Europe Muscle Stimulation Devices Market Research Report By Product, Application, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis, Size, Share, Growth, Trends, & Forecasts (2026 to 2034)

Europe Muscle Stimulation Devices Market Size

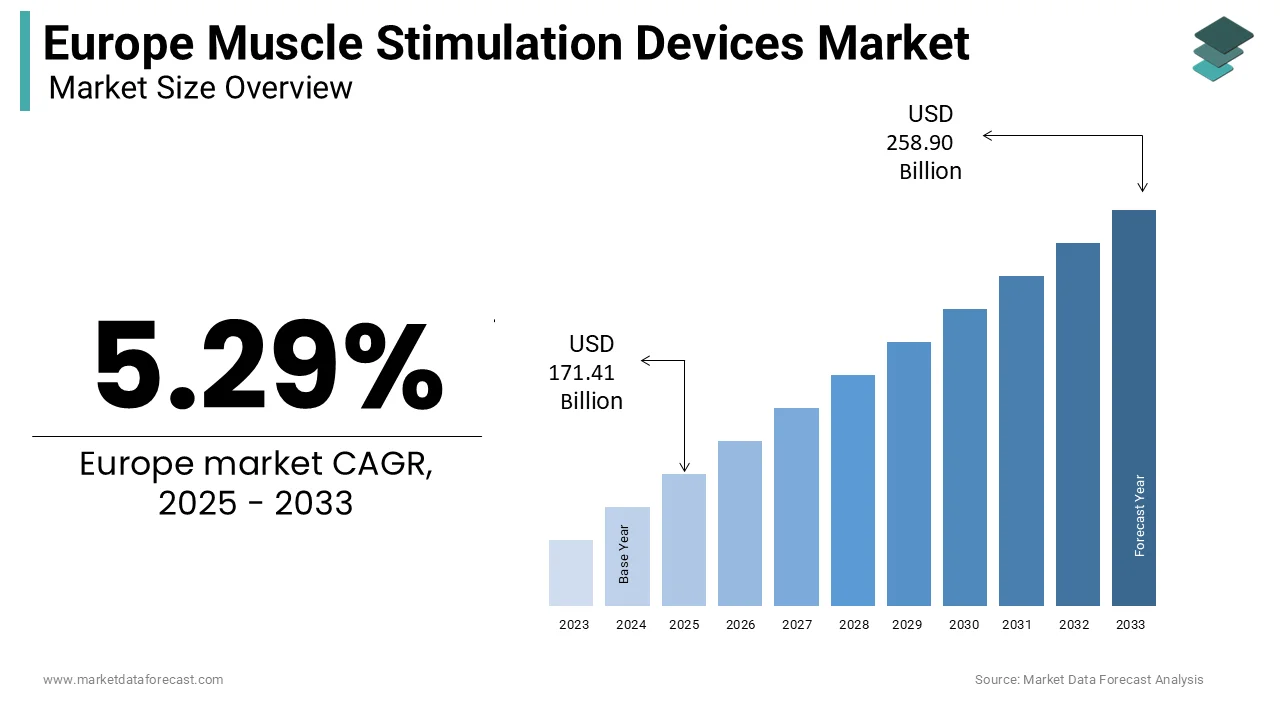

The europe muscle stimulation devices market was valued at USD 171.40 billion in 2025, is expected to have a 5.29 % CAGR from 2026 to 2034 and be worth USD 272.60 billion by 2034 from USD 180.48 billion in 2026.

Muscle stimulation devices are external, electrically-powered devices that deliver controlled electrical impulses to elicit muscle or nerve contractions. These devices operate by delivering controlled electrical impulses to motor nerves or muscle fibers to elicit contractions or modulate pain signals. As per sources, a portion of adults aged 55 and above in the European Union reported chronic musculoskeletal pain limiting daily activities. According to research, Work-related musculoskeletal disorders are the most common work-related health problems in the EU, affecting a substantial number of workers across all sectors and leading to significant economic costs. A large percentage of workers report experiencing musculoskeletal complaints, which indicates the widespread nature of this problem. These health burdens create a sustained clinical and consumer demand for non-invasive therapeutic interventions. Furthermore, the integration of digital health platforms and wearable biofeedback systems is reshaping device functionality and user engagement across both clinical and home care settings in the region.

MARKET DRIVERS

Rising Prevalence of Musculoskeletal Disorders Drives Clinical Adoption

The escalating burden of musculoskeletal conditions across European populations is a major booster for the growth of the Europe muscle stimulation devices market. According to the Global Burden of Disease Study, musculoskeletal disorders accounted for a notable share of total years lived with disability in Western Europe. As per a 2023 WHO statement, approximately 619 million people globally experienced low back pain (LBP) in 2020. National health systems increasingly recognize electrotherapy as a cost-effective non-pharmacological intervention, particularly amid efforts to reduce opioid prescriptions. These institutional endorsements, coupled with aging demographics where a portion of the EU population was aged 65 or older in 2023, according to Eurostat, amplify demand for devices that support functional recovery and pain relief without systemic side effects.

rowing Integration of Digital Health and Tele-Rehabilitation Platforms

The convergence of muscle stimulation technology with digital health ecosystems is accelerating adoption across both clinical and consumer segments in the region, and this bolsters the expansion of the Europe muscle stimulation devices market. As per research, a share of EU citizens now use digital tools for health monitoring or management. This shift enables muscle stimulation devices to function as connected peripherals within tele-rehabilitation programs, where real-time usage data and compliance metrics are transmitted to healthcare providers. Moreover, Nordic countries have integrated such devices into publicly funded digital care pathways for chronic pain management. The European Innovation Partnership on Active and Healthy Ageing has also endorsed hybrid rehabilitation models that combine wearable stimulators with mobile coaching applications. These developments not only enhance treatment efficacy but also align with EU policy priorities on scalable decentralized care models that reduce hospital readmissions and outpatient burdens.

MARKET RESTRAINTS

Stringent Regulatory Requirements Under EU MDR Delay Market Entry

The implementation of the European Union Medical Device Regulation has introduced compliance hurdles that impede the timely commercialization as well as the expansion of the Europe muscle stimulation devices market. As per research, the medical device regulations in Europe that took full effect in recent years now mandate detailed clinical data, technical documentation, and continuous market monitoring for medium- and high-risk medical devices. According to sources, many smaller medical device companies have experienced significant delays in securing certification approvals under this updated framework. The regulation mandates that notified bodies assess not only safety and performance but also risk management throughout the product lifecycle, which increases development costs and administrative complexity. This barrier restricts market access, particularly for innovative startups seeking to introduce next-generation stimulators with adaptive algorithms or AI-driven protocols. Consequently, product launches are postponed and investment in R&D is tempered by regulatory uncertainty despite strong underlying clinical demand.

Limited Reimbursement Coverage Constrains Widespread Utilization

Reimbursement policies across European healthcare systems remain inconsistent and often exclude advanced or home usage of these devices, which further constrains the expansion of the Europe muscle stimulation devices market. Public reimbursement for neuromuscular electrical stimulation in outpatient rehabilitation is limited to a small number of European countries, as per research. In countries like Italy and Spain, coverage is typically restricted to hospital-based use post-surgery, while home-based devices are considered out-of-pocket expenses. In Germany, funding is granted only if medical devices clearly demonstrate better results than existing therapies, according to sources. This financial barrier limits adoption among cost-sensitive patients and small physiotherapy practices. A 2022 survey by the European Confederation of Physiotherapy revealed that 68 percent of private clinics in Southern Europe avoided purchasing new electrotherapy equipment due to uncertain return on investment. Many private clinics in Southern Europe tend to be cautious about investing in new electrotherapy equipment because of unclear financial prospects, as per research.

MARKET OPPORTUNITIES

Expansion of Sports Medicine and Elite Athletic Performance Programs

Professional sports organizations and national athletic federations are increasingly adopting these devices as integral components of recovery and performance optimization protocols, which is setting up new opportunities for the Europe muscle stimulation devices market. Use of neuromuscular electrical stimulation has become standard practice for recovery and injury prevention in top football clubs across Europe, as per research. Most clubs in major leagues in England now regularly use portable stimulators during training sessions and while traveling, according to sources. National investments in sports science infrastructure further amplify demand. France’s national sports programs have also invested in upgraded recovery infrastructure, with advanced stimulators now deployed in training centers, according to sources. These institutional endorsements not only validate device efficacy but also create spill-over effects into semi-professional and amateur sports markets where performance-driven consumers emulate elite protocols.

Rising Geriatric Population Fuels Demand for Home-Based Rehabilitation Solutions

The rapidly aging demographic is causing a structural shift toward decentralized and self-managed rehabilitation solutions, and this is providing fresh prospects for the expansion of the Europe muscle stimulation devices market. As per research, the proportion of elderly individuals in European countries is steadily rising and is expected to continue this trend in the coming decades. This cohort faces elevated risks of sarcopenia, joint replacement, ts apost-strokeoke mobility impairments necessitating long-term muscle maintenance therapies. Advanced medical procedures like hip and knee replacements are now frequently performed across the region, according to sources. Home-based electrostimulation offers a viable alternative to frequent clinic visits, particularly in rural areas where access to physiotherapy is limited. National aging strategies promote assistive technologies that enable independent living, which further legitimizes the role of muscle stimulators in geriatric care pathways.

MARKET CHALLENGES

Clinical Evidence Gaps for Emerging Indications Limit Therapeutic Expansion

Robust European clinical validation exists for muscle stimulation devices in postsurgical rehabilitation and pain management, but not yet for newer medical applications such as lymphedema and neurogenic bladder dysfunction, which holds back the growth of the Europe muscle stimulation devices market. Regulatory bodies, including the UK Medicines and Healthcare products Regulatory Agency, emphasize the need for evidence before endorsing expanded labeling. This evidentiary shortfall discourages healthcare providers from prescribing devices off-label and deters manufacturers from investing in costly clinical trials without reimbursement guarantees. The therapeutic reach of these devices will remain limited to established uses, regardless of recent advancements, until robust multicenter studies can demonstrate consistent benefits for diverse patient groups.

Consumer Misuse and Safety Incidents Affect Trust in Over-the-Counter Devices

The proliferation of direct-to-consumer muscle stimulation units, particularly those marketed for fitness or aesthetic purposes, has raised safety concerns, which further hinders the expansion of the Europe muscle stimulation devices market. This is due to inconsistent user compliance and inadequate guidance. As per research, he number of adverse incident reports related to home use of electrostimulators was filed in 2023, involving skin burn, nerve irritation, or interference with implanted devices. These consumer devices often bypass clinical validation and fall into a regulatory gray zone under general wellness exemptions, unlike prescription-grade units. This has led to public health advisories in countries cautioning against unsupervised use, particularly among individuals with cardiovascular conditions or pacemakers. Such incidents erode professional and patient confidence in the broader category, potentially affecting the adoption of clinically validated systems. Restoring trust requires stricter enforcement of safety standards for consumer-grade products and clearer differentiation between medical and wellness device classifications across EU jurisdictions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, End User, and Region. |

| Various Analyses Covered | Global,Regional,l and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Zynex, Inc., NeuroMetrix, Inc., Omron Corporation, DJO Global, Inc., RS Medical, Inc., Beurer GmbH, EMS Physio Ltd., Compex (DJO Global, Inc.), Schwa-Medico GmbH, Globus Corporation |

SEGMENTAL ANALYSIS

By Product Type Insights

The transcutaneous electrical nerve stimulator segment held the largest share of 38.2% of the European muscle stimulation devices market in 2025. The dominance of the transcutaneous electrical nerve stimulator segment is because of its widespread acceptance as a non-invasive first-line therapy for acute and chronic pain conditions across both clinical and home settings. The primary driver is the escalating burden of chronic pain, which affects millions of adults in the European Union, as per a study. National health authorities increasingly endorse TENS as a safe alternative to pharmacological interventions amid the continent-wide effort to curb opioid overuse. Apart from these, TENS devices benefit from streamlined regulatory classification under the EU Medical Device Regulation as Class IIa devices, enabling faster market access compared to higher-risk neuromodulation systems. Their portability, ease of use, and cost effectiveness further reinforce adoption among aging populations managing conditions like osteoarthritis and lower back pain without frequent clinic visits.

The neuromuscular electric stimulation segment is estimated to register the fastest CAGR of 9.4% from 2025 to 2033. The rapid expansion of the neuromuscular electric stimulation segment is due to the integration of NMES into post-acute rehabilitation protocols following orthopedic and neurological events. As per a source, joint replacement surgeries are common across the EU, with significant country-by-country variation in rates and frequency. Furthermore, national stroke rehabilitation guidelines in some countries mandate NMES for upper limb motor recovery within a few months post-event. These institutional endorsements, combined with advances in wearable stimulator design that enable unsupervised yet monitored home use, are driving rapid clinical and consumer uptake across the region.

By Application Insights

The pain management segment led the Europe muscle stimulation devices market and captured 42.2% share in 2025. The prominence of the pain management segment is attributed to the high prevalence of chronic pain conditions and the strong policy push toward non-pharmacological pain relief. As per research, chronic pain is a widespread issue among adults in Europe, with lower back discomfort being a leading cause of reduced quality of life. According to sources, European health authorities now highlight TENS and similar therapies as essential parts of modern pain management programs in both clinics and hospitals. In Germany, institutional adoption of these technologies is high, which reflects growing confidence in their effectiveness, as per research. Moreover, digital pain clinics bundle connected stimulators with cognitive behavioral therapy modules, enhancing adherence and outcomes. The convergence of regulatory support, clinical validation, and digital health integration sustains the segment’s dominance.

The movement disorder management segment is anticipated to witness the fastest CAGR of 10.1% during the forecast period, owing to the rising incidence of Parkinson’s disease and post-stroke motor impairments, coupled with advances in targeted stimulation protocols. According to sources, the number of people living with Parkinson’s disease in European countries is steadily increasing and is expected to climb even higher in the coming years. Recent clinical evidence has validated NMES for freezing of gait and tremor modulation. As per research, recent clinical trials indicate that daily neuromuscular stimulation can help reduce the risk of falls among Parkinson’s patients. Similarly, European medical organizations have also updated treatment guidelines to include stimulation therapies for rehabilitation in stroke patients, as per a study. National neurorehabilitation centers in France and Italy have incorporated these protocols into publicly funded care bundles, accelerating device adoption. The segment’s growth is further amplified by AI-enabled stimulators that adapt pulse parameters in real time based on motion sensor feedback, enhancing therapeutic precision.

By End User Insights

The physiotherapy clinics segment captured the majority share of 36.3% of the Europe muscle stimulation devices market in 2025. The growth of the physiotherapy clinics segment is driven by the central role of outpatient rehabilitation in national healthcare systems and the high volume of referrals for musculoskeletal and post-surgical recovery. According to research, there is are large number of licensed physiotherapists practicing across the EU with a share regularly using electrotherapy modalities. In countries like Germany and the Netherlands, physiotherapy is fully reimbursed under statutory insurance for up to 24 sessions per indication, provided consistent device utilization is maintained. Furthermore, professional training standards mandated by national physiotherapy associations ensure proper device application and outcome documentation, which enhances clinical credibility. The integration of stimulators into multimodal treatment plans that combine manual therapy exercise and patient education further cements their indispensability in clinic-based care delivery.

The home care segment is likely to experience the fastest CAGR of 11.3% from 2025 to 2033. The rapid expansion of the home care segment is propelled by policy shifts toward decentralized care models and rising consumer demand for self-managed health solutions. National strategies actively promote home-based medical devices to reduce hospital readmissions and outpatient congestion. Home use of neuromuscular stimulation after hip replacement is helping more patients stick to their recovery routines compared to clinic-only approaches, as per research. Remote monitoring platforms that work with certified home stimulators are also expanding in Europe, backed by substantial investment in digital health, according to sources. These structural enablers, combined with user-friendly device designs and telehealth support, are transforming home care into the most dynamic growth frontier.

COUNTRY LEVEL ANALYSIS

Germany Muscle Stimulation Devices Market Analysis

Germany outperformed other regions in the Europe muscle stimulation devices market by accounting for 22.7% of the regional market in 2025. Its robust healthcare infrastructure and strong reimbursement mechanisms have largely contributed to the prominence of Germany. The country’s statutory health insurance system covers a wide range of electrotherapy treatments for both pain and rehabilitation indications, creating consistent demand across outpatient and inpatient settings. According to research, millions of physiotherapy prescriptions included electrostimulation in 202,3, emphasizing its clinical integration. Germany also hosts leading research institutions, which regularly publish evidence supporting device efficacy in conditions like chronic low back pain and post-stroke spasticity. These factors are combined with an aging population.

United Kingdom Muscle Stimulation Devices Market Analysis

The United Kingdom followed closely in the Europe muscle stimulation devices market and occupied a 16.3% share in 2025. Factors such as centralized clinical guidelines and expanding tele-rehabilitation services are driving the growth of the United Kingdom. The National Health Service routinely incorporates TENS and NMES into standardized care pathways for conditions ranging from osteoarthritis to post-surgical recovery. The use of electrotherapy in community physiotherapy is becoming more widespread across healthcare services in the United Kingdom, as per research. Guidelines for neuromuscular electrical stimulation to strengthen muscles soon after knee replacement surgery have been updated and are now widely adopted in NHS trusts, according to sources. Furthermore, the UK’s Accelerated Access Collaborative has fast-tracked reimbursement for connected stimulators that integrate with digital physiotherapy platforms. The steady growth in the market for muscle stimulation devices is primarily fueled by two factors: an increase in orthopedic surgeries and a growing population of people aged 65 and over.

France Muscle Stimulation Devices Market Analysis

France saw steady growth in the Europe muscle stimulation devices market due to comprehensive public health coverage and strong sports medicine adoption. The French National Health Insurance reimburses TENS devices for chronic pain and NMES for post-traumatic rehabilitation under strict prescription protocols. As per a study, hundreds of thousands of electrostimulation devices were dispensed through pharmacies in 2023. France’s prominence in elite sports also fuels demand, with national federations for rugby football and athletics integrating NMES into athlete recovery regimens. Furthermore, the country’s aging demograph, with a share of citizens aged 65 or older, according to research, amplifies the need for home-based and clinic-based muscle maintenance solutions, particularly in rural areas with limited physiotherapy access.

Italy Muscle Stimulation Devices Market Analysis

Italy expanded moderately in the Europe muscle stimulation devices market due to high musculoskeletal disease prevalence and expanding private rehabilitation networks. According to research, millions of adults suffer from chronic joint or back pain, with osteoarthritis affecting a portion of those over 65. While public reimbursement for home devices remains limited, private physiotherapy clinics have proliferated, particularly in northern regions where out-of-pocket health expenditure is higher. Apart from these, Italy’s professional football leagues mandate the use of muscle stimulators in player recovery protocols, creating secondary demand in sports medicine. The growing elderly population and the increased incidence of osteoporotic hip fractures have created a more intense need for effective neuromuscular rehabilitation.

Spain Muscle Stimulation Devices Market Analysis

Spain is likely to grow in the Europe muscle stimulation devices market during the forecast period, owing to growing awareness of pharmacological pain management and government-backed digital health initiatives. Chronic pain affects millions of adults in Spain, according to research, with lower back pain being the leading cause of disability among working-age adults. The Ministry of Health’s 2023 National Strategy for Pain Management promotes TENS as a first-line intervention in primary care settings. As per research, a growing number of private clinics in Spain now provide home device rental services to help patients maintain consistent care. Spain’s aging population is increasing steadily, with a significant portion aged 65 and above, according to sources. This demographic trend, combined with rising orthopedic surgery rates among active older adults, is driving steady growth in demand for muscle stimulation solutions, as per research.

COMPETITIVE LANDSCAPE

The Europe muscle stimulation devices market features a competitive landscape shaped by a mix of multinational medtech firms and specialized European manufacturers. Differentiation is driven by technological sophistication, clinical validation,n and alignment with national reimbursement frameworks. Companies compete on waveform precision, device ergonomics, and integration with digital health ecosystems rather than price alone. Regulatory hurdles under the EU MDR have raised entry barriers favoring established players with dedicated compliance infrastructure. At the same time, rising demand from home care and sports medicine segments has attracted niche innovators offering wearable and AI-enhanced stimulators. National variations in healthcare delivery mean that success requires tailored go-to-market approaches for DACH, Benelux, Southern Europe, and Nordic regions. Competitive intensity is further amplified by frequent product iterations and collaborations with academic medical centers to generate real-world evidence. Overall, the market rewards companies that combine regulatory diligence,e, clinical rrrelevancend digital innovation.

KEY MARKET PLAYERS

Prominent Companies leading the europe muscle stimulation devices market profiled in the report are

- Zynex, Inc.

- NeuroMetrix, Inc.

- Omron Corporation

- DJO Global, Inc.

- RS Medical, Inc.

- Beurer GmbH

- EMS Physio Ltd.

- Compex (DJO Global, Inc.)

- Schwa-Medico GmbH

- Globus Corporation

TOP PLAYERS IN THE MARKET

- DJO Global, a subsidiary of Enovis Corporation, is a prominent player in the Europe muscle stimulation devices market, offering a comprehensive portfolio of TENS and NMES systems for clinical and home use. The company integrates advanced waveform technologies user-centric design to support pain relief and neuromuscular rehabilitation. DJO Global has strengthened its European footprint through strategic collaborations with national physiotherapy associations and digital health platforms.

- BTL Industries is a leading European manufacturer specializing in electrotherapy and medical aesthetic devices with a strong presence in over 30 countries. Headquartered in the Czech Republic, the company supplies TENS interferential and NMES units to hospitals, physiotherapy clinics, and sports medicine centers across the continent. BTL emphasizes clinical validation and regulatory compliance under the EU Medical Device Regulation.

- Zimmer MedizinSysteme GmbH is a German-based innovator known for high-precision muscle stimulation and pain therapy systems widely used in orthopedic and neurological rehabilitation. The company’s devices are integrated into standard care protocols in German, SwSwissand Austrian clinics due to their reliability and evidence-based designZimmer MedizinSysteme actively collaborates with university hospitals to validate therapeutic efficacy through clinical studies.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe muscle stimulation devices market prioritize regulatory compliance under the EU Medical Device Regulation by investing in robust clinical evidence and post-market surveillance systems. Companies are increasingly embedding digital connectivity into devices to enable remote monitoring and integration with tele-rehabilitation platforms. Strategic partnerships with national healthcare providers and professional physiotherapy bodies enhance clinical adoption and guideline inclusion. Product portfolios are being expanded to include indication-specific neurological and geriatric application protocols. Besides, firms are localizing customer support and training programs to address regional variations in reimbursement and clinical practice across EU member states.

MARKET SEGMENTATION

This research report on the europe muscle stimulation devices market has been segmented and sub-segmented into the following categories.

By Product Type

- Burst mode alternating current (BMAC)

- Interferential (IF)

- Transcutaneous electrical nerve stimulator (TENS)

- Neuromuscular electric stimulation (NMES)

By Application

- Musculoskeletal disorder management

- Pain management

- Neurological

- Movement disorder management

By End User

-

Physiotherapy clinics

-

Homecare

-

Hospitals

-

Sports clinics

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which countries are major contributors to the Europe Muscle Stimulation Devices Market?

Germany, the UK, France, Italy, and Spain are the leading markets in

Europe due to advanced healthcare systems, innovation focus, and high prevalence of musculoskeletal disorders in these countries.

2. What are the main applications of devices in the Europe Muscle Stimulation Devices Market?

Key applications in the Europe Muscle Stimulation Devices Market include

pain management, rehabilitation, sports medicine, and the treatment of chronic musculoskeletal

conditions such as muscle atrophy and spasms.

3. Who are the primary end-users for the Europe Muscle Stimulation Devices Market products?

The Europe Muscle Stimulation Devices Market serves hospitals, physiotherapy clinics,

sports clinics, rehabilitation centers, and home users managing pain or requiring

physical therapy at home.

4. What are the main growth drivers for the Europe Muscle Stimulation Devices Market?

Growth in the Europe Muscle Stimulation Devices Market is driven by rising

musculoskeletal disorder cases, a move toward non-invasive therapies, sports medicine advancements,

and increased awareness about electrical stimulation benefits.

5. How does pain management impact the Europe Muscle Stimulation Devices Market?

Pain management is a core segment in the Europe Muscle Stimulation Devices Market,

as healthcare providers and patients look for drug-free, device-based solutions to treat acute and chronic pain conditions.

6. What regulatory guidelines affect the Europe Muscle Stimulation Devices Market?

The Europe Muscle Stimulation Devices Market is governed

by the Medical Device Regulation (MDR) and requires CE marking for approval and

market access, ensuring products meet rigorous safety and efficacy standards.

7. How do reimbursement policies influence the Europe Muscle Stimulation Devices Market?

Favorable reimbursement policies in countries like Germany support

the adoption of devices for pain and post-stroke rehabilitation, while variations in

policies across Europe can impact market growth for muscle stimulation devices.

8. Which technology trends shape the Europe Muscle Stimulation Devices Market?

The Europe Muscle Stimulation Devices Market sees trends like wireless devices,

Bluetooth connectivity, app-based controls, and targeted therapy innovations for home-based and

clinical treatments.

9. What challenges does the Europe Muscle Stimulation Devices Market face?

Main challenges in the Europe Muscle Stimulation Devices Market include high

device costs, competition from alternative therapies, and differing regulatory requirements among countries,

which may slow adoption rates.

10. Who are the key players in the Europe Muscle Stimulation Devices Market?

Leading manufacturers in the Europe Muscle Stimulation Devices Market include

international medical device firms specializing in pain management, rehabilitation, and sports medicine equipment.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com