Europe Influenza Market Research Report By Product Type, Consumer and Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe) - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2026 to 2034)

Market Size, 2025

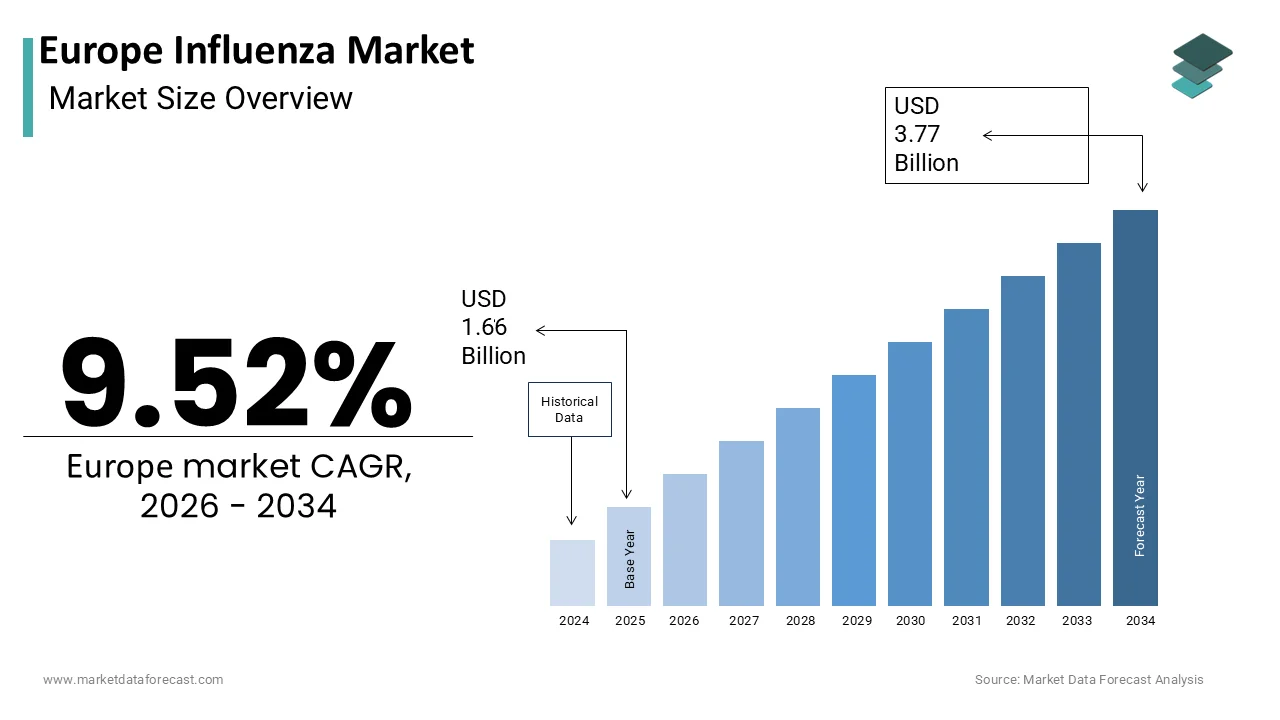

$1.66 BnMarket Estimate, 2026

$1.82 BnMarket Forecast, 2034

$3.77 BnCAGR, 2026–2034

9.52%Europe Influenza Market Summary

The Europe influenza market was valued at USD 1.52 billion in 2024, is estimated at USD 1.66 billion in 2025, and is projected to reach USD 3.45 billion by 2033, growing at a CAGR of 9.52% from 2025 to 2033, driven by aging demographics, expanding national vaccination mandates, rising adoption of enhanced vaccine formulations, and strengthened cross-border influenza preparedness under the European Health Union framework.

Key Market insights

- 2024 (actual): USD 1.52 billion

- 2025 (est): USD 1.66 billion

- 2033 (forecast): USD 3.45 billion

- CAGR (2025–2033): 9.52%

Quick growth drivers

- Rapid expansion of the elderly population with high influenza-related morbidity and mortality risk.

- Government-funded national immunization programs aligned with European Centre for Disease Prevention and Control and World Health Organization strain recommendations.

- Broadened vaccination eligibility covering healthcare workers, pregnant women, and high-risk chronic disease populations.

- Increasing preference for adjuvanted and high-dose vaccines to counter immune senescence.

- Strengthened seasonal preparedness and stockpiling under the European Health Union framework.

Principal restraints

- Persistent vaccine hesitancy among working-age adults and non-elderly high-risk populations.

- Suboptimal vaccination uptake outside senior cohorts despite policy availability.

- Biological and logistical limitations of egg-based vaccine manufacturing with long lead times.

High-value opportunities

- Accelerated adoption of enhanced vaccines (high-dose, adjuvanted, cell-based, recombinant).

- Integration of influenza vaccination with RSV and pneumococcal campaigns.

- Expansion of pharmacy-led and workplace vaccination programs.

- Growth of antiviral utilization through updated early-treatment clinical guidelines.

Key operational challenges

- Antigenic mismatch driven by rapid viral drift and delayed strain selection cycles.

- Fragmented national procurement systems causing supply imbalances and wastage.

- Uneven surveillance and real-time strain reporting across Eastern and Western Europe.

Fastest-growing segments

- Antiviral drugs: 8.1% CAGR driven by early-treatment protocols and pandemic stockpiling.

- Adjuvanted & high-dose vaccines: fastest uptake within vaccines due to superior elderly protection.

- Combined respiratory campaigns: influenza co-administration with RSV and pneumococcal vaccines.

Regional leadership & dynamics

- Germany: Market leader with high senior coverage, strong statutory reimbursement, and national stockpiles.

- United Kingdom: Centralized NHS campaigns with rapid uptake of enhanced vaccines.

- France: Expanding free-vaccination eligibility and mandatory coverage for defined worker groups.

- Italy & Spain: Strong growth driven by aging populations and expanded regional outreach programs.

What wins commercially

- Alignment with national immunization calendars and procurement cycles.

- Differentiated vaccines offering improved immunogenicity in elderly populations.

- Reliable manufacturing scale and long-term government supply contracts.

- Participation in surveillance, effectiveness monitoring, and public-health partnerships.

Top strategic ask for executives

- Prioritize enhanced vaccine platforms and real-world effectiveness evidence.

- Support coordinated EU-level seasonal procurement and forecasting mechanisms.

- Expand education and confidence-building campaigns to close uptake gaps.

- Strengthen integration of influenza prevention into multi-disease respiratory strategies.

Leading players

Sanofi Pasteur · Seqirus · Roche · GSK · AstraZeneca

Europe Influenza Market Size

The Europe influenza market is projected to grow from USD 1.66 billion in 2025 to USD 1.82 billion in 2026 and reach USD 3.77 billion by 2034, registering a CAGR of 9.52% during the forecast period from 2026 to 2034.

Influenza remains a significant public health burden, with annual epidemics causing substantial morbidity, healthcare strain, and economic loss. According to the European Centre for Disease Prevention and Control, seasonal influenza is associated with tens of thousands of deaths annually in Europe, with the highest mortality occurring among adults aged 65 and older and individuals with chronic comorbidities. The market operates under coordinated frameworks such as the EU Joint Procurement Agreement for pandemic preparedness and national immunization programs aligned with World Health Organization strain recommendations. As per Eurostat, EU member states procure tens of millions of influenza vaccine doses each year for seasonal campaigns, reflecting sustained public‑health prioritization. Recent advances in adjuvanted, cell‑based, and recombinant vaccine platforms are gradually supplementing traditional egg‑based production, which is enhancing strain fidelity and scalability. The market is further shaped by the EU’s 2023 adoption of the European Health Union, which mandates strengthened cross‑border surveillance and equitable vaccine access, embedding influenza response within broader health‑security architecture.

MARKET DRIVERS

Aging Population and Heightened Vulnerability to Influenza Complications

Europe’s rapidly aging demographic profile is a primary driver of sustained demand for influenza prevention and treatment solutions, which is driving the European influenza market growth. According to Eurostat, 21.6% of the EU population was aged 65 or older in 2025, reflecting a long‑term demographic shift. This cohort faces significantly elevated risks of severe influenza outcomes; as per the European Centre for Disease Prevention and Control,l adults over 65 account for the majority oinfluenza-relateded hospitalizations and fatalities in Europe each year. National immunization policies reflect this vulnerability, with Germany, France, and Italy mandating or strongly recommending free seasonal influenza vaccination for all seniors, with uptake targets of 75% under the EU’s 2009 Council Recommendation. In the United Kingdom, official NHS data for the 2023–2025 season reported vaccination coverage of more thanthree-quarterss among those aged 65 and above, supporting reductions in winter hospital admissions. Furthermore, the European Medicines Agency has prioritized approval of high-dose and adjuvanted vaccines specifically designed for immune senescence, such as Sanofi’s Fluzone High Dose and Seqirus’ Fluad. These tailored products address diminished immune responsiveness in older adults, reinforcing public health reliance on advanced influenza countermeasures across an increasingly geriatric population.

Expansion of National Influenza Vaccination Mandates and Target Group Broadening

European governments are progressively expanding influenza vaccination eligibility beyond the elderly to include broader at-risk populations and essential workers, which is significantly amplifying prophylactic demand and contributing to the European influenza market expansion. According to the European Centre for Disease Prevention and Control, many EU member states recommend annual influenza vaccination for healthcare workers, with several northern countries reporting high compliance. In 202,4 France extended its free vaccination program to include individuals with obesity (BMI over 30), diabetes, and chronic respiratory conditions by adding a substantial number of people to its target cohort. Similarly, Germany’s Standing Committee on Vaccination added pregnant women in all trimesters to its universal recommendation list in 2023, which is citing evidence of reduced neonatal influenza risk. As per the European Commission’s 2025 State of Vaccine Confidence Report, rt school-based influenza vaccination pilots in the Netherlands and Portugal achieved strong parental participation, indicating feasibility for broader pediatric rollout. These policy shifts are driven by cost-benefit analyses as Health Technology Assessment bodies in Sweden and Belgium report that expanding vaccination coverage reduces outpatient visits during peak season, supporting system‑wide efficiency. This systematic widening of eligible groups transforms influenza immunization from a narrow geriatric intervention into a comprehensive public health strategy.

MARKET RESTRAINTS

Vaccine Hesitancy and Suboptimal Uptake in Key Target Populations

Persistent vaccine hesitancy among segments of the European population remains a significant restraint on influenza market penetration, particularly in working-age adults and younger high-risk groups. According to the 2025 Eurobarometer Survey on Vaccine Confidence, around one-third of Europeans expressed doubts about the necessity or safety of annual influenza vaccination, with skepticism highest in several Western and Eastern member states. National immunization data reflects this gap. As per the European Centre for Disease Prevention and Control,l vaccination uptake among adults aged 18 to 64 with chronic conditions remains below recommended levels in many EU countries. Misinformation amplified through social media plays a key role. The EUvsDisinfo Task Force documented widespread false or misleading narratives about influenza vaccines during the 2023–2025 season, contributing to public uncertainty. This hesitancy limits the public health impact of existing programs and reduces procurement predictability for manufacturers. Even in countries with strong healthcare systems, such as Germany, Robert Koch Institute data shows that fewer than half of the recommended high risk non elderly adults received vaccination in recent seasons. Overcoming this cognitive barrier requires sustained investment in science communication and trusted community outreach, without which market growth remains capped by behavioural resistance rather than supply constraints.

Delays and Inefficiencies in Egg-Based Vaccine Production Timelines

The continued reliance on egg-based manufacturing for the majority of Europe’s seasonal influenza vaccines introduces inherent biological and logistical constraints that limit responsiveness and efficacy, which further hampers the European influenza market growth. According to the European Medicines Agency, egg-based production can introduce antigenic changes that reduce vaccine match and effectiveness, particularly when circulating strains evolve rapidly. Furthermore, the production cycle requires at least six months from WHO strain selection to final distribution, leaving little room for mid-season adjustments. As per the European Commission’s Health Emergency Preparedness and Response Authority, production disruptions at major egg-based facilities have previously caused delivery delays to multiple member states, affecting national campaign timing. These vulnerabilities are particularly problematic in pandemic scenarios, where speed is critical. Although cell-based and recombinant platforms offer faster timelines. According to the data from the European Vaccine Manufacturers Association, these technologies still represent a minority share of the EU influenza vaccine supply. Until production diversification accelerates, the market remains exposed to biological unpredictability and supply chain fragility inherent in avian egg dependence.

MARKET OPPORTUNITIES

Accelerated Adoption of Adjuvanted and High-Dose Vaccines for Enhanced Immunogenicity

An emerging opportunity in the European influenza market lies in the rapid uptake of next-generation vaccines engineered to overcome immune senescence and improve real-world effectiveness. Adjuvanted and high-dose formulations, which stimulate stronger and more durable immune responses in older adults, are gaining preferential status in national procurement policies. According to European health technology assessment reports, several EU countries,s including Italy, Spain, and the Netherlands, ds reimburse adjuvanted influenza vaccines for seniors based on demonstrated cost-effectiveness, reflecting growing policy alignment. In 2025, Germany’s Federal Joint Committee approved premium reimbursement for high-dose quadrivalent vaccines after real-world evidence from the Robert Koch Institute showed reduced influenza-related hospitalizations among adults aged 75 and older, supporting preferential use. Similarly, the UK’s Joint Committee on Vaccination and Immunization recommended transitioning all adults over 65 to enhanced vaccines by 2026. As per a 2025 analysis published in The Lancet Infectious Diseases, adjuvanted vaccines significantly improve antibody responses in elderly populations, reinforcing their clinical value. This scientific and reimbursement momentum is transforming enhanced vaccines from niche options into standard of care, opening a high-value segment with limited generic competition.

Integration of Influenza Vaccination into Broader Respiratory Disease Prevention Programs

A strategic opportunity is unfolding through the bundling of influenza immunization with other respiratory disease interventions, particularly in the post pandemic era of integrated respiratory surveillance. European public health authorities are increasingly co-administering influenza and RSV vaccines during autumn campaigns to maximize coverage and logistical efficiency. According to the European Centre for Disease Prevention and Control, multiple EU countries launched combined influenza RSV vaccination pilots in 2025, targeting older adults and immunocompromised groups, reflecting a shift toward integrated respiratory protection. In Sweden and Denmark, pharmacies now offer simultaneous influenza and pneumococcal vaccination under a single appointment model, with national public health data showing higher uptake compared to separate scheduling, demonstrating operational benefits. The European Commission’s 2025 Cross Disease Preparedness Strategy explicitly endorses this convergence, allocating funding for shared cold chain infrastructure and digital appointment systems. Additionally, workplace wellness programs in Germany and the Netherlands are incorporating influenza vaccination into annual health checks alongside spirometry and smoking cessation counselling. This holistic approach not only improves public health outcomes but also creates stable multi-disease demand streams that enhance planning reliability for vaccine manufacturers and distributors.

MARKET CHALLENGES

Antigenic Mismatch Due to Rapid Viral Drift and Surveillance Gaps

A persistent challenge facing the European influenza market is the frequent antigenic mismatch between circulating strains and vaccine components, undermining public confidence and clinical impact. Influenza viruses undergo continuous antigenic drift, and the six-to-eight-month lead time for egg-based production often results in vaccines that poorly reflect dominant strains by the time of administration. According to the European Influenza Surveillance Network, vaccine effectiveness varies widely by season and strain, with reduced protection observed when late emerging variants diverge fromWHO-selectedd strains, as seen in recent H3N2‑dominant seasons. Surveillance gaps exacerbate this issue. Eastern European countries report influenza data with an average delay compared to Western counterparts, limiting real-time strain tracking. As per the European Centre for Disease Prevention and Control, mismatches can reduce vaccine effectiveness to low levels in some seasons, contributing to public skepticism. This scientific limitation fuels public uncertainty and complicates health economic justifications for expanded programs. Until real-time genomic sequencing and rapid manufacturing platforms become standard, the market will remain vulnerable to biological unpredictability that erodes both efficacy and trust.

Fragmented Procurement Systems and Lack of Pan-European Vaccine Harmonization

The absence of a unified European influenza vaccine procurement and distribution mechanism creates inefficiencies that hinder equitable access and emergency responsiveness, which further challenge the expansion of the European influenza market. While the EU Joint Procurement Agreement exists for pandemic scenarios, seasonal vaccine acquisition remains fragmented across 27 national systems with divergent timelines, strain preferences, and delivery models. According to the European Court of Auditors, procurement timelines vary significantly across member states, contributing to supply imbalances and inconsistent campaign starts. In 2023, Poland faced a shortfall in high-dose vaccine deliveries due to late tendering, while Belgium reported excess inventory of standard doses that expired unused. This fragmentation also impedes investment in next-generation platforms as manufacturers face uncertain demand signals when each country negotiates separately. As per the European Commission’s 2025 assessment,t only a limited number of countries opted into the proposed voluntary seasonal vaccine coordination mechanism, whichreflectsg slow progress toward harmonization. Without deeper alignment in forecasting, strain selection, and logistics, the market remains prone to waste, inequity, and delayed response during high burden seasons or emerging threats.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Type, Application, Disease Indications, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Sanofi-Pasteur (U.S.), AstraZeneca (United Kingdom), F. Hoffmann-La Roche (Switzerland), Novartis (Switzerland), GlaxoSmithKline (U.K.), Pfizer Inc. (U.S.), Merck & Co. (U.S.), Abbott Laboratories (U.S.), Mitsubishi Tanabe Pharma Corporation (Japan) and CSL Limited (Australia). |

SEGMENTAL ANALYSIS

By Product Type Insights

The vaccines segment overwhelmingly dominated the European influenza market in 2025, owing to their foundational role in public‑health prevention strategies across all EU member states. National immunization programs prioritize vaccination as the primary intervention to reduce influenza‑related hospitalizations, mortality, and healthcare strain during seasonal peaks. According to the Paul‑Ehrlich‑Institut, more than 20 million influenza vaccine doses were released in Germany alone for the 2023–2025 season, reflecting strong regional demand within Europe’s broader vaccination framework. Scientific consensus further reinforces vaccine value: data from national public‑health agencies show that vaccinated adults over 65 experience significantly lower rates of ICU admission during seasonal waves. The European Commission’s 2023 Influenza Preparedness Action Plan also mandates minimum vaccine stockpiles across member states, creating predictable annual procurement cycles aligned with WHO strain updates. Unlike therapeutics, which are used reactively, vaccines operate within structured, recurring national programs to ensure stable, scalable, and policy‑anchored market dominance. Vaccines are expected to maintain their leadership over the forecast period as EU immunization strategies continue to emphasize prevention and high‑risk population coverage.

The drugs segment is the fastest-growing component of the European influenza market and is expected to record a CAGR of 8.12% over the forecast period, owing to the evolving clinical guidelines that now endorse early antiviral use not only for severe cases but also for outpatient management in high‑risk populations. According to the European Society of Clinical Microbiology and Infectious Diseases, 2025 treatment protocols recommend initiating antivirals within 48 hours of symptom onset for adults over 65 or those with chronic comorbidities, expanding the eligible treatment population substantially. National stockpiling initiatives also contribute. According to the European Commission’s Health Emergency Preparedness and Response Authority, increased antiviral reserves across many member statesares part of pandemic‑readiness planning. The 2025 approval of baloxavir marboxil by the European Medicines Agency further boosts adoption. Antiviral drugs are expected to grow rapidly over the forecast period as clinical guidelines broaden eligibility and member states reinforce pandemic‑preparedness stockpiles.

COUNTRY LEVEL ANALYSIS

Germany Influenza Market Size

Germany had 23.4% of the European influenza market share in 2025 and stood as the top performer in this regional market. The leading position of Germany in the European market is supported by its comprehensive statutory health‑insurance system and strong public‑health infrastructure. According to the Paul‑Ehrlich‑Institut, more than 20 million influenza vaccine doses were released for the 2023–2025 season, reflecting the country’s large‑scale vaccination capacity. Germany maintains high senior‑vaccination rates compared with other EU nations, supported by clear recommendations from the Standing Committee on Vaccination. The country also upholds a national antiviral reserve managed by federal authorities, ensuring preparedness for severe influenza seasons. Strong public trust in institutional health guidance and automated pharmacy recall systems reinforces predictable annual demand. With its robust reimbursement model and established surveillance network, Germany is expected to remain the cornerstone of Europe’s influenza‑response ecosystem.

United Kingdom Influenza Market Size

The United Kingdom captured thesecond-largestt share of the European influenza market in 2025. The growth of the UK in the European market is driven by its centralized National Health Service and highly coordinated vaccination campaigns. According to the NHS England, more than 18 million people were vaccinated in the 2025–2025 season, underscoring the scale of national outreach. The UK consistently achieves strong uptake among older adults, supported by GP networks, community pharmacies, and targeted communication strategies. Enhanced vaccines are widely used for seniors, reflecting the Joint Committee on Vaccination and Immunization’s recommendations. The UK also integrates antiviral access into winter‑preparedness plans, ensuring timely treatment for high‑risk groups. With its strong digital‑health infrastructure and proactive public‑health policies, the UK is positioned to remain one of Europe’s most influential influenza markets.

France Influenza Market Size

France accounts for a prominent share of the European influenza market. The strong public‑health mandates and expanded eligibility criteria are driving the French market expansion. National policy requires influenza vaccination for healthcare workers in specific care settings, reinforcing high compliance levels. France continues to broaden its free‑vaccination program for individuals with chronic conditions, improving accessibility across risk groups. The National Health Insurance Fund fully reimburses influenza vaccines for eligible populations, supporting high annual uptake. Public‑health agencies also run extensive awareness campaigns to increase vaccination among vulnerable groups. With its combination of regulatory action, financial accessibility, and strong institutional oversight, France is expected to maintain its high‑volume market position.

Italy Influenza Market Size

Italy is estimated to witness a healthy CAGR in the European influenza market over the forecast period, owing to its regionalized healthcare system and strong focus on elderly protection. National surveillance data show that influenza affects millions annually, reinforcing the need for widespread vaccination. Italy’s National Prevention Plan coordinates vaccine distribution across regions, ensuring consistent access for older adults and high‑risk groups. Northern regions continue to lead in vaccination uptake, supported by mobile clinics and home‑visit programs for frail seniors. Italy also maintains a national antiviral reserve for severe seasons. With ongoing digital‑health initiatives and targeted outreach, Italy is expected to strengthen its influenza‑prevention capacity in the coming years.

Spain Influenza Market Size

Spain is anticipated to account for a notable share of theEuropeane influenza market during the forecast period, owing to the universal access and strong primary‑care integration. National health authorities emphasize vaccination for adults over 60 and individuals with chronic conditions, with primary‑care nurses delivering the majority of doses. Spain’s warm climate and large elderly population reinforce the importance of seasonal vaccination. Studies highlight the effectiveness of high‑dose influenza vaccines among older adults in Spain, supporting continued investment in enhanced formulations. Regional programs increasingly integrate influenza vaccination with chronic‑disease management and co‑administration strategies for older adults. With its strong public‑health infrastructure and proactive outreach, Spain is positioned to remain a model for equitable influenza protection in Southern Europe.

COMPETITIVE LANDSCAPE

The European influenza market features structured competition anchored in public health procurement rather than consumer dynamics. Vaccine manufacturers compete on scientific validation, regulatory compliance,e and alignment with national aging society strategies rather than price alone. The market is dominated by a few global players with established manufacturing infrastructure and long-term government contracts ensuring predictable annual demand. Antiviral competition remains limited due to the entrenched position of oseltamivir and slow uptake of newer agents like baloxavir outside pandemic scenarios. Differentiation centers on product attributes such as enhanced immunogenicity production platform and dosing convenience. National health authorities act as gatekeepers, influencing formulary inclusion through health technology assessments and reimbursement decisions. While entry barriers are high due to regulatory complexity and scale requirements, the market is evolving toward premium differentiated vaccines,s creating opportunities for innovation. Overall, competition is collaborative in nature, with players functioning as public health partners rather than commercial adversaries.

KEY MARKET PLAYERS

Companies playing a pivotal role in the europe influenza market are

- Sanofi-Pasteur (U.S.)

- AstraZeneca (United Kingdom)

- F. Hoffmann-La Roche (Switzerland)

- Novartis (Switzerland)

- GlaxoSmithKline (U.K.)

- Pfizer Inc. (U.S.)

- Merck & Co. (U.S.)

- Abbott Laboratories (U.S.)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- CSL Limited (Australia)

TOP LEADING PLAYERS IN THE MARKET

- Sanofi Pasteur is a cornerstone of theEuropeane influenza market through its portfolio of seasonal and enhanced influenza vaccines, including VaxigripTetra and Fluzone High Dose. The company leverages itsLyon-basedd European vaccine hub to supply over 50 million annual doses to EU member states under long term public health contracts. In 2025, Sanofi accelerated the rollout of its high-dose quadrivalent vaccine across Germany, France, and Italy, ly following national recommendations for seniors. It also partnered with the European Centre for Disease Prevention and Control to enhance real-world effectiveness monitoring using digital health records. These initiatives reinforce Sanofi’s role in aligning product innovation with evolving European public health priorities while maintaining its leadership in global influenza vaccine supply.

- Seqirus contributes significantly to theEuropeane influenza market as the sole provider of adjuvanted seasonal influenza vaccine Fluad and a major supplier of cell-based vaccines via its Holly Springs and Liverpool manufacturing network. The company benefits from strong adoption in countries prioritizing enhanced immunogenicity for elderly populations. In 2025, Seqirus expanded fill and finish capacity at its UK facility to meet growing demand for adjuvanted formulations in Scandinavia and Benelux nations. It also collaborated with national health institutes to integrate Fluad into combined respiratory vaccination pilots with RSV immunizations. By focusing on next-generation platforms and public health integration, Seqirus strengthens its position as a strategic partner in Europe’s aging society preparedness.

- Roche plays a critical role in the European influenza market through its antiviral drug Tamiflu (oseltamivir), which remains a cornerstone of outpatient and pandemic influenza treatment protocols across the continent. The company ensures a continuous supply through its Basel-based pharmaceutical network and maintains strategic stockpile agreements with multiple EU governments. In 2025, Roche supported the European Medicines Agency’s updated guidance on early antiviral use by funding physician education programs in Spain and Poland. It also enhanced its pharmacovigilance system to monitor real-world safety in high-risk comorbidity groups. These actions solidify Roche’s commitment to therapeutic readiness and reinforce Tamiflu’s entrenched position in European clinical guidelines.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European influenza market prioritize alignment with national immunization policies by tailoring vaccine formulations to elderly and comorbidity-based populations. They invest in next-generation platforms such as adjuvanted high-dose and cell-based vaccines to improve real-world effectiveness and meet regulatory preferences. Strategic partnerships with public health agencies enable participation in surveillance effectiveness monitoring and combined respiratory vaccination initiatives. Companies maintain robust government stockpile agreements for both vaccines and antivirals to ensure emergency readiness. Digital health integration, including electronic immunization records and automated patient recall systems, enhances coverage and compliance. These strategies collectively reinforce public health value, scientific credibility, and supply reliability in a highly regulated and policy-driven market environment.

MARKET SEGMENTATION

This research report on the European influenza market has been segmented and sub-segmented into the following categories.

By Product Type

- Vaccines

- Drugs

By Type

- Safety Biomarkers

- Efficacy Biomarkers

- Validation Biomarkers

By Application

- Diagnostics Development

- Drug Discovery and Development

- Personalized Medicine

- Disease Risk Assessment

- Other Applications

By Disease Indications

- Cancer

- Cardiovascular Disorders

- Neurological Disorders

- Immunological Disorders

- Other Diseases

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which countries dominate the Europe Influenza Market and why?

The United Kingdom leads the Europe Influenza Market with a projected CAGR of 4.2%, followed by Germany (3.9% CAGR) and France, due to robust government vaccination initiatives like the UK's Universal Childhood Influenza Vaccination Program, well-developed healthcare infrastructure, and strong emphasis on preventive healthcare measures.

2. What are the primary drivers of growth in the Europe Influenza Market?

The Europe Influenza Market growth is primarily driven by rising seasonal influenza outbreaks affecting 10-30% of the European population annually, aging demographics with higher vulnerability, government-led vaccination campaigns achieving up to 77% coverage among healthcare workers, and continuous advancements in antiviral drug development.

3. How does the Europe Influenza Market segment by product type?

The Europe Influenza Market is segmented into vaccines and drugs, with vaccines commanding significant market share due to widespread immunization programs recommended by WHO and ECDC for high-risk populations including pregnant women, elderly individuals, children aged six months to five years, and those with chronic health conditions.

4. What are the major challenges facing the Europe Influenza Market?

The Europe Influenza Market faces significant challenges including high treatment costs exceeding €250 per infant case and €130 per elderly case, limited healthcare access in rural Eastern European regions, complex regulatory requirements for new vaccine development, and disparities in healthcare infrastructure across member states.

5. How does vaccination coverage impact the Europe Influenza Market?

Vaccination coverage significantly impacts the Europe Influenza Market, with countries like the UK and Italy achieving up to 55% vaccination rates among elderly populations in 2024, reducing overall disease burden while simultaneously driving demand for preventive treatments and supporting market expansion through government-funded programs.

6. What opportunities exist for growth in the Europe Influenza Market?

The Europe Influenza Market presents substantial opportunities through technological advancements in locally acting antiviral agents, European Medicines Agency approvals of innovative therapies, personalized medicine approaches, increased R&D investments by pharmaceutical companies, and growing medical tourism in emerging European markets.

7. How does the aging population affect the Europe Influenza Market dynamics?

The aging population significantly impacts the Europe Influenza Market as elderly individuals face higher risk of severe flu complications and hospitalization, driving demand for both preventive vaccines and therapeutic antivirals, particularly in countries like Italy and Germany with substantial senior demographics requiring specialized healthcare interventions.

8. What are the key segmentation criteria in the Europe Influenza Market analysis?

The Europe Influenza Market is comprehensively segmented by product type (vaccines and drugs), application (diagnostics development, drug discovery, personalized medicine, disease risk assessment), disease indications (cardiovascular, neurological, immunological disorders), and geographic distribution across UK, Germany, France, Italy, Spain, and other European nations.

9. How do government policies influence the Europe Influenza Market expansion?

Government policies profoundly influence the Europe Influenza Market through mandatory vaccination programs for high-risk groups, reimbursement policies facilitating treatment access, ECDC recommendations for annual immunization, Universal Childhood Influenza Vaccination initiatives, and strategic healthcare funding that collectively support market growth and accessibility.

10. What is the economic burden of influenza in the Europe Influenza Market region?

The economic burden in the Europe Influenza Market is substantial, with treatment costs exceeding €250 per infant case and €130 per elderly case, while Spain recorded over 1,850 influenza-related deaths in 2018, demonstrating the significant financial and healthcare system impact that drives ongoing investment in prevention and treatment solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com