Europe Microwave Oven Market Size, Share, Trends & Growth Forecast Report By Type, Distribution Channel, Application, and By Country (Germany, United Kingdom, France, Italy, Spain, Netherlands, Sweden & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Microwave Oven Market Summary

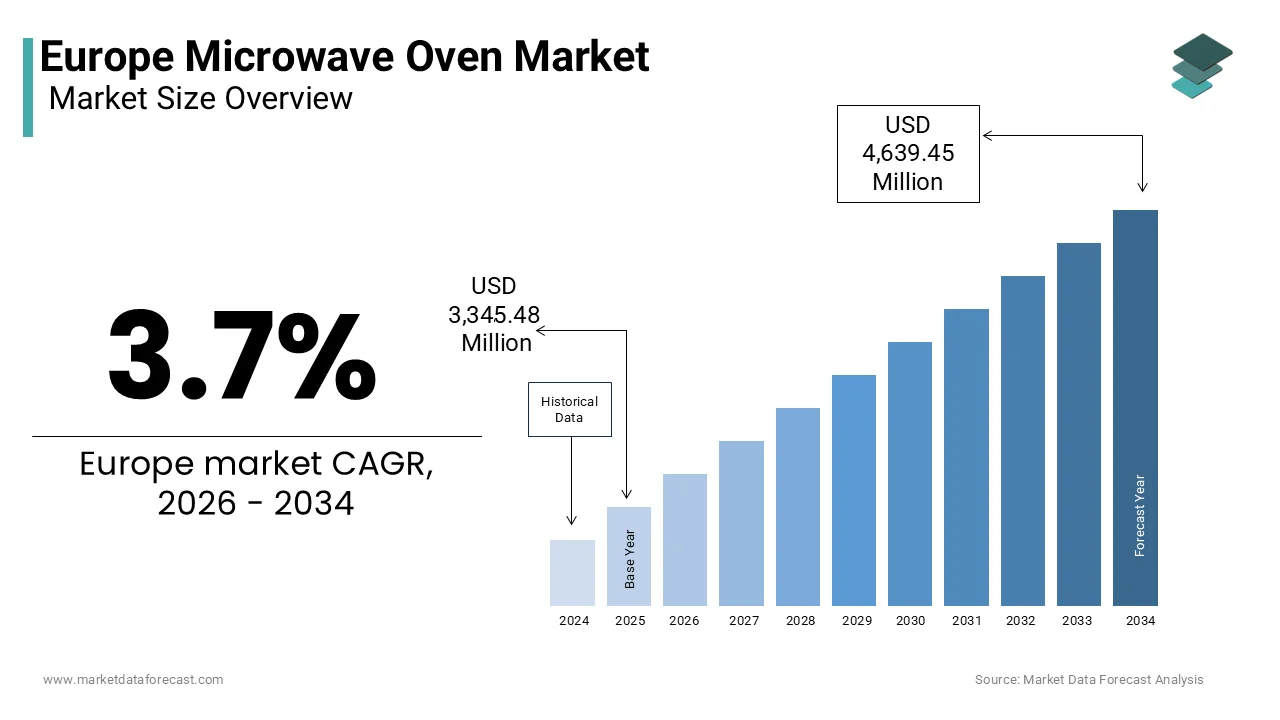

The Europe microwave oven market, valued at USD 3.35 billion in 2025, is projected to reach USD 4.64 billion by 2034, expanding at a CAGR of 3.7% driven by urbanization, compact living trends, energy efficiency regulations, and rising demand for smart and multifunctional kitchen appliances.

Market Snapshot

- 2025 Market Size: USD 3,345.48 million

- 2026 Estimate: USD 3,469.26 million

- 2034 Forecast: USD 4,639.45 million

- CAGR (2026–2034): 3.7%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Rising urbanization and growth of compact apartments across European cities

- High penetration of dual-income and single-person households

- EU Ecodesign and Energy Label regulations improving efficiency standards

- Increasing adoption of smart, connected kitchen appliances

- Strong demand from residential replacement cycles and commercial foodservice

Principal Restraints

- Consumer perception of microwaves as reheating-only appliances in Southern Europe

- Market saturation in Western and Northern European households

- Rising compliance costs due to strict energy efficiency and e-waste regulations

- Margin pressure from frequent product redesigns to meet EU standards

High-Value Opportunities

- Expansion of inverter technology for precision cooking and energy savings

- Growth of ready-to-eat and frozen meal consumption

- Rising demand for built-in and integrated kitchen solutions

- Smart microwave integration with connected home ecosystems

Key Market Challenges

- Competition from multifunctional built-in ovens with microwave features

- Volatility in raw material prices and logistics disruptions

- Supply chain dependency on Asian manufacturing hubs

- Balancing cost, sustainability, and technological innovation

Fastest-Growing Segments

- Convection Microwave Ovens: ~9.6% CAGR — multifunctionality and energy efficiency

- Online Distribution Channel: ~12.3% CAGR — digital adoption and price transparency

- Commercial Applications: ~10.1% CAGR — cloud kitchens, hospitality, and institutional catering

Regional Leadership & Dynamics

- Germany (18.7%) — energy efficiency leadership and strong appliance replacement cycle

- United Kingdom (16.2%) — high ready-meal consumption and urban living density

- France — integration into rental housing and energy renovation programs

- Italy — accelerating urbanization and shifting cooking habits

- Spain — tourism-driven commercial demand and compact housing growth

What Wins Commercially

- Compliance with EU Ecodesign and Energy Label regulations

- Compact, space-efficient designs for urban households

- Inverter-based energy-efficient cooking technology

- Smart connectivity and app-enabled functionality

- Integration with modular and built-in kitchen ecosystems

Top Strategic Ask for Executives

Prioritize energy-efficient, multifunctional, and digitally integrated microwave platforms while strengthening supply chain resilience and partnerships with kitchen system integrators to sustain growth in Europe’s mature appliance market.

Leading Players

Some of the companies that are playing a dominating role in the Europe microwave oven market include:

- Samsung Electronics

- LG Electronics

- Panasonic Corporation

- Whirlpool Corporation

- Beko (Arçelik A.Ş.)

- Electrolux AB

- Sharp Corporation

- Toshiba Corporation

- Haier Group

- Miele & Cie. KG

- Bosch (BSH Hausgeräte GmbH)

- Siemens (BSH Hausgeräte GmbH)

Europe Microwave Oven Market Size

The Europe microwave oven market was valued at USD 3,345.48 million in 2025, is estimated to reach USD 3,469.26 million in 2026, and is projected to reach USD 4,639.45 million by 2034, growing at a CAGR of 3.7% from 2026 to 2034

A microwave oven is a common electric kitchen appliance that heats and cooks food rapidly using electromagnetic radiation in the microwave frequency range. These appliances serve as essential kitchen tools valued for speed, convenience, and evolving multifunctionality beyond basic reheating. While market saturation exists in Western Europe, demand is increasingly shaped by urbanization, energy efficiency mandates,s and the redefinition of domestic cooking behaviors. Microwave oven ownership is widespread across European households, with particularly high adoption rates in many Western and Northern Europ,,ean nations. However, market penetration is not uniform, with lower, though still significant, adoption levels observed in certain Southern and Eastern European countries compared to the European average. The European Commission’s Ecodesign Directive has significantly influenced product development, mandating reduced standby power consumption and improved energy labeling since 2021. Concurrently shifting meal patterns driven by dual-income households and single-person dwellings sustain functional relevance for rapid cooking appliances. Unlike emerging markets, Europe’s microwave evolution is less about volume growth and more about technological refinement,nt sustainability integration, and alignment with contemporary culinary ecosystems.

MARKET DRIVERS

Rising Urbanization and Compact Living Spaces Drive Space-Efficient Appliance Adoption

Urban density across the region has intensified demand for kitchen appliances that deliver functionality without occupying a significant footprint, particularly in major metropolitan areas, and thereby drives the growth of theEuropeane microwave oven market. A significant portion of the European Union population resides in urban or semi-urban areas, leading to a continued, high demand for smaller, dense housing units in major capital cities like Paris, Berlin, and Amsterdam. This spatial constraint favors compact and multifunctional kitchen solutions where microwave ovens, especially combination models with convection grilling or steam functions, replace bulkier conventional ovens. Due to a high number of single-person households and a strained housing market, new residential construction in Sweden is heavily focused on small-format apartments, such as studios and one-bedroom units. Similarly, urban rental trends in the Netherlands are driving demand for compact, integrated kitchen solutions like under-counter microwaves to maximize limited space. Developers and kitchen designers now routinely integrate microwave cavities into modular cabinetry, reducing external appliance clutter. This urban spatial economy,y coupled with the normalization of small household units, ensures that microwave ovens remain indispensable not merely as reheating tools but as primary cooking appliances in space-optimized European homes.

Integration of Smart Connectivity Features Aligns with Digital Kitchen Ecosystems

European consumers increasingly expect household appliances to integrate seamlessly into connected home environments, which enables remote control, voice activation, and energy monitoring, and contributes to the expansion of the European microwave oven market. This behavioral shift has propelled manufacturers to embed Wi-Fi, Bluetooth, and voice assistant compatibility into microwave ovens, transforming them from standalone devices into nodes within broader smart kitchen networks. In major European markets, a significant proportion of new kitchen appliances are now purchased with smart-enabled features, as consumers prioritize connectivity, energy efficiency, and remote control capabilities. Brands like Miele and Bosch now offer microwave models that synchronize with cooking apps,s suggest optimized heating programs based on food type, and send maintenance alerts via smartphone. Among younger households in Italy, the adoption of connected, built-in kitchen appliances like microwaves is rising rapidly, driven by a preference for convenient, digitally integrated, and aesthetically appealing kitchen technology. Furthermore, the European Union’s Cybersecurity Certification Framework for consumer IoT devices, introduced in 2022, has instilled consumer confidence by ensuring data privacy and secure firmware updates. This regulatory reassurance, combined with rising digital literacy, accelerates the transition toward intelligent microwave solutions that offer precision automation and interoperability within evolving European domestic technology landscapes.

MARKET RESTRAINTS

Persistent Consumer Perception of Limited Culinary Capability Restrains Premium Uptake

A significant portion of European consumers continues to view microwave ovens as tools for reheating or defrosting rather than serious cooking appliances, despite technological advancements, which limits willingness to invest in higher-end multifunctional models, and the growth of the European microwave oven market. A minority of European consumers view microwave ovens as appropriate for preparing full, complete meals, with this sentiment being notably less prevalent in Southern European countries like Italy and Spain, where traditional cooking methods are preferred. This perception stems from cultural culinary traditions that prioritize conventional methods such as stovetop roasting and baking, which are deeply embedded in national food identities. Consequently, manufacturers struggle to justify premium pricing for convection or steam combination microwaves in markets where perceived utility remains narrowly defined. Microwave ownership in France has reached a point of high saturation, resulting in a plateau in new purchasesine recent years, while the lifecycle of existing appliances is extending. This attitudinal inertia suppresses innovation adoption and confines demand primarily to entry-level models, thereby constraining market value expansion even as functionality advances.

Stringent Energy Efficiency and E-Waste Regulations Increase Compliance Costs

The European Union’s aggressive sustainability agenda imposes rigorous design and disposal requirements that elevate production complexity and cost for microwave oven manufacturers. Consequently, this hinders the expansion of the European microwave oven market. The updated European Union Ecodesign requirements now mandate significantly lower standby power consumption for electronic products and require energy labels to use a revamped, stricter A to G scale, eliminating the previously inflated efficiency ratings. Following the implementation of new, more demanding energy standards, a large majority of microwave models in the European market were moved to lower, less-efficient classifications, which necessitated product redesigns and devalued existing inventory. Additionally, European Union legislation obliges manufacturers to take financial responsibility for the entire lifecycle of their electronic products, including funding the collection, recycling, and safe disposal, with high minimum, weight-based recycling targets established for the industry. In Germany, the Electrical and Electronic Equipment Act mandates that manufacturers and importers must register every specific product model with the national EAR Foundation and regularly report sales data, creating a significant administrative and financial compliance workload, particularly for smaller companies. According to the German Electrical and Electronic Manufacturers Association, compliance with environmental regulations and reporting requirements has created an upward trend in expenses for small appliance producers, with costs rising significantly in the early 2020s. These regulatory layers, while environmentally necessary,y compress margins and complicate time to market,, et especially for innovative features that require new material certifications or thermal management systems.

MARKET OPPORTUNITIES

Expansion of Inverter Technology Enhances Cooking Precision and Energy Performance

Inverter technology gives a pivotal opportunity in Europeanrope microwave oven market by replacing traditional on-off magnetrons with continuous power delivery. This technology enables precise temperature control. Unlike conventional models that cycle full power, leading to uneven heating, inverter microwaves maintain consistent low power levels ideal for delicate tasks such as melting chocolate or simmering sauces. Consumer adoption is accelerating, particularly in Northern Europe,e where energy consciousness is high.gh Sweden reported a year-on-year increase in inverter microwave sales in 2023. Leading manufacturers, including Panasonic and Samsung, have expanded their European inverter portfolios with compact and built-in variants to cater to urban kitchens. Furthermore, the technology aligns with the EU Energy Label’s emphasis on real-world efficiency metrics, giving inverter models a competitive edge in class A and B ratings. European households are increasingly favoring energy-conscious, versatile appliances, allowing inverter microwaves to secure a top-tier market position once dominated by conventional ovens.

Growth in Ready Meal Consumption Fuels Demand for Reheating Optimization Features

The normalization of pre-prepared meals across the region has created a dedicated functional niche for microwave ovens optimized for reheating performance rather than primary cooking, which is likely to promote the growth of the European microwave oven market. European sales of chilled and frozen ready meals are expanding significantly, driven by a surge in demand for high-quality, convenient food options and limited consumer time, with particularly strong growth observed in specific Central and Southern European nations. This trend incentivizes manufacturers to develop microwaves with sensor-reheating, automatic steam injection, and multi-stage programs tailored to specific meal types. In the United Kingdom, a significant portion of the adult population consumes ready meals weekly, leading manufacturers to integrate smart technology into kitchen appliances that automatically cook packaged meals based on barcode data. The German frozen food market is experiencing a deep integration between food and appliance ecosystems, with a substantial majority of frozen meal packaging designed specifically for direct, efficient microwave use. This symbiotic relationship ensures sustained relevance for microwave ovens not as legacy appliances but as essential partners in the modern European convenience food value chain, where reheating fidelity directly impacts consumer satisfaction and repeat purchase behavior.

MARKET CHALLENGES

Intensifying Competition from Multifunctional Built-In Kitchen Appliances Erodes Standalone Microwave Demand

The growing popularity of integrated kitchen solutions is diminishing the role of standalone microwave ovens, particularly in new residential construction and high-end renovations across the region, which impedes the growth of the European microwave oven market. Consumers increasingly opt for built-in ovens with microwave functionality or combination steam microwave units that eliminate the need for separate countertop appliances. In Germany and Austria, the demand for space-saving, multifunctional, and integrated cooking appliances, particularly those combining oven and microwave functions, has become a standard feature in modern kitchen installations. This shift is amplified by minimalist interior design trends that prioritize seamless surfaces and reduced visual clutter. Across Scandinavia, the prevalence of sleek, integrated kitchen designs has led to a decline in the market for standalone, countertop microwave appliances in favor of built-in solutions. Premium brands like Gaggenau and Neff have discontinued basic countertop models, entirely focusing on integrated solutions. This architectural integration trend sidelines traditional microwave manufacturers who lacbuilt-inin product lines or kitchen ecosystem partnerships, thereby fragmenting the market between appliance specialists and kitchen system integrators and pressuring standalone unit relevance in evolving European domestic spaces.

Material and Logistics Volatility Amplifies Supply Chain Fragility

Persistent disruption from fluctuating costs and availability of critical components, including magnetrons, transformers, and specialized ceramics used in cavity construction, is among the major barriers to the European microwave oven market. European manufacturers of small domestic appliances faced significant upward pressure on production costs due to volatile metal prices, energy price spikes, and ongoing semiconductor shortages for components. Geopolitical tensions and shipping disruptions in the Red Sea forced maritime traffic to take longer routes, resulting in extended transit times for goods traveling from Asian manufacturing hubs to Europe. These delays forced European retailers to hold higher safety stock, exacerbating warehouse congestion,n particularly in the Netherlands and Belgium,, um key distribution gateways. In response, manufacturers like Electrolux temporarily shifted production of select microwave lines to Poland and Romania to shorten supply chains, yet labor shortages in Central Europe limited scalability. Due to heightened supply chain risks and logistics disruptions, a substantial portion of European importers in Asia adjusted their contracts and delivery terms to manage volatility. This operational uncertainty not only inflates costs but also impedes the timely launch of new models, thereby weakening competitive responsiveness in a market where technological iteration and inventory agility are increasingly decisive.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Distribution Channel Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Samsung Electronics, LG Electronics, Panasonic Corporation, Whirlpool Corporation, Beko (Arçelik A.Ş.), Electrolux AB, Sharp Corporation, Hitachi, Ltd., Toshiba Corporation, Haier Group, Miele & Cie. KG, Bosch (BSH Hausgeräte GmbH), Siemens (BSH Hausgeräte GmbH), GE Appliances (Haier Group), Candy Hoover Group, Smeg S.p.A., Russell Hobbs (Spectrum Brands), Galanz |

SEGMENTAL ANALYSIS

By Type Insights

The solo microwave segment remained the largest segment in theEuropeane microwave oven market by accounting for a 52.6% share in 2025. The supremacy of the solo microwave segment is attributed to affordability, functional simplicity,, ty and widespread suitability for basic reheating and defrosting needs across diverse household profiles. In an economic climate marked by inflationary pressures, European households exhibit heightened price consciousness, particularly in Southern and Eastern regions. High inflation and slow real income growth across the European Union have driven consumers toward more budget-conscious purchasing behaviors for household appliances. In Central and Eastern European markets, budget-priced solo microwaves dominate, as first-time buyers and cost-sensitive consumers prefer basic, essential models. Even in wealthier markets like Germany, solo models remain prevalent in student housing and secondary residences where full cooking functionality is unnecessary. Major European electronics retailers prioritize shelf space for functional solo microwaves to meet high demand for affordable, entry-level coo, king appliances. This economic pragmatism ensures that, despite technological advances,s the solo segment retains primacy in volume terms due to its alignment with fundamental consumer utility and affordability thresholds. In highly saturated Northern European markets, the replacement cycle for microwaves has lengthened as consumers hold onto appliances longer, favoring durability and repairs over immediate replacement. When upgrading, ng consumers often opt to replace like with like,ike, particularly when existing usage patterns do not justify premium features. Swedish consumer data indicates that simple solo models remain the preferred choice for replacement, even among households that possess, or have access to, more advanced combination ovens. This behavioral inertia stems from ingrained usage habits where the microwave serves a dedicated reheating role distinct from primary cooking appliances. Furthermore, compact urban dwellings often lack space for larger convection units, reinforcing the retention of smaller footprints. This structural dynamic of replacement conservatism, combined with spatial constraints, solidifies the solo microwave as the backbone of Europe’s volume market despite declining novelty.

The convection microwave segment is expected to exhibit a noteworthy CAGR of 9.6% from 2026 to 2034 due to culinary diversification and energy efficiency alignment. Younger European households increasingly view the microwave not as a reheating tool but as a primary cooking appliance capable of baking, grilling, and roasting. Younger adults in Denmark are increasingly incorporating microwave cooking, specifically for preparing full meals rather than just reheating, reflecting a shift towards convenience. This shift is amplified by food media and recipe platforms that promote microwave-specific cooking techniques. Manufacturers respond with convection models featuring crisp functions, sensor cooking, and preset programs for global cuisines. Convection microwaves have become a significant component of the premium, integrated kitchen appliance market in Germany, with major brands integrating them into modular systems. The convergence of culinary curiosity, curiosity space constraints, t,s, and performance expectations positions convection as the innovation frontier in European microwave adoption. The European Union’s revised Energy Label, introduced in 2021, penalizes inefficient standalone appliances while favoring multifunctional units that reduce reliance on larger ovens. Convection microwaves are a highly energy-efficient alternative to conventional ovens, offering substantial energy savings when used for smaller, daily cooking tasks. This efficiency advantage translates into lower class ratings for traditional ovens and higher ratings for advanced microwaves, thereby influencing consumer choice at the point of sale. In France, the Energy Transition for Green Growth Act provides tax incentives for households replacing inefficient appliances with A-rated models, further boosting consumer uptake. As European climate targets tighten, the functional versatility and energy economy of convection microwaves align with both policy direction and evolving domestic sustainability practices.

By Distribution Channel Insights

The retail stores segment maintained the majority share of 48.5% of the European microwave oven market in 2025. The prominence of the retail stores segment is credited to consumer preference for tactile evaluation, immediate availability,y and bundled kitchen appliance promotions. Major European electronics and home appliance retailers such as El Corte Inglés in Spain and Saturn in Germany have transformed microwave sections into interactive cooking zones where customers can test reheating performance and view convection results in real time. In-store demonstrations significantly influence microwave buyers in Europe, with consumers valuing hands-on experience before purchasing, note retail market reports. Additionally, many retailers frequently bundle microwaves with refrigerators or cooktops, offering discounts that enhance perceived value. According to Italian market data, a significant portion of microwave sales occurs during kitchen remodeling projects, reflecting a preference for built-in, integrated kitchen solutions. This experiential and promotional model leverages physical retail’s unique capacity to convey performance and build trust, particularly for mid to high-end models where feature differentiation is critical. Despite digital growth, European consumers continue to value same-day pickup and in-person technical consultation pparticularlyyy for appliances requiring installation or integration. European consumers prioritize purchasing major appliances from retailers that provide comprehensive, on-site services, including delivery and warranty, over pure e-commerce options. In rural and peri-urban areas where logistics infrastructure is less dense, retail stores serve as essential access points. Outside major metropolitan areas in the Netherlands, microwave consumers place a high value on convenient, local service and reliability as key decision factors in their purchasing decisions. This enduring reliance on physical channels underscores the limitations of pure e-commerce in categories where trust, installation, and immediacy remain paramount.

The online stores segment is predicted to witness the highest CAGR of 12.3% during the forecast period,, od owing to rising e-commerce penetration among younger demographics, competitive pricing, and dynamic inventory algorithms that enhance the online value proposition. Younger European consumers increasingly rely on major online marketplaces to research and purchase home appliances, favoring convenience and speed in their buying journey. These consumers prioritize price transparency, user reviews,ws and home delivery convenience, often cross-comparing dozens of models before purchase. Despite a general decline in Swedish e-commerce, digital maturity and robust logistics continue to drive online purchasing for home electronics, with consumers seeking the best value. Brands now optimize product pages with 360-degree views, cooking tutorial,s, and energy label visuals to replicate in-store engagement digitally. This generational shift, coupled with mobile payment adoption, accelerates online channel dominance, especially for standardized solo models. E-commerce platforms utilize dynamic pricing and promotional campaigns to offer competitive prices for home appliances, challenging traditional physical retail outlets. Algorithms also enable personalized recommendations based on browsing history, thereby increasing conversion for targeted models. Online retailers are capturing a significant portion of entry-level household appliance sales in Spain, driven by aggressive discounts during seasonal shopping periods. Furthermore, free returns and extended digital warranties mitithe gate perceived risk of online appliance purchases. Same-day delivery in European cities is bridging the gap between online and offline shopping, cementing e-commerce as the leading growth sector.

By Application Insights

The residential segment led the European microwave oven market by holding a substantial share in 2025 because of the appliance’s entrenched role in domestic food preparation routines across all household types. Microwave ovens are now considered essential kitchen infrastructure in new residential developments across the continent. Across the European Union, the modernization of new residential buildings is increasingly incorporating standardized, integrated spaces for kitchen appliances in new apartment construction. German social housing prioritizes efficiency and accessibility, but usually, renters must provide their own kitchen appliances, including microwaves. Similarly, in France, modern furnished rental property listings frequently feature standard, pre-installed kitchen conveniences, including devices for rapid heating. This institutionalization transforms the microwave from a discretionary purchase into a baseline expectation for habitability, thereby sustaining steady replacement and first-time adoption even in saturated markets. European dietary patterns have evolved toward convenience without sacrificing nutrition withh microwaves enabling quick reheating of home-cooked meals and ready-prepared dishes. According to European consumer behavior studies, the primary usage of microwave ovens in northern European households is for heating frozen food or warming up previously cooked meals. This routine integration is reinforced by multi-generational familiarity with the appliance as a safe and efficient tool. In Nordic countries, where meal prepping is culturally prevalent,t microwave usage correlates strongly with weekly batch cooking cycles. This deep behavioral embedding ensures consistent demand irrespective of technological novelty as the appliance fulfills non-substitutablele functional niche in contemporary European domestic life.

The commercial segment is estimated to register the fastest CAGR of 10.1% from 2026 to 2034. The rapid growth of the commercial segment is propelled by efficiency demands in modern food operations. The proliferation of delivery-only and hybrid food outlets across urban Europe has elevated microwave ovens from auxiliary tools to core production equipment. Driven by the demand for rapid delivery, cloud kitchens in the European Union are increasing their reliance on high-speed, commercial-grade microwave equipment to meet consumer demand. To manage high-demand periods and meet delivery time targets, a significant portion of delivery-focused restaurants in the United Kingdom usehigh-power commercial microwave ovens. These establishments prioritize speed c,,onsistency,, and compact footprint, attributes where commercial microwaves outperform conventional ovens. Brands like Rational and Electrolux now offer countertop models with programmable multi-stage cycles tailored for specific menu items, further embedding microwaves into back-of-house workflows. Hotels,, hospita, ls, and corporate cafeterias across Europe face acute labor shortage,s prompting automation of food service processes. Institutional catering across Europe has experienced notable staffing challenges, forcing operators to maintain consistent meal volumes with a smaller labor force. In response, facilities increasingly deploy sensor-equipped commercial microwaves that automatically adjust time and power based on food load, reducing training needs and human error. The adoption of advanced, programmable cooking systems in German institutional kitchens, such as hospital canteens, is helping to reduce labor expenses associated with food reheating. This operational imperative transforms the commercial microwave from a simple appliance into a productive tool, a ccelerating adoption beyond traditional fast food contexts into broader institutional foodservice ecosystems.

COUNTRY LEVEL ANALYSIS

Germany Microwave Oven Market Analysis

Germany dominated the European microwave oven market by capturing a 18.7% share in 2025. The supremacy of the German market is driven by its manufacturing strength, household density, and appliance replacement culture. Germany’s leadership stems from a combination of high household formation rates technologicall adoption, and stringent energy standards. A high number of German householdscombinedd with a predictable replacement cycle for major home appliances, ensures steady demand for new products. The country’s Energiewende policy has made energy labeling a decisive purchase factor. A large majority of German consumers prioritize energy efficiency ratings, driven by EU eco-design standards and high energy awareness, making efficiency classes a critical factor in purchasing decisions. Leading domestic brands like Bosch Siemens and Miele drive innovation in convection and smart microwaves, while discount retailers such as Aldi and Lidl ensure mass market access to solo models. Furthermore, Germany’s robust network of specialized electrical retailers and service technicians ensures comprehensive, in-person support and demonstration capabilities, maintaining high service levels for consumers. This ecosystem of policy, consumer awareness, s,s and retail depth sustains Germany’s position as Europe’s largest and most sophisticated microwave oven market.

United Kingdom Microwave Oven Market Analysis

The United Kingdom followed closely in Europe microwave oven market by holding a 16.2% share in 2025. The expansion of the UK market is fuelled by urbanization, convenience culture, and high ready meal consumption. The United Kingdom remains a European leader in the consumption of prepared convenience meals, with a substantial portion of the adult population frequently consuming ready meals as part of their weekly diet, according to findings on national food habits. This behavioral norm ensures near-universal microwave ownership in most households. London’s high-density living, with average apartment sizes among the smallest in Western Europe, favors compact and multifunctional models. Online retail dominates distribution. The UK marketplace shows high digital maturity, with online platforms serving as a primary channel for purchasing household electronics and appliances. Post Brexit appliance standards remain aligned with EU ecodesign rules,e ensuring continued focus on efficiency. The combination of culinary convenience,ce urban constraints,nts and digital purchasing behavior solidifies the UK’s strong and resilient microwave market position.

France Microwave Oven Market Analysis

France is also a major player in the European rope microwave oven market due to culinary tradition adaptation and social housing mandates. It presents a unique duality where traditional cooking coexists with pragmatic microwave adoption, particularly among younger and urban populations. Regulations governing social housing primarily focus on core safety and cooking amenities, rather than the mandatory inclusion of small appliances like microwaves to ensure appliance penetration. In the 2023 rental market, particularly within urban areas and for furnished properties, the presence of a microwave has become a common feature in property listings, reflecting a shift in expected convenience amenities on rental platforms like SeLoger. Despite skepticism from older generations, younger French consumers are turning to microwaves for oil-free steaming and reheating, notes Coast Appliances. The government’s energy renovation subsidies also incentivizethe replacement of inefficient models with A-rated convection units. This blend of policy-driven access, generational shift,t and functional reinterpretation within a gourmet culture maintains France’s significant and evolving microwave market role.

Italy Microwave Oven Market Analysis

Italy occupies a significant position in the European microwave oven market owing to the delayed but accelerating modernization of kitchen infrastructure. Historically, Italy exhibited lower microwave penetration due to strong stovetop cooking traditions, but urbanization and demographic shifts are rapidly changing this. According to the National Statistics Agency (ISTAT), the proportion of people living alone in Italy has grown significantly over the last decade, leading to a higher demand for appliances that facilitate individual meal preparation. Real estate developers in major hubs like Milan and Rome are increasingly outfitting new residential units with space-saving cooking appliances to cater to the fast-paced lifestyles of urban professionals living in smaller apartments. Additionally, the rise of frozen ready meals tailored to Italian cuisine, such as lasagna and risotto, has normalized microwave use even among traditionalists. Retailers like Unieuro have expanded demonstration zones showing microwave adaptations of classic recipes. This cultural recalibration, combined with rising energy costs that favor efficient appliances,s propels Italy’s growing relevance in the European microwave landscape.

Spain Microwave Oven Market Analysis

Spain is predicted to expand in the European microwave oven market over the forecast period due to tourism-driven commercial demand and rising urban household formation. It benefits from a dual engine of residential and commercial growth. Spain's leading position in European tourism supports a vast, busy hospitality sector that frequently utilizes professional microwaves to manage high service demands. The Spanish hospitality sector increasingly relies on professional, fast-acting heating technology to ensure efficient, rapid, and high-quality room service delivery. Simultaneously Rapid urbanization and the rise of smaller, compact living arrangements in major Spanish cities are driving widespread adoption of convenient, space-saving kitchen appliances. Energy poverty concerns also drive demand for efficient reheating versus full oven use, with government rebates available for A-rated models. This synergy between tourism infrastructure, domestic convenience needs, and policy support positions Spain as a dynamic and expanding microwave market in Southern Europe.

COMPETITIVE LANDSCAPE

The European microwave oven market features a competitive landscape shaped by the coexistence of global appliance giants, premium European specialists, and value-oriented Asian manufacturers. Competition centers on technological sophistication, energy performance,ce and integration within modern kitchen ecosystems rather than price alone. Established players leverage brand heritage, service infrastructure, and regulatory expertise to defend premium segments while agile entrants capture volume through online channels and streamlined models. The shift toward multifunctionality has intensified rivalry as traditional microwave makers compete with b,,uilt in oven specialists for kitchen real estate. Innovation cycles have accelerated with features like inverter technology, smart sensors, and recyclable materials becoming key differentiators. Regulatory pressures around energy efficiency and circularity further raise barriers to entry, favoring firms with robust R and D and sustainability commitments. This dynamic environment rewards adaptability,y, and deep understanding of regional culinary behaviors across Europe’s diverse consumer base.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global European microwave oven market include

- Samsung Electronics

- LG Electronics

- Panasonic Corporation

- Whirlpool Corporation

- Beko (Arçelik A.Ş.)

- Electrolux AB

- Sharp Corporation

- Hitachi Ltd.

- Toshiba Corporation

- Haier Group

- Miele & Cie. KG

- Bosch (BSH Hausgeräte GmbH)

- Siemens (BSH Hausgeräte GmbH)

- GE Appliances (Haier Group)

- Sharp Electronics

- Candy Hoover Group

- Smeg S.p.A.

- Russell Hobbs (Spectrum Brands)

- Galanz (European distribution)

TOP LEADING PLAYERS IN THE MARKET

- Whirlpool Corporation maintains a strong presence in the European microwave oven market through its portfolio of reliable and energy-efficient appliances under brands such as Whirlpool, Bauknecht, nd Indesit. The company leverages its deep manufacturing footprint in Italy and Poland to serve diverse European consumer segments with both standalone and built-in microwave solutions. Whirlpool actively aligns its product development with EU energy labeling and ecodesign regulations, ensuring compliance and consumer appeal. Its innovation reinforces its commitment to integrating convenience, sustainability, ty and digital functionality across residential and light commercial applications throughout the region.

- Miele & Cie KG contributes significantly to the premium segment of tEuropeanope microwave oven market with its high-end integrated and multifunctional appliances designed for discerning consumers. Headquartered in Germany, the company emphasizedurabilityyy,,y precision engineering, and seamless kitchen integration with microwaves often embedded in its MasterChef and steam oven systems. Miele’s products comply with the strictest European energy and safety standards while offering advanced sensor cooking and automatic program selection. Their advancement strengthens its leadership in sustainable luxury kitchen solutions across Western and Northern Europe.

- Panasonic Corporation plays a distinctive role in the European microwave oven market through its pioneering inverter technology and compact design philosophy that caters to urban households. Although headquartered in Japan, Panasonic has maintained a dedicated European product development team that tailors microwave featEuropeanano regional cooking habits and kitchen layouts. The company is widely recognized for its reliability and precision heating capabilities, especially in solo and grill models. Additionally,lly the firm enhanced its distribution partnerships with major online and specialty retailers to improve accessibility across Southern and Eastern Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European microwave oven market focus on product differentiation through energy-efficient inverter technology and multifunctional convection capabilities. They prioritize compliance with stringent European Union ecodesign and energy labeling regulations to maintain market access and consumer trust. Companies invest in smart connectivity features, including voice assistant integration and mobile app control,l to align with digital kitchen trends. Strategic partnerships with kitchen furniture manufacturers and real estate developers ensurbuilt-inin microwave inclusion of microwaves in new residential projects. Geographic expansion into emerging Eastern European markets is pursued through localized pricing service networks and distribution alliances to capture growing urban demand.

MARKET SEGMENTATION

This research report on the europe microwave oven market is segmented and sub-segmented into the following categories.

By Type

- Solo Microwave Ovens

- Grill Microwave Ovens

- Convection Microwave Ovens

By Distribution Channel

- Retail Stores

- Online Stores

By Application

- Residential

- Commercial

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Sweden

- Rest of Europe

Frequently Asked Questions

1. What are the main types in the Europe Microwave Oven Market?

In the Europe Microwave Oven Market, key types include solo for basic reheating, grill for added browning, and convection for baking and roasting, offering multi-functionality. Countertop models dominate households, while built-in options suit modern kitchens, catering to diverse needs from simple defrosting to complex meal prep in urban settings.

2. Who are the top players in the Europe Microwave Oven Market?

Leading companies in the Europe Microwave Oven Market include Siemens, Samsung, Whirlpool, Panasonic, and Haier, focusing on innovation like IoT integration and energy efficiency. They compete through product diversification, capturing shares in residential and commercial segments across Western and Eastern Europe.

3. How does urbanization impact the Europe Microwave Oven Market?

Urbanization in the Europe Microwave Oven Market drives demand for space-saving countertop and built-in microwaves, ideal for compact city apartments. Busy urban professionals rely on these for fast meal solutions, amplifying the need for multi-functional models that combine reheating, grilling, and steaming in limited kitchen spaces.

4. What role do smart features play in the Europe Microwave Oven Market?

Smart features like app control, voice activation, and AI recipe suggestions are transforming the Europe Microwave Oven Market by appealing to tech-savvy consumers. These IoT-enabled ovens integrate with home systems for remote operation and precise cooking, enhancing user experience amid rising smart home adoption.

5. Why prefer convection microwaves in the Europe Microwave Oven Market?

Convection microwaves lead the Europe Microwave Oven Market for their versatility in baking, roasting, grilling, and reheating, mimicking traditional ovens while saving time. European consumers favor them for healthy, oil-minimal cooking, making them a staple in diverse households seeking all-in-one kitchen solutions.

6. What trends shape the Europe Microwave Oven Market?

Key trends in the Europe Microwave Oven Market include energy-efficient designs, inverter technology for uniform heating, and sustainable materials aligning with EU regulations. Demand rises for connected appliances supporting frozen foods and ready-to-eat meals, driven by dual-income households prioritizing convenience.

7. How does the residential segment influence the Europe Microwave Oven Market?

The residential segment dominates the Europe Microwave Oven Market, fueled by one-person households and families needing quick appliances for daily reheating and cooking. Features like auto-cook programs cater to varied European cuisines, from pizza to pasta, simplifying routines in fast-paced lifestyles.

8. What is the importance of energy efficiency in the Europe Microwave Oven Market?

Energy efficiency is crucial in the Europe Microwave Oven Market due to strict EU standards and consumer focus on sustainability. Inverter models reduce power use while providing consistent cooking, appealing to eco-conscious buyers who value lower bills and environmental impact alongside performance.

9. Which regions lead the Europe Microwave Oven Market?

Germany, France, UK, Italy, and Spain lead the Europe Microwave Oven Market with high penetration from mature demand and urbanization. Eastern Europe shows potential through rising incomes, while Western markets emphasize premium smart and compact models for modern living.

10. How do consumer lifestyles affect the Europe Microwave Oven Market?

Evolving lifestyles with working professionals and frozen food consumption propel the Europe Microwave Oven Market toward convenient, multi-tasking appliances. Demand surges for models handling reheating takeout, steaming vegetables, and quick defrosting to fit hectic schedules without compromising meal quality.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com