EU level guidelines on hearing aid coverage perpetuates inequity and fragments the market.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Health Monitoring Features Opens Premium Segments

The incorporation of artificial intelligence and biometric sensing into hearing aids is creating high value opportunities beyond traditional sound amplification by transforming devices into multifunctional health platforms. According to the European Hearing Instrument Manufacturers Association, over 60 % of premium hearing aids launched in Europe since 2022 feature AI driven sound classification that automatically adjusts settings based on environment such as restaurants traffic or quiet rooms. Companies like Sonova and WS Audiology have partnered with telehealth providers to integrate hearing aids into remote patient monitoring programs for elderly populations reducing hospital readmissions.

Growth of Direct to Consumer and Online Hearing Care Models Expands Market Reach

The emergence of direct to consumer and online hearing care channels is democratizing access to hearing solutions among younger adults and underserved rural populations is creating new opportunities for the growth of Europe hearing aid market. These models reduce barriers of cost convenience and stigma by enabling discreet at home assessment and delivery. Countries like the Netherlands and the United Kingdom have updated regulatory frameworks to allow certain classes of hearing aids to be sold without mandatory in person fitting provided they meet safety thresholds under the EU Medical Device Regulation. Major manufacturers have responded by launching proprietary e commerce platforms and partnering with telehealth insurers.

MARKET CHALLENGES

Shortage of Qualified Audiologists Constrains Service Capacity and Timely Intervention

The lack of trained audiologists is impeding timely diagnosis device fitting and follow up care thereby delaying treatment and reducing effectiveness, which is ascribed to hinder the growth of Europe hearing aid market. Although the European Qualifications Framework includes audiology standards implementation varies widely and mutual recognition of credentials remains limited. The shortage directly impacts outcomes as delayed fitting beyond six months post diagnosis correlates with reduced speech recognition scores as confirmed by research from the University of Padua.

Rapid Technological Obsolescence and Lack of Standardized Recycling Infrastructure Create Sustainability Concerns

The accelerating pace of innovation in hearing aid technology is leading to shorter device lifespans and growing electronic waste with limited recycling infrastructure is also to inhibit the growth of Europe hearing aid market. According to the European Environment Agency the average replacement cycle for hearing aids has decreased from six years in 2010 to under four years in 2023 driven by consumer demand for Bluetooth connectivity rechargeability and AI features. Yet less than 15 % of discarded hearing aids are formally collected or recycled as per the EU’s Waste Electrical and Electronic Equipment database due to their small size complex composition and lack of dedicated take back systems. Most devices end up in household waste or are stored indefinitely contributing to resource inefficiency. Hearing aids contain rare earth metals lithium batteries and microelectronics that pose environmental hazards if improperly disposed.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Hearing Loss, Product, End-user, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | GN Store Nord A/S (Denmark), Cochlear Limited (Australia), MED-EL (Austria), SeboTek Hearing Systems, Starkey Hearing Technologies, Inc. (U.S.), Widex (Denmark), William Demant Holding A/S (Denmark), LLC (U.S.), Sivantos Pte. Ltd. (Singapore), Sonova (Switzerland), and Zounds Hearing, Inc. (U.S.). |

SEGMENT ANALYSIS

By Hearing Loss Insights

The sensorineural hearing loss segment was accounted in holding a dominant share of the Europe hearing aid market in 2024. Sensorineural hearing loss dominates the European hearing aid market due to its high prevalence among aging populations and its irreversible physiological basis which necessitates long term amplification solutions. As per the European Commission’s Joint Research Centre, more than 83 million people in the European Union live with disabling hearing loss with sensorineural cases constituting nearly 90 % of all diagnoses. National health systems across Germany France and the United Kingdom routinely fund hearing assessments and device provision for this cohort under public audiology programs.

The conductive hearing loss segment is lucratively growing with an expected CAGR of 6.8% during the forecast period with the rising awareness of non-surgical bone conduction solutions and improved early diagnosis in pediatric populations. Conductive loss often stems from middle ear pathologies such as otitis media which affects over 1.2 million children annually in the European Union according to the European Centre for Disease Prevention and Control. Traditional hearing aids are ineffective for these cases but bone anchored hearing systems and advanced air conduction devices now offer viable alternatives. Countries like Sweden and Denmark have integrated universal newborn hearing screening which detects conductive anomalies within the first weeks of life enabling timely intervention. Additionally, the European Medicines Agency has streamlined regulatory pathways for Class IIa hearing devices facilitating faster market entry for innovative conductive solutions.

By Product Type Insights

The Ear hearing aids segment was accounted in holding 48.2% of the Europe hearing aid market share in 2024. According to the British Society of Audiology, over 65% of first time hearing aid users in public healthcare systems are initially fitted with BTE devices owing to their ease of handling battery longevity and resistance to earwax occlusion. BTE devices also accommodate advanced features such as Bluetooth connectivity telecoil and directional microphones without compromising on size or battery life. Their open fit variants minimize occlusion effect enhancing user comfort particularly among elderly populations. Furthermore, BTE units are easier to repair and maintain in community audiology clinics which is in rural regions with limited specialist access.

The Receiver In The Ear hearing aids segment is likely to grow with an expected CAGR of 9.2 % during the forecast period with their optimal balance of discreet design high performance and user comfort which appeals strongly to active adults and early onset hearing loss patients. RITE devices separate the receiver from the main processor placing it directly in the ear canal which reduces feedback and improves sound quality particularly for high frequency losses common in sensorineural impairment. Technological integration has further boosted adoption with major brands embedding rechargeable lithium ion batteries and direct smartphone streaming capabilities.

By End User Insights

The adults segment was the largest by occupying a significant share of the Europe hearing aid market in 2024. Adults overwhelmingly dominate the Europe hearing aid market due to the high and rising prevalence of age related and noise induced hearing loss coupled with supportive public health infrastructure. National health systems in countries like Germany the United Kingdom and Sweden provide subsidized or fully funded hearing assessments and device fittings for adults through universal healthcare programs. Additionally, workplace noise regulations under the European Agency for Safety and Health at Work have increased employer sponsored hearing conservation programs driving early detection among working age adults. Public awareness campaigns such as the UK’s “Hearing Matters” initiative further normalize device adoption reducing stigma and encouraging help seeking behavior.

The pediatrics segment is likely to grow with an expected CAGR of 7.5% during the forecast period with the near universal implementation of newborn hearing screening programs and early intervention mandates across the European Union. According to the European Centre for Disease Prevention and Control over 98 % of infants born in EU member states in 2023 underwent hearing screening before hospital discharge enabling diagnosis within the first month of life. Technological advances such as tamper proof battery doors water resistant casings and remote parental monitoring via smartphone apps have enhanced safety and usability for young children.

COUNTRY LEVEL ANALYSIS

Germany Market Analysis

Germany was the top performer of the Europe hearing aid market with 24.3% of share in 2024 with its aging population comprehensive public reimbursement and high density of audiology professionals. Statutory health insurance covers basic hearing aids every six years with supplementary private plans enabling access to premium digital models. Germany has over 6500 licensed hearing care centers as per the German Association of Hearing Aid Acousticians ensuring widespread access even in rural areas. The country also leads in tele audiology adoption with 40 % of follow up fittings conducted remotely as documented by the German Medical Association in 2023. Strong domestic manufacturing by companies like Sonova and WS Audiology headquartered in Germany further reinforces the ecosystem.

United Kingdom Market Analysis

The United Kingdom hearing aid market held 18.2% of share in 2024 with the rising prominence for the advanced technology. While public provision focuses on Behind The Ear models the private market offers advanced Receiver In The Ear and rechargeable devices catering to early onset and lifestyle oriented users. The British Society of Audiology mandates that all adults receive a hearing assessment within 18 weeks of referral ensuring timely intervention. Over 70 % of UK adults aged 60 and above have had a hearing test according to the Office for National Statistics reflecting high health literacy.

France Market Analysis

France hearing aid market growth is likely to grow with the hybrid public private reimbursement model and strong emphasis on early diagnosis. The French National Authority for Health implemented the “100 % Santé” initiative in 2019 which eliminated out of pocket costs for a basket of essential hearing aids for all insured citizens. France mandates hearing screening for all school aged children and provides free audiological assessments for adults over 65 through local health agencies. The country has over 4200 audioprothesists registered with the National Order ensuring professional standards and geographic coverage. Research institutions like INSERM actively collaborate with manufacturers on noise induced hearing loss prevention particularly in industrial and military settings.

Italy Market Analysis

Italy hearing aid market growth is likely to grow with the recent healthcare reforms and demographic pressures. The Italian National Institute of Statistics reports that 23.5 % of the population is aged 65 or older with hearing impairment prevalence exceeding 65 % in this group. In 2022 Italy expanded its Essential Levels of Care decree to include full reimbursement for basic digital hearing aids for low income seniors and children. Italy has over 3800 authorized hearing aid centers primarily concentrated in the north but expanding southward through tele audiology partnerships. The University of Padua leads EU funded research on Mediterranean noise exposure patterns informing regional prevention strategies.

COMPETITIVE LANDSCAPE

The Europe hearing aid market is characterized by intense competition among a few dominant multinational players who leverage technological innovation clinical integration and digital ecosystems to differentiate themselves. Sonova WS Audiology and Demant collectively shape industry standards through rapid advancement in AI driven sound processing rechargeable platforms and health connected features. Competition extends beyond hardware to service models with tele audiology remote fine tuning and subscription based care gaining prominence. The market is bifurcated between public healthcare channels which prioritize cost effective reliable devices and private or direct to consumer segments demanding premium features discretion and connectivity. Regulatory harmonization under the EU Medical Device Regulation has raised quality and safety benchmarks intensifying pressure on smaller manufacturers. Meanwhile new entrants from the consumer electronics space are testing the waters with hearables blurring the line between wellness and medical devices.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe hearing aid market include

- GN Store Nord A/S (Denmark)

- Cochlear Limited (Australia)

- MED-EL (Austria)

- SeboTek Hearing Systems

- Starkey Hearing Technologies, Inc. (U.S.)

- Widex (Denmark)

- William Demant Holding A/S (Denmark)

- LLC (U.S.)

- Sivantos Pte. Ltd. (Singapore)

- Sonova (Switzerland)

- Zounds Hearing, Inc. (U.S.)

Top Players in the Market

- Sonova Holding AG headquartered in Switzerland is a global leader in hearing care with a strong presence across Europe through its Phonak and Advanced Bionics brands. The company offers a comprehensive portfolio ranging from premium hearing aids to cochlear implants and wireless communication accessories. Sonova has pioneered innovations such as AI powered sound processing and lithium ion rechargeability now considered industry standards. In 2023 the company expanded its telehealth platform Audéo Live which enables real time remote fine tuning by audiologists across 20 European countries.

- WS Audiology formed through the merger of Widex and Sivantos is a major force in the Europe hearing aid market with headquarters in Denmark and Germany. The company leverages dual brand strength to serve both public healthcare systems and private retail channels across the continent. WS Audiology has invested heavily in sustainable product design introducing the world’s first carbon neutral hearing aid in 2023 and achieving full recyclability of its packaging across Europe. The company also enhanced its Signia AX platform with augmented Xperience technology that uses motion sensors to optimize sound based on user activity.

- Demant A/S a Denmark based hearing healthcare group operates globally through its Oticon brand and owns a network of audiology clinics including HearUSA and Audika. In Europe Demant combines product innovation with direct patient access through over 3000 owned or affiliated hearing centers. The company introduced the Oticon Intent hearing aid in 2023 featuring brain behavior tracking that adapts amplification based on cognitive load and listening intent. Demant also strengthened its digital ecosystem by integrating its ON app with national e health platforms in Sweden and the Netherlands enabling seamless data sharing with public health records.

Top Strategies Used by the Key Market Participants

Key players in the Europe hearing aid market employ several strategic approaches to maintain its dominance. Continuous investment in artificial intelligence and sensor technology enables differentiation through personalized sound processing and health monitoring features. Expansion of telehealth and remote fitting platforms enhances accessibility and aligns with post pandemic digital care expectations. Strategic partnerships with national health systems insurers and e health providers facilitate integration into public and private reimbursement pathways. Commitment to sustainability through carbon neutral manufacturing recyclable materials and take back programs addresses growing regulatory and consumer environmental demands.

MARKET SEGMENTATION

This report has segmented and sub-segmented the European hearing aid market into the following categories.

By Hearing Loss

- Sensorineural

- Conductive

By Product

- In-The-Ear

- Canal Hearing Aids

- Receiver-In-The-Ear

- Behind-The-Ear

- Cochlear Implants

- Bone Anchored Systems

By End-User

- Adults

- Pediatrics

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe Hearing Aid Market and what are its growth drivers?

The Europe Hearing Aid Market includes hearing devices designed to assist those with hearing loss. Market growth is driven by an aging population, rising hearing impairment prevalence, technological innovations, and reimbursement policies

2. Which countries contribute most to the Europe Hearing Aid Market?

Germany, United Kingdom, France, Italy, and Spain are the leading countries with strong healthcare infrastructure and adoption rates

3. What types of hearing aids are most popular in Europe?

Behind-the-ear (BTE) and in-the-ear (ITE) hearing aids dominate, with increasing use of fully digital and rechargeable devices

4. How does the aging population impact the Europe Hearing Aid Market?

An increasing elderly demographic boosts hearing impairment prevalence, thereby increasing demand for hearing aids

5. What technological advances influence the Europe Hearing Aid Market?

Advancements like AI integration, Bluetooth connectivity, and teleaudiology improve device functionality and user satisfaction

6. How do reimbursement policies affect market growth?

Government and insurance reimbursements enhance affordability and access, positively affecting growth especially in Germany and France

7. Who are key players in the Europe Hearing Aid Market?

Notable companies include Sonova Holding AG (Phonak), WS Audiology, Demant A/S (Oticon), Starkey Hearing Technologies, GN Store Nord, Cochlear Limited, and MED-EL

8. How do distribution channels affect the market?

Expansion of online and retail sales channels improves accessibility and convenience for consumers

9. What challenges face the Europe Hearing Aid Market?

High device costs, stigma around hearing loss, and uneven healthcare access present challenges

10. Why is patient compliance important?

Effective hearing aid use depends on comfort, ease of use, and support services, impacting adoption and outcomes

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com