Europe Laparoscopy Devices Market Research Report - Segmented By Product Type (Internal Closure Devices, Hand Access Instruments, Robotic-Assisted Surgical System, Laparoscopes, Direct Energy Systems, Insufflation Devices), Therapeutic Application, End Users & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis From 2024 to 2033

Europe Laparoscopy Devices Market Report Summary

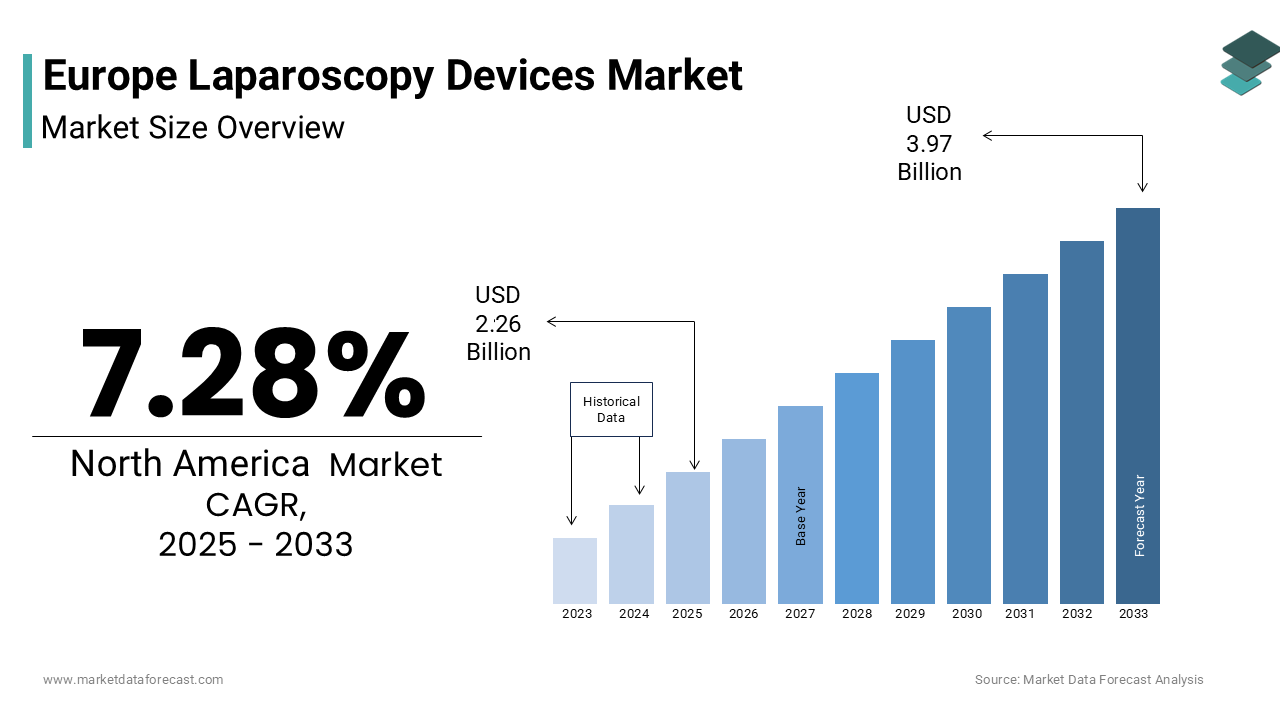

The Europe laparoscopy devices market was valued at USD 2.26 billion in 2025 and is projected to reach USD 4.25 billion by 2034, growing at a CAGR of 7.28% during the forecast period from 2025 to 2033. The growth of the Europe laparoscopy devices market is driven by the rising adoption of minimally invasive surgical procedures, increasing prevalence of chronic and lifestyle-related diseases, and strong clinical preference for procedures that reduce hospital stay and postoperative complications. The expansion of Enhanced Recovery After Surgery (ERAS) protocols, increasing bariatric and oncologic surgeries, and growing integration of robotic-assisted laparoscopy are further fueling market growth. Moreover, supportive reimbursement frameworks, technological advancements in energy-based devices, and growing outpatient surgical volumes are enhancing the adoption of advanced laparoscopic instruments across Europe.

Key Market Trends

- Growing preference for minimally invasive surgical techniques due to reduced postoperative pain, shorter hospital stays, and faster recovery times.

- Rising adoption of robotic-assisted laparoscopy in urology, gynecology, and colorectal surgery for improved precision and surgical outcomes.

- Increasing use of advanced energy-based devices for effective tissue sealing and hemostasis in complex procedures.

- Expansion of ambulatory and day-case laparoscopic surgeries driven by healthcare cost containment initiatives.

- Rising focus on surgeon training, simulation-based education, and standardized laparoscopic skill development programs across Europe.

Segmental Insights

- Based on product type, the direct energy systems segment held the largest share of the Europe laparoscopy devices market in 2024. The segment’s dominance is attributed to its essential role in tissue dissection, vessel sealing, and bleeding control across general, bariatric, and colorectal surgeries, along with regulatory-driven replacement of legacy electrosurgical platforms.

- Based on end user, the hospitals segment accounted for the largest share of the Europe laparoscopy devices market in 2024. This leadership is driven by the concentration of complex surgical procedures, availability of advanced operating room infrastructure, and strong alignment with national health technology assessment and reimbursement systems.

- Based on therapeutic application, the general surgery segment captured a significant share of the Europe laparoscopy devices market in 2024. The segment’s growth is supported by the widespread adoption of laparoscopic cholecystectomy, appendectomy, and hernia repair as standard-of-care procedures across European healthcare systems.

Regional Insights

The Europe laparoscopy devices market is witnessing steady growth across major economies, supported by advanced healthcare infrastructure, standardized surgical protocols, and strong public healthcare funding.

- Germany was the largest contributor to the Europe laparoscopy devices market in 2024, driven by high surgical volumes, early adoption of advanced minimally invasive technologies, and strong reimbursement support for laparoscopic and robotic procedures.

- The United Kingdom continues to perform strongly, supported by centralized procurement systems, outcome-based surgical reporting, and widespread implementation of minimally invasive surgical guidelines.

- France is experiencing robust growth due to rising bariatric and robotic-assisted laparoscopic procedures, supported by national cancer care initiatives and obesity management programs.

- Italy is emerging as a key market, driven by high utilization of laparoscopic techniques in general and gynecological surgery, along with centralized public procurement mechanisms.

Competitive Landscape

The Europe laparoscopy devices market is characterized by the presence of established global and regional medical device manufacturers with strong clinical validation, regulatory compliance, and broad product portfolios. Leading companies are focusing on innovation in energy-based systems, robotic-assisted platforms, and ergonomically advanced instruments, while expanding surgeon training programs and digital integration. Strategic collaborations with hospitals, surgical societies, and academic institutions are strengthening market penetration. Prominent players in the Europe laparoscopy devices market include Boston Scientific Corporation, Karl Storz, ConMed, Aesculap, Covidien, Olympus, Intuitive Surgical, Stryker, Medtronic, B. Braun Melsungen AG, and Ethicon US LLC.

Europe Laparoscopy Devices Market Size

The Europe laparoscopy devices market size was valued at USD 2.26 billion in 2025 and is anticipated to reach USD 2.42 billion in 2026 from USD 4.25 billion by 2034, growing at a CAGR of 7.28%. during the forecast period from 2026 to 2034.

Laparoscopic devices are minimally invasive surgical instruments, including trocars, insufflators, graspers, staplers, and energy-based systems, used to perform abdominal and pelvic procedures through small incisions under video guidance. In Europe, this market is deeply embedded in modern surgical care pathways due to well established clinical protocols public health system reimbursement structures and a strong culture of surgical innovation. The market operates within a stringent regulatory environment shaped by the European Union Medical Devices Regulation which emphasizes real world performance data and post market surveillance. According to sources, minimally invasive surgical procedures have seen a sustained increase and adoption across general surgery, urology, and gynecology in the EU over recent years. As per research, the average hospital length of stay for laparoscopic cholecystectomy is significantly shorter than for open surgery, leading to demonstrated system efficiency gains and the increasing preference for the minimally invasive approach. Furthermore, the European Commission's "Europe's Beating Cancer Plan" provides substantial funding to support comprehensive cancer care, including initiatives that enhance access to advanced and innovative surgical techniques like minimally invasive oncologic surgery. These structural and policy drivers position laparoscopic devices as critical enablers of high quality efficient and patient centered care across the region.

MARKET DRIVERS

Rising Prevalence of Chronic and Lifestyle Related Surgical Conditions

The growing burden of obesity related and age associated diseases is significantly amplifying the growth of the Europe laparoscopic devices market. A major driver is the increasing incidence of gallstone disease and benign abdominal conditions that are optimally managed through minimally invasive approaches. According to research, across the European Union, the prevalence of adult obesity continues to rise, with national rates varying significantly and some countries, like the United Kingdom and Hungary, experiencing particularly high burdens relative to the European average. This trend directly correlates with rising cholecystectomy volumes as gallstone formation is strongly linked to metabolic syndrome. Similarly, the incidence of colorectal cancer in Europe remains high compared to global averages, with a notable trend towards increasing diagnoses among younger adults; concurrently, minimally invasive surgical techniques, such as laparoscopy, are becoming the standard of care for many cases. An additional reinforcing factor is the aging population which increases susceptibility to hernias pelvic organ prolapse and gynecologic pathologies amenable to laparoscopy. National health systems increasingly mandate laparoscopic techniques for recurrent or bilateral hernias due to lower chronic pain rates. This convergence of demographic and epidemiological shifts ensures a steady procedural pipeline that sustains demand for advanced laparoscopic instrumentation.

Accelerated Integration of Minimally Invasive Techniques in National Surgical Pathways

The regional healthcare systems are systematically embedding laparoscopy into standardized care protocols through clinical guidelines and value-based reimbursement models, which further propels the expansion of the Europe laparoscopic devices market. A key stimulant is an updated endorsement for laparoscopic resection as the preferred approach for stage I and II colorectal cancer, provided adequate lymph node clearance is achieved. The adoption of this standard has led to increased utilization of advanced energy devices and articulating staplers in many centers across Europe. Similarly, the European Association of Urology mandates laparoscopic or robotic partial nephrectomy for small renal masses to preserve renal function aligning with broader organ conservation trends. A further institutional driver is the use of procedure based funding mechanisms that reward efficiency and reduced complications. National surgical quality registries in Norway and the Netherlands also publicly report laparoscopic conversion rates incentivizing hospitals to invest in training and technology. This policy driven normalization of minimally invasive surgery creates a stable predictable demand environment for laparoscopic device manufacturers.

MARKET RESTRAINTS

Stringent Regulatory Requirements Under the EU Medical Devices Regulation

The full enforcement of the European Union Medical Devices Regulation has introduced compliance burdens that impede the growth of the Europe laparoscopic devices market. This constrains market entry and product iteration for laparoscopic device manufacturers. Unlike the previous directive the regulation mandates comprehensive clinical evidence for legacy devices reclassification of certain instruments as higher risk and ongoing post market surveillance through unique device identification and EUDAMED database reporting. The European Commission's transition to the Medical Devices Regulation (MDR) has resulted in a substantial volume of legacy devices requiring re-certification, with many facing prolonged review timelines and additional data requests due to stringent new requirements and limited Notified Body capacity. Small and medium enterprises particularly struggle with the cost of generating new clinical investigations for established products like reusable trocars or graspers. Furthermore, the regulation’s emphasis on substance safety has triggered reformulation of polymer and coating materials used in disposable instruments. The European Chemicals Agency (ECHA) has incrementally added plastic chemicals to the list of Substances of Very High Concern (SVHC) under the REACH regulation, reflecting an increasing regulatory focus on limiting hazardous substances in medical devices and other products. These changes can alter device performance characteristics such as torque transmission or tissue grip requiring new validation studies. The administrative and financial overhead diverts R&D resources from innovation to compliance and delays the introduction of next generation features such as integrated sensing or enhanced ergonomics. Regulatory intensity currently serves as a structural restraint on niche innovators, a situation likely to persist until guidance is harmonized.

Persistent Shortage of Trained Laparoscopic Surgeons in Rural and Eastern Regions

Laparoscopic surgery faces uneven adoption owing to a serious deficit of skilled practitioners outside major urban centers, despite widespread clinical endorsement, which in turn obstructs the expansion of the Europe laparoscopic devices market. According to sources, a recognized trend in surgical education and practice is the concern that many general surgeons across various regions of Europe may not perform a sufficient volume of specific advanced laparoscopic procedures annually to maintain high levels of proficiency, highlighting a variability in practice experience. This gap stems from fragmented surgical training curricula and limited access to simulation-based education in lower income member states. As per research, significant variability exists in the structure and implementation of surgical residency programs across the European Union, with the mandatory integration of simulation-based training for laparoscopic skills being inconsistent, leading to potential differences in technical readiness among graduating surgeons. The shortage is exacerbated by an aging surgical workforce. Hospitals in these regions often revert to open surgery not due to clinical necessity but due to lack of trained personnel. This not only affects patient outcomes but also reduces volume stability for device suppliers who cannot justify full portfolio distribution in low utilization zones. The lack of harmonized EU upskilling programs creates a regional gap in access to laparoscopic care, hindering market growth in about a third of Europe, even with new technologies like tele proctoring and mobile training labs being available.

MARKET OPPORTUNITIES

Adoption of Enhanced Recovery After Surgery Protocols Across Public Hospitals

The continent-wide implementation of Enhanced Recovery After Surgery programs aligns procedural choice with system level efficiency goals. This offers a significant opportunity for the Europe laparoscopic devices market. These multimodal pathways prioritize minimally invasive techniques as a cornerstone for reducing opioid use shortening hospital stays and accelerating return to function. The implementation of Enhanced Recovery After Surgery (ERAS) protocols has become a widespread and continuously growing trend in academic and general hospitals across the EU due to their proven benefits in patient recovery and outcomes. National health agencies in Finland and the Netherlands tie hospital performance bonuses to ERAS compliance metrics directly incentivizing investment in laparoscopic instrumentation. A further opportunity lies in the integration of laparoscopy into day case surgery models. As per research, driven by clinical advancements and national initiatives, the trend toward performing common procedures like hernia repairs and cholecystectomies as same-day surgeries is increasing across Denmark and the UK. This shift is associated with substantial healthcare cost containment and improved patient satisfaction when appropriate protocols are followed. Device manufacturers are responding with single use instrument sets optimized for rapid turnover and reduced sterilization burden. Laparoscopic devices are indispensable enablers of sustainable surgical care delivery, allowing health systems to maximize patient throughput under fiscal pressure without compromising safety standards.

Expansion of Robotic Assisted Laparoscopy in Gynecology and Urology

The gradual democratization of robotic platforms beyond elite centers is opening fresh prospects for the Europe laparoscopic devices market. This expansion is creating new demand channels for compatible laparoscopic instruments across the region. Modular, table-mounted systems from companies are gaining popularity in mid-sized hospitals because they offer a less capital-intensive alternative to full robotic systems. According to research, robotic assisted laparoscopic prostatectomy accounted for a portion of all prostate cancer surgeries in Western Europe. These procedures require specialized articulating graspers and energy devices that command premium pricing and recurring consumable revenue. A complementary trend is the use of robotic assistance in complex gynecologic oncology where precision and 3D visualization improve outcomes in radical hysterectomy and lymphadenectomy. National reimbursement codes now explicitly differentiate robotic assisted laparoscopy allowing hospitals to recover added costs. This ecosystem of clinical evidence reimbursement support and skill development is expanding the addressable market for high end laparoscopic devices beyond traditional manual users into the rapidly growing robotic assisted segment.

MARKET CHALLENGES

High Cost of Advanced Disposable Devices in Price Sensitive Healthcare Systems

The rising shift toward single use advanced laparoscopic instruments is a financial challenge for publicly funded regional health systems, which face budget constraints, and negatively impacts the expansion of the Europe laparoscopic devices market. Energy based sealing devices articulating staplers and high-definition trocar systems can increase per procedure costs compared to reusable alternatives. According to the European Health Procurement Observatory national tendering agencies in Spain, Italy, and Portugal rejected a portion of premium disposable device bids due to cost per procedure thresholds despite demonstrated clinical benefits. This forces hospitals to either revert to older reusable platforms or limit advanced device use to complex cases only. The tension is particularly acute in bariatric and oncologic surgery where multiple high-cost instruments are often required in a single case. Manufacturers counter with value dossiers showing reduced complication rates but payers remain skeptical without long term system level savings data. "Cost pressures will persist in hindering widespread adoption and curbing market expansion in budget-constrained areas until innovative pricing strategies, such as outcome-based contracts or the availability of affordable and high-quality alternatives, become standard practice.

Risk of Port Site Metastasis and Complications in Oncologic Procedures

Laparoscopic surgery in oncology carries specific clinical risks, despite its advantages, that temper unrestricted adoption and influence device selection and thereby constrain the expansion of the Europe laparoscopic devices market. A persistent concern is port site metastasis where cancer cells implant at trocar insertion points particularly in aggressive malignancies like gastric or ovarian cancer. According to a 2024 meta analysis published in the European Journal of Surgical Oncology the incidence of port site recurrence in non contained laparoscopic gastrectomies was 2.1 percent compared to 0.7 percent in open surgery prompting many surgeons to use specimen retrieval bags and wound protectors as standard. These auxiliary devices add cost and procedural steps but are increasingly mandated by institutional protocols. A further challenge is the limited tactile feedback in laparoscopy which can compromise complete resection in bulky tumors. Medical guidelines express caution regarding laparoscopic cytoreduction because of the potential for incomplete resection. Laparoscopic methods are generally reserved for early-stage cases, while open surgical approaches are more common for advanced conditions. Newer prototypes featuring integrated imaging and haptic feedback are being developed, though they have not yet reached widespread clinical validation. Legitimate clinical caution will continue to constrain the adoption of laparoscopic approaches in specific oncologic domains until existing safety and efficacy gaps are resolved through technological or technique-based solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.83% |

| Segments Covered | By Product Type, Therapeutic Application, End Users, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Boston Scientific Corporation, Karl Storz, ConMed, Aesculap, Covidien, Olympus, Intuitive Surgical, Stryker, Medtronic, B. Braun Melsungen AG, and Ethicon US LLC. |

SEGMENTAL ANALYSIS

By Product Type Insights

The direct energy systems segment led the Europe laparoscopic devices market and accounted for a 28.5% share in 2025. The dominance of the direct energy systems segment is driven by the critical role these devices play in achieving hemostasis and tissue division during complex minimally invasive procedures across multiple surgical specialties. An additional growth factor is its widespread adoption in colorectal and bariatric surgery where reliable vessel sealing and organ transection are essential for patient safety and procedural efficiency. A further second key driver is the integration of energy systems into enhanced recovery after surgery protocols which prioritize reduced blood loss and shorter operative times. National health technology assessment bodies in Sweden and Denmark now include energy device performance as a criterion in surgical quality benchmarks. Furthermore, the European Union Medical Devices Regulation has accelerated the retirement of legacy electrosurgical units lacking real time impedance feedback compelling hospitals to upgrade to next generation platforms. This combination of clinical necessity regulatory modernization and system efficiency cements direct energy systems as the most utilized and continuously evolving segment in the European laparoscopic ecosystem.

The robotic assisted surgical systems segment is estimated to register the fastest CAGR of 14.3% from 2025 to 2033. The rapid growth of the robotic assisted surgical systems segment is propelled by the increasing accessibility of modular and table mounted robotic platforms that lower the capital barrier for mid-sized hospitals. Moreover, the expansion of robotic indications beyond prostatectomy into gynecologic oncology and complex general surgery is also a major growth enabler of this segment. Robotic-assisted radical hysterectomy is a widely adopted surgical approach for cervical cancer within Western Europe, indicating a significant preference for this minimally invasive method. A different driving factor is the establishment of national robotic surgery training networks funded under the EU4Health program. Some member states of the EU have started offering certified curricula for robotic surgery. Simulation-based credentialing has become mandatory in some member states, including Belgium, the Netherlands, and Finland. These changes indicate a growing trend in standardized training for advanced surgical techniques within Europe.This infrastructure addresses the historical barrier of surgeon adoption. Additionally, reimbursement policies are evolving with France and Italy introducing differentiated diagnosis related group payments for robotic procedures that cover the added device cost. These systemic enablers, clinical validation training standardization and financial recognition, are transforming robotic assistance from a premium novelty into a scalable component of Europe’s minimally invasive surgical future.

By End Users Insights

In 2025, the hospitals segment dominated the Europe laparoscopic devices market and accounted for a substantial share. The supremacy of the hospitals segment is credited to its role as the primary site for complex inpatient surgeries including oncologic resections major hernia repairs and emergency laparotomies converted from laparoscopy. In addition, a different growth driver of this segment is fueled by the concentration of advanced surgical infrastructure in public and academic hospitals, including hybrid operating rooms, high definition imaging towers, and sterile processing departments capable of handling reusable instruments. A further supporting factor is the alignment of hospital procurement with national health technology assessment frameworks that evaluate device cost effectiveness over the full care pathway. Laparoscopic device tenders in public hospitals now routinely require evidence of reduced length of stay and readmission rates. This favors integrated device portfolios from established manufacturers who can supply clinical outcome data across thousands of European cases. Furthermore, the EU Medical Devices Regulation mandates institutional vigilance systems that are most robust in large hospitals with dedicated medical device safety officers. This regulatory maturity makes hospitals the natural anchor for high-risk high value laparoscopic technologies while smaller settings remain limited to basic procedures.

The ambulatory surgical centers segment is anticipated to witness the fastest CAGR of 9.8% during the forecast period owing to national policies promoting same day discharge for low-risk procedures to alleviate hospital congestion and reduce public expenditure, and the expansion of laparoscopic cholecystectomy and inguinal hernia repair into outpatient settings. An additional driver of this segment is the standardization of safety protocols that enable complex laparoscopy in freestanding facilities. National health agencies in Sweden and Ireland license ambulatory centers to perform laparoscopic adrenalectomy and sleeve gastrectomy provided they meet stringent staffing and emergency transfer criteria. Device manufacturers are responding with compact insufflation units single use trocar kits and pre sterilized instrument trays optimized for rapid room turnover. This convergence of policy clinical validation and tailored product design is rapidly expanding the procedural scope and geographic footprint of ambulatory laparoscopic care across Europe.

By Therapeutic Application Insights

The general surgery segment captured the leading share of 32.2% of the Europe laparoscopic devices market in 2025. The prominence of the general surgery segment is because of the breadth of abdominal conditions routinely managed through minimally invasive approaches including cholecystectomy appendectomy and ventral hernia repair. Moreover, the near universal adoption of laparoscopic cholecystectomy as the standard of care for symptomatic gallstones is another major growth enabler of this segment. A further key factor is the integration of laparoscopy into emergency surgical pathways for acute abdominal pain. National surgical quality registries in Germany and France track laparoscopic conversion rates as a performance indicator further institutionalizing the technique. In addition, the rising prevalence of obesity related abdominal wall hernias sustains demand for trocars mesh fixation devices and insufflators. This combination of high-volume routine procedures and expanding emergency indications ensures general surgery remains the bedrock of laparoscopic device utilization across the continent.

The bariatric surgery segment is likely to experience the fastest CAGR of 10.5% from 2026 to 2034 due to the escalating obesity epidemic and its recognition as a chronic disease requiring surgical intervention, and the updated European guidelines on obesity management issued by the European Association for the Study of Obesity which expanded eligibility criteria to include patients with a body mass index of 30 or higher with comorbidities. The prevalence of adult obesity in the European Union has shown a consistent and significant increase over recent decades. This ongoing rise in obesity is a major public health concern, with more than half of the adult population in the EU now classified as either overweight or obese. The trend indicates a growing challenge in managing weight-related health issues across the region. The robust long-term evidence supporting laparoscopic sleeve gastrectomy and gastric bypass in reducing diabetes incidence and cardiovascular mortality also fuels the expansion of this segment. These procedures require high end laparoscopic staplers trocars and energy devices often in multiples per case driving disproportionate device consumption. Health systems are focusing more on the long-term financial benefits of bariatric surgery, which include lower medication and hospitalization costs over a 10-year span. Consequently, this application is expected to experience continued high growth.

REGIONAL ANALYSIS

Germany Laparoscopic Devices Market Analysis

Germany outperformed other countries in the Europe laparoscopic devices market and captured a 22.6% share in 2025. The leading position of the German market is driven by its dense network of high volume surgical centers strong medical technology manufacturing base and early adoption of minimally invasive protocols. The Federal Joint Committee’s positive health technology assessments for advanced energy devices and robotic platforms ensure broad statutory health insurance reimbursement. Furthermore, Germany hosts major R&D hubs for European subsidiaries of global device manufacturers who co develop instruments with local surgeons to meet precision and durability expectations. This ecosystem of clinical excellence regulatory clarity and industrial innovation sustains Germany’s dominant position in the regional market.

United Kingdom Laparoscopic Devices Market Analysis

The United Kingdom followed closely in the laparoscope devices market in Europe and accounted for a 16.1% share in 2025 because of centralized procurement and strong outcome tracking. The implementation of specific surgical recovery protocols has standardized the application of laparoscopic devices across a number of healthcare institutions. Most major abdominal surgeries are now performed using minimally invasive techniques. Performance metrics regarding surgical approaches and outcomes are openly available for public review. The National Institute for Health and Care Excellence regularly updates technology appraisals for laparoscopic staplers and energy systems based on real world evidence from the Hospital Episode Statistics database. Besides, the UK’s early implementation of the EU Medical Devices Regulation through the MHRA has created a rigorous but predictable certification route for innovative devices. These systemic mechanisms ensure consistent high-quality adoption while controlling costs through national framework agreements.

France Laparoscopic Devices Market Analysis

France expanded steadily in the Europe laparoscopic devices market owing to strong growth in robotic and bariatric laparoscopy. The country’s surgical landscape is shaped by national cancer plans and obesity strategies that prioritize minimally invasive approaches. Laparoscopic resection is a procedure considered for a specific stage of colorectal cancer within designated facilities. A government plan involving funding has been put in place to enhance the availability of bariatric surgery services. Furthermore, the country's approach to reimbursement for robotic-assisted procedures has facilitated the adoption of new platforms in a number of hospitals. The presence of leading surgical training academies in Lyon and Paris also ensures a steady pipeline of skilled laparoscopists. This policy driven expansion across oncology and metabolic surgery underpins France’s robust market position.

Italy Laparoscopic Devices Market Analysis

Italy is another key player in the Europe laparoscopic devices market and demonstrated high utilization in general and gynecological laparoscopy. The country performs one of the highest volumes of laparoscopic cholecystectomies in Europe with regional health agencies in Lombardy and Emilia Romagna mandating minimally invasive approaches for all eligible patients. Laparoscopic gallbladder removals are widely performed, indicating a common practice in general surgery. In the field of gynecology, there is an established consensus that supports the use of laparoscopic management for conditions such as endometriosis and fibroids. This approach is considered a primary treatment method in clinical guidelines. Public hospitals benefit from centralized purchasing through Consip which negotiates pan European pricing for trocars insufflators and energy devices. However, adoption of advanced robotics remains concentrated in northern private clinics due to budget fragmentation in southern regions. This mix of high-volume routine surgery and emerging advanced applications defines Italy’s dynamic market character.

Netherlands Laparoscopic Devices Market Analysis

The Netherlands is predicted to grow in the Europe laparoscopic devices market from 2026 to 2034 due to its leadership in day case and enhanced recovery surgery. The country pioneered same day discharge for laparoscopic procedures with a portion of cholecystectomies and inguinal hernia repairs completed in ambulatory settings. National protocols mandate the use of single use trocar kits and pre sterilized instrument sets to ensure rapid room turnover and infection control. Furthermore, Dutch health insurers require proof of procedural volume and outcome data for hospital accreditation driving consistent device utilization and data collection. This focus on efficiency safety and standardization makes the Netherlands a model for scalable high quality laparoscopic care.

COMPETITIVE LANDSCAPE

Competition in the Europe laparoscopic devices market is characterized by a dynamic interplay between global innovators and regional specialists operating within a highly regulated and clinically driven environment. Differentiation hinges not on price alone but on demonstrable clinical value regulatory compliance training support and alignment with national surgical standards. Multinational corporations leverage scale and broad portfolios to bundle solutions across general surgery oncology and bariatrics while European manufacturers compete through localized service rapid delivery and sustainability credentials. The enforcement of the EU Medical Devices Regulation has elevated the barrier to entry favoring established players with robust quality management systems and post market surveillance capabilities. At the same time the rise of robotic assisted platforms is reshaping competitive dynamics with new entrants challenging incumbents through modular cost effective systems. Public procurement processes increasingly demand health technology assessment data linking device use to reduced length of stay and complication rates. This ecosystem rewards companies that integrate deeply into clinical workflows provide continuous education and demonstrate long term system value beyond the operating room

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the European laparoscopy devices market include

- Boston Scientific Corporation

- Karl Storz

- ConMed

- Aesculap

- Covidien

- Olympus

- Intuitive Surgical Stryker Medtronic

- B. Braun Melsungen AG

- Ethicon US LLC

Top Players in the Market

Medtronic plc maintains a leading presence in the Europe laparoscopic devices market through its comprehensive portfolio of energy systems staplers and advanced trocars under the Hugo robotic-assisted surgery platform. The company contributes globally by integrating artificial intelligence and data analytics into surgical workflows to enhance procedural consistency. It also launched a next generation ultrasonic energy device with real time tissue feedback specifically designed to meet the European Society of Surgical Oncology’s guidelines for colorectal resection reinforcing its clinical alignment and regulatory readiness in the region.

Johnson & Johnson through its Ethicon division is a pivotal innovator in laparoscopic stapling and energy-based hemostasis technologies widely adopted across European hospitals. The company’s global influence stems from its long standing partnerships with surgical societies and robust clinical evidence generation. It also collaborated with the European Board of Surgery to co develop a digital credentialing module for laparoscopic suturing integrated into national surgical training curricula. These initiatives deepen its integration into Europe’s educational and clinical governance frameworks.

B. Braun SE headquartered in Germany is a major European player offering a full range of reusable and disposable laparoscopic instruments with a strong emphasis on sustainability and cost efficiency. The company leverages its local manufacturing base to ensure rapid supply chain responsiveness and compliance with EU environmental directives. It also partnered with public hospitals in Southern Europe to implement instrument reprocessing programs aligned with national circular economy targets. This focus on eco conscious innovation and public health system collaboration strengthens its position as a trusted regional partner in minimally invasive surgery.

Top Strategies Used by the Key Market Participants

Key players in the Europe laparoscopic devices market are prioritizing clinical evidence generation through real world data partnerships with national surgical registries and academic institutions to support reimbursement and guideline inclusion. They are investing in surgeon education by establishing certified training academies and digital credentialing platforms aligned with European Board of Surgery standards. Companies are increasingly offering hybrid portfolios that combine reusable high precision instruments with single use advanced disposables to meet diverse hospital procurement strategies. Strategic collaborations with public health agencies on enhanced recovery after surgery and day case surgery protocols embed their devices into standardized care pathways. Additionally firms are developing eco efficient product lines with reduced packaging sterilization burden and circular design to comply with EU sustainability mandates and hospital green procurement policies.

MARKET SEGMENTATION

This research report on the European Laboratory devices market has been segmented and sub-segmented into the following categories

By Product Type

- Internal Closure Devices

- Hand Access Instruments

- Robotic-Assisted Surgical System

- Laparoscopes

- Direct Energy Systems

- Insufflation Devices

By Therapeutic Application

- Colorectal Surgery

- Gynecological Surgery

- General Surgery

- Bariatric Surgery

- Urological Surgery

By End Users

- Hospitals

- Clinics

- Ambulatory Surgical Centers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe Smith & Nephew.

Frequently Asked Questions

What are laparoscopy devices?

Laparoscopy devices are minimally invasive surgical instruments used to perform procedures through small incisions using a camera and specialized tools.

What is driving the growth of the Europe laparoscopy devices market?

Growth is driven by the increasing preference for minimally invasive surgeries, shorter hospital stays, and faster patient recovery.

Which procedures commonly use laparoscopy devices in Europe?

Laparoscopy devices are widely used in general surgery, gynecology, urology, bariatric surgery, and colorectal procedures.

What types of laparoscopy devices are available in the market?

Key devices include laparoscopes, energy devices, trocars, insufflators, suction and irrigation systems, and robotic-assisted systems.

Which countries are leading the Europe laparoscopy devices market?

Germany, France, the UK, Italy, and Spain lead the market due to advanced healthcare infrastructure and high surgical volumes.

How does technological advancement impact the market?

Innovations such as high-definition imaging, 3D visualization, and robotic-assisted laparoscopy are improving surgical precision and outcomes.

What role does robotic surgery play in laparoscopy?

Robotic-assisted laparoscopy enhances dexterity, visualization, and surgeon control, driving adoption in complex procedures.

What challenges does the Europe laparoscopy devices market face?

Challenges include high equipment costs, skilled surgeon requirements, and reimbursement constraints in some regions.

Who are the key players in the Europe laparoscopy devices market?

Major players include Medtronic, Olympus, Stryker, Karl Storz, and Boston Scientific Corporation.

What is the future outlook for the Europe laparoscopy devices market?

The market is expected to grow steadily, driven by innovation, rising surgical volumes, and increasing preference for minimally invasive techniques.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com