Europe Indoor Plant Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Type, Application, Product, And By Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Indoor Plant Market Report Summary

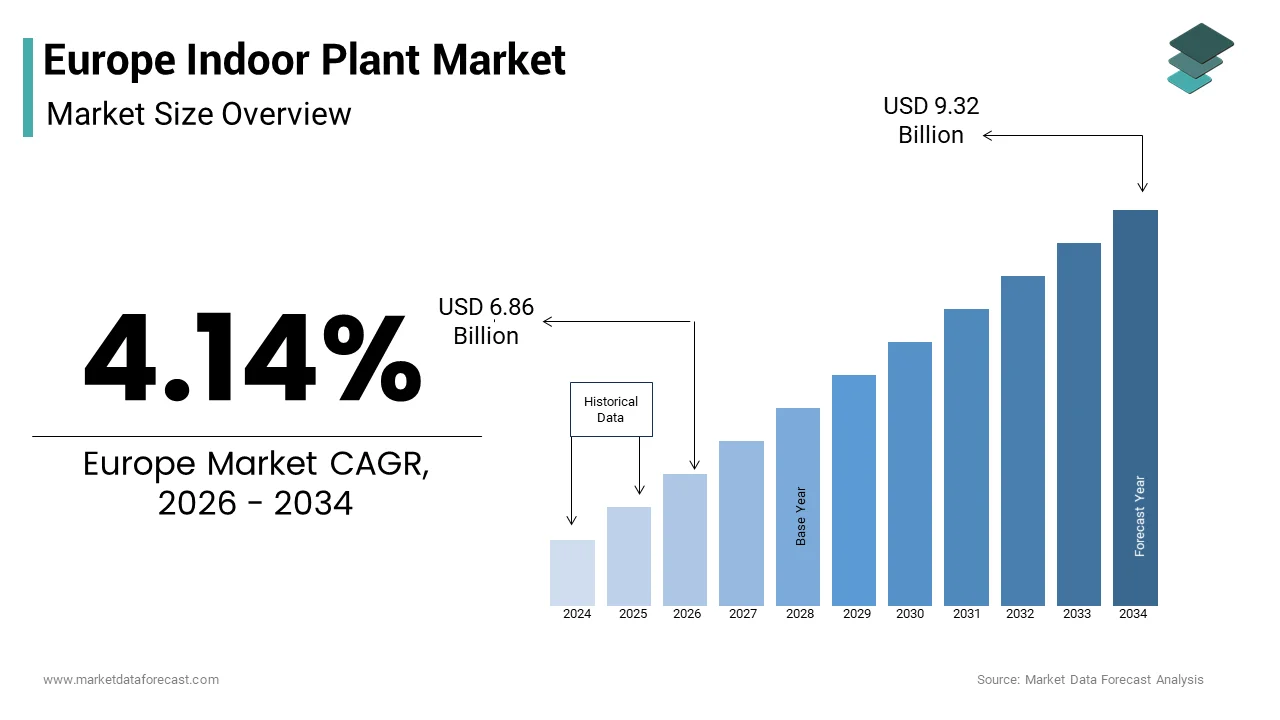

The Europe indoor plant market was valued at USD 6.58 billion in 2025, is estimated to reach USD 6.86 billion in 2026, and is projected to reach USD 9.32 billion by 2034, growing at a CAGR of 4.14% during the forecast period from 2026 to 2034. The growth of the Europe indoor plant market is driven by increasing consumer interest in biophilic living, rising awareness of the health and wellness benefits associated with indoor greenery, and the growing popularity of aesthetically designed living and workspaces. Demand for indoor plants is expanding across residential, commercial, and hospitality sectors as consumers seek natural décor solutions that improve indoor air quality, enhance mental well-being, and create visually appealing environments. The rapid growth of e-commerce plant retailers, subscription-based plant delivery services, and social media-driven home décor trends has further accelerated market expansion. Moreover, increasing adoption of low-maintenance plant varieties and sustainable gardening practices is encouraging wider consumer participation across Europe.

Key Market Trends

- Growing consumer preference for biophilic interior design is increasing the integration of indoor plants into homes, offices, hotels, and commercial spaces.

- Rising popularity of online plant retailers, subscription services, and direct-to-consumer platforms is expanding product accessibility across Europe.

- Demand for low-maintenance and air-purifying plant varieties is growing as consumers prioritize convenience, wellness, and healthier indoor environments.

- Sustainable cultivation practices, recyclable plant packaging, and eco-friendly gardening products are becoming important purchasing considerations.

- Social media platforms and interior design influencers are encouraging younger consumers to incorporate indoor plants into modern lifestyle and home décor trends.

Segmental Insights

Based on type, the low-light plants segment held the largest share of the Europe indoor plant market in 2025. The segment's leadership is supported by increasing demand for easy-to-maintain plants that thrive in indoor environments with limited natural sunlight, making them ideal for apartments, offices, and commercial buildings.

Based on application, the home decoration segment accounted for 43.2% of the Europe indoor plant market share in 2025. Rising consumer spending on home improvement, interior aesthetics, and wellness-focused living spaces continues to drive the widespread adoption of indoor plants as decorative elements.

Based on product, the herbaceous plants segment captured 45.3% of the Europe indoor plant market share in 2025. Their popularity is attributed to their attractive foliage, ease of cultivation, versatility across indoor settings, and suitability for both decorative and functional applications.

Regional Insights

The Europe indoor plant market is witnessing healthy growth across major economies as consumers increasingly embrace sustainable lifestyles and nature-inspired interior design. Germany led the regional market by accounting for 34.2% of the Europe indoor plant market share in 2025, supported by high consumer spending on home décor, a mature horticulture industry, and strong retail distribution networks. France ranked second with 18.9% of the regional market, driven by growing interest in premium indoor gardening and stylish residential interiors. The United Kingdom continues to experience steady market expansion, supported by an active community of plant enthusiasts, strong online retail adoption, and innovative plant subscription services. Italy is witnessing increasing demand for indoor plants as consumers blend natural elements with contemporary interior design, while Spain is steadily expanding its market through rising appreciation for indoor greenery despite its favorable outdoor growing conditions.

Competitive Landscape

The Europe indoor plant market is highly competitive, with horticultural producers, plant breeders, garden centers, home improvement retailers, and online plant platforms focusing on product innovation and customer experience. Leading companies are expanding their product portfolios with rare plant varieties, low-maintenance species, decorative planters, and personalized plant care solutions to meet evolving consumer preferences. Strategic investments in e-commerce, sustainable cultivation techniques, digital marketing, and efficient supply chain management are strengthening market competitiveness across Europe. Many companies are also collaborating with interior designers, lifestyle brands, and retail chains to expand their customer reach while promoting environmentally responsible production and packaging practices. As demand for wellness-oriented living spaces continues to grow, innovation, sustainability, and omnichannel retail strategies are expected to remain the primary competitive differentiators in the Europe indoor plant market.

Prominent players in the Europe indoor plant market include The Sill (U.S.), IKEA (Sweden), Dümmen Orange Group, Florensis, Selecta One, Urban Jungle (Netherlands), Lowe's Companies, Inc. (U.S.), Home Depot (U.S.), Bloomscape (U.S.), Costa Farms (U.S.), Folly Plants (U.K.), and Patch Plants (U.K.).

Europe Indoor Plant Market Size

The Europe indoor plant market size was valued at USD 6.58 billion in 2025 and is anticipated to reach USD 6.86 billion in 2026 to reach USD 9.32 billion by 2034, growing at a CAGR of 4.14% during the forecast period from 2026 to 2034.

The indoor plants are ornamental foliage and flowering species, specifically adapted for interior environments, including homes offices and commercial spaces. European Union population resides in urban areas, where access to private outdoor green space is limited thereby increasing reliance on indoor vegetation for aesthetic and environmental enhancement. The European Environment Agency emphasizes that indoor plants contribute to improved air quality by filtering volatile organic compounds, which is particularly relevant given that Europeans spend nearly 90% of their time indoors. Mental health concerns have risen significantly post pandemic prompting individuals to seek natural stress relievers within their living spaces. The diverse range of species from low maintenance succulents to large statement trees like Ficus and Monstera. Regulatory frameworks within the European Union strictly monitor phytosanitary standards to prevent the introduction of invasive pests ensuring the safety of imported plant material. Consumer behavior is increasingly influenced by sustainability trends with a preference for locally grown plants and eco-friendly pots. The integration of digital platforms for plant care advice and e-commerce sales has further democratized access to horticultural knowledge.

MARKET DRIVERS

Escalating Focus on Mental Well Being and Biophilic Design Principles

The escalating focus on mental well-being and biophilic design principles is promoting the growth of the Europe indoor plant market. Biophilia hypothesis suggests that humans possess an innate tendency to seek connections with nature, which translates into improved cognitive function and reduced stress levels when exposed to greenery. This scientific validation has prompted corporations across major European cities to integrate extensive indoor landscaping into their workplace strategies. The residential sector mirrors this trend, as remote work arrangements have led individuals to curate home environments that support mental clarity and emotional balance. Retailers respond by marketing plants not merely as decor but as essential wellness tools often bundling them with mindfulness guides. The rise of interior design trends that prioritize natural elements further amplifies demand. Consumers are willing to invest in larger statement plants that serve as focal points in living spaces. This shift from aesthetic appreciation to functional wellness utility ensures sustained growth.

Rapid Urbanization and Limited Access to Private Outdoor Spaces

The rapid urbanization and limited access to private outdoor spaces is fuelling the growth of the Europe indoor plant market. The average living space per person in urban European households has decreased by 5% over the last decade compelling residents to maximize interior aesthetics through vertical greenery, as per the research. This spatial constraint drives the adoption of compact indoor species that thrive in low light and confined areas. The concept of urban jungles has gained traction on social media platforms, where users share tips for creating lush interiors, despite square footage limitations. Real estate developers are increasingly incorporating plant friendly features, such as dedicated grow lights and irrigation systems in new builds to attract buyers. Municipal initiatives promoting green cities also encourage indoor planting as a complement to public green infrastructure. The need to personalize sterile urban living spaces fosters a strong emotional connection to indoor plants.

MARKET RESTRAINTS

High Susceptibility to Pests and Diseases in Controlled Environments

The high susceptibility to pests and diseases in controlled environments is impeding the growth of the Europe indoor plant market. Indoor conditions often lack the natural predators and ventilation found in outdoor ecosystems making plants vulnerable to infestations. As per the study, the incidence of indoor plant pests has increased by 18% in recent years due to the widespread trade of exotic species. This high mortality rate discourages repeat purchases among beginners, who perceive plant care as overly complex or risky. The use of chemical pesticides indoors is restricted due to health concerns limiting treatment options for consumers. Organic alternatives, while safer often require more frequent application and expertise, which many casual owners lack. Retailers face challenges in maintaining stock health during transit and display resulting in shrinkage losses. The negative experience of losing plants can damage consumer confidence and reduce long term engagement with the hobby. Educational gaps regarding proper watering humidity and light management exacerbate these biological vulnerabilities.

Logistical Complexities and Perishability in Supply Chain Management

The logistical complexities and perishability in supply chain management is also degrading the growth of the Europe indoor plant market. Plants are living organisms requiring specific temperature humidity and light conditions throughout transportation, which complicates logistics significantly. The cross border shipments within the EU face additional scrutiny and documentation requirements increasing lead times and costs. The fragility of foliage and root systems necessitates specialized packaging, which adds to operational expenses and environmental waste concerns. Seasonal weather extremes such as winter freezes or summer heatwaves pose risks to plant viability during last mile delivery. E-commerce retailers struggle to balance speed with care often facing customer complaints about damaged or stressed arrivals. The lack of standardized cold chain infrastructure for horticultural products across all European regions creates inconsistencies in quality. These logistical hurdles increase the final retail price affecting affordability. The inherent risk of product degradation requires robust insurance and return policies, which strain profit margins.

MARKET OPPORTUNITIES

Integration of Smart Technology and Automated Care Systems

The integration of smart technology and automated care systems is solely to create new opportunities for the growth of the Europe indoor plant market. Innovations, such as self-watering pots, soil moisture sensors, and app connected grow lights simplify plant maintenance for busy urban dwellers. These technologies provide real time data on plant health enabling users to adjust care routines proactively reducing the risk of neglect. Manufacturers are developing subscription models that combine hardware with curated plant deliveries creating recurring revenue streams. The appeal of tech enabled gardening attracts younger demographics, who value efficiency and data driven insights. Retailers partner with tech firms to offer bundled packages that lower the barrier to entry for novice growers. The ability to monitor plants remotely via smartphones enhances user engagement and satisfaction. This technological synergy transforms plant care from a chore into an interactive experience. As artificial intelligence improves predictive capabilities for plant needs, the market will see increased adoption.

Expansion of Plant Subscription Services and Curated Boxes

The expansion of plant subscription services and curated boxes is also to promote new opportunities for the growth of the Europe indoor plant market. These services deliver selected plants and care accessories directly to consumers on a regular basis fostering a sense of community and continuous engagement. The subscription economy in Europe has expanded significantly with lifestyle boxes gaining popularity, among millennials and Gen Z consumers. The plant subscription retention rates are higher than traditional one-off purchases due to the ongoing relationship with the brand. Companies curate boxes based on skill level light conditions and aesthetic preferences ensuring high success rates for recipients. This model reduces decision fatigue for consumers and introduces them to new species they might not otherwise choose. Subscription services often include educational content and access to online expert support enhancing the user experience. The predictability of recurring revenue allows businesses to optimize inventory and reduce waste. Social media unboxing trends amplify brand visibility and attract new subscribers through peer influence. This direct to consumer approach bypasses traditional retail margins allowing for competitive pricing. The personalization aspect strengthens customer loyalty and lifetime value.

MARKET CHALLENGES

Climate Change Impact on Cultivation and Supply Stability

The climate change impact on cultivation and supply stability is one of the major challenges for the growth of the Europe indoor plant market. Extreme weather events, such as heatwaves, droughts, and floods disrupt greenhouse operations and open field nurseries that supply indoor species. Shifting climate zones are altering the suitability of traditional growing regions forcing producers to relocate or invest in costly climate control systems. Energy prices for heating and cooling greenhouses have surged increasing production costs, which are passed on to consumers. Unpredictable weather patterns lead to inconsistent crop quality and volume causing supply chain hurdles. Import dependencies on regions affected by climate instability further exacerbate volatility. Retailers face difficulties in maintaining consistent stock levels leading to customer dissatisfaction. The carbon footprint of transporting plants from distant warmer climates conflicts with sustainability goals prompting a search for local alternatives, which may be limited. Adaptation strategies require significant capital investment, which small growers cannot afford.

Regulatory Hurdles and Phytosanitary Compliance Costs

The regulatory hurdles and phytosanitary compliance costs is additionally to pose as a challenge for the growth of the Europe indoor plant market. The European Union enforces strict regulations on the import of plants to prevent the spread of invasive pests and diseases. Compliance with these regulations requires extensive documentation inspections and certifications which increase administrative burdens and costs. The non-compliant shipments are frequently rejected or destroyed leading to financial losses for exporters and importers. The complexity of navigating varying national interpretations of EU rules creates fragmentation and delays in cross border trade. Small and medium sized enterprises often lack the expertise to manage these regulatory requirements efficiently. Recent updates to plant health laws have tightened controls on high-risk genera affecting popular indoor species. The cost of obtaining necessary certifications and implementing biosecurity measures reduces profit margins. Delays at borders due to increased checks can compromise plant health due to prolonged transit times. Consumers may face limited variety and higher prices as a result of these restrictions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.14% |

| Segments Covered | By Type, Application, Product, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic,c & Rest of Europe |

| Market Leaders Profiled | The Sill (U.S.), IKEA (Sweden), Dummen Orange Group, Florensis, Selecta One, Urban Jungle (Netherlands), Lowe's Companies, Inc. (U.S.), Home Depot (U.S.), Bloomscape (U.S.), Costa Farms (U.S.), Folly Plants (U.K.), Patch Plants (U.K.) |

SEGMENTAL ANALYSIS

By Type Insights

The low light plants segment was the largest by holding a dominant share of the Europe indoor plant market in 2025 due to the architectural realities of modern urban housing, where natural illumination is often limited. A significant proportion of European apartments face north or are situated in dense city centers where high rise buildings block direct sunlight. According to Eurostat, over 70% of the urban population in the European Union lives in flats, which typically have fewer windows and lower light exposure compared to detached houses. The energy efficiency regulations have led to improved insulation but sometimes reduced window sizes to minimize heat loss further limiting interior light penetration. Species thrive in these conditions requiring minimal photosynthetic input, making them ideal for hallways bathrooms and corners. The resilience of low light plants reduces the risk of failure for novice gardeners, who may not understand complex lighting requirements. Retailers prioritize these varieties because they have higher survival rates during transit and display periods. The aesthetic versatility of foliage plants allows them to complement various interior design styles from minimalist to industrial. This alignment with the structural limitations of urban dwellings ensures that low light plants remain the most purchased category.

The high light plants segment is expected to witness a fastest CAGR of 10.2% during the forecast period owing to the increasing popularity of south facing apartments and home conservatories. Consumers are actively seeking properties with ample natural light to support a wider variety of botanical species including flowering plants and succulents. New residential developments are prioritizing larger windows and balcony spaces to meet buyer demand for light filled interiors. This architectural trend enables the cultivation of high light species. The rise of sunrooms and glass extensions in suburban homes provides ideal microclimates for these demanding plants. Social media influencers showcase vibrant blooming indoor gardens inspiring followers to invest in high light varieties. Retailers are expanding their offerings of flowering indoor plants, which were previously considered difficult to maintain.

By Application Insights

The home decoration segment was the largest by accounting for 43.2% of the Europe indoor plant market share in 2025, as consumers increasingly view plants as essential elements of interior styling rather than mere horticultural hobbies. The rise of social media platforms like Instagram and Pinterest has popularized styles, which rely heavily on strategic plant placement. Data from housing market reports indicates that staged homes with indoor plants sell faster and at higher prices suggesting a strong perceived value in aesthetic enhancement. Large statement plants like Monstera Deliciosa and Ficus Lyrata serve as focal points in living rooms, while trailing vines add texture to shelves and walls. The affordability of plants compared to other decor items makes them an accessible way to refresh living spaces seasonally. Retailers collaborate with interior designers to create curated collections that match specific color palettes and styles. The emotional connection to a personalized space drives frequent purchases of new varieties to update the look.

The application of absorbing harmful gases segment is likely to witness a fastest CAGR of 9.2% during the forecast period with the heightened health awareness and concerns about indoor air quality. Consumers are increasingly educated about volatile organic compounds VOCs emitted by furniture paints and cleaning products. The indoor air pollution can be two to five times higher than outdoor levels posing significant health risks. The poor indoor air quality contributes to respiratory issues and allergies affecting millions of Europeans. Scientific studies cited in media campaigns validate these benefits driving consumer interest. Retailers label specific plants as air purifying creating a distinct category that appeals to health-conscious buyers. The rise of asthma and allergy rates in urban populations further stimulates demand for natural filtration methods.

By Product Insights

The herbaceous plants segment was the largest by capturing 45.3% of the Europe indoor plant market share in 2025 due to their versatility rapid growth and wide variety of forms. These plants are easier to propagate allowing retailers to maintain steady supply and lower costs. Their non woody stems make them lightweight and easy to transport reducing shipping damage and costs. Consumers appreciate the quick visual reward of new leaf growth which provides a sense of accomplishment. Herbaceous plants are suitable for both hanging baskets and tabletop displays offering flexibility in decor arrangements. Social media trends often highlight specific herbaceous varieties driving spikes in demand. Their resilience to occasional neglect makes them ideal for busy urbanites.

The hydroponic plants segment is esteemed to register a fastest CAGR of 9.2% from 2026 to 2034 owing to the desire for cleanliness and convenience. Hydroponics involves growing plants in water without soil eliminating mess pests and dirt associated with traditional potting. The pre potted hydroponic plants in glass vessels are among the top selling gift items. The aesthetic appeal of visible root systems in clear containers aligns with modern minimalist decor trends. Consumers appreciate the simplicity of watering and the reduced risk of overwatering, which is a common cause of plant death. Hydroponic systems are ideal for offices and apartments, where soil spills are a concern. The perception of hydroponics, as a modern and scientific approach to gardening attracts tech savvy consumers. Retailers offer complete kits with nutrients and instructions lowering the barrier to entry.

COUNTRY ANALYSIS

Germany Indoor Plant Market Analysis

Germany was the top performer in the Europe indoor plant market by capturing 34.2% of share in 2025 with a strong culture of home gardening and high environmental awareness. As the largest economy in Europe, Germany has a robust retail sector for horticultural products. Consumers prioritize sustainability and often prefer locally grown plants. The presence of major garden centers and online retailers ensures wide availability. Government initiatives promoting green living encourage indoor planting. The high disposable income allows for investment in premium and rare varieties. Germany serves as a trendsetter for eco-friendly horticultural practices in the region. The combination of cultural affinity and economic strength secures its leading role.

France Indoor Plant Market Analysis

France indoor plant market was ranked second by holding 18.9% of share in 2025 with a deep appreciation for aesthetics and interior design. French consumers view indoor plants, as essential decor elements that enhance the elegance of their homes. The horticultural sector is vibrant with strong demand for ornamental plants. The influence of French interior design trends promotes the use of large statement plants and artistic arrangements. Retailers focus on presentation and style catering to discerning tastes. The climate in southern France supports local production of certain indoor species. Cultural traditions of bringing nature indoors sustain steady demand.

United Kingdom Indoor Plant Market Analysis

The United Kingdom indoor plant market growth is steadily growing with a passionate community of plant enthusiasts and strong retail innovation. British consumers have embraced the urban jungle trend with high engagement on social media. The plant sales have surged post pandemic, as people invested in their homes. The prevalence of smaller living spaces in London drives demand for compact and vertical gardening solutions. Retailers offer extensive online services and subscription models. The rainy climate encourages indoor hobbies.

Italy Indoor Plant Market Analysis

Italy indoor plant market growth is likely to grow with the strong design heritage and love for natural elements. Italian consumers integrate plants into their homes to complement architectural beauty. Data from Coldiretti indicates that indoor plants are popular gifts and home accessories. The warm climate allows for the cultivation of Mediterranean species indoors. Designers often use plants to create vibrant living spaces. Retailers emphasize style and quality. The cultural importance of home aesthetics drives purchases.

Spain Indoor Plant Market Analysis

Spain indoor plant market growth is likely to grow with the interest in indoor greenery, despite its warm outdoor climate. Urbanization in cities like Madrid and Barcelona has increased demand for indoor nature. The indoor plant sales are rising as apartment living becomes common. Data from MAPA shows that young consumers are driving the trend. The availability of local nurseries supports supply. Retailers are expanding their indoor sections.

COMPETITIVE LANDSCAPE

The competition in the Europe indoor plant market is characterized by the presence of several large international breeders alongside numerous regional nurseries and local growers, who cater to specific consumer preferences. Major global companies leverage their extensive research and development capabilities to introduce innovative plant varieties that boast improved resilience aesthetic appeal and ease of care. These firms often engage in strategic collaborations with retail chains to secure shelf space and promote exclusive collections. Companies differentiate themselves through strong branding educational content and digital engagement strategies that connect with hobbyist gardeners and interior designers. Regulatory compliance regarding phytosanitary standards and sustainability also shapes competitive dynamics, as firms navigate complex legal frameworks.

KEY MARKET PLAYERS

A dominating market players that are in the Europe indoor plant market are

- The Sill (U.S.)

- IKEA (Sweden)

- Dummen Orange Group

- Florensis

- Selecta One

- Urban Jungle (Netherlands)

- Lowe's Companies, Inc. (U.S.)

- Home Depot (U.S.)

- Bloomscape (U.S.)

- Costa Farms (U.S.)

- Folly Plants (U.K.)

- Patch Plants (U.K.)

Top Players In The Market

- Dummen Orange Group is a global leader in ornamental plant breeding and propagation with a significant presence in the European indoor plant market. The company specializes in developing innovative varieties of foliage and flowering plants that are tailored for indoor environments and consumer preferences. Recently, Dummen Orange has strengthened its position by investing in sustainable production methods and expanding its portfolio of low maintenance and air purifying species. They have enhanced their digital platforms to provide growers and retailers with real time data on plant care and market trends. The company collaborates closely with European retailers to ensure consistent supply and high-quality standards.

- Florensis is a major contributor to the Europe indoor plant market, offering a wide range of high quality young plants and cuttings for professional growers. The company emphasizes innovation in plant breeding to create varieties with superior vigor disease resistance and visual appeal. Florensis recently expanded its production facilities in the Netherlands to increase capacity for popular indoor species, such as Anthurium and Spathiphyllum. They have invested heavily in biological pest control methods, which align with stringent European environmental regulations. The company works closely with growers to provide technical support and training on best practices for indoor plant cultivation. Florensis strategic partnerships with distributors ensure efficient delivery of their products to end consumers.

- Selecta One plays a crucial role in the Europe indoor plant market by providing premium genetics and young plants for ornamental foliage and flowering crops. The company develops specialized varieties that thrive in indoor conditions ensuring robust growth and long-lasting beauty. Selecta One recently launched new collections of compact and colorful indoor plants designed for small urban living spaces. These products support the trend towards space efficient gardening favored by European consumers. The company engages in extensive research to understand specific needs of indoor gardeners and tailor their offerings accordingly. Selecta One collaborates with agricultural experts to promote integrated crop management strategies that reduce chemical usage. Their digital tools help growers monitor plant health and optimize production processes.

Top Strategies Used By Key Market Participants In The Market

Key players in the Europe indoor plant market primarily focus on product innovation through the development of unique and resilient plant varieties that cater to urban living constraints. Companies invest heavily in breeding programs to create low light tolerant and air purifying species that appeal to health-conscious consumers. Strategic partnerships with retailers and online platforms enhance market penetration and ensure efficient supply chain management. Digitalization is a strategy where companies utilize mobile apps and smart sensors to engage directly with consumers providing personalized plant care advice. Sustainability initiatives, such as peat free substrates and biodegradable pots are increasingly adopted to meet environmental standards. Educational campaigns and social media engagement help build brand loyalty and raise awareness about the benefits of indoor greenery.

MARKET SEGMENTATION

This research report on the Europe indoor plant market is segmented and sub-segmented into the following categories.

By Type

- Shade-Loving Plants

- Low Light Plants

- High Light Plants

By Application

- Absorb Harmful Gases

- Home Decoration

By Product

- Succulent Plants

- Berbaceous Plants

- Woody Plants

- Hydroponic Plants

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Why is the Europe indoor plant market experiencing strong growth?

The market is expanding due to increasing urbanization, rising interest in home décor, growing awareness of indoor air quality, and the popularity of biophilic living spaces.

What are indoor plants and why are they becoming increasingly popular in Europe?

Indoor plants are ornamental or functional plants grown inside homes, offices, and commercial spaces to enhance aesthetics, improve indoor environments, and support well-being.

Which plant segment accounts for the largest share of the Europe indoor plant market?

Ornamental foliage plants account for the largest market share due to their low maintenance requirements, decorative appeal, and suitability for indoor environments.

How do indoor plants improve indoor environments and well-being?

They enhance interior aesthetics, help improve air quality, reduce stress, create a calming atmosphere, and contribute to healthier living and working spaces.

What factors are driving the growth of the Europe indoor plant market?

Growing consumer interest in home gardening, increasing spending on interior decoration, expanding e-commerce sales, and rising awareness of sustainable lifestyles are driving market growth.

Which industries generate the highest demand for indoor plants?

Residential households, offices, hospitality, retail stores, healthcare facilities, educational institutions, and commercial real estate are the primary end users.

What trends are shaping the future of the Europe indoor plant market?

Smart indoor gardening, self-watering planters, organic cultivation, premium ornamental plants, sustainable packaging, and online plant retail are shaping the market.

How are growers and retailers improving indoor plant offerings?

They are introducing low-maintenance varieties, eco-friendly packaging, digital plant care solutions, subscription services, and improved logistics for live plant delivery.

What challenges could affect the growth of the Europe indoor plant market?

Seasonal demand fluctuations, pest and disease management, transportation challenges, rising production costs, and changing consumer spending patterns could affect market growth.

Which countries are expected to lead the Europe indoor plant market?

Germany, the Netherlands, the United Kingdom, France, and Italy are leading markets due to strong horticulture industries, high consumer demand, and well-developed garden retail networks.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com