Europe Endoscopy Devices Market Research Report By Product, Application & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2026 to 2034)

Market Size, 2025

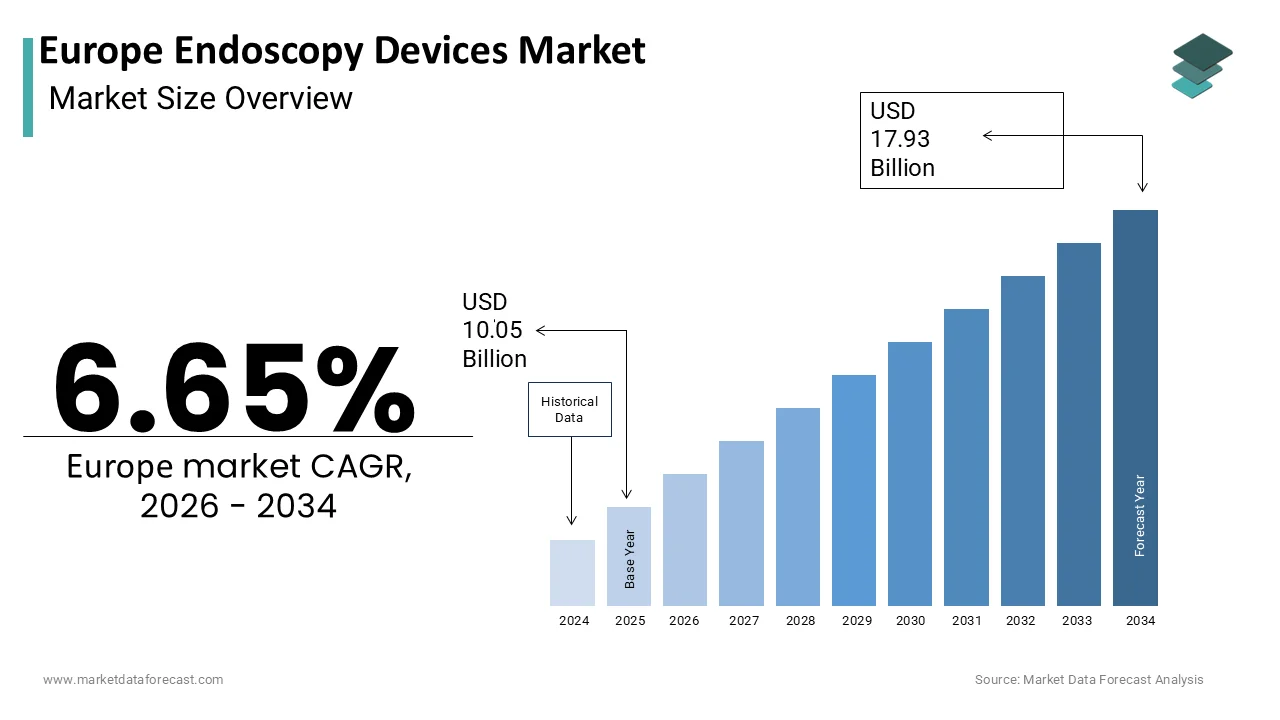

$10.05 BnMarket Estimate, 2026

$10.71 BnMarket Forecast, 2034

$17.93 BnCAGR, 2026–2034

6.65%Europe Endoscopy Devices Market Summary

Market Size & Growth

- The Europe Endoscopy Devices Market was valued at USD 10.05 billion in 2025.

- Expected to reach USD 10.71 billion in 2026 and USD 17.93 billion by 2034, growing at a CAGR of 6.65% from 2026 to 2034.

- Germany led the market with a 22.8% share in 2024.

Key Market Segments

- By Product: Endoscopes, Visualization Systems, Other Endoscopy Equipment, Electrical Endoscopy Equipment

- By Application: GI Endoscopy, Bronchoscopy, Laparoscopy

- By Country: Germany leads with a 22.8% share (2024); the Netherlands is a fast-growing market (2025–2033)

- Endoscopes held the largest product share at 49.7% in 2024; Visualization Systems is the fastest-growing product segment at a 10.4% CAGR (2025–2033)

- GI Endoscopy held the largest application share at 43.8% in 2024; Bronchoscopy is the fastest-growing application at a 9.9% CAGR

Key Drivers

- Expansion of national colorectal and gastric cancer screening programs across EU member states, increasing procedural volume.

- Integration of artificial intelligence and advanced imaging (AI-powered polyp detection, confocal laser endomicroscopy) into endoscopy platforms.

- Rise of single-use endoscopes and expansion of outpatient/ambulatory endoscopy centers across Germany, the Netherlands, Sweden, and France.

Key Players

Ethicon, Stryker Corporation, Karl Storz GmbH, Boston Scientific Inc., Olympus Corporation, Covidien Plc, Smith and Nephew Inc., Fujifilm Holding Corporation.

Europe Endoscopy Devices Market Size

The Europe Endoscopy Devices Market is projected to grow from USD 10.05 billion in 2025 to USD 10.71 billion in 2026 and reach USD 17.93 billion by 2034, registering a CAGR of 6.65% during the forecast period from 2026 to 2034.

Endoscopy devices are minimally invasive diagnostic and therapeutic instruments used to visualize internal organs and perform interventions without open surgery. These include flexible and rigid endoscopes, video imaging systems, insufflators, biopsy forceps, and advanced platforms integrating artificial intelligence and high definition imaging. Europe’s endoscopy ecosystem is distinguished by its early adoption of medical technology, stringent regulatory oversight under the European Union Medical Device Regulation, and a healthcare infrastructure that prioritizes patient safety and procedural efficiency. European healthcare systems are experiencing a steady rise in the volume of minimally invasive diagnostic and therapeutic interventions across multiple medical specialties, supported by comprehensive statistical monitoring of surgical activities by regional authorities. The implementation of organized national cancer control plans across Europe is successfully expanding the reach of colorectal screening programs, leading to higher participation rates in several member states as they align with professional quality guidelines. Additionally, updated European regulatory frameworks are increasingly prioritizing rigorous device sterilization protocols and seamless data exchange between healthcare technologies, which is fundamentally altering how hospitals select equipment and how manufacturers design future medical tools. This confluence of public health policy, clinical demand, and regulatory evolution defines the strategic landscape of the European Endoscopy Devices Market.

MARKET DRIVERS

Expansion of National Cancer Screening Programs Drives Procedural Volume

The systematic rollout of colorectal and gastric cancer screening initiatives across the region drives the growth of the European endoscopy devices market. This has significantly increased the demand for high-quality endoscopy devices. The number of EU member states with established, population-based colorectal cancer screening programs has been steadily increasing, aiming for broader and more equitable coverage across the region. The utilization of colorectal cancer screening tests and related diagnostic procedures, such as colonoscopies following positive primary tests, has generally increased as screening programs have expanded and improved. These programs mandate the use of high-definition endoscopes with narrow-band imaging or chromoendoscopy capabilities to detect early-stage neoplasia. National cancer plans and screening programs are increasingly emphasizing adherence to robust quality and safety standards, which include advancements in diagnostic technology and data collection methods. Similarly, France's organized colorectal screening program maintains a significant participation rate, contributing to a continuous need for appropriate medical equipment in public hospitals to manage screening activities. The sustained procedural volume ensures stable demand for both capital equipment and disposable accessories across diagnostic and interventional endoscopy because the EU has an ambitious, clear goal to significantly increase cancer screening coverage across member states by a target year in the near future.

Integration of Artificial Intelligence and Advanced Imaging Enhances Clinical Utility

The incorporation of artificial intelligence and real-time image analytics into endoscopy platforms is transforming diagnostic accuracy and procedural standardization across the regional healthcare systems, which is among the key factors fuelling the expansion of the European endoscopy devices market. AI-powered polyp detection systems are gaining regulatory approval under the EU Medical Device Regulation and are demonstrating improved detection performance in clinical studies compared to traditional methods. The integration of AI assistance in screening colonoscopies is becoming more common across Europe, although national guidelines and professional society recommendations vary in their enthusiasm due to ongoing debate about overall patient benefit versus potential added burden. Similarly, endomicroscopy and confocal laser endomicroscopy, technologies that provide cellular-level imaging during procedures, are gaining traction in tertiary centers. Real-time imaging technologies, such as probe-based confocal endomicroscopy, are being used in procedures like Barrett's esophagus surveillance to help clinicians make immediate assessments and potentially reduce the number of unnecessary tissue samples taken. The European Commission has dedicated significant funding through programs like the Digital Europe Programme to accelerate the testing, validation, and deployment of AI solutions across various healthcare sectors, including medical imaging and endoscopy. The quickening pace of AI adoption, spurred on by reimbursement bodies like Germany’s G-BA classifying it as a value-added service, is driving manufacturers to integrate intelligent features that improve clinical results and workflow streamlining.

MARKET RESTRAINTS

Stringent Reprocessing and Infection Control Regulations Increase Operational Burden

The European Union’s rigorous reprocessing standards for reusable endoscopes impose significant logistical and financial constraints on healthcare facilities, which act as a key restraint to the European endoscopy devices market. The evolving regulatory landscape, including the Medical Devices Regulation and related quality standards, increasingly emphasizes the need for a highly validated, consistent, and fully traceable reprocessing cycle for all reusable endoscopes to ensure patient safety. Reprocessing protocols for flexible endoscopes involve multiple steps with varying timelines, and guidelines from public health bodies emphasize the importance of following validated, manufacturer-specific instructions for the entire process to ensure effective disinfection. Concerns have been consistently raised across various European regions regarding hospital endoscopy backlogs, which are sometimes linked to the practical challenges and capacity limitations of complex endoscope reprocessing procedures. Regulatory bodies emphasize stringent traceability and documentation in endoscope reprocessing in healthcare facilities, with audit processes ensuring compliance with established hygiene standards to prevent service disruptions. These compliance pressures have accelerated the shift toward single-use endoscopes, yet cost barriers remain high; single-use duodenoscopes cost a significant amount per unit compared to those for reusable equivalents, amortized over numerous uses. The adoption of reusable devices will remain limited by operational inefficiencies and infection control risks until EU-wide standards and automated reprocessing infrastructure are established.

Fragmented Reimbursement Policies Across Member States Limit Technology Access

The absence of harmonized reimbursement codes for advanced endoscopy procedures and devices across the regional countries creates market access barriers and delays in clinical adoption, and thereby inhibits the expansion of theEuropeane endoscopy devices market. While Germany and France provide specific payment codes for AI-assisted colonoscopy and endoscopic submucosal dissection, countries like Poland, Romania, and Greece reimburse only basic endoscopic services under flat diagnosis-related group tariffs. According to sources, only fewEU member states had distinct reimbursement for high definition endoscopy with image enhancement. This fragmentation discourages hospitals in lower-income regions from investing in premium devices. Even when new technologies are clinically validated, the absence of predictable revenue streams impedes procurement. Market growth in nearly half of the EU region is constrained because innovation diffusion is uneven, a situation that will persist until the EU establishes minimum coverage standards for advanced endoscopic care under its Cross-Border Healthcare Directive.

MARKET OPPORTUNITIES

Rise of Single-Use Endoscopes Addresses Infection and Workflow Challenges

Single-use endoscopes are emerging as a major opportunity in the European Endoscopy Devices Market. This is achieved by directly addressing persistent concerns over cross-contamination and reprocessing complexity. Hospitals have faced documented outbreaks of infection, including multidrug-resistant bacteria, linked to inadequately reprocessed reusable endoscopes, prompting a stronger focus on single-use alternatives for certain procedures to enhance patient safety. Companies like Ambu and Boston Scientific now offer CE-marked single-use bronchoscopes, uroscope,s and gastroscopes that eliminate reprocessing entirely. Authorities and professional bodies in various countries, including Denmark, have explored and in some cases implemented the use of single-use bronchoscopes in an effort to eliminate the risk of cross-contamination inherent in reprocessing reusable devices and to streamline clinical workflows. Health services, such as the NHS, have conducted cost analysethatch suggest that switching to single-use devices for certain procedures, such as flexible cystoscopies, can lead to significant financial savings in areas like sterilization labor, water consumption, and maintenance, especially in high-volume settings or where reprocessing infrastructure is a challenge. The European Commission's evolving Green Public Procurement (GPP) criteria, which now consider infection prevention as a valid sustainability metric, are helping to justify the use of single-use devices on grounds other than mere cost-effectiveness. The introduction of many new single-use models, all bearing CE certification, is significantly elevating infection safety benchmarks within European endoscopy suites.

Expansion of Outpatient and Ambulatory Endoscopy Centers Creates New Deployment Models

The shift from inpatient to outpatient endoscopy in the region is opening new avenues for compact, portable, cost-efficient device adoption, which is expected to propel the expansion of the European endoscopy devices market. The long-standing and ongoing trend in Germany, the Netherlands, and Sweden involves a continuous movement of diagnostic endoscopies and various other surgical procedures from inpatient hospital settings to outpatient ambulatory surgery centers or specialized clinics. This shift aims to improve efficiency and reduce costs. These settings prioritize ease of use, rapid turnover,r and minimal footprint—characteristics met by next-generation portable endoscopy towers and battery-powered scopes. The French healthcare system, guided by organizations like the French National Authority for Health (HAS), has been actively promoting and expanding the capacity for day surgery and ambulatory endoscopy units, indicating a consistent increase in such facilities and procedures over time. This trend favors modular platforms like Fujifilm’s LASEREO Smart and Olympus’s EVIS X1 Core, which offer high performance in reduced form factors. Additionally, teleendoscopy, where images are streamed to remote specialists, is gaining traction in rural Spain and Finland, supported by 5G health corridors funded under the EU’s Digital Europe Programme. The push to reduce hospital congestion and improve access means the ambulatory care model is increasing demand for flexible, connected, and operator-friendly endoscopy devices designed for decentralized care.

MARKET CHALLENGES

High Cost of Advanced Endoscopy Systems Constrains Adoption in Public Hospitals

The premium pricing of next-generation endoscopy platforms is a significant barrier to widespread adoption, particularly in publicly funded healthcare systems facing budget austerity, which degrades the growth of the European endoscopy devices market. High-definition endoscopy systems featuring advanced technologies like AI integration, narrow-band imaging, and 4K resolution represent a significant capital investment for healthcare facilities. The adoption of these modern systems is a growing trend driven by the potential for improved diagnostic accuracy and efficiency, but their cost remains a notable factor in procurement decisions. Reports and data from health organizations indicate that a substantial number of public hospitals in Southern and Eastern Europe faced constraints on their capital equipment budgets in the recent past, particularly during the period between 2020 and 2023. This trend reflects the financial pressures on healthcare systems in the region and the phasing out of some temporary COVID-19-related funding. In Italy, the portion of a public hospital's annual budget dedicated specifically to acquiring new medical technology appears to be a very small part of the overall expenditure. This low investment in new equipment, compared to other spending categories, highlights ongoing challenges and variations in health expenditure priorities within the country's public health system. Documentation and reports from the Portuguese Ministry of Health and related organizations have emphasized a significant issue with the age of certain medical equipment, such as gastroscopes. A large amount of this equipment in use has been noted to be older than its professionally recommended service life, indicating a need for substantial modernization of the inventory. Emerging leasing and pay-per-procedure models face slow adoption due to regulatory obstacles tied to device ownership and data governance. Many European institutions will operate suboptimal systems, compromising diagnostic quality and procedural efficiency, until financing mechanisms align with the pace of technological advancement.

Shortage of Trained Endoscopists Limits Procedural Capacity Despite Device Availability

The growing demand for endoscopic services in the region is outpacing the supply of qualified endoscopists, which creates a human resource barrier that undermines device utilization and thereby negatively impacts the European endoscopy devices market expansion. There are indications of significant workforce challenges in the field of gastroenterology and endoscopy across various European regions, potentially leading to service backlogs and strains on existing staff. Also, the European Society of Gastrointestinal Endoscopy provides specific guidance on the minimum number of supervised procedures required before an endoscopist's competency can be formally assessed. In addition, the number of available training positions in Spain's endoscopy programs may not align perfectly with the anticipated demand for new specialists, potentially indicating a future gap in the workforce. This gap forces existing specialists to work extended hours. Endoscopists in the UK often manage high workloads, with many professionals potentially performing more procedures per session than recommended by official guidelines, leading to concerns about quality and working conditions. Hospitals may acquire state-of-the-art devices, but without skilled operators, throughput and diagnostic yield suffer. The European Commission’s Health Workforce Observatory warns that without coordinated EU-level training expansion and cross-border recognition of credentials, the endoscopy capacity gap will widen, rendering even the most advanced devices underutilized in high-need regions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Ethicon, Stryker Corporation, Karl Storz GmbH, Boston Scientific Inc., Olympus Corporation, Covidien Plc, Smith and Nephew Inc., and Fujifilm Holding Corporation. |

SEGMENTAL ANALYSIS

By Product Insights

In 2024, the endoscopes segment led the European Endoscopy Devices Market by capturing a 49.7% share. The leading position of the endoscopes segment is attributed to the irreplaceable role of endoscopes as the primary physical interface between clinician and patient anatomy across nearly all minimally invasive specialties. Every gastrointestinal, bronchoscopic, or urological procedure requires a dedicated scope, and with millions of endoscopic interventions performed annually in the EU, the baseline demand remains immense. Technological obsolescence further amplifies replacement cycles. High definition imaging,g narrow band illumination, and articulating tip mechanisms have rendered pre 2018 models clinically inadequate in many settings. Medical societies have adjusted screening guidelines, necessitating the use of colonoscopes equipped with advanced imaging technologies to meet new standards for image clarity and diagnostic capabilities. Evolving regulations require medical device manufacturers to generate and maintain ongoing clinical performance evidence for every device model they offer on the market, prompting healthcare institutions to gradually discontinue the use of equipment models that lack the necessary updated performance documentation. This combination of procedural necessity,ity regulatory compliance, ance and rapid innovation ensures endoscopes remain the central and highest value component of the endoscopy ecosystem.

The visualization systems segment is likely to experience the fastest CAGR of 10.4% from 2025 to 2033 due toindustry-wide wide shift from analog and HD to 4K and 3D integrated platforms that serve as command centers for procedural intelligence. Modern visualization towers no longer merely display images—they integrate artificial intelligence for lesion detection, document procedural quality metrics, and link to hospital information systems for seamless reporting. There has been a consistent pattern of medical facilities modernizing their imaging infrastructure in response to evolving quality guidelines within the field. A clear focus is emerging on enhancing the connectivity and interoperability of medical imaging systems through dedicated funding and support programs across the region. Furthermore, modular designs from companies like Stryker and Richard Wolf allow hospitals to incrementally add fluorescence imaging or AI modules without replacing entire towers, lowering entry barriers. The shift in endoscopy towards data-powered insights positions visualization systems as key hubs in procedural suites, driving significant investment across healthcare.

By Application Insights

The gastrointestinal endoscopy segment was the prominent segment in theEuropeane endoscopy devices market by accounting for a 43.8% share in 2024. The prominence of the gastrointestinal endoscopy segment is credited to Europe’s comprehensive cancer prevention infrastructure, rising incidence of chronic digestive disease,s and the dual diagnostic therapeutic utility of GI scopes. Across numerous European nations, there is a distinct pattern of extensive implementation of colorectal cancer screening initiatives, making millions eligible for and accessible to these organized programs. Beyond cancer detection, a substantial portion of the European populace lives with chronic inflammatory bowel diseases necessitating consistent endoscopic observation, and endoscopic procedures are increasingly employed for advanced therapeutic interventions like non-surgical treatment of certain early-stage cancers. This indicates a considerable and rising application of diverse endoscopic techniques within the European healthcare environment for screening, monitoring, and therapeutic purposes. The combination of population-scale public health mandates and clinical versatility ensures GI endoscopy remains the procedural and economic backbone of the European endoscopy landscape.

The bronchoscopy segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 9.9% during the forecast period, owing to the convergence of lung cancer screening, expansion of respiratory disease burden, and the advent of navigation-guided interventional techniques. Several European nations are implementing low-dose CT screening programs for lung cancer. Most lesions detected through these screening programs require confirmation via bronchoscopic biopsy, often utilizing advanced diagnostic tools such as radial endobronchial ultrasound or electromagnetic navigation systems. There is also an expanding prevalence of chronic respiratory ailments, with bronchoscopy frequently used for airway evaluation and sometimes for the placement of endobronchial valves to manage emphysema. New technological platforms have been approved, suggesting continued expansion in the use and capabilities of navigational bronchoscopy for accessing peripheral lung nodules. Bronchoscopy is moving into the clinical mainstream, driven by increased policy focus on respiratory health and advances in minimally invasive diagnostics.

COUNTRY LEVEL ANALYSIS

Germany Endoscopy Devices Market Analysis

Germany dominated the European Endoscopy Devices Market by capturing a 22.8% share in 2024. The dominance of the German market is driven by a rigorous regulatory framework, high procedural volume,e and universal access to advanced endoscopic care. Germany performs a substantial number of endoscopic procedures annually, with colonoscopy alone exceeding significant numbers. The Federal Joint Committee enforces strict quality indicators requiring high-definition imaging,g procedural documentation, and minimum adenoma detection rates for all screening centers. These mandates drive continuous device refresh cycles and create a premium market for AI-enabled platforms. Germany also maintains one of Europe’s densest networks of ambulatory endoscopy centers with numerous accredited facilities enabling high throughput and rapid technology adoption. The presence of global R and D hubs, including Karl Storz and B Braun, ensures close clinical collaboration and rapid iteration. This ecosystem of regulation scale and innovation cements Germany’s role as Europe’s endoscopy benchmark.

France Endoscopy Devices Market Analysis

France followed closely in the European endoscopy devices market by accounting for a 17.5% share in 2024. The expansion of the French market is fuelled by its centrally organized cancer screening programs, standardized training pathways, and equitable access model. France’s colorectal cancer screening initiative achieved a notable participation rate,e serving a large volume of citizens with colonoscopy follow-up. The National Cancer Institute mandates that all screening endoscopy units use scopes with image enhancement and electronic reporting capabilities, ensuring nationwide technology alignment. France also leads in therapeutic endoscopy witha considerable number of endoscopic resections performed annually for early gastrointestinal cancers. Additionally, France’s national health data platform Health Data Hub enables real-time quality monitoring of endoscopic outcomes across public and private providers. This integration of public health strategy, workforce development, and digital oversight makes France a uniquely coordinated and scalable endoscopy market.

United Kingdom Endoscopy Devices Market Analysis

The United Kingdom holds a noteworthy position in theEuropeane Endoscopy Devices Market due to a strong focus on outpatient care, digital health integration, and early adoption of single-use and AI technologies. The National Health Service performs a notable number of endoscopic procedures yearly, witha considerable number conducted in dedicated endoscopy units rather than acute hospitals. This ambulatory model favors compact, portable,e anhigh-efficiencycy systems that maximize daily throughput. The UK also leads Europe in single-use bronchoscopy adoption, with a significant share of procedures now using disposable scopes following National Institute for Health and Care Excellence guidance on infection prevention. Furthermore, the National Endoscopy Quality Assurance Programme publishes annual performance dashboards that drive device upgrades based on clinical outcomes. This culture of innovation, transparency,ncy and decentralized delivery positions the UK aforward-lookingking and responsive market.

Italy Endoscopy Devices Market Analysis

Italy is moving ahead steadfastly in the European Endoscopy Devices Market owing to Europe’s most aged population and high burden of gastrointestinal cancers. Italy faces heightened demand for colorectal and gastric cancer screening due to a large elderly population. Efforts to expand preventive care have increased access to diagnostic procedures, resulting in a high volume of completed screenings annually. Regional disparities in healthcare quality and accessibility persist, with some areas meeting benchmarks while others face resource limitations, including a scarcity of specialized professionals and outdated equipment. A targeted financial investment is aimed at modernizing diagnostic equipment in underserved areas. Additionally, a high prevalence of a common bacterial infection in the adult population contributes to high volumes of related upper gastrointestinal diagnostic procedures. Despite fiscal constraints, Italy’s demographic imperative ensures sustained demand, making it a high-volume market with significant modernization potential.

Netherlands Endoscopy Devices Market Analysis

The Netherlands is anticipated to expand in theEuropeane Endoscopy Devices Market from 2025 to 2033. The country stands out for its national quality registry, real-time performance feedback, and outcome-based reimbursement model. All Dutch endoscopy centers report procedural data to the National Endoscopy Registry, which publishes annual benchmarks on adenoma detection,n cecal intubation success, and complication rates. This transparency drives continuous improvement and justifies investment in premium devices. Integration of automated diagnostic tools has transitioned from an elective enhancement to a standard component of gastrointestinal screening protocols within certain regions. The adoption of computer-aided detection systems is intended to improve the identification of anomalies during routine medical examinations. Healthcare systems are increasingly pivoting toward disposable instrumentation for specialized pulmonary procedures to mitigate risks associated with equipment contamination. There is a shift in clinical practice toward prioritizing single-use medical devices in public health settings to enhance patient safety standards. The transition to advanced screening technologies reflects a broader pattern of incorporating real-time analytical assistance into diagnostic workflows. Dutch health insurers reimburse endoscopy based on quality metrics rather than procedure count, thereby incentivizing technology that improves outcomes. This ecosystem of measurement accountability and value-based payment makes the Netherlands Europe’s most analytically rigorous and quality-focused endoscopy market.

COMPETITIVE LANDSCAPE

Competition in the European Endoscopy Devices Market is characterized by a mix of established Japanese and European manufacturers and emerging innovators specializing in single-use and AI-enabled solutions. Leading companies differentiate through optical quality imaging resolution and ecosystem integration rather than price alone. The European Union Medical Device Regulation has raised the technical and clinical evidence bar, favoring firms with robust regulatory capabilities and post market surveillance systems. National quality initiatives and cancer screening programs drive demand for high-performance devices, but fragmented reimbursement policies across member states create uneven adoption. Innovation is increasingly centered on workflow efficiency, infection prevention, and data interoperability as hospitals seek to improve outcomes and reduce costs. While incumbents dominate capital equipment, new entrants are gaining ground in disposable scopes and software analytics. The market rewards those who align technological advancement with Europe’s emphasis on quality, transparency, and patient safety.

KEY MARKET PLAYERS

A few prominent europe endoscopy devices market companies profiled in this report are

- Ethicon

- Stryker Corporation

- Karl Storz GmbH

- Boston Scientific Inc.

- Olympus Corporation

- Covidien Plc

- Smith and Nephew Inc.

- Fujifilm Holding Corporation

TOP LEADING PLAYERS IN THE MARKET

- Olympus Corporation is a global leader in endoscopy with deep integration across the European Endoscopy Devices Market through its advanced gastrointestinal and surgical visualization platforms. The company supplies high-definition endoscopes, AI-enabled imaging towers, and therapeutic accessories to hospitals in numerous European countries. It also established a clinical training academy in Hamburg to support endoscopist education on advanced resection techniques. These initiatives reinforce Olympus’s commitment to clinical excellence, digital innovation, and workforce development across Europe while maintaining its influence in global endoscopy standards.

- Karl Storz SE & Co KG is a German-based pioneer in rigid and flexible endoscopy with a strong footprint in urology, ENT, and laparoscopy across Europe. The company leverages its engineering heritage to deliverhigh-precisionn optical systems and integrated OR solutions compliant with the EU Medical Device Regulation. It also partnered with university hospitals in France and Sweden to validate AI algorithms for image enhancement in bronchoscopy. By combining optical excellence with digital interoperability and clinical collaboration, Karl Storz continues to shape procedural standards in European operating rooms and endoscopy suites.

- Fujifilm Corporation has emerged as a significant player in the European Endoscopy Devices Market through its ELUXEO platform, which combines 4K imaging with dual focus and laser light enhancement for superior mucosal visualization. The company focuses on gastroenterology and bronchoscopy, offering both reusable and single-use scopes tailored to European infection control protocols. It also opened a dedicated endoscopy service center in the Netherlands to reduce device downtime and improve clinical support. These actions reflect Fujifilm’s strategy of integrating diagnostic imaging expertise with artificial intelligence to address quality and safety priorities in European healthcare settings.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Endoscopy Devices Market prioritize integration of artificial intelligence and high definition imaging to enhance diagnostic accuracy and procedural standardization. They invest in clinical education and training academies to build user proficiency and drive adoption of advanced platforms. Companies actively pursue CE Mark certification under the EU Medical Device Regulation to ensure regulatory compliance and market access. Strategic collaborations with academic hospitals enable real-world validation of new technologies such as AI algorithms and fluorescence imaging. Additionally, firms expand service and support infrastructure across Europe to minimize device downtime and strengthen customer relationships in a highly competitive environment.

EUROPE ENDOSCOPY DEVICES MARKET NEWS

- In March 2023, Olympus Corporation launched the EVIS X1 endoscopy system with integrated AI polyp detection, receivingthe CE Mark and strengthening its Europe Endoscopy Devices Market presence.

- In May 2024, Karl Storz SE & Co KG expanded its IMAGE1 S 4K platform to include fluorescence imaging modules for minimally invasive surgery, thereby strengthening its European Endoscopy Devices Market presence.

- In September 202,3 Fujifilm Corporation received CE Mark for itAI-powereded colonoscopy support system, enabling real-time polyp characterization, strengthening its European Endoscopy Devices Market presence.e

- In November 202,3 Olympus Corporation established a clinical training academy in Hamburg to advance endoscopist education on endoscopic submucosal dissection, strengthening Europeanrope Endoscopy Devices Market presence.

- In February 2024, Fujifilm Corporation opened a dedicated endoscopy service center in the Netherlands to enhance device support and reduce clinical downtime, strengthening its Europe Endoscopy Devices Market presence

MARKET SEGMENTATION

This research report on the europe endoscopy devices market has been segmented and sub-segmented into the following categories.

By Product

- Endoscopes

- Flexible Endoscopes

- Rigid Endoscopes

- Capsule Endoscopes

- Visualization Systems

- Other Endoscopy Equipment

- Electrical Endoscopy Equipment

By Application

- Laparoscopy

- Bronchoscopy

- GI Endoscopy

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which countries lead the Europe Endoscopy Devices Market?

Germany leads the Europe Endoscopy Devices Market, followed by the UK and France, due to advanced healthcare infrastructure and high procedure volumes. Germany benefits from a large geriatric population (22.8% over 62) driving orthopedic and GI endoscopies, while the UK sees growth from minimally invasive surgeries and tech advancements. These nations account for the majority of Europe's 7.4 million annual procedures.

2. What drives growth in the Europe Endoscopy Devices Market?

Key drivers for the Europe Endoscopy Devices Market include rising chronic diseases like GI cancers, an aging population, and demand for minimally invasive surgeries offering quicker recovery and fewer infections. Technological innovations such as AI-integrated lesion detection, ultra-high-definition visualization, and robotic platforms further propel expansion, alongside favorable FDA/CE approvals and reimbursements.

3. What are the main challenges in the Europe Endoscopy Devices Market?

Challenges in the Europe Endoscopy Devices Market encompass high costs of advanced devices, shortage of trained endoscopists, and risks like infections or perforations from procedures. Intense competition and availability of alternatives also hinder growth, though innovations in disposable endoscopes mitigate some reprocessing issues prevalent in hospitals and ambulatory centers.

4. Who are the top companies in the Europe Endoscopy Devices Market?

Leading players in the Europe Endoscopy Devices Market include Olympus, Pentax Medical, and Medtronic, focusing on innovations like video processors and fluorescence imaging. Recent moves, such as Olympus acquiring Quest Photonic for EUR 50 million, enhance minimally invasive capabilities, while Cosmo Pharmaceuticals' GI Genius AI system gains FDA approval for lesion detection.

5. How does technology impact the Europe Endoscopy Devices Market?

Technological advancements like AI for real-time analysis, robotic-assisted platforms, and high-definition imaging transform the Europe Endoscopy Devices Market. Single-use scopes and capsule endoscopes improve precision and patient comfort, with segments like robot-assisted showing rapid growth amid Europe's focus on precision medicine and ambulatory procedures.

6. What is the market segmentation in Europe Endoscopy Devices Market?

The Europe Endoscopy Devices Market segments by product (endoscopes, visualization systems, accessories), application (gastroenterology, urology, pulmonology), and end-user (hospitals, ambulatory centers). Endoscopes hold the largest share, with GI applications leading due to high procedure volumes in leading nations like Germany.

7. Why is Germany dominant in the Europe Endoscopy Devices Market?

Germany dominates the Europe Endoscopy Devices Market with over 420 hospitals performing 3.2 million procedures annually, fueled by advanced infrastructure, high-definition systems, and investments. Its geriatric population and demand for flexible/disposable scopes in minimally invasive GI and orthopedic surgeries solidify its leadership position

8. What future trends shape the Europe Endoscopy Devices Market?

Future trends in the Europe Endoscopy Devices Market include AI integration for automated detection, robotic systems for precision, and growth in single-use devices for infection control. Sustainability, ambulatory shifts, and expansions in capsule endoscopy will drive the market towards USD 16+ billion by 2033 amid aging demographics.

9. How does the aging population affect the Europe Endoscopy Devices Market?

Europe's aging population significantly boosts the Europe Endoscopy Devices Market, with high chronic illness rates necessitating frequent screenings and interventions. Countries like Germany (22.8% over 62) see increased demand for GI and orthopedic endoscopies, aligning with preferences for minimally invasive options reducing hospital stays.

10. How do regulations influence the Europe Endoscopy Devices Market?

Stringent EU regulations like CE marking ensure safety and quality in the Europe Endoscopy Devices Market, promoting innovations while challenging compliance. Favorable reimbursements in mature systems like Germany's accelerate adoption of AI and robotic tech, balancing growth with patient safety standards.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com