Europe Infant Nutrition Market Segmented By Type (Infant Milk Formula, Follow-Up Milk Formula, Growing Up Milk Formula, Specialty Baby Milk Formula), Formulation (Powder, Liquid Concentrate, Ready to Feed), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) – Size, Share, Trends, Growth, Forecast (2026 to 2034)

Europe Infant Nutrition Market Size

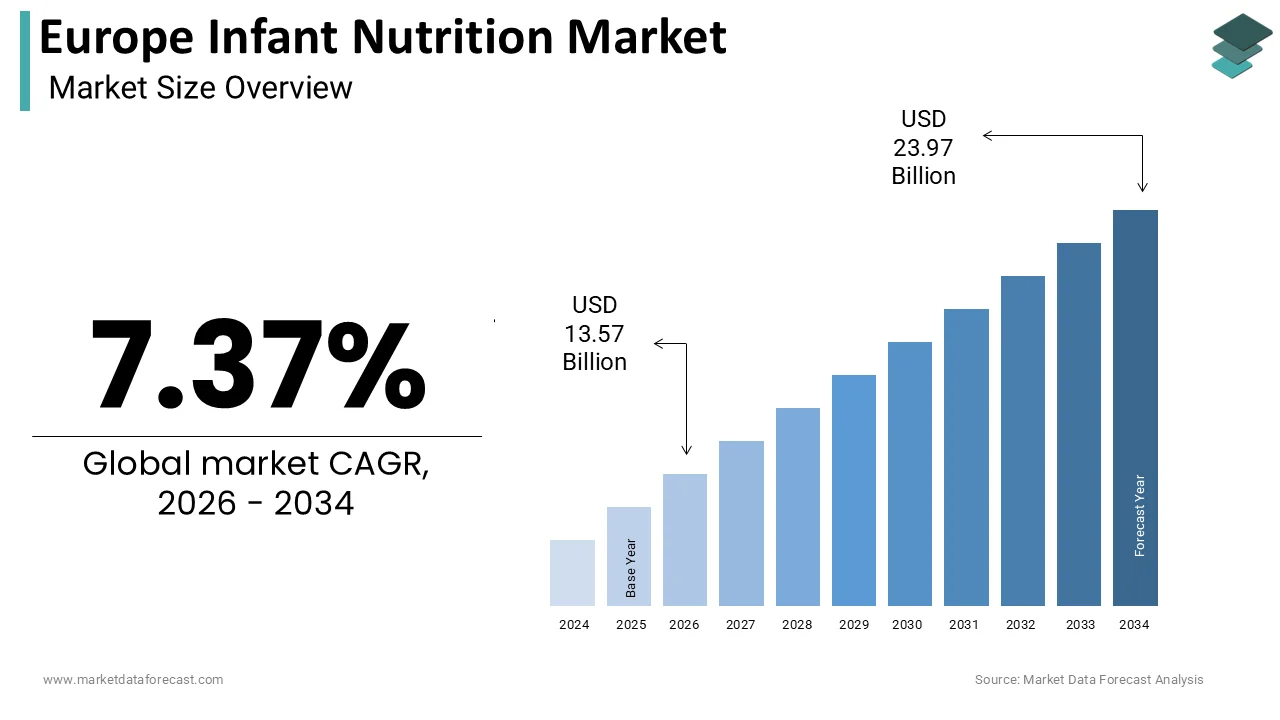

The Europe infant nutrition market size was calculated to be USD 12.64 billion in 2025 and is anticipated to be worth USD 23.97 billion by 2034, growing from USD 13.57 billion in 2026 at a CAGR of 7.37% during the forecast period.

Infant nutrition refers to the dietary practices and essential nutrients required for the healthy growth and development of children from birth through the first two years of life. These products serve as either complements or alternatives to breast milk and must comply with the European Union’s rigorous compositional and safety standards. Despite public health initiatives favoring breastfeeding, a significant proportion of European infants rely partially or fully on formula due to physiological, social, or economic factors. According to health organization reports, exclusive breastfeeding rates for infants during their first half-year remain notably low in high-income European nations, falling well below recommended international targets. Data from the European Union statistical office shows that fertility rates have continued to decline, reaching a new low and indicating a sustained, long-term reduction in the number of newborns. Nevertheless, demand persists for premium, functional, and specialized formulations that align with evolving parental expectations and clinical recommendations, shaping a dynamic and highly regulated market landscape.

MARKET DRIVERS

Rising Prevalence of Lactation Challenges Fuels Demand for Alternative Nutrition

An increasing number of mothers across the region face biological or logistical obstacles to sustained breastfeeding, which directly drives reliance on infant formula, and thereby contributes to the growth of the Europe infant nutrition market. Many new mothers in certain European regions encounter challenges with infant feeding, such as milk supply issues or difficulty with latching during the initial weeks after birth. The prevalence of exclusive breastfeeding for six months remains relatively low in several Western European nations. A significant portion of European women return to full-time work within the first year postpartum, which may influence the duration of breastfeeding. In response, manufacturers are developing formulations that incorporate human milk oligosaccharides, probiotics, and optimized fatty acid profiles to replicate the functional benefits of breast milk. These innovations cater to informed parents seeking safe, nutritionally equivalent alternatives, thereby sustaining consistent demand despite policy support for breastfeeding.

Stringent Regulatory Frameworks Enhance Consumer Trust and Product Differentiation

The European Union’s regulatory regime, particularly Commission Delegated Regulation EU 2016 127, imposes exacting standards on nutrient composition, ingredient sourcing, and labeling for infant and follow-on formulas. This propels the expansion of the Europe infant nutrition market. Regulatory changes in the infant formula industry have included prohibiting certain added sugars and requiring minimum levels of essential fatty acids like docosahexaenoic acid. Meeting these requirements has spurred innovation, resulting in more formulas achieving docosahexaenoic acid concentrations similar to those in breast milk. Recent updates to labeling laws mandate clearer information about the origin of dairy ingredients, aligning with consumer demand for greater ingredient traceability. These regulations not only ensure baseline safety but also enable brands to differentiate through clinical validation, ethical sourcing, and clean label positioning. Consequently, products available through pharmacy channels, accounting for a portion of sales in Italy and Spain, benefit from heightened credibility, reinforcing a market where regulatory adherence translates into consumer preference and professional endorsement.

MARKET RESTRAINTS

Intensifying Public Health Campaigns Promoting Breastfeeding Suppress Formula Consumption

National and EU-level initiatives continue to prioritize breastfeeding as the gold standard for infant nutrition, a factor that constrains the addressable market for formula and the growth of the Europe infant nutrition market. Many European nations have adopted initiatives in maternity settings that prioritize breastfeeding and limit the use of infant formula to cases with specific medical indications. Healthcare facilities in certain regions that have implemented these specialized breastfeeding protocols observe a decrease in the percentage of newborns receiving formula supplementation. Public health campaigns aimed at encouraging breastfeeding in parts of the United Kingdom correspond with a decrease in the overall sales volume of standard formula products. Additionally, generous parental leave policies facilitate longer breastfeeding durations. These institutional and cultural forces diminish demand for standard formulas, particularly in Northern and Western Europe, compelling manufacturers to focus on narrow therapeutic or organic niches that remain subject to strict marketing restrictions under the EU’s interpretation of the International Code of Marketing of Breastmilk Substitutes.

Economic Volatility and Cost Sensitivity Constrain Premium Product Adoption

Persistent inflation and household budget pressures have heightened price sensitivity among European parents, which limits uptake of premium infant nutrition products and expansion of the Europe infant nutrition market. During 2023, high food price inflation in the European Union, including significant increases in the cost of essential products like infant formula, exceeded the rise in average household income. This contributed to a decline in purchasing power, as wage growth failed to keep pace with the cost of living. This burden is especially acute in lower-income regions. Household income levels in certain Eastern European regions are characterized by lower average monthly earnings. Consumer purchasing behavior in Germany shows a trend of shifting from premium or organic infant formulas toward more budget-friendly alternatives to manage household expenses. Market trends in Italy indicate growth in the economy segment, while premium product sales have remained stagnant. These trends reveal a structural vulnerability: as infant formula is often perceived as a discretionary expense, its consumption becomes elastic during economic downturns, pressuring manufacturers’ margins and reducing incentives for high-cost innovation in functional or organic formulations.

MARKET OPPORTUNITIES

Emergence of Personalized Infant Nutrition Driven by Genomic and Microbiome Science

Cutting-edge research in infant gut microbiome development and nutrigenomics is paving the way for personalized nutrition solutions in the region, which is predicted to fuel the growth of the Europe infant nutrition market. Research indicates that a significant portion of an infant's gut microbiota is established early in life, potentially influencing long-term metabolic and immune health. Studies suggest that formulas supplemented with specific human milk oligosaccharides may lead to a microbiome composition more closely resembling that of breastfed infants. Nutritional companies are introducing products designed to support the infant microbiome, often collaborating with academic researchers. Public funding supports research into personalized early-life nutrition. Consumer interest exists for specialized formulas aligned with infant nutritional needs. This convergence of science, policy support, and consumer receptivity positions personalized nutrition as a high-potential growth vector beyond conventional product categories.

Expansion of E-Commerce and Direct-to-Consumer Channels Enhances Market Accessibility

Digital retail transformation is dramatically improving access to specialized infant nutrition across geographically diverse European markets. This provides fresh prospects for the Europe infant nutrition market. Many households in European countries use online shopping, and products for infants are a quickly expanding part of this market. In areas where pharmacies are not common outside cities, online stores have made it easier to get special baby formulas. Online shopping helps solve problems with getting these specific baby formulas to more people, especially where there are fewer physical stores. A growing number of shoppers are choosing to receive baby formula regularly through subscription plans to make sure they have a steady supply. Regulatory evolution supports this shift. The European Commission’s digital labeling guidelines permit QR code-based access to full sourcing and nutritional data, aligning with transparency demands. Direct-to-consumer brands such as Kendamil and Holle integrate telehealth consultations and social media engagement to build trust and loyalty. This digital ecosystem reduces distribution barriers, lowers customer acquisition costs, and enables rapid iteration based on real-time feedback, which makes e-commerce a strategic engine for both market penetration and innovation diffusion.

MARKET CHALLENGES

Supply Chain Vulnerabilities Expose the Market to Ingredient Sourcing Disruptions

Supply chain fragility, due to concentrated sourcing of critical raw materials, challenges the growth of the Europe infant nutrition market. The production of high-purity ingredients for nutritional products is geographically concentrated within a small number of regions. Reliance on a localized cluster of specialized processing facilities creates potential vulnerabilities in the international supply chain. Disruptions in one major market can impact the availability of essential components used in manufacturing across other regions. Interconnected global networks mean that a localized shortage of specialty additives can lead to broader instabilities in the production of infant nutrition. Climate-related dairy output volatility adds further strain. Prolonged drought conditions in Southern Europe during the 2023 season, particularly in Spain and Italy, strained dairy production by reducing water availability and forage, causing significant pressure on dairy herd management and contributing to a decline in milk yields in those specific regions. Geopolitical instability also impacts inputs. Ukraine’s role as a source of sunflower oil and vitamins meant that the war triggered reformulation efforts across multiple brands. Assessments of ingredient procurement suggest that dependence on a narrow range of suppliers for components like specific probiotics and nucleotides increases the risk of manufacturing disruptions. Maintaining ingredient uniformity in certain nutrition sectors requires dual sourcing approaches and holding supplementary inventories. Employing these methods to reduce risk leads to increased operational expenditures, indicating that reliance on concentrated supply chains presents a difficulty for enduring production resilience.

Mounting Regulatory Scrutiny Over Health Claims and Ingredient Safety

Regulatory bodies across Europe are intensifying oversight of scientific substantiation and ingredient safety in infant formulas, which negatively impacts the expansion of the Europe infant nutrition market. Regulatory reviews of health claims often find that submitted clinical evidence does not consistently meet the required standards. Evaluations of nutritional products sometimes identify safety considerations regarding specific probiotic strains intended for early life consumption. Proposed amendments to regulations for infant products are influenced by studies finding certain compounds at higher levels than desired. These evolving standards necessitate extensive re-formulation and re-validation, with manufacturers reporting average approval timelines of eighteen months for ingredient substitutions. National agencies add another layer. Such scrutiny, while protective of infant health, slows innovation and discourages investment in novel functional ingredients, ultimately constraining the pace at which scientifically advanced nutrition solutions can reach European consumers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.37% |

| Segments Covered | By Type, Formulation, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Mead Johnson & Company, Nestle, Abbott, Danone, Meiji Holdings, Synutra International Inc, Beingmate Group, The Kraft Heinz Company, Glanbia, and Perrigo Company |

SEGMENTAL ANALYSIS

By Type Insights

The infant milk formula segment accounted for 41.4% of the regional market share in 2025. Infant milk formula remains indispensable for newborns in the zero-to-six-month age group, particularly when breastfeeding is medically contraindicated or logistically unfeasible. According to the World Health Organization, many European infants receive some formula within the first month of life, with supplementation rates reported as higher in urban maternity wards of countries such as Germany and Italy. This early life reliance stems from physiological realities such as maternal hypogalactia, which affects a portion of postpartum women as documented by the European Board of Neonatology, and structural factors like limited parental leave duration in several EU states. Consequently, infant milk formula is not a discretionary purchase but a medical and nutritional necessity during a biologically critical window, ensuring consistent baseline demand. Manufacturers reinforce this indispensability through compliance with EU compositional mandates requiring iron, vitamin D, and docosahexaenoic acid at levels calibrated to support neurodevelopment and immune function, further cementing its central role in infant feeding protocols across hospitals, pharmacies, and households.

The specialty baby milk formula segment is the fastest-growing segment and is estimated to register a CAGR of 9.3% over the forecast period, owing to the escalating incidence of food allergies and inborn errors of metabolism among European infants. As per the European Academy of Allergy and Clinical Immunology, cow’s milk protein allergy affects a small but growing share of infants across the EU, with diagnosis rates rising due to enhanced clinical awareness and standardized testing protocols. Similarly, national newborn screening programs have increased early detection of conditions like phenylketonuria and galactosemia, which collectively affect a small proportion of live births according to the European Reference Network for Rare Metabolic Disorders. These diagnoses necessitate lifelong or stage-specific use of medically tailored formulas, which creates a captive and growing patient pool. With public healthcare systems in Germany, Sweden, and the Netherlands covering a significant portion of specialty formula costs, access barriers are low, ensuring consistent and expanding consumption that outpaces demographic trends in the general infant population.

By Formulation Insights

The powdered segment led the market by holding 85.1% of the European infant nutrition market share in 2025. Powdered infant formula remains the preferred choice across European households and institutional settings due to its superior cost-to-volume ratio and logistical advantages. According to Eurostat, powdered formula is significantly more affordable than ready-to-feed alternatives, a critical differentiator in an era of persistent inflation. This affordability is especially consequential in Eastern and Southern Europe, where disposable income constraints amplify price sensitivity. In countries such as Romania and Greece, most formula sales occur in powder form, as reported by national retail audits. Additionally, powdered formulas exhibit a shelf life of up to 24 months when unopened compared to shorter durations for liquid formats, reducing waste and enabling bulk purchasing. These attributes make powder the default option for public procurement programs such as those managed by Spain’s Ministry of Health for neonatal units and for families managing long-term feeding needs, particularly for infants requiring specialty nutrition. The economic and practical efficiencies of powder thus ensure its entrenched position despite the convenience appeal of liquid formats.

The ready-to-feed segment is the fastest-growing formulation segment in Europe and is anticipated to register a CAGR of 10.3% over the forecast period due to changing family dynamics in high-income urban centers, where time scarcity and convenience are paramount. As per Eurofound, many households with infants in cities such as London, Paris, and Amsterdam include two full-time working parents, creating strong demand for time-saving feeding solutions. Ready to feed eliminates the need for water sterilization, precise scooping, and bottle preparation as these are the steps that take several minutes per feed according to time use studies. In Germany, sales of ready-to-feed formats in metropolitan areas grew in 2024, per retail tracking data, driven by premium brands like HiPP and Holle that position their products as sterile, travel-friendly, and ideal for nighttime or on-the-go feeding. The segment’s appeal is further amplified by rising night nanny and childcare services in Western Europe, where professionals prefer ready-to-feed for its consistency and reduced preparation error risk, embedding it within modern infant care ecosystems.

REGIONAL ANALYSIS

Germany Infant Nutrition Market Analysis

Germany stood as the largest infant nutrition market in Europe and commanded for 23.5% of the regional market share in 2025. The country’s market strength stems from its robust healthcare infrastructure, high awareness of nutritional science, and significant demand for both standard and specialty formulas. According to Destatis, Germany recorded hundreds of thousands of live births in 2024, with many mothers supplementing with formula within the first month, as documented by the German Federal Centre for Health Education. The market is heavily pharmacy-driven, with a majority of infant formula units sold through apotheken, where pharmacists provide personalized recommendations based on infant health profiles. Public health policy further supports the sector, as Germany’s statutory health insurance covers medically prescribed hydrolyzed or amino acid-based formulas for infants diagnosed with cow’s milk protein allergy according to the German Society for Pediatric Gastroenterology. Additionally, stringent national adherence to EU compositional standards and strong domestic manufacturing led by companies like Hero and Hochdorf ensures consistent product availability and quality, reinforcing Germany’s position as both a consumption leader and innovation hub in European infant nutrition.

France Infant Nutrition Market Analysis

France was the second leading regional segment in the European infant nutrition market in 2025. The growth of France in the European market is attributed to its deeply integrated healthcare system and high reliance on medically endorsed nutrition. As per the French National Institute of Statistics and Economic Studies, France registered hundreds of thousands of births in 2024, yet exclusive breastfeeding rates at six months remain relatively low according to the French Ministry of Solidarity and Health. This gap fuels consistent formula demand, particularly for products aligned with national dietary guidelines that emphasize iron and omega three fortification. A defining feature of the French market is partial reimbursement of infant formula through the national health insurance system for infants with diagnosed allergies or digestive disorders, according to the French Health Insurance Fund. Pharmacies dominate distribution, accounting for a large share of sales as reported by Syndicat National des Industries de l’Alimentation Infantile. Furthermore, French consumers exhibita strong preference for organic and locally sourced formulas, with organic infant milk representing a significant portion of total formula sales in 2024 as per Agence Bio.

UK Infant Nutrition Market Analysis

The United Kingdom is estimated to witness a promising CAGR in the European infant nutrition market over the forecast period, owing to the evolving feeding practices and strong regulatory oversight post Brexit. The Office for National Statistics reported hundreds of thousands of live births in 2024, while Public Health England data indicates that exclusive breastfeeding rates remain low in the early weeks, creating sustained reliance on formula. Unlike many EU countries, the UK permits limited advertising of follow-on and growing-up milks, enabling greater brand visibility and consumer education, though infant formula remains strictly restricted under the UK Infant Formula Regulations 2023. The market is increasingly polarized between budget private label offerings and premium organic brands, with the latter growing annually according to the UK Department for Environment, Food and Rural Affairs. Notably, the National Health Service’s “Start4Life” program, while promoting breastfeeding, also provides evidence-based guidance on formula preparation. Additionally, the UK’s high penetration of e-commerce accelerates access to niche and imported specialty formulas, as per Ofcom, fostering a dynamic and responsive market that balances public health messaging with pragmatic consumer needs.

Italy Infant Nutrition Market Analysis

Italy is expected to exhibit a notable CAGR in the Europe infant nutrition market over the forecast period, owing to the cultural feeding traditions and rising health consciousness among new parents. Istituto Nazionale di Statistica recorded hundreds of thousands of births in 2024, and while breastfeeding initiation is high, early supplementation is common due to maternal employment, according to Eurofound. This reality sustains demand for follow-on and growing-up milks, which together account for a large portion of formula volume sales as per Federazione Industrie Alimentari. Italy also exhibits strong regional preferences, with Northern regions favoring premium European brands while Southern regions show higher uptake of economy-tier products amid economic disparities. A key growth catalyst is the rising diagnosis of food sensitivities, as per the Italian Society of Pediatrics, some infants suffer from non-IgE mediated cow’s milk reactions, driving sales of partially hydrolyzed formulas. Moreover, Italian consumers prioritize “made in Italy” dairy provenance, with domestic manufacturers like Plasmon leveraging local milk sourcing as a trust signal.

Spain Infant Nutrition Market Analysis

Spain is anticipated to account for a noteworthy share of the European infant nutrition market over the forecast period, owing to the demographic pressures and growing reliance on scientifically formulated nutrition. According to Spain’s National Statistics Institute, the country recorded hundreds of thousands of births in 2024, continuing a decade-long decline linked to Europe’s low fertility rate. Despite this, per capita formula consumption is rising, as exclusive breastfeeding rates remain relatively low according to the Spanish Ministry of Health. The market is distinguished by strong pharmacy channel dominance, with a majority of sales occurring in farmacias where pharmacists act as trusted advisors. Public healthcare supports access to specialty formulas, with regional systems like Catalonia’s covering costs for infants with diagnosed allergies according to the Spanish Agency of Medicines and Medical Devices. Additionally, Spanish parents increasingly seek formulas with added probiotics and nucleotides, aligning with Mediterranean health paradigms. Sales of such functional products grew in 2024, as per the Spanish Federation of Nutrition Industries.

COMPETITION OVERVIEW

Competition in the Europe infant nutrition market is characterized by high barriers to entry, stringent regulatory requirements, and intense focus on scientific credibility. Established multinational companies dominate through deep integration with healthcare systems, pharmacy networks, and robust research pipelines. The market is not driven by price but by trust, clinical validation, and compliance with evolving EU safety standards. Players differentiate through specialty formulation,s personalized nutrition, and sustainability initiatives such as recyclable packaging and carbon-neutral production. Innovation in human milk oligosaccharides, probiotics, and allergen-free profiles is central to competitive positioning. While demographic pressures like declining birth rates constrain overall volume growth, companies offset this by targeting premium and medically indicated segments. Digital engagement through parenting platforms, telehealth, and e-commerce further sharpens competitive dynamics as brands seek direct relationships with informed and cautious European caregivers.

KEY MARKET PLAYERS

A few major players of the Europe infant nutrition market include

- Mead Johnson & Company

- Nestle

- Abbott

- Danone

- Meiji Holdings

- Synutra International Inc

- Beingmate Group

- The Kraft Heinz Company

- Glanbia

- Perrigo Company

Top Strategies Used by the Key Market Participants

Key players in the Europe infant nutrition market prioritize scientific innovation through clinical research and partnerships with pediatric institutions to validate product efficacy. They invest heavily in regulatory compliance, ensuring formulations strictly adhere to EU compositional and labeling mandates. Companies are increasingly adopting sustainable packaging and transparent ingredient sourcing to align with European consumer values. Expansion of direct-to-consumer and e-commerce channels enhances accessibility, particularly in underserved regions. Additionally, firms focus on specialty nutrition segments such as hypoallergenic and metabolic formulas to address rising pediatric health concerns. Strategic collaborations with pharmacies and healthcare systems solidify professional endorsement and distribution dominance. Continuous product reformulation based on emerging nutritional science and microbiome research further differentiates offerings in a highly regulated and competitive landscape.

Leading Players in the Market

- Nestlé S A is a leading force in the Europe infant nutrition market through its globally recognized NAN and BEBA brands. The company leverages extensive pediatric research and clinical partnerships to develop formulas enriched with human milk oligosaccharides and probiotics tailored to European regulatory and nutritional standards. In recent years, Nestlé has accelerated its focus on sustainability and clean label formulations, launching recyclable packaging and reducing palm oil content across its European infant formula portfolio. Its investment in digital parenting platforms and direct-to-consumer channels further strengthens engagement with health-conscious caregivers while reinforcing scientific credibility through collaborations with European pediatric societies.

- Danone S A operates prominently in Europe under its Aptamil and Nutrilon brands, offering science-backed infant and follow-on formulas aligned with EU compositional mandates. The company has deep integration with pharmacy and healthcare networks, particularly in France, Germany, and the UK, where its products are frequently recommended by paediatricians. Danone recently enhanced its market position by expanding its portfolio of specialty formulas for allergy-prone infants and advancing clinical trials on gut microbiome modulation. It also prioritized traceability by implementing blockchain-enabled dairy sourcing in the Netherlands and launched carbon-neutral certified products in Sweden to meet rising demand for sustainable nutrition solutions.

- Reckitt Benckiser Group supports the Europe infant nutrition segment primarily through its Enfamil and Nutramigen brands, focusing on medical and hypoallergenic formulations. The company emphasizes clinical validation and partnerships with neonatal units across Western Europe to ensure its specialty products meet stringent hospital protocols. In recent actions, Reckitt strengthened its European footprint by modernizing its production facility in the Netherlands to comply with updated EU hygiene standards and expanding its e-commerce distribution in Southern Europe. It also intensified digital health collaborations, offering virtual nutrition consultations to new parents, thereby embedding its products within integrated infant care ecosystems and reinforcing trust among medical professionals and caregivers.

RECENT HAPPENINGS IN THE MARKET

- In March 202,4 Nestlé launched a new line of carbon-neutral certified infant formulas in Germany and France using fully recyclable packaging and dairy sourced from regenerative farms. This initiative reinforced its sustainability leadership and aligned with EU Green Deal consumer expectations.

- In June 2024, Danone expanded its Aptamil specialty range in the UK and Spain with new extensively hydrolyzed formulas clinically proven to reduce eczema risk in high allergy risk infants. This move strengthened its presence in the fast-growing medical nutrition segment.

- In September 2024, Reckitt Benckiser upgraded its Nutramigen production facility in the Netherlands to meet the European Commission’s updated sterility and traceability standards for amino acid-based formulas. This ensured an uninterrupted supply to neonatal units across Western Europe.

- In November 2024, Danone partnered with the Karolinska Institute in Sweden to launch a digital nutrition platform offering personalized feeding guidance based on infant gut microbiome profiles. This enhanced itsdirect-to-consumerr engagement and scientific differentiation.

- In January 2025, Nestlé introduced ablockchain-enabledd traceability system for its BEBA organic formulas in Switzerland and Austria, allowing parents to verify dairy origin and processing steps. This action boosted transparency and reinforced premium positioning in high-income markets.

MARKET SEGMENTATION

This research report on the Europe infant nutrition market has been segmented and sub-segmented based on type, formulation, and region.

By Type

- Infant Milk Formula

- Follow-Up Milk Formula

- Growing Up Milk Formula

- Specialty Baby Milk Formula

By Formulation

- Powder

- Liquid Concentrate

- Ready to Feed

By Region

- UK

- France

- Spai

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech

- Republic

- Rest of Europe

Frequently Asked Questions

1. What is the growth outlook?

Analysts expect continued growth driven by health awareness, rising disposable incomes, and demand for premium and organic products. Some segments (e.g., infant formula) are forecast to grow at mid-single-digit CAGRs through the late 2020s/early 2030s.

2. Which countries lead the market in Europe?

Major markets often include Germany, France, and the UK due to larger populations of young families, high purchasing power, and well-developed retail channels

3. How is the market segmented?

Key segments include by product type( infant formula, baby food purees, cereals, snacks), organic/specialty nutrition, by age group (0-6 months, 6-12 months, 12-24 months, etc), and distribution channel (retail, pharmacy, and increasing e-commerce)

4. What are the major growth drivers?

Primary drivers include rising health consciousness among parents focusing on balanced, nutrient-rich infant foods, increasing disposable incomes enabling purchases of premium and organic products, and the expansion of e-commerce giving wider access to niche and international brands.

5. What challenges does the market face?

Key restraints include stringent regulatory requirements for food safety, labeling, and nutrient standards, high competition from established global and regional players, and demographic headwinds in parts of Europe with declining birth rates.

6. What role does regulation play?

Regulations in Europe emphasize nutritional safety, clear labeling, and allergen information on infant food products, aimed at protecting consumer health and enabling informed choices.

7. What trends are shaping product innovation?

Current trends include a shift toward organic, clean-label, allergen-free, and specialty nutrition products, Functional ingredients such as prebiotics, probiotics, DHA, and plant-based formulations, and Packaging innovations offering transparency and sustainability.

8. Who are the key players in the market?

The market includes major multinational brands and regional leaders such as Nestlé, Danone, Abbott, FrieslandCampina, and specialized organic baby food brands, all investing in product innovation and distribution expansion.

9. How do distribution channels differ across Europe?

Traditional supermarkets and pharmacies still hold a significant share, but e-commerce and direct-to-consumer sales are growing rapidly, especially for premium and niche products.

10. How do demographic and socioeconomic factors influence the market?

Factors such as dual-income households, urban lifestyles, parental education on nutrition, and cultural preferences influence product demand and uptake of premium and functional infant nutrition items.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com