Europe Hydroponics Market Size, Share, Trends, & Growth Forecast Report Segmented By Equipment, Type, Crop Type, Input Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest Of Europe), Industry Analysis From (2026 to 2034)

Europe Hydroponics Market Size

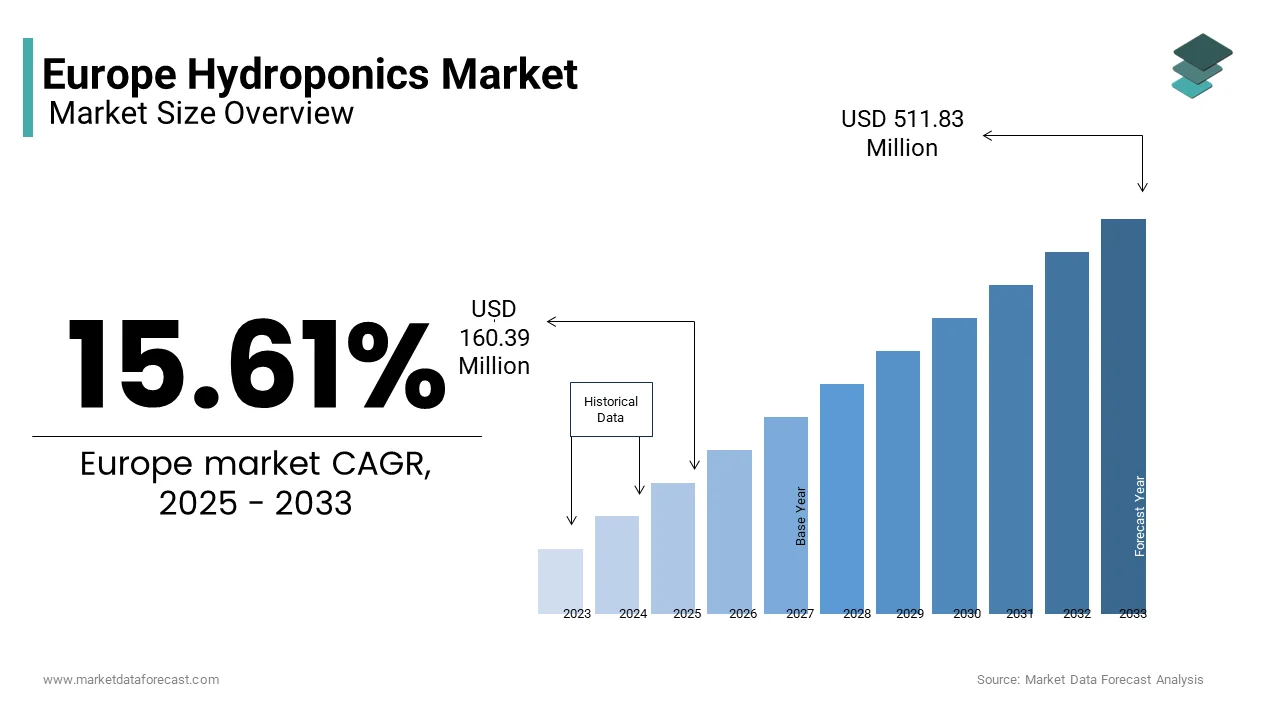

The Europe hydroponics market was valued at USD 160.39 million in 2025, and it is anticipated to reach USD 185.43 million in 2026 from USD 591.75 million by 2034, Europe is expected to grow at a compound annual growth rate (CAGR) of 15.61% growing at a CAGR of during the forecast period from 2026 to 2034.

Hydroponics are designed to deliver precise water and nutrient dosing in greenhouses and vertical farms. Its strategic relevance stems from water resilience and pesticide-reduction imperatives. In 2022, the EU’s Joint Research Centre indicated 47% of Europe was under drought “warning” and 17% under “alert,” underscoring climate-driven volatility that disrupts conventional field yields. Hydroponics can cut irrigation needs by up to 90–95% versus soil systems, as per FAO and a peer-reviewed synthesis in Energies (MDPI). Policy tailwinds also matter: the European Commission’s Farm-to-Fork strategy targets a 50% cut in chemical pesticide use and risk by 2030, creating strong incentives for controlled-environment cultivation with closed-loop inputs.

MARKET DRIVERS

Water stress and climate variability elevate controlled-environment demand.

Multi-year droughts and heat waves have sharpened Europe’s focus on water efficiency and yield stability. The European Environment Agency estimates that improving sectoral water efficiency is essential to Europe’s water resilience, with its 2025 briefing calling out escalating uncertainty in water availability. Hydroponics addresses this directly: closed systems typically save 80–95% water compared with soil cultivation while maintaining high crop uniformity; FAO cites aquaponic/hydroponic savings near 90%, and a recent MDPI review reports up to 95% irrigation reduction. Together, these factors convert hydroponics from a niche technology to a risk-mitigation tool for European supply chains.

Regulatory pressure to curb pesticides and nutrient losses

Europe’s Farm-to-Fork agenda embeds hard targets: a 50% reduction in chemical pesticide use and risk, and parallel curbs on hazardous substances by 2030. That regulatory arc steers buyers and growers to residue-controlled produce and production systems that minimize off-field externalities. Hydroponic greenhouses and vertical farms operate in sealed or semi-sealed environments with integrated pest management, enabling precise fertigation and recirculation that sharply reduces runoff. Academic and policy synopses reiterate the 50% pesticide target and the drive for cleaner inputs and traceability across the chain. As retailers commit to pesticide-risk cuts and audit-ready sourcing, hydroponics’ data-rich process control (nutrient EC/pH logs, climate telemetry) becomes a commercial differentiator aligned with EU compliance trajectories, accelerating adoption across leafy greens, herbs, and high-value fruiting crops.

MARKET RESTRAINT

Energy intensity and price volatility

Hydroponic and vertical farms are electricity-reliant (lighting, pumps, HVAC). EU energy prices spiked after 2021. Reuters points out a persistent “power-price divide” with southeastern Europe bearing higher costs, compressing margins for year-round controlled-environment operations. Although prices moderated in 2023–2024. For hydroponic operators, this volatility complicates lighting strategies (photoperiod/DLI), sizing of heat pumps, and payback on efficiency retrofits, often delaying expansions or forcing partial seasonality unless paired with on-site renewables or long-term power contracts.

Capital intensity and skills scarcity

High-spec greenhouses (active climate screens, CO₂ dosing, robotics) and multi-tier vertical farms demand substantial capex and advanced agronomic control. Sector diagnostics show uneven readiness across Europe. At the same time, Wageningen University & Research emphasizes the need for autonomous cultivation, resilient systems, and energy transition expertise, capabilities still scarce among mid-size growers. These gaps increase commissioning timelines and raise the cost of errors (e.g., nutrient imbalance, microclimate drift), which can wipe out crop cycles. The result is a slower diffusion curve outside core clusters such as the Netherlands unless financing, training, and integrator support expand in tandem.

MARKET OPPORTUNITIES

Urban proximity, year-round supply, and retail programming

With most Europeans living in cities and urbanization pressures rising globally, proximity agriculture can reduce food miles and offer a consistent, spec-compliant supply. UN and World Bank urbanization datasets point to a continued global urban share rising toward two-thirds by 2050, reinforcing demand for reliable, local fresh produce. Europe already houses sophisticated greenhouse clusters; Dutch sources show thousands of hectares under glass and polymer, with ongoing modernization that integrates automation and data-driven cultivation. Hydroponic operators can lock multi-year programs with retailers seeking residue control, tight sizing, and predictable shelf life, benefits magnified for salad greens and herbs. Co-location near logistics nodes also mitigates weather-related volatility that has repeatedly disrupted southern European open-field harvests.

Circular nutrient strategies and input independence

The EU is pivoting toward circular fertilizers to cut reliance on Russian mineral inputs and high-energy ammonia. The Financial Times points out that the bloc’s push for manure-derived “Renure” and biogas pathways to reduce synthetic fertilizer dependency and costs. Hydroponic/recirculating systems dovetail with this shift: closed-loop fertigation curbs nutrient discharge and enables tighter mass balance. As fertilizer cost/availability shocks persist, nutrient recovery and precision dosing reduce opex and improve ESG metrics. Pairing greenhouses with on-site biogas or green power further derisks cost structures and helps buyers meet Scope 3 targets, positioning hydroponic produce as a compliance-friendly choice for European retailers and foodservice buyers.

MARKET CHALLENGES

Policy fragmentation and delivery gaps

Even as Farm-to-Fork sets pesticide and nutrient ambitions, implementation can lag. The European Court of Auditors and independent coverage indicate gaps between CAP incentives and Green Deal goals. Without clearer, consistent metrics and support for controlled-environment upgrades (e.g., energy contracts, capex grants, training), growers face uncertainty on compliance pathways for crop protection and nutrient discharge. This policy-execution friction impedes bankability for hydroponic projects that require multi-year certainty on input rules, carbon accounting, and water standards, especially outside leading greenhouse regions.

Decarbonizing energy-hungry production at scale

Hydroponics thrives on reliable, low-carbon electricity and heat. Yet the EU’s energy crisis exposed grid and pricing vulnerabilities; despite partial normalization, price volatility remains a planning risk. Europe must still cut emissions steeply toward 2040, and senior EU climate advisors warn agriculture and adjacent systems need stronger price signals to meet targets, implying potential cost pass-throughs. For operators, the challenge is financing electrification (heat pumps), adding thermal storage, and securing PPAs or on-site renewables while maintaining competitive unit economics. Until low-carbon power is both abundant and predictably priced, expansion of energy-intensive vertical farms and winter tomato/cucumber programs will remain cautious.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 16% |

| Segments Covered | By Equipment, Type, Crop Type, Input Type, Aggregate Hydroponics Systems, Liquid Hydroponic Systems, Closed Sys,tems and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | BASF SE, Biostadt India Limited, Valagro SpA, Novozymes A/S, Biolchim SpA, Isagro SpA, and Koppert B.V. |

SEGMENTAL ANALYSIS

By Equipment Insights

The HVAC systems segment commanded Europe’s hydroponics equipment landscape. These systems ensure precise temperature, humidity, and ventilation control, essential in indoor cultivation. As of recent forecasts, HVAC holds the highest share within Europe’s equipment category. The prominence of HVAC reflects its foundational role in securing stable climate conditions year-round, preventing mold, and ensuring energy-efficient operations. Across global analysis, HVAC is also confirmed as the dominant equipment type, driven by growers’ need for environmental precision to safeguard crop quality and minimize loss. Such data underscores HVAC’s stratified importance in sophisticated hydroponic setups.

The LED grow lights are Europe’s equipment segment growing at the fastest rate. Forecasts during 2025–2033 anticipate the highest CAGR in this segment,t which is driven by mounting indoor farming expansion and the phasing out of less efficient lighting systems. Their ability to tailor spectral output helps growers manipulate plant traits, yield, flavor, and morphology while improving energy performance. The European ban on older halogen technologies also catalyzes LED adoption. As indoor growers increasingly experiment with “light recipes,” LEDs’ scalability and precision place them at the technological frontier of hydroponic productivity.

By Crop Insights

The tomatoes segment led Europe’s hydroponic crop choice. A notable share of hydroponically cultivated crops in the region is tomatoes, reflecting the crop’s versatility, high yield per square meter, and alignment with controlled environment performance. Tomatoes’ rapid cycle, reduced water demand, and culinary ubiquity make them an ideal hydroponic staple, especially in supermarkets and restaurant supply chains. These factors underscore tomatoes’ enduring popularity as the primary driver of hydroponic expansion.

The lettuce and other leafy greens segment is the hydroponic sector’s fastest-growing crop segment, with global projections indicating growth of around 15% CAGR through 2033. Indoor systems suit lettuce cultivation perfectly: rapid cycles, low space needs, and high turnover. With consumer demand for ready-to-eat, pesticide-free leafy greens rising, hydroponic lettuce appeals to convenience-focused European buyers and retail chains. These demand signals fuel robust growth in the segment across the region.

By Liquid Hydroponic Systems Insights

The Nutrient Film Technique (NFT) segment emerged as the most widely used across Europe. NFT’s simplicity, thin nutrient flow across plant roots, offers efficient space usage and easy scalability. Farmers favor NFT for its compact infrastructure and alignment with vertical or urban setups where floor area is constrained.

The Liquid hydroponic systems segment is growing at the fastest rate, with an estimated GRdGR of 14% over the forecast horizon through 2033. Unlike aggregate-rooted setups, these systems immerse or mist roots directly in nutrient solution, accelerating growth and yields. They also facilitate automation and recirculation, key ftoefficiency and consistency in commercial vertical farms. As growers seek high-output, scalable solutions in urban environments, these liquid systems gain ground rapidly.

By Closed Systems Insights

The drip systems segment is the leading method by adoption. Their flexibility, regardless of farm size or crop type, and ease of reticulation make them highly practical. Farmers appreciate drip systems for their precision nutrient delivery and straightforward setup in polyhouse and vertical frameworks, driving their prevalence across European operations.

The aggregate systems segment is the fastest-growing among closed-system categories. These media-based designs provide inert support media and facilitate nutrient recirculation while buffering root zones. Global forecasts project aggregate systems to dominate share and grow rapidly throughout this decade, a pattern mirrored in Europe. Their scalable design and lower technical threshold help explain their accelerating adoption. Here, automation is still catching up.

COUNTRY ANALYSIS

United Kingdom Hydroponics Market Analysis

The UK tops the regional hydroponics market, projected to hold the largest share over the forecast period. Government support for innovation, urban agriculture initiatives, and citizen attention to sustainable sourcing heighten demand for controlled-environment agriculture. The UK’s vertical farming ventures and consumer demand for local, pesticide-free produce bolster hydroponics’ commercial footprint.

Germany Hydroponics Market Analysis

Germany ranks second, buoyed by advanced greenhouse clusters and innovation. State-of-the-art setups and agribusiness investment proliferate, supported by a culture of precision horticulture. The German system’s engineering excellence and commercial diffusion spur hydroponic growth across various crops.

France Hydroponics Market Analysis

France exhibits significant expansion, with hydroponics penetrating both traditional and new,c complementary greenhouse sectors. Consumer interest in local, high-quality produce, combined with France’s structured agricultural modernization, supports equipment and system uptake.

Italy Hydroponics Market Analysis

Italy’s hydroponics market continues maturing, with diffusion in greenhouse-rich zones—especially in the north, where growers transition to more automated, precision systems as land and water constraints rise.

Spain Hydroponics Market Analysis

Spain follows closely, where smart controlled-environment agriculture spreads faster in water-scarce areas like Almería. Spain’s intense horticultural heritage and shift toward soilless systems fuel hydroponic interest for cucumbers, lettuce, and peppers.

COMPETITIVE LANDSCAPE

Europe’s hydroponics market is increasingly vibrant, characterized by engineering-rich expertise, expanding automation benchmarks, and nimble mid-tier innovators. Eastern and Northern European firms like iFarm and Botman introduce precision automation and harvest technologies that reduce labor and substrate waste. Meanwhile, Dutch-rooted suppliers such as Hydroponics Europe excel in nutrient chemistry and distribution networks. Competition isn’t just technology-driven: it’s grounded in differentiation, whether through turnkey automation, customized nutrient chemistry, or validated applications in Asia, which double as proof points. This dynamic intensifies as growth forecasts (double-digit CAGRs in various reports) signal accelerating demand, especially in leafy greens and vertical farming segments where environmental control and efficiency distinguish winners from followers.

KEY MARKET PLAYERS

These are some of the notable players in the European hydroponics market.

- Argus Control Systems

- Koninklijke Philips NV

- Botman Hydroponics (Belgium)

- Hydroponics Europe (Netherlands)

- iFarm (Finland)

- Greentech Agro LLC

- Logiqs B.V.

- Lumigrow, Inc.

- General Hydroponics, Inc.

Top Players In The Market

- iFarm is a Helsinki-based ag-tech innovator offering software-driven solutions and modular hardware for vertical farming and hydroponics. The company’s platform supports automated, pesticide-free production of salads, microgreens, and strawberries. In the Asia-Pacific region, iFarm has expanded pilot installations and R&D tie-ups, notably launching solutions in Japan and collaborating on precision indoor farming projects in Singapore to tailor systems for tropical climates. This expansion sharpens iFarm’s global reach, showcasing scalable, outcomes-focused automation and strengthening its competitive position in Europe.

- Operating from the Netherlands, Hydroponics Europe supplies hydroponic inputs, notably serving as the official distributor of Masterblend fertilizer across the continent. While its primary market is European, it also supports distributors in Southeast Asia, helping standardize nutrient formulations suited for hydroponic operations. Recently, the company broadened its range to include tailored nutrient blends for urban farms and greenhouse clusters, deepening its product relevance to both regional and Asia-Pacific growers.

- Belgium’s Botman Hydroponics designs systems that reduce substrate usage by up to 75% and develops automated lettuce-harvesting technology that delivers significant labour savings. The company has engaged with pilot vertical farms in Malaysia and Vietnam, showcasing its substrate-efficient, labor-smart systems adapted to high-cost-labour APAC environments. These efforts both validate the robustness of its engineering and invigorate its appeal back in Europe, where efficiency and sustainability remain priorities.

Top Strategies Used by Key Market Participants

Leading European hydroponics firms deploy a toolkit of strategies to advance their positions. First, they emphasize automation and labor efficiency, as Botman does with its automated harvesting systems. Second, they pursue modular, scalable product design, enabling faster deployment, seen in iFarm’s plug-and-play grow modules. Third, they expand via geographic testing. Piloting systems in Asia boosts product validation and adaptation. Fourth, they foster specialized nutrient customization, exemplified by Hydroponics Europe layering formulations for urban and greenhouse needs. Through these strategies, businesses enhance technological credibility, accelerate adoption, and tailor value propositions across differing regional priorities.

RECENT MARKET NEWS

- In March 2025, iFarm Europe Hydroponics Market, a controlled-environment software and hardware provider, expanded R&D collaborations in Singapore. This Europe Hydroponics Market partnership is anticipated to accelerate the adoption of tropical vertical farms and strengthen its automation portfolio.

- In November 2024, Hydroponics Europe Eugan will distribute tailored urban-farm nutrient blends across Southeast Asia. This Europe Hydroponics Market expansion is anticipated to reinforce its fertilizer customization capabilities and enhance cross-regional relevance.

- In June 2024, Botman Hydroponics Europe Hydroponics Market launched an automated lettuce-harvest module in Belgian greenhouse trials. This Europe Hydroponics Market innovation is anticipated to reduce labor demand significantly and validate automated harvesting at scale.

- In February 2025, iFarm Europe Hydroponics Market piloted plug-and-play vertical farming units in Japan. This Europe Hydroponics Market deployment is anticipated to showcase its software-driven indoor systems’ adaptability to differing regulatory and climatic contexts.

- In September 2024, Hydroponics Europe Entroduced fast-delivery Masterblend kits from a new German distribution hub. This Europe Hydroponics Market logistics upgrade is anticipated to improve responsiveness for urban farms and integrators across Europe.

MARKET SEGMENTATION

This market research report on the European hydroponic market is segmented and sub-segmented into the following categories.

By Equipment

-

HVAC

-

LED Grow Light

-

Communication Technology

-

Irrigation Systems

-

Material Handling

-

Control Systems

By Type

-

Aggregate

-

Liquid

By Crop Type

-

Tomato

-

Lettuce & Leafy Vegetables

-

Cucumber

-

Pepper & Strawberry

By Input Type

-

Nutrients

-

Growth Medium

By Aggregate Hydroponics Systems

-

Closed Systems

-

Open Systems

By Liquid Hydroponic Systems

-

Nutrient Film Technique (NFT)

-

Floating Hydroponics and Aeroponics

By Closed Systems

-

The Water Culture System

-

The EBB and Flow System

-

Drip Systems

-

The Wick System

By Country

-

UK

-

France

-

Spain

-

Germany

-

Italy

-

Russia

-

Sweden

-

Denmark

-

Switzerland

-

Netherlands

-

Turkey

-

Czech Republic

-

Rest of Europe

Frequently Asked Questions

What is the Europe hydroponics market?

The Europe hydroponics market refers to the production, systems, and supplies used to grow plants without soil by delivering nutrients through water, primarily for vegetables, herbs, and high-value crops in controlled environments.

Why is hydroponics important for agriculture?

Hydroponics enables efficient water and nutrient use, year-round crop production, higher yields on smaller land areas, and reduced environmental impact compared to traditional soil farming.

What drives growth in the Europe hydroponics market?

Growth is driven by urbanization, rising demand for fresh and locally grown produce, sustainability goals, technological advances, and increasing adoption in commercial and urban farming.

What systems are used in hydroponics?

Common hydroponic systems include NFT (Nutrient Film Technique), DFT (Deep Flow Technique), ebb and flow, drip systems, aeroponics, and vertical hydroponic setups.

What crops are commonly grown using hydroponics in Europe?

Hydroponics is widely used for lettuce, tomatoes, cucumbers, herbs, leafy greens, strawberries, and other high-value produce.

How does hydroponics support sustainability?

Hydroponics reduces water usage, minimizes fertilizer runoff, enables local food production, decreases transportation emissions, and supports resource-efficient agriculture.

Which regions in Europe are key hydroponics markets?

Major adoption is seen in Western and Northern Europe where urban farming, greenhouse integration, and controlled-environment agriculture (CEA) technologies are advancing rapidly.

What trends are shaping the hydroponics market?

Key trends include integration with vertical farming, automation and robotics, IoT sensors for monitoring nutrient levels, data-driven climate control, and sustainable energy use.

What challenges does the Europe hydroponics market face?

Challenges include high initial setup costs, technical skills requirements, energy consumption concerns, and regulatory complexity for controlled-environment food production.

How does hydroponics benefit food supply chains?

Hydroponics enables year-round production close to demand centers, shorter supply chains, reduced spoilage, and consistent quality and yield.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com